Quick Answer

Define monetization obligations before choosing rails, then gate expansion country by country. Use a Market-Readiness Scorecard with a documented low/medium/high friction rating, require one traceable payout test path to final status, and keep a fallback route for late returns or missing confirmations. Build launch decisions around evidence: named owners, hold-and-release behavior, and explicit unknowns marked as TBD. For build platform creator economy payment architecture 1-to-many monetization, this sequence keeps go/no-go calls tied to operating proof instead of TAM or audience momentum.

Why Creator Platforms Need 1-to-Many Payment Architecture#

If you want to build platform creator economy payment architecture 1-to-many monetization, start with payment resilience, not a feature list. Your first decision is whether the design can hold up under real operating pressure in the markets you plan to enter.

The creator economy is often described as a global industry, not a niche trend. One cited source puts it at more than $250 billion today and forecasts more than $480 billion by 2027. Treat that as market context, not proof that a launch is operationally ready.

When you combine multiple monetization streams, payments stop being a back-office detail. Secure transaction handling becomes the foundation, and that foundation has to hold as your platform changes.

Before you start. Assume demand will be uneven. Creator businesses can be exposed to concentration risk when they rely too heavily on one algorithm, and some segments face payment bans, chargebacks, content takedowns, and platform fees at 20% or higher. Your payment model should reduce those pressures, not reproduce them.

Separate audience proof from payment readiness early. A documented YouTube snapshot from 1 November 2024 shows one channel with 396 videos, more than 42 million views, and 285,000 subscribers. That kind of reach can show demand, but it does not confirm that your payout operations are ready.

Follow this sequence.

- Define monetization obligations. Write down who gets paid, when, and why for each revenue event.

- Set market-readiness criteria. If you plan a multi-country rollout, make explicit go or no-go decisions using your own operating signals, not surface demand.

- Map the 1-to-many money flow. Trace the path from customer charge to allocation, payout trigger, and final status.

- Validate controls before launch. Test edge cases first, including retries, disputes, and post-sale adjustments.

The rest of this guide follows that sequence so you can make hard launch calls while changes are still cheap.

Prepare the inputs before you design anything#

Do this work first. If scope and operating constraints are fuzzy, architecture decisions drift toward copied features instead of your actual operating model.

| Input | What to capture | Key note |

|---|---|---|

| One-page scope | Target creator segment, launch scope, and v1 monetization model | State the unit you monetize |

| Operating input pack | Core operating-model assumptions and launch-critical dependencies | Keep known unknowns visible as TBDs |

| Non-negotiables | Controls and payout capabilities that are mandatory at launch versus optional for v1 | Define before vendor conversations |

| v1 acceptance criteria | What "ready" means for operations, reconciliation, and payout outcomes | Keep in the same scope document |

Start with a one-page scope. Define your target creator segment, launch scope, and v1 monetization model. State the unit you monetize, because that choice changes payout and policy assumptions. Different monetization units do not create the same downstream requirements.

Use this checkpoint. Someone outside your team should be able to read the page and clearly answer who pays, who gets paid, and what the platform is optimized for.

Build a first-pass operating input pack. Start with operating inputs, not TAM slides. Capture core operating-model assumptions and launch-critical dependencies, and keep known unknowns visible as TBDs.

Treat this pack as an unknowns detector, not an expansion pitch. If a launch-critical requirement is still TBD, pause design for that scope.

Define non-negotiables before vendor conversations. Document which controls and payout capabilities are mandatory at launch versus optional for v1. This narrows the field quickly and keeps tradeoffs explicit.

Set v1 acceptance criteria in plain language. Agree on what "ready" means for operations, reconciliation, and payout outcomes. Put those criteria in the same scope document so product, payments, support, and finance evaluate launch readiness against one standard.

With those inputs in place, you can define what the platform actually owes before you choose how money moves.

For a step-by-step walkthrough, see Earned Wage Access Architecture: How to Build EWA Into Your Gig Platform.

Define monetization obligations before you pick rails#

Define the obligation first, then choose rails that can execute it. That order keeps your payment architecture aligned to what your product promises, instead of whatever a vendor happens to support by default.

Name each monetization event in plain language. Start with the unit of value: what is sold or billed. If the unit is unclear, billing decisions will be unclear too.

| Monetization line | Unit of value to define | Who pays | Amount basis to document |

|---|---|---|---|

| Subscription tiers | Recurring access or service tier | Customer | Tier price and billing cadence |

| Direct billing | Direct user billing event | Customer | Published price or defined price rule |

| Usage-based pricing | Measured consumption or actions | Customer | Usage metric and calculation rule |

| Pay-per-outcome | Defined completed outcome | Customer | Outcome trigger and price rule |

| Marketplace integration | Platform-mediated transaction | Depends on marketplace model | Marketplace fee and transaction basis |

Quick check: for one sample event per line, a reviewer should be able to answer what happened, who pays, what the amount is based on, and whether an amount is due.

Turn each event into a short obligation record your billing logic can enforce.

For each event type, document:

- trigger condition

- amount basis (fixed, tiered, usage-based, or outcome-based)

- who pays

- expected billing timing

- reversal or adjustment conditions

Use exact wording so product, support, and finance interpret the event the same way.

Keep revenue-capture models separate when they behave differently. Define subscription, usage-based, pay-per-outcome, and marketplace patterns explicitly instead of blending them into one vague rule set.

This matters in practice. Model choice affects behavior, observability, billing logic, API limits, uptime, and profitability. If any line depends on measured consumption, set usage tracking instrumentation before launch so billing stays auditable, and track accuracy so manual overrides stay limited.

Treat timing as part of the obligation. Do not leave it as a rail choice for later. Document when billing should occur for each event and what timing expectations apply.

Before you choose rails, validate the obligation set with a small evidence pack: pricing terms, fee policy, sample event payloads, and one worked example per monetization line. If those artifacts conflict, the obligations are not ready yet.

Related: A guide to 'Network Effects' for community-based products.

Score market readiness by country before committing GTM#

Prioritize countries where you can meet onboarding and payout obligations with sustainable operations. If compliance feasibility or payout reliability is not credible, defer launch even when demand looks strong.

The previous section defined what you owe. This section decides where you can deliver those obligations with acceptable risk.

Build a country-by-country Market-Readiness Scorecard before you rank by TAM. Use one row per country and the same columns each time.

| Scorecard column | What to check | Why it matters |

|---|---|---|

| Compliance burden | Whether your model requires identity checks, eligibility checks, centralized resolution controls, or added review before payout | Withdrawal or cash-out capability adds a compliance stack, not just a product toggle |

| Operational integrity readiness | Whether accounting, resolution, anti-manipulation, and liquidity operations are defined for this market | Reliability depends on operational integrity, not demand alone |

| Payout path reliability | Whether payout routes are available and whether a fallback path exists | Inaccurate or late payouts are a real business risk |

| Expected support load | Likely onboarding questions, payout-status follow-ups, and exception-handling volume | Creator platforms often operate a long-tail workforce with small, frequent payments that strain legacy finance operations |

| Dispute and reversal handling | How exceptions could affect adjustments or payout timing | Unclear exception handling increases support pressure and payout risk |

| Timing reliability | Any requirement that changes onboarding flow or payout release timing | Timing breakdowns raise the risk of late or inaccurate payouts |

If you support withdrawals, cash prizes, or redemption, score that model separately from non-withdrawable value models. A no-cash, no-redemption model can reduce licensing burden, while payout-enabled models increase compliance and operational scope.

Use compliance feasibility as the first real gate. The practical question is whether you can onboard the right entities, run required checks, and release payouts without creating a manual back office you cannot sustain.

Use a simple friction scale of low, medium, or high, and record the reasons in writing. Require a small evidence pack before you green-light a country:

- one sample creator onboarding path

- one sample onboarding path for entities you expect to pay, if applicable

- expected payout release conditions

- known hold or review scenarios

- named compliance owner

If that pack is missing, treat the country as not launch-ready.

Do not confuse payout coverage with payout reliability. A country can be "supported" and still be a poor first-wave launch if payout outcomes are hard to predict or exceptions are slow to resolve.

Require at least one traceable test path from payout creation to final status, plus a documented fallback path. If ownership for late returns or missing confirmations is unclear, reliability is not good enough yet.

Add the legal and operational friction that will drive day-to-day support load. Then rank countries by launch fit rather than demand alone. Where countries are close, prefer the one with cleaner payout execution and lower manual review pressure.

Use a hard rule for wave inclusion:

- Compliance feasibility is credible for your monetization model.

- Payout reliability supports accurate, on-time payouts without unsustainable manual effort.

If either fails, defer launch.

For monetization model tradeoffs, see Choosing Creator Platform Monetization Models for Real-World Operations.

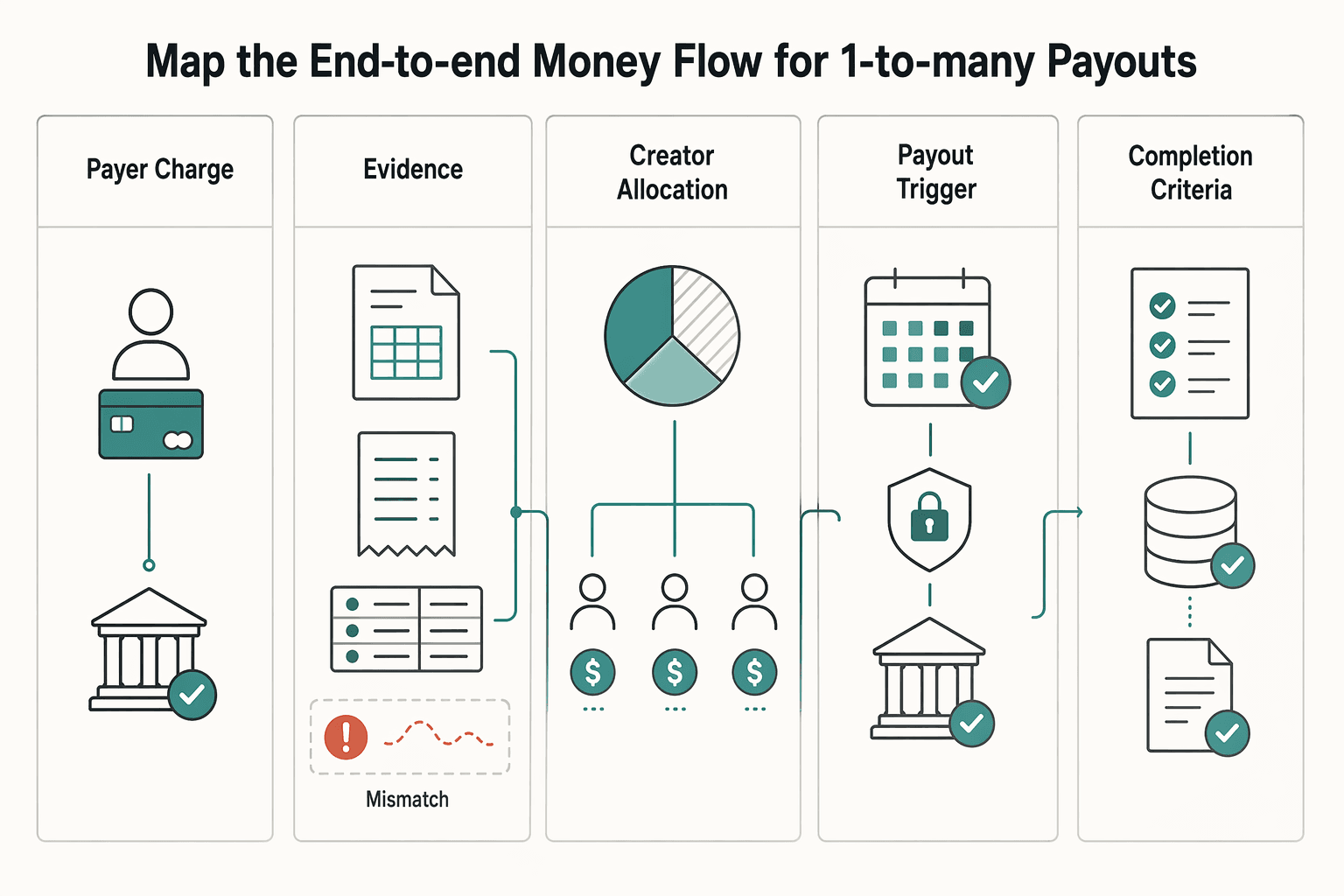

Map the end-to-end money flow for 1-to-many payouts#

Treat this as a launch gate. If your team cannot explain the full money path end to end, your payment architecture is likely not ready.

| Checkpoint | What to define | Control note |

|---|---|---|

| Payer charge | Include it in one continuous flow | Show every handoff where value or liability changes |

| Internal financial record | Include it in one continuous flow | Tie payout statuses back to internal financial records |

| Creator allocation | Mark it separately | Do not hide allocation logic inside a generic processing box |

| Payout trigger | Make the checkpoint explicit | Use a stable internal reference at payout-creation boundaries |

| Completion criteria | Make the checkpoint explicit | Resolve unclear ownership before you add payout complexity |

Draw one continuous flow that combines product and finance. Do not keep separate views. In platform models, value moves in multiple directions between payer, creator, and platform, so your map should show every handoff where value or liability changes.

For your proposed design, define checkpoints such as payer charge, internal financial record, creator allocation, payout trigger, and completion criteria. The exact payout state machine depends on your implementation, so make your chosen checkpoints explicit. If ownership is unclear at any checkpoint, resolve that before you add payout complexity.

Make 1-to-Many Monetization decisions explicit in the diagram. Mark separately where Payout Orchestration runs. Do not hide allocation logic inside a generic processing box.

Keeping allocation and payout stages distinct makes post-sale adjustments easier to reason about. Your team should be able to see where changes apply when balances move after the initial allocation.

Add control points for stale states, retries, and duplicate-risk handling before implementation. At each retry boundary, define what prior record should exist before another attempt is allowed.

Use a stable internal reference, such as an idempotency-style request key, at payout-creation boundaries so you can check retries against prior attempts instead of reissuing them blindly.

Set a verification requirement for payout statuses where possible. Status labels that live only in an external dashboard may be insufficient for operational control unless they can be tied back to internal financial records.

This is where API-first design matters. Front-end states such as pending, paid, or failed should align with event-level records in your financial systems so financial governance can hold as payout complexity grows.

For the ledger side of this architecture, see How to Build a Deterministic Ledger for a Payment Platform.

Design the split engine and sub-ledgers so audits are easy#

Make split outcomes explainable from records you already hold. If your team cannot trace a balance change through the method and version used at the time, audit review gets harder.

Start with split determinism. Define and document your own inputs and precedence, then retain version history so historical outcomes can be replayed consistently.

Avoid hidden mutation across profile, policy, or product fields. At minimum, make method changes explicit so older transactions are interpreted in their original context.

Keep balance states and movement history easy to review. A single blended total may be easier in the product UI, but internal review still needs clear state definitions. The provided excerpts do not prescribe one required sub-ledger pattern.

Use explicit change history rather than silent overwrites where your system allows it. For each movement, retain enough context for reconstruction, including what changed, when it changed, and which rule version or operator action applied.

Decide reversal handling before launch, including how refunds and chargebacks are applied in your own policy. The goal is consistency and clear ownership, not policy complexity.

Set reversal testing and exception governance based on your internal risk tolerance.

Document your split methodology as an operating artifact, not just code behavior. The IAB report published in April 2025 explicitly includes a "Detailed Methodology for The Creator Economy Estimates" section on page 146. Use that level of transparency internally.

That matters even more when market conditions vary. Research published online on 30 March 2026 highlights cross-national variation in regulatory approaches, increasing institutional hybridization, and an ongoing debate over how far platform regulation should go. The same article says no underlying dataset was used, so treat it as policy context rather than an empirical payments-operations blueprint.

Set compliance and tax gates at the action level#

Once your ledger states are clear, gate the money-moving actions themselves. Earning can stay active while payout actions remain restricted until defined compliance or tax checks are complete.

Map checks to actions, not to one broad account status. Treating "verified" as a permanent yes or no across your payment architecture can hide differences in risk and reporting exposure.

Attach decision points to each action that moves or reroutes funds, and document a clear owner and outcome for each gate. A practical baseline is one policy table that answers four questions per action: what is attempted, what check applies, what can still proceed if incomplete, and what status appears in the ledger and payout flow while it is pending.

Define failure outcomes before launch so blockers are explicit, not silent. If a check fails or remains incomplete, show a specific operational state instead of a vague pending label.

Keep the block as narrow as possible so commercial state and compliance state stay aligned. Then test these paths at scale across support, finance, and operations views before you lock policy. Locking policy before you test it at scale is a known failure pattern.

Give tax-sensitive actions their own decision path. Tax blockers discovered only at payout time can create avoidable operational risk. Exact trigger rules, jurisdiction requirements, and hold timing are policy-specific and should be treated as unknown until defined.

For each blocked action, keep an evidence pack with the trigger event, affected action, unresolved dependency, owner, and next allowed action. Treat this as a versioned governance artifact that remains reviewable and explainable.

Expose holds so support and finance can explain them from one screen. Support should see gate type, triggering action, open time, owner, requested remediation, and scope of impact. Finance should see the linked ledger state and payout state.

If teams cannot explain a hold quickly, creators can end up in repeated tickets and workarounds. In a multi-platform environment where creators spread activity to stabilize income, opaque holds can increase switching risk.

For training and readiness, see How to Build a Payment Compliance Training Program for Your Platform Operations Team.

Choose rails and settlement strategy for your first launch wave#

Once funds are eligible to move, keep your first launch wave narrow. Start with the payout rail your team can trace, explain, and recover when it fails, then add Instant Payouts only where expectations, coverage, and economics are already validated.

Anchor v1 on the rail with the clearest operational story. The launch test is simple: support and finance should be able to explain each payout status and the next action from one view.

| Option | Best use in first wave | Verification checkpoint | Main red flag |

|---|---|---|---|

| Primary payout rail | Default method for broad launch coverage | Each payout maps cleanly from ledger event to payout attempt to final outcome | Long-lived generic statuses with no practical reason |

| Instant Payouts | Selective add-on where faster access is a clear need | Coverage, fee impact, and downgrade path are documented before launch | Fast route fails and leaves ownership of resolution unclear |

| Experimental crypto-native settlement | Narrow pilot, separate from core payouts | Isolated cohort, explicit operating boundary, and separate monitoring | Experimental path becomes a hidden dependency for general payouts |

Add Instant Payouts only when the tradeoff is explicit. Keep a stable baseline route so you can fall back cleanly if fast-route coverage or exception handling underperforms.

Trust controls are part of that decision, especially for agent-initiated flows. AP2, announced on September 16, 2025, with input from more than 60 organizations, calls out authorization, authenticity, and accountability as core controls. AP2 also warns that autonomous agents can break the old assumption that a human always approves a payment click by click. If your Payment Architecture allows automated payout initiation, confirm who granted authority, how request authenticity is validated, and who owns the audit trail when something goes wrong.

Treat compliance readiness as a launch gate, not a post-launch cleanup. Before expanding rails, confirm your MVP can handle KYC and basic AML end to end.

Keep experimental settlement paths out of the broad launch wave unless the use case is tightly bounded. x402 is presented as a settlement layer for crypto-native payments and cites micropayments as small as $0.01 within 200ms. The same source also describes current concentration around Base, USDC, and Coinbase, with multi-chain support and decentralized facilitation still unresolved.

That does not make x402 unusable. It does mean it should stay in a controlled pilot until your core payout operations are stable and explainable. If settlement variability is likely to confuse creators in a market, reduce launch options first and expand after operating signals are stable.

Related reading: How to Build a Finance Tech Stack for a Payment Platform: Accounts Payable, Billing, Treasury, and Reporting.

Build reconciliation operations before you scale volume#

Build reconciliation before you scale. If your team cannot consistently explain why balances and payout statuses do or do not match, adding markets or payout options only increases operational risk.

| Measure | Figure | Context |

|---|---|---|

| Digital payment penetration | 78% | In 2020 |

| Consumers using two or more digital payment methods | 45% to 58% | Rising in the same period |

| In-app payments | 57% | Most common form in the same period |

| Online payments | 53% | Most common form in the same period |

Digital payment use is broad, and method mix has grown, with 78% penetration in 2020 and consumers using two or more digital payment methods rising from 45% to 58%. In that same period, in-app and online payments were the most common forms (57% and 53%). At the same time, trust can erode when outcomes are unclear, some payment behavior shifts may not be permanent, and many consumers remained unaware of or uninterested in contactless payments. Treat reconciliation readiness as a pre-scale control, not a post-scale cleanup.

Document your reconciliation method early. The sources here do not specify a required daily or month-end workflow design, so set one internal method and keep it explicit as volume grows.

Define exception handling in your own operating model. The sources do not establish required exception categories or evidence-pack templates, so choose a stable internal approach and apply it consistently.

Set ownership and handoffs intentionally. These sources do not prescribe a mandatory team structure or payout-traceability standard. Document responsibilities clearly so unresolved items do not accumulate.

A practical standard is to document your method as explicitly as strong measurement work documents methodology. The IAB report includes a dedicated methodology section for creator-economy estimates. Once that method is stable, scaling becomes an operating decision instead of a judgment call.

For staffing and workflow design at scale, see How to Build a Compliance Operations Team for a Scaling Payment Platform.

Plan failure handling for disputes and payout exceptions#

Plan failure handling before you scale so retries and manual recovery do not create duplicate liabilities. In payout operations, each dispute, refund, and payout failure should follow a defined state path with one consistent balance outcome across creator, support, and finance views.

Use clear state models for disputes, refunds, and payout failures. Tie each state to operator actions and customer-facing messaging. Do not collapse them into one generic exception type.

Keep event intake separate from payout logic, and process recovery through asynchronous handlers. This keeps state transitions clearer during failures and aligns with event-driven implementation guidance. As a practical check, each case should be traceable from records alone: what happened, what balance changed, and what the creator was told.

Make restart paths idempotent and auditable. If a payout retry runs more than once, it should not create a second financial effect.

Use a stable operation key for replayable actions, and make sure retries return the existing accepted outcome unless a real state change occurred. Pair this with automated auditing and reconciliation so each attempt leaves a verifiable trail. Message queues can improve resilience and fault tolerance, but only if duplicate consumption cannot produce duplicate transactions.

If you run an exception queue, order it by operational risk. Prioritize payout-critical and dispute-related failures ahead of cosmetic mismatches so financial exposure is handled before presentation cleanup.

Make dispute management and payment monitoring visible in the same operational flow so teams can quickly distinguish review blockers from delivery failures.

Document disputed-fund handling before live disputes arrive. The priority is consistency. One disputed event should produce one balance story across creator-facing views and finance reporting during investigation.

If customer and finance views diverge during a dispute, trust drops and recovery work gets harder. This is where weak backend handling turns into lost revenue, strained creator relationships, and avoidable technical debt.

Decide what to build and what to buy#

Use a Build vs. Buy matrix before implementation so you only build capabilities that materially shape your platform's value. Platform companies do not need to internalize every capability, and lower barriers to entry increase pressure to focus internal effort where differentiation is real.

Score each capability in one view using four questions. Check integration complexity, governance burden, capability coverage, and speed to market. If you do not compare those tradeoffs side by side, teams can overbuild work that feels strategic but does not change outcomes.

| Capability | Build when | Buy when | Verification checkpoint |

|---|---|---|---|

| Allocation rules logic | Your allocation logic is a core product behavior and changes with your monetization model | Your rules are relatively stable and not a major product differentiator | Run sample sale, refund, and dispute paths and confirm one consistent balance outcome |

| Payout execution | Execution behavior is central to your product promise | You prioritize faster access to established operational coverage | Confirm payout ownership, final-status visibility, and retry behavior are explicit |

| Compliance checks | Decision logic is part of your market or risk strategy | Reviews are mostly standardized and operational | Confirm where decisions, remediation records, and hold/release history are tracked |

| Reconciliation evidence | Finance needs custom evidence tied to your internal views | Standard exports are sufficient for close and audit workflows | Request a failed-case evidence pack before launch |

Treat this as a living decision document, not a one-time workshop artifact.

Build first where ownership is likely to change customer outcomes or risk profile in a meaningful way. Buy first where the capability is necessary but not differentiating. In many platform contexts, that can mean keeping tighter control over monetization logic while using external infrastructure for more standardized operations.

Keep flexibility in mind as you scale. Platforms often need to reconfigure their value proposition to stay competitive, and overbuilding commodity components early can make later changes harder. One common failure mode is staying tied to legacy methods while faster competitors adapt.

Set integration boundaries explicitly before launch and treat them as governance decisions, not assumptions. Define who is accountable for key payout, compliance, and reconciliation actions so exception handling remains clear under load.

Run one tabletop case end to end: payout triggered, held for review, released, then questioned by finance. Then answer three questions clearly: who executed the payout action, who made or recorded the compliance decision, and who can produce the evidence tying ledger event, payout status, and support explanation together?

If ownership is overlapping or unclear, resolve it before go-live. For a deeper comparison, see Payments Infrastructure for Creator Platforms: A Complete Build vs. Buy Guide.

For an adjacent example, read How to Build a Rent Collection Platform: Payment Architecture for PropTech Marketplaces.

If your build-vs-buy matrix favors outsourcing rail execution while keeping your own allocation logic, review Gruv Payouts to pressure-test operational fit.

Make the launch decision and copy-paste checklist#

Use one rule for go or no-go: launch only when your own readiness checklist, policy-gated dependencies, and release evidence all pass together. If any one is still based on assumption, treat launch as no-go.

Demand signal alone is not enough. One example in the material is a policy-gate failure: in a Medium post dated Mar 21, 2026, the author says their Medium Partner Program access was revoked after content was flagged under an AI-content policy. If any revenue path depends on partner enrollment or policy approval, require a documented owner and fallback before launch.

Require verifiable release evidence, not cross-thread sign-off. One grounded example is a release artifact tied to a commit marked with GitHub's verified signature. It also includes an explicit package inventory, "Files Included (8 files)." Your format can differ, but the check should be just as clear: reviewers can confirm the exact approved bundle and whether anything required is missing.

Also be explicit about unknowns. This section does not set KYC, KYB, or AML trigger thresholds, country rail reliability scores, settlement SLAs, or a universal reconciliation evidence standard. Fill those in with your own contracts and controls, or defer launch.

Copy/paste checklist. Assign one owner per line.

- Monetization dependencies documented, including any partner-program or policy-gated approvals

- Country and payment-ops specifics are either evidenced in your own controls or explicitly marked unknown here

- Any split-rules/sub-ledger assumptions are either evidenced in your own design docs or explicitly marked unknown

- Any payout-orchestration specifics are either evidenced in your own runbooks or explicitly marked unknown

- Any settlement-timing commitments are contract-backed or removed from launch messaging

- Reconciliation and exception evidence requirements are defined in your own controls (not assumed from this section)

- Build vs. Buy decisions documented with owners, risks, and launch fallback paths

- Any partner-program or policy-gated monetization dependency reviewed with a fallback if access is revoked

- Launch packet versioned, approval-locked, and checked against its included artifact list

Final decision rule: if a checklist item cannot be evidenced, it is not complete.

Before launch, align product, ops, and engineering on one implementation path and edge-case handling in Gruv Docs.

Frequently Asked Questions

What does 1-to-Many Monetization actually mean in payment operations?

It means one platform has to allocate and pay out funds across a large creator base, often hundreds or even thousands of counterparties. In practice, this is a long-tail payments pattern with many small, frequent transactions, which can strain legacy accounts-payable and procurement processes. The risk is not just operational: late or inaccurate payments can disrupt creator work, and missed day-of-production payments can halt work.

What are the minimum components of a launch-ready Payment Architecture?

A launch-ready baseline supports more than one monetization mode, not just a single revenue stream. The grounded scope includes subscriptions, PPV, tipping, DM monetization, live streaming, and agency tools, with payment infrastructure that can help smaller teams support capabilities like multi-currency and instant payouts. Build-vs-buy timelines can also differ sharply, with cited ranges of 12 to 18 months and $500K to $1.5M for custom builds versus 45 to 60 days for white-label paths.

How do Tiered Subscriptions, tips, and Direct Sales change split and payout design?

They move you from a single monetization path to a hybrid operating model. In this guide’s grounded model, that means handling multiple monetization modes consistently instead of forcing every flow into one pattern. The practical takeaway is to design for mixed modes from launch, not to assume one universal split rule will fit all of them.

How should we compare countries before expanding Cross-border Payout Rails?

This guide does not provide a country-by-country scoring framework or definitive expansion criteria. A practical next step is to use your own operating evidence to evaluate payout delivery and support reliability by market. If payout expectations and exception handling are unclear for a country, treat rollout risk as high.

When do we require KYC, KYB, or AML before payout release?

Exact KYC, KYB, and AML trigger points are not established in this guide. A practical next step is to define your hold-and-release policy clearly for your markets and providers before launch. Your team should be able to explain why a payout is blocked, what clears it, and who can approve release.

How do we handle Chargebacks and Refunds without corrupting creator balances?

The evidence here supports that chargeback protection is retention-critical. It does not provide one prescribed refund or chargeback workflow, liability model, or threshold set. Treat this as a design area that needs explicit transaction handling so balance outcomes remain explainable.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- cmr.berkeley.edu/assets/documents/promo/best-article-award/sa...trusted

- hbs.edu/ris/Publication%20Files/The%20Platform%20Org...trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC9707275trusted

- dco.org/wp-content/uploads/2024/12/Digital-Economy-T...external

- dl.acm.org/doi/10.1145/3544548.3581106external

- iab.com/wp-content/uploads/2025/04/Measuring-the-Dig...external

- lumanu.com/blog/2025-enterprise-guide-to-paying-creator...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Payments Infrastructure for Creator Platforms: A Complete Build vs. Buy Guide

Treat this as an operating decision, not a branding exercise. This guide helps founders and ops teams choose build, buy, or hybrid for creator payment infrastructure. The goal is to avoid committing roadmap, compliance effort, and go-to-market spend in the wrong markets.

Building Rent Collection Payment Architecture for PropTech Marketplaces

The hard part is not launching a rent payment button. It is choosing a payment architecture your team can operate, reconcile, and defend as volume, markets, and exceptions grow.

Network Effects for Community-Based Products as a Professional Moat

You've heard the advice everywhere: join communities, network, stay active. For a global professional running a business of one, that advice is too vague to be useful and loose enough to be costly. It assumes your time is unlimited. Worse, it misses the real issue: **risk**.