Quick Answer

Set your publisher payment threshold minimum payout limit by segment instead of using one platform-wide floor. Start with 90-day rail and currency data, then enforce release order: eligibility checks, compliance status, tax-document status, and only then threshold evaluation. Keep rules method-specific because the article shows EFT, check, and wire can follow different payout behavior. Launch with audit logs and rollback criteria based on fee-to-payout ratio, complaint growth, and failed retries.

How to set payout thresholds without creating payout confusion#

Set payout minimums to manage transaction costs, but only if recipients can still predict when they will be paid. If thresholds are unclear or scoped poorly, you may lower fee drag while increasing rollover balances and "where is my payout?" pressure on operations.

The goal is straightforward: set a publisher payment threshold minimum payout limit that protects unit economics without degrading recipient experience. In many publisher programs, payment is released only after a confirmed or payable balance reaches a minimum, and balances that miss the minimum roll into the next cycle.

One global number is rarely practical because threshold rules vary by payment method, currency, and network scope. For example:

- Awin lists minimums of £20, €20, and $20, and processes payments twice per month.

- Rakuten Advertising applies a network minimum of 50 currency units per network across marketing channels in the account.

- Google Payments recommends at least $100 for wire transfers because wire fees can exceed $50.

These are not copy-paste defaults. They show why threshold policy has to match your payout setup.

This guide is for finance ops, product, and engineering teams running marketplace, contractor, affiliate, or creator payouts. You need a rule that is efficient to operate and easy to explain when a recipient asks why funds were held.

Before you change thresholds, verify what actually blocks release. It is not always balance alone. Some programs require complete tax and bank details for on-time payment, and some require forms such as W-8 or W-9 to determine withholding. Payment method can also change arrival timing, so recipients with similar balances may still be paid at different times.

A common failure mode is setting the minimum above what recipients typically earn in a cycle, which can delay payouts. Rakuten warns that thresholds far above typical monthly commissions delay payment. Amazon KDP shows the same pattern operationally: balances can keep rolling until the minimum is exceeded, and for check or wire payments, payment occurs 60 days after the end of the month in which the threshold is met.

In practice, define scope first, set decision rules instead of one global threshold, implement controls in your ledger and payout release flow, and monitor fee impact and payout exceptions each cycle.

If you want a deeper dive, read Affiliate Network Payment Software: How to Evaluate Publisher Payout Infrastructure.

Define threshold scope before touching a number#

Set scope first, then set the number. A threshold is only reliable when you define exactly which balance bucket it applies to.

- Map scope dimensions before picking an amount.

Write down how your rule applies across the dimensions your program uses, for example account, network, currency, marketplace, and payout rail such as PayPal, Direct Deposit, Wire Transfers, and Check Payments. The same threshold value means different things when scope changes.

- Use live policy models to pressure-test your scope.

Rakuten Advertising uses a network-level minimum of 50 currency units per network across account channels, including check, direct deposit, and PayPal, with a documented Brazil-network exception. Amazon KDP scopes differently: royalties accrue by marketplace and local currency, EFT has no threshold, and check and wire thresholds apply after applicable withholding. Awin requires a threshold and defines it by payout currency (£20 / €20 / $20) with rollover when the cutoff is missed. Impactbytes presents threshold as optional and supports carryover when not reached.

- Document payout-release checks alongside threshold policy.

In some programs, release involves checks beyond commission accrual, including account setup requirements. For each threshold rule, record both the threshold policy and the release checks in your policy record and recipient-facing help text.

- Standardize threshold terms before launch.

Keep one shared vocabulary for terms such as confirmed commission, payable balance, carryover, network minimum, marketplace threshold, and cycle cutoff so hold and release outcomes are described consistently.

Gather the input pack before you set limits#

Do not debate a threshold until you have a compact input pack for the rail and currency scope you defined. The point is to separate cost drivers, recipient friction, and release blockers before anyone argues about the number.

| Input area | What to capture | Why it matters |

|---|---|---|

| Payout activity by rail and currency | Payout count, average payout size, failure and retry rates; statuses split into pending, paid, failed, and canceled | Blending rails or currencies into one average hides the real failure and fee pattern |

| Minimum evidence pack | Current rail-level fees and reconciliation exceptions; payout-delay ticket categories; representative "where is my payout?" complaints | Separates cost drivers, recipient friction, and release blockers before debating the threshold |

| Compliance readiness | KYC, business-entity and beneficial-owner verification where required, and AML coverage; segment as fully verified, partially verified, and blocked | If verification completion is weak, changing the minimum will not fix release timing |

| Tax-document dependencies | W-9 and TIN readiness for U.S. persons; W-8 BEN for foreign persons; whether a payment settlement entity handles Form 1099-K; onboarding validation lag up to 48 hours | Tax and payout profile checks can delay release expectations even after balance is sufficient |

Step 1#

Pull a consistent lookback window of payout activity by payout rail and currency, not a platform-wide total. For each segment, capture payout count, average payout size, and failure and retry rates. If available, export by transaction type and date range, then split statuses into pending, paid, failed, and canceled.

Checkpoint: totals should tie to your ledger or reconciliation output, and failed payouts should be tracked as a separate exception stream. If you blend different rails or currencies into one average, you lose the real failure and fee pattern.

Step 2#

Build a minimum evidence pack before proposing any threshold value. Include current rail-level fees and reconciliation exceptions, plus payout-delay ticket categories and representative "where is my payout?" complaints if you track them.

Keep the pack lean but mandatory for every threshold decision. If one rail or currency is driving complaints, treat that as a segment issue. Published threshold models can be currency-specific, for example £20 / €20 / $20, rather than global.

Step 3#

Add compliance readiness by segment: KYC, business-entity and beneficial-owner verification where required, and AML coverage. Reaching a balance threshold does not guarantee payout release if verification or account holds are unresolved.

Use a simple cut per segment: fully verified, partially verified, and blocked. If verification completion is weak, changing the minimum will not fix release timing.

Step 4#

Confirm tax-document dependencies before modeling payout timing. For U.S. persons, verify W-9 and TIN readiness. For foreign persons, confirm W-8 BEN requirements with the payer or withholding setup. For card or third-party network flows, confirm whether a payment settlement entity handles Form 1099-K reporting.

Also log onboarding validation lag in your flow. If tax and payout profile checks can take up to 48 hours, include that delay in release expectations.

For a step-by-step walkthrough, see Understanding Payment Platform Float Between Collection and Payout.

Benchmark market norms without copying competitors#

Benchmarking gives you guardrails, not a default threshold. Retrieved policies differ by network, rail, marketplace, and configurability, so there is no single default you can safely lift.

Step 1#

Build a comparison table that separates documented facts from unknowns so assumptions stay visible.

| Platform | What is known from retrieved sources | What is configurable | What is still unknown from retrieved sources |

|---|---|---|---|

| Rakuten Advertising | Network minimum threshold is 50 currency units for each network, applies to every marketing channel, and applies regardless of whether payment is by check, direct deposit, or PayPal. Brazil network commissions are exempt. | No publisher self-configuration is stated in the retrieved page. | Whether publishers can set higher thresholds, how exceptions beyond Brazil work, and how failed or returned payouts affect release timing. |

| Awin | Publishers must set a minimum payment threshold. Published minimums are £20 / €20 / $20. Payments are processed twice per month. | Publishers can adjust payment threshold and frequency at any time. | Rail-specific differences, exception handling, and what happens when compliance or payout-profile issues delay release. |

| Amazon KDP | EFT payments do not have a threshold. For check and wire, there is a minimum threshold in each marketplace. Payment occurs 60 days after the end of the month in which royalties meet the threshold. | Configuration is not stated in the retrieved policy excerpt. | Marketplace-by-marketplace threshold amounts in this comparison, and whether authors can tune thresholds themselves. |

| Trackier | Retrieved material defines payout threshold generally and documents publisher-specific payout setup, including different payouts for different publishers. | Publisher-level payout customization is documented. | A verified platform-wide default minimum threshold is not shown in the retrieved pages. |

| Impactbytes | Support page says there is no required minimum threshold and unpaid earnings carry over to the next month if a threshold is not met. Page shows last updated March 4, 2024. | Threshold appears optional from the retrieved page. | Currentness beyond that update date, plus rail, currency, and exception specifics. |

Verification point: for every row, log the source URL, the rule scope, and the unknowns. If scope is unclear, whether network-level, marketplace-level, or rail-level, do not treat the number as directly comparable.

Step 2#

Read the source type before you read the threshold number. Rakuten's policy sits in a Publisher Help Center, while Awin's page sits in a Partner Success Center with self-service threshold and frequency controls.

That changes what you can infer. Both pages state threshold rules, but the retrieved pages do not provide full edge-case handling details. If you copy only the headline number, you can import the wrong policy shape.

Step 3#

Use benchmarks to reject bad fits, then set your own rule from your operating data. If your mix is mostly EFT, KDP's no-threshold EFT policy can support a lower floor. If your mix includes more checks or wires, Rakuten's 50-unit network minimum and KDP's method split can support a higher floor.

The common failure mode is copying a threshold from a different payout setup. Awin allows threshold and frequency changes, but if your team is not ready to support self-service variance, that flexibility can add support overhead. Use external policies to pressure-test your draft, then choose the threshold that fits your payout rails and operations.

Need the full breakdown? Read How to Build a Payment Sandbox for Testing Before Going Live.

Choose threshold logic by segment not one global rule#

A segmented policy is usually more durable than one number for every recipient. A single floor can break down quickly when your mix includes low-cost rails, high-cost rails, currency differences, and network-specific exceptions.

Treat the threshold as a base rule plus conditional overrides. That matches how payout conditions vary across methods, markets, and risk.

Step 1 group segments around real cost and rule differences#

Start with one base rule, then split only where cost, availability, or release behavior changes. Practical first segments are payout rail, currency, network or market, and risk profile.

| Segment lens | Grounded evidence | Practical policy action |

|---|---|---|

| Rail | Amazon KDP says EFT has no threshold, while check and wire do. Liftoff examples show ACH at USD $50.00 minimum with USD $0.75 fixed fee, and wire at USD $1000.00 minimum with USD $15.00 fixed fee. | Avoid one shared floor across low-cost and high-cost rails. |

| Currency | Awin lists minimums of £20 / €20 / $20 and default thresholds including 100 CAD / PLN and 500 SEK / NOK when no threshold is set. | Segment by currency when payout economics differ. |

| Network or market | Rakuten applies a 50 currency unit minimum per network and documents a Brazil Network exemption. | Add explicit network-level exceptions where rules differ. |

Verification check: each segment should have a clear reason, such as cost, currency behavior, market rule, or risk. If not, remove it.

Step 2 set decision direction before exact numbers#

Set the rule shape first, then tune the values from your payout data. If fixed transfer cost is high and payouts are frequent, a higher floor can reduce fee drag. If faster access to funds matters more for a segment, use a lower floor and tighter cycle controls.

KDP shows why method-level logic matters: EFT has no threshold, check and wire do, and payment is 60 days after month-end once royalties meet threshold. Separate rail logic first, then tune speed and floor by segment.

Step 3 create exception lanes only when explicit#

Add exceptions only when they are documented or intentionally approved. Rakuten's Brazil case is explicit: Brazil network commissions are exempt from the minimum threshold, and payment options depend on country and advertiser network. Selecting PayPal can block payments for Brazil-network commissions.

Use that same standard in your own policy: named market exceptions, named network restrictions, or clearly approved internal tiers with defined qualification rules.

Step 4 define threshold ownership and controls#

Decide where thresholds are self-set versus platform-enforced by segment. Awin requires publishers to set a threshold, with stated minimums and defaults, and says balances roll over when the threshold is not met. Impactbytes states there is no required minimum threshold.

Document each segment in a short policy matrix: segment, threshold owner, configurable or enforced, rail and currency scope, exceptions, rationale, and review trigger. That keeps product, finance, engineering, and support aligned on why one segment releases differently from another.

Related: Invisible Payouts: How to Remove Payment Friction for Contractors Without Sacrificing Compliance.

Set explicit decision rules for raising or lowering thresholds#

Set decision rules before you change thresholds. Otherwise fee pressure can push you into changes that overlook holds, retries, or communication gaps.

Step 1 define trigger inputs before you change anything#

Use a short, named trigger set per segment so finance and product review the same signals. Practical inputs can include fee-to-payout ratio, payout volume spikes, complaint rate, and failed payout retries.

Include payout timing impact in every review, not just transfer cost. If a recipient does not meet a threshold, payment can roll to the next cycle, so a higher floor can increase latency by design.

Verification point: before approval, confirm one reporting pack can show transfer fee totals, payout count, threshold-related support tags, and retry or return reasons by rail. If any of that is missing, postpone the change.

Step 2 write a rollback rule that favors recipient experience when the tradeoff turns bad#

Make rollback explicit. A practical internal approach is to return a segment to its prior threshold when recipient support pressure appears to outweigh expected savings, log the reason, and re-test only after improving recipient messaging.

Treat this as an internal control, not a universal formula. Payment timing already varies with transaction timing, invoice closure, and payment criteria, so threshold changes can be misread as platform failure if policy language is unclear.

Also check non-threshold blockers before you blame the new floor. Reaching a payment threshold may still not release funds when holds, tax-document requirements, or bank-detail approvals are unresolved.

Step 3 require approval and a durable audit trail#

Handle threshold updates as controlled policy changes. Set clear approval ownership, such as finance plus product, so cost and reconciliation impact on one side and recipient UX impact on the other are both owned.

Maintain a durable change log with segment, old threshold, new threshold, rationale, expected effect, launch date, and rollback owner. That keeps decisions auditable when reporting workflows later require corrections, recipient statements, TIN handling, backup withholding, or penalty review.

Step 4 place freeze windows around tax and reporting deadlines#

Pause threshold changes during filing and correction windows. Freeze periods should align to your reporting calendar, especially for U.S. reporting and cross-border account workflows.

Document the dates your team operates against: January 31 (Form 1099-NEC), February 28 or March 31 (Form 1099-MISC by filing method), and April 15 for FBAR with automatic extension to October 15. FBAR reporting is tied to a $10,000 aggregate foreign-account value trigger, while FEIE is computed on Form 2555 and depends on residency or physical-presence tests. Keep freeze-window length platform-specific, but tie it to real filing and review work.

Build compliance and tax gates into release logic#

Treat threshold as a late check, not the first one. In payout logic, balance alone is often not a reliable release signal.

| Release gate | Grounded check | Hold or timing note |

|---|---|---|

| Eligibility | Define a clear internal sequence for payout release before balance is evaluated | Treat release as eligibility first and balance second |

| Identity and AML checks | Identity verification is part of AML controls under a Customer Identification Program | If threshold holds are mixed with AML or tax holds under a generic pending review, support will misdiagnose delays |

| Tax-document status | Form W-9 provides a correct TIN for IRS information reporting; Form W-8 BEN is submitted when requested by the payer or withholding agent | Model submitted and accepted separately; tax and payout profile validation can take up to 48 hours |

| Threshold | Public publisher policies show thresholds can apply after withholding and by payment method in local marketplace currency | Calculate eligibility on the right post-withholding and method-specific basis |

Step 1 enforce gate order before you evaluate balance#

Define a clear internal sequence for payout release: eligibility, identity and AML checks, tax-document status, then threshold. A recipient can meet the threshold and still stay on hold when onboarding, review, or tax setup is incomplete.

That sequence aligns with documented regulated workflows: identity verification is part of AML controls under a Customer Identification Program, and procedures are meant to support a reasonable belief in true customer identity. Some marketplace programs also require payout-account and tax-form setup before payment can be received. Treat release as eligibility first and balance second in your own policy design.

Verification point: each hold reason should map to one primary blocking status. If threshold holds are mixed with AML or tax holds under a generic "pending review," support will misdiagnose delays.

Step 2 make tax completeness a hard release condition#

Treat tax status as a release gate, not just a document-upload checklist. Form W-9 is used to provide a correct TIN for IRS information reporting, and Form W-8 BEN is submitted when requested by the payer or withholding agent.

Model submitted and accepted as different states. Tax and payout profile validation can take up to 48 hours, so release logic should wait for validation, not just file presence.

Also define how withholding interacts with thresholds. Public publisher policies show thresholds can apply after withholding and by payment method in local marketplace currency, so calculate eligibility on the right post-withholding and method-specific basis.

Step 3 document cross-border timing exceptions where VAT and jurisdiction matter#

Document where jurisdiction can affect timing so threshold policy does not get blamed for unrelated delays. For EU cross-border programs, specify exactly how VAT number verification, for example via VIES, is used in your flow: pre-release, reconciliation, or segment-specific.

Document non-tax timing dependencies too. Payment time frames can vary by country or region and payout account type, and customer terms like Net 45 or Net 60 can push payouts later.

Step 4 lock down PII in ops screens and stored artifacts#

Build PII controls into the release workflow design. In ops views, mask payment data and restrict full-field access to authorized staff with a legitimate business need. For PAN display, keep to the first six and last four digits maximum.

Store tax artifacts such as W-8 and W-9 files with encryption and enforce least privilege so each role gets only the minimum access required. Practical check: if support can open full tax forms or raw identifiers without escalation, data-exposure controls need tightening.

We covered this in detail in How to Build the Ultimate Finance Tech Stack for a Payment Platform: Tools for AP Billing Treasury and Reporting.

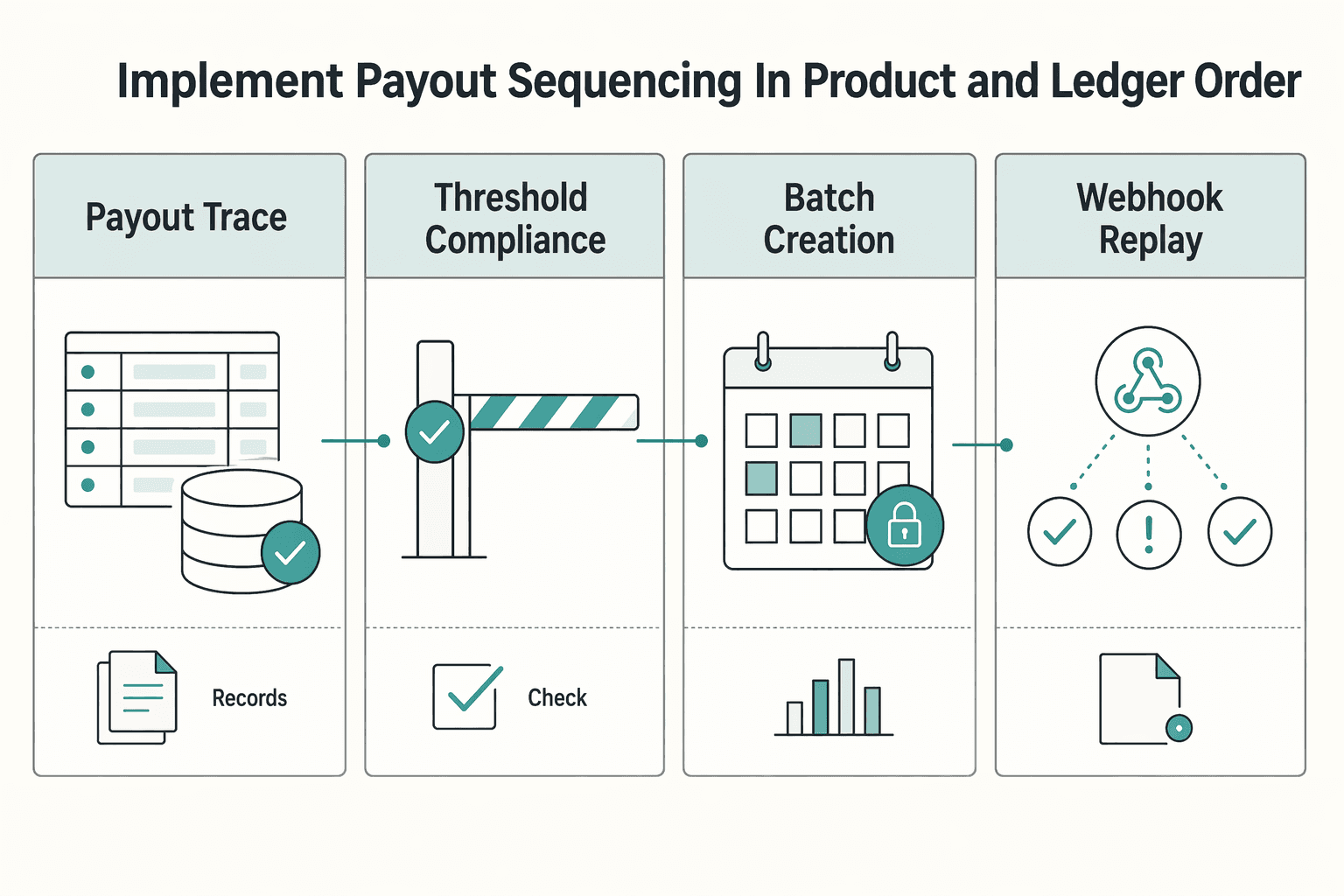

Implement payout sequencing in product and ledger order#

Use a payout release sequence that starts from ledger truth, then controls, then provider state. Threshold is one gate, not the only gate. Let the ledger define eligibility, let compliance veto release, and treat provider events as status updates only after they match an internal payout record.

| Stage | Key action | Control point |

|---|---|---|

| Ledger accrual | Base threshold eligibility on ledger state, not gross cash received or a dashboard summary | Keep total credited and eligible balances separate; finance should be able to trace eligible balance to specific ledger entries |

| Threshold and compliance recheck | After an eligible balance snapshot, run threshold evaluation, then a final compliance check right before payout creation | Recompute threshold status when returns arrive so ready states stay accurate |

| Batch creation | Use idempotency keys and persist the provider identifier returned at creation time, such as payout_batch_id | Repeated calls with the same key should return the original result; reused PayPal sender_batch_id values from the last 30 days are rejected |

| Webhook reconciliation | Treat webhooks as asynchronous and non-sequential, with deduplication and sequencing logic | Parity checks should confirm internal and provider outcomes at both batch and item level |

Step 1 accrue funds in the ledger before you test eligibility#

Base threshold eligibility on ledger state, not gross cash received or a dashboard summary. Payout reconciliation runs against transaction history, and a payout object may not include the individual transactions behind its total.

A common control is to keep two balances separate: total credited and eligible. Test your threshold against eligible balance only. If you operate as a Merchant of Record, keep KYC/AML obligations explicit in payout eligibility logic.

Verification point: for any sampled recipient, finance should be able to trace eligible payout balance to specific ledger entries. If they can only see one net payout number, reconciliation turns into manual investigation.

Step 2 evaluate threshold, then recheck compliance before batch creation#

After the ledger produces an eligible balance snapshot, run threshold evaluation, then run a final compliance check right before payout creation. This keeps threshold logic tied to ledger facts while preserving compliance holds as release vetoes. A passed threshold should mean financially ready, not auto-send.

Define exactly how Virtual Accounts affect matching and eligibility. Unique assignment can automate matching and reduce manual reconciliation, while returns or reversals should still flow back into eligibility calculations.

One failure mode is marking funds eligible and not recomputing threshold status when returns arrive. That creates a "ready" dashboard state while treasury or provider records already pulled funds back.

Step 3 create payout batches with idempotent keys and persist provider IDs#

Make payout creation replay-safe with idempotency keys. Repeated calls with the same key should return the original result instead of creating duplicates. Stripe guidance also notes keys can be up to 255 characters and can be removed after they are at least 24 hours old.

Persist the provider identifier returned at creation time on the internal payout record. For PayPal Payouts, capture payout_batch_id and use it for later status retrieval. If you submit PayPal batches, include sender_batch_id in duplicate protection design because reused values from the last 30 days are rejected. This matters more when splitting large runs, since batch size can range from 1 to 15000 items.

Verification point: after retry testing, you should see one internal payout record, one provider batch reference, and no duplicate disbursements.

Step 4 reconcile webhook status asynchronously and enforce parity checks#

Treat webhooks as asynchronous and non-sequential. Providers can deliver duplicates, and events can arrive out of order, so consumers need deduplication and sequencing logic based on event identifiers, timestamps, or versioned status fields, not arrival time.

Make status parity a standing control. Internal payout states should map cleanly to provider outcomes, for example submitted, pending, paid, failed, returned, and canceled, and parity checks should use transaction-level provider reporting where available. The core test is simple: provider outcomes and ledger outcomes agree at both batch and item level.

Give the exception queue a clear owner, then classify mismatches explicitly: missing provider batch ID, duplicate webhook, status mismatch, amount mismatch, or return not posted back to ledger. For month-end, package evidence, not just summaries: internal payout export, provider batch and transaction reports, webhook exception log, and unresolved deltas carried into the next close.

If you are standardizing threshold checks, batch creation, and retry-safe release flows, review Gruv Payouts workflows.

Write recipient-facing policy text that prevents tickets#

Good payout policy text should follow the same order as your release logic. Recipients should see, in plain language, what keeps funds pending, what makes them eligible, and what can still block release after the minimum is reached.

Step 1 Write the rule in release order#

State the release path directly: balance accrues, eligible balance is checked against the minimum payment threshold, holds are checked, then payout is issued on the next payout cycle. Include carryover behavior in the same block so users know sub-threshold balances continue as a running total.

Be explicit that crossing threshold alone does not guarantee payout. Say clearly that payout issues only when threshold conditions are met and no payment holds apply, so users can distinguish timing from verification or other hold-related blockers.

Verification point: your help article, payout settings text, and support macros should describe the same release rules.

Step 2 Show progress and timing in the dashboard#

Show threshold progress, payout eligibility, and estimated pay in the payout history dashboard, not only in help-center copy. If users can set a higher threshold, include a warning that setting it much higher than typical monthly earnings can delay payout.

Use concrete timing language from your actual cycle rules, not vague promises.

Step 3 Separate rail and region exceptions#

Document rail-specific rules separately when timing or requirements differ by method, for example PayPal, Wire Transfers, and Direct Deposit/ACH where available. For PayPal, state that recipients must have an eligible account and meet applicable verification requirements, including confirmed email and, where required, verified mobile number.

Document region-specific exceptions in their own line. If a region is exempt from a minimum threshold, say so plainly. Link the current policy from both payout settings and your publisher help center.

Monitor cost, churn signals, and exceptions every cycle#

The operating question each cycle is simple: is your threshold lowering payout cost without increasing support load or release blockers? Review the scorecard and the exception queues together so threshold decisions are not confused with AML, tax-doc, or return-related issues.

Step 1 Track a compact scorecard#

Keep one shared view that finance, product, and engineering can all use:

- Cost per payout, split by rail and currency

- Payouts per recipient, to see whether balances are batching or carrying over across cycles

- Support contacts per 1,000 recipients, using payout ticket tags, a practical adaptation of support-efficiency tracking, not a universal benchmark

- Threshold-related churn indicators, such as changes in recipient activity around threshold updates or repeated sub-threshold carryover. Treat these as warning signals, not proof of causation.

Verification point: align every metric to the same payout-cycle cutoff date used by ledger and provider reporting.

Step 2 Review exception queues before blaming the threshold#

Work queues by blocker type so threshold tuning and release blockers stay separate operational problems.

At minimum, monitor:

- AML and verification holds

- Failed tax-document cases for Form W-9 and Form W-8 BEN

- Unresolved payout returns or refunds

Missing or failed tax details can pause payout release even when balance is sufficient. Some providers state payouts may unpause within two business days after valid W-8 or W-9 submission if no other requirements remain, which gives you a practical queue-aging checkpoint.

Each queue item should include recipient ID, hold reason, owner, last action date, and next required evidence.

Step 3 Run a monthly threshold review and pre-approve rollback#

Hold a monthly cross-functional threshold review. That cadence is practical even when payout programs differ in frequency, including programs that pay monthly and others that pay four per month.

Go into the review with pre-approved rollback criteria. If support pressure rises faster than cost improvement, exception backlogs grow, or returns distort payout visibility, revert the affected segment to its prior threshold and log the decision: old value, new value, segment, release date, and rollback owner.

Step 4 Turn findings into product and infrastructure fixes#

Use monitoring output to drive fixes in the same cycle. If tax-doc failures are common, improve onboarding prompts and pre-release status text. If returns or refunds reduce payable balances, explain that behavior more clearly in recipient-facing payout transparency. If provider and ledger status diverge, fix reconciliation before you touch thresholds again.

Then update recipient surfaces, including help-center policy and payout tracker messaging. For a recipient-facing model, see Payment Transparency for Contractors: How to Build a Payout Tracker Your Recipients Trust.

Related reading: How to Calculate the All-In Cost of an International Payment.

Final takeaway and copy/paste launch checklist#

Treat your payout threshold as an operating control, not a static settings field. It works only when policy, support language, compliance and tax gates, ledger sequencing, and retry behavior are aligned before launch.

Lock scope before you lock the number. Define rules by rail, currency, and account, network, or marketplace, then confirm product logic, finance policy, and recipient-facing copy all match. Threshold scope varies in practice, so any mismatch between help text and release logic is a launch risk.

Map release gates that can block payout even after balance is met. Keep KYC verification states and tax-document states (Form W-8 BEN/Form W-9) explicit, and route reporting correctly where Form 1099-K applies instead of 1099-MISC or 1099-NEC.

Test sequencing and retries end to end, then define rollback before rollout. Use idempotency keys for retry-sensitive payout operations so retries do not create duplicates, and predefine trigger conditions and restoration steps for reverting threshold rules.

- Scope defined by rail, currency, account, network, or marketplace

- Segment matrix approved: owner, threshold, exception rules, review cadence

- Compliance gates mapped (

KYC) and tax gates mapped (Form W-8 BEN/Form W-9) withForm 1099-Krouting rules - Ledger and payout sequencing implemented with idempotent retries

- Recipient messaging published with progress-to-threshold visibility

- Scorecard live for cost, tickets, retries, and churn signals

- Rollback criteria documented and tested before full rollout

Before you lock policy for production, validate rail coverage and compliance gates for your rollout in a coverage planning call.

Frequently Asked Questions

What is a minimum payout threshold?

A minimum payout threshold is the balance a publisher must reach before payout is released. In practice, it is the confirmed-commission amount required before payment is issued. Reaching that amount does not always guarantee release if other account holds still apply.

Is a threshold set per currency, per account, or per network?

Any of those can be correct, depending on the platform design. Some systems vary thresholds by reporting currency, some apply separate thresholds per payments account, and some set a network-level minimum across channels. Define the scope explicitly in policy, product copy, and release logic so support and engineering are describing the same rule.

Can publishers set their own payout threshold?

Sometimes, but not universally. Some programs allow eligible publishers to set a threshold above the platform minimum. If you support this, make the effective threshold visible to support and operations.

What happens if a balance never reaches the threshold?

You should publish a clear carryover or backstop release rule. In some programs, sub-threshold balances roll into the next payment cycle. Others document a longer backstop, such as a year-end or next-quarter release behavior for balances that stay below the minimum.

Do payout method and tax withholding affect threshold behavior?

Yes, and the behavior is platform-specific. Some programs apply no threshold for one payout rail but apply thresholds for others, and some evaluate eligibility after tax withholding for specific methods. Other programs apply the same threshold regardless of whether payment is by check, direct deposit, or PayPal.

How often should thresholds be reviewed?

There is no universal industry-required review interval. Set an internal cadence you can sustain, and run out-of-cycle reviews based on your own operational signals.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/docs/manual/06_AssessingComplianceWithBSAReg...trusted

- csrc.nist.gov/glossary/term/least_privilegetrusted

- ec.europa.eu/taxation_customs/viestrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- fdic.gov/banker-resource-center/bank-secrecy-act-anti...trusted

- irs.gov/forms-pubs/about-form-w-9trusted

- irs.gov/instructions/i1099mectrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Choosing Affiliate Network Payment Software for Publisher Payout Fit

If you are evaluating **affiliate network payment software**, start by defining the exact job you need done before you compare feature lists. Teams make poor decisions when they treat partner discovery, tracking, and payment operations as the same problem.

Invisible Payouts: How to Remove Payment Friction for Contractors Without Sacrificing Compliance

Invisible payouts should make life easier for contractors without hiding the controls your team needs. Contractors should get a predictable, low-friction flow, while internal teams can still enforce and document payout decisions when needed. If you run contractor payouts at scale, you need both outcomes at once. We recommend treating every easy payout as a controlled release path your team can replay later.

Building a Contractor Payout Tracker Recipients Trust

A payout tracker can help build trust when recipients can see what is happening, what happens next, and whether they need to act, without opening a support ticket. When payout status is vague, routine questions can turn into tickets, calls, and escalations. When status is clear, timestamped, and action-oriented, recipients can self-serve and support teams may spend less time chasing updates.