Quick Answer

Start by treating delivery and settlement as different workflows: an RTB win is not a payable. Map who invoices buyers, who carries collections risk, and which deductions can reduce publisher proceeds, then hold approval until auction IDs, statement references, ledger status, and payout state all align. Use schain plus finalized statements as controls instead of dashboard estimates. Program timing can also differ from impression timing, including monthly release windows such as payments issued between the 21st and 26th when conditions are met.

Mapping the Payment Chain#

If you are evaluating this market, focus on payment execution before role labels. The hard part is not memorizing definitions. It is knowing who bills whom, when cash is released, and what can break between an auction win and a publisher payout as identity signals get less reliable. We recommend starting there so your team does not confuse market labels with payout accountability.

At a high level, the roles are straightforward. A Demand-Side Platform (DSP) is the buy-side tool marketers use to purchase auction-based media. A Supply-Side Platform (SSP) represents publisher inventory and connects that supply to multiple demand sources. An Ad Exchange is the real-time auction marketplace in the middle, and an Ad Network is an intermediary that aggregates buying and selling across multiple sites or apps. Those basics help, but they do not explain settlement.

Delivery and cash movement are connected, but they are not the same process. An impression can clear in real time and still be paid later because of thresholds, payment holds, or contract terms. Public docs only show pieces of it. For example, AdSense says payment is issued between the 21st and the 26th of the month only when the balance exceeds the threshold and no payment holds apply. That is an operating signal, not a market-wide settlement rule.

This article focuses on the gap between media flow and money flow. That means billing ownership, settlement logic, payout reliability, reconciliation evidence, and the tradeoffs that show up when you add a program or partner type. If your product moves funds from buy-side spend through sell-side counterparties to publishers, treat the payment chain as a sequence of obligations and checkpoints, not one revenue-share line. We would rather map each handoff explicitly than ask your team to explain it from memory later.

A simple rule up front: if a partner cannot show how impression-level activity maps to invoice lines and payout states, treat that as operating risk. Do not assume help-center content covers the full commercial picture. In some cases, public documentation says the complete payment terms sit in the Terms and Conditions rather than the support article. If you cannot see the contract path and the payout path together, your team is still missing part of the money story.

Cookie and identity shifts make this more important. Official records show that in July 2024 Google said it would no longer remove third-party cookies from Chrome, and in April 2025 it changed course again on the planned standalone prompt. So this piece does not assume a settled cookieless endpoint. What is documented is the operating pressure: signal loss has affected addressability and measurement, which can lower confidence in what happened and when.

The core operator question is simple: where does the money path diverge from the media path, what evidence do you need before payout approval, and when does program complexity become reconciliation risk? A useful checkpoint is whether your team can trace one partner transaction from auction event to ledger posting to payout status without relying on manual explanation. Use that trace test before approving any new partner pattern.

Get the market map right before discussing money#

Get role clarity first. DSP, SSP, ad exchange, and ad network labels tell you market function, not guaranteed payment responsibility. A Demand-Side Platform (DSP) is the buy-side tool advertisers use to purchase auction-based media. A Supply-Side Platform (SSP) represents publisher inventory and connects that supply to demand. An Ad Exchange is the marketplace where buying and selling meet. An Ad Network is an intermediary that aggregates inventory across multiple sites or apps.

In Programmatic Advertising, the core mechanism is automated buying and selling of digital inventory. Real-Time Bidding (RTB) is one transaction method within that model, with auctions that occur in less than a second. That explains how impressions clear, not who invoices, approves adjustments, or releases publisher payouts.

Buy-side and sell-side incentives can create reconciliation questions early. Buyers optimize audience, timing, and budget outcomes. Suppliers optimize revenue ranges. If performance or revenue views diverge, ask a direct scoping question before launch: in this deal, is each partner acting as buyer, seller, marketplace, or packaged intermediary, and does that role change by product or channel?

Apply the same discipline to company names in stack discussions. Google Ad Manager is positioned by Google as a publisher ad-management platform for larger publishers, with support for multiple exchanges and networks. Magnite and PubMatic are commonly presented as sell-side companies. Do not assume those labels imply the same commercial terms, payment timing, or adjustment policy.

Use a simple checkpoint in your partner summary sheet: stated role, connected counterparties, reporting surface, and the entity shown on statements or invoices. Role blur is often where payment-chain confusion starts. Have your finance owner review that sheet before launch so the team is not reconciling entity names after spend starts.

Separate impression delivery from cash movement#

A won auction is a delivery signal, not a cash-ready payable. Teams that treat RTB logs as settled revenue can approve too early and unwind later. If your team cannot point to the release rule, it should not treat delivery as payout-ready.

Once roles are clear, split the process into three lanes: delivery, cash, and reconciliation. Delivery can happen in less than a second. Cash settles later. Reconciliation is where records are matched, adjusted, and either approved or held. We recommend keeping those lanes separate in your operating review so you can see where money timing actually diverges.

| Participant | Ad delivery path | Cash path | Reconciliation path |

|---|---|---|---|

| Demand-Side Platform (DSP) | Receives bid request, evaluates impression data, and returns a bid or creative | Owes media spend under contract terms with the sell-side counterparty; an auction win is not settlement | Matches bid request or auction ID, response reference, spend records, and post-auction billing events |

| Ad Exchange | Routes bid requests and responses between buy and sell sides | Its role in billing can vary by setup | Provides auction-level or aggregate reporting used to connect bid activity to billing records |

| Supply-Side Platform (SSP) | Represents publisher inventory and passes winning demand for serving | Calculates publisher payables from delivery and billing records, with room for valid adjustments | Reconciles buyer or exchange records with publisher delivery records and queues exceptions |

| Publisher | Makes inventory available and serves impressions on site or app | Receives remittance after the sell-side counterparty validates and releases payables | Compares internal delivery and revenue views with SSP or network statements before accepting totals |

The actual order of operations#

- Bid request is sent.

Exchange-side infrastructure sends the request to bidder infrastructure. In one documented RTB flow, response time is limited to 80 to 1000 ms.

- Bid wins and impression is delivered.

This is still a delivery event. An impression can be counted when a creative begins to load.

- Billing events are created later.

Auction time and billing time can be separate, so reported CPM movement does not automatically equal same-period remittance.

- Payout obligations are calculated.

Sell-side counterparties turn delivery and billing records into payables, with room for later adjustments.

- Exceptions are queued before close.

Missing references, timing gaps, invalid-activity adjustments, and cross-system mismatches should be held for review.

Where timing gaps appear#

- Auction win to counted impression: counting points can differ across systems, so impression and click totals can diverge.

- Counted impression to billable event: some implementations model delay between auction and billing.

- Initial earnings to final payable: month-end delivery, earnings finalization, and cash release are separate events in documented monthly payment flows.

A discrepancy is not automatically misconduct. In one major ad measurement context, discrepancies of up to 20 percent are described as normal, so classify first and escalate second.

What operators should verify before close#

Before you approve a payout batch, confirm the basic trace points. If a required reference is missing, hold the line item and resolve it before payout approval:

| Checkpoint | Confirm before approval |

|---|---|

| Event IDs present | Bid request or auction ID and partner response or statement reference |

| Handoffs matched | DSP-to-exchange or SSP records and SSP or network-to-publisher records |

| Ledger status confirmed | Billed, pending, adjusted, or held, not just reported |

| Payout state confirmed | Draft, queued, approved, released, or blocked |

| Exception queue reviewed | Missing IDs, late adjustments, invalid-activity changes, duplicate lines |

Map who bills whom and where margin leakage hides#

Your payout model is only as reliable as your billing map. You need to know who invoices buyers, who remits publishers, and who carries collections risk.

In a direct Supply-Side Platform (SSP) relationship, the SSP can act as the billing counterparty. In at least one public SSP model, PubMatic states it invoices Demand-Side Platforms (DSPs), collects gross media payments, and may still owe Publishers when buyer collection fails. So billing ownership and collections risk should come from contract terms, not from auction flow alone.

With an Ad Network, the network intermediates buying and selling across many sites or apps. A common tradeoff is transparency. Statements may show earnings totals while still giving limited detail on how specific post-delivery adjustments changed net proceeds.

Use the payment chain, not the auction chain#

Use OpenRTB schain as a control check for payment-flow visibility. It is designed to enumerate entities in the direct flow of payment for inventory, so mismatches between schain participants and invoice or remittance records should be treated as reconciliation risk. Auction logs alone may not be enough. They show who touched delivery, but not necessarily who owns invoicing, collections, and downstream adjustments.

Where publisher proceeds usually get reduced#

Many payout reductions show up in statement logic and adjustment handling, not just auction mechanics. Documented deduction points include debit or credit earnings adjustments, advertiser non-payment adjustments, invalid-traffic refunds, and payout holds that can delay release. Public publisher-program documentation also indicates that some valid adjustment categories may still lack day-level or channel-level detail, which limits auditability.

Use this rule before you sign: if you need transparent revenue-share reporting by Publisher, avoid counterparties that cannot provide line-item adjustment evidence. Aggregated adjustment totals may be tolerable for small tests, but they are weak once disputes scale or publishers start asking for support. Invalid traffic and advertiser default deserve explicit modeling because both can reduce final publisher payout after delivery has already happened.

Contract fields you want before launch#

| Contract data field | Why it matters | What good looks like |

|---|---|---|

| Billing counterparty and invoicing owner | Defines who bills buyers and who remits publishers | Named legal entity for buyer invoicing, named legal entity for publisher payout, and explicit collections-risk allocation |

| CPM basis and rate definition | Prevents gross, net, and adjusted pricing disputes | CPM tied to billable event, currency, tax treatment, and fee treatment |

| Floor commitment fields | Connects pricing commitments to executable deal terms | Explicit use of imp.bidfloor and/or deal.bidfloor, plus precedence rules when both appear |

| Deduction reason codes | Makes post-delivery reductions auditable | Enumerated codes for invalid traffic, advertiser default, and debit or credit adjustments, with clear labels for any additional deduction categories |

| Payout release conditions | Prevents avoidable payment-timing disputes | Stated cadence, required approval or hold conditions, and release window once conditions are satisfied |

| Statement grain and reference fields | Enables reconciliation to internal records | Periodized transactions by type, invoice or statement IDs, and adjustment references |

These fields are operational, not legal decoration. Inconsistent invoice fields are a known source of mismatch and delay, so require sample statements and adjustment memos before launch. Then verify that records are organized by period and transaction type and that payout-release logic is explicit.

Related: Airline Delay Compensation Payments: How Aviation Platforms Disburse Refunds at Scale.

Understand what cookieless pressure changes in payment risk#

Cookieless pressure can change payment risk mainly by reducing shared confidence in measurement, attribution, and impression matching between the buy side and sell side. It is not just a targeting issue.

Google's measurement guidance flags data loss from privacy laws, third-party cookie pressure, and platform changes, and IAB Tech Lab describes identity signals ranging from deterministic to inferred. As identity shifts from known to inferred, settlement can get harder. The question is no longer only whether an ad served, but whether both sides can prove the same user, event, or conversion chain with enough certainty to support money movement.

Why disputes get sharper at the DSP and SSP handoff#

Risk can concentrate at handoffs where records should align but often do not. ISBA and PwC reported that data captured by a Demand-Side Platform (DSP) for an impression was not equally captured by Supply-Side Platforms (SSPs), which hindered impression matching. In its Q1 2020 sample, 15 advertisers, 8 agencies, 5 DSPs, 6 SSPs, and 12 publishers, 15% of advertiser spend was an unknown delta that could not be attributed.

That does not mean every cookieless change becomes a cash dispute. It does show why weaker identity certainty can increase reconciliation pressure before settlement, credits, or clawbacks.

What this changes operationally#

The practical shift is simple: raise the proof standard before payout decisions. If buyers and agencies keep pushing for "complete, open, transparent and future-proofed" measurement, and transparency programs keep emphasizing proprietary log-level reconciliation, summary reporting alone may be challenged more often.

One caveat: do not base policy on the assumption that third-party cookies have already been fully deprecated everywhere. Public sources conflict on rollout trajectory, including later UK regulatory updates noting Google restated it would not deprecate third-party cookies. The operating signal still holds because pressure comes from broader privacy and platform change, not one browser event.

Tighten evidence standards before payout#

If identity methods are opaque, tighten pre-payout evidence at the SSP and ad exchange boundary before funds leave your ledger, for example:

| Evidence item | What to retain |

|---|---|

| Log-level impression records | Event timestamp, auction or transaction ID, counterparty reference, and schain or supply-path context |

| Identity-method labeling | Deterministic versus inferred signals, plus available match-status or confidence fields |

| Adjustment support | A reason code and periodized memo for each debit, credit, or unattributed bucket |

Use this checkpoint: can your team trace a disputed earning line from the publisher statement to the SSP log and back to a buy-side reference without relying on screenshots or aggregate dashboards? If not, treat fast payout terms based only on summary numbers as higher risk.

Use publisher control levers that directly affect payout outcomes#

If you want to change payout outcomes, start with what enters and clears the auction. Floor policy, inventory quality filters, and placement-level controls all shape which bids clear, how much inventory fills, and how outcomes vary across partners.

A floor that sits above bids that regularly clear in RTB can leave more impressions unfilled. A floor that is too low can cheapen inventory. The tradeoff is fill versus price discipline, not a one-way optimization.

Start with the levers that move settlement inputs#

A floor in Prebid is the lowest CPM a bid must meet. In Google Ad Manager, pricing rules centralize floor management for non-guaranteed demand, including different floor prices or Target CPM by inventory size. Those settings directly affect whether a top bid clears or falls below floor.

Use inventory quality controls as commercial filters, not automatic upgrades. Category blocking can improve brand fit, but it can also narrow eligible demand. Placement controls work similarly: tighter rules can improve control, while broader access can improve fill.

High floor versus fill-rate strategy#

A high-floor strategy protects price on impressions that clear, but it raises unfilled risk when bids miss the threshold. A fill-rate strategy lowers the threshold to monetize more impressions, but it can weaken realized value per impression.

Target CPM sits between those strategies. It is designed to improve fill and yield while keeping an average minimum price, which can help when demand quality differs by placement or size.

| Approach | What you gain | What can go wrong | Better fit when |

|---|---|---|---|

| High floor | Protects price on cleared impressions | More unfilled impressions | You can tolerate swings in delivery |

| Lower floor for fill | More monetized impressions | Lower realized value per impression | You prioritize steadier fill |

| Target CPM by placement or size | Balances fill and yield | Misconfiguration can hurt delivery | Demand quality varies across inventory |

If payout volatility is the priority, track partner-level variance and below-floor loss patterns before broad floor changes.

Review on a regular cadence with evidence, not memory#

Do not tune floors from memory. Run a recurring checkpoint, for example monthly, that links control changes to partner outcomes:

- floor or pricing-rule changes by placement or inventory size

- partner-level Yield group impressions and any other partner metrics you define internally

- unfilled impressions and below-floor losing-bid patterns

- net payout variance by SSP

Use Yield partner reporting, for example Yield group impressions with the Yield partner dimension, alongside SSP statements and your payout ledger for the same period. If a floor change lines up with lower fill or wider partner variance, roll it back or narrow it to placements that can support it.

Evaluate retail media paths separately from open web paths#

Treat Retail Media Network (RMN) expansion as a separate operating path from open web programmatic. On the open web, payment operations often center on delivery-to-billing reconciliation. In RMN, payment outcomes can be more tightly tied to data permissions, measurement rules, and partner governance.

On the open web, DSP, SSP, and exchange relationships are primarily about programmatic buying and selling at scale. In RMN models, those partners may still be present, but settlement outcomes are also shaped by who can use retailer data, how outcomes are measured, and how partners reconcile commercial terms.

| Path | Common dependency pattern | Where payment complexity usually shifts |

|---|---|---|

| Open web programmatic | DSP buying through SSP or exchange on publisher inventory | Delivery-to-billing reconciliation and payment operations |

| RMN on-site | Retailer-owned inventory plus commerce data, often with external adtech partners | Data-use terms, attribution definitions, and partner settlement workflows |

| RMN off-site | Retailer data activated on third-party inventory, often with DSP, SSP, and a Data Clean Room | Data collaboration approvals, cross-party measurement, and cross-party reconciliation |

Where RMN gets harder than open web#

RMN can strengthen value by linking ads to point-of-purchase context and closed-loop attribution, but it also adds governance load. Clean rooms are controlled collaboration environments, and rules can reject queries or remove rows. Privacy checks can also filter rows from outputs, which can create gaps between what commercial teams see in reporting and what finance teams need for settlement.

Standards and interoperability are still a practical constraint. IAB Europe sources cite different barrier levels, 53% and 70%, for standards, and also flag interoperability gaps that make cross-network deduplication harder. Operationally, that can increase debate over credited outcomes and cross-network reconciliation.

What to verify before launch#

Before launch, verify the parts of the model that can break settlement later:

- contract terms for data usage rights, attribution definitions, and settlement logic

- partner ID mapping across delivery reports, clean-room outputs, and settlement statements

- exception handling when privacy filters remove rows or queries are rejected

- whether invoicing and statements are still manual, since manual invoicing slows payment and disrupts reconciliation

When RMN should be phase two#

Keep RMN as phase two when your open-web reconciliation is still unstable, data-collaboration terms are not fully defined, or off-site execution depends on multiple external providers from day one. Move earlier only when data permissions, measurement definitions, and close-cycle reconciliation are already aligned across delivery, attribution, and settlement.

Build the compliance and tax artifact pack before launch#

Paperwork is often the real launch blocker, not product readiness. Treat your compliance and tax artifact pack as a hard gate. If the required records, tax handling rules, retention rules, and accountable owners are not in place, do not launch payouts for that market or program.

Build a minimum pack that is explicit by country and program path. Different payout models and cross-border payees can trigger different documentation and reporting needs, so avoid one generic template.

| Artifact | Minimum contents | Operator checkpoint | Common failure mode |

|---|---|---|---|

| Onboarding records | Legal name, address, entity type, payee country, beneficial-owner documentation when required | Confirm records are complete before the first payable event | Commercial approval exists, but payment cannot run because core identity or tax fields are missing |

| Payout policy evidence | Contracted payout timing, holds, deductions, release conditions, exception approvers | Confirm finance, product, and compliance are using the same policy version | Commercial terms and payment operations drift apart |

| Tax form handling | Collection, validation, storage, expiry monitoring, escalation rules, including Form W-8BEN where applicable | Confirm tax status is linked to the payee record and used in payout decisions | Missing or stale forms cause delays, incorrect withholding treatment, or close-cycle rework |

| Exception audit trail | Case ID, date, reason code, approver, supporting evidence, remediation outcome | Confirm manual overrides are searchable and retained | Disputes or audits arrive, and payout decisions cannot be reconstructed |

Cross-border caveats that matter in practice#

Do not assume every cross-border payment falls into the same tax bucket. If you are acting as a withholding agent for certain income paid to foreign addresses, Form 1042-S may apply. For most U.S.-source income paid to a foreign person, the general NRA withholding rate is 30%, unless treaty treatment changes the result.

That makes document collection a launch control. Form W-8BEN is a core example: foreign beneficial owners provide it to the withholding agent or payer when requested, including when claiming a reduced treaty rate. Before launch, define who collects it, where it is stored, how refresh timing is tracked, and what happens when it is missing at payment time.

Do not mix up FATCA, Form 8938, and FBAR#

Treat these as separate compliance tracks with different triggers. FATCA is implemented through country-level intergovernmental agreement structures focused on identifying and reporting U.S. accounts. Form 8938 and FBAR are separate regimes, and filing one does not replace the other.

| Item | Key distinction | Threshold/detail |

|---|---|---|

| FATCA | Implemented through country-level intergovernmental agreement structures focused on identifying and reporting U.S. accounts | Separate from Form 8938 and FBAR |

| Form 8938 | Separate regime; filing one does not replace the other | $50,000 / $75,000 for certain unmarried or separately filing individuals living in the U.S.; higher thresholds for joint filers and individuals living abroad |

| FBAR | Separate regime; filing one does not replace the other | Aggregate foreign account value exceeds $10,000 at any time during the calendar year; filed as FinCEN Form 114, due April 15 with an automatic extension to October 15 |

Check each form against its own thresholds. FBAR applies when aggregate foreign account value exceeds $10,000 at any time during the calendar year. It is filed as FinCEN Form 114, due April 15 with an automatic extension to October 15. Form 8938 uses different threshold sets. They include $50,000 / $75,000 for certain unmarried or separately filing individuals living in the U.S., with higher thresholds for joint filers and individuals living abroad.

Ownership and retention before rollout#

Require legal and tax confirmation before you make rollout commitments, because applicability varies by country, taxpayer status, income type, and program design. As an internal control, assign named owners for compliance controls, evidence retention, and remediation timing before launch.

At minimum, assign owners for tax form collection, exception approvals, retention periods, and record location. A practical baseline is 3 years for standard IRS record-retention situations, while certain records required under Bank Secrecy Act rules are retained for 5 years.

Run reconciliation in a fixed sequence to prevent payout incidents#

A fixed close sequence helps prevent avoidable payout incidents. In programmatic flows, statement timing, adjustment logic, and data access can differ across SSP, ad network, and publisher relationships, so discipline matters more than speed.

Use one order every cycle#

- Ingest partner statements and settlement files.

- Match statement lines to internal delivery, billing, and publisher-ledger records.

- Resolve breaks and document outcomes.

- Approve the payout batch.

- Release funds.

- Archive the evidence pack.

This is a control pattern, not a universal contract sequence for every DSP, SSP, or network setup. The key rule is stage closure: do not move to approval until matching and break resolution are closed.

Make ledger-level traceability non-negotiable#

Anchor controls at the payable line level. Each publisher payable line should trace to your internal record and the counterparty reference in the SSP or ad network report. If you cannot trace it, keep it out of the batch.

That also supports audit readiness. Programmatic financial audits depend on timely access to log-level supply-chain data. ISBA's Financial Audit Toolkit is built around that access, including the Data Fields List, Audit Permission Letter, and Principles of Use. If those permissions are weak, audit and reconciliation work can slow down.

Approve only from finalized statements#

Do not treat estimated revenue as payable revenue. Google Ad Manager states revenue is finalized at month end, and estimated values do not represent the final payout amount. It also notes prior-month balances are processed and verified by the 2nd of the month, which should inform your payout timing.

Breaks to escalate before release#

Escalate the breaks that can distort payables after delivery has already happened:

- Unmatched adjustments: delayed processing, rounding differences, and invalid traffic protections can create adjustments that do not cleanly map to original lines. Require reason codes and source-file evidence.

- Preliminary-to-finalized variance: if finalized statements differ from earlier estimates, recalculate payable amounts before approval rather than forcing estimates through.

- Late reversals after payout approval: Google notes that, in rare cases, invalid activity can be detected after payment is issued. Keep a documented post-payout recovery path, not only a pre-payout checklist.

Archive more than the final batch file. Keep the exact statement version used, break logs, approval records, and exception decisions so payout outcomes can be reconstructed later.

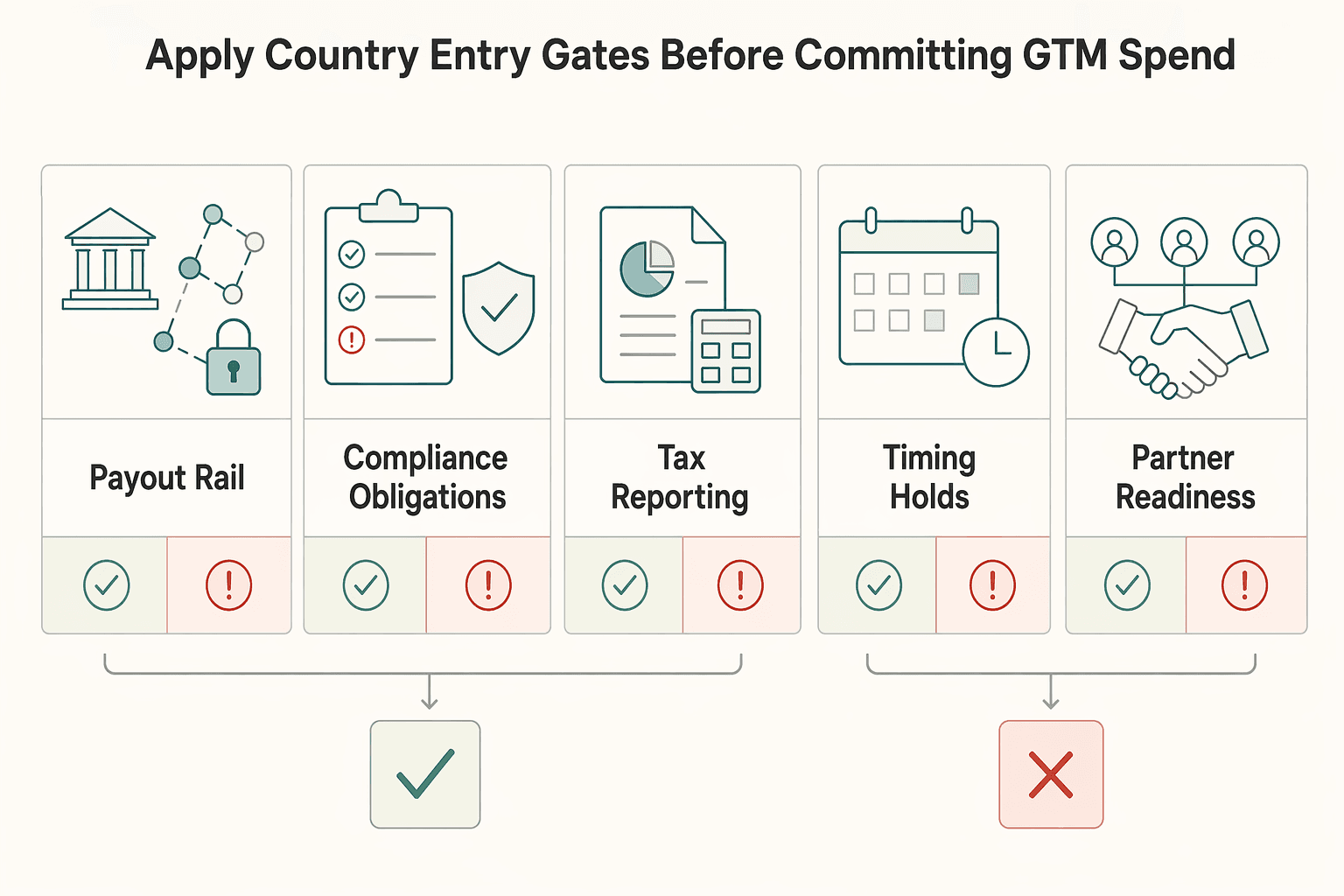

Apply country entry gates before committing GTM spend#

Make country entry a go or no-go operations decision before you commit GTM budget. If payout rail coverage, compliance readiness, or settlement evidence quality is weak, delay full rollout.

A short yes or no gate set is usually more reliable than a weighted scorecard because the core risks are binary. Either you can move funds and defend payout outcomes, or you cannot. That matters when DSP, SSP, ad exchange, and ad network counterparties provide uneven settlement detail.

| Gate | What to verify before launch | Go signal |

|---|---|---|

| Payout rail coverage | Your payment provider supports the target country, and the publisher payment method is available there | Supported country and usable local payout option |

| Compliance obligations | Required onboarding data by location, business type, and capabilities is known up front | Named owner and collected requirements before onboarding |

| Tax and reporting burden | Country-specific tax info requirements are clear; where relevant, you have a plan for Form 1042-S, FATCA IGA handling, and potential FBAR exposure over $10,000 | No missing tax artifact that can block payout readiness |

| Timing and holds | Hold rules and payout timing fit your cash model. For example, initial payouts can be scheduled 7-14 days after first payment, and some publisher programs issue payments between the 21st-26th when holds or payment-info changes are complete by the 20th | Timing fits your close calendar and reserve policy |

| Partner readiness | For each DSP and SSP, review statement quality, adjustment visibility, and observed exception handling from test cases | Final statements support reconciliation, not just dashboard estimates |

| What is still unknown | Record payment terms that are not publicly disclosed, including terms that may sit in a Service Order | Unknowns listed with an owner and due date before scale |

Two checks catch avoidable launch risk early. First, inspect sellers.json and the OpenRTB SupplyChain object, schain, to verify who is in the payment path and whether supply is direct or reseller. Second, compare dashboard reporting with finalized settlement outputs. Some reports are not finalized earnings, some invalid-activity deductions may not expose line items during finalization, and some deductions are final and non-appealable.

Use this as an operating rule: if multiple critical gates are still failing, delay full launch. Run a constrained pilot with capped volume, manual review, and explicit exception logging until the unknowns are closed.

For a step-by-step walkthrough, see How to Launch a Legal Compliance Platform for Freelancers and Handle Their Payments.

If your go/no-go checklist passes but payout rail and exception-handling details are still fuzzy, review how to structure operational controls in Gruv Payouts.

Choose your operating model for scale without losing control#

A practical default is a phased hybrid model. Start with direct counterparties you can audit, then add aggregator-style channels only after reconciliation and payout controls stay stable across monthly closes.

Keep one distinction clear across ad exchange, SSP, and ad network paths: RTB runs the impression auction, but it does not determine settlement ownership, adjustment evidence, or payout incident accountability.

| Model | Where it fits | Control | Speed to coverage | Reconciliation burden | Compliance load | Incident response |

|---|---|---|---|---|---|---|

| Direct integrations with major partners | Core relationships where auditability and source-level evidence matter most | High visibility into counterparty data and direct-versus-intermediary status | Varies by partner and implementation depth | Less partner-layer ambiguity, but still needs strong internal matching | Concentrated on your team and each direct partner | Fewer hops can make ownership easier to assign |

| Aggregator-led model | Expansion across multiple demand or supply sources | Lower direct visibility when an intermediary sits in the path | One control point can speed initial reach across multiple sources | Exception handling can increase when statements or deductions are summarized | Still significant; mediation setup includes privacy and consent configuration, for example GDPR and US state settings | Harder when failures span intermediary and underlying partners |

| Hybrid model | Core volume on direct paths, edge coverage through mediated paths | High control on core partners, moderate elsewhere | Balanced | More manageable when direct and mediated paths are separated by clear ownership rules | Split across paths, but easier to phase | More complex than pure direct, easier to contain than all-aggregator |

The decision is less about direct versus indirect in theory and more about whether you can prove the payment path when disputes happen. Before scaling direct relationships, verify sellers.json and ads.txt so direct sellers and intermediaries are clear.

Aggregator-led paths are useful when speed matters, especially when one layer serves ads from multiple sources. But centralization is not the same as simplicity. Mediation can combine bidding and waterfall setups, including sequential chains ordered by expected yield or CPM, which can make issue ownership less obvious.

Before you add volume, use a strict integration checkpoint:

- require idempotent retries for payout-triggering writes so transient failures do not create duplicate side effects

- verify webhook authenticity before processing, and make handlers replay-safe because undelivered events can be retried for up to three days

- keep your own audit trail for close and reconciliation; provider event retrieval can be limited to the last 30 days, and idempotency keys may be removable after they are at least 24 hours old

A common failure pattern is delivery failure, replay, duplicate ledger impact, then month-end surprises. If direct and mediated channels do not share deduping and ledger-reference rules, scale can expose that gap quickly.

Related reading: Healthcare Staffing Platform Payments Compliance for Safer Rollouts. Before locking your integration model, use the Gruv docs to map idempotent retries, webhook handling, and reconciliation-ready status flows to your rollout plan.

Conclusion#

Treat auction logic and cash logic as separate jobs. If you cannot name the counterparty, evidence trail, and payout release rule at each handoff, you are not ready to expand. We would rather see your team delay launch than approve payout logic it cannot explain cleanly.

Open-auction buying often has no direct relationship with the buyer, and buyers may not know exactly which media-owner network they are buying on. So media can clear while the money path stays weak. The teams that scale safely are the ones that document who bills whom, how deductions are explained, and what records are required before cash is released. If your team cannot document those three points, your rollout case is weaker than it looks.

Validate each handoff with evidence, not assumptions. On the supply-path side, sellers.json helps buyers verify whether an entity is a direct seller or an intermediary. On the payout side, Google Ad Manager shows why settlement timing and delivery timing diverge. Payment is sent at the end of the next month after the balance reaches threshold. Revenue rolls forward if threshold is not met, and payment records can include deductions tied to adjustments or fees. That is why month-end revenue reports and publisher cash receipts do not align automatically. We recommend making your team prove that timing gap on one live payout path before it scales the program.

Keep transparency expectations realistic. Reported unattributable spend improved from 15% to 3% in a later study, but not to zero, and a 58% impression match rate still signals imperfect reconciliation. Do not approve a new DSP, SSP, ad network, or publisher program unless it can provide line-level adjustment references, batch-level payout status, and a documented dispute path. If a partner can only provide summary statements, treat that as a real risk signal. We would rather hold the launch than ask your team to defend missing line-level evidence later.

Cross-border rollout raises the bar further. Payment onboarding may require tax information by location, and Form 1042-S, FATCA, Form 8938, and FBAR cover different reporting or withholding obligations. Exact obligations depend on entity facts and country setup, so commit GTM only after finance, compliance, and product align on document ownership, evidence retention, and exception remediation timing. If your owners cannot name who keeps those records, your team is not ready to widen the rollout.

Use this final pre-launch check:

- Confirm the legal counterparty for billing, adjustments, and disputes in each market.

- Verify the evidence pack you will retain: auction or impression identifiers, partner statement references, deduction reason codes, ledger posting status, and payout approval records.

- Check release conditions before launch, including payment thresholds, cycle timing, tax-information requirements, and who approves reversals or late adjustments.

If those checks are still unclear, delay expansion or run a constrained pilot. The advantage is not moving fastest into new supply. It is scaling revenue with enough counterparty clarity and reconciliation discipline to reduce hidden payout risk later. We recommend keeping the pilot narrow until your team can explain the payment path without hand-waving.

Frequently Asked Questions

What is the practical difference between a DSP, SSP, Ad Exchange, and Ad Network when money is moving to publishers?

A DSP is the buy-side platform marketers use to buy auction-based media, while an SSP represents publishers on the sell side. An ad exchange is the real-time marketplace layer connecting buyers and inventory, and an ad network is an intermediary that aggregates supply and demand across multiple sites or apps. For payout risk, the practical question is who your settlement counterparty is and who can provide adjustment evidence.

How do publishers actually get paid after RTB auctions close?

RTB decides the auction winner, but payout happens later through billing, reconciliation, and release rules. In Google Ad Manager, the winner is based on the highest net bid, and sellers are paid the closing price net of revenue share, with payment not falling below the configured CPM floor. Timing depends on program rules rather than RTB itself. For example, AdSense runs monthly and eligible payments are issued between the 21st and 26th.

What changes in publisher payment risk in a cookieless environment?

The risk can shift toward weaker attribution confidence, which may increase disputes, adjustments, and approval friction before payout. Browser policy is also date-sensitive: Google described an early-2025 phase-out plan, while the CMA later recorded a shift to user choice and, in April 2025, no standalone prompt rollout and no intention to deprecate third-party cookies. When identity inputs are less reliable, require stronger pre-payout evidence at the SSP or exchange boundary.

Who usually controls pricing and revenue outcomes, and where does Floor Price policy matter most?

Buyers set bids, but publishers and sell-side partners often control the price rules that determine whether impressions clear and at what yield. In Google Ad Manager, floor prices apply after revenue-share deductions, so floor policy directly affects net outcomes, not just headline CPM. If you want steadier revenue, tune floors carefully and review win rate, fill, and net payout variance by SSP each month.

How should operators compare open-web expansion versus Retail Media Network expansion?

Open-web expansion can increase reach, but auditability may be weaker. In ANA’s measured cohort, only 36 cents of each dollar entering a DSP effectively reached the consumer. RMN expansion can create new opportunities, but governance and measurement standards remain a constraint, and IAB Europe reported that 70% of buyers cited lack of standards as a barrier to investment. If data rights, settlement logic, and reconciliation ownership are still unclear, treat RMN as a later phase rather than day-one scope.

What are the minimum checks before entering a new country or program with cross-border payouts?

Start by confirming withholding and reporting ownership, required tax forms, payout-rail availability, and cross-border dispute handling. For U.S.-linked reporting, verify whether Form 1042-S may apply to certain income paid to foreign-country addresses, and do not treat FATCA, Form 8938, and FBAR as interchangeable. IRS pages in this area cite a $50,000 baseline Form 8938 threshold for certain U.S. taxpayers and a $10,000 FBAR aggregate-account trigger, but exact obligations depend on taxpayer and entity facts, so legal and tax review should happen before launch.

Which records are essential to defend payout calculations during disputes or audits?

Keep log-level auction and impression IDs, partner statement references, applied floor settings, deduction reason codes, payout batch approvals, and bid-traffic billing references such as BidRequest.imp.ext.billing_id when available. IRS guidance is to retain supporting records that substantiate income items, including receipts and canceled checks. If you only have summarized monthly statements with no line-level identifiers, your dispute and audit position is weak.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- assets.publishing.service.gov.uk/media/68f213ce06e6515f7914c728/Decision_to_r...trusted

- assets.publishing.service.gov.uk/media/5fa557668fa8f5788db46efc/Final_report_...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- irs.gov/individuals/international-taxpayers/nra-with...trusted

- irs.gov/businesses/corporations/foreign-account-tax-...trusted

- justice.gov/archives/opa/pr/justice-department-sues-goog...trusted

- sec.gov/Archives/edgar/data/1422930/0001422930250000...trusted

- alliancedigitale.org/publication/english-version-white-paper-prog...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Best Community Platforms for SaaS Businesses

Start by classifying the job. If you want access to other people's audience, ideas, or conversations, you are choosing a community to join. If you want a place your customers or members use under your brand, with your rules and structure, you are choosing software you will need to operate every week.

Airline Delay Compensation Payments for Customer Experience and Control

If you are evaluating an `airline compensation payments customer experience delays platform`, split the work into three lanes first: legally owed refunds, discretionary compensation, and outsourced claims recovery. Vendor pages often blur these together, but they lead to different policy choices, ledger treatment, and customer outcomes.

IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments

If you own compliance, legal, finance, or risk for a platform paying foreign contractors, sellers, or creators, you may need to make **Form 1042-S** operational. That means clear decisions, reliable checks, and escalation points your team can apply and defend.