Quick Answer

Model cash flow forecasting for payment platforms as a release-control process, not a reporting exercise: approve each batch only after reconciliation clears, funds are settled, and reserve deductions are applied. Anchor the run to one frozen data cut, then test whether net payout obligation still clears your post-payout buffer. If Stripe pending balances or Adyen payout-delay timing can miss cutoff, reduce scope or defer cohorts instead of forcing full release.

What the Forecast Needs to Show Before You Release Payouts#

For payout decisions, a forecast is only as useful as the cash that is actually settled, reconciled, and releasable before cutoff. If pending processor funds are treated like settled funds, or reconciliation breaks are ignored, the output may still help with planning, but it is less reliable for payout release decisions. If your team treats pending cash like spendable cash, your release call will drift before you notice it. If you are approving a run, your forecast should tell you what cash is truly releasable, not just what looks available on a dashboard.

Keep these checks in view from day one#

-

Separate payout timing from cash availability. In Stripe, funds are usable for payouts after they settle into the available balance. Stripe also states that payout schedule changes affect when payouts are sent, not when pending funds become available. A daily payout schedule does not mean today's batch cash is already usable.

-

Treat reconciliation as a release check. Payment reconciliation means matching transaction records with accounting records to confirm consistency. At the PSP layer, a transaction-level export like Adyen's Settlement details report supports transaction-level settlement reconciliation. If a forecast cannot point to the report extract and accounting snapshot used for the run, confidence in the release number drops.

-

Model a buffer, not just a balance. Stripe minimum balances are meant to reduce negative-balance risk after payouts when refunds, disputes, or fees arrive later. Releasing every available dollar can turn normal post-payout adjustments into liquidity stress.

Start with settlement truth#

Use one rule first. Only count cash expected to settle in time for the payout you plan to send. Blending captured volume, processor balances, and bank cash can hide cutoff risk.

Timing differences are real. Stripe's payout FAQ includes a daily payout example based on transactions captured 3 business days earlier. Adyen documents a default Sales day payout setup with a two days payout delay. Both can work, but they are not interchangeable and should not be collapsed into a generic "daily cash in" assumption.

What good looks like#

For each payout run, you should be able to answer four questions. Which obligations are due? Which funds are settled and eligible? What reserves or holds reduce releasable cash? Which exceptions still block release? Finance, ops, and product should see the same answer from the same data cut, even if each team owns different checkpoints.

A simple quality gate helps. Before forecasting releasable cash, confirm inputs tie to your accounting records and latest reconciliation exports. If they do not, treat the number as planning-only until the mismatch is resolved. Related: What Is Invoice Factoring? How Platforms Can Offer Early Payment to Contractors in Cash Flow Crunch.

Stop buying tools before you define payout decisions#

Define payout decisions and control ownership before selecting forecasting software. A common failure mode is unclear release actions and unclear accountability when numbers conflict.

Software comparisons and vendor promises are easy to find. GTreasury, BILL, and Martus all market forecasting benefits through integrations, historical data, scenario planning, or predictive modeling. The key operating question comes first: what action changes when the forecast changes? We recommend answering that before your team adds another dashboard or model. We use that question to decide whether your team is adding a real control or just another chart.

Name the payout decisions before naming the tool. Your forecast should map to explicit actions, such as:

- release or reduce a payout batch

- prefund an upcoming run

- top up a reserve

- hold specific items for review

Then define the operating constraint for each action. With Adyen, reserve funding can be deducted from payable balance when the payout batch closes. With Stripe manual payouts, you can control timing, but payouts still must occur within the allowed country-specific timeframe.

Assign ownership for your payout go/no-go decision before adding more modeling. You should be able to identify who prepares the recommendation, who reviews reconciliation, and who signs off for the run. We would rather see your team own one clear release decision than hide the call inside a forecasting tool. If you cannot name that owner, your model is not ready to drive release.

That split is a control, not admin overhead. Review-and-approval guidance supports explicit sign-off and can reduce single-operator risk when balances do not match during reconciliation.

Use vendor forecasts as inputs, not release proof. Release decisions should still tie to General Ledger records and reconciliation evidence.

Forecasting tools can integrate with core finance systems, but ledger settlement still has to be matched and checked. If forecast output cannot be tested against the ledger snapshot, reconciliation status, and open exceptions, treat it as planning support only.

Prepare the minimum inputs before modeling#

If inputs are not named, timestamped, and separated by confidence level, your forecast is planning input, not payout evidence. Before modeling, make the dataset auditable enough that another operator can rerun it and reach the same decision.

Confirm source systems and owners per legal entity. Cash forecasting is configured and calculated per legal entity in Dynamics-style setups, so one global extract is often insufficient. For each entity, assign an owner for the systems in scope (for example ERP, General Ledger, bank feed, and PSP reconciliation export), and confirm ledger prerequisites are set: system currency and exchange-rate type.

Checkpoint. Every feed should have an accountable owner, extraction method, and fallback contact if the feed is late. Watch for cases where bank data appears complete while PSP reconciliation status is stale.

Create one canonical data cut. Stamp each item with clear timestamps for event time, Settlement Timing, and expected payout timing. This is not a universal standard, but it is a practical structure for separating transaction occurrence, cash availability, and payout obligation.

Set report boundaries explicitly. Stripe payout reconciliation slices data by a daily window (12:00 am to 11:59 pm), and a Report Run can normalize output timestamps to a declared timezone, for example Etc/UTC. Mixed local-time and UTC stamps will skew cutoff logic.

Split clean data from provisional data before the model runs. Keep posted ledger events and reconciled payouts in the clean set. Keep pending ACH or direct-debit items, other delayed-notification methods, and items with unresolved disputes in provisional until outcomes are known.

Cash can be overstated here. Settlement time is when funds become available, not when the transaction was created.

Build an evidence pack for every run. Include source extract IDs or Report Run IDs, reconciliation status, and forecast-versus-actual variance checks where available. For Stripe flows, retain the payout reconciliation reference that links each bank payout to the settled transaction batch.

Red flag. Manual payouts break deterministic transaction grouping, so separate reconciliation proof is required. Without this pack, you can still have a forecast, but not release-grade evidence. For a step-by-step walkthrough, see Discounted Cash Flow DCF Valuation for Solo Professionals.

Define the forecast unit and cash states#

Forecast at Payout Obligation level, not just account-balance level. Headline cash can look sufficient while payouts still miss cutoff when funds are pending, reserve-held, or otherwise not usable for the due cohort.

| Cash state | Use in model | Article detail |

|---|---|---|

| available | Matched available cash can fund payouts | Use provider availability states as the base |

| restricted | Visible but not releasable cash | Includes reserve-held balances; returns to available when the hold period ends |

| buffered | Internal operating cushion | Keeps withheld cash intentional and explainable |

| unsettled inflows | Track separately by Payment Rail | Keep out of generic expected cash until settlement time passes and reconciliation matches |

Model each Payout Obligation as its own liability line with fields like amount, due window, and eligibility status. That keeps exposure, timing, and release readiness visible in one record instead of scattering decisions across notes and exception lists.

Treat timing as part of the liability itself, not a side comment. IFRS 7's maturity-analysis framing is a useful operating analog. Remaining contractual maturity helps show when liability risk becomes practical. In practice, bucket obligations by release cadence, for example next cutoff, later today, or after the current batch.

Checkpoint. Total modeled obligations for the run should reconcile to the payout file or the relevant General Ledger control total for that entity and batch.

One workable approach is to split cash into states that explain payout usability: available, restricted, and buffered, with unsettled inflows tracked separately by Payment Rail. The goal is decision clarity, not a universal naming standard.

Use provider availability states as the base. Stripe explicitly distinguishes pending from available, and settlement timing can vary by market, payment method, and transaction type. So unsettled inflows should stay out of generic "expected cash."

Use restricted for funds visible but not releasable, including reserve-held balances. Keep buffered explicit as an internal operating cushion so withheld cash is intentional and explainable.

Rail and method timing should also be explicit in the model. Stripe Connect may show availability on a 2-day rolling basis, with country and account variation. Same Day ACH has a 4:45 p.m. ET submission cutoff with 6:00 pm ET interbank settlement in that third window. Fedwire transfers are immediate, final, and irrevocable once processed.

Define state transitions with named rules tied to Settlement Lag and reconciliation status. A simple flow works well. Pending inflow stays excluded until settlement time passes and reconciliation matches. Matched available cash can fund payouts. Cash moves to restricted when a reserve hold applies. Restricted cash returns to available when the hold period ends.

Make exclusion reasons operationally visible. Every excluded amount should carry one reason and one next-change condition, such as "awaiting settlement," "unreconciled," or "reserve hold active."

If obligation-level tagging is missing in the General Ledger, treat automation and forecast-frequency scaling as higher risk until the taxonomy is fixed. Otherwise, you may be automating account-balance math rather than payout decisioning.

Build a ledger-first dataset that survives audit#

Use the General Ledger as the authoritative base, then layer in reconciliation and bank or provider detail for timing and traceability. That keeps booked amounts and dates stable while still giving ops enough detail to explain payout decisions.

Anchor on the General Ledger. Start each forecast cut from posted General Ledger journals where possible. The ledger is your complete accounting record, so it is a strong control point when finance, ops, or audit asks how a payout decision was made.

Add historical accounting data from ERP modules, bank events, and provider exports as enrichment. Use them to improve context and timing, but do not let enrichment override booked ledger amounts or posting dates.

Join reconciliation records with stable references. Join PSP Reconciliation records to ledger events with stable matching attributes, not fragile text fields. Reconciliation is a comparison process, so match quality depends on durable references such as transaction IDs, payout or batch IDs, and reconciliation references.

Provider artifacts support this structure. Stripe separates payout-batch reconciliation from unsettled ending-balance reconciliation. Adyen settlement reporting includes batch, date, and unique-identifier fields that are useful for traceable joins. Keep unmatched lines in a documented exception workflow with a unique reference so they can be resolved and reviewed.

Keep settlement and payout events separate. Settlement time covers when funds become available, while payout activity is reported separately in reconciliation views. Combining them too early can hide usable-cash risk.

Keep that separation through your forecast inputs, and document reconciliation checks so breaks are visible and reviewable. If inputs do not tie cleanly to your accounting records for a run cut, flag and investigate the discrepancy before relying on the output. Related reading: Build a Contractor Payment Flow for Home Services Marketplaces.

Map settlement behavior by payment rail#

Choose the rail based on release reliability, not preference. Use rails with stable settlement behavior for urgent payouts, and apply larger Reserve Account cushions where timing or reversals are less predictable. If a rail's Settlement Lag distribution becomes unstable, route high-urgency payouts away from it until performance normalizes.

Build a rail table from documented timing and your own actuals. Start with published Settlement Timing, then add your observed lag from instruction time to funds-available confirmation. The goal is rail-level operating truth in your environment: expected timing, actual lag, reversal or return exposure, and repeat failure patterns.

| Payment Rail | Expected Settlement Timing | Observed Settlement Lag to track | Return or reversal behavior | Common failure pattern |

|---|---|---|---|---|

| ACH | Windowed and business-day constrained. FedACH same-day windows include 10:30 a.m. ET submission for 1:00 p.m. ET settlement, 2:45 p.m. ET for 5:00 p.m. ET, and 4:45 p.m. ET for 6:00 p.m. ET. ACH settles four times each business day. | Track actual settlement versus intended window, plus delay from settlement to usable-bank confirmation. | Reversals for erroneous entries can be initiated within 5 banking days following the Settlement Date. Unauthorized debit return threshold is 0.5%. | Missed cutoff, weekend or holiday assumptions, late file delivery, returns after funds were treated as clean. |

| FedNow | Funds are to be made available as soon as practicable and no more than a few seconds after receipt of advice when participating institutions are connected. | Track accepted instruction time to recipient funds-available confirmation. | A common operational risk is reachability or availability rather than batch-window drift. | Recipient path not available on the rail at execution time. |

| RTP | The RTP network is available around the clock, including weekends, holidays, and after hours. Credit transfer settlement is final and irrevocable. | Track instruction acceptance to final confirmation; flag drift away from near-immediate behavior. | Final and irrevocable once processed for credit transfers. | Counterparty not reachable on RTP, forcing fallback to a slower rail. |

| Fedwire | Real-time gross settlement. Transfers are immediate, final, and irrevocable once processed. Business day runs 9:00 p.m. ET to 7:00 p.m. ET, with a 6:45 p.m. ET third-party deadline. | Track release to processed confirmation, especially near deadline. | Final once processed. | Approval or file delay near cutoff turns same-day plans into next-day funding. |

| CHIPS | Fast and final payments for high-value USD transfers during the business day. | Track initiation to final settlement confirmation for large-value obligations. | Fast and final. | Timing depends on business-day operations for high-value flows. |

Checkpoint for every run. Compare expected window versus actual bank or provider confirmation timestamp for the last completed cycle. If ACH submissions intended for the 2:45 p.m. ET window repeatedly miss the expected 5:00 p.m. ET settlement pattern, treat that rail as unreliable for that use case until performance recovers.

Set Reserve Account assumptions by reversal and timing risk. Set rail buffers from observed risk, not a fixed multiplier. ACH typically needs more caution because settlement is windowed and reversals or returns can change what is safe to release.

Separate "settled on schedule" from "safe to spend for payout." For ACH-backed inflows, hold more in Reserve Account when you see elevated return activity, recent reversals, unresolved exceptions, or repeated cutoff misses. Use evidence from current operations instead of a universal rail rule.

Use Nacha's 0.5% unauthorized debit return threshold as a warning signal for payout planning. If debit-originated inflows trend toward that level, reduce same-day release against fresh ACH-funded balances until return behavior is cleaner.

On real-time rails, timing buffers may be smaller when recipient reachability is confirmed. That benefit depends on actual execution conditions, not the rail label alone.

Route urgent payouts away from unstable rails. Treat lag instability as a routing trigger before it becomes a payout failure. Practical signals include widening gaps between expected and actual confirmation times, repeated fallback events, or sudden inconsistency for similar submissions.

- If urgency is high and recipient reachability is confirmed on FedNow or RTP, prefer that route over ACH.

- If value is high and timing is critical, use Fedwire only when approvals can clear before the

6:45 p.m. ETthird-party deadline. - If your plan depends on an ACH same-day window already missed, do not model those funds as available today. Hold, split, or reroute.

Log evidence for each reroute: original rail, fallback rail, submission timestamp, confirmation ID, and instability reason. That record explains payout delays, rail-switch costs, and forecast decisions during review.

Model payout obligations and reserve logic#

Model releasable cash as a waterfall from gross due to net Payout Obligation. Settled or reported balance is not automatically payout-ready. Subtract anything pending, disputed, reserved, or otherwise ineligible before approving release. If the projected post-payout buffer breaches policy, consider reducing release scope or staging release rather than forcing a full payout.

Build a payout waterfall from General Ledger truth. Use obligation-level gross due from your General Ledger and Enterprise Resource Planning (ERP) cut, not a processor dashboard alone. For each payout cohort, calculate in order: gross due, explicit holds, eligibility filters, reserve deductions, and net releasable Payout Obligation.

Keep eligibility strict. Exclude items in pending balance, incoming funds that have not settled, obligations backed by unsettled inflows, unreconciled items, and payouts not due in the current window.

Run one hard checkpoint before release. Gross due must tie to the same ledger population for that run, and net releasable must not exceed the balance state you treat as payout-ready.

Separate Chargeback risk from settled cash. Treat disputes as immediate cash-out risk. In Stripe card disputes, payment funds are reversed immediately, and the disputed amount plus dispute fee are debited. For Stripe indirect charges, refunds, disputed amounts, and associated fees are debited from the platform balance.

Model an explicit exposure horizon. Cardholders can typically initiate disputes within 120 days of the original payment, with some cases allowing longer. A reserve is a temporary hold for expected disputes, refunds, and related losses, so settled cash is not overcounted as releasable cash.

Model processor reserve mechanics directly. Adyen recalculates deposit requirements daily, and reserve top-ups are deducted from payable balance when the payout batch closes. Reserve funds are used only if in-process funds are insufficient. A balance that looks sufficient earlier can tighten at close. Also treat negative next payout balance as a potential release gate. It may block payouts and refunds, and if pending and next payout balances are insufficient and reserve funds are not enough, refunds can fail.

Stress-test the waterfall before release. Use a small set of operating scenarios before approval to confirm reserve policy still holds when conditions worsen.

| Example day type | What changes in the model | What to verify before release |

|---|---|---|

| Baseline day | Normal settlement lag, current reserve deduction, current dispute or refund load | Net releasable stays above minimum post-payout buffer and ties to reconciled balances |

| Delayed-settlement day | More inflows remain in pending balance; same-day payable cash is lower | No payout amount depends on unsettled funds |

| High-reversal day | Higher dispute or refund pressure and stronger reserve pressure | Post-payout balance remains clear of negative next payout balance and required reserve deductions |

Decision rule. If the stressed view breaches policy, baseline alone should not drive full-batch approval. Consider reducing payout amount, holding lower-priority cohorts, or releasing in stages after more funds settle or risk clears. This is where release discipline protects payout and refund continuity.

Keep a run evidence pack: ledger snapshot time, waterfall version, reserve amount used, next payout balance, open dispute count and value, and the scenario result that set the final release amount.

Set explicit payout release gates#

Use payout gates to decide what should be released now, not just what the waterfall says is theoretically releasable. This is where model output becomes an operational release decision.

| Gate | Batch check | Evidence from same run |

|---|---|---|

| Reconciliation | Confirm exactly which transactions are in the payout | Payout reconciliation report; unresolved Exception Queue count; unreconciled PSP Reconciliation value |

| Funding sufficiency | Verify the payout still leaves enough retained balance | Proposed payout amount; payout-ready balance; retained minimum balance; projected post-payout balance |

| Compliance and eligibility | Confirm required capabilities are active and verification is completed where needed | Risk-based compliance checks; account-level payout pauses; unresolved pauses can cancel and return funds after 10 days |

| Final decision | Log a named Payout Go/No-Go Decision and decision owner | Run snapshot references; reconciliation report or extract ID; unresolved exception count; unreconciled value; Forecast Variance if used |

One workable gate order is reconciliation, funding sufficiency, compliance and eligibility, then a final Payout Go/No-Go Decision. Keep all gates on the same data cut so approvals and investigations use the same run state.

Pass reconciliation before release. Confirm exactly which transactions are in the payout. Payout reconciliation is an operator responsibility, and the payout reconciliation report is the control view for transaction composition.

Make this gate measurable for the batch under review: unresolved Exception Queue count and unreconciled PSP Reconciliation value. Because exception queues are typed, classify exception drivers and check for reporting-period or timezone mismatches before escalation.

Where your controls support it, pause payouts on affected connected accounts. If not, hold the broader batch.

Confirm funding sufficiency on the same cut. After reconciliation passes, verify the payout still leaves enough retained balance. Automatic payouts release funds above the configured minimum balance, and draining too far can leave insufficient funds for refunds or disputes.

Review these fields together: proposed payout amount, payout-ready balance, retained minimum balance, and projected post-payout balance from the same run snapshot. You can also log Forecast Variance as an internal review signal if your team uses it when deciding whether to slow or stage release. If the post-payout cushion is thin, reduce scope or release in stages instead of forcing a full batch.

Validate compliance and payout eligibility. Treat compliance and eligibility as release gates, not post-approval checks. For connected accounts, required capabilities must be active, and activation often depends on completed verification.

Record whether the payout population passed your risk-based compliance checks, and use account-level payout pauses when issues are isolated. Do not leave paused payouts unresolved. Extended pauses can result in cancellation and funds returning to balance after 10 days.

Log the final decision for reconstruction. Close with a named Payout Go/No-Go Decision, decision owner, and evidence references. Log each gate outcome with run snapshot references, reconciliation report or extract ID, unresolved exception count, unreconciled value, and any review metrics used, including Forecast Variance if it is part of your process.

After execution, attach payout tracking identifiers. Webhook payout events and payout Trace ID create a clear trail from approval through bank investigation if expected funds do not arrive. Before you lock release tolerances, map each gate to concrete payout states and retry behavior in Gruv Docs.

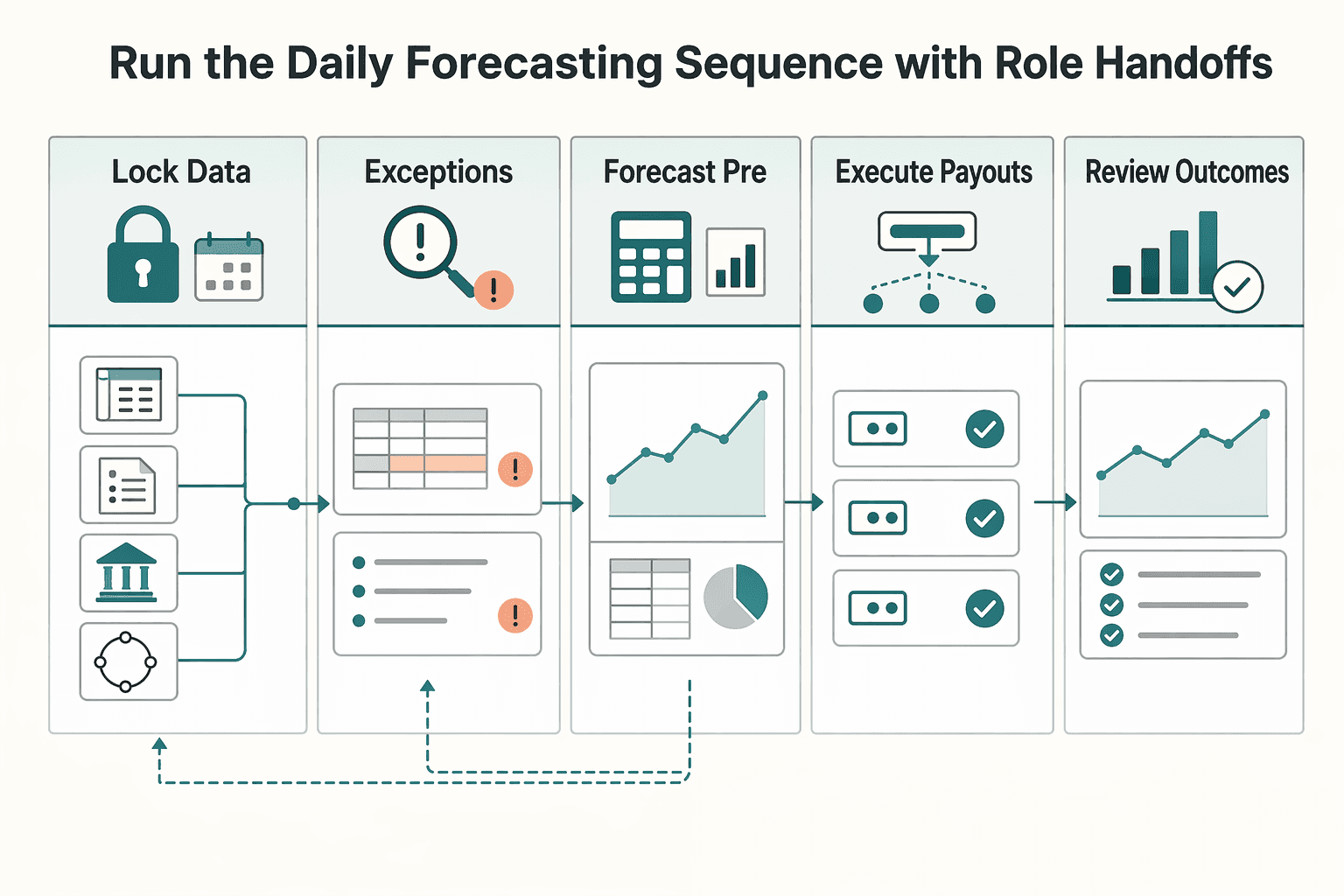

Run the daily forecasting sequence with role handoffs#

Daily forecasting is easier to govern when each run follows a consistent sequence, uses one shared data cut, and has explicit handoffs before the Payout Go/No-Go Decision.

| Run step | Key action | Recorded detail |

|---|---|---|

| Lock the data cut | Pull one consistent cut across General Ledger, payables or receivables data, bank activity, and PSP Reconciliation exports | Assign a run ID; record extract IDs and timestamps; mark the run provisional if a required bank file or PSP export is late |

| Reconcile and route exceptions | Use the payout reconciliation report to tie the bank-facing payout to grouped underlying transactions | Move mismatches into the Exception Queue; Finance owns reconciliation evidence; Ops triages exception items |

| Forecast and pre-cutoff check | Run the forecast on the same frozen cut, then hold a pre-cutoff decision check | If inputs change during approval, reopen on a new run state; time sign-off to the rail cutoff such as 2:45 p.m. ET for same-day ACH |

| Execute payouts | Submit payouts with idempotent request handling | Reuse the same idempotency key on retry; require reapproval if a rerun changes the decision basis; keep a run ID to request mapping |

| Review outcomes | Attach payout tracking identifiers and review failed payout outcomes in the daily reconciliation cycle | Route process-flow or control-setting changes through formal review |

Lock the data cut and ingest source data. Start by pulling one consistent cut across core finance and payout inputs, including General Ledger, payables or receivables data, bank activity, and PSP Reconciliation exports. Cash flow forecasting can integrate data across core finance modules, so analyzing a single run cut helps avoid mixed snapshots.

Assign a run ID and freeze the extract set before review starts. Record the exact extract IDs and timestamps, and mark the run as provisional if a required bank file or PSP export is late.

Reconcile first, then route exceptions to owners. Reconcile before trusting the forecast. Use the payout reconciliation report to tie the bank-facing payout to grouped underlying transactions, and move mismatches into the Exception Queue for investigation.

Keep ownership clear at handoff:

- Finance owns reconciliation evidence from the frozen run cut.

- Ops triages

Exception Queueitems by exception type and coordinates investigation. - Approval and reconciliation responsibilities stay separated by role.

Run the forecast and hold a pre-cutoff decision check. After required setup and reconciliation tasks are complete, run the forecast on that same frozen cut, then hold a pre-cutoff decision check. If inputs change during approval, reopen the decision on a new run state.

Time sign-off to your payout rail cutoff. For example, if targeting a same-day ACH transmission at 2:45 p.m. ET, finalize with enough time to act. The approval pack can include run ID, reconciliation report or extract ID, unresolved Exception Queue count, unreconciled PSP Reconciliation value, projected post-payout balance, and runtime alerts.

Document accountability for the Payout Go/No-Go Decision, while still keeping dual-control initiation and approval duties separate from reconciliation.

Execute payouts with retry-safe controls. On a go decision, submit payouts with idempotent request handling. Reusing the same idempotency key on retry helps prevent duplicate payout side effects after connection failures.

Keep reruns safe by separating recalculation from release. If a rerun changes the decision basis, require reapproval, and keep a run ID to request mapping for recovery, especially when provider idempotency keys may be removed after at least 24 hours.

Review outcomes and control changes after execution. Close the run by attaching payout tracking identifiers and reviewing failed payout outcomes in the daily reconciliation cycle. This confirms not just approval quality, but settlement outcomes.

If process flow or control settings changed during execution, route those changes through formal review so future daily runs stay consistent and auditable. For upstream demand assumptions, read Payment Volume Forecasting for Platforms: How to Predict Cash Flow.

Measure forecast quality and tune assumptions#

Once the daily run is stable, judge forecast quality where payout decisions are made, not only at the platform total. Track Forecast Variance at Payment Rail, cohort, and payout-batch levels, and keep assumptions explainable enough to diagnose misses before cutoff.

Break variance down to the decision level. Review three cuts every cycle: Payment Rail, payout cohort, and payout batch. A platform-level result can look acceptable while one rail settles late or one cohort carries more dispute activity than expected.

Show forecast versus realized cash at each layer, with the signed-off run ID and payout identifiers. If transaction-to-payout linkage is preserved in reconciliation, you can trace misses to the exact batch instead of debating aggregate totals.

Before updating assumptions, confirm actuals come from realized outcomes, not refreshed estimates. Mark still-moving periods as provisional and exclude them from tuning.

Run rolling error review on cash-availability assumptions. Use rolling review across test windows, not a single score. Forecast performance should be checked by window because one calm period can hide assumptions that fail under settlement stress.

Prioritize assumptions that directly move payout decisions:

Settlement Timingby segment (for example, location or payment method/rail)- observed

Settlement Lagbetween expected and available funds Chargebackor dispute incidence by cohort and age bucket

Keep dispute review lag-aware. Recent periods can still change because cardholders may dispute a payment up to 120 days later, and sometimes longer, so treating recent dispute data as final too early can understate risk.

Use multiple metrics when assessing revisions. RMSE, MAPE, MASE, and WAPE expose different error patterns.

Validate every revision on a holdout slice of historical data. Before promoting a model or assumption change, test it on a holdout period not used for fitting. That is the clean check for out-of-sample improvement.

Set holdout coverage to at least your longest forecast horizon. A common starting point is about 20% of the sample, but horizon coverage matters more than the exact share.

Record each revision in a short change note: prior assumption, new assumption, holdout period, metrics by backtest window, and any rail or cohort that worsened even if aggregate results improved.

Favor explainable controls for payout operations. For payout control, explanation speed is operationally important. Predictive Modeling can help, but if the team cannot quickly isolate whether misses came from Settlement Lag, dispute behavior, or stale inputs, the control is too opaque.

Use transparent inputs and documented assumptions by default, then add complexity only when holdout results support it. Keep ongoing monitoring and outcomes analysis focused on two questions: what changed, and why realized cash differed from forecast.

Handle the failure modes competitors skip#

Treat reconciliation drift as a payout-control risk first. When upstream files arrive late or incomplete, matches break because counterpart records have not landed yet. The Exception Queue can swell as unmatched items are routed for investigation.

Monitor these patterns each cycle:

- late settlement or bank files that leave gaps in payout matching

- stale transaction-to-payout joins that no longer tie out cleanly

- instant payout paths that are not fully reconciled to transaction history

- failed payout cases tied to bank-account data errors or return-code outcomes

When PSP Reconciliation is incomplete near cutoff, take a conservative release approach based on your risk controls. Unresolved cohorts can be deferred to the next run until transaction-to-payout matching is complete.

For every incident, publish a short postmortem that records impact, mitigation steps, root cause, and follow-up actions.

Conclusion#

For cash flow forecasting for payment platforms, the decision that matters is whether a payout batch should be released, reduced, or paused based on reconciled records, settlement timing, and reserve or hold impacts. If your forecast cannot support that decision cleanly, your team is still planning, not controlling release risk. We recommend keeping your release decision and your forecast on the same review page.

1. Reconcile inputs before trusting the forecast. Use General Ledger, Enterprise Resource Planning (ERP), bank activity, and PSP Reconciliation outputs together. Match payouts to bank deposits and transaction batches, and use settlement reconciliation detail, including payments, refunds, and chargebacks, so unmatched items are explicit before release decisions.

2. Keep settlement timing tied to actual payout windows. Availability depends on timing rules, not just totals. Adyen's default Sales day payout uses a two-day delay, with a default sales day of 00:00 to 23:59 and an optional close extension to 7:00 AM. Stripe computes payout reconciliation data daily beginning at 12:00 am for activity between 12:00 am and 11:59 pm.

3. Forecast net payout obligation, not gross due. Reserves and holds change what is safely releasable. Reserve funding can reduce payable balance when the payout batch closes, so recalculate net Payout Obligation before finalizing any batch.

4. Treat unresolved exceptions as provisional. This is especially important for manual payouts, where reconciliation to transaction history is your responsibility. If you cannot tie a payout amount to its underlying transactions, hold that portion out of the release amount until it is resolved. We recommend forcing that hold in the same workflow your reviewer uses, so your team is not relying on memory at cutoff. If you leave that hold outside your workflow, your team will bypass it under pressure.

5. Document the final payout release decision as an internal control. Keep a replayable record: ledger snapshot, bank reconciliation status, payout or settlement reconciliation output, reserve treatment, and unresolved exceptions.

Copy and paste checklist

- Reconcile bank activity with

PSP Reconciliationoutputs, and compare againstGeneral Ledger/Enterprise Resource Planning (ERP)context - Confirm settlement timing windows and reserve inputs for the current run

- Recalculate net

Payout Obligationafter holds and reserve deductions - Isolate unresolved exceptions from releasable payout amounts

- Record the final payout release decision with the reconciliation snapshot

If you want to pressure-test your payout release workflow against real market and compliance constraints, talk to Gruv. We recommend doing that before your next payout cycle if your team is still relying on manual overrides.

Frequently Asked Questions

What is cash flow forecasting for payment platforms?

For platforms, cash flow forecasting is not just projected inflows and outflows. It forecasts when funds move from pending to available and what is actually releasable after reconciliation, settlement timing, and reserve holds are applied. If pending funds are treated as spendable, payout capacity is overstated.

How do I model payout obligations versus expected settlements?

Model the obligation side first: amount due, due window, and release eligibility. Then offset only cash expected to settle in time, using observed settlement lag or configured settlement delay days. Validate the model against bank-received payouts and payout reconciliation reports, since refunds and chargebacks can reduce what settles.

What data is mandatory before a forecast is trustworthy?

There is no universal minimum checklist. In practice, forecasts are more reliable when General Ledger, Accounts payable, Accounts receivable, bank activity, and payout reconciliation data align and tie payouts back to transaction batches. If bank deposits do not match payout records or unresolved exceptions remain, treat the forecast as provisional.

How often should a platform reforecast?

Use a rolling cadence that matches your operation: daily, weekly, or monthly. Re-run closer to payout cutoff when settlement timing shifts, returned payouts increase, or available-versus-pending balances move. The right cadence is the one that keeps release decisions aligned with current settlement and reconciliation state.

What are common failure points in payout forecasting?

Common failure points include incomplete reconciliation, weak reserve or negative-transaction assumptions, and releasing payouts before related transactions are reflected in settled funds. Settlement outcomes also matter, because refunds and chargebacks reduce net funds. Incorrect destination details can lead to returned payouts, and a failed payout can disable the external account involved until it is updated.

Do we need predictive models from day one?

No. Documented forecasting approaches include machine learning, statistical, driver-based, and trend-based methods. A reliable process can use non-ML methods when assumptions and reconciliation controls are clear.

What settlement details should I watch most closely?

Watch the time gap between transaction event, settlement availability, and payout due time, because that gap determines whether funds are usable or still pending. This matters most across locations and payment methods where settlement timing varies. For example, Nacha reports that approximately 80% of ACH volume settles in one banking day or less, so not all payments settle on that timeline.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/manual/OfficeOfForeignAssetsControl/01trusted

- canons.sog.unc.edu/blog/2024/04/08/the-bank-reconciliation-a-ke...trusted

- fdic.gov/risk-management-manual-examination-policies/...trusted

- federalreserve.gov/paymentsystems/fedfunds_about.htmtrusted

- federalreserve.gov/paymentsystems/fednow-additional-questions-a...trusted

- finance.cornell.edu/controller/internalcontrols/unitlevelactivit...trusted

- publishedguides.ncua.gov/examiner/content/examinersguide/electronicpa...trusted

- sao.wa.gov/sites/default/files/2023-05/Best-Practices-f...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: