Quick Answer

Reconcile cash first: beginning cash plus net change should equal ending cash, and those totals should tie to the balance sheet for the same accounting period. Then read Operating activities before Investing activities and Financing activities. If ending cash improves because borrowing or one-off funding increased, treat that as support, not operating strength. Use invoice aging, payroll dates, and chargeback logs to decide whether to tighten billing terms before adding hiring or discretionary spend.

Read your cash flow statement like an operator#

Start with one operating question: will cash arrive in time to cover what you must pay? If that answer is uncertain, prioritize cash reliability before you add optional spend, hiring, or growth bets.

Start with cash timing, not finance terms. A cash flow statement shows historical cash changes for a period and groups them into operating activities, investing activities, and financing activities. For practical decisions, both the labels and the pattern matter. The statement shows where cash came from, where it went, and whether normal work is producing usable cash.

That is the right lens if you are learning how to read a cash flow statement as a freelancer or running a small team. It helps you spot timing gaps early, before they push you toward reactive borrowing or higher fee pressure.

Tie the statement to the risks that hit small firms first. For small businesses, customer payments are often the main cash source, so payment timing is a core operating risk. Federal Reserve small-business reporting found that roughly four of every five small firms face payments-related challenges. A Boston Fed summary reports 80% with send or receive payment issues. Two commonly cited problems were fees and slow payments.

Read the statement against the pressures you actually feel: unpaid billing, client delays, processor fees, and fixed outflows like pay runs. A month can look profitable on the income statement and still be cash-tight if receipts land after obligations. The statement also will not give you every billing-level detail, so pair it with your billing and payment records.

Use one simple checkpoint to cut noise: match the statement period to the same month or quarter used for billing, bank activity, and pay dates.

Make a risk-first call as you plan growth. Decide whether cash from normal operations is covering routine obligations. Cash-flow reporting is useful because it shows cash generation, obligation coverage, and whether outside financing may be needed.

Pay timing makes this more urgent. In the U.S., covered wages under federal guidance are due on the regular payday for the pay period covered. If collections lag, those deadlines do not.

Watch for this trap: sales or net income rise while collections lag and recurring payments stay fixed. When that happens, treat financing inflows or one unusually large client payment as temporary support, not proof that cash from operations is stable.

For the rest of this guide, review one period-specific pack together: the statement, billing records, bank activity, and pay schedule. That turns the statement from a finance document into an early-warning tool. If you want a deeper dive, read Hiring Your First Subcontractor: Legal and Financial Steps.

Gather these documents before you start#

Start with one aligned evidence pack. Cash-flow analysis gets misleading fast when statement dates do not match.

Pull the three statements for one accounting period. Collect the cash flow statement, income statement, and balance sheet for the same review window. The cash flow statement and income statement should cover the same period, and the balance sheet should be dated at that period end.

Quick check before you analyze:

- Cash flow statement start and end dates match the income statement period.

- Balance sheet date lands on that same period end.

If those dates do not align, re-export first.

Export the transaction evidence behind the statements. Then pull the records that support the statement totals for that same period:

- Open and paid billing or invoice exports

- Any dispute notes, including chargeback entries, if you track them

- Bank export plus matching statement PDF

A chargeback is a reversed card charge after a dispute, so a missing reversal can make customer cash look higher than it is. Keeping bank records in the same pack also helps later reconciliation.

Prepare your fixed-outflow file. Build a short list of cash obligations you still need to track when clients pay late:

- Payroll amounts and pay dates

- Recurring loan payment due dates and current account status

Keep your pack orderly, traceable, and safe. A practical version is the three statements, billing exports, dispute or chargeback notes, bank export and statement PDFs, payroll report, and loan schedule. Related: The Best Bank Accounts for Freelancers in Germany.

Use this reading order to find payment risk fast#

Once your pack is aligned, a practical reading order is: reconcile cash first, read the operating section next, then use Investing activities and Financing activities for context.

| Review step | What to check | Why it matters |

|---|---|---|

| Cash reconciliation | Beginning cash, ending cash, and net change in cash for the accounting period; beginning and ending cash agree with the cash totals on the balance sheet | A mismatch at this stage makes the rest of the read unreliable |

| Operating activities | Whether normal work is generating cash | If this section is weak, near-term liquidity pressure can build even when profit looks acceptable |

| Investing activities | Cash flows from acquiring or disposing of long-term assets and other investments outside cash equivalents | Heavy investing outflows can tighten cash when the operating section is already thin |

| Financing activities | Cash flows that change equity and borrowings | A higher ending cash balance can come from debt or equity inflows rather than stronger core cash generation |

| Verification checkpoint | Whether cash is coming from normal operations, or mainly from investing and financing movements | If net cash improved but the operating section is weak, the position can be more fragile unless operating cash improves |

Confirm the cash movement is real. Start with beginning cash, ending cash, and net change in cash for the accounting period. Check that they reconcile, and that beginning and ending cash agree with the cash totals on the balance sheet.

If they do not tie, stop there and fix the pack. A mismatch at this stage makes the rest of the read unreliable.

Read operating activities first. After cash ties out, go straight to Operating activities. Under IAS 7, this section covers principal revenue-producing activity, so it is a key signal of whether normal work is generating cash.

This is where you test whether reported performance is turning into usable cash. If this section is weak, near-term liquidity pressure can build even when profit looks acceptable.

Read investing activities for cash tied up elsewhere. Then read Investing activities. This section shows cash flows from acquiring or disposing of long-term assets and other investments outside cash equivalents.

Use it to judge timing and tradeoffs. Heavy investing outflows can tighten cash when the operating section is already thin.

Read financing activities as context. Then review Financing activities. These cash flows change equity and borrowings. Treat this section as context, not proof of operating strength. A higher ending cash balance can come from debt or equity inflows rather than stronger core cash generation.

Verification checkpoint. If net cash improved but the operating section is weak, treat that as a caution signal and investigate what is driving the change.

Ask one direct question: is cash coming from normal operations, or mainly from investing and financing movements? If it is mostly the latter, the position can be more fragile unless operating cash improves. For a step-by-step walkthrough, see How to Read a Balance Sheet.

Judge operating activities before you trust growth#

If you need one section before making a growth decision, start with Operating activities. Your day-to-day work should bring in enough cash inflow to support required cash outflow. If it does not, growth plans are harder to sustain.

Run a simple check with what you can verify:

- List the main cash inflows

- List the main cash outflows, including pay runs

- Check whether inflows are supporting required outflows

This is a practical risk test. When inflows and outflows do not line up, liquidity pressure can follow. When they stay balanced, operations are easier to keep running.

| Operating check | What to verify | Why it matters |

|---|---|---|

| Operating activities | Inflows and outflows are tracked and compared for the period | Mismatches can create liquidity pressure |

| Cash inflow vs payroll outflow | Main inflows are compared against required pay runs | Payroll is part of cash outflow that should be monitored |

| Tracking discipline | Inflow and outflow lists are current and clear | Simple lists help you judge cash pressure during the period |

| Context check (Investing activities and Financing activities) | Operating signals are reviewed alongside investing and financing activity | Cash-flow analysis should be read in broader context |

Once the operating picture is clear, use investing and financing activity to understand what is adding pressure or providing support. Related reading: Build a Pro Forma Financial Statement for Freelance Cash Decisions.

Read investing activities and financing activities in context#

Investing and financing lines matter, but they do not answer the first question on their own. Use them to decide whether cash improved because the business is carrying itself, or because assets were sold or outside funding filled the gap.

Read investing activities as allocation choices. Treat Investing activities as long-term allocation choices, not proof of day-to-day operating health. These lines show cash used for or generated from long-term assets and investments, so they help you read strategy and timing.

For large investing outflows, separate what the statement confirms from what still needs additional context:

- Cash tied to purchases or sales of long-term assets and investments

- Whether the timing or priority of that spending is flexible

Read financing activities as funding support. Treat Financing activities as cash from capital structure decisions. This section shows cash raised or returned through funding sources, including borrowing, repayment, and equity-related actions.

If ending cash rose while operating cash stayed weak, identify the financing line driving the increase. Treat that as financing support, not operating strength.

Check for dependence, not just a single boost. A financing inflow can bridge a timing gap, but repeated weak operating cash plus repeated financing inflows points to ongoing dependence on external capital. The real test is durability: can the business generate future cash and meet obligations without recurring financing support?

Look at today's support against tomorrow's pressure. Check whether current financing inflows are paired with repayment outflows. Financing can include both proceeds from long-term debt and payments on long-term debt, so today's cash increase can create future fixed-payment pressure.

Read the three sections together. Investing shows where cash is being placed for the long term. Financing shows how cash is being sourced. Operating shows whether the business is carrying itself.

Explain why profit and cash disagree without guessing#

When profit and cash disagree, do not guess. Start with the operating bridge from Net income to cash, then test that explanation against the Balance sheet and your records.

Start with the operating bridge, not the bank balance. Under the indirect method, Operating activities starts with Net income, then adjusts for non-cash effects and accrual or deferral timing so profit is translated into operating cash.

In practice, profit can be recorded before cash arrives. If you issue a bill near period end, the Income statement can show revenue before collection. The reverse timing can happen on costs too.

A practical read:

- Positive Net income plus rising receivables can mean profit is ahead of collections.

- Positive Net income plus large depreciation or amortization can mean part of the gap is non-cash.

A business can be profitable on paper and still run into cash pressure if revenue is not collected on time or expenses are paid too quickly.

Cross-check that bridge against the balance sheet. Before you decide anything, compare the bridge against the Balance sheet. The cash flow statement links the Income statement and Balance sheet, so balance-sheet movement should support your explanation.

Compare beginning and ending balances for:

- Receivables and other collection-related items

- Accrued expenses and payables

- Accrued payroll liabilities

- Cash and cash equivalents

If operating cash is weak while profit is positive, you should be able to see the matching balance-sheet movement that explains why.

Name the cause, then respond to it. "Profit is fine but cash is tight" is too vague to act on. "Profit is ahead of collections" or "cash is going to clear prior obligations" is operational.

The main risk is treating booked profit as spendable cash. Team pay is especially sensitive because payroll timing is usually fixed. ADP warns that without tracking accrued payroll liabilities, employers can spend funds intended for payroll and risk wage claims and tax penalties.

Keep the review pack simple: same-period Cash flow statement, Income statement, Balance sheet, billing aging or paid and unpaid billing list, and payroll schedule. Then act on the actual driver: speed up collections if timing is the issue, or delay new commitments if recurring cash outflow is outpacing inflow. This pairs well with our guide on Build a Statement of Cash Flows with the Indirect Method.

