Quick Answer

Invoice factoring lets a contractor get cash early by selling unpaid invoices to a factor, which usually advances part of the invoice and then collects from the customer. For platforms, the key decision is who funds the advance, who handles collections, who absorbs nonpayment risk, and whether the economics still work when disputes and exceptions appear.

How contractor invoice factoring works on a platform#

If you run a platform for contractors, early payment is a product and risk decision before it is a goodwill feature. Ask four things up front: Who funds the advance? Who collects from the payer? Who absorbs nonpayment risk? Do the unit economics still work once disputes and exceptions show up?

Payment friction is not an edge case. The Federal Reserve's 2024 Report on Payments, published December 05, 2024, says customer payments are the primary source of cash for small businesses, and roughly four of every five small firms face payment-related challenges. That makes early payment worth serious attention. It also underscores why invoice quality and payer behavior matter before broad rollout.

- This guide focuses on operating decisions, not basic definitions.

Factoring is when a company sells or assigns receivables to a factor for immediate cash. In most arrangements, the factor also collects from the customer. That design choice changes contractor experience, collections touchpoints, support load, and how much payout control your platform keeps.

- The scope is contractor-focused early payment in real cash-flow crunches.

We cover factoring, invoice financing, dynamic discounting, supplier finance, and cash advance paths for contractors with uneven payment timing. These models are not interchangeable. In many arrangements, factoring is treated as an asset sale rather than a loan, while supplier finance depends on buyer-approved invoices and pays ahead of original terms after approval.

- The emphasis is execution reality, unit economics, and risk ownership.

Before you scale, you need a minimum proof set for each advance: invoice validity, payer identity, dispute history, and receivables aging. You also need a clear recourse position. In recourse factoring, the seller bears nonpayment risk tied to financial inability. In non-recourse factoring, the factor bears that risk.

- This guide adds the operator layer.

The point is to help you set implementation order, choose the first eligible cohort, and spot failure modes early. If you cannot explain, invoice by invoice, who approved it, who funded it, who collected it, and who owns the loss, you are not ready to scale.

How to use this list and who it is for#

Use this list when you are making a product and risk decision, not trying to pick a generic winner. It is for teams serving contractors with uneven cash flow that need to choose an early-payment model, decide who handles collections, and clarify recourse versus non-recourse terms when an invoice goes bad.

Use it when you are choosing between models#

This is for founders, revenue leads, product teams, and finance operators comparing factoring, receivables discounting in an invoice-finance style, dynamic discounting, and a merchant cash advance offer. They are different structures, not interchangeable products. In factoring, the finance provider typically handles collections, and structures can be recourse or non-recourse. In dynamic discounting, a bank or finance provider does not supply the financing. In an MCA, the business receives upfront cash in exchange for a share of future sales or revenue.

Do not use it as a provider ranking#

Do not treat this as a provider ranking. Cross-provider comparisons are hard because terminology is inconsistent, and many ranking pages are commercially influenced or explicitly not complete. If you need planning context before you compare options, see Payment Volume Forecasting for Platforms: How to Predict Cash Flow.

What invoice factoring means in platform terms#

Treat factoring as a receivables-purchase model with product consequences, not just a funding label. The key test is simple: does a factoring company buy receivables from outstanding invoices and take over payment flow?

- Core mechanic

In factoring, the contractor sells receivables to a factor at a discount. The factor typically advances cash upfront, often around 70% to 90% of invoice value. The real differentiator is ownership and payment flow. The receivable shifts to the finance provider, and the buyer pays the provider rather than the contractor.

- Platform consequence

This is a product decision because collections touchpoints usually move with the receivable. In typical setups, the factor manages debtor collections, and factoring is normally disclosed to the buyer. Map it out operationally. Who sends payment instructions? Who follows up on overdue invoices? Who explains the process to contractors when collections begin? If the factor owns those moments, you are giving up some control over customer interactions.

- Why contractors use it

Contractors use factoring to reduce the pressure of waiting 30, 60 or 90 days to be paid for completed work. That matters when operating costs come due before customer payment arrives. The tradeoff is straightforward: faster cash now, but not full invoice value. Cited fees are often around 1% to 5%. It is typically a cash-flow timing tool rather than a margin tool.

