Quick Answer

To calculate true cost per payout, define one stable Completed Payout unit, build a traceable data pack, tag costs across pre-payout, execution, and post-payout stages, and apply explicit overhead allocation rules consistently each month. The result should be an audit-ready per-payout measure tied to ledger, provider, FX, and compliance records, with failures, retries, and late updates handled by documented internal policy.

Why most payout unit economics break at scale#

Payout unit economics break at scale when teams track revenue and headline margin, but not the full cost layers behind each disbursement. If finance, ops, and product cannot trace margin drift back to underlying records, the metric is not ready to guide decisions.

Where the drift hides#

Revenue can rise and headline margin can still overstate reality when cost layers are missing. Unit economics only works when inclusion choices are explicit, because what you count changes the answer. If the unit is negative, adding volume increases losses instead of fixing them.

Pick the right unit for payout operations#

This article uses payout execution work as the unit, not customer acquisition performance. The scope is operating cost per payout, with explicit rules for what is included and excluded. CAC and observed LTV still matter, but they answer a different question than the operating cost of delivering payouts each month.

Build a model you can defend, not just present#

The goal is an audit-ready per-payout cost model that finance, ops, and product can run monthly and defend. That means a stable unit definition, clear in-scope and out-of-scope cost rules, and source data behind the published number. If you cannot explain movement with itemized cost layers and supporting records, the model will not hold up in review.

What to expect from the rest of the article#

The article follows that sequence. First define the unit. Then prepare the minimum data pack, estimate cost per payout, handle edge cases, apply decision rules, and finish with a copy-and-paste close checklist. The target is not a cleaner KPI slide. It is a monthly operating measure you can trust.

Define the unit before you calculate anything#

Define the unit and boundary before you run any math, or the result will not survive review. If your unit is Completed Payout, define it explicitly. Then set the True Cost per Payout boundary so scope changes do not quietly change the number.

Lock the Completed Payout definition#

Treat Completed Payout as a reporting definition, not just a product label. Write down the scope and measurement point you use, and keep that definition stable for reporting.

In true-cost work, boundary choices come first. Be explicit about the measurement point, and distinguish production-side cost from consumption-side cost in the KPI spec shared by finance, ops, and product.

Set the denominator boundary before cost math#

Set the denominator to only the records that match your written unit definition. Decide, document, and apply edge-case handling consistently so unit counts do not drift across periods.

Keep execution activity and completed units separate. If those get mixed together, average cost per unit can move for tracking reasons instead of operating performance.

Separate payout cost from CAC and LTV#

Keep payout execution economics separate from growth economics. CAC is the total cost to acquire a new customer, and LTV is estimated total revenue across that customer relationship.

Many startup models use four growth metrics: CAC, LTV, CAC payback period, and LTV/CAC ratio. Those are useful for growth decisions, but they do not define payout execution cost.

Set one reversals and reissues policy#

There is no single required treatment for reversals and reissues in this framework. If they matter in your reporting, document one internal rule and apply it consistently across periods.

That keeps month-to-month movement explainable instead of debatable.

For a step-by-step walkthrough, see ERP Integration for Payment Platforms: How to Connect NetSuite, SAP, and Microsoft Dynamics 365 to Your Payout System.

Prepare the minimum data pack before modeling#

Before you model cost per payout, build a traceable evidence pack that ties each modeled unit to execution, conversion, and compliance records. In practice, data gaps can undermine confidence faster than formula choices.

| Element | Include | Checkpoint |

|---|---|---|

| Core ledger records | Same period and payout population defined in your reporting policy; provider references used in reconciliation attached | From a sampled payout, move from a modeled unit to an internal posting to provider evidence, and back again, without changing population or period |

| Provider fee and status data | Provider fee and status data; available event-history evidence that explains payout state changes | Explain fee records and final outcomes for the same modeled payout population |

| FX quote inputs and outcomes | FX quote inputs with actual conversion outcomes; keep each route distinct, including convert-transfer-convert-back flows | Compare harmonized all-in costs by rail, corridor, and payment value |

| KYC, KYB, and AML evidence | Include review costs only where the review trigger, outcome, and linkage to the modeled payout population are clear | If a cost cannot be tied to modeled activity with a defensible rule, keep it in a separate pending-allocation bucket |

Export core ledger records and keep reconciliation references attached#

Start with your core ledger records for the same period and payout population defined in your reporting policy, then keep the provider references used in reconciliation attached.

Your pass-fail check is traceability. From a sampled payout, you should be able to move from a modeled unit to an internal posting to provider evidence, and back again, without changing population or period. This matters even more across cross-border corridors, where cost and speed can vary materially by corridor.

Pull provider fee data and status-event evidence#

Pull provider fee and status data from payout systems, and include available event-history evidence that explains payout state changes. A status snapshot alone is often not enough for review.

You do not need a perfect event taxonomy. You do need enough provider-side evidence to explain fee records and final outcomes for the same modeled payout population.

Capture FX quote inputs and actual conversion outcomes#

For cross-currency payouts, keep FX quote inputs with actual conversion outcomes. Without both, it is harder to separate provider pricing from FX effects.

Structure extracts so you can compare harmonized all-in costs by rail, corridor, and payment value, rather than averaging unlike flows together. If you run multiple rails, keep each route distinct, including convert-transfer-convert-back flows.

Build a policy evidence pack for KYC, KYB, and AML costs#

Include KYC, KYB, and AML review costs only where the review trigger, outcome, and linkage to the modeled payout population are clear. Compliance costs are a valid category, but unsupported allocations should stay out of the unit line.

If a cost cannot be tied to modeled activity with a defensible rule, keep it in a separate pending-allocation bucket until finance and ops align. Before modeling, sample payouts with compliance steps and verify that the chain is consistent across internal ledger impact, provider execution evidence, and policy review records.

If you need a benchmark for whether your payout costs are actually improving, see Payment Benchmarking for Platforms: How to Compare Your Payout Performance Against Industry.