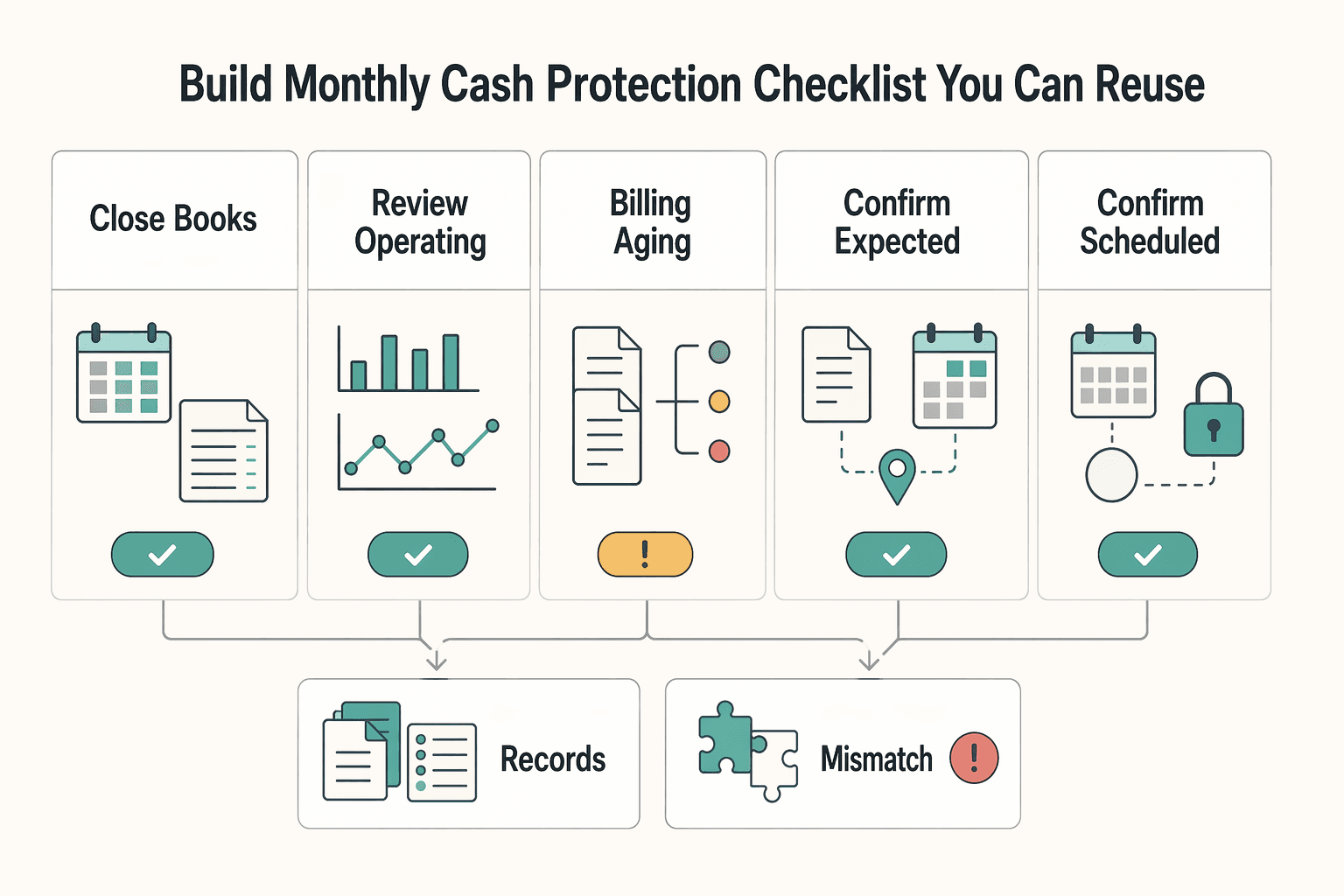

Build a monthly cash protection checklist you can reuse#

A good month-end process is simple and repeatable. Close the accounting period, review operating cash flow, and set next-month cash controls before you approve new commitments.

Cash flow is money moving into and out of the business. Your checklist should focus on whether operations are generating usable cash and where that cash could fail to arrive.

Align the review to one period. Align your Cash flow statement, Income statement, Balance sheet, billing records, and dispute log to the same accounting period.

Then check beginning cash, ending cash, and net cash change for that same window. If support files include activity from a different period, treat conclusions as provisional until the period is reconciled.

Read operating activities first, then test the story. Operating cash flow is a concrete monthly review checkpoint. Do not stop at "positive" or "negative." Confirm that the result matches what happened in collections and outflows.

If operating cash looks weak, document the likely driver from your records before you act. Keep this operational, not interpretive.

Make next-month obligations explicit. In the same review, include internal checkpoints for billing aging, expected pay runs, and scheduled loan payment dates.

For planning, separate likely collections from uncertain amounts. Track disputes and potential reversals separately so expected cash reflects what is actually likely to be collected.

Add a red-flag line for disputes and chargebacks. Reversals are easier to absorb when they are planned as risk, not assumed as spendable cash.

If you use a decision rule, label it as an internal control rule, not an accounting threshold. Example: define in advance what level of weaker operating cash triggers tighter client terms before adding new delivery commitments.

| Control | Owner | Due date | Evidence | Pass/Fail |

|---|---|---|---|---|

| Close books for the Accounting period | Cash flow statement, Income statement, Balance sheet for the same period | |||

| Review Operating cash flow | Operating section notes tied to records | |||

| Check billing aging and likely collections | Open and paid billing records and aging view | |||

| Confirm expected pay runs | Payroll schedule | |||

| Confirm scheduled Loan payment dates | Payment calendar or lender records | |||

| Review disputes and Chargeback risk | Dispute, refund, or chargeback log | |||

| Set next-month cash controls | Written actions and owners |

Mark non-applicable rows as N/A instead of deleting them so the review stays consistent from month to month. For a related framework, see How to Build a 3-Statement Financial Model.

Turn statement signals into better client terms and billing rules#

The statement is most useful when it changes behavior. Map one statement signal to one contract, billing, or spending action so your next decision is tied to evidence, not mood.

Pick one statement trigger for each rule. Anchor each rule to a specific line in Operating activities, Investing activities, or Financing activities, then define how you will verify it.

| Statement signal | What it suggests | Rule to apply | Verification evidence |

|---|---|---|---|

| Operating activities are weak or negative for the Accounting period | Delivery is not converting into usable cash fast enough | Collect part of payment earlier in the project and confirm terms before work starts | Signed contract, issued bill, proof of receipt |

| Operating activities swing sharply period to period | Collections are too uneven for predictable outflows | Replace one large final bill with milestone or time-period billing | Billing issue dates, paid and open billing list |

| Large end-loaded invoices keep appearing | Too much cash depends on final acceptance or one late payment | Use progress invoicing so part of the work is billed during delivery | Project schedule matched to billing schedule |

| Financing activities are carrying routine cash needs | External funding is covering operating pressure | Add approval checks before discretionary spend in Investing activities | Cash flow statement, purchase request, approval note |

A good check is simple: for every rule change, you should be able to point to one statement signal and one record that supports it.

Rewrite contract and invoice timing around that trigger. Put payment terms in both the contract and the bill so timing and method are explicit. If you default to Net 30, remember what that means. The buyer gets 30 days from the billing issue date to pay in full. That can add liquidity pressure when collections already lag.

If operating cash is volatile, consider shortening billing cadence. More frequent billing, including weekly billing or billing right after a completed phase, can support faster payment and steadier inflows. For longer projects, use progress invoicing by milestones, time periods, or phases so cash comes in during delivery instead of at the end.

Define late-payment actions before invoices go past due. Make late-payment handling specific and operational. Set a clear due date, a clear late-payment process, and a defined next action such as a reminder schedule, work pause, or no next milestone until payment is received.

Clear terms reduce billing ambiguity when payment is late or missing. Check your aged billing report in the next accounting period. If bills stay in the same aging bucket, the rule is not working yet.

Tighten discretionary investing controls when financing is filling the gap. If Financing activities rise while Operating activities stay weak, treat that as a warning signal and consider tighter discretionary spending controls in Investing activities.

Use an internal control such as deferring optional asset purchases or requiring written approval until operating cash stabilizes. Keep the evidence together for each decision: current cash flow statement, purchase request, and a short note on why the spend is essential or deferrable.

You might also find this useful: How to Read an Income Statement (P&L). If collections are inconsistent, standardize deposits, milestones, and due dates with this free invoice generator.

Recover quickly when cash pressure hits mid-month#

When cash gets tight mid-month, speed matters more than elegance. A practical triage order is to protect hard-date obligations, keep delivery billable, and pause optional outflows until the cash picture is verified.

Protect payroll first. Treat payroll as a date-fixed cash out when US FLSA wage rules apply: required wages are due on the regular payday for the covered pay period.

Then ring-fence only the minimum spend needed to keep active client work deliverable and billable. Move discretionary tools, equipment, and other noncritical spend into a review queue until pressure eases.

Pull a same-day cash snapshot. Build one rapid snapshot from:

- Open billing status, ideally with an accounts receivable aging report

- Near-term obligations with due dates, including any scheduled Loan payment

Use the aging view to separate invoices that are more current from those that are more overdue. Count only inflows tied to a real billing status, and only outflows tied to a due date or payment schedule.

Hold back cash exposed to chargebacks. If a Chargeback or payment dispute is active, treat that cash as unstable. Disputes can reverse the payment and pull funds from your account, and dispute fees may also be deducted.

Keep a buffer and do not commit that money to new spend while dispute risk remains.

Log each intervention for the next accounting period. Document each action: collection follow-ups, paused spend, renegotiated due dates, and delivery changes. Keep each entry short and consistent with date, amount affected, reason, and expected cash impact.

In the next Accounting period, compare projected impact with actual cash movement. If an action did not improve collections, reduce outflows, or protect obligations, change the playbook instead of repeating it.

Keep tax and cross-border records aligned with cash reality#

Your cash records should support what you file without a reconstruction project later. If a deposit, transfer, or payout cannot be traced to a bill, a bank or payout record, and the tax document it affects, treat that record as incomplete before period close.

Match each period to the tax file it feeds. Set up one folder per accounting period, then attach the tax artifacts that period supports. For U.S. self-employment income, keep records that support amounts reported on Schedule SE (Form 1040), which is used to calculate self-employment tax on net earnings.

Keep the evidence pack simple:

- Billing export

- Bank statement or payout statement

- Receipts or canceled checks for expenses

- Any Internal Revenue Service (IRS) correspondence tied to that period

The standard is practical: your records should clearly show income and expenses and support the items reported on the return.

If you need U.S. residency certification for treaty or foreign tax-benefit purposes, store the whole chain together: Form 8802, issued Form 6166, and the payer or withholding correspondence that triggered the request. If you need process details, see How to Get a Certificate of Residence (Form 6166) from the IRS.

Checkpoint: pick one international payment and confirm you can trace it from billing to bank deposit to the IRS or treaty document behind the tax treatment.

Split FBAR and Form 8938 support into separate files. Keep FBAR and Form 8938 records in separate, clearly labeled files. They can overlap, but one filing does not satisfy the other.

FBAR (FinCEN Form 114) is filed electronically through FinCEN's BSA E-Filing system, not with the IRS. For U.S. persons with a financial interest in, or signature or other authority over, foreign financial accounts, filing is required when aggregate account value exceeds $10,000 at any point in the year. It is due April 15, with an automatic extension to October 15. Required FBAR records must be retained for 5 years and include account-identifying details such as the name in which each account is maintained and the account number or other designation.

Form 8938 is attached to your annual tax return under FATCA, and filing it does not replace FBAR. Some taxpayers must file both, and penalties are separate.

| Where you live | Filing status | Form 8938 threshold |

|---|---|---|

| In the U.S. | Unmarried or married filing separately | More than $50,000 on the last day of the tax year, or more than $75,000 at any time |

| In the U.S. | Married filing jointly | More than $100,000 on the last day of the tax year, or more than $150,000 at any time |

| Outside the U.S. | Unmarried or married filing separately | More than $200,000 on the last day of the tax year, or more than $300,000 at any time |

| Outside the U.S. | Married filing jointly | More than $400,000 on the last day of the tax year, or more than $600,000 at any time |

A common failure mode is filing one form and assuming the other is covered. It is not. Form 8938 failures may trigger a $10,000 penalty, increase up to $50,000 for continued failure, plus a 40 percent penalty on understatement tied to undisclosed assets.

Keep international invoice evidence by country and period. For international invoicing, organize records by country and period so each payment is explainable in minutes, not hours.

For each period, keep these together:

- Invoice PDF

- Contract or statement of work

- Payout processor statement

- Bank receipt

- Customer tax or withholding correspondence

If cash received differs from the billed amount, add a one-line reconciliation note explaining whether the difference came from fees, currency conversion, or payer withholding. That keeps your cash records aligned with both filing support and later financial statement analysis.

Retention baseline: keep general tax-return support through the IRS general 3 year assessment period, and keep foreign-account records for 5 years where FBAR applies. If one record supports both, keep it for the longer period. Need the full breakdown? Read How to Build a Freelance Financial Model That Protects Cash Flow.

Use this copy-paste checklist at month end#

Use this sequence at month end to reduce cash surprises. Align the reporting window, review operating cash, explain the gap from Net income to cash, then check whether Investing activities or Financing activities could increase next-month pressure.

| Step | What to check | Evidence to save | Pass/Fail |

|---|---|---|---|

| Step 1 | Confirm the Cash flow statement and Income statement are aligned to your review period, and the Balance sheet date matches the close date you are reviewing | Statement exports or PDFs and bank cash snapshot for the same close | |

| Step 2 | Start with Operating activities and compare cash from core work against fixed outflows like pay runs | Cash flow statement, payroll schedule, bank cash snapshot | |

| Step 3 | Reconcile the main gap between Net income and cash using Non-cash items and billing timing | Cash flow detail, billing aging, customer receipts report | |

| Step 4 | Check Investing activities and Financing activities for choices that add future cash obligations | Asset purchase records, loan or repayment schedule, financing records | |

| Step 5 | Tighten billing controls if collections slip, account for chargeback risk, and save the month-end evidence pack before close | Open and paid billing lists, dispute or chargeback log, payroll and tax records, bank exports |

Step 1. Align the period before making decisions. Your Cash flow statement and Income statement are period-based, while the Balance sheet is point-in-time. For month-end analysis, align them to one defined close window so you are not reacting to timing noise.

Step 2. Start with operating cash. Operating activities show cash from your principal revenue-producing work, so this checklist starts here. If operating cash is repeatedly weak while pay runs stay fixed, treat it as an early warning even when total cash still looks fine.

Step 3. Explain profit-to-cash differences in writing. Do not guess when profit and cash diverge. Under the indirect method, reconcile from Net income through Non-cash items and accrual timing, then name the top drivers. Common drivers include non-cash adjustments and billing timing.

Step 4. Flag pressure created by investing or financing. Separate essential purchases from deferrable spend in Investing activities. Then check Financing activities for cash coming from borrowings or other funding that may increase next-month commitments.

Step 5. Close with billing controls and records. If collections are slowing, shorten the gap between delivery and invoicing and reduce dependence on one payment date. If dispute risk is active, plan for reversals early because chargebacks can pull funds from your account and may also add a dispute fee.

Save the evidence pack before close: statement exports, billing aging, paid-billing detail, dispute logs, payroll records, and bank files. Keep records long enough to substantiate your return positions, and keep employment tax records for at least four years after filing the fourth quarter for the year. After you finish the checklist, keep improving your cash controls with practical templates and calculators in Gruv tools.

Frequently Asked Questions

What are the three sections of a cash flow statement?

A cash flow statement has three main sections: operating activities, investing activities, and financing activities. Operating covers cash from core revenue-producing work, investing covers buying or selling long-term assets and investments, and financing covers changes in borrowings and equity. A quick check is that beginning cash plus net increase, or minus net decrease, equals ending cash for the period.

What does positive cash flow vs negative cash flow actually mean for a freelancer?

Positive cash flow means cash increased during the period, and negative cash flow means cash decreased. For a freelancer, positive cash flow is generally linked to a stronger ability to stay solvent and grow, while negative cash flow means cash is moving the other way. Also check where the change came from, because higher cash from financing is different from higher cash from operations.

In what order should I read a cash flow statement if I need fast decisions?

There is no universal required reading order. For fast decisions, one practical sequence is to start with the cash reconciliation, then review operating activities, then investing and financing. That sequence helps you confirm the cash movement first, judge whether core operations are producing cash, and then see what asset moves or funding changed the result.

Why can my business show profit but still run short on cash?

Profit and cash are not the same thing. Under accrual accounting, revenue can be recorded before payment is received, while cash accounting records income when cash arrives. With the indirect method, operating cash starts from profit or loss and adjusts for non-cash items and timing differences, which is where the gap becomes clear.

Which section should I trust most when deciding whether to hire or subcontract?

Start with operating activities because they reflect the principal revenue-producing side of the business. Do not make a hire-or-subcontract decision from one section alone. Cross-check investing and financing activity and confirm your overall cash position before you add commitments.

How often should a small team review its cash flow statement?

Review it on the same cadence as the reporting period used by your statements. The statement is period-based and reconciles beginning-to-ending cash for that period, so your review cadence should match that structure.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- consumerfinance.gov/ask-cfpb/how-can-i-get-a-refund-on-a-product...trusted

- dol.gov/agencies/whd/compliance-assistance/handy-ref...trusted

- irs.gov/businesses/small-businesses-self-employed/wh...trusted

- irs.gov/businesses/small-businesses-self-employed/em...trusted

- online.hbs.edu/blog/post/how-to-read-a-cash-flow-statementtrusted

- sba.gov/funding-programs/loans/make-payment-sbatrusted

- sec.gov/newsroom/speeches-statements/munter-statemen...trusted

- sec.gov/files/cash-flow-statement-bblocks.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Hiring a Subcontractor for the First Time Without Costly Surprises

**Start with a risk-control sequence, not an ad hoc handoff.** As the Contractor, your goal is simple: deliver cleanly, control scope, and release payment only when the work and file are complete.

How to Get a Certificate of Residence (Form 6166) from the IRS

Start with purpose, not paperwork. Before anyone opens Form 8802, get clear on why the foreign payer or tax authority wants a U.S. residency certificate. That answer drives almost everything that follows: whether you should file at all, how the request should be framed, what tax period matters, and how much lead time you really need. If the reason stays vague, the rest of the process gets expensive fast.

The Best Bank Accounts for Freelancers in Germany

Pick the account that protects cashflow and keeps records clean when client behavior gets messy, not the one with the nicest app.