- What it is not

Keep factoring separate from invoice financing and internal early-payment programs. With invoice financing, the business borrows against invoices and customer payment can remain under the original arrangement. Early-payment programs are distinct and can sit alongside factoring. If receivables are not purchased and collections do not transfer, use a different label.

For a step-by-step walkthrough, see How US Consultants Can Invoice a Swiss GmbH Without Payment Delays.

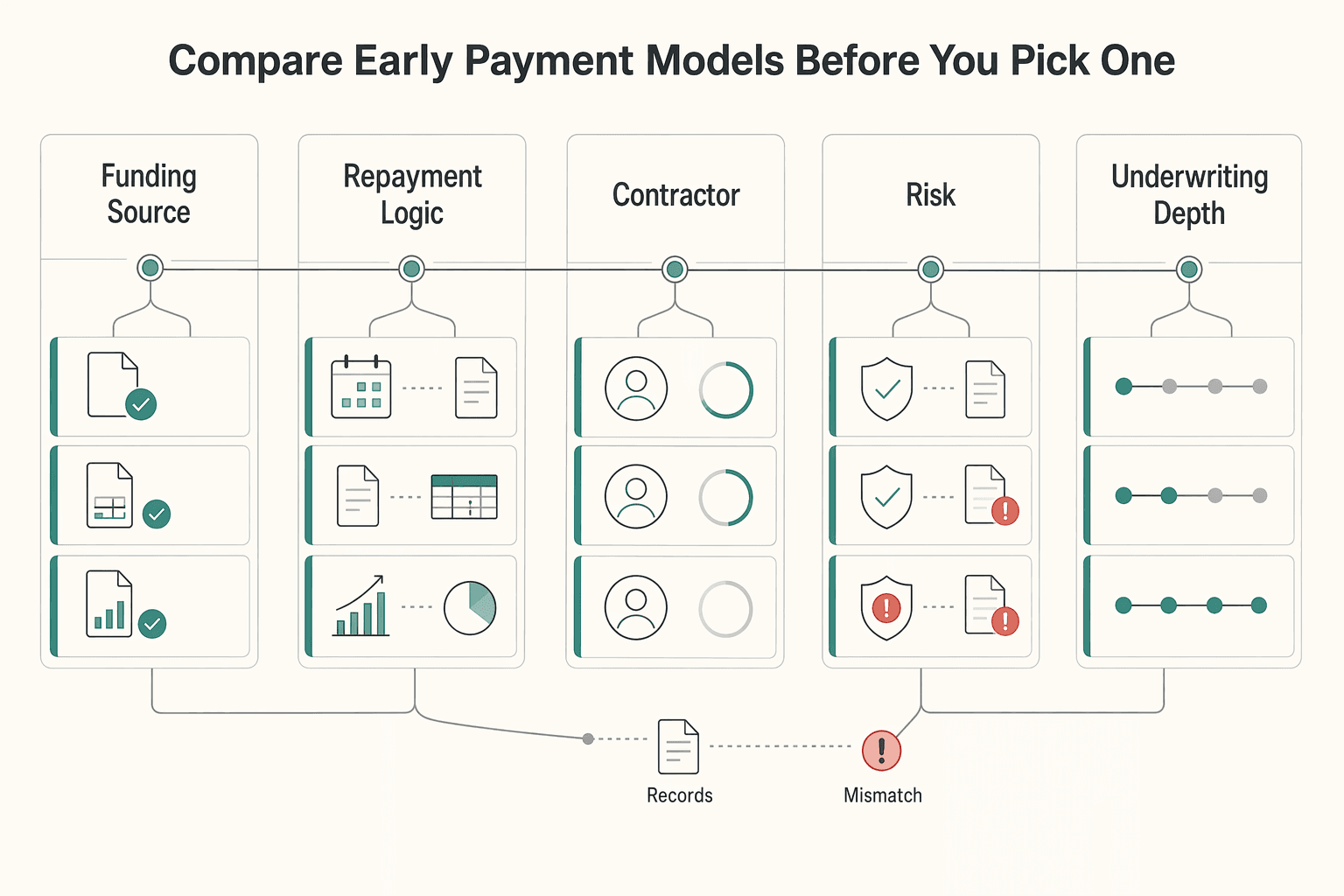

Compare early payment models before you pick one#

Start with repayment logic and collections control. Those two choices determine how much underwriting and reconciliation work you carry, and how much of the payment experience you still own.

A useful first filter is the data you already have: approved invoices, unpaid invoices, or mostly sales history. Dynamic discounting depends on approved invoices. Invoice-backed products depend on receivables quality. Cash-advance-style products are repaid from sales or revenue over time.

| Comparison point | Invoice factoring | Invoice financing | Dynamic discounting | Cash advance |

|---|---|---|---|---|

| Funding source | External factor buys receivables | External provider advances against unpaid invoices used as collateral | Buyer funds early payment with its own funds | Provider advances funds and is repaid from sales or revenue |

| Repayment logic | Buyer pays the factor on the sold invoice | Funding is repaid from invoice proceeds; receivables are collateral, not sold | Seller takes early payment at a discount on approved invoices | Repayment is a percentage of sales or revenue over time |

| Contractor UX | Early cash, but payment instructions and collections contact can shift to the factor | Early cash with less collections handoff than factoring | Early-payment option on approved invoices; discount changes with timing | Early cash tied to ongoing revenue deductions, not a specific invoice settlement |

| Risk concentration | Exposure is tied to receivables quality | Advance sizing follows provider risk criteria on unpaid invoices | In buyer-funded programs, capacity depends on buyer liquidity and approved-payables process | Exposure is tied to future sales or revenue performance |

| Underwriting depth | Receivables and debtor-book quality are central | Risk-based against unpaid invoices using provider criteria | More dependent on invoice approval and buyer process than external receivables underwriting | Centered on sales or revenue performance rather than invoice-by-invoice review |

| Collections control | Factor may run collections and credit-control services | Finance-only structure; collections and ledger services are not bundled like factoring | Runs through buyer payables process, not factor-led debtor collections | No invoice-collections transfer; repayment is taken from revenue flow |

| Recourse or non-recourse support | Recourse and non-recourse variants exist, depending on contract terms | Not typically framed as recourse vs non-recourse factoring | Not applicable in factoring terms | Not applicable in factoring terms |

| Onboarding friction for small businesses | Provider-specific; typically tied to receivables quality and process requirements | Provider-specific; tied to unpaid-invoice quality and risk review | Provider-specific; tied to approved-invoice workflow maturity | Provider-specific; tied to consistency and visibility of sales or revenue history |

| Expected documentation or data | Provider-specific receivables and invoice-quality data | Provider-specific unpaid-invoice and receivables-quality data | Approved-invoice status and settlement-timing data | Sales or revenue records that support percentage-of-revenue repayment |

| Reconciliation burden across A/R flows | Can rise when receivable ownership and payment destination change | Often closer to existing A/R flow than factoring, but still requires funding reconciliation | Can be cleaner in buyer-led payables flow, with discount-by-date tracking | Requires matching revenue deductions to repayment activity |

| Decision checkpoint | Start here if you want receivables sale mechanics and can accept third-party collections control | Start here if you want invoice-backed funding with less collections transfer than factoring | Start here if approved invoices exist and timing-based discounts are the priority | Start here if invoice evidence is weak but revenue visibility is strong and sales-linked repayment is acceptable |

Use the table to narrow the field, then validate the economics and compliance in your own setup. Factoring is currently treated separately from covered credit transactions in CFPB interpretation. Merchant cash advance treatment is still in motion under a proposed 11/13/2025 rule with comments due by December 15, 2025. For background on the cash side of the business, you might also find How to Read a Cash Flow Statement useful.

Best option for fastest launch with external capital partner#

If speed matters more than full product control, partner-led factoring can be a practical first move. You get third-party capital and operations to support earlier contractor payouts, but you give up some control over collections interactions.

Choose this route when you already have outstanding invoices and do not want to build internal credit rails first. Factoring is commonly positioned as faster cash access than bank financing. It is often used where contractors would otherwise wait 30, 60, or 90 days to get paid. In construction examples, advances are often around 70% to 90% of invoice value.

The balance-sheet appeal is that some external-capital receivables programs are structured to make receivables liquid without incurring debt. Operationally, partner-led programs can run through existing invoice-approval workflows, with approved invoice files sent to the funding partner. One bank example shows payment timing at day 10 instead of day 120. Treat that as illustrative, not guaranteed.

The tradeoff is control. In factoring, the factor typically collects from customers, so your team may have less control over collections communication and handling. That differs from invoice financing, where customer payments continue going to your business. Before you launch, confirm exactly when payment instructions change, what contractors see, and who handles disputes. Unclear handoffs can create support and reconciliation problems quickly.

If you want a deeper dive, read Embedded Working Capital for Platforms: Invoice Financing Factoring and Cash Advance Compared.

Best option for tighter margin control and product ownership#

When speed is no longer the main constraint, in-house or hybrid early payment can fit better. You keep more control over pricing, routing, and experience, but only if you are prepared to own underwriting, monitoring, and reporting.

- Dynamic discounting inside your own payout flow

Brief description: Dynamic discounting is buyer-led early payment on outstanding invoices at a variable discount, where earlier payment can carry a larger discount. Key differentiator: You can directly control liquidity and pricing because the buyer can set available liquidity, payment schedules, and blocked calendar days. Treat this as a product and cash-control decision, not just a funding setup. Before you enable any cohort, confirm who funds early payment and what liquidity limits apply.

- Invoice financing when you want to keep customer and payer steps

Brief description: With invoice financing, you borrow against invoices instead of selling them, and you still bill and collect from clients before repaying the lender. Key differentiator: Compared with factoring, this keeps customer-facing collections, exception handling, and service tone under your control. It can also support cost discipline, since factoring generally costs more in part because the factor takes over collections operations.

- Hybrid routing with selective escalation

Brief description: A tighter design is to route cleaner receivables through internal early-payment paths and escalate edge cases to external financing when risk, liquidity, or documentation falls outside policy. Key differentiator: This preserves product ownership where your data is strongest without defaulting to blanket approvals. The burden is control quality. Receivables-based programs require stronger underwriting, credit administration, controls, and monitoring, and supplier-finance-style arrangements can carry material reporting and disclosure expectations, including ASU 2022-04 context. If you cannot produce clear policy logs, approval traces, and month-end exception reporting, keep the program narrow until controls are audit-ready.

We covered this in detail in SOC 2 for Payment Platforms: What Your Enterprise Clients Will Ask For.

Best option when risk transfer is the deciding factor#

If loss ownership is the deciding issue, recourse factoring is often the lower-cost liquidity option when you can retain nonpayment risk. Non-recourse factoring can make more sense when covered buyer default risk is the bigger concern.

- Recourse factoring

Brief description: In recourse factoring, you still receive an early cash advance, but you remain responsible if the customer does not pay. If the receivable is uncollectable at maturity, some or all of that loss can return to you. Key differentiator: Pricing is typically lower than non-recourse because the factor is not taking full nonpayment risk. Invoice factoring examples often cite advances around 70% to 90% upfront with fees around 2% to 5%, though exact terms vary by agreement.

Before you route invoices here, assess payer concentration and actual payment behavior, not just average payment outcomes.

- Non-recourse factoring

Brief description: In non-recourse factoring, the factor absorbs nonpayment loss under defined contract conditions. The protection is real, but only to the extent the agreement actually covers it. Key differentiator: This structure can fit when reducing covered nonpayment exposure is the priority, but it usually costs more because the factor assumes more nonpayment risk.

Treat contract scope as the real decision point. The IRS framing ties coverage to debtor financial inability, so confirm what qualifies as covered nonpayment and what is excluded.

- Blended routing by payer cohort

Brief description: Some programs use both recourse and non-recourse, based on debtor credit quality. For platforms serving construction contractors, this can be a practical alternative to forcing one structure across all payers. Key differentiator: You can reserve higher-cost risk transfer for cohorts that need it while using recourse terms for other cohorts.

This can be useful in sectors where slow payments are common, including construction. Some construction factoring guidance notes invoice terms in the 15 to 90 days range.

Decision rules that connect monetization to unit economics#

Widen access only when payout reliability, pricing, and risk control stay visible by payer cohort. That should anchor the rest of the program design.

- Reliability over per-advance margin when delayed payment drives churn

If delayed payout is driving churn, prioritize dependable payment timing before you optimize yield on each advance. That can mean accepting lower per-transaction margin to protect payment volume, contractor activity, or retention over time. There is some directional operator evidence. Block reported sellers who took a Square Loan grew 6% faster on average, and sellers who adopted a full suite of banking products showed a 15% improvement in retention. This is not contractor-factoring proof, but it is a credible signal that liquidity products can matter commercially.

- Thin gross margin means tighter underwriting, not broader approval

When margin is thin, broad eligibility can turn the offer into a hidden subsidy very quickly. Federal Reserve guidance warns that relaxing prudent credit underwriting standards increases risk, and the small-business backdrop still supports caution: more than 9 in 10 firms reported a financial or operational challenge in 2023, and 77% reported one or both major cost challenges in the 2026 Fed report. Gate on invoice quality, not demand volume: aging, dispute history, payer identity, and collectability on normal terms. If exceptions start driving approvals, narrow access before you add volume.

- No broad promise without payer-behavior visibility

Do not promise broad factoring access if you cannot verify payer behavior at scale. Past-due receivables and weaker account-customer credit quality both increase non-collection risk. Start with a narrow cohort and explicit eligibility rules, then expand only when the data supports it. Track payment speed, aging drift, and dispute frequency by payer, not just by contractor. Decide early whether payment routing stays with the business, as in invoice financing, or moves to a factor. That choice changes collections control and contractor experience.

- Put the go/no-go test on one page

Use a one-page monthly matrix that ties monetization to loss exposure and operating load before scale hides problems. This aligns with supplier-finance disclosure framing around working capital, liquidity, and cash flows, including IFRS visibility expectations effective 1 January 2024.

| Dimension | What to review monthly | Go signal | No-go signal |

|---|---|---|---|

| Take rate and margin | Net revenue after funding cost, credits, and servicing cost by cohort | Positive and stable versus plan | Margin depends on frequent exceptions or manual rescue work |

| Loss exposure | Realized nonpayment, aging drift, dispute rate, and payer concentration | Losses match expected risk for the approved cohort | Deterioration is concentrated in payers you did not underwrite well |

| Operational overhead | Manual reviews, reconciliation issues, support tickets, settlement delays | Ops load is predictable and shrinking with experience | Volume growth is being bought with manual handling and opaque exceptions |

If a row stays red across consecutive review cycles, treat that as a pause signal, not a reporting footnote.

Underwriting and eligibility evidence you need before launch#

Do not launch until your evidence pack is explicit and easy to review consistently. Fund only receivables you can validate, segment only where payer behavior is visible, and pause expansion when ops starts compensating for weak underwriting.

- Set a minimum evidence pack for every request

As policy, every file should establish four things: the invoice is real, the payer is real, the work or goods were accepted, and the receivable is still collectible. A practical pack can include the invoice record, underlying contract or work authorization, proof of delivery or service completion, payer identity details, dispute notes if any, and an accounts receivable aging view showing what that payer already owes and how those invoices are performing. Title 12 guidance shown as current to 3/23/2026 highlights aging, debtor concentration, and performance against terms of sale as core eligibility signals. If you cannot tell whether an invoice is current, already paid, disputed, or sitting in a slowing payer stack, treat it as not underwritable.

- Split policy by seller and buyer segment before you scale

One policy usually fails because risk is not uniform. Small and mid-sized businesses that rely on factoring are often less able to absorb the loss of a large nonpaying account debtor, and payment difficulties vary by terms and arrangements, so segment-specific controls matter. On the buyer side, even when an account debtor appears strong, concentration still needs explicit checks. Banking guidance for pooled receivables says high concentrations should trigger review of individual exposures, not just pool averages. The Federal Reserve small business payments report published December 05, 2024 found roughly four of every five small firms report payments-related challenges, and those difficulties differ by payment terms and arrangements.

- Write red-line exclusions that approvers cannot waive casually

Some invoices should fail immediately. Red lines should include weak or inconsistent documentation, repeated disputes with the same payer, unclear acceptance of work, signs an invoice may already be paid, and repeat approvals based on the same missing evidence. Under UCC 9-404, an assignee's rights remain subject to the underlying agreement and to defenses or claims from the original transaction, and those claims can reduce what the account debtor owes. In practice, assignment does not clean up a disputed receivable. Review exceptions on a regular cadence. If the same missing proof is repeatedly overridden on outstanding invoices, the problem is policy design, not reviewer discipline.

- Gate each expansion phase with risk and ops checkpoints

As eligibility expands, controls should tighten with risk instead of staying static. The OCC states that lenders apply varying degrees of collateral control based on borrower risk, and the same operating logic applies here. Before you move from a narrow pilot to broader factoring access, require checkpoints for delinquency trends, dilution, payer concentration, dispute rates, and collectability by cohort. Pair that with an ops checkpoint: can your team trace each funded invoice to its evidence pack and reconcile final settlement without manual rescue work? If either answer is no, keep the cohort narrow. Expansion should follow verified receivable quality, not approval demand.

Implementation sequence across product, ops, and finance#

Roll this out as a controlled sequence with explicit handoffs. Set eligibility first, then pricing and funding mechanics, then payout operations and reconciliation. Expand only after those controls hold in production.

- Define eligibility and approval data flow first.

Start with invoices that are unconditionally approved for payment, and require buyer approval plus transmission of approved-invoice data before any early-payment offer. In one documented program flow, the approval file is sent at Day 1, with supplier election after approval visibility around Day 10.

- Lock underwriting and pricing with finance.

Document credit terms and conditions up front so product rules and pricing stay aligned as volume grows.

- Design funding and payout operations with clear ownership.

Assign initiator, approver, and reconciler responsibilities explicitly, and define who owns collections, fund transfer, and contractor support escalations across product, finance, and operations.

- Build reconciliation and audit artifacts from day one.

Keep policy logs, approval traces, and invoice-level payout and settlement records so expected versus realized cash flow can be reviewed without manual reconstruction.

- Add failure handling before controlled expansion.

Define what happens when settlements are delayed, invoices are disputed, or collected amounts differ from expected cash flow, and require timely dispute reporting. Then broaden access only after those paths work reliably.

Need the full breakdown? Read Build a Contractor Payment Flow for Home Services Marketplaces. Use this rollout sequence as your implementation checklist, then map each control to real API events and status handling in the Gruv docs.

Red flags that should stop rollout or force a redesign#

Pause expansion when demand starts outrunning control quality. Strong contractor uptake is not enough if unit economics deteriorate, underwriting exceptions become routine, receivable disputes rise, or your team cannot consistently explain outcomes from approval to settlement.

- Approval growth with weaker realized unit economics

Rising approved volume is a red flag when realized unit economics keep missing plan and exceptions are rising. There is no universal numeric threshold, but worsening economics alongside growth can indicate underwriting drift. If finance cannot show expected versus realized results by cohort or invoice, stop adding new sellers or buyers until controls are tightened.

- Underwriting exceptions become the normal path

If exceptions are carrying approvals, your actual policy has already drifted. Competition can push teams to relax underwriting, which increases risk, so scaling should wait until approvals consistently map to explicit credit policy and disciplined administration. If approvers cannot produce decision support such as invoice-validity checks and receivables-aging review, tighten scope before expanding factoring to new cohorts.

- Disputes rise or receivables start aging more slowly

Treat higher dispute volume and worsening receivable days as asset-quality warnings, not support noise. Increasing receivable days should be investigated, especially where recourse factoring leaves the seller responsible if the customer does not pay. Reassess buyer quality first, then whether recourse or non-recourse terms still fit that segment. Also check for verification drift such as fake invoices, duplicate financing, and misrepresented receivables.

- No end-to-end explanation for payout outcomes

If product, ops, and finance cannot give the same payout explanation, stop expansion. Teams should be able to trace how approved invoices move through advance and settlement and explain where losses, exceptions, disputes, and adjustments occurred. This matters even more when discussing risk transfer, because non-recourse protection is limited and does not cover all late-payment scenarios. If you cannot explain outcomes at invoice level, the program is not ready to scale. For related reading, see Cash Pickup Payouts for Unbanked Contractors in Cash-Preferred Markets.

Conclusion#

The key call is not whether to offer early payment. It is which model fits your risk appetite, unit economics, and operating capacity.

- Choose the risk-and-economics model deliberately.

Factoring converts receivables into immediate cash by selling them at a discount. Recourse and non-recourse structures shift non-payment risk differently, and that tradeoff shows up in pricing. When the factor takes more debtor risk, discounts are typically higher.

- Run factoring as a controlled product, not a generic payout feature.

Set explicit eligibility and verification gates, then measure outcomes from approval through settlement. Early-payment structures can improve working capital and access to finance, and results depend on keeping risk, operations, and economics aligned.

- Start narrow, then scale through a phased pilot.

A phased pilot is not hesitation. It is risk control. Pick one contractor segment, apply your decision rules, and expand only after outcomes are stable and auditable. Once your pilot scope is defined, validate risk ownership, payout operations, and reconciliation design with a focused review through Gruv.

Frequently Asked Questions

What is invoice factoring for contractors in plain terms?

Invoice factoring lets a contractor turn unpaid invoices into cash before the customer pays. In many setups, the receivable is sold to a factor and the customer pays the factor. For a platform, that can change collections, payout communication, and settlement reconciliation.

Is invoice factoring a loan?

It is often structured as a sale of receivables rather than a traditional loan. UCC Article 9 explicitly covers sales of accounts. Treatment can still vary by structure and documentation.

How much of an invoice can a contractor get paid early?

Common advance ranges in factoring are about 75% to 95% of invoice value. Other receivables programs may state up to 90%, and some approved-invoice programs market financing on 100% of approved invoices. Approval status can affect both timing and the available advance amount.

When should a platform offer factoring instead of asking contractors to wait for payment?

Offer it when long payment terms are creating real cash-flow strain and receivable quality is clear. Some programs market funding in 1-2 days after approval or payment on day 10 instead of day 120. If invoice validity or payer behavior is unclear, waiting is usually safer than advancing against weak receivables.

What are the main tradeoffs between invoice factoring and dynamic discounting?

Factoring typically adds a factor and can change payment routing and collections control. Dynamic discounting is buyer-led early payment on approved invoices where the seller accepts a timing-based discount. It also uses the buyer's own funds rather than financing from a bank or finance provider.

How do recourse factoring and non-recourse factoring change platform risk?

In recourse factoring, unpaid invoices can be charged back to the client, so the client keeps debtor credit risk. In non-recourse factoring, the factor assumes debtor credit risk on purchased receivables under defined contract conditions. The key control point is contract scope, because non-recourse terms do not cover every non-payment scenario.

What should a platform verify before launching an early payment program?

Verify invoice validity and approval status before approving advances. Confirm whether collections stay with the business or move to a factor, since that changes payment routing and contractor experience. Before launch, lock in recourse versus non-recourse terms and a clear process from approval to payout to settlement.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- archives.gov/records-mgmt/policy/pilot-guidance.htmltrusted

- archives.gov/files/records-mgmt/pdf/pilot-guidance.pdftrusted

- consumerfinance.gov/rules-policy/regulations/1002/104trusted

- dfpi.ca.gov/alert/advisory-to-small-businesses-speak-up-...trusted

- ecfr.gov/current/title-12/chapter-III/subchapter-B/pa...trusted

- ecfr.gov/current/title-17/chapter-II/part-229/subpart...trusted

- federalregister.gov/documents/2025/11/13/2025-19865/small-busine...trusted

- federalreserve.gov/publications/files/3000_2.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: