Quick Answer

Start with operability: map a seven-sequence rental journey, choose rails by observed tenant behavior, and lock ledger and event mappings before UI work. For rent collection platform payment architecture proptech marketplaces build decisions, run a narrow pilot where finance ops can trace one successful payment and one failure from initiation to payout block. Gate irreversible payout actions with recorded verification states, and expand only when exception queues, reconciliation output, and audit records stay explainable under retries and delayed webhooks.

What a Rent Collection Payment Architecture Needs to Handle#

The hard part is not launching a rent payment button. It is choosing a payment architecture your team can operate, reconcile, and defend as volume, markets, and exceptions grow.

That focus is practical, not theoretical. An August 16, 2023 field study described rent collection as a major landlord pain point and reported that property managers were increasingly burdened by manual, inefficient processes. The same study also reported collection rates declining from pre-COVID levels of 96-98% to 92-95% in 2021. Those conditions are a good reminder that payment design has to hold up when collections get harder.

Start with operability before go-to-market. If your team cannot clearly explain how a tenant pay-in becomes a landlord payout, where reconciliation happens, and which records make up the audit trail, you do not have an architecture decision yet.

Use this lens up front. Check:

- where manual steps still exist in your rent collections process flow

- how your collections tooling and process hold up as conditions tighten

- legal and financial handoff points when tenants fall behind

- operational complexity your team can absorb

This guide stays narrow on purpose. It focuses on online rent payment system design for marketplaces handling tenant pay-ins, landlord payouts, reconciliation, and auditability. It is not a broad property management playbook. The goal is to help you make architecture choices that survive real operations, especially when collections fail and operational, legal, and financial complexity show up at the same time.

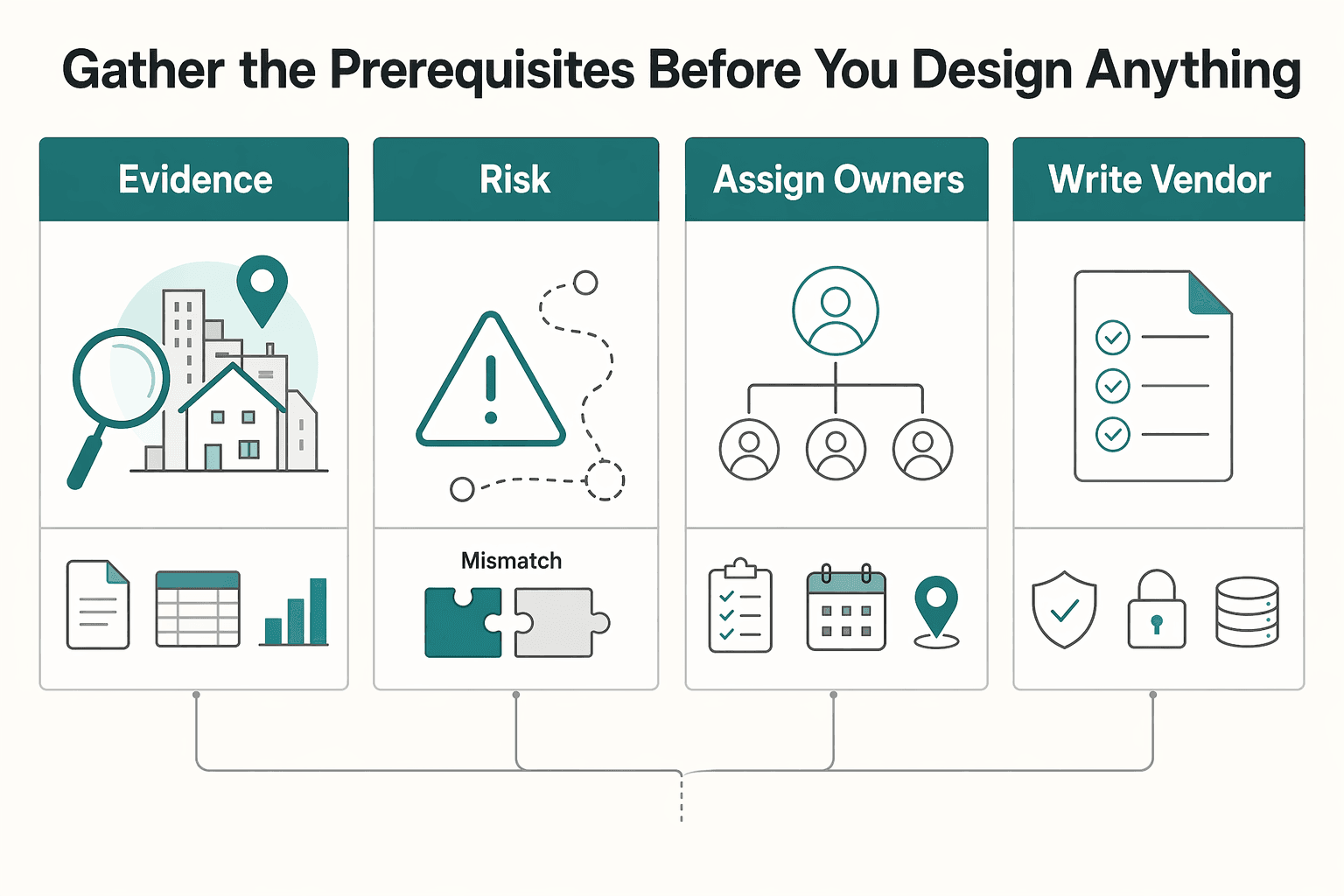

Gather the prerequisites before you design anything#

Start with evidence, not vendor demos. Before you start building, document how renting actually works in each target market, record open policy and operations unknowns in writing, and assign clear owners. If you skip this, architecture decisions get made on assumptions that are expensive to unwind later.

| Step | Written artifact | Why it matters |

|---|---|---|

| Map the real rental journey and build a market evidence pack | Use the seven-sequence rental journey; capture what is known versus assumed; note where quality or trust can fail | Prevents architecture decisions from being made on assumptions that are expensive to unwind later |

| Turn unknowns into written risk signals | Create a short note for each target market with open questions, current assumptions, and owners for follow-up | Keeps what is known versus unknown written and versioned |

| Assign owners and create a shared journey dictionary | Assign owners for product decisions, risk review, and operations follow-through; use one meaning per state across teams | Prevents decision rights drift and diverging reconciliation language |

| Write vendor non-negotiables before taking sales calls | Use a pre-call checklist and answer four core implementation questions before committing to tooling | Keeps selection based on operability, not demo quality |

Step 1. Map the real rental journey and build a market evidence pack.

Start with current renter behavior. Intermediary rental sites can be scattered and incomplete, and renters may move across waiting queues, social groups, and classifieds. Your inputs should reflect that path.

Use a seven-sequence rental journey as your minimum map, ending with post-move feedback. For each sequence, capture what is known versus assumed, plus where quality or trust can fail, such as stale listings, weak listing detail, or unsafe interactions. Your baseline should also test whether the experience supports transparency, reliability, privacy, and feedback.

If the pack relies mostly on vendor material or one internal viewpoint, it is not ready.

Step 2. Turn unknowns into written risk signals.

Treat unresolved legal, finance, and operations questions as explicit unknowns from day one. Create a short note for each target market with open questions, current assumptions, and owners for follow-up.

Keep this written and versioned, not verbal. If the team cannot show what is known versus unknown for each journey sequence, the design is still underdefined.

Step 3. Assign owners and create a shared journey dictionary.

Set ownership before architecture decisions harden. At minimum, assign owners for product decisions, risk review, and operations follow-through. Without that, decision rights drift and reconciliation language starts to diverge.

Pair those owners with a shared dictionary for journey states across the seven sequences, from search through post-move feedback. The point is simple: one meaning per state across teams.

Step 4. Write vendor non-negotiables before taking sales calls.

Define your vetting criteria before vendor conversations start. Feature-led selection can hide operational gaps until late in the process.

Use a pre-call checklist, and make sure your team can answer four core implementation questions before committing to tooling. Ask vendors for concrete evidence that their solution supports the mapped rental journey, addresses listing quality gaps, and supports transparency, reliability, privacy, and feedback. That keeps selection based on operability, not demo quality.

For recurring billing architecture trade-offs, see How to Build a Subscription Billing Engine for Your B2B Platform: Architecture and Trade-Offs.

Choose payment rails by market reality not feature demos#

Choose rails based on observed payment behavior in each target market and on how your team handles failures, not on the smoothest demo flow. If your evidence pack indicates bank-transfer-dominant behavior, prioritize bank-transfer rails and account validation first. If your evidence pack indicates high card usage, prioritize card controls, evidence retention, and dispute operations before you scale.

Step 1. Build a per-market rail matrix from observed behavior.

Make this decision market by market, not once for the whole product. Start with observed renter and landlord behavior from your evidence pack, then test each rail against operating reality.

Compare each candidate rail on habit fit, status visibility, likely failure points, exception ownership, and reconciliation difficulty. The goal is to pick the rail that creates the fewest high-cost surprises for users and operations.

| Rail option | What to verify in each market | Main failure mode to model | Ops burden to confirm before launch |

|---|---|---|---|

| ACH or local bank debit | Whether renters expect account-based recurring payments | Possible NSF returns, incorrect account details, delayed status changes | Account validation coverage, return/reversal event mapping, payout hold rules |

| Card | Whether renters will use cards for rent and landlords accept dispute exposure | Possible disputes, expired cards, retry-driven duplicates | Card controls, dispute evidence handling, retry logic, payout release timing |

| Local bank transfer alternative | Whether renters already trust a local transfer method and include usable references | Possible unmatched deposits, incomplete remittance, manual posting errors | Reference handling, exception queue design, reconciliation to provider reports |

Checkpoint. Finance ops should be able to walk one successful payment and one failure scenario for each rail, naming every record from initiation through return, reversal, or payout block.

Step 2. Pick the first rail by failure economics, not conversion hopes.

Your first rail should be the one your team can explain, reconcile, and support under stress. Keep ACH and cards in the same decision frame, then choose based on actual payment behavior and operational readiness.

If bank-transfer behavior is dominant, invest early in account validation, returned-payment handling, and clear internal states for pending, returned, and released funds. If cards are central in a segment, treat cards as both a product decision and an operations decision. Document dispute handling, evidence retention, retry policy, and payout rules when reversal risk is still open.

Do not accept optimization claims you cannot audit. Research on rental proptech platforms warns that fragmented, uneven data topologies can produce unequal outcomes when platforms automate ordering and judgments. Require clarity on inputs, exceptions, and appeal paths.

Step 3. Stress-test "fast launch" claims against your obligations.

Payments-as-a-service is often presented as a fast launch path, but that does not tell you who owns support, reconciliation, or compliance accountability. Validate claims with evidence, not slides. PropTech research also warns that many firms fail and money is lost, so treat "fast launch" as a hypothesis to test, not proof of operational readiness.

Pressure-test three points before committing:

- Who owns onboarding and exception support in practice.

- Whether real event payloads exist for success, returns, reversals, payout failures, and retries.

- Which compliance obligations remain on your side after integration.

Then run one end-to-end failure scenario for each rail, including request, webhook sequence, retry behavior, and final report entry. If only the happy path is demonstrated, launch risk is still unresolved.

For broader PropTech bundles, keep payment integration decisions separate from pricing or revenue tooling decisions. In the U.S. case filed on January 7, 2025, a proposed Final Judgment was filed on December 23, 2025. The judgment bars use of revenue-management software that relies on competitively sensitive data and requires an antitrust compliance policy. A clean payments integration does not remove adjacent antitrust exposure.

Working rule. Launch the rail your market already uses and your team can operate with clear evidence. Reject any "fast launch" path that leaves compliance ownership or exception handling undefined.

For a deeper dive, read How Accommodation Rental Platforms Pay Hosts: Payout Architecture for Short-Term Rental Marketplaces.

Define the money model before building tenant or landlord UX#

Lock the money model before you design tenant or landlord UX. In PropTech, the payment layer sits between resident-facing flows and core accounting, and ambiguity here tends to reappear later as operating and reconciliation friction.

| Step | What to define | Control objective |

|---|---|---|

| Declare the ledger as the money source of truth | Use one internal ledger as the place that determines financial truth | Trace one successful and one failed payment path using internal records alone |

| Separate lifecycle status from funds availability | Keep payment lifecycle status separate from funds availability | Avoid treating every positive provider update as money ready to move |

| Define event contracts before webhook consumption | Write the event contract before integrating webhooks | The same event replay should resolve to the same internal result or a clear no-op |

| Require deterministic mappings plus an audit trail | Define and version the mapping between each external provider status and internal status | Mapping clarity and auditability |

Step 1. Declare the ledger as the money source of truth.

Use one internal ledger as the place that determines financial truth, then design screens from that model. Document your own object set and state definitions explicitly before launch.

Your state names are an implementation choice, but the control objective is traceability. Teams should be able to trace one successful and one failed payment path using internal records alone. If outcome interpretation depends on provider dashboards, the model is still incomplete.

Step 2. Separate lifecycle status from funds availability.

Keep payment lifecycle status separate from funds availability so your operations team does not treat every positive provider update as money ready to move. Exact internal funds states and provider-label mappings are implementation-specific and should be documented by your team.

This separation matters more as rental platforms digitize more of the tenant-landlord lifecycle. Hidden state logic can get expensive once product, support, and finance all operate on the same flow.

Step 3. Define event contracts before webhook consumption.

Write the event contract before you integrate webhooks so retries and replays do not create inconsistent internal outcomes. Define signature verification, retry schedules, replay windows, and exact mapping formats as part of your implementation design work.

Idempotency details are implementation-specific. The control objective is simple: the same event replay should resolve to the same internal result or a clear no-op.

Step 4. Require deterministic mappings plus an audit trail.

Treat mapping clarity and auditability as launch requirements. The exact deterministic mapping between each external provider status and internal status is not specified in the sources, so define and version your own mapping with an audit trail. That lowers the risk that fragmented processing paths drive inconsistent or unfair outcomes, a known risk in automated rental platform environments.

Do not make this a one-time exercise. Repeat the same happy-path and failure-path walkthrough whenever you add a provider, change payout logic, or adjust landlord-facing flows. Keep that discipline consistent with the stack-review approach highlighted in the PropTech guide (pp. 156-158).

Related: How to Build a Platform for the Creator Economy: Payment Architecture for 1-to-Many Monetization.

Design compliance gates and onboarding in the actual payment flow#

Once your ledger states are defined, put compliance checks on the money path itself. In PropTech, onboarding often breaks when verification is treated as a separate front-door task and the gap appears only when someone expects a payout.

| Step | Policy decision | Required record or rule |

|---|---|---|

| Place verification at the first irreversible money action | Decide which verification checks should happen before the first irreversible money action that creates payout exposure | Store the current verification state, who or what set it, when it was set, and which actions remain blocked |

| Define onboarding depth by risk | Document which account types can list, accept funds, and receive payouts | If policy references a rule, keep the official PDF and version date in your internal evidence trail |

| Block risky actions until verification is complete and logged | Use explicit gate results: allowed, blocked, allowed by approved exception | If exceptions are granted, log the approver, reason, timestamp, and supporting record |

| Tune sequence when conversion drops, not control quality | Adjust sequence, timing, and explanation before weakening controls | Redesign the path when friction appears, but keep the control and document why it exists |

Step 1. Place verification at the first irreversible money action.

Decide which verification checks, for example identity and payout-account checks, should happen before the first irreversible money action that creates payout exposure. The exact sequence is your design choice, but the control objective should be explicit. Unresolved verification details should not surface for the first time when money is ready to move.

This is about failure timing, not adding friction for its own sake. If verification gaps appear only at payout time, funds movement delays, support burden, and trust risk can rise together.

Verification checkpoint. For each payout-eligible account, store the current verification state, who or what set it, when it was set, and which actions remain blocked until it changes. If status must be inferred from a provider dashboard, the gate is likely too loose.

Step 2. Define onboarding depth by risk, then document where light onboarding stops.

Define in writing which account types can list, which can accept funds, and which can receive payouts. That boundary is your real onboarding policy. "Light onboarding" on its own is not a policy.

Where legal interpretation matters, validate against official editions. FederalRegister.gov states that it is not an official legal edition and directs legal research users to verify against official editions. Entries also link to official PDFs on govinfo.gov. If your policy references a rule, keep the official PDF and version date in your internal evidence trail.

Step 3. Block risky actions until verification is complete and logged.

Block high-risk actions until your internally required verification states are complete and recorded. Keep the gate result explicit and auditable:

- allowed

- blocked

- allowed by approved exception

If exceptions are granted, log the approver, reason, timestamp, and supporting record. Hidden product logic is not a policy artifact. For sensitive automated decisions, define an explicit compliance policy.

Step 4. Tune sequence when conversion drops, not control quality.

If onboarding drop-off appears in a segment, adjust sequence, timing, and explanation before weakening controls. You can change when checks appear and how users are guided without changing the underlying gate.

Avoid reducing review quality for harder segments based on thin behavioral signals. Research on data-driven renter classification warns that these systems can exclude and invisibilize people, creating both fairness and operational risk. The practical rule is simple: redesign the path when friction appears, but keep the control and document why it exists.

For ledger design, reconciliation, and auditability, see How to Build a Deterministic Ledger for a Payment Platform.

Decide what to automate and what needs human review#

Draw the line explicitly. Automate only decisions your system can explain end to end, and require human review wherever judgment or ambiguity enters the flow. In rent-platform operations, a major risk is hidden discretion in scripts and operational workflows that can quietly change how renters are ordered, judged, or excluded.

That caution is supported by research on rental proptech platforms, though one source is UK-specific and should be read in context. It describes automated judgments, broad data use, and rules shaped by assumptions about an "ideal" tenant. Related work describes renter data becoming operational metrics and recursive feedback loops that can harden exclusion. Treat that as a design warning. Your automation boundary should be explicit, reviewable, and auditable.

Step 1. Automate only deterministic paths your ledger can reconstruct.

Automate a path only when one event maps to one valid internal state with no policy conflict. For each automated action, keep enough internal evidence to reconstruct why it happened, including the event reference, affected record, resulting state, timestamp, and rule version. If your team has to infer what happened from external dashboards or partial signals, route that case to review instead of auto-processing.

Step 2. Model discretionary decisions as formal product policy.

Document every override point where a person can change the default outcome. For each point, define who can decide, what evidence is required, what evidence is out of scope, and what record must be left behind. This keeps exceptional handling from becoming invisible policy and reduces the chance that uneven data or subjective assumptions drive outcomes.

Step 3. Review automation boundaries on a schedule, not only after incidents.

Automation rules drift as product goals, data inputs, or funding pressure change. Run recurring checks on both automated and manually reviewed outcomes to confirm that your boundary still matches your stated policy and risk posture. When you find drift, update the rule and the review criteria together so operations stays consistent and explainable.

Build integration reliability into day-one architecture#

Treat reliability as a design requirement, not cleanup work after launch. Property-management operations are described as growing in scale and complexity, and the February 2026 PropTech study also warns that tools can miss frontline operator needs. Your integration design should hold up in real operating conditions, not just in a clean demo flow.

Step 1. Make retried money calls resolve to one clear outcome.

Assume requests can be repeated and delayed, then design payment and ledger flows so a retry can be matched to prior intent instead of creating a second action. Where your provider or internal APIs support replay-protection patterns, such as idempotency controls, apply them consistently and store enough request history to explain what happened.

The check is simple. If the same request is replayed after a timeout, aim for one economic result and an audit trail your finance team can follow.

Step 2. Process asynchronous provider signals as delayed updates.

Treat webhook-style events as useful but delayed signals, and design processing so latency in one stage does not create avoidable confusion in another.

The practical goal is recoverability. Failed processing should be traceable and re-runnable with the original event context intact.

Step 3. Reconcile provider records and internal ledger states with a documented operating rhythm.

Use a documented reconciliation rhythm that fits your operating load, and compare both detailed records and rolled-up totals. This helps catch missing entries, duplicates, and state drift before they become support or finance escalations.

Do not stop at a surface match. Your team should be able to identify what is unmatched on each side and what status each record currently shows.

Step 4. Pressure-test failure paths before broad rollout.

Before broad rollout, run a failure-path rehearsal that includes retries, delayed asynchronous updates, and reconciliation where those behaviors apply to your stack. Base release confidence on whether the flow remains explainable under stress, not just on happy-path calls succeeding.

If your team cannot walk the sequence from request to final ledger state without guesswork, the integration may still be misaligned with real PropTech operating needs.

For a step-by-step walkthrough, see Earned Wage Access Architecture: How to Build EWA Into Your Gig Platform.

Roll out in phases with explicit go and no-go gates#

Phased rollout only works when each phase has a real go or no-go decision based on operating evidence, not growth pressure. The point is not to move slowly. It is to expose failure modes while they are still small enough to control.

Step 1. Pilot a narrow operating slice.

Start with a tightly scoped live slice so your team can trace one full path from pay-in to payout and ledger state without extra variation.

Your go signal is operational clarity. You can reconcile on a fixed rhythm, explain unmatched items, and resolve delayed or duplicate provider updates to one clear internal outcome. Keep monitoring hands-on in this phase so ambiguous exceptions are identified and owned early.

Step 2. Expand only after exception handling is repeatable.

Add payout complexity only after exception handling is stable and repeatable. Use a simple gate: recurring exception types have clear owners and standard resolution paths, and finance does not need custom investigation for routine cases.

If exceptions are aging, reopening, or escalating to ad hoc senior judgment, treat that as no-go.

Where automation is involved, separate payment-scale decisions from screening-scale decisions. Research in rental PropTech highlights risks from automated judgments, including formulaic tenant rejections and unequal outcomes when decisions rely on historically uneven data.

Step 3. Localize market controls without rewriting core ledger logic.

As you expand across markets, keep core ledger logic stable. Localize controls around it, for example legal checks and operating evidence packs.

For U.S. legal checkpoints, do not rely on a FederalRegister.gov page alone for compliance conclusions. Verify against the official Federal Register edition on govinfo.

A concrete checkpoint example is the 01/21/2026 notice (2026-01009, 91 FR 2592) on the proposed final judgment and competitive impact statement in United States of America et al. v. RealPage, Inc. et al. The notice includes a 60-day public comment window and is proposed, not a final adjudicated outcome.

Step 4. Pause expansion when queues outrun resolution capacity.

Use a clear no-go signal. If exception queues continue growing relative to your team's resolution capacity, pause expansion. Do not add markets, segments, or payout paths until backlog age and explainability return to control.

Keep your phase packet simple and auditable:

- Reconciliation output with unmatched items clearly listed

- Exception aging trend showing whether backlog is shrinking or growing

- Audit-trail samples for a normal flow, a delayed update, and a return/reversal

- Market-specific legal and operations sign-off notes

Handle the common failure modes before they become incidents#

Treat failure handling as a launch requirement. In rental PropTech, work is often fragmented across multiple tools, commonly 5 to 7, and platforms mediate critical landlord-tenant operations. This combination can blur financial visibility and raise reconciliation and oversight risk when records drift across systems.

Step 1. Name the predictable breaks before launch.

Document the failure modes your team expects to see in live operation, including:

- delayed or missing handoffs between tools

- inconsistent records across systems

- exceptions caused by uneven data inputs

- payout and ledger states that no longer match

Keep this list explicit and reviewable so these cases are handled as known operating paths, not ad hoc exceptions.

Step 2. Define accountability and review paths for each failure mode.

For each failure mode, decide in advance who reviews it, how the corrected state is verified, and what records are retained so someone outside the incident can reconstruct what happened and why the final state is correct.

Step 3. Keep business-critical rent flows on rails with durable records.

Because fragmented operations can limit financial visibility, keep core rent collection and payout flows in processes that support reliable review and reconciliation. If a flow cannot be consistently reviewed and reconciled at close, treat it as higher risk before placing it on the business-critical path.

Use a market expansion scorecard before committing GTM budget#

Do not commit GTM budget until a pilot clears a documented scorecard for rail fit, compliance complexity, and operational execution, with records your team can reconstruct. This is where market ambition has to meet operating proof.

Step 1. Score market fit with evidence.

Judge fit on evidence, not market-size narratives.

| Scorecard area | What to judge | Evidence to require |

|---|---|---|

| Rail fit | Whether your current pay-in and payout path can support the market path you need | Provider documentation, pilot transaction logs, settlement and payout records |

| Compliance complexity | How much onboarding depth, ID verification, and policy review the market adds | Onboarding requirements, blocked-action rules, reviewed compliance notes |

| Operational readiness | Whether finance ops and support can run expected exceptions | Exception samples, owner assignments, closure notes, audit-trail records |

Keep the portfolio-fit lens explicit. As the PropTech stack framing suggests, tooling is not one-size-fits-all. A market is a weak candidate when it forces controls or systems that do not fit your operating model.

Step 2. Add an execution score from pilot operations.

Score API integration maturity and event-handling behavior from live pilot operations, not sandbox demos.

Use concrete checks. Repeated requests should not create duplicate payouts or duplicate internal records, and delayed or replayed events should still resolve to one correct internal outcome. If the event trail is not clear, the execution score is not ready.

Step 3. Set an explicit go/no-go gate before spend approval.

Define the decision rule before GTM planning. Expand only when the pilot meets your minimum score and the review package is complete.

Include a legal checkpoint for pricing-adjacent tooling or landlord data sharing. In the LivCor matter, the DOJ complaint filed on January 7, 2025 and the proposed Final Judgment filed on December 23, 2025 highlight antitrust risk around competitively sensitive information, including proposed limits on certain revenue-management software use and data sharing.

If you are planning the operating model around this architecture, see How to Build a Compliance Operations Team for a Scaling Payment Platform.

Before you approve expansion, pressure-test your idempotency, webhook, and reconciliation assumptions against the integration references in the Gruv docs.

Final takeaway and copy-paste launch checklist#

Use this as a launch gate. If any item below lacks a named owner and a written artifact, pause expansion.

- We selected target users and markets based on repeat-use fit, not top-line demand alone.

A rollout risk is building for a one-time user group. Confirm landlord and tenant onboarding and verification needs are covered before expansion.

- We documented stack direction with written answers to four stack-selection questions before committing tools.

Payment architecture choices sit inside a broader PropTech stack, and PropTech explicitly overlaps with FinTech.

- We placed onboarding controls in the payment flow, including ID verification and bank account validation where supported.

Design these controls into onboarding from the start, rather than adding them after launch.

- We reviewed failure paths and downside risk before launch.

Do not validate on happy paths alone. In PropTech, firm failure and capital loss are real outcomes for part of the field.

- We treated fast deployment timelines as vendor claims, not readiness proof.

Claims like "less than 2 weeks" can describe integration speed, but they are not proof that controls and support operations are production-ready.

- We paused expansion until user-group fit and stack decisions were explicit in writing.

Keep written answers to your four stack-selection questions visible as you scale.

Related reading: How to Build a Finance Tech Stack for a Payment Platform: Accounts Payable, Billing, Treasury, and Reporting.

If you want a market-by-market read on payout controls and operational fit for your rollout plan, talk to Gruv.

Frequently Asked Questions

What is the minimum viable payment architecture for a rent collection marketplace?

Treat "minimum viable" as the smallest setup your team can operate and explain. A practical interpretation is a clear pay-in path, a controlled payout path, and records that let finance trace each payment outcome. If your team cannot reconstruct what happened from the audit trail, the setup is not ready.

How should we choose between ACH, cards, and other rails for each country?

The material here does not support a universal country-by-country rule, so avoid generic defaults. Choose rails from your own observed payment behavior and pilot evidence, then prioritize options your team can reconcile when failures occur. If a rail looks clean in demos but produces unclear outcomes in live logs, treat it as a weak fit.

What should be fully automated versus manually reviewed by operations?

Automate repeatable, low-judgment paths, and require human review when records conflict or outcomes materially affect renters or landlords. The evidence warns that fragmented data and automated judgments can produce uneven outcomes, especially when systems begin to score or sort people for operational efficiency. Require a named reviewer and a written reason for conflicting records or payout-impacting overrides.

Which controls are non-negotiable before launching landlord payouts?

A practical baseline for landlord payout controls includes transparency, reliability, privacy, and feedback, plus clear handling of fragmented records and automated decisions. If payout outcomes cannot be explained from records and documented actions, treat launch readiness as incomplete.

What usually breaks during migration from manual rent collection to digital flows?

A common break is fragmented records. Landlord finance workflows often already span 5 to 7 tools, so digital rollout can add status confusion unless you define a single source record. Another common break is hidden manual judgment becoming automation on weak inputs, which the evidence links to uneven outcomes.

How do we know our reconciliation and audit trail are strong enough to scale?

A practical bar is whether finance can trace any payment outcome through system records, operator actions, and final resolution. The rental-platform evidence supports this emphasis on transparency, reliability, privacy, and feedback across the full renter journey. If unmatched items linger or overrides are unexplained, you are not ready to scale.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- federalregister.gov/documents/2026/01/21/2026-01009/united-state...trusted

- federalregister.gov/documents/2025/09/05/2025-17086/united-state...trusted

- govinfo.gov/content/pkg/FR-2026-01-21/pdf/2026-01009.pdftrusted

- sbs.ox.ac.uk/sites/default/files/2018-07/PropTech3.0.pdftrusted

- scholarworks.law.ubalt.edu/cgi/viewcontent.cgitrusted

- alpaca.vc/2023/08/landlord-technology-solutions-facili...external

- appinventiv.com/blog/real-estate-chatbotexternal

- californialawreview.org/print/a-home-for-digital-equityexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: