Quick Answer

No. There is no single nationwide determination for marketplace payout licensing, even when the federal side is clear. FinCEN MSB registration with the Department of the Treasury and its two-year renewal cycle can apply, but that does not answer state Money Transmitter License exposure. The deciding facts are operational: who receives funds first, who can pause or release disbursements, and whether live behavior still matches the partner contract.

How to Assess State Licensing for Marketplace Payouts#

If your platform pays sellers, creators, or contractors in the United States, treat licensing as an operating decision from day one, not a label to clean up later. The core issue behind state money transmitter licenses us states marketplace payouts is this: federal status and state licensing answer different questions, and teams get into trouble when they treat one as a substitute for the other.

At the federal level, a Money Services Business, or MSB, is a non-bank financial institution category under Bank Secrecy Act rules, and a money transmitter is one class within it. FinCEN's registration rule requires MSBs to register with the Department of the Treasury and renew that registration every two years. That matters, but it does not by itself resolve whether your payout model raises separate state licensing questions. FinCEN also said in its May 9, 2019 guidance that it "does not establish any new regulatory expectations or requirements." That is a useful reminder not to read federal guidance as automatic state clearance.

That gap is why marketplace payouts quickly become an operations problem. You are not only asking, "Are we a money transmitter?" You are also asking who touches funds, who controls release timing, what the provider contract actually covers, and which states may be implicated by where payers and payees sit. CSBS describes itself as the nationwide organization of banking regulators from all 50 states, which is a practical shorthand for the real posture here. State-level analysis can differ, so one nationwide answer may not be reliable.

Before launch, or before changing payout flows, force three checkpoints and document them in writing:

- Confirm the actual fund flow: who receives money first, who can hold or pause it, and who triggers disbursement.

- Verify the legal posture you are relying on: your own analysis, a partner's licensed program, or an unresolved question that needs counsel.

- Map the state footprint touched by the product as designed, not as marketed.

Keep the evidence simple and durable. Save a current fund flow diagram, copies of provider agreements and terms, internal sign-off from Legal and Compliance, and a short memo explaining why you think a partner's coverage does or does not apply. One useful verification step is to compare product behavior to contract language every time payout timing, beneficiary onboarding, or release conditions change. If those no longer match, your earlier conclusion may not hold.

For the rest of this article, use a simple rule. Separate federal MSB obligations from state Money Transmitter License analysis, document the facts before relying on a partner, and treat unresolved edge cases as escalation items rather than launch assumptions. That is a reliable way to keep Compliance, Legal, Finance, and Payments Ops working from the same set of facts.

Start with the terms that drive licensing scope#

Start with this baseline: an MTL is state licensing, and MSB is a federal category that can apply in parallel. Treating one as a substitute for the other is where marketplace payout decisions break down.

CSBS describes money transmitters as a subset of money services businesses and describes oversight as a state regulator function across all 50 states, the District of Columbia, Guam, Puerto Rico, and the U.S. Virgin Islands. In practice, federal requirements do not remove state requirements, and a partner's federal status does not end state analysis for your flow.

Set tight internal meanings for recurring terms. "Marketplace payouts" should mean the actual movement of funds from payer to payee in your product, not a feature label. "Agent-of-payee treatment" should be handled as a state-specific legal position you may rely on, with written validation where it matters.

Anchor conclusions to legal sources, not provider commentary. If your position depends on a state Money Transmitters Act or similar statute, start there, then confirm with regulator materials, and retain the exact statute or regulator page, access date, and matching contract clauses tied to your fund flow.

Also separate convenience text from official legal text. FederalRegister.gov states its displayed content is not the official legal edition and points to the official PDF on govinfo.gov. For decisions with legal impact, verify against the official version before treating the point as settled. Related: A Guide to the Money Transmission Modernization Act (MTMA).

Decide when partner licenses are enough and when they are not#

Partner licenses are potentially enough only when your operating model stays inside that licensed program as implemented; federal MSB guidance does not resolve this on its own. FinCEN's guidance is interpretive, does not create new requirements, does not cover every fact pattern, and says models not specifically listed may still have BSA obligations.

Use this checkpoint table before you rely on partner-license coverage:

| Checkpoint | If this is true | Treat as higher-risk and escalate |

|---|---|---|

| Custody of funds | Funds flow stays within the licensed provider's program terms | Your platform can hold, route, or otherwise control funds outside that scope |

| Control of payout timing | Release timing is governed by the provider program as contracted | Your team can pause, sequence, or release payouts through platform logic |

| Control of recipient onboarding | Onboarding follows the provider's governed flow for the program | Your platform controls onboarding decisions that affect payout eligibility or release |

| License relationship in force | The live product, contracts, and operations match the same licensed relationship | Contract posture and live operations diverge, or coverage assumptions are unclear |

If your platform controls movement logic or beneficiary release conditions, treat that as a higher-risk branch and run a state-by-state MTL analysis. If your role is narrowly software facilitation under a licensed provider's terms, document exactly where that applies and where it does not.

Also keep source hygiene strict: FederalRegister.gov's XML rendering is described as unofficial and not legal notice, so verify legal conclusions against official legal text before treating them as settled. Related reading: EU Digital Services Act for Marketplace Operators.

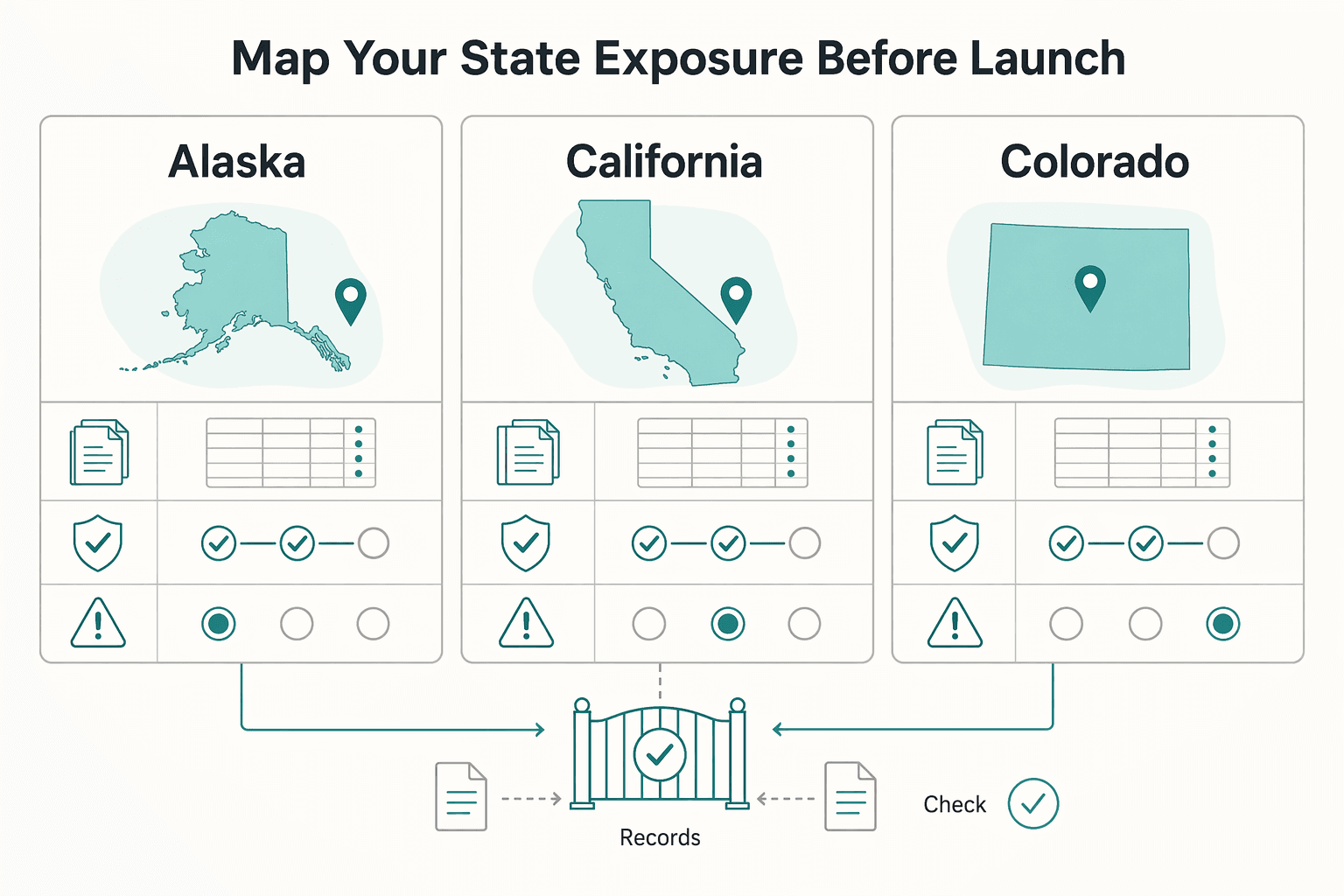

Map your state exposure before launch#

Build a state inventory before launch, and treat Legal sign-off as a gate: no new-state launch until Legal confirms that state's exposure classification and licensing or exemption posture.

Start with the states you expect to hit first, not all 50 at once. For most teams, that means your first payer and payee concentrations plus states where go-to-market is already active. Use Alaska, California, and Colorado as early rows so your team documents state-level decisions instead of relying on national assumptions.

For each state, log the launch sequence, payer/payee geography, fund-flow control points, regulator steps, complaint-channel status, and the evidence behind your current view.

| State | Regulator step to log | Complaint channel status | Known evidence attached | Unknowns blocking launch |

|---|---|---|---|---|

| Alaska | State of Alaska Division of Banking & Securities | Verify current intake path on regulator site | Launch sequence, payer/payee geography, fund-flow diagram, provider contract terms | Exposure classification, licensing/exemption posture, Legal sign-off |

| California | Department of Business Oversight materials or current agency record relied on by counsel | Verify current intake path on regulator site | Same evidence set, plus any California-specific memo/provider analysis | Whether your exact payout role still fits prior assumptions |

| Colorado | Colorado Division of Banking | Verify current intake path on regulator site | Same evidence set, with owner for regulator outreach | Open questions on control of disbursement timing or release |

Add a strict known vs unknown field and apply it consistently. Mark items as known only when backed by regulator materials your counsel cites, a written outside-counsel memo, or binding provider contract language that covers your actual activity. Treat draft or non-final materials as unknown until validated; if a document is labeled Working Document - Subject to Change, do not treat it as launch approval.

Keep federal and state analysis separate. A FinCEN finding that an entity is an MSB with BSA obligations does not answer state money-transmitter licensing for marketplace payouts. The same fragmentation is reflected in the CRS report Who Regulates Whom? (updated 10/13/2023), so your launch file should remain state-specific.

Date-stamp each regulator page and complaint channel, store the snapshot you relied on, and record who verified it. If your memo depends on older agency materials, re-verify current complaint and supervisory paths before launch.

Build the evidence pack regulators and auditors will ask for#

After you map state exposure, make the file reviewable: a regulator or auditor should be able to see who controlled each payout decision and why.

| Artifact | Include |

|---|---|

| Control narrative | Who initiates the transfer request; who can pause or release payouts; where KYC/KYB, OFAC screening, and other policy checks run; which provider or internal service executes the payment |

| Customer and payee terms | Version dates and clauses on payout authority, holds, reversals, and complaints |

| Partner contracts and program terms | In-force contracts, program terms, and any addenda that change onboarding, payout timing, or funds release |

| Complaint logs | Intake date, state, allegation, owner, resolution, and any regulator contact |

Start with a control narrative that is explicit and current:

- Who initiates the transfer request.

- Who can pause or release payouts.

- Where KYC/KYB, OFAC screening, and other policy checks run.

- Which provider or internal service executes the payment.

Keep the core artifacts together by default:

- Current customer and payee terms (with version dates and the clauses on payout authority, holds, reversals, and complaints).

- In-force partner contracts, program terms, and any addenda that change onboarding, payout timing, or funds release.

- Complaint logs mapped to your

state complaint process(intake date, state, allegation, owner, resolution, and any regulator contact).

Your audit trail should let a reviewer pick one payout and reconstruct the path end to end: onboarding status, KYC/KYB result, OFAC outcome, exception approval (if any), provider response, ledger posting, and reconciliation output. The main risk is not missing a payout record; it is being unable to show which control approved release, who overrode a hold, or whether the outcome matched your own policy.

When evidence conflicts, treat it as a launch stop signal. If contract language, control settings, and observed payout behavior do not match, reopen the state analysis before launch.

If you cite supervisory references in your memo, date-stamp them and keep the exact version in the file. For example, the OCC Payment Systems handbook shows a Risk Management section and a Third-Party Risk Management topic (Version 1.0, October 2021), and notes updates through March 20, 2025.

Run ongoing obligations as an operating calendar#

Run licensing as a live operating calendar, because drift after launch is usually the bigger risk than initial filing. Treat annual license renewal, state examination readiness, and regulator correspondence as recurring operations, not one-time documentation.

Keep one calendar for state and federal obligations, with separate tracks and clear owners. For states where your position depends on a Money Transmitter License (MTL), track renewal dates, attestations, notice triggers, and correspondence history. If you are also a Money Services Business (MSB), track that separately on the same calendar: FinCEN says MSBs must register with Treasury, renew every two years, and maintain an agent list updated annually. Federal MSB registration does not resolve state licensing requirements.

Build one calendar teams can run#

A usable calendar should show, for each item:

- The obligation

- The legal entity and product in scope

- The jurisdiction

- The filing or notice owner

- The completion evidence retained

Keep the evidence with the calendar entry: filed form, submission confirmation, regulator acknowledgment (if any), and the policy or product configuration in force at filing time. If you monitor rule text on FederalRegister.gov, require a check against an official edition before changing policy, since the site states its prototype edition is not the official legal version.

Review the signals that change your risk profile#

Run a monthly control review for complaint trends, failed payouts, manual exceptions, and out-of-policy fund releases. Treat complaint intake as an early warning signal: CFPB intake includes money transfers, virtual currency, and money services; CFPB also says it sends more than 100,000 complaints to companies each week and that most companies respond within 15 days. Do not treat that 15-day statement as a state deadline.

If exceptions become routine, treat your licensing analysis as potentially stale even when filing dates are current.

Make product change review mandatory before release#

Require compliance impact review before deployment whenever fund flow, payout timing, onboarding control, or disbursement authority changes. This includes provider migrations, routing logic changes, and new hold or reserve features. If control of disbursement changes, reopen the state analysis before release.

For New York-specific questions, Choosing Between a New York Money Transmitter License and BitLicense explains where those regimes diverge.

Set escalation triggers for Legal and outside counsel#

Escalate immediately when the facts behind your last licensing view change. That includes entering a new state, adding a new payout rail, or changing who can pause, release, or sequence disbursements.

Escalate before launch if your terms rely on agent-of-payee treatment and you do not have explicit state-by-state validation for each target state and product variant. If your support is only a provider explainer or an old deal memo, treat that as a gap.

Escalate when state and federal posture start to blur together. MSB analysis under FinCEN rules does not, by itself, resolve the state MTL question, and the reverse is also true. FinCEN's May 9, 2019 interpretive guidance says it does not create new requirements and covers only certain business models, not every fact pattern.

Escalate as a combined issue when Compliance is discussing MSB posture, Finance is requesting FBAR-related account data, and Product is changing payout control at the same time. Send one package with current terms, the fund-flow diagram, provider contracts, and release-decision logic so counsel can assess the actual operating model.

For a step-by-step walkthrough, see A Deep Dive into Florida's Money Transmitter License Rules.

Align product and engineering controls to compliance decisions#

Make compliance decisions enforceable in the product, and treat compliance sign-off as a release gate for payout-flow changes.

Licensing conclusions hold only if your runtime behavior matches them. If your documented position says your team cannot control disbursement timing, but an internal tool can still release funds, your facts and implementation are out of sync, and that can create problems in a state examination.

Your minimum control set should cover:

- Policy gates on payout initiation so payouts start only when required checks pass for that product variant and recipient state

- Tamper-evident event logging for decision path, actor, timestamp, and policy result on every payout and exception

- Role-based approvals for overrides so support or ops cannot bypass holds, sequencing rules, or release restrictions without proper authority

Idempotency is also mandatory. Each payout request should carry a stable internal identifier and, where supported, a provider idempotency key, so retries reconcile to the original request instead of creating a second outbound instruction. Keep an unbroken trace: request received, policy decision rendered, provider response stored, ledger posting created, reconciliation outcome recorded.

Use a simple verification checkpoint: walk one completed payout and one failed payout end to end. You should be able to show who initiated the action, which rule allowed or blocked it, the provider response or error code, and the resulting ledger entry.

Keep tax-reporting boundaries separate from payout controls. Product logs can support adjacent review, but they do not satisfy filing obligations by themselves. Form 8938 is used to report specified foreign financial assets when total value exceeds the applicable reporting threshold, and it is attached to the tax return. IRS materials also state that reporting applies to taxable years starting after March 18, 2010, and that certain domestic entities must file for tax years beginning after December 31, 2015; the instructions cite a $50,000 year-end / $75,000 any-time threshold pair for specified domestic entities. Do not treat Form 8938 as interchangeable with FBAR, and do not treat FATCA references as a substitute for filing analysis.

If a release changes payout routing, release authority, exception handling, or ledger timing, do not ship until Compliance signs off on both the updated facts and the controls enforcing them.

Conclusion and next actions#

The practical win is a decision-led model, not a broad theory about whether Money Transmitter License (MTL) rules apply to marketplace payouts. Start with your actual role in the money movement, verify that role state by state, and do not scale until Legal has signed off on the documented facts. That is the cleanest way to reduce surprise licensing work, bad partner assumptions, and launch rework.

Keep federal and state conclusions separate on purpose. If you also have a federal Money Services Business (MSB) analysis, treat it as one input, not a substitute for state licensing review. FinCEN's guidance issued on May 9, 2019 is interpretive and does not create new requirements. FinCEN also notes that guidance examples do not cover every fact pattern, and unlisted models may still have BSA obligations. In practice, that means a comfortable federal read does not answer every state question, especially once your payout logic, recipient onboarding, or release controls change.

The teams that handle this well treat licensing as a live control discipline. The October 2021 OCC payment systems handbook is a good reminder of what that looks like in operations: policies and procedures, internal controls, risk assessment, and notice requirements all matter after the memo is written. The common failure mode is simple. Product adds a manual hold, Ops starts sequencing releases, or a new rail is introduced, but nobody reopens the licensing analysis because the original conclusion is sitting in a folder marked "done."

Your next actions should be concrete and sequenced:

- Build the state exposure table first. Include target state, payer and payee geography, product variant, whose licensed program you rely on if any, known versus unknown legal coverage, and the approval owner.

- Define escalation triggers before launch. At minimum, trigger review when you add a new state, a new payout rail, a new manual exception path, or any change in who controls disbursement timing.

- Map controls and evidence to that baseline. Tie the exposure table to fund flow diagrams, partner contracts, customer terms, complaint handling, event logs, and the calendar for renewals, notices, and internal reviews.

One verification checkpoint is worth adopting immediately. Pick one completed payout and one failed payout each month and confirm you can show initiation, policy decision, provider response, ledger effect, and any manual approval without hunting across tools. If you cannot do that quickly, your control story is weaker than your legal memo suggests.

If you want a simple rule to carry forward, use this one: when the facts change, the answer may change. That is the right posture for state money transmitter licensing in U.S. marketplace payouts, and it is the difference between a launch that is merely fast and one that is defensible.

For budgeting and sequencing, How to Get a Money Transmitter License: A State-by-State Timeline and Cost Guide outlines typical timelines and cost drivers.

Frequently Asked Questions

Do marketplace payouts require an MTL in every US state?

No blanket answer is supported here, and you should be wary of anyone giving one. The real question is whether your product facts change by state: who holds funds, who controls payout timing, and whether your role stays inside a licensed provider’s program terms. If those facts differ by product variant or recipient state, get a state-specific review before launch rather than assuming one conclusion travels everywhere.

Can we rely on a provider like PayPal or Stripe instead of getting our own license?

Sometimes, but not automatically. Whether a provider relationship helps depends on your contracts, fund flow, and state-specific analysis.

What is the difference between MSB status and state MTL obligations?

MSB status is a federal FinCEN concept for certain non-bank financial institutions, while an MTL is a state licensing question. FinCEN says that, with few exceptions, each MSB must register with the Department of the Treasury, renew every two years, and maintain a list of agents that is updated annually. That federal registration does not settle state licensing, even if your federal analysis is clear. FinCEN also says a person that is an MSB solely because it serves as an agent of another MSB is generally not required to register, but that is still not a blanket answer to state law.

What ongoing duties continue after licensing approval?

Treat approval as the start of recurring obligations, not the finish line. You will likely still need renewal tracking, regulator correspondence handling, complaint monitoring, and change reviews when product or routing changes alter who controls disbursement. If you have federal MSB status, keep the FinCEN two year renewal cadence and annual agent list update on the calendar. If adjacent products touch California digital asset activity, note that the DFAL license date was moved to July 1, 2026, which can matter even when your core payout product is separate.

Which internal team should own the state complaint process and regulator responses?

Pick one named owner before launch, document the intake and escalation path, and make every team use that path. The red flag is split ownership that leaves complaint logs or response records incomplete.

What evidence should we keep to prepare for a state examination?

Keep records that support your legal position and your actual controls, and retain the federal registration file if applicable. FinCEN places MSB registration responsibility on the owner or controlling person of the MSB.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- congress.gov/crs-product/R44918trusted

- consumerfinance.govtrusted

- dfpi.ca.gov/regulated-industries/digital-financial-asset...trusted

- dlr.sd.gov/banking/money_transmitters/default.aspxtrusted

- federalregister.gov/documents/2021/10/27/2021-20621/determinatio...trusted

- federalreserve.gov/boarddocs/supmanual/cch/cch.pdftrusted

- fincen.gov/resources/money-services-business-msb-regist...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Get a Money Transmitter License State by State Without Cost Surprises

Start with sequence, not sticker price. If you are building contractor payouts, creator monetization, marketplace settlement, or embedded payments flows, the bigger risk is not just getting the **money transmitter license state by state cost** wrong. It is spending on the wrong filings, in the wrong order, before you have nailed down what your product actually does with customer funds.

Money Transmission Modernization Act and State Licensing Decisions

If you accept, hold, or pass through client funds across state lines, treat licensing analysis as a pre-launch requirement. One recurring risk is quiet scope creep: work that starts as basic billing can become controlled money movement without a clear decision point.

California Money Transmitter License Requirements for First-Time Filers

Start with scope, not forms. If you're evaluating a California money transmitter license, map your money flow first: what you control, for whom, and where control starts and stops.