Quick Answer

Handle these flows as three separate money jobs: rent collection, deposit custody and refunds, and service-provider payouts. Choose rent rails by verified initiation, completion, and failure behavior, make deposit handling launch-ready only when the holder, release trigger, and evidence are clear, and block vendor payouts until the payee, destination account, and ledger reference all align.

Design PropTech payment flows before adding features#

With proptech marketplace payments rent deposits and service-provider payouts, the real decision is operational design, not feature count. You need a setup that can run across countries without creating manual cleanup, custody ambiguity, or reconciliation gaps after launch.

Scope the decision around three money jobs#

Start by separating the problem into three jobs: rent collection, deposit handling, and payouts to service providers such as maintenance vendors. They can share one product surface, but operationally they behave differently. Treating them as one generic payments feature is where hidden ops debt begins.

The tension shows up immediately. Tenants want speed, vendors want payout certainty, and property managers want control and traceability. If you optimize only checkout, you can still end up with delayed refunds, unclear deposit ownership, and manual ledger fixes.

Use this early checkpoint: can each money movement be traced from user action to accounting outcome? If rent does not post cleanly into accounting software, or deposit handling is not clearly tied to the holder and release conditions, the design is not launch-ready.

Use go or no-go checks, not trend commentary#

This guide is for go or no-go decisions on rails, custody, and payout design, not trend commentary. That framing matters because manual workflows still show up in property operations, and they create both drag and error risk.

Paper checks, manual refunds, delayed payouts, and labor-heavy entry do more than slow teams down. They weaken dispute handling and reduce confidence in month-end close.

Two red flags are practical and immediate:

- Staff must rekey data between payment events and the ledger.

- Custody language is vague where a rental deposit account or escrow account is involved.

If the holder, release trigger, and retained evidence are unclear, treat that as a stop signal.

Define success before you expand#

Success in expansion is operationally simple: low payment friction, clear gates for deposit and payout handling, and audit-ready execution as volume rises. In practice, that means fewer manual interventions, explicit approval paths, and records that hold up in disputes and close cycles.

Validate behavior, not just adoption. A solid collection flow supports recurring monthly payments and one-time monthly payments. A solid back-office flow posts payment outcomes directly into accounting records instead of relying on manual reconciliation.

Keep deposit handling market-specific. In the Switzerland example, tenant deposits can be locked in escrow up to three months' rent, with examples from 500 to 7,000 Swiss francs. Use that as a control reminder, not a rule to apply elsewhere.

Read the rest of this guide through one filter: reduce friction without hiding responsibility. Growth with unclear custody, delayed posting, or manual payout cleanup is not scale. We covered this in detail in Payoneer Marketplace Payments Review: Test Channels, Costs, and Controls First.

What to prepare before you design the flow#

Do the prep before you sketch screens or choose rails. Without it, teams usually build on assumptions and then have to rework onboarding, refunds, and reconciliation after launch.

Build a country brief from operating reality#

Build one brief per launch country, even if the product looks the same. For each market, document local bank transfer norms, whether Open Banking is usable for your users and partners, and whether Direct Debit is a current behavior or a later option.

Keep each brief operational:

- expected payer action

- expected settlement signal

- what finance needs to post the event cleanly

Tag every assumption to a named internal owner such as legal, local operations, or a banking partner. If a rail is included because it is common elsewhere, mark it as unverified.

Lock down deposit custody questions early#

Treat deposit handling as its own prep stream, not a rent add-on. Confirm who can hold a Rental Deposit Account or Escrow Account in the target market, who can approve release, and how a Security Deposit Refund is triggered, reviewed, and evidenced.

If custody language is vague, stop and narrow scope. You should be able to state the holder, the refund trigger, and the record that proves the decision before deposit design moves forward.

Confirm payout destination data before onboarding build#

Payout destination requirements shape onboarding, so confirm them early. Clarify whether service providers need local account details, IBAN, SWIFT Code, or a mix.

Then test your draft onboarding form against real vendor profiles. This catches a common failure mode: building for domestic payouts first, then rebuilding later for cross-border or multi-format destination data.

Define the first 90-day operator pack#

Before launch, define the operator pack you will actually use so operations are traceable from day one. Document the owner map, escalation path, and evidence logs for settlement delays, failed pulls, and unmatched returns.

At minimum, retain:

- payment reference

- event timestamps

- user or vendor identifier

- action taken

- resolution outcome

If this pack is missing, the product can look clean while day-to-day operations still break down.

Separate the three money jobs before choosing tools#

Split the architecture into three distinct jobs before you compare vendors or rails: rent collection, deposit custody and refunds, and service-provider payouts. Treating them as one "payments" feature usually leads to mismatched controls, weak ledgers, and support failures during disputes.

| Money job | Primary objective | Key control |

|---|---|---|

| Rent collection | Collect successfully, detect failure quickly, and keep the tenant obligation clear | A failed or reversed collection should change payment state, not contractual obligation by accident |

| Deposit custody and refunds | A control-and-evidence workflow | In England and Wales, deposits must be protected in an approved scheme within 30 days and agreed returns must be paid within 10 days |

| Service-provider payouts | Speed comes after verification | No payout leaves until payee, destination account, and ledger reference align |

Separate rent collection from the other flows#

Rent collection should have one core objective: collect successfully, detect failure quickly, and keep the tenant obligation clear. Optimize this flow for collection performance and clean settlement signals, not for custody logic or fast outbound disbursement.

Use a simple check: a failed or reversed collection should change payment state, not contractual obligation by accident. In the UK, the Direct Debit Guarantee can require an immediate refund for an error, while the underlying bill may still be owed.

Isolate deposit custody and refund controls#

Deposit custody is a control-and-evidence workflow, not a standard rent payment reversal. A Security Deposit Refund follows a different operational path from both a rent reversal and a card authorization reversal.

Be explicit in process language. In England and Wales, tenancy deposits must be protected in an approved scheme within 30 days, and agreed deposit returns must be paid within 10 days. If disputed, resolution depends on evidence such as the deposit return request, tenancy agreement, and check-in and check-out records. Reusing a generic "refund payment" action often strips out the approval trail you need to justify release.

Gate payouts on verification before speed#

Provider payouts should be a separate job where speed comes after verification. Fast rails can improve timing and finality, but they do not replace payee and ownership checks.

In the U.S., covered institutions must identify and verify beneficial owners of legal-entity customers under 31 CFR 1010.230. Keep a hard release gate. No payout leaves until payee, destination account, and ledger reference align.

Use Zego Pay and Finexer as reference patterns for how vendors package these flows, then validate each assumption at country level before you adopt it. For a step-by-step walkthrough, see How to Build a Dispute Resolution Workflow for Marketplace Payments: From Claim to Resolution.

Choose rent collection rails by market economics and failure behavior#

Choose a rent-collection rail only after you can verify, in your own market, when a payment is initiated, settled, failed, or still uncertain. Until those states are reliable, keep tenant-facing and ledger posting states conservative instead of treating attempts as final.

Define the proof you need before comparing rails#

Set the evidence standard before you compare vendors. Decide what event marks initiation, what event marks completion, and what record your support team can use when a tenant says they paid. If those answers are unclear, your rollout criteria are not ready.

Use a test matrix and observed outcomes#

Compare options only through observed behavior in pilot traffic.

| Option in scope | Status signals to verify | Failure scenarios to simulate | Posting rule before certainty |

|---|---|---|---|

| Primary collection rail | initiation, completion, and failure states | delayed failure discovery, duplicate events, auth or session drop-off | keep as pending until completion evidence is consistent |

| Backup collection rail | same state coverage as primary | retry collisions, late callbacks, ambiguous reversals | no final posting without clear completion or final-state signal |

Validate operator controls before scaling#

Before you scale, test the controls around each rail. That includes webhook handling for late, out-of-order, or duplicate events, idempotent retries, and strict separation between projected and settled balances. The same payment should resolve to one final ledger state, even under replay or delayed messaging.

Stage rollout by evidence, then expand#

Roll out in stages based on measured outcomes in your tenant base, not market lore. Keep one primary rail plus a live fallback until failure timing and support load are predictable. For deeper architecture guidance, see How to Build a Rent Collection Platform: Payment Architecture for PropTech Marketplaces.

You might also find this useful: How Marketplace Operators Choose a Platform Payments Architecture That Lasts.

Decide who holds deposits and how refunds are released#

Do not treat deposit custody as an extension of rent collection. If you cannot state, for a specific market, who legally holds the money, who can approve release, how disputes are decided, and what evidence you retain, do not launch deposit custody yet. Launch rent collection first and gate deposits to a second phase.

Fix the holder model before you design the product#

Decide the control model first, then design the flow. Whether you call it an Escrow Account or a Rental Deposit Account, use the same four checks:

| Check | What must be clear before launch |

|---|---|

| Legal holder model | Who is the holder or controller of the deposit, and whether your platform can operate in that role |

| Dispute pathway | Who decides when landlord and tenant disagree, and whether your platform decides, documents, or only transmits |

| Release approvals | Whether release needs one party, both parties, or manual review under policy |

| Audit artifacts | What records prove receipt, holding, review, release, or retention |

If any answer is vague, stop. The risk is not only compliance uncertainty. It is operational uncertainty when support is asked why funds are locked or why a refund was denied.

Keep this grounded in reality: digital rental workflows can still include manual input and subjective judgment. Deposit disputes are not purely payment events, so decision traceability has to be designed in.

Separate market assumptions early, especially inside one country#

Validate each launch area as its own case before you enable custody. As an operating example, handle Switzerland and Geneva as separate checks until confirmed otherwise, rather than assuming one onboarding flow and one release explanation will fit both.

The point is not to assert a specific local rule without confirmation. It is to recognize that local norms and tenant expectations can change onboarding friction and support load, even when product labels look familiar. Do not assume an Escrow Account label is interchangeable with a Rental Deposit Account across markets.

Define the refund sequence as an auditable chain#

Your Security Deposit Refund flow should be fixed internally and easy to defend:

- Capture the trigger event

Record what initiated review and tie it to the deposit record with a timestamp.

- Run approval checks

Verify required approvals for that market and holder model. If a manual reviewer intervenes, log the reason and policy basis.

- Issue the payout instruction

Send the instruction only after beneficiary details match the approved decision.

- Confirm refund completion

Mark the refund complete only when completion evidence exists, not when an instruction is created.

This is a speed-versus-reversibility control. Automate what you can later explain, and keep clear reasons for each state change.

Keep a dispute evidence pack for every deposit decision#

For each dispute or exception, keep the same minimum evidence pack:

- timeline logs of state changes and communications

- policy decision or reviewer rationale

- beneficiary details used for release or retention

- immutable status history showing who changed what and when

Explainability and data integrity are practical requirements, not optional polish. GAO's review of rulemakings, legal cases, and enforcement actions from 2019-2024 reinforces that process defensibility and data quality matter during scrutiny, not only the final customer-facing outcome.

If you cannot reconstruct how a dispute was decided, custody is not operationally ready. For a deeper dive, read How Accommodation Rental Platforms Pay Hosts: Payout Architecture for Short-Term Rental Marketplaces.

Design service provider payouts with explicit policy gates#

Once deposit custody is separated and auditable, keep provider payouts policy-first and speed-second. In PropTech, where stack decisions overlap with FinTech and accounting tooling, payout design is an operating model choice, not just a feature toggle.

Define payout eligibility before enabling faster paths#

Define an explicit internal payable state before you enable any faster rail. Do not rely on a generic status like "approved vendor." Document the checks your business, partners, and launch market expect for each provider type and corridor.

If bank identifier fields are part of your flow, define them clearly in your policy and implementation notes, then apply them consistently. For a refresher on identifier differences, see What is an IBAN and How is it Different from a SWIFT Code?.

Use faster rails where timing changes the outcome#

Treat Instant Payments and other real-time rails as targeted tools, not the default for every payout. Prioritize them where delay creates real operational risk, and keep routine disbursements on a path optimized for control and reconciliation.

Set routing rules per payout type#

Set one routing policy per payout category, including the normal path, failure path, and manual-review triggers. The goal is a shared decision record that support, operations, and finance can follow without interpretation gaps.

Keep one traceable chain through accounting#

Require a single reference chain from payout request to approval to ledger posting to the provider-facing reference. Before broad rollout, test sample payouts and confirm your team can reconstruct what was requested, what was approved, what was sent, and what was posted.

Related: CleanTech Marketplace Payments: How to Pay Solar Installers and Energy Auditors at Scale.

Run a country readiness screen before product or GTM spend#

Before you commit build or launch spend, run a country screen that returns go, hold, or no-go. For the UK, this evidence supports tax and entity-readiness checks. It does not clear rail availability, deposit custody legality, payout destination coverage, or dispute enforceability without separate local validation.

Score the five gates and label unknowns#

A credible launch screen records what is verified, what is unknown, and which evidence cleared each gate.

| Gate | What you can verify now for the UK | Status with this evidence |

|---|---|---|

| Rail availability | Verify Open Banking, Direct Debit, and instant-rail coverage with each provider | Hold |

| Deposit custody legality | No support here for escrow, rental deposit accounts, or refund rules | Hold |

| Payout destination coverage | No support here for local account, IBAN, or SWIFT requirements | Hold |

| Verification burden | Structure affects tax and legal responsibilities; records are required; some users must register for Self Assessment; some cases cannot use the standard online filing path | Partial pass |

| Dispute enforceability | No support here for property-payment dispute enforcement or deposit claims | Hold |

This is intentionally conservative. The screen is a decision record, not a sales artifact.

Define what hold allows and blocks#

Use hold when a gate is still unknown instead of forcing yes or no. Define what can proceed now and what must wait.

With this UK evidence, you can continue research and validation work. You should pause anything that assumes live collections, deposit handling, provider payouts, or public GTM claims about those capabilities. Treat "not disproven" as not approved.

Require each gate to show an owner, source link, check date, and next action to clear hold.

Run UK administrative checks with exact thresholds and deadlines#

For UK readiness, HMRC timelines are hard gates. GOV.UK says you must tell HMRC by 5 October 2025 if you need to complete a tax return for the previous year; late notification can lead to a penalty. In the cited example, that year is 6 April 2024 to 5 April 2025.

| UK check | Requirement or threshold | Section note |

|---|---|---|

| Tell HMRC if you need to complete a tax return for the previous year | 5 October 2025 | Late notification can lead to a penalty |

| Sole trader registration | More than £1,000 in a tax year | Sole traders must register |

| Recordkeeping | When they start trading | Sole traders must keep records |

| Online filing | Unique Taxpayer Reference (UTR) | Users who file online need a UTR |

| Filing path | Commercial software or other forms | Some users must use them |

| Existing account status | Reactivate an existing account | Filing without reactivating may delay a return |

If your launch depends on sole traders or self-employed providers, this is operationally material. Sole traders must register if they earn more than £1,000 in a tax year, and they must keep records when they start trading.

Also check filing-path exceptions before launch. GOV.UK says some users must use commercial software or other forms, and filing without reactivating an existing account may delay a return. Users who file online also need a Unique Taxpayer Reference (UTR).

Treat trend signals as prompts, not proof#

Use PYMNTS or similar coverage only to decide where to investigate. It does not clear a launch gate in this evidence set.

Apply the same rule to imported UX assumptions: if your flow depends on behavior seen in the United Kingdom or Switzerland, re-test it locally before product or GTM spend.

Need a practical implementation baseline for those five launch gates? Use Gruv's developer docs to map policy checks, webhooks, and replay-safe payment states before build starts.

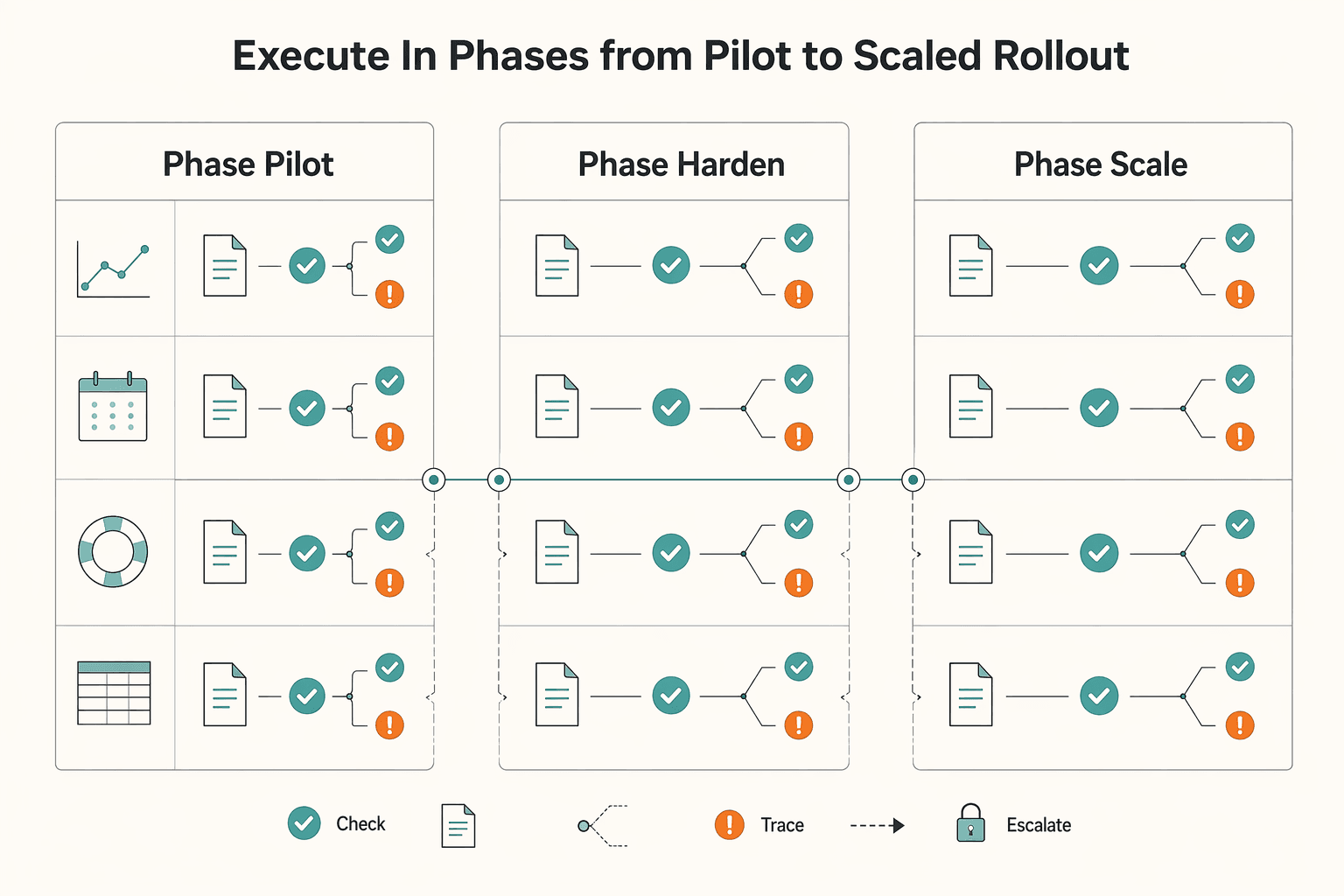

Execute in phases from pilot to scaled rollout#

A market can pass readiness screening and still fail in execution, so scale only after one narrow payment path is observable and recoverable end to end. Use each phase to prove the same four checkpoints before you expand scope: settlement visibility, reconciliation lag, failed-collection recovery time, and payout-exception closure time.

| Phase | Keep scope narrow to | Add only when | Verification focus |

|---|---|---|---|

| Phase 1 pilot | One country, one rent rail, one deposit model, one payout path | Core states and exceptions are visible end to end | Settlement visibility, first-pass reconciliation, basic exception capture |

| Phase 2 harden | Same market, with fallback collection or payout paths | Recovery behavior is predictable and edge cases are resolved without ledger confusion | Reconciliation lag, failed-collection recovery time, deposit-release edge-case handling |

| Phase 3 scale | Higher volume, more counterparties, higher throughput controls | Manual work drops as volume rises | Payout-exception closure time, automated checks, approval controls, integration quality |

Pilot one narrow money path#

Start with one country and one collection method. That is usually enough to expose what breaks first: unclear settlement status, missing return reasons, and payout exceptions without clear ownership.

Instrument every state transition, not just creation and success. You should be able to trace collections and payouts through completion, failure, and reversal paths from logs and exports.

This matters most when settlement is delayed or exceptions arrive late. In the cited U.S. rental context, rent collection commonly runs on ACH and cards. ACH can take two to three business days to fully settle, and card disputes can surface up to 120 or even 180 days after processing. Phase 1 evidence should stay concrete: settlement reports, reconciliation exports tied to ledger entries, an exception log, and before-and-after metrics with a quick-start checklist.

Harden failure handling before widening scope#

Expand only after the primary path fails in controlled, understandable ways. Add fallback rails and retry behavior when recovery is clear, not when launch pressure is high.

Faster rails can improve clearing speed, but they still require verification, fraud screening, and exception resolution. Speed only helps if reconciliation drag and exception backlog stay controlled.

For ACH-like flows, explicitly test reversals tied to insufficient funds, account errors, and unauthorized debits. For deposit-related flows, test release edge cases before opening new corridors.

Scale only after integration removes manual work#

Scale should mean more throughput with less manual intervention, not bigger batch sizes on fragile operations. Add payout batching, automated reconciliation checks, and role-based approvals only when they reduce operator effort without hiding defects.

Integration quality is the practical gate. A PropTech stack is most effective when specialized tools work together, and tool-to-PMS integration helps remove manual entry and prevent costly mistakes.

Keep phase reviews evidence-based. Compare the same four checkpoints across phases and continue only if throughput rises while reconciliation lag and exception closure remain controlled.

Plan failure handling before launch day#

Lock failure handling before launch. In rent deposits and provider payouts, failures are manageable. Unclear ownership, duplicate actions, and weak audit trails are what create expensive damage.

Document the failure classes you will operate#

Use a short, operator-facing list: bank-auth drop-off, delayed Direct Debit returns, unmatched incoming credits, and blocked provider payouts. Treat these as working classes for your flow design, not as assumptions about market-wide failure rates.

For each class, define:

- detection signal

- required system state transition

- evidence required before action

An operator should be able to confirm from logs and exports whether a payment is pending, failed, reversed, or unmatched. If that still depends on copy and paste across tools, the control is fragile. Those handoffs are where inaccurate balances, missed escalations, and compliance slip-ups tend to appear.

Define deterministic recovery paths#

Each failure class needs one replay-safe path so retries, reruns, or resubmissions cannot create duplicate money movement. Keep the path explicit: retry rule, manual investigation queue, counterparty communication, then reconciliation closeout.

For unmatched credits, do not force ledger posting just to clear a dashboard. Hold an exception state, cross-check bank feeds, flag anomalies, and close only after beneficiary and purpose are confirmed. Where payments slip, include tenant-friendly nudges as part of recovery operations.

Limit override powers and log every decision#

Rental workflows still include manual input and subjective judgment, so overrides are necessary. Keep powers narrow by role and tie them to auditable actions.

At minimum, every override record should capture who acted, what changed, prior state, reason, and attached evidence. Interaction-level logging is the practical audit-readiness requirement. Without it, disputed deposit or payout decisions are harder to defend.

Add one rollback trigger per critical flow#

Set one explicit rollback trigger for each critical flow so a bad release cannot keep mutating states silently. The trigger can be simple, but it must stop propagation and force review.

The operational check is straightforward: can you pause, inspect, and recover a broken path without corrupting deposit or payout balances? If not, keep rollout scope narrow until failure handling is stronger than the happy path.

Related reading: How to Launch a Legal Compliance Platform for Freelancers and Handle Their Payments.

Track the few metrics that predict expansion success#

Track a small scorecard that can actually drive expansion decisions. If a metric cannot tell you whether to expand, pause, or redesign, it is noise.

Instrument each collection rail separately#

Do not collapse rent collection into one blended number. Track Open Banking, Direct Debit, and any instant option as separate rails, with two core measures per rail: collection success and time to finality.

Define those metrics precisely: what starts the clock, what ends it, and which state counts as final. If your team cannot verify that from logs, webhook history, and provider exports, the metric is not decision-ready.

Use a before-and-after checkpoint per rail: expected operator touchpoints before launch, then actual touchpoints and exception load after launch. This shows whether the rail reduced time spent chasing rent payments or merely shifted the work into ops queues.

Split deposit operations into their own scorecard#

Treat deposits as a separate workflow. For Security Deposit Refund flows, track average completion time, dispute rate, and the share requiring manual intervention.

That prevents a false signal where rent collection looks healthy while deposit handling is slow or dispute-heavy. For delayed or disputed refunds, keep the evidence trail easy to retrieve: trigger event, approval record, payout instruction, status history, and manual actions.

Measure payout health by rail and exception burden#

For service provider payouts, track first-attempt success, exception volume, and resolution time by Instant Payments and standard payouts. Fast payout paths can expose weak account validation and exception handling sooner.

Count exceptions consistently: failed sends, held payouts, returned funds, and any case that leaves straight-through processing. Measure resolution time from exception detection to confirmed closeout.

| Area | Core metrics | Decision signal |

|---|---|---|

| Rent collection | Success rate and time to finality by Open Banking, Direct Debit, instant option | Whether each rail is operationally reliable |

| Deposit operations | Average Security Deposit Refund completion time, dispute rate, manual intervention share | Whether refund handling is stable enough to scale |

| Provider payouts | First-attempt success, exception volume, resolution time by payout path | Whether payout speed is adding to or reducing ops load |

Tie every metric to an expand, pause, or redesign trigger#

Define the decision triggers before you enter the next market. Set what metric pattern means expand, what means pause, and what means redesign.

Use your own pilot baseline as the reference point. Expansion succeeds when performance stays stable as volume grows. Pause or redesign when exceptions and manual work grow faster than throughput. Keep this strict: in an adjacent property-tech datapoint, 92% of firms had started or planned AI pilots, but only 5% had achieved all program goals. The gap is execution discipline, not launch activity.

Need the full breakdown? Read How to Build a SaaS Marketplace That Manages Subscriptions and Contractor Payouts.

Common mistakes and how to recover quickly#

Most fast recoveries come from fixing the basics before problems compound: screening, agreement clarity, and response discipline.

| Mistake | Recovery | Why it matters |

|---|---|---|

| Skipping proper tenant verification | Require background checks, employment verification, and reference checks before approving a tenant | This lowers exposure to late or unpaid rent, property damage, legal disputes, and unauthorized occupants |

| Leaving core rental terms unclear in the agreement | Make sure one rental agreement clearly defines rent amount, payment schedule, security deposit terms, maintenance responsibilities, and notice period | If terms are fragmented, disputes and operational confusion escalate quickly |

| Delayed responses to tenant issues | Enforce a consistent response process for tenant issues and track adherence | Faster handling helps reduce tenant dissatisfaction, early move-outs, and reputation harm |

Mistake 1: Skipping proper tenant verification#

Recovery: require background checks, employment verification, and reference checks before approving a tenant. This directly lowers exposure to late or unpaid rent, property damage, legal disputes, and unauthorized occupants.

Mistake 2: Leaving core rental terms unclear in the agreement#

Recovery: make sure one rental agreement clearly defines rent amount, payment schedule, security deposit terms, maintenance responsibilities, and notice period. If those terms are fragmented, disputes and operational confusion escalate quickly.

Mistake 3: Delayed responses to tenant issues#

Recovery: enforce a consistent response process for tenant issues and track adherence. Faster handling helps reduce tenant dissatisfaction, early move-outs, and reputation harm.

This pairs well with our guide on Platform-to-Platform Payments: How to Build B2B Settlement Between Two Marketplace Operators.

Frequently Asked Questions

What is the practical difference between rent collection, deposit custody, and service-provider payouts in a PropTech marketplace?

They are different money movements with different controls, so they should not be designed as one flow. Rent collection focuses on successful collection, quick failure detection, and clear tenant obligation, often with per-unit tracking and delayed-payment alerting. Deposit custody needs holder, approval, and evidence controls, while service-provider payouts are outbound vendor payments that should not leave until verification is complete.

Open Banking vs Direct Debit for rent collection: which should we start with in a new country?

There is no supported default choice for every new country in this guide. Start with the rail that, in pilot traffic, gives you reliable initiation, completion, and failure signals and lets you match payments cleanly to the unit and payer without manual cleanup.

When do instant payout rails improve operations enough to justify added complexity?

This guide does not set a universal threshold. Use faster payout rails when delay changes the operational outcome, but keep routine disbursements on a path optimized for control and reconciliation. In all cases, no payout should leave until payout eligibility, payee, destination account, and ledger reference align.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- gao.gov/assets/gao-25-107196.pdftrusted

- law.stanford.edu/wp-content/uploads/2025/07/Corporate-Tech-La...trusted

- scholarworks.law.ubalt.edu/cgi/viewcontent.cgitrusted

- sec.gov/Archives/edgar/data/1903382/0001104659250979...trusted

- sec.gov/Archives/edgar/data/1948697/0001929980230002...trusted

- blog.vopay.com/proptech-embedded-payments-vs-manual-paymentsexternal

- buildium.com/blog/proptech-trendsexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: