Quick Answer

Short-term rental platforms pay hosts through a payout architecture that connects guest collection, hold and release rules, host verification, payout routing, provider responses, and reconciliation. The exact payout method and timing vary by country, recipient type, and provider coverage, so platforms need clear ownership for KYC, AML, failed payouts, and finance close before launching a market.

What a Host Payout Architecture Needs to Support#

Choose your payout architecture before you pick your next country. The usual break point is where host payments meet local payout-method coverage, identity checks, risk review, and finance close requirements.

That matters because host payouts are not uniform across markets. Airbnb states that accepted payout options vary by country or region, and even after a platform releases funds there can still be processing time before the money arrives with the payment provider. In some review cases, funds can be delayed up to 45 days after guest check-in. For stays of 28 nights or longer, payout timing can shift again into monthly installments. If your product promises a simple payout experience without accounting for those branches, ops will absorb the gap.

Another early trap is onboarding design. Connected-account verification requirements depend on account location, business type, and requested capabilities, so the KYC path for an individual host in one market may not match the path for a company in another. Treat that as a product decision, not just a compliance afterthought. A good checkpoint is simple: before you open a market, confirm exactly what host data must be collected for each recipient type and when you need it to release funds.

Before you start#

- List target countries and recipient types.

Separate individuals from businesses, and note your expected payout flows for each market. Outcome to verify: you can name the payout method expectation and verification burden for each market before discussing provider fit.

- Assign KYC, AML, and release ownership.

FATF Recommendations, as amended in October 2025, remain the international AML/CFT baseline countries build from. Your practical question is who can approve, pause, or reject a payout when a review is triggered. If that owner is vague, exceptions can sit unworked and hosts will feel it quickly.

- Define reconciliation evidence up front.

Reconciliation is not just reporting. It is how finance tracks payouts against bank deposits and gets the books closed accurately. Verification point: every payout should be traceable through a provider reference, an internal transaction ID, a policy decision, and the final deposit outcome.

This guide focuses on that operating layer. It is less concerned with whether a tool can send money in principle and more concerned with whether you can launch a market without creating unowned failures.

By the end, you should be ready to compare countries, choose a payout model, and sequence launch work around KYC scope, AML review paths, and reconciliation ownership rather than surface-level feature checklists.

Related reading: Schedule E for Foreign Rental Property Without a Year-End Scramble.

What payout architecture actually means in short-term rentals#

Payout architecture is the end-to-end money and control system, not just a provider payout feature. If you cannot show how funds move from guest collection to host disbursement, who can pause or release funds, and how exceptions are resolved, you have an integration, not an operating architecture.

- Step 1: Map the full chain.

In marketplace terms, payout architecture coordinates guest pay-ins and host payouts through payment partners, while also supporting trust and compliance functions. In short-term rentals, that usually means charge creation, ledger posting, eligibility checks, release approval, payout routing, provider response, deposit confirmation, and exception branches for returns or manual review. Your operator should be able to inspect one payout and see the internal transaction ID, provider reference, policy decision, and latest outcome in one traceable flow.

- Step 2: Separate integration from control ownership.

Connecting Stripe or integrating Redsys REST gives you payment rails, not full payout governance. Provider integration is different from owning release rules, failed-payout recovery, and reconciliation sign-off. Teams that treat a provider callback as final completion often discover returned funds, blocked recipients, or missing finance evidence only after launch.

- Step 3: Assign responsibility boundaries early.

Set ownership for Merchant of Record, failed-payout recovery, and reconciliation sign-off before country-level rollout logic is built. In Connect setups, MoR can depend on charge type; for direct charges, the connected account is the MoR. Also, provider verification does not replace your independent legal KYC obligations, so those responsibilities must be explicitly assigned in writing.

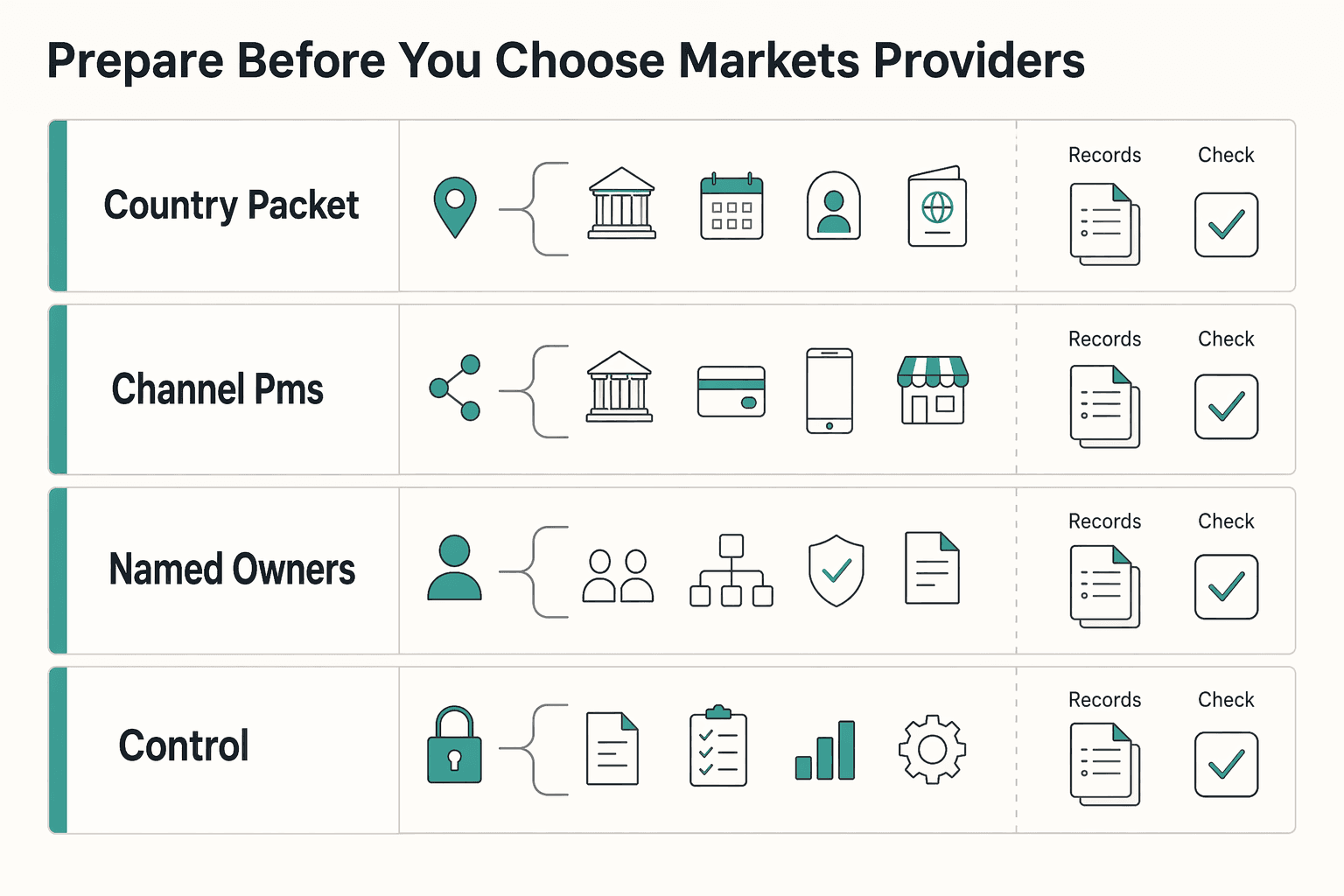

What to prepare before you choose markets or providers#

Before you compare markets or providers, write the prerequisite packet. Lock the inputs that determine whether a market is operable.

| Step | What to lock | Checkpoint |

|---|---|---|

| Country packet | Per country, capture the expected payout rail, timing assumptions, seller type, and host legal profile; keep individuals and businesses separate | For each country, answer what rail you expect, who the seller is legally, and which documents you request first |

| Channel and PMS dependencies | Define where payment state is created and what must sync into your PMS versus stay channel-native; for Vrbo, include the payout summary report | Account for bank availability about 5-7 business days after disbursement and a new partner's first payout around 30 days after guest payment |

| Named owners | Assign a named AML owner, who can approve release decisions, and who signs off reconciliation evidence; AML program approval sits with senior management | Run one failed-payout scenario and confirm who reviews, who re-approves release, and who closes finance evidence |

| Control requirements | Define required payout statuses, required evidence exports, and replay-safe retry behavior; require idempotent payout creation and duplicate-event handling | Resend the same payout request with the same idempotency key and replay the same webhook without duplicate movement or duplicate ledger posting |

Step 1: Build a country-by-country prerequisite packet. Capture, per target country, the expected payout rail, timing assumptions, seller type, and host legal profile. Keep individuals and businesses separate from the start, because onboarding and verification scope differ by business type and channel compliance flows (including KYP) split requirements by entity type. Verification point: for each country, you can answer what rail you expect, who the seller is legally, and which documents you request first.

Step 2: Document channel and PMS dependencies before payout logic. If you distribute through Airbnb, Booking.com, or Vrbo, define where payment state is created and what must sync into your PMS versus stay channel-native. This is an architecture input, not a cleanup task after integration. For Vrbo, include the payout summary report as an evidence artifact, and account for timing: bank availability can be about 5-7 business days after disbursement, and a new partner's first payout can be around 30 days after guest payment.

Step 3: Name owners for AML, release approvals, and reconciliation sign-off. Governance must be explicit before buildout. Assign a named AML owner, assign who can approve release decisions, and assign who signs off reconciliation evidence; AML program approval also sits with senior management. Checkpoint: run one failed-payout scenario and confirm exactly who reviews, who re-approves release, and who closes finance evidence.

Step 4: Lock non-negotiable controls before vendor demos. Define required payout statuses, required evidence exports, and replay-safe retry behavior up front. Require idempotent payout creation and duplicate-event handling for webhooks, since duplicate deliveries can occur and undelivered webhook events can be resent for up to three days. Verification test: resend the same payout request with the same idempotency key and confirm no second movement; replay the same webhook and confirm no duplicate ledger posting or release action.

Map the host payout flow before selecting tooling#

Map the full payout flow, with owners and audit evidence, before you evaluate tools. If this stays vague, provider dashboards can hide where money stalls, duplicates, or fails to reconcile.

Step 1: Write the payout sequence from reservation event to closed case. Start with the release trigger, then map the operating chain end to end: collect guest funds, hold funds, clear eligibility, route payout, confirm provider outcome, reconcile the batch, and close or escalate exceptions. Keep release logic separate from payout execution. Booking.com's model shows why: funds are released per reservation on the check-in day, while Stripe performs the payout.

| Flow step | Minimum internal state | Artifact to store | Common branch |

|---|---|---|---|

| Guest funds collected | collected | reservation ID, amount, currency | payment later reversed or changed |

| Funds held | on_hold | hold reason, release date/rule | manual review or eligibility block |

| Eligibility cleared | eligible | policy decision, reviewer or rule ID | KYC/AML or recipient data issue |

| Payout routed | submitted | internal transaction ID, provider reference | rail unavailable or recipient mismatch |

| Provider outcome received | pending / in_transit / paid / canceled / failed | provider status, event timestamp | delayed settlement or returned payout |

| Batch reconciled and case closed | reconciled / exception_open / closed | reconciliation evidence, close note | unmatched item remains open |

Verification point: for one reservation, identify the exact release trigger, payout submission moment, and closure condition.

Step 2: Define failure branches before you define "success." Use explicit payout states (pending, in_transit, paid, canceled, failed) and avoid collapsing them into "sent." Also separate provider completion from recipient availability: a posted payout can still be delayed by the recipient bank. Include returned payouts as a dedicated branch. Returns are typically seen in 2-3 business days, but can take longer by country. Build duplicate-event and retry controls from day one: webhook endpoints can receive the same event more than once, and undelivered events can be retried for up to three days. One payout request should map to one idempotency key, and one provider event should be processed once.

Step 3: Attach audit evidence at every step, not just at payout time. Store four internal fields on every payout record: provider reference, internal transaction ID, policy decision, and reconciliation evidence. If you use Stripe, also capture the balance transaction link so you can trace entries through the source field. Provider objects do not include your internal policy decisions or handoff metadata, so keep those in your own ledger or case record. Treat reconciliation as a settlement-batch workflow, not spot checks. Finance should be able to validate each payout batch, identify unmatched items, and document why any exception remains open.

Step 4: Add cross-border checkpoints and handoffs before unresolved items start aging. Validate recipient location, business type, and requested capabilities before routing payouts, because verification requirements vary across those dimensions. Check local-currency payout support and route availability early, since rail and timing can differ by market.

- Product owns state definitions, release rules, and blocker visibility in the UI.

- Payments ops owns recipient fixes, failed or returned payouts, and resubmission decisions.

- Finance owns the Reconciliation Workflow, settlement-batch review, and closure evidence.

Red flag: unresolved payouts sitting in a generic "payments" queue with no named next action.

Related: The Best Software for Managing Short-Term Rentals.

Compare integrated payouts and standalone payouts with a market-entry lens#

Choose based on your operating model, not API effort alone. If you are entering one market with limited ops capacity, integrated payouts are usually the cleaner start. If multi-country payout complexity is core to your plan, define standalone control earlier. The key tradeoff is control vs. speed, with Merchant of Record (MoR) responsibility and exception handling as the deciding factors.

Compare the options on the operating axes that matter#

| Decision lens | Integrated payouts | Standalone payouts |

|---|---|---|

| Control | Lower control over payout logic, exception paths, and provider routing when product features abstract those layers | More control over charge model, payout states, routing, and internal evidence requirements |

| Launch speed | Faster when your scope is narrow and the product already supports owner payouts | Slower because you must define account model, onboarding, payout rules, and support handling |

| Dependency risk | Higher concentration risk when collection, release, payouts, and support all sit in one stack | Lower concentration risk if you can segment or switch providers and maintain your own ledger/state model |

| Operational overhead | Lower at launch for small teams | Higher from day one because onboarding, controls, and reconciliation are more exposed |

| MoR clarity | Can look simple in product UI while leaving core obligations with you | Usually forces earlier clarity on who is merchant and who holds legal/compliance obligations |

Use competitor positioning as context, not proof. Hospitable frames owner payouts as built-in, but Owner Payouts and Owner Payments are on the Mogul plan only. It includes the first payout run each month, then charges 1.5% (capped at $5) for additional runs. That is the integrated trade: faster operational setup, but clear boundaries on plan access and payout-run economics.

Check Merchant of Record before feature depth#

MoR is not a UI detail. Stripe defines the merchant of record as the entity legally authorized and responsible for processing payments, including financial, legal, and compliance duties such as KYC and AML. Adyen's marketplace documentation similarly requires marketplace terms to clearly split responsibilities between marketplace and sellers.

Charge model also changes operating responsibility. In Stripe Connect, direct charges are between connected accounts and their customers, while destination charges and separate charges and transfers are between your platform and customers of connected accounts. For Express Dashboard accounts, Stripe states the platform is always responsible for negative balances. If you cannot clearly document your charge model, MoR assignment, and negative-balance policy, market-entry risk is still undefined.

Verification point: before market approval, keep MoR assignment, marketplace terms, and negative-balance policy in one review packet.

Pressure-test concentration risk against your entry plan#

RentalWise positions payout handling through Stripe and Redsys integrations, which can support a speed-first launch in a first market. SuiteOp positions itself as a unified operations platform, which reflects the same convenience pattern.

Test that convenience against exception handling. If your process depends mostly on one provider stack, failure handling in later markets can become slow when payout failures, returns, account changes, or local edge cases appear. The practical screen is simple: can your team reroute, resubmit, and reconcile without waiting on the same stack that created the bottleneck?

A practical rule of thumb: if the next 12 months are one market, one seller type, and thin ops coverage, integrated is a reasonable start. If growth depends on different seller types, cross-border onboarding, or market-specific payout behavior, define standalone control earlier, even if you launch first with one provider.

Decide rollout order with explicit go or no-go checkpoints#

Rank markets by operational readiness, not TAM alone. If a country cannot pass KYC, AML, reconciliation, and failure-handling checks with evidence, it is a no-go for launch sequencing.

| Step | Required proof | No-go signal |

|---|---|---|

| Country readiness | Score provider support for the country and required payout method, whether settlement is local or shifts to cross-border transfer handling, and whether support can explain timing, returns, and required documents | If local payout is unavailable and settlement depends on cross-border transfer handling, move the market down the queue unless your operating playbook is already ready |

| KYC and AML path | Include a written AML program, the country- and capability-specific KYC field set, sample onboarding records, and clear ownership for escalations | If pilot verification timelines miss your launch timeline, treat that as no-go |

| Reconciliation pilot | Finance must trace each payout batch to underlying payments, refunds, and chargebacks, then match batches to bank statements | If reconciliation cannot close within your reporting cycle, do not launch that market yet |

| Failure-case drill | Run returned payout, account mismatch, and suspended recipient scenarios with provider reference, internal transaction ID, current funds location, next action owner, and host-facing message | If this still depends on manual inbox chasing, the market is not ready |

Step 1. Rank countries by operational readiness first. Start with payout rail coverage and support burden. Verification requirements vary by country and capabilities, provider country support is limited, and host payout options are location-dependent. Before committing product work, score each country on:

- provider support for the country and required payout method

- whether settlement is local or shifts to cross-border transfer handling when local payout is unavailable

- whether support can clearly explain timing, returns, and required documents in that market

If local payout is unavailable and settlement depends on cross-border transfer handling, move that market down the queue unless your operating playbook is already ready.

Step 2. Test the KYC and AML path with real host profiles. Do not accept "onboarding works" as a pass. You must collect and verify required information to enable charges and payouts, and provider verification does not replace your independent legal KYC obligations. Your pre-launch packet should include:

- a written AML program

- the country- and capability-specific KYC field set

- sample onboarding records for the host types you plan to support

- clear ownership for escalations when review fails or stalls

If pilot verification timelines miss your launch timeline, treat that as no-go.

Step 3. Prove end-to-end Reconciliation Workflow on pilot volume. Before launch, finance must trace each payout batch to underlying payments, refunds, and chargebacks, then match batches to bank statements. Use a hard gate: if reconciliation cannot close within your reporting cycle, do not launch that market yet.

Step 4. Drill failure cases in the Host Payout Flow. Run a pre-launch drill for returned payout, account mismatch, and suspended recipient. Returned payouts can happen for multiple reasons, incorrect destination details are a common cause, and returns are typically seen in 2-3 business days but can take longer by country; payouts can also be blocked for compliance reasons. For each scenario, require: provider reference, internal transaction ID, current funds location, next action owner, and host-facing message. If this still depends on manual inbox chasing, the market is not ready.

Build the control layer that keeps payouts reliable at scale#

Once a country clears go/no-go, reliability comes from controls you can verify before money moves. Do not release host funds unless policy checks, retry safety, payout status, and reconciliation ownership are all explicit and auditable.

| Control area | Minimum requirement | Evidence or queue |

|---|---|---|

| Release checks | Confirm KYC identity verification, AML review status, and payout eligibility for the specific payout event | Keep one internal decision record with host ID, policy outcome, last check time, and supporting evidence |

| Idempotency | Use one stable idempotency key for payout create, update, and cancel actions, webhook ingestion, and retry jobs; store that key with your internal transaction ID | Log processed event IDs and skip already-processed events |

| Payout visibility | For every payout, show current lifecycle status, latest provider event, unresolved blocker, and next action owner | Operators should not need raw webhook logs or engineering help to answer basic status questions |

| Exception routing | Tie exceptions to structured queues with clear ownership between ops and finance | Use practical queues for duplicate-risk review, missing evidence, unmatched provider event, and released-but-unreconciled |

Gate payout release with explicit policy checks#

Block payout release behind policy checks, not just account creation or a generic "ready" state. At minimum, confirm KYC identity verification, AML review status, and payout eligibility for the specific payout event.

Keep one internal decision record per release decision. Include host ID, policy outcome, last check time, and supporting evidence so a later review can confirm why funds were released or held.

Make retries safe with idempotency#

Use idempotency anywhere retries could duplicate money movement: payout create/update/cancel actions, webhook ingestion, and retry jobs. Treat one intended payout action as one stable idempotency key across retries, and store that key with your internal transaction ID.

For webhook handling, log processed event IDs and skip already-processed events. If retries generate new keys or duplicate events are reprocessed, duplicate payouts become an operational risk.

Set a payout visibility standard ops can use#

Define a minimum payout view that ops can use quickly. For every payout, show:

- current lifecycle status

- latest provider event

- unresolved blocker

- next action owner

If operators still need raw webhook logs or engineering help to answer basic status questions, the control layer is not ready for scale.

Tie exception queues to reconciliation ownership#

Route exceptions through structured queues with clear ownership between ops and finance. Reconciliation should confirm that documentation matches actual fund movement, and completed reconciliations should be documented as part of internal controls.

Avoid a single "failed payouts" bucket. Split exceptions into practical queues, for example duplicate-risk review, missing evidence, unmatched provider event, and released-but-unreconciled, and include the evidence needed to resolve each item.

We covered a related control pattern in Earned Wage Access Architecture: How to Build EWA Into Your Gig Platform.

Common mistakes that delay expansion and how to recover#

Most expansion delays come from control gaps, not missing APIs. Fix these four before the next country launch so payouts stay explainable when ops and finance need to verify what happened.

Step 1. Treat Integrated Owner Payouts as a feature, not full architecture. Integrated owner payouts are useful, but they do not prove your full payout architecture is covered. Recovery: map the controls around Merchant of Record boundaries, approval ownership, and exception handling before rollout. Verification point: for one payout, confirm who approved release, who owns liability boundaries, and where the exception record is tracked.

Step 2. Add payout-state sync to your Property Management System (PMS), not just channel sync. Channel connectivity often centers on rates, availability, and reservations, so payout states can be missed. Recovery: define a bidirectional payout-status contract between your payout layer and PMS so statement-linked states move reliably, including transitions like Published to Paid. If payout status and statement status diverge, expansion risk rises quickly.

Step 3. Require Reconciliation Workflow closure after provider success signals. A success callback is not the same as reconciliation closure. Recovery: require unmatched-item review and close items only when documentation matches actual funds movement, with provider references and internal transaction records attached. If successful payouts remain unmatched with no clear owner, controls are not ready for scale.

Step 4. Harden retries with strict idempotency before scale-up. Weak retry design creates duplicate-operation risk. Recovery: use one stable idempotency key per intended payout action and make event consumers replay-safe, because duplicate delivery can happen. If you use Stripe, idempotency keys can be up to 255 characters; if retries generate new keys for the same action, fix that before adding markets.

Conclusion#

The right call is not which vendor demo looks cleanest. It is which Payout Architecture you can operate with clear ownership when payouts fail, hosts need verification, and finance asks you to prove every movement.

Copy and paste this into your launch review. Then require evidence before any country goes live:

- Confirm the Merchant of Record

Write down who is the Merchant of Record for customer charges and who carries transaction liability. That matters because the MoR is the entity legally authorized to process customer payments and is liable for the financial, legal, and compliance aspects of those transactions. If your team cannot point to one named entity and one owner for charge handling and compliance obligations, you do not have a launch-ready boundary.

Verification point: the decision memo should name the MoR, the liability split, and whether your platform ever holds or manages customer funds. Red flag: if you do manage funds, architecture viability can change because licensing requirements may shift.

- Validate KYC and AML gating for the actual host mix

Do not approve payouts based on a generic "verification supported" claim. Test the gating path for the host types you actually expect in that market, including individuals and businesses. Adyen's platform guidance is clear that users must be verified before payments are processed or funds are paid out. Separately, KYC and AML obligations are not optional parts of ownership.

Evidence pack: sample onboarding records, the exact fields collected, and the blocked states that prevent release. If business hosts are in scope, make sure your AML procedures cover beneficial ownership where required. For U.S. covered institutions, written procedures to identify and verify beneficial owners are explicit under 31 CFR 1010.230.

- Prove the Host Payout Flow with replay-safe idempotency

Run the full payout path from guest payment through release, payout creation, provider response, and exception handling. Your test is not "did money move once." Your test is "can the same request be retried without creating a second payout." Stripe supports idempotent requests for this reason, with keys up to 255 characters, and notes keys can be pruned after at least 24 hours.

Failure mode: retries from jobs, webhooks, or manual ops actions create duplicates because different paths generate different keys. Verification point: one intended payout action maps to one stable idempotency key and one internal transaction ID.

- Run pilot reconciliation before full launch

Finance should sign off only after pilot volume proves the Reconciliation Workflow closes cleanly. Reconciliation is the point where internal and external records are compared to verify amounts match. If provider status says success but finance cannot match it to internal records and external statements, the launch is not ready.

Ask for a daily unmatched-items report during the pilot. Red flag: success callbacks with no provider reference, no ledger link, or no owner for returned payouts.

- Approve countries only where cross-border handling is supportable

Cross-border payouts are not just a rail choice. They come with country availability limits, compliance boundaries, and sometimes extra cost. For example, Stripe documents that self-serve cross-border payouts are limited to listed regions, and in that documented path each cross-border payout incurs a 0.25% fee.

Final rule: if recipient country support, currency handling, or exception recovery is still unclear, do not launch there yet. In a short-term rental payout setup, disciplined no-go decisions are usually cheaper than repairing a messy market entry.

For a step-by-step walkthrough, see Short-Term Rental Industry in 2026: Compliance, Automation, and Niche Strategy.

Frequently Asked Questions

What is payout architecture in a short-term rental marketplace?

Payout architecture is the full money movement and control setup, not just a payout provider. It covers guest collection, hold or release rules, host eligibility checks, payout execution, status updates, and the records finance needs to reconcile each movement.

How do platforms move money from guest payment to host payout without losing traceability?

Platforms keep traceability by carrying the same core evidence through each stage: provider reference, internal transaction ID, payout status, and the policy decision that allowed release. Ops should be able to trace one payout from reservation to final status without asking another team.

Integrated payouts or standalone payouts which is better for a new country launch?

Neither model is always better. Integrated payouts usually reduce rollout effort when you need speed and have limited ops capacity, while standalone payouts make more sense earlier when cross-border complexity and exception control are central. The decision should turn on who owns onboarding, verification data collection, reconciliation, and failed payout recovery.

What must be true before we enable host payouts in a new market?

Before enabling host payouts in a new market, you need a tested KYC path for the seller types you will support. You also need replay-safe payout creation with idempotency, clear status visibility for hosts and ops, and a finance process that can match provider outcomes to your ledger. If you choose API onboarding, the platform owns account interactions and collection of verification information.

What breaks first when short-term rental platforms scale cross-border payouts?

The first things to break are usually verification gaps, unclear ownership for exceptions, and weak reconciliation when provider success does not match what finance can prove. Duplicate execution on retries is another common failure mode, which is why idempotency matters. If one intended payout action does not map to one stable key, scale increases risk.

When should we add owner payouts inside PMS operations?

Add owner payouts when owner statements and payout records become a real property-management responsibility, not just a finance export. Your PMS should at least reflect payout state even if the money moves elsewhere. A good check is whether an owner statement can move cleanly from pending to paid, held, or returned without manual spreadsheet patching.

Which operating metrics matter more than “fast payouts” claims?

The most useful metrics are traceability and closure metrics, not speed claims alone. Watch the share of payouts with a visible current status, unmatched items awaiting reconciliation, returned or blocked payouts, and cases that still need manual intervention after a provider says success. If you cannot see the latest provider event and unresolved blocker for each payout, you have a visibility problem.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- docs.stripe.com/api/idempotent_requeststrusted

- docs.stripe.com/webhookstrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1029trusted

- finance.cornell.edu/controller/internalcontrols/unitlevelactivit...trusted

- stripe.com/ae/resources/more/merchant-of-recordtrusted

- airbnb.com/help/article/425external

- airbnb.com/resources/hosting-homes/a/how-youll-get-paid...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Integrated Payouts vs Standalone Payouts for Platform Architecture Decisions

**Treat integrated and standalone payouts as an architecture decision, not a product toggle.** The real split is the same one you see in payment processing more broadly: either payments are connected to the core platform experience, or they are not. [Lightspeed](https://www.lightspeedhq.com/blog/payment-processing-integrated-vs-non-integrated) puts that plainly in POS terms: your payment terminal either speaks to your point of sale, or it does not. For platform teams, the equivalent question is whether payment flows run through one connected system or sit in separate lanes you manage independently.

The Pros and Cons of Short-Term vs. Long-Term Rentals

You are probably not chasing the biggest headline revenue number. You want rent that arrives, stays collected, and does not turn into a second job or a cross-border tax headache. For an owner living internationally, the real choice between a short stay and a long-term lease is about risk first. Which model gives you lower compliance exposure, less remote operating drag, and more cash left after fees, taxes, and reporting?

The Best Software for Managing Short-Term Rentals

If you own or manage a short-term rental, your job is not just answering guest messages and turning over a property. You are managing an income-producing asset. The real work is protecting cash flow, reducing operating mistakes, and making sure one missed detail does not turn into a booking issue or a compliance problem.