Quick Answer

Start by rating each corridor as go, hold, or pilot, then choose rails only after KYC, KYB, AML, VAT, and tax-document blockers are mapped. Smart contracts may improve settlement timing in some lanes, but they do not replace off-ramp controls, reversal handling, or reconciliation. A hybrid setup is often the practical first move when speed matters but approvals and dispute ownership remain operational. Keep forecasts as context, and advance only where evidence proves reliable execution from release decision to final ledger entry.

Why this article matters for marketplace payouts in 2030#

2030 blockchain narratives can be useful directional context for marketplace payouts, but they are not proof that payout operations, compliance, or reconciliation are solved. The real production question is not chain mechanics alone. It is whether you can run an end-to-end payment flow that Finance, Compliance, and Treasury can actually operate, with regulated money handling, wallet infrastructure, and clear ownership when something fails.

A lane can settle on-chain and still fail the business test if redemption is impaired, an issuer failure exposes the stack, or your team cannot produce accounting-grade reconciliation. If a proposed rail cannot answer those points early, treat it as exploration, not a roadmap commitment.

Read this article as a decision tool, not a prediction exercise. It is meant to help you decide where blockchain rails are worth testing now, where a hybrid model is more realistic, and where traditional rails should stay in place until the control burden changes.

Use a practical filter. Can the stack support 24/7 availability, auditable payout records, compliance gates, and an operating layer that behaves like a payment rail rather than a developer tool? If it depends on your team directly managing chain-ops overhead, that is a red flag for many marketplace operators.

Be strict with hype. Growth headlines and trend narratives may be useful context, but they do not prove corridor-level execution for marketplace payouts. Even bullish 2030 scenarios leave the core build-versus-buy questions open: ownership, failure handling, and reconciliation quality in a specific corridor and vertical.

If you want a deeper dive, read eCommerce Reseller Payouts: How Marketplace Platforms Pay Third-Party Sellers Compliantly.

What to prepare before you evaluate any blockchain payout option#

Do not compare payout options until you have four basics documented: your current payout map, sign-off owners, release gates, and tax and documentation handling. Without that baseline, it is easy to evaluate contract logic before you know what actually blocks payouts in live operations.

Map your current payout lanes#

Start with a corridor-by-corridor, vertical-by-vertical map of how payouts run today. For each lane, capture settlement delays, failure patterns, reversals or returns, and where exceptions are created. That lets you test whether a new rail solves a real problem or just moves it somewhere else.

Use this checkpoint before you evaluate any new lane: who is paid, when value is considered late, how failures are handled, and how reversals are resolved.

Name the sign-off owners#

Set decision ownership before demos or architecture workshops. Assign clear internal owners and define who decides when priorities conflict. A simple operating test works well here: every open issue has one owner and one decision date.

Freeze your non-negotiable release gates#

Write release gates as hard blockers, not review notes. Define your internal compliance and data-completeness hold conditions up front, then treat incomplete requirements as a hold condition in the evaluation model.

Assemble the tax and documentation pack#

Build an inventory of tax documentation and foreign account reporting your structure may trigger. For FBAR planning where relevant, anchor your workflow to FinCEN Form 114 rules:

| FBAR item | Rule | Detail |

|---|---|---|

| Filing threshold | Required when a single-account maximum or aggregate maximum exceeds $10,000 | Anchor workflow to FinCEN Form 114 rules where relevant |

| Maximum account value | Use the highest reasonable value during the calendar year | Periodic statements may be used when they fairly reflect that maximum |

| Currency conversion | Use the Treasury Financial Management Service rate for the last day of the calendar year | If unavailable, use another verifiable rate and record the source |

| Rounding | Report whole U.S. dollars rounded up | $15,265.25 becomes $15,266 |

| Amendments | File a new FBAR and mark it as amended | Include prior report identifier details |

| Unknown aggregate amount | If you have fewer than 25 accounts and cannot determine whether aggregate maximum values exceeded the threshold | Complete the account sections and mark the amount as unknown |

| Deadlines | Keep deadline controls for April 15th and the automatic extension to October 15th | Monitor for event-based FinCEN relief notices |

Related: PropTech Marketplace Payments: How to Handle Rent Deposits and Service Provider Payouts.

Set a realistic 2030 baseline before committing roadmap budget#

Use forecast decks as context, not as approval to spend. If a source cannot explain how money moves in your actual payout corridor, it should not drive a build-versus-buy decision.

1. Sort claims into the right bucket. Third-party forecasts can be useful, but only if you classify them clearly as:

- General blockchain market growth

- Tokenization growth

- Marketplace payout viability

Do not collapse those buckets into one story. Growth in tokenized assets does not prove your payouts will clear faster, handle returns, or pass compliance review in a specific corridor.

2. Ask for corridor mechanics, not adjacent-sector signals. For every source, pressure-test four operator questions: who funds the payout, where FX happens, how off-ramping works, and what happens when a payout is returned, frozen, or disputed.

If those answers are missing, stop there. A 2025 paper on peer-to-peer energy trading in microgrids is not payout-operations evidence. A February 2026 paper covering 588 academic articles and 1,168 industry documents is still centered on EV battery supply chains with adoption challenges. Treat material like that as a maturity signal, not release evidence.

3. Score new claims against business as usual. In other domains, programs use explicit checkpoints such as measurement, reporting, and verification (MRV), tamper-evident audit trails, and credibility indexes tied to stated goals. Apply the same discipline here.

Compare each blockchain payout claim to your current settlement time, exception rate, reconciliation effort, and support burden. Recent stablecoin settlement experimentation over the last 12 months is a directional signal, not lane-level proof. If a claim does not beat your current corridor on execution detail, keep it on the watchlist rather than the roadmap.

Score each launch market before touching product design#

Score each corridor before you design product flows. As a working default, if compliance effort appears high and expected payout volume appears low, keep traditional rails first and defer blockchain lanes until corridor evidence improves.

Build a market-readiness table#

Create one row per launch corridor, with columns for legal clarity, KYC or KYB burden, AML trigger points, VAT handling, and tax-document obligations. Use a simple scale such as 0 for unknown or blocked, 1 for workable with manual effort, and 2 for clear enough to pilot.

Treat every score as evidence-backed, not opinion-backed. If a cell cannot point to a document or operating artifact, keep it marked as unverified.

Add the operating columns that usually decide launch#

The fields many teams skip can decide support load after launch: payout return handling, dispute handling, FX support, and local banking-partner coverage.

"Instant settlement" does not remove exception work. Weak beneficiary checks, weak controls, or missing manual review paths can make a bad release harder to unwind.

For each corridor, keep explicit evidence for:

- return and reversal handling

- off-ramp and FX support

- banking-partner dependencies

- dispute and exception ownership across Product, Ops, Finance, and Legal

Separate implementation evidence from market noise#

Use vendor and forecast material as context, not as launch proof for a specific corridor.

The Nevermined post (Jan 6, 2026) is vendor-authored and frames the value as usage-based billing, instant settlement, and agent-to-agent transactions. It also reports metrics such as 106% year-over-year, $46 trillion annually, under 500 milliseconds, and below $0.001. It argues that card rails can be uneconomic for sub-cent activity. None of that, by itself, proves corridor-level readiness for compliance, returns, disputes, or off-ramp reliability.

Apply the same filter to other weak inputs:

- RWA excerpt shown as a "Latest Posts" feed, including April 4, 2026 and April 3, 2026 cards

- SEC and MPRA excerpts that are title-level only

If the support is a vendor blog, a post feed, or a title-only document, mark the cell unverified.

Apply a default decision rule#

Set the default rule before edge-case debates begin: high compliance burden plus low payout volume should default to holding blockchain lanes until stronger corridor evidence is available. Use a compact rubric:

| Corridor pattern | Default decision | What must be true to move forward |

|---|---|---|

| High compliance burden, low expected payout volume | Hold | Keep traditional rails, gather corridor evidence, review later |

| Mixed compliance burden, meaningful strategic volume, operator gaps open | Pilot | Limit scope, define exception handling, confirm off-ramp and banking support |

| Evidence-backed compliance path, clear ops coverage, sufficient volume | Go | Confirm ownership, review cadence, and exception monitoring from day one |

Close each corridor with an explicit status#

Do not leave the table as research only. End each corridor as go, hold, or pilot, with clear rationale and the evidence needed to move to the next status.

For a step-by-step walkthrough, see How to Build a SaaS Marketplace That Manages Subscriptions and Contractor Payouts. If your go/hold table is ready, map each corridor decision to implementation requirements in Gruv Docs.

Choose payout architecture by corridor and risk profile#

Do not force one payout architecture across all markets. Once corridor scoring is done, pick the lightest model that can handle compliance burden, exception volume, and settlement expectations. In many cases, hybrid is the practical first choice because it can improve settlement timing without removing off-ramps, approvals, disputes, or tax checks.

Compare the three architecture options#

Use one operating-evidence table for every corridor review. It is for corridor-level selection, not for naming a universal winner.

| Model | Where it fits | What you keep or gain | Main tradeoff |

|---|---|---|---|

| Traditional rails only | Corridors with high exception handling, unclear digital-asset posture, or low expected volume | Familiar bank processes, established dispute handling, easier alignment with existing approvals and payout reversals | Slower settlement windows may remain, even as cross-border architecture evolves through ISO 20022 harmonisation and interconnection of domestic real-time systems |

| Hybrid rails | Corridors where faster or 24/7 value movement matters, but payout still ends through conventional off-ramps | Regulated stablecoins or tokenized deposits can support programmable, 24/7 settlement while you keep existing approvals, off-ramp checks, and support ownership | Adds interoperability and governance requirements, plus an extra handoff between the on-chain leg and the off-ramp leg |

| Blockchain-forward lanes | Narrow corridors with clear digital-asset permissibility, explicit custody decisions, and low exception volume | More payout logic can be handled through programmable release conditions | Premature when reversals, compliance reviews, or tax workflows dominate. Always-on rails also make latency and downtime direct business risk |

Choose hybrid when timing matters but control stays off-chain#

Hybrid is often the right call when settlement speed is the issue but operational control still sits in your existing approval and exception processes. If users still cash out through banks and your team still runs approval queues, hybrid can improve transfer timing without forcing you to rebuild the full payout stack.

Use a direct test: can you accelerate value transfer while keeping the controls that prevent bad payouts? If the answer is yes, keep beneficiary approval, AML review, and tax-document checks as release gates, even when an intermediate leg uses regulated stablecoins or tokenized deposits.

Verification should show a complete evidence chain for each payout:

- on-chain transaction reference

- off-ramp or bank payout reference

- approver or rules outcome authorizing release

- final ledger entry

If any link is missing, speed improved but control weakened.

Hold blockchain-forward lanes when exceptions drive workload#

If reversals, compliance exceptions, or tax workflows consume most of your support effort, blockchain-forward lanes are usually premature. Faster settlement does not remove investigation, correction, or documentation work, and it may make issues harder to unwind once value has moved.

Pressure-test the idea with recent operations data. Classify cases by reversals, AML review, beneficiary mismatch, missing tax documents, VAT questions, and routing delays. If exceptions and documentation dominate, stay on traditional rails or tightly controlled hybrid until those queues stabilize.

Jurisdiction still sets hard boundaries. Some policy examples emphasize licensing, custody, and disclosure standards for digital-asset platforms. Others can block certain asset types outright. The cited Dubai privacy-token ban is a reminder that corridor viability can fail at the policy level regardless of product design.

Decide custody and control before any blockchain-forward pilot#

Institutional activity is a signal, not a template. Participation in tokenized-asset and digital-money infrastructure does not answer your custody model or control design.

Do not approve a blockchain-forward pilot until ownership is explicit:

- who can move funds

- who can pause payouts

- who can rotate credentials or signing authority

- who produces disclosure, audit, and exception evidence

If those responsibilities are split across teams and providers without a written approval matrix, stop there.

At minimum, your decision pack should define asset type, wallet or account control model, custody owner, release-approval path, ledger of record, and corridor-specific legal posture. Federal policy framing includes a dedicated stablecoin-and-payments domain, so payment controls may face closer scrutiny.

Working rule: if conventional off-ramps and human intervention are still required, start hybrid. If reversals, compliance holds, and document chasing still dominate, stay traditional. Move toward blockchain-forward only where asset permissibility is clear, custody is explicit, and the evidence chain is complete from release approval to final settlement.

Related reading: Payment Infrastructure Trends 2026: How Marketplace Operators Should Prioritize Real-Time Rails, Stablecoins, BNPL, and Embedded Checkout.

Design smart contract payout logic around failures not happy paths#

Design payout logic for interruption, not straight-through release. Tokenization may create efficiencies, but those outcomes are still potential, and DLT use in financial services remains in an experimental phase, so dependency breaks should be treated as a core design case.

Define payout states before you write contract logic#

Name the payout states, and the evidence required to move between them, before writing code. At minimum, define release conditions, hold conditions, and cancellation paths in plain language.

Keep the model tight. Requested, approved, held, released, cancelled, and settled is often enough. For each transition, set one owner and one proving event so Ops can explain why the payout moved or stopped. If a failed case does not fit your state model, the model is too thin.

Map sequence breaks, not just success conditions#

Map failure points in the sequence, not only the happy path. Multi-step flows are exposed to sequential dependencies, and increased dependencies and interconnectedness raise the chance that one bad handoff distorts the payout outcome.

Use your own incident patterns to define outcomes for the breakpoints you actually see. Each breakpoint should map to one state and one next action such as hold, restart, cancel, or manual investigation before launch.

Set manual stops for mid-flow compliance changes#

Write an explicit house rule for mid-flow compliance changes. For example, if a new compliance concern appears during execution, consider moving to hold pending manual review instead of default auto-retry.

That aligns with a control-first posture in corridors where authorities apply checkpoints such as specific guidance, sandbox regimes, or new or amended rules. When scrutiny is high, a real human override path is often safer than a silent timer-based retry.

Link contract events and payout records so retries stay controlled#

Keep contract state and payout state linked through clear internal events. Where possible, use one shared payout identifier across contract events, internal ledger records, and provider or bank references so retries and investigations are easier to trace.

Run failure replays for sequence interruptions and verify one final economic outcome with a clear event trail for retry decisions. If records conflict after value movement, move to investigation hold before any further fund movement.

This pairs well with our guide on State Money Transmitter Licenses: Which US States Require a License for Marketplace Payouts.

Build compliance and tax gates into payout release decisions#

Treat tax eligibility as a payout-release gate, not post-release cleanup. If FEIE-related tax artifacts are missing, incomplete, or conflicting, the payout should move to hold or manual review, not release.

Define required artifacts before release logic runs#

Set a minimum FEIE artifact set in your own policy, then enforce it consistently in payout logic. For each required FEIE artifact, track status and relevant dates, and tie it to the beneficiary and payout record. Release should only be available when the required FEIE set is present and internally matched.

Handle FEIE as reviewable tax logic, not a simple flag#

If FEIE affects payout treatment, handle it as a structured check, not an auto-pass. A claimant still files a U.S. tax return reporting the income, and IRS process documentation describes FEIE claims as made through Form 2555 or 2555-EZ.

| FEIE check | Requirement | Note |

|---|---|---|

| Claim method | A claimant still files a U.S. tax return reporting the income | IRS process documentation describes FEIE claims as made through Form 2555 or 2555-EZ |

| Minimum time | 330 full days during a 12-month period | If the count is below 330 full days, the physical presence test is not met |

| Full day definition | A full day is 24 consecutive hours from midnight to midnight | Qualifying days do not have to be consecutive |

| Tax home | Days count only while the person's tax home is in a foreign country | Days in a foreign country while violating U.S. law are not treated as physical presence for this test |

| Part-year qualification | If qualification is only for part of the year, the maximum exclusion must be adjusted by qualifying days | Apply an adjusted maximum exclusion rather than a full-year amount |

| Adverse conditions | Route the case to specialist review if the person left because of war, civil unrest, or similar adverse conditions | The minimum time requirement may be waived |

| Legal violation income | Income earned from services during a period of legal violation does not qualify as foreign earned income | Treat it as not qualifying for FEIE |

Define escalation paths before funds move#

Set escalation paths before money moves. At minimum, define what happens with incomplete FEIE records, conflicting tax-home or day-count data, and potential waiver cases. Queue those cases for manual resolution with a clear reason code and owner so reviewers are working from the same evidence.

Enforce no-artifact, no-release in contract and ops layers#

Keep one non-negotiable execution rule: no automated payout release when required FEIE artifacts are missing or FEIE eligibility checks fail. The release path should open only after tax checks are explicitly passed. Otherwise, the payout stays on hold until the gap is resolved.

Lock down reconciliation and audit evidence before scaling volume#

Before you scale payout volume, lock down reconciliation and audit evidence so every release, hold, retry, and adjustment can be explained later from one defensible record.

Choose one authoritative payout event record#

Pick one payout event record as your operational truth, then reconcile related system views back to it. Keep transaction decisions, execution outcomes, and accounting impact connected in that record.

One useful design cue is the Tripartite Accounting Framework, a proposed hybrid model that combines blockchain, conventional data/accounting components, and ERP integration. In that framing, blockchain provides an immutable, transparent layer, while operations still need a joined record across transaction and accounting systems.

Define and retain a policy-based evidence chain#

Set a documented minimum evidence pack in your own policy before increasing throughput, and apply it consistently. The goal is simple: an independent reviewer should be able to reconstruct why each payout was released, held, or retried from retained records.

This is also where adoption risk shows up in practice. The research highlights unclear third-entry understanding, missing established accounting methods, and compliance challenges. If your evidence chain is weak, a payout can execute technically and still face audit scrutiny.

Document consistency behavior and reconciliation operations#

Document how reconciliation should work across your blockchain records, internal ledgers, and ERP postings, including which record is authoritative for accounting decisions. Keep the process aligned to applicable accounting and regulatory frameworks, including GAAP and IFRS where relevant.

Independent auditable accounts and explicit transaction-integrity oversight by a trusted third entity are practical controls when systems disagree and investigations need a clean starting point.

Need the full breakdown? Read How Platforms Should Prepare for CBDC Payments in Contractor Payouts.

Roll out in phases with verification checkpoints at every stage#

A phased rollout is stronger when each phase has explicit verification gates. Current DeFi research describes both opportunity and challenge, including smart contract vulnerabilities, liquidity challenges, and regulatory variation across major jurisdictions.

| Phase | Scope | Checkpoint |

|---|---|---|

| Phase 1 (pilot) | Keep scope narrow | Confirm your controls can detect and explain failures before broader rollout |

| Phase 2 (controlled expansion) | Add new markets | Only after pilot evidence shows your governance and regulatory approach can hold across jurisdictions |

| Phase 3 (scale) | Increase automation and throughput | Only after exception handling remains stable and auditable across repeated cycles |

Set pause and rollback conditions in advance, then enforce them. If checkpoint evidence is weak, treat that as a controls problem to fix before adding more markets.

Common mistakes that create compliance debt and payout breakage#

A common failure pattern is letting narrative outrun evidence. A June 2024 systematic literature review covering 45 studies from 2012-2023 identified seven governance models and highlighted persistent corruption/transparency challenges in centralized systems. That is useful context for governance design; it is not proof that a payout lane will be reliable in specific corridors.

| Mistake | Why it creates debt | Recovery checkpoint |

|---|---|---|

| Choosing rails from trend narratives | Promotional or high-level sources can describe direction without proving operational payout reliability. | Re-rank corridors by evidence quality, and require corridor-specific evidence before promotion. |

| Automating release logic before exception workflows exist | If exception handling is undefined, edge cases can become opaque failures or accidental releases. | Define hold and escalation paths before expanding automation, and treat specific AML or tax queue designs as unproven in the provided evidence. |

| Treating AI-agent narratives such as Fetch.ai, SingularityNET, or Bittensor as readiness signals | Product or network narratives are not the same as production payout evidence. | Require reliability and recovery evidence for your payout lane, not storyline strength. |

| Under-specifying reconciliation | Weak traceability can make payout issues harder to diagnose and resolve. | Set explicit reconciliation gates, including reference matching and replay behavior, before scale, and treat them as internal control requirements. |

If checkpoint evidence is thin, pause expansion and improve evidence quality first.

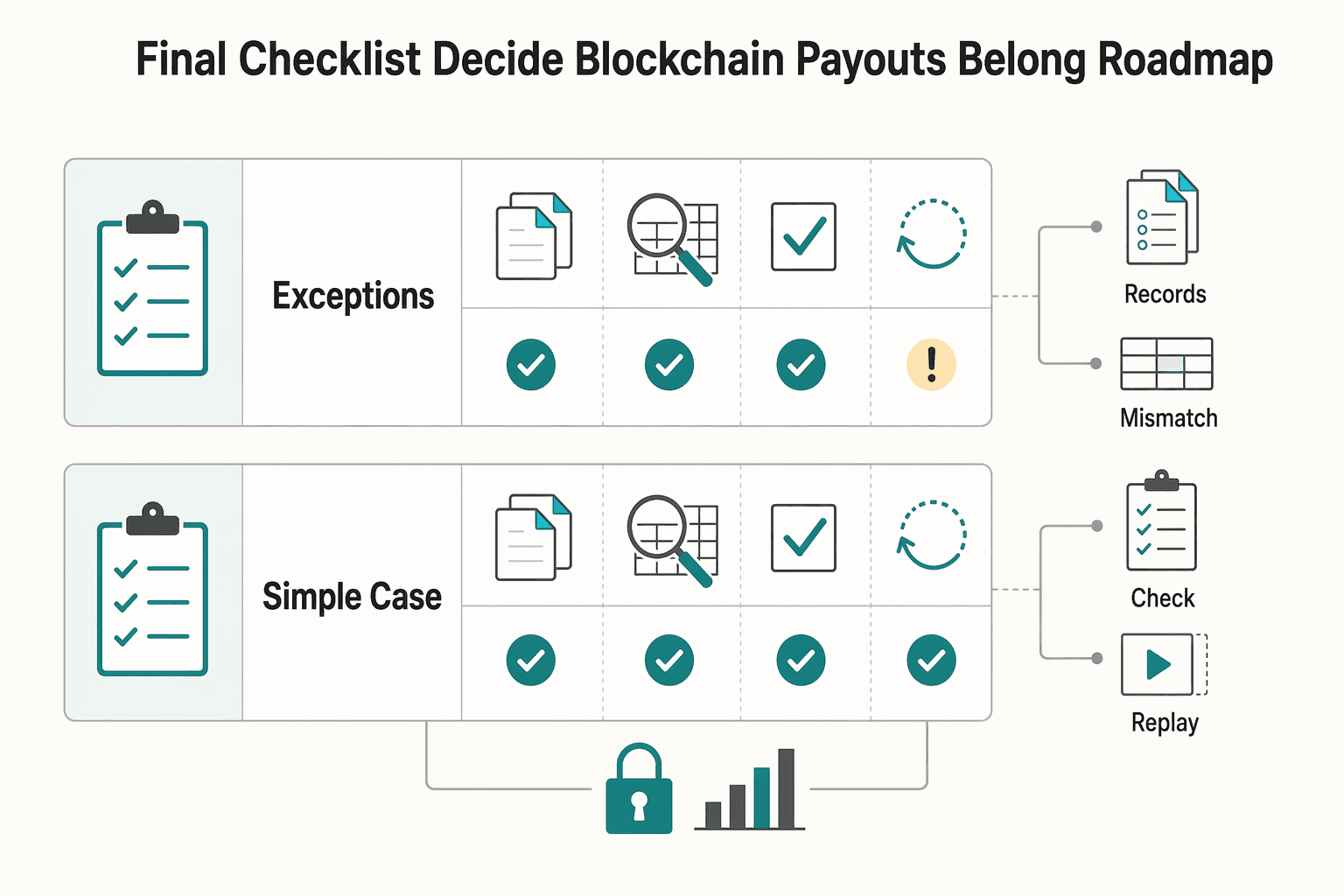

Final checklist to decide where blockchain payouts belong in your roadmap#

Do not make one global payout decision. Decide corridor by corridor, prove each lane in production, and expand only after compliance checks, failure handling, and reconciliation stay stable under real support load.

1. Confirm corridor readiness before choosing rails. Review KYC, KYB, AML, VAT, and the tax-document path your payout flow depends on where those controls apply, then verify that beneficiaries in that corridor can actually complete those checks. If you cannot show a complete beneficiary profile and document path, mark the corridor hold, not pilot.

Regulatory conditions are not unified. The Q4 2025 Asia view is explicitly fragmented, with examples such as biometric KYC requirements in India, including live selfie and eye-tracking checks, and outright privacy-token bans in Dubai. If your design assumes one reusable identity flow or one asset policy everywhere, it is too broad.

2. Choose architecture per corridor and write the tradeoff in plain language. In practice, the options are usually traditional rails, a hybrid lane, or a narrow blockchain-forward route. Do not set one as a global default because it looks faster in strategy discussions.

Use a simple rule:

- If compliance exceptions, tax review, reversals, or off-ramp dependency dominate, start traditional or hybrid.

- If release conditions are simpler and traceability requirements are strong, test a narrow blockchain lane.

Reported early use of fiat-backed stablecoins over the last 12 months for faster cross-border settlement is directional evidence, not corridor-readiness proof for your marketplace.

3. Validate contract logic against failure paths, not happy paths. Define release, hold, cancellation, and manual-override authority before launch, then test adverse scenarios such as beneficiary mismatch, provider timeout, webhook delay, partial execution, and an AML flag mid-flow.

Your checkpoint is operational control: can Ops stop, inspect, and resolve a payout without breaking state history? If manual approval is required, contract state and payout state should stay tied to one auditable event trail.

4. Require ledger-level traceability and complete reconciliation before expansion. Wallet balances or provider dashboards alone are not enough. For each payout, retain a complete evidence chain: request, policy-check result, provider or chain reference, journal entry, status changes, and the export artifact used by Finance or Compliance.

The practical test is whether one payout can be reconstructed end to end without engineering log interpretation. Blockchain may improve traceability between parties that do not fully trust each other, but implementation challenges remain, including privacy, trust, and resilience issues.

5. Launch in phases with explicit go or hold decisions. Start with one corridor, one vertical, and a limited counterparty set. Promote only after compliance handling, payout reliability, and support burden remain acceptable through at least one full reconciliation cycle.

Expand only where controls are already working in production, not where the market narrative is strongest. That is the real roadmap test.

Frequently Asked Questions

Will smart contracts replace marketplace payout systems by 2030?

No clear evidence here supports full replacement by 2030. A grounded position is partial adoption: smart contract automation could handle parts of payout logic, while other controls remain outside the contract layer. Treat full-replacement claims as narrative until you can show reliable payout-lane outcomes.

What has to be true before blockchain payouts can run at marketplace scale?

You need operating proof, not just momentum. At minimum, verify observed behavior under real volume rather than relying on adoption narratives alone. If the story is strong but observed payout behavior is thin, readiness is not established.

What changes faster by 2030 in practice: payout rails, contract logic, or compliance rules?

From the 2026-2030 trend framing, technical and product adoption appears to move steadily. Keep implementation flexible instead of locking into a single contract path.

How should founders decide the first country and vertical to launch?

You cannot credibly pick a specific country or vertical in advance. Choose an initial lane where outcomes can be observed clearly under real usage, then expand based on measured results rather than narrative alone.

When is a hybrid payout architecture better than blockchain-first?

Hybrid can be the safer choice when you want smart contract automation but still need controls outside the contract layer. It lets you adopt automation where behavior is verifiable without assuming the whole payout system is proven end to end. A blockchain-first approach is easier to justify after reliable behavior is observed, not inferred.

What evidence is still missing in current forecasts for smart-contract marketplace payouts?

The main gap is operating proof in the payout lane itself. Forecasts and trend narratives can show direction, but they do not prove reliable payout performance. Even large on-chain systems highlight risks such as liquidity-provider attrition, which reinforces that narrative alone is not enough.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- digitalcommons.odu.edu/cgi/viewcontent.cgitrusted

- documents.dps.ny.gov/public/Common/ViewDoc.aspxtrusted

- fincen.gov/reporting-maximum-account-valuetrusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- govops.ca.gov/wp-content/uploads/sites/11/2021/06/BWG-Fina...trusted

- govops.ca.gov/wp-content/uploads/sites/11/2020/07/BWG-Fina...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Marketplace Platforms Pay Third-Party Sellers Compliantly

Generic marketplace payout advice usually skips the part that breaks in production. Paying many sellers is not just moving money out. It is deciding who gets paid, when they become eligible, what happens when a buyer disputes a payment, and how finance proves every release later. If you are working on **ecommerce reseller payouts marketplace platforms pay third-party sellers**, this guide is for the marketplace operator, not for solo freelancer banking tips.

PropTech Marketplace Payments: How to Handle Rent Deposits and Service Provider Payouts

With **proptech marketplace payments rent deposits** and service-provider payouts, the real decision is operational design, not feature count. You need a setup that can run across countries without creating manual cleanup, custody ambiguity, or reconciliation gaps after launch.

Choose Freelance Platforms by Failure Mode, Not Features

If you want more resilience, do not ask, "What platform should I switch to?" Ask where a single vendor can interrupt cash, break compliance, or slow client payment. The real risk is dependency, not whether you picked the "right" marketplace.