Quick Answer

Start by sequencing decisions, not chasing a headline total for money transmitter license state by state cost. Build one normalized model that separates filing work, surety bond planning, compliance setup, and recurring maintenance, then label scope assumptions for each jurisdiction. Run filings in waves only after your evidence pack is owner-mapped and versioned. Keep New York BitLicense on its own track, and lock recurring federal duties into an owned calendar so expansion does not outpace controls.

What Changes From State to State#

Start with sequence, not sticker price. If you are building contractor payouts, creator monetization, marketplace settlement, or embedded payments flows, the bigger risk is not just getting the money transmitter license state by state cost wrong. It is spending on the wrong filings, in the wrong order, before you have nailed down what your product actually does with customer funds.

In the United States, there is no single nationwide Money Transmitter License. Money transmission is handled at the state level, while federal obligations can still apply under Money Services Business rules in the Bank Secrecy Act. If your activity fits the MSB category and includes money transmission, assume two workstreams may matter at the same time: federal registration and state licensing analysis. That is why the fastest compliant path is usually a sequencing question first and a budgeting question second.

Before you start#

Run these checks before you trust any broad estimate or approve application spend:

| Check | What to confirm | Why it matters |

|---|---|---|

| Map the money movement | Who receives funds, who holds them, who instructs movement, and where settlement happens | If that flowchart is fuzzy, your legal analysis will be fuzzy too. |

| Confirm your federal baseline | MSB registration with the Department of the Treasury, renewal every two years, and annual agent-list updates | If you cannot say who owns those obligations, your launch plan already has a gap. |

| Choose a rollout shape | Whether you are launching in a few states first or selling nationally from day one | State order changes both cost and timeline. |

- Map the money movement. Write down who receives funds, who holds them, who instructs movement, and where settlement happens. If that flowchart is fuzzy, your legal analysis will be fuzzy too.

- Confirm your federal baseline. MSBs must register with the Department of the Treasury and renew that registration every two years. They also must maintain a list of agents and update it annually. If you cannot say who owns those obligations, your launch plan already has a gap.

- Choose a rollout shape. Decide whether you are launching in a few states first or selling nationally from day one. State requirements can differ on applications, bonding, net worth, compliance protocols, and ongoing reporting, so state order changes both cost and timeline.

Use this checkpoint before you move on. Legal should be able to summarize the product's licensing theory in plain English. Finance should know what assumptions sit behind the first budget. Ops should own the AML and KYC procedures that match the product flow, and Engineering should be able to show how those controls are implemented in the product. If any one of those owners is missing, expect rework.

This guide is built to help you budget and phase an MTL program across the United States without pretending every jurisdiction behaves the same.

One red flag up front: if someone gives you a national licensing number without saying whether federal MSB work is included, which states are in scope, or how state-specific exceptions are being handled, you do not have a decision-ready estimate. You have a placeholder. The rest of this guide is about replacing that placeholder with a plan your legal, finance, ops, and engineering teams can actually run.

Want a quick next step for "money transmitter license state by state cost"? Try the free invoice generator.

Decide if you should pursue your own MTL now#

Start only when you can defend, in writing, why your own licensing path is needed now, where to start, and which federal obligations run in parallel.

Step 1#

Treat this as a scope call first. If Legal concludes your product may involve federal MSB and Bank Secrecy Act obligations and may also require state money transmission analysis, treat licensing analysis as required, not optional.

Before choosing a filing path, require Legal to document what is known, what is still open, and which product facts could change the conclusion. If core flow facts are unsettled, such as who receives funds or who has authority over movement, you are not ready to choose a filing strategy.

Keep federal reporting calendars separate from state MTL timing. In the cited FBAR notice, certain covered individuals were extended to April 15, 2027, while other individuals with an FBAR obligation remain due April 15, 2026. Those are BSA reporting dates, not state MTL application deadlines.

Step 2#

Match the path to your commercial rollout. If near-term volume is concentrated in a few launch states, test a phased approach first. If buyers expect broad coverage early, model a wider first wave and compare owning the MTL stack now versus staying partner-dependent longer.

Compare the paths directly. Owning licenses can increase direct responsibility for filings, regulator responses, and annual renewal work. A partner-dependent route can reduce direct filing work, but it can also tie launch scope and timing to partner approvals and contract terms.

Step 3#

Set a hard go/no-go checkpoint with Legal, Finance, and Product before approving application spend. Require:

- a current product flow diagram

- a written licensing position memo

- a budget that clearly states what is included and excluded

If those artifacts are incomplete, your state-by-state estimate is still a placeholder.

The common failure modes are predictable: spending while core facts are still moving, and mixing federal reporting detail into state timing logic. Keep those tracks separate. Federal reporting can be precise down to recording maximum account values in U.S. dollars rounded up to the next whole dollar ($15,265.25 becomes $15,266), so your go/no-go package should be just as explicit.

Build one normalized cost model before you compare vendor numbers#

Build one shared model first: if estimates use different assumptions, the totals are not comparable.

Step 1#

Normalize every estimate into the same buckets before you react to price. At minimum, use four fixed lines: application and filing, surety bond program, legal and compliance setup, and recurring annual license renewal plus exam overhead. If a quote will not break out those lines, treat it as incomplete.

Keep the legal/compliance line explicit. With limited exceptions, each MSB must register with the Department of the Treasury, and the registration filing is the responsibility of the owner or controlling person. So when a quote says "compliance setup," confirm whether it covers MSB registration support, AML program materials, and internal review cycles. If not, you are not looking at a full cost picture.

Use one spreadsheet structure for every estimate and remove mystery categories. Blended first-year totals make vendor comparisons and rollout sequencing decisions unreliable.

Step 2#

Create an included-versus-excluded table for each estimate. This is where weak all-in numbers usually fail.

| Area | What the estimate must say | Why it changes the comparison |

|---|---|---|

| Jurisdiction scope | Whether New York BitLicense is included, excluded, or priced separately; whether Washington, D.C. is included | "National" can reflect different jurisdiction sets |

| Internal staffing | Whether internal Legal, Compliance, Finance, Product, and Engineering time is counted | External fees alone do not represent total spend |

| Regulator follow-up | Whether post-submission question rounds, document updates, and resubmissions are included | Follow-up work can materially change effort |

| Ongoing upkeep | Whether annual license renewal work and exam-readiness support are included, and for how many years | Filing-only quotes are not operating-cost quotes |

Require each row to be labeled included, excluded, or client-owned. If that cannot be stated clearly, do not treat the estimate as decision-grade.

Step 3#

Separate fixed lines from activity-sensitive lines, then model low/base/high scenarios. Keep surety bond and ongoing compliance operations on separate rows so activity assumptions are visible.

You do not need precision theater. You need explicit assumptions for each scenario and clear answers on what changes in bond-related spend and ongoing compliance work, including evidence handling and exam preparation. The MSB examination framework uses a risk-based approach to BSA examinations, which is a practical signal not to assume oversight effort stays flat.

Use a hard rule: reject any all-in number that does not state MTL scope, jurisdiction count, and maintenance period. If a quote cannot tell you whether it is filing-only, first-year, or multiyear, it is not a go/no-go input.

Prioritize states by product risk and commercial value#

Prioritize wave one where commercial demand and execution readiness are both strong, and treat a day-one national launch as a parallel-workstream plan, not a sequential one.

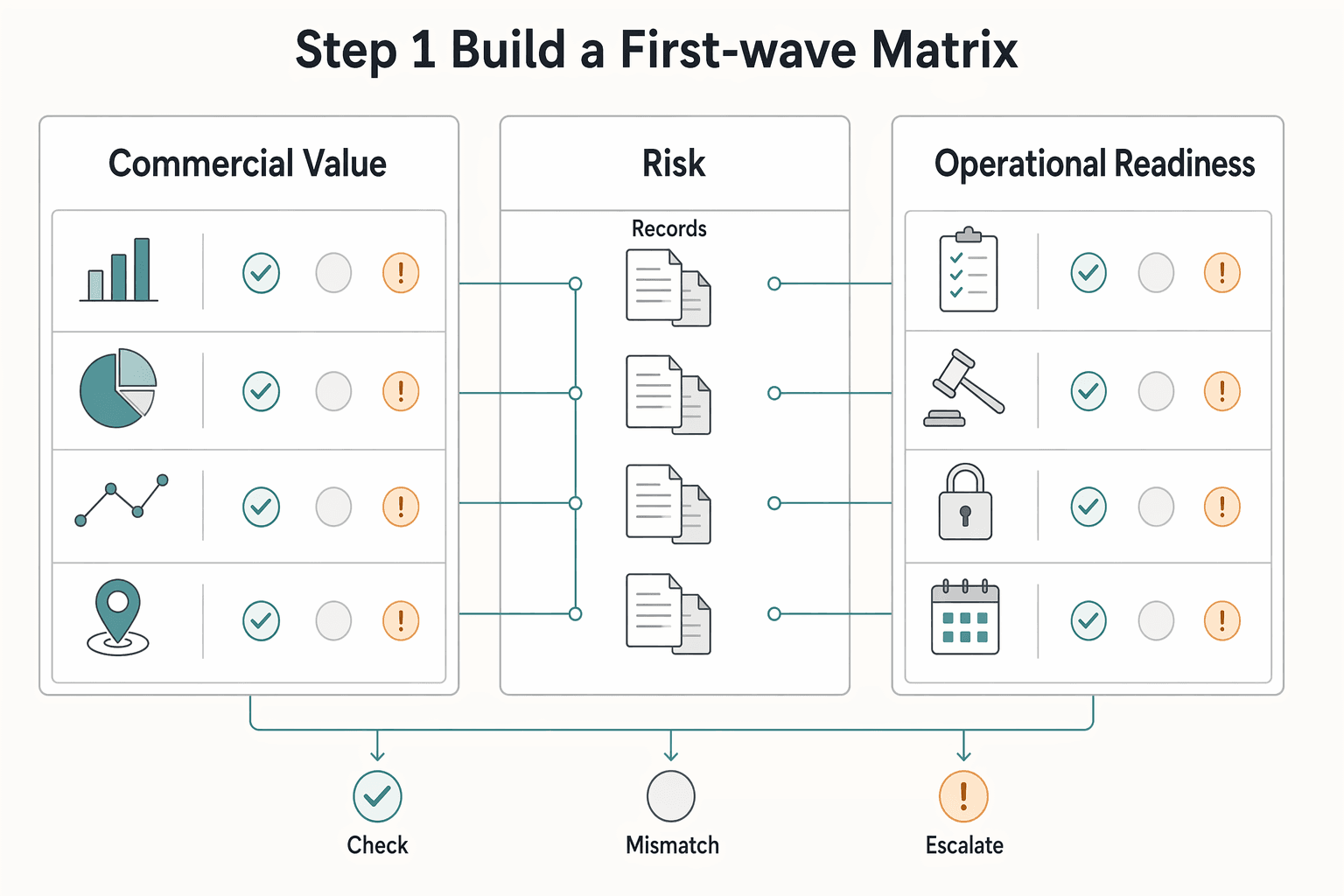

Step 1 Build a first-wave matrix#

Score each candidate jurisdiction on the same dimensions, and require evidence for every score.

| Matrix column | What to score | What to verify before you include the state |

|---|---|---|

| Commercial value | Pipeline, signed customers, launch commitments, expected volume | Customer-by-state view, contract terms, Finance-owned assumptions |

| Regulatory risk | How the product may implicate state money transmission laws | Counsel memo, product flow map, open legal questions |

| Operational readiness | Whether owners, controls, and documentation are ready for filing and follow-up | Named owners, approved policies, evidence locations, escalation path |

Do not let demand alone decide wave one. If readiness is weak, move that jurisdiction to a later wave unless leadership is explicitly accepting delay and rework risk.

If your product includes remittance transfers, flag that clearly in the matrix. The CFPB describes remittance transfers as generally almost all international electronic transfers of money by consumers. Use that as a complexity signal, not as a state-prioritization shortcut.

Step 2 Keep jurisdiction-specific edge cases as explicit branches#

Do not hide edge-case jurisdictions inside an "all states" label. Track them as separate assumptions with counsel's written view on scope, open questions, and whether each item is in wave one, separately scoped, or deferred.

This prevents a common planning miss: budget assumptions that look complete while legal scope is still unresolved.

Step 3 Use MTMA as a drafting aid, then confirm current state differences#

If counsel identifies partial alignment with the Money Transmission Modernization Act, use that to speed issue-spotting and draft structure, then verify what state-specific requirements and instructions still apply. A Guide to the Money Transmission Modernization Act (MTMA) can support that review.

Decision rule: if early customers are concentrated, sequence those jurisdictions first and use that work to harden your filing process. If the business needs broad coverage immediately, fund the added legal, compliance, and operational capacity up front.

For a step-by-step walkthrough, see How Creative Professionals Protect Flow State With a Compliance, Operations, and Client Firewall.

Assemble the pre-filing evidence pack before submission#

Before you submit any state application, lock your federal posture and evidence ownership so filings do not outrun your controls.

| Workstream | What to include | Key detail |

|---|---|---|

| FinCEN and MSB starting position | What product activity may make the business a money transmitter or other MSB; whether counsel concludes federal registration is required now, later, or remains open; what recurring federal maintenance follows | MSB registration renews every two years, and MSBs must maintain an agent list and update it annually. |

| BSA, AML, KYC, and OFAC artifacts | BSA/AML policy materials, KYC procedures, OFAC or sanctions-screening procedures, and evidence those controls run as documented | A reviewer should be able to move from policy to procedure to system evidence without guessing. |

| Owner map and version index | Named owner, storage location, approval date, and latest version for each artifact | Legal owns policy language, Ops owns procedures, Engineering owns control evidence and audit logs. |

Step 1 Confirm your FinCEN and MSB starting position#

Document whether your planned activity puts you in Money Services Business territory for federal purposes. FinCEN's rule applies to five classes of financial businesses, including money transmitters, and requires MSBs to register with Treasury. Treat that as a pre-filing dependency, not a substitute for state licensing.

Your working note should answer:

- What product activity may make the business a money transmitter or other MSB

- Whether counsel concludes federal registration is required now, later, or remains open

- What recurring federal maintenance follows from that posture

Keep the cadence explicit: MSB registration renews every two years, and MSBs must maintain an agent list and update it annually. If your model uses agents, assign that owner before launch.

Step 2 Gather baseline BSA, AML, KYC, and OFAC artifacts#

Build a baseline set that connects policy language to operating proof: BSA/AML policy materials, KYC procedures, OFAC or sanctions-screening procedures, and evidence those controls run as documented.

Use one test: can a reviewer move from policy to procedure to system evidence without guessing? If a policy says screening happens before activation, Ops should show the procedure and Engineering should show the audit trail or control output.

Step 3 Build one owner map and version index#

Create one filing index that maps each artifact to a named owner, storage location, approval date, and latest version. Keep ownership clear: Legal owns policy language, Ops owns procedures, Engineering owns control evidence and audit logs.

Your checkpoint is simple: every filing package maps each required artifact to one owner and one current approved version.

Related reading: Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

Run filings in waves and manage regulator follow-up like an ops queue#

Treat filings as an ops queue, not a one-time form task: run a prep stage, a submission stage, a regulator-question stage, and an approval-tracking stage with clear owners.

Step 1 Group submissions into waves. File in controlled waves using one locked document set per wave, then track exceptions separately. In licensing programs generally, reviews are often handled in cohorts rather than as a single continuous stream, so your internal process should match that reality.

Step 2 Define internal SLAs and escalation paths. Set an intake SLA for new regulator questions, an owner-assignment SLA, a draft-response SLA, and a clear escalation trigger. If a question requires a control or policy change, move it out of routine queue handling and into formal remediation.

Step 3 Keep one tracker for all active jurisdictions. Use a single tracker so follow-up cannot disappear across teams or firms. At minimum, track jurisdiction, filing date, current stage, last regulator contact, response due date, owner, blocker, and next action.

Step 4 Pause expansion when repeat follow-up exposes control gaps. If follow-up repeatedly surfaces the same issue, stop opening new filings and fix the root control before resuming. It is usually cheaper to correct policy, procedure, and evidence once than to defend inconsistent responses across multiple jurisdictions.

Budget year-two operations while you are still in year one#

Build year-two operations now, not after approvals: federal MSB deadlines are recurring from day one, and your state obligations add ongoing overhead.

Step 1 Lock recurring obligations into one owned calendar. Start with what is clearly required. If you operate as an MSB, register with Treasury, renew that registration every two years, and maintain an agent list that is updated annually. Put each item on one calendar with an owner, draft date, review date, and filing date, then add each state or Washington, D.C. obligation from the actual approval notice, portal, counsel memo, or bond paperwork.

Use one checkpoint: every recurring deadline in your tracker should point to the document that created it. If it cannot, treat it as unverified until you confirm it.

Step 2 Keep evidence current while work is fresh. Do not wait for regulator follow-up to assemble support. Maintain a live folder with current policies, recent control evidence, regulator correspondence, and proof that recurring obligations were completed on time.

The common failure mode is relying on the original filing pack even after AML procedures, agent records, or operating workflows changed. Keep the record updated as those changes happen.

Step 3 Fund support before wave two if bandwidth is thin. If one person is covering renewals, federal MSB obligations, surety bond coordination, and regulator mailboxes, slow expansion and add support first. Assign clear owners for bond-related reviews and notices in each active jurisdiction so obligations do not drift between teams.

The tradeoff is straightforward: support costs you now, but preventable lapses usually cost more than pausing one expansion wave.

If you want a deeper dive, read A Deep Dive into California's Money Transmitter License Requirements.

Avoid the mistakes that create expensive rework#

Rework gets expensive when state licensing scope, New York BitLicense decisions, and federal FBAR/BSA execution are blended into one plan. Separate them early, use fixed inclusion rules, and map obligations to evidence and deadlines before you expand.

| Mistake | Recovery | Specific detail |

|---|---|---|

| Comparing headline totals without inclusion logic | Rebuild estimates with standardized MTL cost categories and explicit inclusions/exclusions for state filing work, federal compliance implementation, internal staffing, and recurring maintenance | Remove any line item that cannot be traced to a named category or assumption. |

| Filing too broadly before controls are mature | Start with a narrow first wave under state money transmission laws in the jurisdictions that matter most commercially, then expand after controls and evidence handling are stable | Expand only after controls and evidence handling are stable. |

| Treating New York BitLicense like a standard add-on | Run BitLicense as a separate workstream with its own budget and go/no-go decision so it does not distort your base-state MTL plan | Keep BitLicense separate from the base-state MTL plan. |

| Under-specifying FinCEN and Bank Secrecy Act obligations in implementation planning | Tie policy controls to system evidence early and separate FBAR deadlines by population | FBAR maximum account values are recorded in U.S. dollars rounded up to the next whole dollar; certain individuals with signature authority but no financial interest are extended to April 15, 2027, while all other individuals with an FBAR filing obligation remain on April 15, 2026. |

Mistake 1: Comparing headline totals without inclusion logic. Recovery: Rebuild estimates with standardized MTL cost categories and explicit inclusions/exclusions for state filing work, federal compliance implementation, internal staffing, and recurring maintenance. If a line item cannot be traced to a named category or assumption, remove it from the decision memo.

Mistake 2: Filing too broadly before controls are mature. Recovery: Start with a narrow first wave under state money transmission laws in the jurisdictions that matter most commercially, then expand after controls and evidence handling are stable.

Mistake 3: Treating New York BitLicense like a standard add-on. Recovery: Run BitLicense as a separate workstream with its own budget and go/no-go decision so it does not distort your base-state MTL plan.

Mistake 4: Under-specifying FinCEN and Bank Secrecy Act obligations in implementation planning. Recovery: Tie policy controls to system evidence early, including how FBAR maximum account values are recorded in U.S. dollars rounded up to the next whole dollar (for example, $15,265.25 becomes $15,266, and negative results are entered as 0). Also separate FBAR deadlines by population: certain individuals with signature authority but no financial interest are extended to April 15, 2027, while all other individuals with an FBAR filing obligation remain on April 15, 2026.

Related: A Deep Dive into Florida's Money Transmitter License Rules.

Conclusion#

The practical answer is simple: treat compliance planning cost as an operating program, not a stack of disconnected applications. Define scope first, normalize every estimate, run work in waves that match your readiness, and build maintenance before growth turns small gaps into expensive rework.

- Define scope before you spend.

Confirm which product flows are in scope for your current compliance program and document what is out of scope. The expected output is a dated internal memo or legal conclusion that names included flows, excluded flows, and open questions. If scope is still shifting, do not start broad filings.

- Build one normalized cost table.

Every estimate should show included versus excluded items, one-time versus recurring work, and key assumptions in plain language. That is the only way to compare vendors, counsel, and internal build costs honestly. A good checkpoint is whether one owner can explain each assumption without hunting through email threads.

- Prioritize wave one with explicit assumptions.

Rank work by customer demand, commercial value, and your actual readiness to answer regulator questions. Keep assumptions and exceptions explicit, then re-validate them against current legal review before execution. The failure mode is easy to spot: a wide plan built on stale summaries instead of current review.

- Finalize the evidence pack and assign owners.

Your filing set should map clearly to Bank Secrecy Act and OFAC responsibilities, with named owners for policy text, procedures, and supporting records. The practical test is simple: every artifact has a current version, an approver, and someone who can defend it in follow-up. If your OFAC position depends on a General License, track exact dates (for example, GL 128B is stated to expire on April 29, 2026, and GL 131D is stated to extend authorization until May 1, 2026).

- Run filings and follow-up in tracked waves.

Use one tracker for submission date, questions received, response owner, due date, and escalation path across planned jurisdictions. If follow-up exposes a real control gap, pause new submissions and fix the root issue first. That delay is usually cheaper than defending inconsistent packages later.

- Stand up year-two operations before wave two.

Renewals, recurring updates, and exam readiness should be funded while you are still in year one. Your internal plan should include rough order-of-magnitude cost ranges, institutional cost analysis, pre-acquisition planning, and project risks. If your team cannot support ongoing maintenance for wave one, do not approve expansion yet.

A final gut check helps: if Legal, Finance, Ops, and Engineering cannot explain the same assumptions from the same document set tomorrow, you are not ready to scale the program.

Frequently Asked Questions

What does a realistic 50 state Money Transmitter License budget include beyond filing fees?

This grounding pack does not provide validated 50-state budget totals or state-by-state cost components beyond filing fees. Use it for federal compliance baselines, and treat state cost modeling as a separate legal/compliance workstream with explicit assumptions and exclusions.

Which MTL cost categories usually recur every year after initial approvals?

The recurring federal items are clear: MSBs must renew Treasury registration every two years and maintain an agent list that is updated annually. Confirm recurring state cost categories with your state regulators.

Which line items change the most with transaction growth, especially surety bond costs?

If you model low/base/high volume cases, label those as planning assumptions rather than sourced facts from this section.

Is Montana actually exempt from money transmitter licensing?

Do not make that call from a summary chart or from this FAQ. Verify the current state rule directly before using Montana as a planning shortcut. A better checkpoint is a written legal conclusion dated to your launch plan, not a recycled note from an older market scan.

How should we handle New York BitLicense in timeline and cost planning?

Keep New York BitLicense separate from the base-state licensing budget and timeline. This section’s sources do not support specific New York timing or cost claims, so the safe move is a separate workstream, separate assumptions, and a separate go or no-go decision. That keeps one high-complexity branch from distorting the broader launch plan.

Do we need full national coverage immediately, or can we launch in waves by state priority?

Use a phased or broad approach based on your legal and compliance readiness, and do not treat FBAR rules as a substitute for state money transmitter license requirements.

What should be prepared first to satisfy FinCEN, AML/KYC, and state regulator expectations?

Start with the federal items: confirm whether you are operating as an MSB, prepare for Treasury registration, track the every-two-years MSB renewal, and track the annual agent-list update. For FBAR where relevant, keep the dates and reporting mechanics straight: certain signature-authority filers have an extended due date of April 15, 2027, while many others remain due April 15, 2026, and amounts are recorded in U.S. dollars rounded up (for example, $15,265.25 becomes $15,266).

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Money Transmission Modernization Act and State Licensing Decisions

If you accept, hold, or pass through client funds across state lines, treat licensing analysis as a pre-launch requirement. One recurring risk is quiet scope creep: work that starts as basic billing can become controlled money movement without a clear decision point.

California Money Transmitter License Requirements for First-Time Filers

Start with scope, not forms. If you're evaluating a California money transmitter license, map your money flow first: what you control, for whom, and where control starts and stops.

A Deep Dive into Florida's Money Transmitter License Rules

Start by proving what your product actually does with customer value. If your notes cannot show where value enters your flow, where it sits, and where it goes next, you may not be ready to file.