Quick Answer

Choose tools by failure mode, not by features. The article argues that the biggest risks are payment holds, account restrictions, missing tax documentation, weak export and retention rules, and fragmented records. Build your stack in this order: compliance first, then cash control, then operations, and test every tool for payout rules, hold language, and exportable records before you rely on it.

Why "Platform Alternatives" Are the Wrong Answer to the Right Question#

If you want more resilience, do not ask, "What platform should I switch to?" Ask where a single vendor can interrupt cash, break compliance, or slow client payment. The real risk is dependency, not whether you picked the "right" marketplace.

That dependency shows up in boring, expensive places. A PayPal payment hold can block access to funds, usually for 21 days or less. Upwork states that off-platform payments can lead to loss of your account. Fiverr says enforcement can range from warnings and account restrictions to permanent suspension. Those are the failure modes that matter: revenue paused, account access limited, and client work stranded inside someone else's rules.

Three decision mistakes usually sit behind the search for alternatives:

- Confusing governance with operations. Decentralization can matter if you care about platform control or dispute design, but it does not fix a missing W-9, a TIN mismatch, or backup withholding at 24% when withholding rules are triggered. Evidence on decentralized dispute systems is conditional, not universally better.

- Choosing consumer convenience for business-critical work. Consumer tools can make onboarding easy, but they may still leave gaps around holds, records, and payer requirements such as Form W-9 and 1099-NEC reporting.

- Assuming enterprise tooling maps to solo needs. It may not. Upwork Enterprise uses customized billing terms, and its compliance classification can take three business days after hiring. That helps some buyers, but it is not the same problem as your day-to-day cash control.

| Decision lens | Alternative hunting | Risk-first stack design |

|---|---|---|

| Cash access | Swap apps, keep one payout dependency | Add redundancy and check hold and restriction policies first |

| Compliance | Hope the platform handles it | Prepare W-9, TIN, invoice, and payer evidence up front |

| Client AP fit | Assume all buyers pay the same way | Match your setup to marketplace, direct, or enterprise billing realities |

The shift is simple: stop evaluating standalone apps and start designing for failure. The next section turns that into a practical stack. If you want a marketplace comparison after that, see 7 Upwork Alternatives for High-Earning Freelancers.

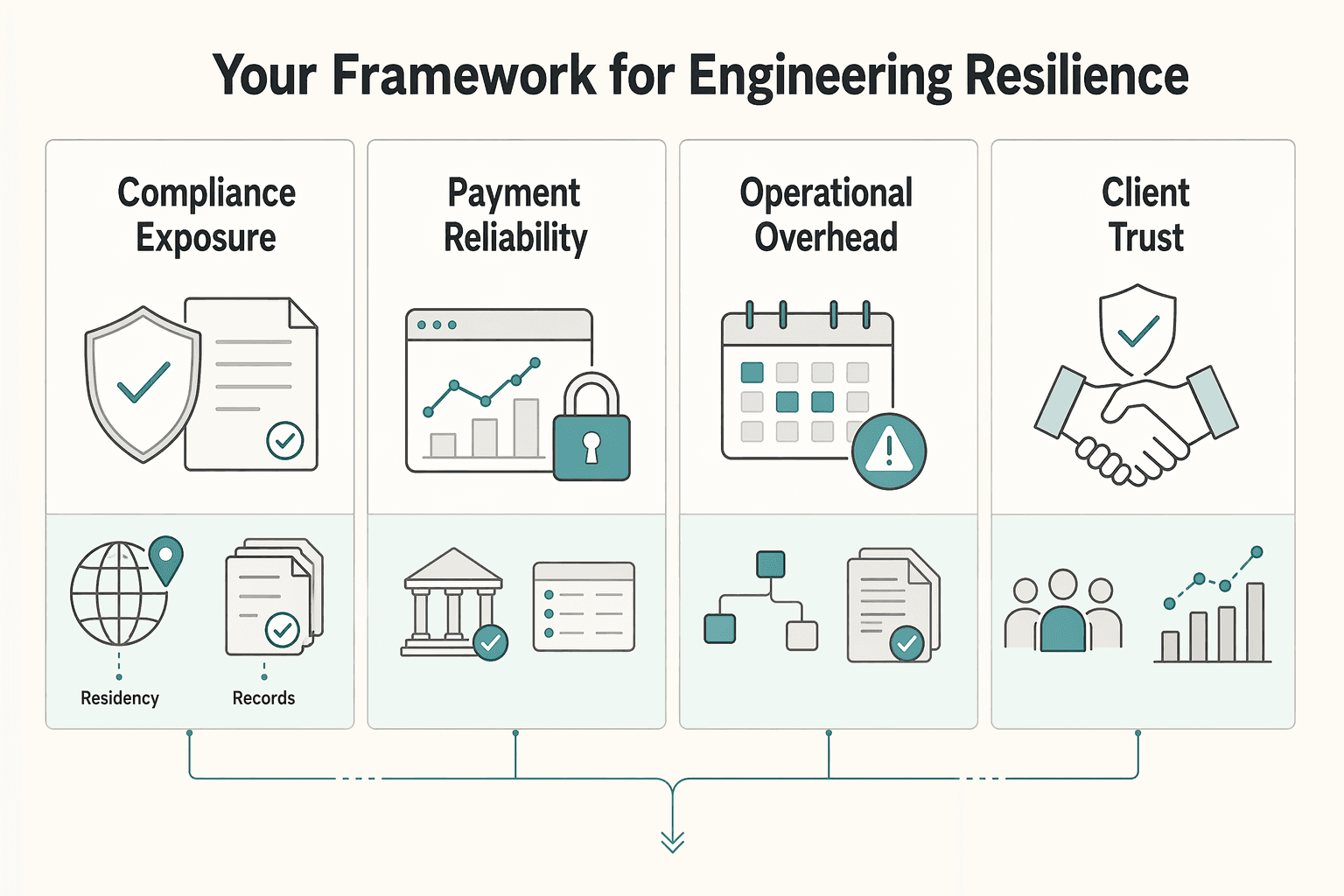

The Sovereign Stack: Your Framework for Engineering Resilience#

Build your stack in three layers, in order: compliance first, then cash control, then operations. This sequence changes the core decision from "Which app is easiest?" to "Which setup reduces failure risk before you invoice?"

| Patchwork tool stack vs Sovereign Stack | Patchwork tool stack | Sovereign Stack |

|---|---|---|

| Compliance exposure | Day counts, tax forms, and account thresholds are scattered and checked late | Residency tracking, cross-border tax documentation, and account monitoring are checked before invoicing |

| Payment reliability | You learn hold rules and release windows after revenue is earned | You select channels based on reserve terms, payout timing, and who is legally processing payment |

| Operational overhead | Re-entry across contracts, invoices, tax docs, and receipts | One client record ties scope, tax docs, invoice status, payment status, and evidence |

| Client trust signals | Buyer has to chase missing forms or verify details manually | You can provide a clean vendor packet with form status, VAT check result, and records on request |

Build the compliance foundation#

Start here, because this layer reduces the risk that payment gets delayed by preventable documentation or residency issues. The decision it changes is simple: treat tax and presence tracking as pre-sale checks, not year-end cleanup.

| Checkpoint | Rule or date | Notes |

|---|---|---|

| IRS physical presence test | 330 full days within a 12-consecutive-month period | Days do not need to be consecutive; a full day is 24 hours from midnight to midnight |

| UK automatic overseas test condition | Fewer than 16 days in the UK | For some people who were UK resident in one of the prior three tax years |

| FBAR account monitoring | $10,000 aggregate trigger during the year | Monitor whether foreign accounts cross it |

| FBAR filing dates | April 15 due date | Automatic extension to October 15 where applicable |

If you work across borders, track days by jurisdiction. For the IRS physical presence test, use 330 full days within a 12-consecutive-month period; days do not need to be consecutive, and a full day is 24 hours from midnight to midnight.

Use country-specific residency rules where relevant. For the UK, one automatic overseas test condition is fewer than 16 days in the UK for some people who were UK resident in one of the prior three tax years. For other countries, verify the current threshold before you rely on it.

Action checks:

- Confirm whether your payer may request Form W-8 BEN and keep it current.

- Monitor whether foreign accounts cross the FBAR $10,000 aggregate trigger during the year.

- Track FBAR filing dates: April 15 due date, with automatic extension to October 15 where applicable.

Once this layer is stable, move to cash access.

Protect the financial core#

This layer reduces the risk that earned revenue is delayed or restricted. It changes how you choose channels: by reserve policy, release timing, invoice acceptance, and legal payment responsibility.

| Item | Grounded detail | Context |

|---|---|---|

| Upwork hourly | Earnings available ten days later | Hourly contract |

| Upwork fixed-price | Funds released five days after milestone approval | Fixed-price contract |

| PayPal access limits | Terms allow limiting access to funds for up to 180 days | Some violation cases |

| VIES VAT check | Returns valid or invalid status only | Before issuing B2B invoices |

| Merchant of Record | Legally responsible for payment processing and key financial, legal, and indirect-tax duties in the transaction | Responsibility shift, not a magic fix |

Before you agree to delivery and payment terms, check:

- Review reserve language; reserves are a common practice and can temporarily hold part of funds.

- Check payout windows by channel and contract type.

- Confirm restriction clauses that can limit access to funds in policy-violation contexts.

Examples from current platform mechanics show why this matters: Upwork timing differs by contract type (hourly earnings available ten days later; fixed-price funds released five days after milestone approval), and PayPal terms allow limiting access to funds for up to 180 days in some violation cases.

For cross-border invoicing, validate EU VAT IDs in VIES before issuing B2B invoices. VIES returns valid or invalid status only, and urgent validation issues should be escalated to local tax authorities.

If you use a Merchant of Record, treat it as a responsibility shift, not a magic fix: the MoR is the entity legally responsible for payment processing and key financial, legal, and indirect-tax duties in the transaction.

With compliance and cash controls in place, operations can be simplified without losing traceability.

Tighten the operational edge#

This layer reduces avoidable friction. It changes the decision from "add another tool" to "keep one traceable record from onboarding through payout."

Use a consistent client file checklist:

- Signed scope

- Tax form status

- VAT validation result (if relevant)

- Invoice

- Payout confirmation

- Receipts and correspondence needed to support the transaction

This is not optional admin. IRS recordkeeping requires you to keep records long enough to prove income or deductions on a return. When records are split across inboxes, chat threads, and separate apps, the cost is slower AP approval, weaker review responses, and harder tax close.

The outcome is straightforward: fewer surprises, clearer trust signals, and better control over when work becomes usable cash. You might also find this useful: Build a Digital Garden That Supports Better Freelance Client Fit.

How to Think Like a CEO When Choosing Your Tools#

Use three decision tests before you adopt any tool: control risk, compliance risk, and cash-flow risk. If a tool fails one of these tests, convenience features do not matter.

A scheduling app is usually an operational choice. A payout stack that can pause or cancel disbursements is a cash-flow choice. A client portal with weak export and retention behavior is a compliance choice. Keep those categories separate so you do not underprice the real risk.

| Option pattern | Control | Compliance readiness | Integration depth | Failure-mode impact |

|---|---|---|---|---|

| Marketplace with platform-enforced payments | Lower. Platform terms may prohibit off-platform payments, and violations can lead to account loss | Mixed. Invoices may be available, but retention windows can be limited; one major platform states five-year invoice access, then permanent deletion | Often strong inside the platform, weaker when moving records out | Restrictions can limit where and how you get paid |

| Payment app or stored wallet balance | Lower to moderate. Access is not the same as full control of held funds | Usually weaker unless you export and archive records yourself | Moderate for payment activity, often weak across full client-to-reconciliation workflow | Reserves may be applied; money held in some P2P apps is typically not FDIC insured |

| Processor stack with exportable ledger reporting | Higher when you control the account and can export records | Stronger when itemized exports and reconciliation reporting are available | Stronger when client, invoice, payout, and reconciliation data stay connected | Still exposed to payout pauses, failed payout handling, and portability limits if not checked upfront |

Reduce the biggest risk first#

Start with the risk that can break your business, not the feature that saves a few clicks. If a tool touches tax forms, invoicing, client identity, or income records, test whether it helps you keep evidence that substantiates income and deductions.

Run one pre-adoption drill: create a sample client, issue an invoice, export all related records, and store them outside the platform. If that workflow is hard, the stack is fragile. If the platform is your only archive and retention is finite, treat that as a decision blocker, not an admin footnote.

Check who actually controls money and records#

Treat this as a hard gate. For each option, confirm the points below.

| Control point | What to confirm | Article detail |

|---|---|---|

| Pending funds | Who controls funds while they are pending | Some platform-connected payout systems allow unilateral payout pauses, including in-flight payouts |

| Payout blocks | Who can pause payouts or block disbursements | If a pause is not lifted within 10 days, a payout can be canceled |

| Exportable records | Who owns exportable records if you leave | Treat this as a hard gate |

| Failed payouts | What happens to the external account involved | Failed payouts can disable the external account involved until remediation |

| App balance terms | Current protection standard for your specific product and jurisdiction | Reserves can hold funds, and terms change over time |

This matters because some platform-connected payout systems allow unilateral payout pauses, including in-flight payouts; if a pause is not lifted within 10 days, a payout can be canceled. Failed payouts can also disable the external account involved until remediation. That is direct cash-access risk.

Apply the same check to app balances. Reserves can hold funds, and terms change over time (for example, the referenced PayPal User Agreement page shows a January 26, 2026 update date). If you keep working cash in an app balance, verify the current protection standard for your specific product and jurisdiction.

Follow the path from intake to reconciliation#

Use one workflow lens: intake -> signed scope -> tax-form status -> invoice -> payout -> reconciliation. If you cannot complete and export that chain quickly, fragmentation is already a risk.

Feature depth in one tool is not enough if records do not travel cleanly across the full path. Prioritize systems that support ledger-level exports and payout-to-transaction reconciliation so month-end close and reviews are straightforward.

Keep this rule: if you cannot trace one invoice from intake to bank deposit and export proof in minutes, do not make that tool central. Outsourcing a function can reduce workload, but accountability stays with you.

If you want a deeper dive, read How to Get Featured in the Press as a Freelance Expert.

Conclusion: You Are the CEO of Your Freedom#

Do not treat this as a search for a better marketplace. Your job is to choose terms, payout mechanics, and records you can verify before your revenue depends on them.

The practical shifts are simple:

- From renting infrastructure to owning your records: if a tool cannot give you usable exports, archives outside the platform, and a payout path you control, it is not your operating base. Keep invoices, contracts, payout confirmations, and tax records outside the platform, and remember the IRS says some records, such as employment tax records, must be kept for at least four years.

- From reacting to risk to checking the failure mode first: read the live help page and agreement before you commit volume. Upwork fee references are not fully consistent across help pages, Fiverr applies a 14-day clearing period before funds are withdrawable, and PayPal can revise terms over time, so your checkpoint is always the current contract or policy page, not an old assumption.

- From asking for access to presenting operating authority: clear process can make approvals easier. If you can show who invoices, where funds settle, what happens if a chargeback or suspension occurs, and how records are retained, you are easier to approve and easier to work with.

That is what the three Sovereign Stack layers are for. Compliance records support safer operations. Financial controls support steadier cash flow. Clear selection criteria help you choose tools without getting distracted by labels or brand familiarity.

For your first pass, keep it narrow:

- list every platform that can delay payment, revise terms, or restrict account access

- verify one payout rule, one hold rule, and one export path for each

- test one invoice, payout, and archive cycle

- add any missing evidence requirements before you rely on the stack

Adopt that decision habit first. Once you verify ownership, risk controls, and operating authority, the better tool choice usually becomes obvious. For a step-by-step walkthrough, see Build a Platform-Independent Freelance Business in 90 Days.

Frequently Asked Questions

What are the best platform alternatives for international professionals?

There is no universal best option. Compare providers by the risk they reduce, the diligence they add, and who controls funds and records when something goes wrong. In practice, stronger choices usually have clearer eligibility rules, clearer payout and redemption mechanics, and governance you can verify.

How can a solo professional build trust with enterprise clients?

Build trust with evidence, not positioning. Ask the client for current vendor requirements before onboarding, and be ready to show a named legal entity, clear decision rights, current documentation, and clear security or compliance leadership if requested. Also check that provider documents are dated and current.

What is a "trust stack" for a global professional?

A trust stack is shorthand for the providers and controls you rely on, not a certification label. For each provider, verify eligibility gates, how hard the offering is to evaluate, when you can exit or get paid, and who governs changes. Treat labels like direct settlement or compliance-ready invoicing as prompts to confirm who holds funds and what records you can export.

Is decentralization the future for freelance platforms?

Maybe, but it should not be your first filter. Governance and exit mechanics matter first, because diligence can be harder and some redemptions may be limited to tender windows or repurchase periods. If a provider claims community governance, verify the legal entity, decision process, and whether stakeholder rights are written down.

How do I protect my income from being frozen by platforms like PayPal?

Reduce concentration before volume grows. Do not let one provider be your only invoice trail, archive, and payout route, and verify hold or reserve language in the governing agreement. Before routing meaningful revenue through the account, test one payout and export cycle.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- consumerfinance.gov/ask-cfpb/is-the-money-i-keep-in-my-payment-a...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- irs.gov/taxtopics/tc307trusted

- paypal.com/us/legalhub/paypal/useragreement-fulltrusted

- security.cms.gov/posts/understanding-and-avoiding-single-poin...trusted

- stripe.com/resources/more/merchant-of-recordtrusted

- web.uri.edu/risbdc/financing-your-business-frequently-as...trusted

- catnmsplan.com/faqexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: