Quick Answer

Yes. Living abroad does not automatically end state tax exposure for digital nomads, especially when California or New York ties remain active. Start by testing domicile and residency status, then separate W-2 wages from self-employed income before choosing a filing treatment. Day counts help, but they are only one signal. Your position is stronger when work-location logs, address history, and required state filings such as Form 540NR align.

Start Here and Decide Your State Tax Risk Without Guessing#

Living abroad does not end state income tax exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

Get the federal baseline right before you touch state conclusions. U.S. citizens and green card holders abroad often still file on worldwide income, and filing thresholds still apply. For 2025, commonly cited thresholds are $15,750 for single filers and $31,500 for joint filers under 65, with a separate $400 trigger for self-employment income. If that baseline is wrong, penalties and interest can begin before any state residency argument is even reviewed.

Use three working labels so everyone involved is speaking the same language:

Tax domicile: your home-base claim for tax purposes.Statutory residency: a residency label a state may apply under its own rules.Nonresident status: the filing posture you claim when your facts support it.

These are operating labels, not universal legal definitions. Each state writes and enforces its own tests, so confirm the exact rules anywhere you may need to file. You do not need perfect certainty on day one. You need one position that stays consistent as facts, logs, and forms are updated.

Then run the analysis in this order:

- Identify where your strongest ties still sit and assess domicile risk first.

- Review each relevant state's residency guidance before choosing a return posture.

- Build your evidence file now so your return, forms, and records tell one consistent story.

Before drafting forms, write a short position memo that states what you are claiming, which records prove it, and which gaps are still open. Include the date key facts changed, who owns each open issue, and when unresolved items will be reviewed again. This memo keeps monthly updates focused and prevents a filing-season scramble where the narrative changes each time you open a worksheet.

A common early mistake is claiming a low-tax address while objective ties still point to the old state. Property access, voter registration, vehicle records, and work-location history can undercut your claim fast. Reconcile your address timeline and work logs monthly, and keep that support with your draft return file. If facts are mixed or changed mid-year, get written advice before choosing resident, part-year, or nonresident treatment.

The Three Tests States Use Before They Tax You#

Most state disputes reduce to three checks: ties, sourcing, and proof. States may use different terms, but this sequence keeps your analysis stable and easier to defend.

| Test | What to review | Key point |

|---|---|---|

| Ties | Where your strongest personal and economic ties actually land | Domicile and statutory residency exposure usually shows up here first |

| Sourcing | Where services were performed | Treatment can differ between wages and independent income |

| Proof | Whether the position can be documented | Keep travel logs, work-location records, payroll or client records, and date-stamped support in one place |

Start with residency facts. Ask where your strongest personal and economic ties actually land, not where you intended them to land. Domicile and statutory residency exposure usually shows up here first. If this first check is shaky, every later conclusion will inherit that weakness.

Next, test sourcing. Where services were performed can matter, and treatment can differ between wages and independent income. If you skip that split, your position can look contradictory even when each income stream would have been reasonable on its own. This is also where many mixed-year files break, because one worksheet uses payroll assumptions while another uses contractor assumptions.

Then test documentation quality. A position you cannot prove is usually weak, even if the story sounds logical. Keep travel logs, work-location records, payroll or client records, and date-stamped support in one place. If support is scattered across inboxes and apps, build an index before you touch return drafts.

Use one hard checkpoint before drafting returns: if tie facts, sourcing assumptions, and your evidence folder point to different answers, stop and resolve the conflict first. Many filings break down at this stage because a clean narrative does not survive line-by-line comparison with the records.

Treat this as an operating method, not a one-size legal formula. Residency tests and day thresholds are state specific, so never assume one state's rule applies everywhere. Running ties, sourcing, and evidence in that order each month also sets up the next section, where you lock the same sequence into a repeatable filing process.

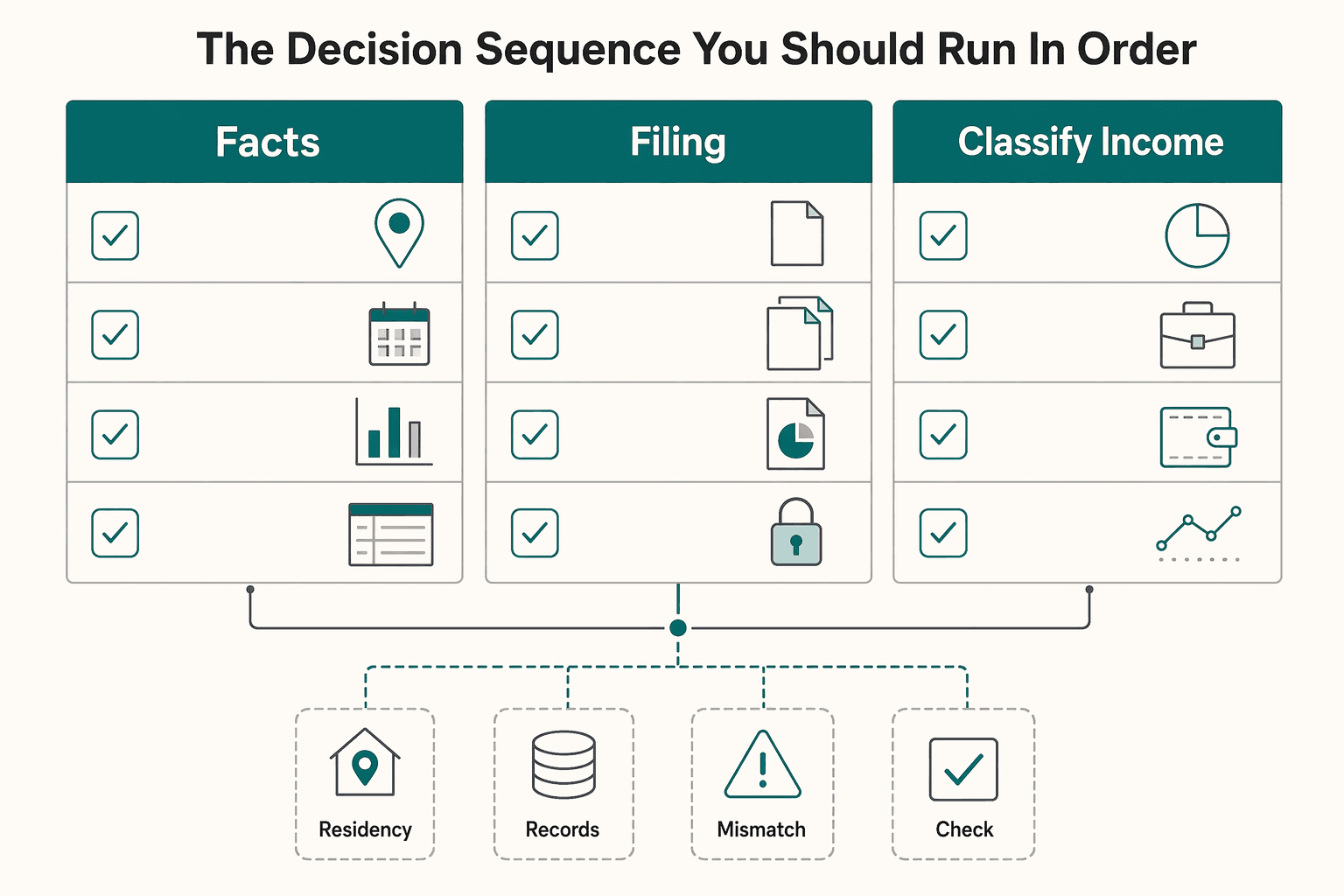

The Decision Sequence You Should Run in Order#

Run this in fixed order. Most filing stress starts when people pick the return type first and try to reverse-engineer facts later.

- Step 1: Identify likely residency classification and active ties. Start with California, New York, or any other state where your records still cluster. List facts first, then classify. If California is in scope, treat residency as a facts-and-circumstances determination, not an intent statement.

- Step 2: Apply each state's own residency definitions. Use resident, nonresident, and part-year rules state by state. In New York, the practical sequence is to classify first, then determine filing requirements.

- Step 3: Classify income stream by stream before choosing treatment. Separate

W-2wages from independent income, then map where services were performed. For California, services performed there are California-source income. UseCA Workdays / Total Workdays = % Ratio, then% Ratio x Total Income = CA Sourced Income. - Step 4: Choose filing posture and attach support. Pick resident,

nonresident status, or part-year treatment based on the first three steps. In California, part-year treatment applies worldwide income while resident and California-source income while nonresident. Nonresidents are taxed on California-source taxable income, commonly reported on Form540NR. If you use Form590, remember it does not apply to employee wages, and an incomplete certificate is invalid. For California-source payments, withholding can be optional at$1,500 or lessfor the calendar year.

After these four steps, lock a monthly snapshot with your classification note, sourcing worksheet, and evidence index. That habit keeps the file coherent and turns year-end prep into a consistency check instead of a reconstruction project. It also makes review faster because every return decision points back to a dated monthly record.

This order solves a common contradiction: forms that technically match totals but rely on incompatible assumptions. By forcing classification and sourcing before filing posture, you reduce late surprises and make it easier for an advisor to validate your approach quickly.

If any step is unclear, pause there and escalate instead of improvising near deadline. A short monthly review in this same order keeps records aligned long before filing season. If you want one place to keep that trail, the Tax Residency Tracker can help you document each decision before year-end.

Why Sticky States Create Most of the Pain#

Sticky states create most disputes because leaving is easier than proving you left. Intent matters, but records usually matter more.

California is explicit here. Residency is a facts-and-circumstances determination, not a single declaration. If you are part-year, California can tax worldwide income during the resident period. If you are nonresident, California can still tax California-source income.

New York follows a similarly practical sequence. You classify first as resident, nonresident, or part-year resident, then determine filing requirements. That order matters because classification limits which filing posture is available.

Treat old-state ties as a dated cleanup process, not a one-time statement. Your timeline should show:

- when filing-relevant facts changed

- monthly location and workday logs with source records

- an allocation worksheet using the California workday ratio above, if California exposure exists

- early support for Form

540NR, if California filing is required - one consistent state position across all records and filings

What makes sticky-state files expensive is the gap between intent and traceable activity. If your stated move date says one thing but payroll, calendar, and property patterns say another, the file becomes hard to defend even when your broader story is reasonable.

A common failure mode is assuming risk ended on move-out day, then discovering California-source wages because services were physically performed in California for part of the year. If your timeline is mixed, get state-specific advice before filing. For tie-cleanup detail, see How to Properly Sever Ties with a 'Sticky' Tax State Like California or New York.

Day Counting and Work Pattern Tracking That Holds Up#

Day tracking is a control function, not admin busywork. A weak log can sink an otherwise reasonable nonresident claim.

Treat 183+ days as a warning signal, not a universal pass-fail rule. Close calls often turn on where personal and economic ties are strongest, especially when travel is frequent and records are uneven.

The strongest files use one log format all year with the same fields every month:

- location by day

- work location by day, not only where you slept

- a work-type marker for each workday

- linked support such as travel records, bank or payment records, and client or payroll records

- notes on meaningful tie changes when they happen

If work-location treatment may affect sourcing, record why work was performed where it was and keep matching employer or client records. Then run a monthly reconciliation so dates, work locations, and income records line up with independent traces.

Add a month-end close routine so the log stays audit ready: finalize the prior month, tie each workday to support, and note unresolved discrepancies with an owner and due date. Keep those open items visible until they are resolved, not buried in old notes. This is often the difference between a defensible file and a plausible but fragile story.

Files usually fail not because of one missing receipt, but because of a pattern of small mismatches across calendars, travel confirmations, and payment timing. Clean those up monthly while facts are fresh, and your year-end position remains stable.

The expensive mistake is rebuilding logs from memory at filing time. Third-party records are usually more precise than memory, and mismatches can weaken your position quickly. If you cannot produce a clean month-by-month file for the full year, treat the posture as high risk and narrow aggressive claims before filing.

W-2 Employees and Self-Employed Nomads Face Different State Risk#

Keep W-2 wages and self-employed income separate from day one. Blending them creates avoidable mistakes before you even reach state sourcing.

| Income type | Social Security and Medicare handling | Core federal artifact | Common mistake |

|---|---|---|---|

| W-2 wages | For most wage earners, employers calculate these taxes through payroll | Wage records and withholding trail | Treating wage income like contractor income |

| Self-employed income | You calculate self-employment tax yourself | Schedule SE on your U.S. federal tax return | Treating contractor income like payroll withholding |

For most wage earners, payroll handles Social Security and Medicare calculations. Self-employed filers calculate self-employment tax on Schedule SE. In this context, self-employment tax means Social Security and Medicare only, commonly 15.3% total with 12.4% Social Security and 2.9% Medicare. It is not your full tax liability.

There is also an in-year tradeoff when pay type changes. Self-employed filers can deduct the employer-equivalent share of self-employment tax for AGI purposes, while wage earners generally cannot deduct payroll Social Security and Medicare withheld from wages. Drafting Schedule SE before year-end and reconciling to monthly records helps catch mismatches early.

For cross-border work, do not ignore Social Security coordination. Dual Social Security taxation can happen without agreement-based relief. When U.S. coverage applies, keep a U.S. Certificate of Coverage from the Social Security Administration with payroll or contract records as support used in covered exemption cases.

If you switched between W-2 and self-employed status in the same year, separate support by period before filing:

- build a month-by-month timeline with start and end dates for each pay model

- tie each period to its records: payroll documentation for wage periods, Schedule SE support for contractor periods

- reconcile Social Security and Medicare amounts across both periods

- review wage-period payroll treatment separately from contractor self-employment calculations

This separation also helps with state sourcing analysis later. When each income type has a clean record trail, advisors and reviewers can test your filing position without guessing which assumptions were applied to which period.

Federal Obligations Still Matter but They Do Not Solve State Residency#

Federal accuracy is non-negotiable, but it does not settle state residency. Keep federal and state analysis connected in your file and separate in your conclusions.

U.S. citizens and resident aliens are taxed on worldwide income, including while abroad. That baseline is mandatory reporting, not proof that any state must treat you as nonresident.

Treat FEIE as a reporting adjustment, not a bypass. It applies only if you are a qualifying individual with foreign earned income from services performed in a foreign country, and it is claimed on Form 2555. Excluded income is still reported on the return.

If you rely on the physical presence test, the threshold is strict: 330 full days in any 12 consecutive months. Days do not need to be consecutive, but each counted day must be a full 24-hour period from midnight to midnight. If you miss that 330-day threshold, that test is not met.

Use current year numbers when you project. The FEIE cap is $130,000 per qualifying person for 2025 and $132,900 for 2026. For 2025, two married individuals who both qualify can exclude up to $260,000. The housing exclusion or deduction is figured first, which can reduce FEIE available.

FTC can also reduce federal tax, but Form 1116 is category specific and each form allows one category selection. Mixed income can require multiple Form 1116 filings. That is one more reason to finish federal accuracy work before locking state posture.

Run this checkpoint before filing:

- reconcile your 330-day count to travel records using the midnight-to-midnight rule

- draft Form

2555and any Form1116entries before finalizing your filing position - keep a separate state memo so FEIE and FTC assumptions do not bleed into domicile conclusions

The practical risk is assumption bleed. Teams finish federal forms, then accidentally let FEIE or FTC logic drive state conclusions that need separate support. Keep a standalone state memo so your residency analysis remains evidence-based.

If travel is fragmented, the day threshold is missed, or multiple Form 1116 categories are required, treat the file as high review and avoid aggressive state conclusions until federal forms reconcile cleanly. For a deeper federal comparison, FEIE vs. FTC: A Strategic Choice for High-Earning US Expats is a useful companion.

Build a Defensible Evidence Pack Before You File#

Build the evidence pack before you file, not after a notice arrives. The critical separation is simple: federal foreign-asset reporting and state residency proof may live in one folder, but they answer different questions.

| Artifact | Why it matters | Concrete checkpoint | Common miss |

|---|---|---|---|

| Form 8938 | Reports specified foreign financial assets when the applicable threshold is exceeded | Attach it to your annual income tax return and file by that return due date, including extensions | Filing it separately from the return, or missing timing |

| FBAR (FinCEN Form 114) | Separate foreign account reporting requirement | File if one account or aggregate maximum account values exceed $10,000 during the calendar year | Assuming Form 8938 replaces FBAR |

| State-residency support file | Separate issue from federal foreign-asset reporting | Validate residency proof under each relevant state rule | Treating federal foreign-asset filings as complete residency support |

For Form 8938, filing depends on whether you exceed the applicable threshold for your category, and it must be attached to the return you actually file. If no income tax return is required for the year, Form 8938 is not required even when assets exceed a threshold.

For FBAR, use a reasonable approximation of each account's highest value during the year. Report values in U.S. dollars, round up to the next whole dollar, and for non-U.S. currency use the Treasury rate for the last day of the calendar year, or another verifiable rate with source support if Treasury data is unavailable.

Before filing, verify mechanics:

- keep periodic account statements that support maximum account value calculations

- save exchange-rate support when you use a verifiable non-Treasury rate

- confirm Form 8938 is attached to the filed return, including extension timing

- validate residency arguments separately under state-specific rules

A practical way to avoid cross-contamination is to maintain two short indexes: one for federal foreign-asset reporting artifacts and one for residency support. You can store them in the same folder, but they should not be interchangeable in your filing logic.

If Form 8938 is prepared but FBAR threshold and maximum-value checks were not completed, treat the return as high review before filing.

Run a Quarterly Compliance Cadence Instead of Annual Panic#

Quarterly discipline prevents annual panic. Most costly errors come from year-end reconstruction, not from one bad line item.

Keep the cadence simple: monthly recordkeeping, quarterly review, then one filing-season consistency pass. Each cycle has one job. Monthly updates capture facts while they are fresh. Quarterly checks catch payment drift and missing records. Filing season then becomes validation rather than salvage.

During the year, pair one monthly habit with one quarterly check:

- Monthly: log income and expenses, then reconcile to statements and invoices.

- Quarterly: review estimated-tax status and confirm records are complete.

- Use April, June, September, and January as recurring reminder months for estimated-tax checkpoints.

A useful quarterly meeting agenda can stay short: confirm what changed in location or work pattern, verify estimated-tax coverage, close missing-document items, and document decisions with dates. You are not trying to finalize the return each quarter. You are keeping the year-end file stable enough that nothing important is left to memory.

Close each quarterly review with three outputs: a dated assumptions note, an updated missing-items list, and a decision on whether your current filing posture still holds. This keeps your file operational instead of turning every review into open-ended discussion.

If no one is withholding for you, actively manage both income-tax and self-employment-tax obligations. Use 15.3% as a planning check for self-employment tax and net self-employment income above $400 as a filing-trigger check before each quarter closes.

When filing season arrives, use the same records and filing assumptions you tracked all year. If facts changed mid-year, update treatment immediately instead of repeating last year's approach. If tie and classification issues remain unresolved, How to Properly Sever Ties with a 'Sticky' Tax State Like California or New York is a practical next step.

Know the Red Flags That Mean Call a Pro Immediately#

Some files stop being practical DIY work. When your position turns on close judgment and your records do not support one clean timeline, call a pro early.

Use this screen before filing:

- You cannot substantiate key day counts with dated records.

- Your FEIE position depends on the physical presence test, but your log may not support

330 full daysin a12-month periodusing true full days (24 consecutive hours, midnight to midnight). - Your FEIE or FTC position is still shifting late in filing season.

- Your FTC work is complex, including multiple income categories or multiple countries on Form

1116, and draft filings are not fully aligned. - Your FEIE qualification covers only part of the year, but you have not adjusted the annual exclusion limit by qualifying days.

- You are treating FEIE as if it removes your U.S. filing requirement.

Bring a compact package to the first meeting: day-count ledger, travel support, draft federal forms, Form 1116 workpapers, and a timeline of filing assumptions. A strong checkpoint is whether the same dates and facts align across your FEIE day count, FTC inputs, and return drafts.

Late escalation usually costs more than early escalation because advisors must untangle unresolved assumptions under filing pressure. If one or more red flags applies, use Contact Gruv to confirm program coverage for your setup.

Scenario Checks for Common Digital Nomad Profiles#

Use scenarios to pressure-test your position, not to copy a template. Find the nearest fact pattern, then confirm one filing position still holds across records, forms, and timeline.

- Former California freelancer abroad full-year: Focus on whether records support nonresident treatment by period, not only a travel narrative. California can tax worldwide income during resident periods and California-source income during nonresident periods. Services performed in California are California-source, so keep dated work-location records and apply the California workday ratio when relevant. If California-source compensation exists, file Form

540NRand keep your tie-change timeline with return workpapers. - New York remote

W-2employee abroad: Classify first as resident, nonresident, or part-year resident before deciding posture. New York explicitly flags telecommuting when a primary office is in New York, so do not assume withholding alone settles the issue. If payroll records, day logs, and planned return treatment do not align, pause and get advice before filing. - Consultant rotating through U.S. visits: Treat day counting as a control point from month one. Keep a monthly log tied to travel dates, service days, invoices, and calendar records. If California workdays are involved, use the same sourcing ratio as a recurring checkpoint.

- Michigan-based nomad starting abroad: Michigan-specific rules are not covered here, so prioritize consistency across records and returns while you confirm local requirements. If California or New York touchpoints appear later, apply stricter checks immediately.

Across all profiles, prepare a compact evidence pack before return prep: an address and tie-change timeline, day-count support, payroll or contractor records, and a draft filing posture. Also verify form fit. Form 590 does not apply to employee wages, and an incomplete certificate is invalid.

Profiles should narrow your questions, not make the decision for you. The pattern that holds up is the same: classification, sourcing, and documentation that agree with each other and hold up under date-by-date review.

For a broader planning walkthrough, The Ultimate Digital Nomad Tax Survival Guide for 2025 can help you pressure-test your approach.

Use Better Financial Records to Lower Audit Stress#

Better records lower audit stress because they let you trace each return line back to real activity. The goal is not perfect paperwork. The goal is a file that is easy to explain and hard to challenge.

Start with traceability. Connect each payment to the related invoice, service period, and supporting records, then reconcile on a regular cadence. Keep one consistent fact pattern across income records, wage inputs, and draft returns.

Use one controlled record set even if your data comes from different tools:

- Income records: invoices, payment confirmations, and reconciliation notes.

- Wage records:

W-2inputs, payroll summaries, and corrections. - Self-employment records: net-earnings support used to prepare

Schedule SE. - Filing records: draft federal return workpapers and a short assumptions memo.

- Cross-check records: tie-outs between source records and return totals.

For self-employment, keep Schedule SE support detailed and organized. In this context, Schedule SE is where the Social Security and Medicare tax calculation is done for people who work for themselves, so the math and support should stay together.

If cross-border Social Security coverage applies, keep Totalization records and a U.S. Certificate of Coverage in the same filing packet. A certificate can support exemption from Social Security taxes in the other country when U.S. coverage applies, but it does not decide state income tax by itself.

If your tools provide audit trails or reconciliation exports, treat them as support rather than a substitute for complete records. If you use Gruv modules, keep audit-ready records and status views available, then confirm coverage by market and program.

When the file is clean, audits are easier because every material return number can be traced to a dated source document. That is the standard to aim for each quarter, not only in the month before filing.

Make One Defensible Filing Position and Support It With Records#

One defensible position beats a low-tax story you cannot prove. That is the central challenge with state taxes for digital nomads.

Start with residency and ties, then evaluate day counts in context. 183+ days can matter, but it is not universal. For FEIE analysis, the tax-home test comes before day counting, so even 330 days outside the US or fewer than 35 days in the US is not enough by itself.

Your evidence pack should show where you lived, where you worked, and what you earned. At minimum, keep:

- a monthly travel log with entry and exit dates by location

- work-location records, such as calendars, contracts, and invoices

- income records organized by payer and service period

- address and tie records aligned with your claimed residency position

- copies of filed returns that match that position

Do not wait until filing season to rebuild facts from memory. Missing or conflicting dates can weaken your posture and increase audit or penalty risk. Keep federal and state conclusions separate. Federal relief can reduce U.S. tax, but it does not automatically remove state exposure.

Escalate early when facts are mixed. If prior ties are still active, if your work setup creates unclear exposure, or if more than one country may claim you, get a CPA or tax attorney to review the position before filing. If you need a tie-severance checklist, How to Properly Sever Ties with a 'Sticky' Tax State Like California or New York is a useful companion.

The finish line is consistency under review. Your timeline, day logs, income records, forms, and filed returns should all tell the same story, month by month.

Frequently Asked Questions

Do digital nomads owe state taxes while living abroad?

Sometimes, yes. Living abroad does not automatically end state tax exposure because rules vary by state. Start by reviewing your domicile and residency facts before assuming you owe nothing.

What is the difference between `tax domicile` and `state tax residency`?

Tax domicile is your legal permanent home for tax purposes, and it is not the same as your physical location or mailing address. You generally have one domicile at a time, and changing it requires formal steps. State tax residency is a separate test a state may apply, often using day counts and other ties.

Does the `183-day rule` always determine whether I owe state tax?

No. Many states use a 183-day statutory residency test, but it is not universal and should not be treated as a single pass-fail rule. Other ties, such as your permanent address, voter registration, and driver’s license, can still affect the result.

Can my old state still tax me after I move overseas?

Yes, it can. Keeping old-state ties active can support a residency presumption even while you live abroad. Your filing position is easier to defend when your records clearly show your current facts.

What documents best prove `nonresident status`?

No single document settles this in every case. The burden is on you to prove nonresident status with consistent documentation. Keep address, voter registration, and driver’s license records aligned with how you file.

How does the `convenience of employer rule` affect remote `W-2` workers abroad?

Some states use this rule to tax remote employee work when it is done for convenience rather than business necessity. Working abroad does not always remove state exposure for remote employees. In some cases, this can also raise double-tax risk.

When should I hire a CPA or tax attorney for state residency issues?

Consider professional help when facts are mixed, records are incomplete, or your state position depends on close judgment calls. Consider it as well if remote employee rules or possible double-tax exposure make outcomes unclear. IRS international FAQs are general federal guidance and are not legal authority for a state residency position.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Properly Sever Ties with a 'Sticky' Tax State Like California or New York

To **sever state tax residency** in a way that holds up, follow this sequence: classify your move year, document your home-base change, then file returns that match the facts. The point is not to outmaneuver California or New York. It is to build a record that is true, documented, and consistent if the state asks questions later.

FEIE vs Foreign Tax Credit for High-Earning US Expats

Start with compliance, then optimize tax. If you are a globally mobile freelancer or consultant filing `Form 1040`, first confirm what you can actually claim and support, then compare the tax result.

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.