Quick Answer

Build the workflow as a clear, auditable path from claim intake to final action. Define dispute categories and rail-specific routing early, assign one owner to each stage, collect structured evidence by case type, use explicit case states, and link every decision to a documented financial or policy action. Keep appeals narrow and track metrics by dispute type, payment rail, and team owner.

Why claim-to-resolution design matters for marketplace payments#

A claim-to-resolution workflow matters because it turns dispute handling from ad hoc judgment into a process you can review, explain, and defend. The goal is simple: move from first intake to final action through a path that stays consistent, traceable, and workable under pressure.

Make the process explicit before scale exposes gaps#

The key requirement is not just choosing an outcome, but showing how you got there. Formal dispute frameworks are useful as process models because they make each stage visible: an initial payment or denial checkpoint, open negotiation, a written decision, and recordkeeping or reporting. You do not need to copy the Federal IDR process to apply that kind of discipline to marketplace payments.

In practice, this guide follows a sequence from intake to execution so cases are less likely to drift across tickets, chat, and spreadsheets. A simple test is whether your team can reconstruct the whole case from notice to final action in one place.

Treat this as an operating model, not a support script#

Disputes often cut across multiple teams, so weak process design creates avoidable drag. When intake is inconsistent and decisions are hard to trace, teams duplicate work, escalate manually, and lose time aligning on what was decided and why.

Process quality also affects fairness. Procedural basics such as timely notice and a reasonable investigation are a useful baseline. That matters most where platforms otherwise have broad discretion and repeat players may hold an advantage over one-time users.

Define scope early so unlike cases do not share one path#

"Marketplace dispute" is an umbrella term, not a single case type. Your scope should separate distinct dispute types so unlike cases do not follow the same path by default.

Those cases may look similar at intake, but they often need different owners, evidence, and payment actions. Merge them too early and decisions can slow down while evidence quality gets worse.

Build a clear sequence with verifiable checkpoints#

This guide gives you an implementation sequence you can assign: ownership by stage, evidence standards by dispute type, payment-rail caveats, and verification checkpoints after each action. The target is not better policy wording on its own. It is a process where notice, investigation, decision, and execution are visible and testable.

One practical rule is worth keeping throughout: every final action should map to a documented decision, and every documented decision should show the evidence reviewed. If you want a deeper dive, read A Guide to Airbnb's Resolution Center.

Prepare policy boundaries and operating inputs before build#

Set your boundaries before you configure queues or automation. If a reviewer cannot point to the policy text, decision authority, and payment record behind an action, the workflow is not ready.

Lock the documents you will actually enforce#

Start by freezing the policy and appeals language your team will use in real cases. Write for consistent enforcement under pressure, not for edge-case perfection.

Run a quick check on recent disputes. Could a reviewer justify the outcome using only those documents? If decisions still depend on unwritten exceptions, tighten the text before you build.

Define case authority and payout pause points#

Assign clear ownership for case actions, including when compliance or risk reviews may pause payouts. You do not need fixed thresholds here, but you do need a named owner who can place a hold, review evidence, and then release or maintain that hold.

Keep one explicit authority path for payment actions and one for policy decisions. If those paths diverge, document the handoff.

Gather the records needed to reconstruct each case#

Make sure each case ties back to a case identifier, payment reference, and relevant system event records. Those inputs let operators trace what happened from intake to final action.

Test that path before launch. Take one case end to end and confirm it can be reconstructed without ad hoc log pulls.

Set guardrails for automation and escalation#

Decide which cases can be automated, which need manual review, and which must escalate before rollout. In dispute operations, automation works best in high-confidence, repeatable cases. Judgment-heavy or sensitive cases should route to human escalation with clear boundaries.

This is an operating decision, not a cosmetic one. Loose boundaries create delays, and delays raise both cost and trust risk. Related: Analyzing the Terms of Service for Upwork and Fiverr: What Freelancers Miss.

Define dispute categories and routing rules your team can apply#

Define categories and routing so unlike cases do not share a queue, and only escalate after a defined earlier step fails. The Federal IDR process follows this pattern: it applies to specific parties and dispute categories and is available after an unsuccessful open negotiation period. Use that as a process example only, since those healthcare rules do not govern marketplace payments.

Build a routing table from policy text and payment records#

Build a routing table from your own policy text and payment records, then test it on intake data. Keep the category set explicit, and define marketplace-specific boundaries and triggers yourself instead of borrowing assumptions from external rules.

Separate category from severity#

Keep category and severity separate. Category decides where the case goes. Severity decides response speed and escalation level. If you use severity dimensions, define clear internal triggers for each so reviewers make the same call under pressure.

Add one early intake rule and one owner per category#

Add one early if-then intake rule and assign clear ownership for each category so cases do not bounce across teams. Then run a consistency check on recent cases. If reviewers cannot reliably land on the same primary route from intake data and policy text, tighten the labels and triggers before you scale automation.

Assign ownership and handoffs across support, ops, risk, and legal#

Put a named owner on every stage before you scale, or cases will drift between teams and the queue will decide ownership for you.

Put one accountable role on each stage#

Put one accountable role on initiation, review, decision, and closure. A practical model is to separate initiation from resolution, then assign one person or team lead to each stage. Use any internal title you want, but name a final reviewer who can make the last call when teams disagree or a case crosses functions.

As a starting template, define owners for intake, payment review, policy or compliance review, legal review, and final approval. Your checkpoint is simple: each open case should show the current owner, when the handoff was accepted, and the next action due.

Split work by judgment type#

Split work by judgment type. Support can own intake quality and customer communications. Payments ops can own transaction and record checks. Risk or compliance can own policy and fraud-related review. Legal can own edge-case terms and external-law interpretation.

| Role | Primary work |

|---|---|

| Support | Intake quality and customer communications |

| Payments ops | Transaction and record checks |

| Risk or compliance | Policy and fraud-related review |

| Legal | Edge-case terms and external-law interpretation |

Keep legal out of routine fact disputes. Bring legal in when terms interpretation, jurisdiction, or settlement language changes the available path.

Make every handoff explicit#

Set explicit handoff rules so a transfer is never silent. A receiving team should accept with a due time, reject with missing inputs, or escalate to the final reviewer.

Use timing as an operational checkpoint at each transfer and decision stage, similar to how formal dispute systems track initiation and determination as separate phases. If the same case type keeps bouncing between teams, your handoff rule is incomplete and needs revision.

Write authority boundaries into terms and SOPs#

Write authority boundaries in both your Marketplace Terms of Service and your SOPs. Terms can define who can submit, what remedies are available, and whether outcomes are final or appealable. SOPs can define who can request evidence, approve remedies, place or release holds, and when final sign-off is required.

For legal edge cases, verify regulatory language against an official Federal Register edition instead of relying only on a web-rendered or scraped page. Retrieval failures happen, including 500 errors, and that should not drive a decision.

Build a claim intake form that creates usable evidence on day one#

If your intake form captures only a loose story and a few screenshots, reviews become less consistent. Design intake so the first submission is already a usable case file: structured facts first, case-specific proof second, narrative last.

Collect structured case data before free text#

Collect structured case data before free text. Start with fields that define the event and dispute category so routing and assignment can happen early.

Use the narrative as supporting context, not the primary record. Add intake controls where possible: validate submitted details against your records, flag likely duplicates, and reduce near-identical repeat submissions that can fragment one case.

Request evidence by case type#

Request evidence by case type, not one generic upload bucket. Ask for proof that matches the claim context. That helps reviewers verify facts without rebuilding the file from scratch.

Store uploads as structured documents with clear labels and metadata. Unlabeled files slow decisions and can create fairness issues when experienced repeat users out-document one-time users.

Standardize evidence packs#

Standardize evidence packs so like cases are reviewed the same way. For each case type, define a minimum pack: required fields, optional fields, and expected documents from each side.

That supports consistency and helps reduce transparency risk. Your operational check is straightforward: two reviewers handling the same case type should see the same field set, checklist, and activity-log structure.

Keep a separate path for negotiated settlements#

Keep one explicit path for negotiated settlements. When a case resolves through negotiated terms, attach the settlement document to the case record and track status in the activity log.

Do not send routine reversals through this path by default. When settlement language is needed, use an approved template path such as What is a Covenant Not to Sue in a Settlement Agreement?. For a step-by-step walkthrough, see How Independent Professionals Build a PCI-Compliant Workflow for Card Payments.

Set payment-rail decision rules before your first high-friction case#

Set rail-first rules before you debate the merits. Different dispute paths bring different deadlines and evidence needs, and they can change how much you can do without external coordination. Once intake is structured, route each case immediately and lock the checklist for that path.

Route by rail first, then assess the claim#

Use one triage view so operators classify the path before narrative review:

| Path | First routing check | Evidence baseline | Timing source you must follow |

|---|---|---|---|

| Chargeback | Transaction reference + dispute reason | Payment record, fulfillment or return proof, customer communications | Your provider notice and case deadlines |

| Internal refund | Entitlement under your policy + prior promises | Order facts, refund amount, case history | Your internal policy clock, unless an external dispute is already active |

| Bank debit dispute | Debit or mandate identifiers + provider case type | Debit details, notice history, customer claim record | Your PSP or bank documentation |

| Faster-transfer dispute | Transfer identifiers + provider case classification | Transfer details, beneficiary details, customer report | Your bank or provider dispute process |

If two operators would route the same case differently, tighten the intake fields before scaling.

Contain first when the external clock is running#

When timing is tight and your file is thin, prioritize containment and clear customer communication before you contest. Klarna's return-dispute flow shows why this matters. The request deadline is 14 days, and if a partner commits to refund but does not execute within 96 hours, Klarna states it will perform an automatic chargeback of the disputed amount.

Build your workflow to prevent that execution gap. Use a mandatory checkpoint for return-style disputes: "Have you received the return?" Require proof with the answer. Klarna's flow uses this checkpoint and requires partners to verify return receipt and update the invoice accordingly.

Keep reason-code discipline#

Treat dispute reason as a routing input, not a reporting tag. Klarna states that each dispute type triggers a specific response flow, so your evidence checklist should change by dispute reason.

For bank-debit and faster-transfer complaints, do not import card assumptions. Pull the provider-specific action sheet before you promise recovery outcomes.

Document authority boundaries and escalation records#

Write down which actions you can execute directly and which require issuer, acquirer, PSP, or bank coordination, then attach that boundary map to operator instructions.

If you are covered by Australia's complaints framework, ASIC Regulatory Guide 271 requires an internal dispute resolution (IDR) system that meets ASIC standards. The highlighted standards are enforceable, effective 5 October 2021. Close each path with a dated final decision record. That date can control external escalation windows. For example, FMOS allows submission within 6 months of receiving a member's final decision.

For a marketplace-specific companion example, see Why Freelance Platform Dispute Resolution Breaks Down and How to Protect Yourself. If your team is formalizing issuer and acquirer paths, map those rules to webhook and ledger events in one implementation pass. Review the docs.

Implement the case state model in product and backend systems#

Build a small, explicit state model so each case follows one auditable path from intake to outcome, not scattered updates across inboxes and chats.

Define a short state list with hard entry and exit rules#

Use a short sequence such as submitted, triaged, under review, decisioned, executed, appealed, and closed. Treat that list as a product design choice, not a legal standard.

Make submitted a real checkpoint with required fields and evidence before a case can move forward. A useful benchmark is the CMS Federal IDR flow. In that flow, parties receive a unique form link, submit the Notice of Offer web form with supporting documentation and a Dispute Reference Number, then receive an acknowledgement email after submission. In your system, submitted should likewise mean provably received.

For under review and decisioned, keep authority explicit. A known ODR failure mode is slow responses or responders without authority to provide a real remedy, so escalate quickly when the current owner cannot decide.

Persist every transition as an append-only event#

Record key system and agent actions as events with trigger source, actor, timestamp, and evidence references. If you maintain a Ledger journal, link case events to immutable journal references instead of relying on editable notes.

Your audit trail should let you answer three questions quickly: what happened, who triggered it, and whether money moved.

Make execution safe to retry with one idempotency rule#

For actions that can move money or apply penalties, use one Idempotency key per intended action so retries return the same result instead of creating duplicates.

This matters most in fast payment systems, which run with instant clearing and round-the-clock availability and still face disputes from fraudulent, erroneous, or contested transactions. A retry should never create a second refund or a second penalty for the same action.

Add exception states for unresolved execution blockers#

When funds or execution status are unresolved, keep those cases in dedicated exception states instead of mixing them into generic review. Use these states to separate reconciliation or execution blockers from claim-merit review and completed execution.

Keep two paths: automated handling when rules are deterministic, and human escalation when facts or authority are unclear. Related reading: How to Build a Milestone-Based Payment System for a Project Marketplace.

Execute decisions with financial and policy actions that reconcile cleanly#

Execution should be consistent. Once a case is decisioned, convert it into one defined action bundle that can be audited end to end.

Map each decision to one action bundle#

Define a single action set per outcome and avoid improvising at execution time. Keep the bundle explicit for both financial and policy consequences so cases are handled consistently.

When a case has both money and conduct elements, execute both in the same bundle so the outcome is complete and traceable.

Post financial actions to the Ledger journal and keep traceability#

Any money movement should be journaled and linked both ways between case and financial records so reconciliation is possible.

Keep rail-specific dispute artifacts with the executed record when relevant. Card flows can include evidence checkpoints, such as retrieval requests and representment decisions, and are sensitive to action deadlines. In fast-payment flows, settlement finality means you should not assume reversal of a completed transfer.

Gate fund release actions before execution#

Apply legal and scheme-level controls before funds move. If required controls are unresolved, route the case to an exception path instead of marking it complete.

A favorable decision alone may not be enough to release funds if control checks are still open.

Verify completion after execution#

Before closing, confirm that required process checks and records are complete for the parties involved and aligned with the case decision.

If any check fails, keep the case open in a verification state until corrected. That is what keeps the process standardized, transparent, and reliable for end users and participants.

Design appeals that are fair but bounded#

Treat appeals as a controlled escalation path, not a full restart of the original review. Keep the scope narrow, define clear intake checks, and make sure the reviewer can actually resolve the issue.

Define what qualifies for appeal#

Write the intake gate in plain language and apply it consistently. Prioritize submissions that add meaningful context to the case record, and be cautious about reopening cases that only restate the same request without new substance.

Use one quick test: does this appeal materially affect the case record or decision context? If not, close it with a clear explanation so persistence alone does not drive outcomes.

Assign review ownership and confirm authority#

Route appeals to a reviewer with decision authority, and use separation where practical so the process is perceived as fair. Appeals tend to stall when responses are slow or the reviewer cannot grant a real remedy.

At intake, send a receipt confirmation and verify the file is complete: original decision, appeal submission, supporting material, and the exact issue under review.

Keep appeal scope tight and auditable#

Use the appeal to reassess the disputed case record and how the existing policy was applied. Do not let a single appeal become a back door for broad policy redesign or unrelated reconciled actions.

If a case surfaces a policy gap, log that as a separate policy work item and keep the appeal decision focused on the case itself.

Close with a documented final disposition#

Use a standard closing template so outcomes are consistent and implementation is easy to audit. When an appeal ends in a negotiated settlement, document the agreement terms and implementation steps in the case record.

For drafting guidance, see What is a Covenant Not to Sue in a Settlement Agreement?.

Add prevention controls that lower dispute volume without harming conversion#

Prevention controls work best when you target the places where confusion and payout exposure are highest, rather than adding blanket friction that slows good users.

Place verification checks where payout risk is real#

Use verification and risk checks at points where payout exposure is highest, especially before releasing funds to sellers. This is mainly a loss-control move: chargebacks can arrive weeks after a seller has already been paid, so releasing funds before key checks are complete can increase exposure.

Keep this operationally clear for support and risk teams. They should be able to see the hold reason, what is missing, and the next action immediately.

Tighten charge clarity across checkout, receipts, and invoices#

Make charge context obvious before and after payment. Confusing billing descriptors are a direct dispute trigger, and multi-party marketplace flows increase that confusion when buyers do not recognize what they were charged for.

Use plain, consistent naming across checkout, receipt, and invoice records so customers can match the transaction without opening a dispute.

Tune pre-dispute workflows instead of leaving them static#

If you use Rapid Dispute Resolution (RDR), treat setup as an ongoing operating decision: pick a provider, gather the required information, and customize rules. Static defaults may be insufficient as dispute patterns change.

The goal is to reduce escalations before they become expensive downstream work.

Add early intervention before arbitration-stage pressure#

Create early internal flags for transactions likely to escalate, then route them to fast support or seller follow-up. Slow responses raise the chance that buyers go to their bank, and once cases move toward chargeback arbitration, fee pressure and operational overhead increase.

Used well, prevention helps protect both dispute volume and your operating capacity as volumes grow.

Track performance with metrics your finance and product teams can act on#

Use a scorecard that separates case speed, financial outcomes, and handling quality. Total dispute volume alone is not enough to run this well.

Disputed transactions can hurt operational and financial performance as well as customer experience, so both timeliness and handling quality need explicit tracking.

| Metric family | Cut the data by | What it should tell you |

|---|---|---|

| Operational KPIs | dispute type, payment rail, team owner | Where cases slow across intake, review, decision, and execution |

| Financial outcomes | dispute type, payment rail, team owner | Which loss patterns repeat and may be preventable |

| Intake and routing quality | routing path, intake completeness, team owner | Whether the right information is collected up front and routed to dedicated dispute support |

| Communication quality | communication path, dispute type, team owner | Whether communication breakdowns are contributing to slower resolution and payment outcomes |

Instrument case-speed metrics at each state change#

Track intake quality, time-to-first-response, time-to-decision, time-to-execution, and appeal reopen rate by dispute type and rail.

Make completeness a hard checkpoint. Each case should include clear handoff ownership and the key timestamps your team needs to see where it slowed.

Treat dedicated dispute routing as an operating control, not an org preference. It helps collect the right information up front, supports more single-interaction handling, and avoids the common failure mode of pushing disputes into unrelated teams.

Tie losses to the payment data that explains them#

Track outcomes against dispute type, payment rail, and team owner so recurring patterns are visible to finance, product, and ops.

Focus reviews on concentration and repeatability: where the same dispute patterns keep showing up, and which cases need better evidence or clearer customer context.

Add communication checks that catch preventable delays#

Track communication breakdowns across team handoffs and customer touchpoints, and monitor whether those cases take longer to resolve.

Use those findings to tighten routing, improve intake completeness, and reduce avoidable delays in dispute outcomes.

Review monthly for quality, not just speed#

Run one monthly review across finance, product, and dispute operations with a single accountable owner.

The goal is to improve resolution quality without worsening customer experience. Watch appeal reopen rate and communication-related issues closely. If speed improves while those signals worsen, quality is likely slipping.

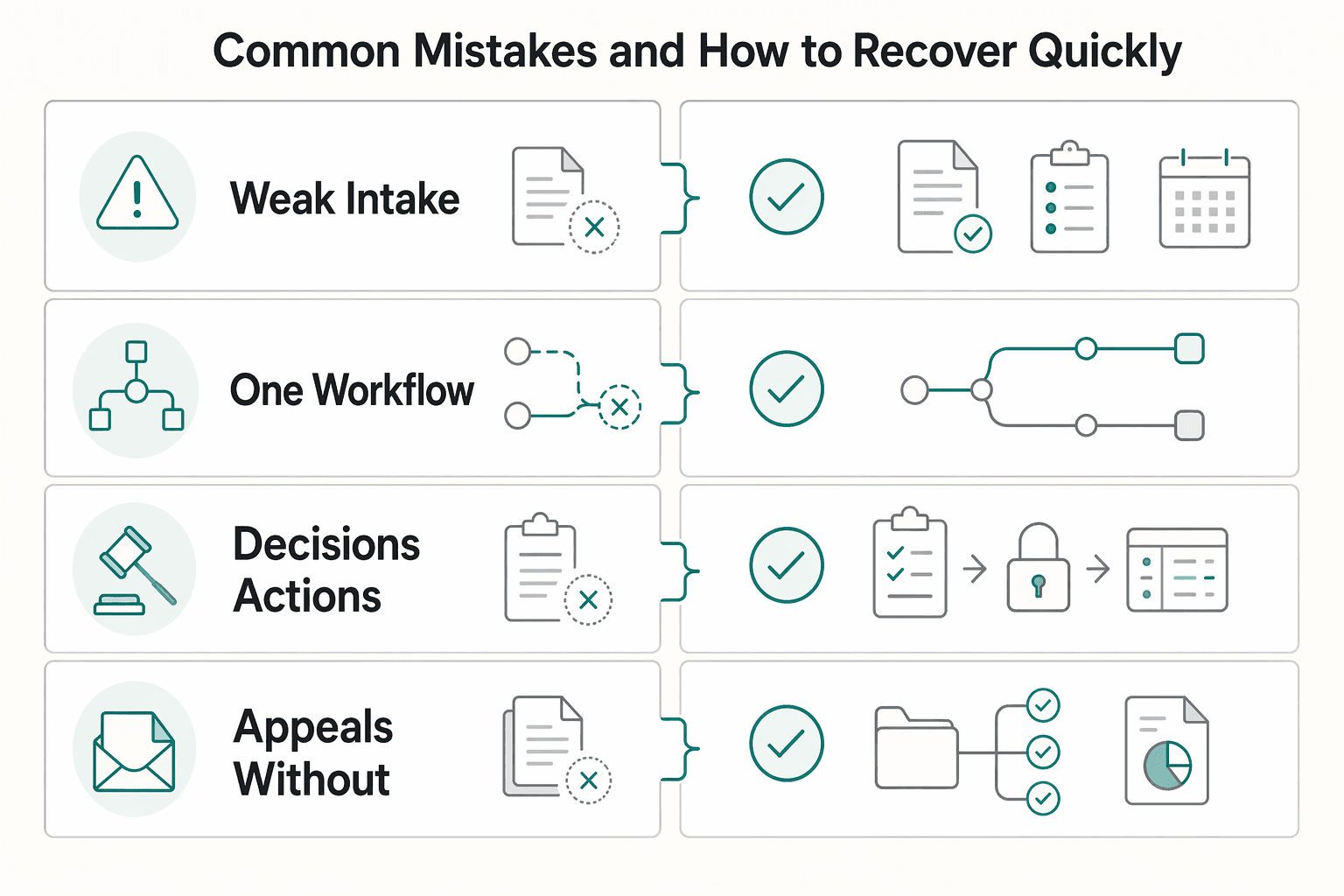

Common mistakes and how to recover quickly#

Common failures in dispute workflows often start at intake and routing, before final decision. A practical recovery path is to remove ambiguity early, separate rail-specific paths, and keep processes standardized and transparent.

| Issue | Why it breaks | Recovery |

|---|---|---|

| Weak intake data | Can lead to slow, inconsistent outcomes | Use dispute-type-specific fields and evidence, and return incomplete submissions for completion |

| One workflow for Chargeback and Fast Payment System (FPS) | Fast payment systems have instant clearing, continuous availability, and settlement finality, so one shared template can hide rail-specific failure modes | Route card-rail cases through a card-specific path and FPS cases through a separate bank-transfer path |

| Decisions and actions in side channels | Recovery and accountability get weaker when decisions happen in side channels | Keep each decision and related action tied to the same dispute record with a clear case reference |

| Appeals without an explicit reopening reason | Appeals become a second first review and slow the queue | Keep a clear basis and scope, and make the reason for reopening explicit in the case record |

Reject weak intake data#

Weak intake can lead to slow, inconsistent outcomes. Use dispute-type-specific fields and evidence, and return incomplete submissions for completion.

For fulfillment disputes, require concrete discrepancy artifacts, such as invoiced quantity versus received quantity, instead of free-text complaints. If a reviewer cannot understand the claim from the case record alone, intake is still incomplete.

Split Chargeback and Fast Payment System (FPS) handling#

Do not assume Chargeback and Fast Payment System (FPS) disputes can be handled as one identical workflow. Fast payment systems have instant clearing, continuous availability, and settlement finality, which creates different dispute constraints.

Route card-rail cases through a card-specific path, and route FPS cases through a bank-transfer path that separately evaluates fraud, error, and contested-transaction scenarios. One shared template for both rails can hide rail-specific failure modes.

Keep decisions and actions in one transparent system record#

Dispute processes should be standardized and transparent. When decisions happen in side channels, recovery and accountability get weaker.

Keep each decision and related action tied to the same dispute record with a clear case reference. Use a quick spot check on closed cases: confirm you can trace the path from intake to decision to action without reconstructing context from chat or offline notes.

Narrow the Appeals process#

Appeals should have a clear basis and scope, not rerun the same review without a defined reason.

If the reason for reopening is not explicit in the case record, appeals become a second first review and slow the queue.

Copy-paste launch checklist for your first production version#

Launch is incomplete if any item below is missing. Your policy text, routing, case record, and financial outcome should all line up without manual guesswork.

-

Marketplace Terms of Service, refund terms, and theAppeals processare published and mapped to case actions (approve, deny, escalate, reopen) for support, payments ops, risk, and legal. - Policy-to-action mapping is validated with sample cases: a reviewer can point to the exact published clause for each decision without relying on side-channel context.

- Any external legal or scheme reference is validated against a controlling source.

FederalRegister.govis explicitly presented as potentially unofficial for legal reliance, and EU file2023/0210(COD)dated22.2.2024is a first-reading text, not a final operating rulebook. - Dispute taxonomy and routing are live for

Chargeback, internal refunds, policy, andIntellectual property claimpaths, with one accountable final reviewer per path. - Intake captures structured evidence: transaction reference, amount, counterparties, timeline, requested remedy, and supporting artifacts; include rail identifiers and a

Reason codewhere applicable. - Case states are explicit and persisted from user actions (for example: submitted, triaged, under review, decisioned, executed, appealed, closed), with financial effects traceable in internal records.

- Retry safety is implemented where money can move, and duplicate-event tests confirm no duplicate refund or reversal outcomes.

- Rail- or partner-specific handling notes are documented with an owner and source of truth, without inventing unsupported deadlines or rights.

- Resolution actions reconcile across case decision, financial records, finance export, customer notice, and payout impact for the flows you use.

- KPI dashboard ownership is assigned with a regular review cadence and a corrective-action owner.

When your dispute workflow is live, connect decisions to payout holds, releases, and retry-safe execution so finance can reconcile faster: Explore Payouts.

Frequently Asked Questions

What are the exact stages from claim intake to final resolution in a marketplace payments dispute?

As an internal design choice, use a short sequence such as submitted, triaged, under review, decisioned, executed, appealed, and closed. The key requirement is that each case stays traceable from claim intake to final financial action.

Who should own each stage across support, payments ops, risk/compliance, engineering, and legal?

The sources do not provide a standard ownership matrix across support, payments ops, risk or compliance, engineering, and legal. Use one accountable owner for each stage, explicit handoffs between teams, and a final reviewer for cross-functional disagreements. Clear ownership helps prevent cases from drifting while timing pressure continues.

When should a case stay in internal resolution versus move to issuer-side chargeback handling?

Keep a case in internal resolution while the payer is still engaging your support path. Move to issuer-side handling when the payer disputes the card transaction through a chargeback instead of customer service. Late involvement can reduce opportunities to preserve key evidence.

What evidence is required to make a defensible decision for delivery, quality, fraud, and policy disputes?

The exact evidence should match the dispute type. Use records that tie the claim to the transaction context, then request case-specific proof such as payment records, fulfillment or return proof, customer communications, and policy or fraud-related review inputs. Standardized evidence packs help reviewers handle like cases the same way.

How should timelines differ across card disputes, direct debit disputes, and fast payment disputes?

Do not run one shared timeline across rails. Chargebacks follow provider notices and case deadlines, internal refunds follow your internal policy clock unless an external dispute is already active, bank debit disputes follow PSP or bank documentation, and faster-transfer disputes follow your bank or provider dispute process. The article also gives source-specific timing examples for credit-card refunds and SEPA Core direct debit disputes, but it does not provide universal Fast Payment System rules.

How do you design an appeals path that is fair to both parties without reopening every case?

Treat appeals as a controlled escalation path, not a full restart of the original review. Define what qualifies for appeal, route it to a reviewer with decision authority, and keep the scope limited to the disputed case record and how the existing policy was applied. Close with a documented final disposition so the reason for reopening and the outcome stay auditable.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- calbar.ca.gov/sites/default/files/portals/0/documents/rfp/...trusted

- cms.gov/files/document/federal-idr-guidance-idr-enti...trusted

- cms.gov/nosurprises/help-resolve-payment-disputes/pa...trusted

- congress.gov/crs-product/R48738trusted

- courts.michigan.gov/49c110/siteassets/reports/odr/sji-evaluation...trusted

- dol.gov/sites/dolgov/files/ebsa/laws-and-regulations...trusted

- ecf.cofc.uscourts.gov/cgi-bin/show_public_doctrusted

- epa.gov/sites/default/files/2015-09/documents/case-s...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: