Quick Answer

Choose a payout model by cost ownership first, then enforce eligibility and traceability before promising speed. The article supports starting with worker-paid instant cash-out for margin protection, using platform-paid speed only for targeted growth cohorts, and scaling with a hybrid policy when segments differ. Keep an explicit exception record for each request and show clear status when instant routes are unavailable, including when users move to scheduled ACH instead of a push-to-card outcome.

Where instant payout costs actually show up#

Fast access can improve worker experience, but speed is not the core decision. The real question is whether you can move money earlier without losing margin discipline, record clarity, or control over exceptions. Instant payouts are an economics and controls choice first, and a UX feature second.

-

Define the product by earned work, not by speed alone. Pay on Demand and Earned Wage Access, or EWA, mean access to wages already earned before the normal payday cycle. Same-day pay is usually straightforward: a worker clocks in, completes hours, then accesses a portion of those earned wages through a platform. That boundary matters because not every instant payment belongs inside payroll. One industry source says 64% of gig payments and 49% of gaming payouts now use instant methods, but it also notes that some of those are ad hoc transactions made outside traditional payroll or invoicing. If the money is not clearly tied to completed work, you are no longer in a clean earned-wages lane.

-

Treat on-demand pay as a payroll-connected operation. Providers describe earned wage access as working through integration with an existing payroll system, not as a standalone cash-out button. In practice, that makes the sequence bigger than the payout rail. Time capture, earnings calculation, disbursement method, security/compliance checks, and payroll reconciliation need to line up in your operating model. Direct deposit may be one delivery option, but the harder question is what data proves the amount was earned and releasable in the first place. A practical internal test is to pick one sample request and trace it end to end: request created, earning event identified, provider outcome accepted or rejected, amount released, and payroll record updated. The sources here do not define a universal audit-trace standard, so use this as an operational control pattern rather than a fixed rule.

-

Choose the model by cost ownership and failure handling. Worker demand can be real. One provider reports that 49% of working Americans are frequently short on money before payday, and 86% prefer daily pay jobs. Still, preference does not settle the business case. Smaller businesses often cite cost concerns, and one instant-payments source notes receiving fees can exceed $11 per transaction for the smallest SMBs. Decide early who pays for acceleration, what happens when an instant transfer fails, and what evidence support will need to resolve disputes. A practical baseline is a clean exception record with the earned amount, request time, released amount, provider status, and how payroll reflected the advance.

That is the lens for the rest of this piece: not "can we offer same-day and on-demand pay," but "can we offer it with records, pricing, and fallback behavior that still hold up at volume?" If you want the settlement-speed cost view, start with Same-Day vs. Next-Day vs. T+2 Payouts: What Settlement Speed Actually Costs Your Platform. If your use case sits in publisher or marketplace payouts, What Is a Demand-Side Platform (DSP)? How Programmatic Ad Platforms Manage Publisher Payouts is a useful parallel.

How to choose the right instant payout model for your platform#

Choose in this order: decide who pays acceleration costs, confirm you can reconcile early releases to earned work, then set a speed promise your rails can consistently support. Starting with an "instant" marketing claim before those checks usually creates avoidable subsidy and support risk.

Use this decision table before you pick a model#

| Decision area | What to verify before launch | What it tells you |

|---|---|---|

| Unit economics | Fee inputs remain unresolved until you verify them with your payment processor, payout provider, and available card/ACH routing options. Confirm who pays in each path: worker, platform, or shared. | This is your first filter. If margins depend on low cash-out usage, avoid broad subsidy at launch. |

| Payout frequency behavior | Estimate cash-out frequency from observed behavior when the option is visible after each earning event, not just stated preference. Review by cohort. | A workable weekly pattern can become expensive when users cash out after every task or shift. |

| Failure-state operations | Confirm you can trace request time, earning event, approval status, rail used, provider response, final release amount, and payroll or ledger treatment for every payout. | If this trace breaks, support load rises and finance confidence drops. |

| Pricing control tradeoff | Decide whether the provider handles more routing/pricing logic or your team owns subsidy rules, eligibility, and fallback behavior. | More control can improve tuning, but it also increases internal operating load and policy risk. |

Four checkpoints that should drive the choice#

- Unit economics first

Start with fee ownership, because it narrows the model quickly. Build one contribution view with your verified inputs, then rerun it for worker-paid, platform-paid, and hybrid before approving launch.

- Payout frequency behavior is the hidden multiplier

Faster pay is a usage pattern, not a one-time event. Workers may multi-home across apps, and payout experience is judged on speed, flexibility, transparency, and reliability, not speed alone. For a settlement-speed comparison by rail, see Same-Day vs. Next-Day vs. T+2 Payouts: What Settlement Speed Actually Costs Your Platform.

- Failure-state operations determine whether the model is supportable

"Instant" is a rail-selection decision. Push-to-card is often practical because it works with existing debit cards, but eligibility still gates access. Proof is one example: users need an eligible Visa debit card linked to Stripe to request instant payout, while scheduled ACH remains available. Design the same clarity in your flow: when fast rails are unavailable or fail, fall back clearly and keep an exception record.

- Pricing control changes your operating load

More pricing and routing control can improve targeting, but your team then owns more policy edges, messaging, and reconciliation review. If payout quality is inconsistent, fix clarity before adding complexity. Slow or unclear payout experiences can reduce active worker participation; for the retention impact, see Bad Payouts Are Costing You Supply: How Payout Quality Drives Contractor Retention.

After choosing a model, run a weekly review cadence in early rollout. Track reconciliation exceptions, payout-related support contacts, fallback usage, and repeat cash-out behavior by cohort. If reconciliation quality is unstable or support signals remain noisy, pause expansion and fix failure paths first; if those signals stay stable over repeated reviews, expand rails, regions, or segments.

If you want a deeper dive, read How Platforms Can Offer Instant Payouts as a Premium Feature Without Margin Surprises.

Want a quick operational next step? Try the free invoice generator.

Best model for margin protection is worker-paid instant cash-out#

If margin protection is your main constraint, worker-paid instant cash-out is usually the safest starting point. It keeps a faster, on-demand option available without creating a platform-wide speed subsidy on day one.

This approach is most practical when you need tighter cost control, when payout behavior varies by user, or when payout operations are still maturing. Keep the standard payout path available, and make faster access a clear opt-in.

Where worker-paid cash-out usually works best#

Worker-paid cash-out works best when your first objective is cost control without removing flexibility.

| Scenario | Why it fits |

|---|---|

| Thin-margin books | Charging only for the faster path creates a clearer cost boundary than subsidizing every accelerated payout. |

| Mixed urgency across users | Some users need same-day access, while others can use scheduled payouts. Optional paid speed supports both without forcing one cost profile. |

| Early-stage payout operations | A narrower launch reduces exposure while status tracking, reconciliation, and payroll tie-outs are still being hardened. |

What to verify before you offer it#

Treat this as an operating model decision, not just a fee setting. Before launch, confirm you can trace each early payout from earning event to final payroll record:

- what was earned

- what was requested

- what was released

- how final payroll reflected it

- what fallback path appears when speed is unavailable

If that chain is incomplete, pricing policy will not prevent cleanup work later.

Where this model starts to break#

Worker-paid cash-out is not universal. If faster pay is part of your hiring or retention strategy, a broad paywall on speed can conflict with that goal, since more frequent pay access can support employer attraction and retention outcomes.

That is usually the point to move from pure margin protection toward a targeted subsidy or hybrid policy.

Need the full breakdown? Read What Is Reverse Factoring? How Supply Chain Finance Lets Platforms Pay Contractors Early at Low Cost.

Related: Same-Day ACH for Platforms: How to Speed Up Contractor Payments Without Wire Transfer Fees.

Best model for growth pushes is platform-paid instant payouts#

Platform-paid instant payouts are most defensible when your goal is growth and you are willing to absorb speed costs for specific cohorts. This model prioritizes faster access to earnings over short-term margin protection.

This is more than positioning. In the March 14, 2024 Uber flexible-pay working paper, offering immediate payout access increased driver work time and earnings. Reported intent-to-treat effects were 2.4% for work minutes and 2.4% for earnings, and treatment-on-the-treated work-time effects ranged from 17.6% to 36.9%. The response was also stronger when drivers were farther from their normal weekly payday, which supports targeted rollout instead of a blanket subsidy.

Where platform-paid payouts earn their keep#

Subsidy is strongest when tied to a measurable growth outcome, not treated as a universal perk.

- Recruiting message

"Get paid right after work" is concrete. In this context, flexible pay is the option to be paid immediately after work, and Instant Pay is an on-demand, within-day withdrawal.

- Cohort-specific growth tests

Use subsidized speed for cohorts where faster pay is part of the activation or reactivation bet, then measure outcomes against a comparable non-subsidized group.

- Cleaner user experience

Free instant payout removes a fee decision at the moment workers want funds. The tradeoff is direct: each subsidized payout adds cost.

How to keep the subsidy from spreading#

Do not launch this universally on day one. Start with explicit eligibility rules, for example new activations, reactivation campaigns, or categories with persistent unfilled demand, and keep those rules auditable.

Track repeat activity, active days, and support contacts by cohort. Two common failure modes are over-subsidy, paying for behavior that would have happened anyway, and operational drag, such as manual reconciliation, multi-currency handling, or settlement delays that weaken the "instant" promise. Also plan for reliability gaps: some "instant" transfers can still be delayed because of bank or card issues.

Before launch, keep a clear evidence pack for each subsidized cohort: eligibility rules, ledger posting status, and KYC/AML status where required.

Related: Bad Payouts Are Costing You Supply: How Payout Quality Drives Contractor Retention.

For a step-by-step walkthrough, see USDC Contractor Payouts for Platforms and Stablecoin Rollout Decisions.

Best model for scale is hybrid pricing with tiered eligibility#

Hybrid pricing with tiered eligibility is often the most practical way to scale when you need growth and cost control at the same time. It keeps Same-Day Pay attractive for priority cohorts while limiting where subsidy applies.

For broader context on how payment speed is evolving across markets, the ECB has covered the topic at a market level. At an operating level, one payout policy across every segment is usually too blunt.

The tiered model that usually holds up#

A durable setup is platform-paid instant payouts for priority cohorts, worker-paid instant cash-out for the long tail, and scheduled payout fallback for exceptions.

| Model type | Best-for scenario | Fee bearer | Eligibility gates | Expected ops load | Failure-handling complexity |

|---|---|---|---|---|---|

| Platform-paid instant payouts | Priority cohorts where speed is strategically important | Platform | Cohort and policy eligibility checks | Medium to high | Medium |

| Worker-paid instant cash-out | Broad user base where margin control matters | Worker | Account and policy eligibility checks | Medium | Medium |

| Scheduled payout fallback | Exceptions, review states, or instant-transfer failures | Standard payout flow | Exception and routing status | Low to medium | High if status messaging is unclear |

If you cannot explain in one sentence why a user sees one option and not another, the policy is already too complex for scale.

Where hybrid pricing earns its keep#

Hybrid pricing is most useful when your user base is mixed and a single fee policy creates avoidable tradeoffs. That aligns with Zuora's pricing guidance that pricing strategy often involves testing, iteration, and combining approaches.

It also gives finance cleaner control: you can cap subsidy exposure by cohort while preserving a clear speed promise where it matters most.

A simple decision rule keeps execution clear:

- If a user is in a promoted cohort and passes trust checks, offer platform-paid instant payout.

- If not, offer worker-paid instant cash-out.

- If an instant request hits review or rail issues, route to scheduled payout and communicate that status directly.

The real risks are policy drift and exception confusion#

Hybrid models break when policy is not auditable in production. Run regular eligibility audits and confirm each subsidized payout has the required cohort, policy, provider, and ledger status fields before expanding access.

Exception handling is the other common failure point. If users request instant payout but are silently rerouted, support volume will look like missing payments. Treat fallback statuses as first-class product and support states, not a generic failure bucket.

For settlement-speed tradeoffs, see same-day versus slower settlement. This section also pairs with What Is Accrual Accounting? Why Payment Platforms Must Match Revenue and Payout Costs in the Same Period.

Hidden costs most teams miss beyond transfer fees#

Transfer fees are only one part of instant payout cost. The bigger hidden costs usually come from running two payout paths at once, handling eligibility and fallback states, and keeping payout status clear when timing varies.

- Dual-rail operations, not just one fast rail

Instant payouts are typically added alongside scheduled ACH, not as a full replacement. That means your team must support both paths at the same time and keep routing logic clear when a user is not on the instant path.

- Eligibility and support overhead

Instant payout access depends on setup details, such as having an eligible Visa debit card linked to Stripe. When that requirement is not met, users fall back to the scheduled payout window, and support load rises if that status is unclear in-product.

- Timing expectations and exception handling

Instant delivery is framed as real-time to a debit card, and early user reports often describe arrival within a minute or two. Treat that as directional performance, not a guaranteed SLA, and design clear status messaging for delays and reroutes.

- Program-level economics beyond fee math

On-demand access is often positioned as a workforce experience lever, including recruiting, retention, and engagement goals. If you use that framing, you still need operational tracking to separate true program impact from simple fee spend growth.

| Cost category | Owner | Trigger | Leading indicator | Mitigation checkpoint |

|---|---|---|---|---|

| Transfer fees | Finance | Each instant payout | Fee spend by payout cohort | Review fee trend against cohort usage |

| Dual-rail operations | Ops | Instant unavailable or ineligible | Growth in fallback cases to scheduled payouts | Weekly audit of routing and status reasons |

| Eligibility support load | Ops and support | Card-linking or eligibility failures | "Why can't I cash out now?" tickets | In-product checks for eligibility before request |

| Timing and exceptions | Ops and product | Delayed or rerouted payouts | Pending/exception queue growth | Trace each payout from request to final status |

Once you price this full stack, the core question is not only "what is the transfer fee." It is whether your operations and payout-state design can support faster access without creating avoidable support and reconciliation work.

Related reading: Crypto Payouts for Contractors: USDC vs. USDT - What Platforms Must Know.

Related reading: How Beauty and Wellness Platforms Pay Stylists and Therapists in Chair Rental and Employee Models.

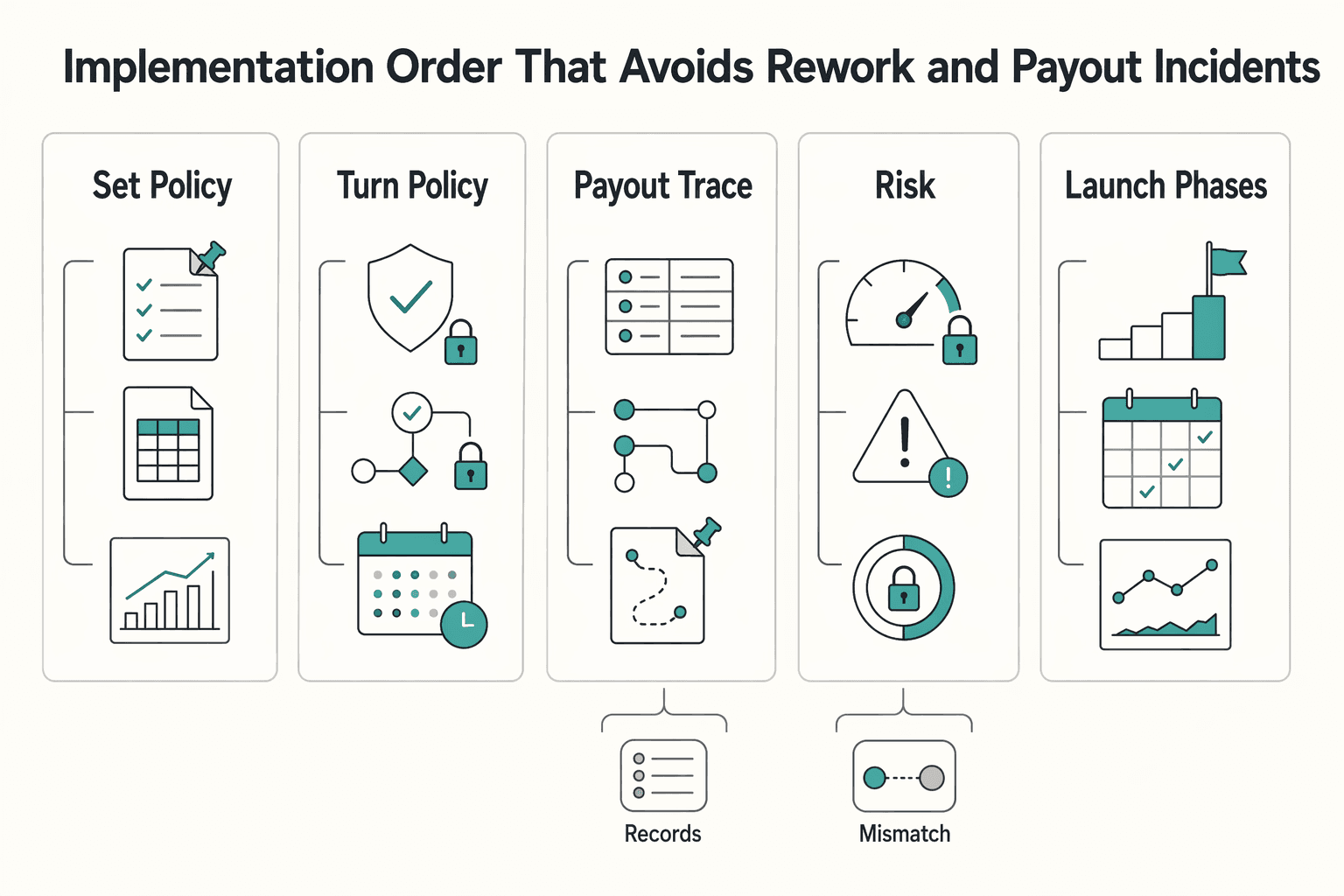

Implementation order that avoids rework and payout incidents#

Build the controls path before the speed path: set economics, eligibility, and traceability first, then expand payout speed.

Fast payouts are not just a speed feature. They combine near-real-time movement with near-continuous availability (24/7), so implementation order has to cover reliability, settlement behavior, and risk controls from the start.

| Step | Focus | What to lock before widening rollout |

|---|---|---|

| 1 | Set policy | Define who pays for speed, which cohorts get instant access, and what fallback promise applies when instant is unavailable. |

| 2 | Eligibility rules | Make eligibility machine-readable so product, ops, and finance return the same decision for the same account. |

| 3 | Traceability | Require one auditable path from payout request to provider outcome to internal record/export output. |

| 4 | Settlement model | Decide settlement approach early and align funding, reconciliation, and reporting to it before launch. |

| 5 | Failure testing | Validate retries, delays, and state changes so failures update one authoritative record instead of creating duplicate outcomes. |

| 6 | Phased launch | Expand in stages with explicit fallback states and consistent status language for users and support. |

- Set policy before wiring payout rails. Fast-payment programs can require meaningful infrastructure investment, so lock cost ownership and release policy before implementation work scales.

- Turn policy into explicit eligibility rules. If a user is not eligible for instant access, show the scheduled path before request submission.

- Treat traceability as a launch gate. If teams cannot follow the lifecycle cleanly from request through final recorded outcome, incident handling will degrade as volume rises.

- Handle settlement-model decisions early. Settlement implications are a core implementation decision, not a post-launch cleanup task.

- Test risk and failure paths before live rollout. Risk mitigation mechanisms and supporting controls are part of readiness, not an optional hardening phase.

- Launch in phases with hard fallback behavior. If instant fails, the fallback state and message should already be defined and consistently applied.

This implementation discipline aligns with the fast-payments lifecycle approach and reduces expensive rework later.

Red flags that mean your instant payout economics are off track#

If these patterns show up, treat them as economics and control issues, not normal launch noise.

| Red flag | What to check | Key point |

|---|---|---|

| High use, weak business case | Recheck who pays for faster payout, who qualifies, and when users should default to Same-Day Pay or scheduled payout. | This is a policy and eligibility problem first, not a routing problem. |

| "Missing payout" tickets that are really promise gaps | Confirm whether the payout used the fast path or a fallback path, and whether your UX promised more than that route can deliver. | Payout speed is context-dependent, so promise language must match actual routing behavior. |

| Status without traceability | Pause expansion until payout request ID, provider reference, ledger posting ID, and export package are consistently linked. | Traceability is a launch gate, not a cleanup task. |

- High use, weak business case

High adoption is not a win if you cannot justify who gets subsidized speed and why. Recheck payer policy, eligibility, and fallback defaults so teams are not treating cost leakage as growth.

- "Missing payout" tickets that are really promise gaps

When delays are reported, first verify the route used and the status language shown to the user. Also treat review-site complaints as signals that need corroboration, since review platforms can show verified interactions without fact-checking every claim.

- Status without traceability

If finance and ops cannot connect one payout across request, provider, ledger, and export records, pause rollout. Without that chain, teams can hold conflicting statuses and still lack an auditable answer.

If you want a deeper dive, read Instant Payouts: The Economics Behind Same-Day Contractor Payments.

You might also find this useful: Unit Economics for Payment Platforms: How to Calculate True Cost Per Payout.

Conclusion#

Fast payout is a trust promise, not a feature badge. simple: make the commercial rule explicit, make the user experience honest about fallback, and expand only when your records can explain every outcome.

- Lock the payer policy before you optimize anything else

Choose your payer policy, then write that choice into eligibility rules so product, finance, ops, and support all describe it the same way. That matters because traditional retail payments still commonly take one or up to a few working days, so any faster option creates a real expectation gap you need to own. Key differentiator: your first checkpoint is not rail speed, it is policy clarity. If one team thinks speed is subsidized and another thinks the recipient pays, you are already creating disputes. If you want a tighter pricing lens before launch, use Instant Payouts: The Economics Behind Same-Day Contractor Payments.

- Treat reliability and fallback clarity as part of the product

"Instant" should mean near-real-time intent, not a blanket promise that every payout lands immediately. In the evidence base, instant payments are described as retail payments shifting toward intra-day or near-real-time delivery, which is useful precisely because it leaves room for real-world variation. Key differentiator: every payout request should expose a current status, a timestamp, and a clear fallback path in user-facing copy. The failure mode is predictable: you market the fastest case as universal, a transfer takes longer, and support is left explaining something the product never disclosed. Keep rail behavior provisional until it is verified, especially if you operate in the euro area, where rollout pace has differed by country even since SEPA Instant Credit Transfers launched in November 2017.

- Scale only when traceability survives new rails, geographies, and cohorts

Broader coverage is not the same as operational readiness. The U.S. Treasury's September 2022 framing encouraged use of instant payment systems, but it also treated minimizing risks as a core policy consideration, which is the right expansion test for you too. Key differentiator: do not widen access until you can trace each payout from request, to eligibility decision, to provider outcome, to the message the user actually saw. Your evidence pack should be boring and complete: request time, decision result, status history, notification record, and final settlement path. If you are weighing which slower path is acceptable when the fast route is unavailable, compare it directly with Same-Day vs. Next-Day vs. T+2 Payouts: What Settlement Speed Actually Costs Your Platform.

Execution checklist: define payer policy, enforce eligibility logic, and require end-to-end traceability before expanding access.

Frequently Asked Questions

What does same-day or on-demand pay actually cost a platform?

Start by treating cost ownership as a policy decision, not a single universal fee line. The sources here do not support one blended number for what instant payouts cost platforms, and that is the first thing to keep straight. In practice, verify whether your provider funds and delivers transfers itself or whether your business takes on more of the timing and cash-flow burden. If you want the settlement-speed tradeoff lens, see Same-Day vs. Next-Day vs. T+2 Payouts: What Settlement Speed Actually Costs Your Platform.

Who should pay the faster-payout fee?

Pick an owner and document it clearly before launch. The supported material shows that delivery models differ, including models where a provider funds and delivers transfers while the employer's payroll process and cash flow remain unchanged, so fee responsibility can differ too. The biggest avoidable risk is unclear policy across product, finance, and support.

What is the practical difference between Same-Day Pay and on-demand pay?

Use the earned-pay definition first, then shape the product language around timing. Same-day pay is described as access to a portion of earned wages before scheduled payday, while on-demand pay is described as access to earned pay on the employee's schedule instead of waiting for payday. If your fallback path can miss the same-day promise, avoid labeling every fast payout as "instant" in user messaging.

How is earned wage access different from a payout advance?

Keep the classification anchored to money already earned. The supported sources describe earned wage access, or EWA, as same-day or on-demand access to already earned pay, not future wages. A practical check is confirming the amount reflects earned work and can be reconciled in payroll records.

What hidden costs matter most after launch besides transfer fees?

Support load and broken timing promises can become major issues. The sources describe a "pay gap" between work and getting paid, often framed against a traditional two-week pay cycle, and note that delays can increase stress and push workers toward high-interest credit or payday loans during emergencies. Operationally, Stripe's explicit checkpoint matters here: "Track payment status," because weak status visibility can turn a timing issue into a larger trust and support problem.

What should be in a minimum viable launch checklist for faster payouts?

Make a few items non-negotiable: policy ownership, a clear earned-pay definition, payment-status tracking, and clear user messaging when payout timing changes. You do not need a perfect program on day one, but you do need to verify what counts as earned pay, how payment status is tracked, and what users will see if the fast route is unavailable. The common failure mode is launching the payout button before those records and messages are dependable.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- anderson.ucla.edu/faculty_pages/keith.chen/papers/WP_InstantPa...trusted

- bis.org/cpmi/publ/d154.pdftrusted

- catalog.usm.maine.edu/content.phptrusted

- congress.gov/112/chrg/CHRG-112shrg77162/CHRG-112shrg77162...trusted

- ecb.europa.eu/euro/digital_euro/timeline/profuse/shared/pd...trusted

- fastpayments.worldbank.org/sites/default/files/2021-11/Fast%20Payment%2...trusted

- federalregister.gov/documents/2024/12/10/2024-27836/defining-lar...trusted

- govinfo.gov/bulkdata/PAI/2023/PAI-2023-JUSTICE.xmltrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Scheduled, Same-Day, and On-Demand Instant Contractor Payouts: Economics, Rails, and Rollout

Treat payout speed as a product and margin decision, not a feature race. This guide helps platform teams choose between scheduled payouts, same-day payouts, and on-demand instant payouts for contractor and creator programs based on economics, controls, and rollout order.

Same-Day vs Next-Day vs T+2 Payouts and the Real Cost to Your Platform

Payout speed is not a vanity metric. For embedded payments teams, it can affect unit economics, working capital, support load, and the level of trust sellers, creators, contractors, or suppliers place in your platform. The useful question is not "how fast can we move money?" but "which settlement tier is worth its cost once real operating friction is included?"

Bad Payouts Are Costing Your Supply in Two-Sided Platforms

Payout issues are not just an accounts payable cleanup task if you run a two-sided marketplace. They shape supply-side trust, repeat participation, and fill reliability. They can also blur the revenue and margin signals teams rely on.