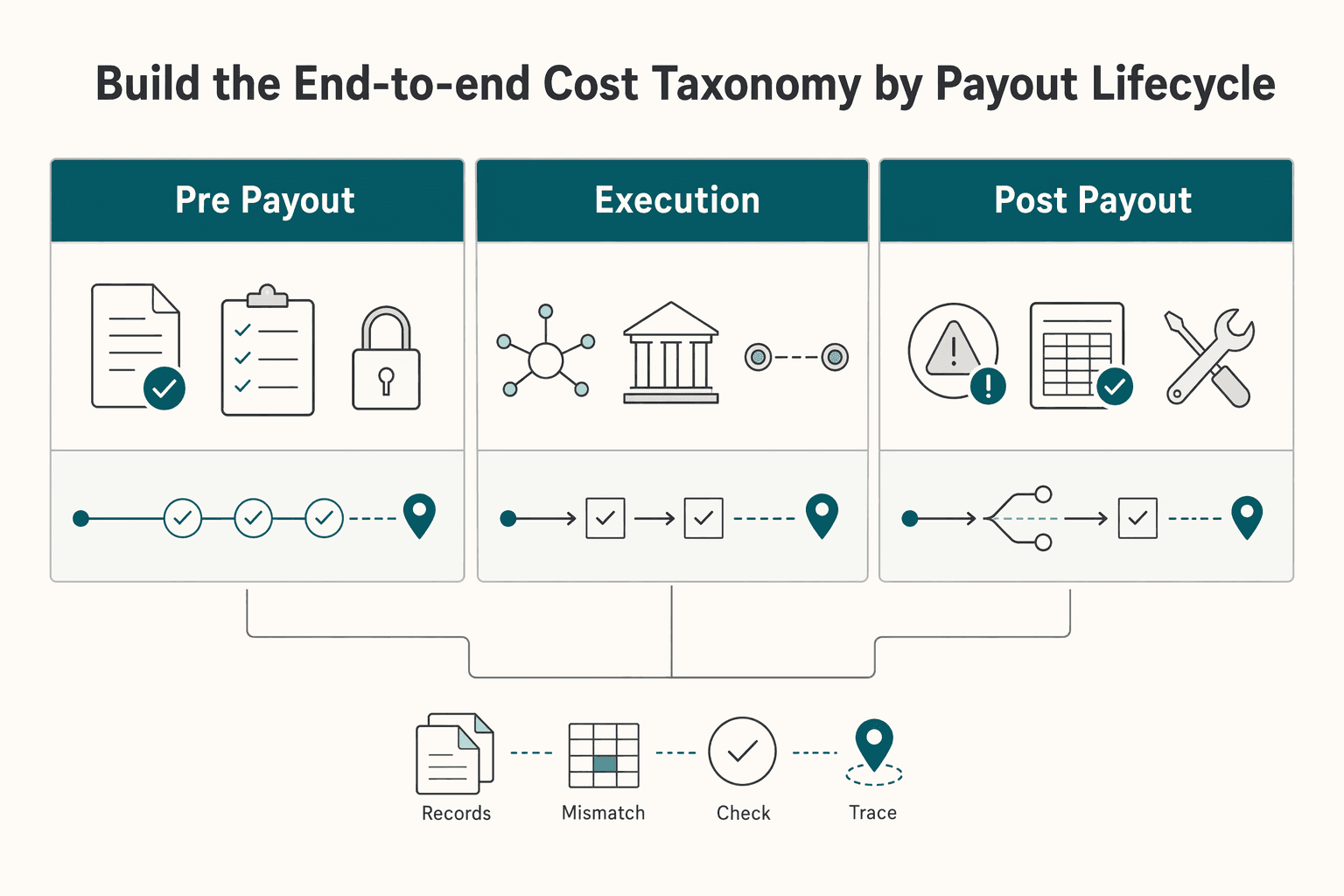

Build the end-to-end cost taxonomy by payout lifecycle#

Use three lifecycle buckets, and only tag costs you can tie to stage evidence: pre-payout controls, execution, and post-payout resolution. If a cost cannot be attached to one stage with a clear artifact, keep it out of the per-payout unit until you can defend the linkage. In this kind of true-cost model, classification errors can create more decision risk than formula errors.

The goal is not a tidy chart of accounts. It is a taxonomy finance, ops, and product can use to explain where cost enters the flow, where it stalls, and where it gets reworked.

| Bucket | What belongs here | Minimum evidence to tag it |

|---|---|---|

| Pre-payout | compliance and approval controls that gate release | review record, approval timestamp or queue history, linkage to the payout population |

| Execution | participant/provider fees, route or rail choice, transaction and settlement timing fields | fee record, route reference, transaction/settlement status and timestamp |

| Post-payout | failed processing, retries, exception handling, support and investigation work | terminal failure or exception event, retry chain, case or investigation record |

Map stages to a real transaction and settlement flow#

Anchor your stages to a rail-specific transaction and finalization flow, not a generic processing box. OCC materials document different flow views for ACH, wire transfer, and card payments, and those product differences are often where cost entry points change. World Bank fast-payments material also separates transaction-message flow, participant fee structure, and participant settlement models.

For each payout path, define four boundaries: what control happens before release, what happens at execution, when finality is reached under your policy, and what exception paths exist after the first attempt. If you run multiple rails or providers, keep those paths separate from day one.

Use one Completed Payout and one failed attempt from the same period as a validation sample. If you cannot name the artifact that marks stage entry and exit, the taxonomy is still too abstract.

Tag pre-payout controls only when they gate payout release#

Put compliance and approval handling in pre-payout only when they gate release or are triggered by the same modeled population. The rule is linkage: tie trigger, outcome, and review record back to the payout population or the account decision that directly controlled release.

Include approval handling time only when it is part of payout release. If work is broader compliance maintenance without a defensible link to the modeled population, keep it out of the unit line until allocation rules are agreed.

Checkpoint: for a sampled payout with a compliance step, you can show the review record, outcome, timestamp, and consistent linkage to the release decision.

Split execution into fee, route, and settlement fields#

Do not stop execution costing at participant/provider fees. Keep three fields together: fee records, route or rail decision, and final-status timing.

Routing is part of cost creation because the path determines how the payout is processed. World Bank treatment of participant fee structure and settlement models reinforces that different paths can carry different fee and timing behavior. You do not need to quantify every timing effect here, but you do need the field captured so later modeling stays consistent.

If you use multiple routes, keep them distinct instead of averaging unlike paths.

Checkpoint: for a sampled payout, you can show the provider or participant reference, fee record, chosen route, and the final outcome for your period policy.

Treat post-payout resolution as a first-class cost bucket#

Treat post-payout resolution as explicit, not residual. Include failed processing, retries, exceptions, and the support or investigation work needed to close them. This aligns with treating product-specific risk paths and control checkpoints as part of the operating model.

Cost this as an incident chain, not raw event volume. One payout can produce multiple operational events or notes, but it should resolve to one coherent exception record to avoid double counting.

Checkpoint: each post-payout line should tie to a terminal failure event or an exception case with retry chain and resolution notes. Once these tags are stable, allocation gets cleaner. You move from arguing about cost type to allocating shared overhead across defined lifecycle buckets with evidence behind each one.

For a broader cost model beyond payout unit economics, see How to Calculate Payment Processing Fees: A Total Cost of Ownership Framework for Platforms.

Allocate shared overhead with accounting rules people can defend#

Allocate shared overhead explicitly, with documented rules, or your True Cost per Payout will stay easy to challenge. If another operator cannot trace your logic and reproduce the result, the allocation rule is not ready.

Keep overhead explicit in the unit-cost view#

Keep overhead explicit instead of treating it as a catch-all. Itemize named operating expenses such as rent, technology, marketing, insurance, and non-billable staff salaries, and state why each line is overhead in your model.

Keep compensation, overhead, and profit in distinct buckets rather than blending them.

Define allocation rules by cost pool and version them#

Pick the rule that best matches each cost pool, then keep it stable for the period.

Version every rule change with an effective date, cost-pool name, and reason for change. Without that history, trend movement can reflect rule drift instead of operating performance.

Keep support and tooling costs visible#

Treat platform support and tooling as explicit allocations, not miscellaneous. A defensible evidence pack is simple: the operating-expense lines you included, the allocation logic you applied, and the final unit-cost output.

Reject rules you cannot defend quickly#

Apply a hard review test: if you cannot explain a rule clearly in one minute to finance, ops, and product, do not use it. If the unit-cost math does not work at low volume, scale is unlikely to fix it. Favor fewer rules with stronger evidence over a more complex model that no one trusts. Here, defendability beats cleverness.

Adjust the model for failures retries and exception paths#

Treat any rules you use for True Cost per Payout and Completed Payout as internal policy assumptions until you validate them with appropriate operational sources.

Separate non-success work from successful outcomes#

No approved excerpt here confirms a required bucket design for failed attempts, retries, or exception handling. If you separate these buckets, present that as a reporting choice, not a grounded benchmark.

Track retries as visible workload#

The provided evidence does not quantify retry burden or define required retry fields. Keep retry-tracking decisions explicit as internal assumptions until stronger source support is available.

Keep exception queues explicit and auditable#

Keep exception-queue details such as causes, ownership, and closure workflows as process hypotheses unless your internal records validate them.

Investigate cost movement with bucket-level evidence#

Before you draw pricing or operational conclusions, validate source authority first: inclusion in an NLM/PMC database is not an endorsement, and publication metadata (journal/date/pages/DOI) should be checked separately from operational applicability.

Related reading: SAP Integration for Payment Platforms: How to Connect Your Payout Infrastructure to SAP ERP.

Compare rails and routing decisions with corridor-level evidence#

Once failure costs are visible, routing decisions get clearer. Use corridor-level rows to compare options, because blended averages can hide tradeoffs. Keep rail type, currency path, and funding path separate so fees, timing, and rework are evaluated on the same unit.

Build the table at decision grain#

Create one row per corridor, provider, rail, currency path, and funding path for the period. Keep ACH, wire transfer, and real-time payments separate rather than combining them in one rail bucket. The OCC handbook treats them as distinct areas, so your operating view should too.

| Rail class to separate | Why keep it separate | Minimum checkpoint field |

|---|---|---|

| ACH | Dedicated product section in OCC handbook | Terminal status timestamp used for timing |

| Wire transfer | Dedicated transaction and settlement flow section | Provider reference plus funding release timestamp |

| Real-time payments | Product-specific risk coverage in OCC handbook | Terminal provider status plus exception reason code |

Then add fields for routing analysis where your own records support them: effective cost per completed unit, failure rate, time to final status, and rework burden. Include retry and exception allocation from the prior section and manual handling cost if assigned. Before you act on the table, sample rows and confirm traceability to ledger entries, provider status data, webhook history, and parent payout IDs.

Split Provider Routing into FX and non-FX views#

If your operation includes both native-currency payouts and payouts that require a Foreign Exchange (FX) Quote, run separate cuts for each view. This keeps routing comparisons readable and avoids blending distinct processing paths.

For FX-required rows, keep quote ID, quote timestamp, payout creation time, execution time, source and destination currency, final converted amount, and whether the original quote was used or replaced. If a row cannot be tied back to stored FX records, mark it incomplete for routing decisions.

Test batched release versus single payout release#

Treat batching as a scenario to test, not a default assumption. Compare batched and single release for the same corridor and payout size band, then review fee, completed count, delay to final status, and rework or exception volume.

Capture comparable timestamps for both paths: creation, approval, release, provider acceptance, and final outcome. This is a practical minimum to evaluate where delay may enter the flow.

Assess VBA funding paths only where evidence is complete#

If Virtual Accounts (VBA) are enabled, evaluate them as a separate funding path for specific flows. Compare like-for-like cohorts, same corridor, provider, and period, and track funding arrival time, unmatched cash incidents, manual interventions, payout holds, provider-reference match rate, and downstream delay. If multiple operating changes happened at once, report VBA results as an observed association rather than a causal routing conclusion.

Route decisions should be based on failure-adjusted corridor evidence, not fee cards alone. Keep the monthly table concise enough for management reporting and complete enough for third-party risk review and internal audit.

If payout timing decisions depend on liquidity, Cash Flow Forecasting for Payment Platforms for Payout Go/No-Go Decisions covers that side of the model.

Before locking corridor routing policy, run a quick sensitivity check in the Payment Fee Comparison to validate effective-cost assumptions.

Set batching and threshold rules that reduce cost without harming reliability#

Use your corridor table as policy input. Make Payout Batch mandatory only where your own evidence shows lower cost per payout with acceptable operational outcomes, and keep it optional or single-release where results are less consistent.

Set rules at the same decision grain you used for routing#

Set policy at the same unit of analysis you used for routing, rather than with one global batching rule. Keeping the same unit of analysis preserves comparability with your evidence.

| Rule row field | Include |

|---|---|

| corridor and provider, or provider group | Include in each rule row |

| payout size band | Include in each rule row |

| cutoff window and release timing | Include in each rule row |

| default release mode | mandatory batch, optional batch, or single release |

| current True Cost per Payout | Include current True Cost per Payout |

| completed volume for the review period | Include completed volume for the review period |

| exception rate and time to final status | Include both measures |

| baseline measurement date and policy owner | Include both fields |

Those are the minimum fields for each rule row.

Only promote a rule to production when it traces to a documented baseline measurement and underlying operational evidence.

Tie thresholds to per-unit economics, not instinct#

Threshold decisions should follow per-unit economics. If low-value payouts add substantial unit volume but weak economics, they can degrade break-even dynamics even when headline fees look stable.

Use two checks in threshold review:

- does this value band have a True Cost per Payout that is out of proportion to the value delivered?

- does it add a large share of completed volume without improving overall economics?

If both are true, review thresholds before treating pricing as the only lever.

Also include usage-based costs where request volume affects spend. In call-based pricing, each additional request contributes to total cost, so extra status checks, retries, or reconciliation calls can materially change true unit cost.

Keep threshold and batching logic under the same policy ownership for consistent approvals. For deeper threshold design, see Publisher Payment Thresholds: How to Set Minimum Payout Limits That Reduce Cost Per Transaction.

Change batch intensity based on volume and exceptions#

Adjust batch intensity as a cost-performance-reliability-security tradeoff, not as a fixed rule. Use current volume, exception patterns, and operational stability as inputs when deciding whether to batch more, batch less, or use single release.

Treat larger batches as higher-consequence decisions. They can lower cost per unit in some cases, but they can also increase the impact of operational failures.

Review against a baseline and refresh on a regular cadence#

After policy changes, record a baseline measurement and compare future periods against that same starting point. Refresh on a regular cadence so policy changes are measured rather than assumed.

Keep the success criterion explicit: lower unit cost with stable completion quality. If cost drops while exceptions, holds, or delay worsen, narrow or roll back the rule by corridor.

Run a monthly close sequence with clear owners and checkpoints#

A good model still fails if the close process is loose. A practical approach is to publish the final KPI pack only after four checkpoints are complete: period evidence is frozen, variances are assigned, accruals are posted, and tax-reportability review is recorded. This helps keep payout-cost reporting defensible during close.

| Checkpoint | What to do | Key record |

|---|---|---|

| Freeze period evidence | Lock one reporting window and pull the same core records in the same order each month | Period label, extraction timestamp, and version name |

| Reconcile variances | Log each variance with one clear owner and consistent cause categories | Owner, cause category, expected resolution date, and whether current-period KPIs are affected |

| Post accrual adjustments | Use accrual accounting so events are recognized when they occur, not only when cash moves | Tie material adjustments back to dated support |

| Tax-reportability review | Record payment classification and document status without broad distribution of raw tax IDs or document images in KPI reporting | classification reviewed, reportability pending, and tax form on file |

Freeze the period and extract the same evidence every month#

Lock one reporting window, then pull the same core records in the same order each month.

Require each extract to carry a period label, extraction timestamp, and version name so finance and ops are working from the same cut. If source data updates after cutoff, flag it as post-cutoff input rather than silently replacing close files.

Reconcile variances and assign each break to one owner#

Reconcile payout activity across systems, then log each variance with one clear owner. Use consistent cause categories so unresolved items can be tracked to closure instead of sitting as general investigations. Before signoff, each open item should show owner, cause category, expected resolution date, and whether current-period KPIs are affected.

Post accrual adjustments before publishing final KPIs#

Post close adjustments using accrual accounting so events are recognized when they occur, not only when cash moves. Apply accruals after variance review is stable enough to support period matching, then tie material adjustments back to dated support.

For a deeper refresher on period matching, see What Is Accrual Accounting? Why Payment Platforms Must Match Revenue and Payout Costs in the Same Period.

Add a tax-reportability checkpoint without exposing PII in ops reporting#

Include a monthly checkpoint for payment classification and document status where federal reporting may apply, because certain vendor or payee payments are reported annually to the IRS.

Track operational status fields such as classification reviewed, reportability pending, and tax form on file, rather than broad distribution of raw tax IDs or document images in KPI reporting.

Avoid hardcoded assumptions. Corporate-payee exclusions can have exceptions, including attorney-services exceptions noted in guidance, and FAQ text may not fit every fact pattern. For Form 1099-K, IRS fact sheet FS-2023-06 (March 2023) is date-stamped and discusses 2022 transition-year details, including $20,000 and more than 200 transactions and delayed implementation of the more than $600 threshold for that year. If FAQ language and taxpayer-specific law application differ, the law controls.

Spot the reporting mistakes that make costs look better than reality#

The biggest risk after a clean close is cosmetic reporting: mixing unlike metrics so payout execution appears healthier than it is. The fix is straightforward. Keep each metric tied to its own purpose and keep cost inclusion rules stable.

Separate payout cost from Gross Margin#

Do not use Gross Margin as a proxy for payout efficiency. Gross margin reflects overall business economics, while True Cost per Payout should reflect per-transaction execution cost. Keep them separate so changes in sales mix or pricing do not mask operational cost movement.

Keep CAC Payback Period out of payout reporting#

Treat CAC Payback Period as a growth metric, not an execution-cost metric. CAC has its own formula, Sales + Marketing Spend / New Customer Acquired, and answers a different question than payout performance. Publish separate scorecards: one for growth, CAC and LTV, and one for payout unit economics.

Include hidden and rework costs in the numerator#

Excluding real cost drivers makes per-unit costs look artificially low. Unit economics is understated whenever costs are omitted, similar to excluding returns, discounts, or payment processing fees in other models. Use one written rule that consistently includes recurring execution and rework costs in the numerator.

Handle delayed updates with one period rule#

Delayed updates can make a month look cleaner than it was. To keep reports trustworthy, define one documented period-close rule for late-arriving updates and apply it consistently each month. If finance and operations use different timing rules, unit-cost reporting will drift.

Related: Spend Analytics for Platforms That Turns Payout Data Into Cost Decisions.

Execute a first 30-day implementation plan#

Once you have one period-close rule, spend the next 30 days making the metric reviewable, not optimized. Use this as a working sequence, not a universal standard. Hold routing or threshold changes until finance, ops, and Internal Audit can trace one number back to the same definitions and records.

Lock the policy in Week 1#

Document how you define Completed Payout, your cost buckets, and your allocation approach. Keep it short, versioned, and dated. Your checkpoint is simple: can finance and payments ops read it and reach the same denominator and cost boundary without a meeting?

Treat naming as a control, not admin overhead. Payment-system work is vulnerable to inconsistent terminology, so if a rule cannot be defended in review, remove it until it can.

Connect the records in Week 2#

Extract payout activity from your Ledger and provider systems, then join records with the same references used in reconciliation. Treat the Ledger as the financial account record, not a side report. Check whether your event history is complete enough to explain final states and exception paths.

Verify coverage before speed: sample payouts and trace each one across ledger entry, provider status, and event history. Then review retries and exception handling so blocked duplicates do not hide operational review work.

Publish a draft view in Week 3#

Publish a draft metric view with provider-routing cuts and an explicit exception-cost overlay where relevant. Keep the first cut narrow and readable. Look for distortions, such as a segment appearing cheap only because failure handling sits outside the model.

Formalize governance in Week 4#

Set the monthly review cadence, provisional KPIs, and escalation triggers for threshold, routing, and batching decisions. Keep trigger values tailored to your institution's risk profile. Lock ownership now: who prepares the pack, who challenges it, what review scope applies, and what gets escalated into management and board reporting when costs move without a clear cause.

Turn this into your monthly operating checklist#

Use this as a monthly close discipline, not a dashboard refresh. If a number cannot be tied to source records or a documented policy, keep it provisional until the gap is resolved.

Lock one stable definition#

Lock one stable definition for your primary unit metric and publish it in the KPI pack every month. If you use Completed Payout internally, treat it as an internal reporting label; this source set does not provide a universal payout definition.

State what is included, what is excluded, and how reporting-period cutoffs are handled. That keeps finance, ops, and product on the same denominator.

Reconcile the core control set#

Before finalizing results, reconcile the inputs that drive blended economics: total marketing spend, fully loaded fulfillment or servicing costs, and customer value. A recurring failure is tracking these in separate views instead of connecting them.

Maintain a variance list with item count, value impact, and owner for each open break. If records conflict, publish with a caveat or hold the metric as draft.

Calculate the fully loaded number#

Calculate true cost per unit as a fully loaded number, not a settled-fees-only number. Include every cost that touches the unit, not only obvious line items.

This is where unit economics often break: headline margin or in-platform ROAS can look healthy until hidden costs are included. Keep a view that shows where every dollar goes per unit or order.

Apply allocation rules consistently#

Apply Accrual Accounting and your allocation rules consistently, and keep a changelog when rules change. Shared costs belong in the core metric only when the allocation driver is documented, repeatable, and reviewable.

Include the current method, effective month, and what changed from the prior version. For period-matching context, use this accrual accounting guide.

Review corridor-level routing outcomes#

Review corridor-level Provider Routing outcomes (where enabled) and make one explicit monthly action. Treat payout-specific routing, batching, threshold, and settlement assumptions as internal and data-dependent; validate corridor-level payout rules against your own operational records.

Do not treat visible fee movement as the whole story. Pair route results with loaded economics and documented exceptions from the same period.

Share one final pack#

Share one final pack across finance, ops, and product with assumptions, caveats, and next-step decisions on page one. The pack should show where economics break, not only whether a top-line KPI moved.

Include the current metric definition, loaded-cost view, open reconciliation breaks, any Accrual Accounting rule changes, and the operating action selected from routing review.

If payout cadence is driving cost or exception volume, Payment Scheduling for Platforms: How to Build Flexible Payout Calendars for Contractors is the more practical next step.

Frequently Asked Questions

What costs should be included in True Cost per Payout?

Include costs directly tied to your defined payout unit first. Add shared-cost allocations only when the rule is clearly documented, repeatable, and supported by the same data each cycle. If a treatment cannot be reproduced, keep it outside the core per-unit number.

How should we define a Completed Payout when statuses are asynchronous?

There is no universal definition in this source set. Choose one unit definition, document the measurement point and boundary, and apply it consistently over time. Keep the supporting data ready so stakeholders can verify how counts were produced.

Do compliance costs like KYC and AML belong in per-payout economics?

Include compliance review costs only when the trigger, outcome, and linkage to the modeled payout population are clear. If the treatment cannot be supported with consistent data, report those costs in a separate view or pending-allocation bucket. Do not blend unsupported allocations into the core per-unit figure.

How do failed payouts and retries change the metric in practice?

In general, failed payouts and retries can worsen per-unit economics when costs rise without improving outcomes. Keep any failure and retry treatment explicit as an internal reporting choice until validated.

How can we compare providers fairly across corridors with different FX behavior?

Use the same unit definition and measurement approach across every option you compare. Keep corridor, provider, rail, currency path, and funding path separate rather than blending them. Bring supporting FX quote inputs and actual conversion outcomes so the comparison is decision-ready.

Should payout thresholds and batching be optimized for cost, speed, or both?

There is no universal optimization rule in the approved sources. Treat thresholds and batching as a policy tradeoff, and base decisions on your unit-economics framework with explicit, repeatable criteria. Review changes against a baseline and favor lower unit cost only when completion quality remains stable.

What is the minimum data required to produce an audit-defensible monthly number?

The approved sources do not define a minimum payout data schema. You need a clearly defined method and enough supporting data for stakeholders to follow, challenge, and reproduce the result. At minimum, the article calls for traceable records across ledger activity, provider data, and other linked evidence used in the model.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cms.gov/files/document/ahead-tech-specs-v30.pdftrusted

- economics.mit.edu/sites/default/files/2022-11/wpiea2022217-pri...trusted

- energy.gov/sites/prod/files/2014/05/f15/tech_brief_true...trusted

- epa.gov/sites/default/files/2017-12/documents/epaccm...trusted

- federalreserve.gov/publications/files/usbranch.pdftrusted

- hbs.edu/ris/Publication%20Files/Du_Huang_Scharfstein...trusted

- irs.gov/pub/taxpros/fs-2023-06.pdftrusted

- jud.ct.gov/LegalResources/Docs/LJDocs/CTReports/FullVol...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: