Quick Answer

To invoice a Swiss GmbH without payment delays, lock one legal payee identity across the contract, invoice, bank account, and any requested tax form. Before sending, verify buyer details, references, service period, currency, payment instructions, and whether a W-8BEN or W-8BEN-E is needed. After submission, keep proof and follow a consistent receipt-check and due-date follow-up process.

From W-8BEN to QR-Bill: A U.S. Consultant's Playbook for Bulletproof Swiss Invoicing#

Treat Swiss invoicing as a pass-or-fail process. Do not send invoice #1 until your legal payee identity, tax form path, currency, and payment details match across the contract, invoice, and receiving account.

Lock the record before work starts#

Start here because payment problems often begin with an identity mismatch, not a missing invoice field. Clear this checkpoint only when one legal name is consistent across your signed contract, invoice template, bank account records, and any requested tax form. If those records conflict, pause and fix identity before billing.

That sounds simple, but this is where avoidable delays often start. The contract may show one payee name, your invoice template may still carry an older version, and the receiving account may be set up under a slightly different holder name. Swiss AP teams may treat those differences as a stop signal because they cannot tell whether the mismatch is harmless, an onboarding error, or a payment-fraud issue.

If you send first and clean up later, the invoice can end up stuck between procurement, AP, and vendor management.

Handle W-8 requests based on payer context. Use W-8BEN if you bill as an individual, and W-8BEN-E if you bill through an entity. Provide the form to the payer or withholding agent that requested it, not to the IRS. If a requested W-8 is missing, instructions warn withholding may default to 30%.

Before work starts, make this a one-time setup task rather than an every-invoice debate. Decide which legal payee you will use for the engagement, make sure the contract reflects that payee exactly, and use that same identity on your template and receiving account. If the client asks for tax documentation, answer that request using the same payee logic instead of treating the tax form as a separate track.

The more you split identity decisions across contract, invoice, and tax paperwork, the more likely AP is to see three slightly different versions of you.

If records do not match, escalate in this order:

- Confirm the legal payee name on the signed contract.

- Confirm the exact account holder name at your receiving bank.

- Reissue the invoice template or contract amendment so all records match.

When you escalate, resolve the mismatch at the source record, not just on the current invoice. If the contract is right and the template is wrong, fix the template. If the bank holder name does not match the agreed payee, solve that before the next billing cycle. The goal is not merely to get one invoice through. The goal is to stop the same mismatch from reappearing each month in a slightly different form.

| Decision | Choose it when | Who owns risk | Tradeoff you accept |

|---|---|---|---|

| W-8BEN | You bill as an individual and the payer or withholding agent requests a W-8 | You (form accuracy) | Simpler form, but not valid for entity billing |

| W-8BEN-E | You bill through an entity and the payer or withholding agent requests a W-8 | You (entity classification and form accuracy) | More fields, but aligned with entity billing and usable by payer when properly completed |

| Invoice in CHF | Swiss-side execution is the operational priority | Contract terms and your post-payment conversion process | Smoother local processing, less predictable USD outcome |

| Invoice in USD | USD outcome predictability is your priority | Contract terms and payer execution process | Cleaner USD planning, possible AP friction |

| Receipt-check follow-up | You sent the invoice and have no intake confirmation after a few business days | You (early detection of submission issues) | More admin early, fewer "not received" surprises later |

| Due-date follow-up | Invoice is unpaid at due date or next business day | You (escalation discipline) and payer (processing delay) | More direct escalation, clearer dispute timeline |

| Standard bank wire setup | You invoice Switzerland occasionally and can tolerate fee or FX variability | You (reconciliation effort) | Familiar process, potentially noisier references and net outcome |

| CHF-capable or multi-currency receiving setup | You invoice Swiss clients regularly or want more conversion control | You (provider due diligence and setup quality) | Better currency control, more upfront setup checks |

Build an invoice AP can approve without questions#

Swiss AP teams can reject avoidable mismatches long before they question your work. Run a field-by-field pre-send check and stop on anything that does not line up. Confirm buyer legal name and address, your payee details, service period, and totals against onboarding records or PO data before sending.

| Invoice item | Verify against | Check |

|---|---|---|

| Buyer legal name and address | Onboarding record or PO | Pull from the onboarding record or PO, not from an older invoice |

| Payee details | Locked template | Pull from the locked template, not from memory |

| Service period | Contract or SOW | Check dates and description do not drift |

| Total, currency, and reference fields | What the client expects to process | Verify they still match before sending |

A simple way to do this is to compare each invoice field to one source of truth before you export the PDF. Pull the buyer legal name and address from the onboarding record or PO, not from an older invoice. Pull your own payee details from the locked template, not from memory. Check the service period against the contract or SOW so dates and description do not drift.

Then verify that the total, currency, and any reference fields still match what the client expects to process. This takes a few minutes and can save far more time than a correction cycle after rejection.

For Swiss VAT-oriented invoicing, include the core required elements: supplier name and address, VAT number where applicable, recipient name and address, accurate service description, consideration, and VAT rate where applicable.

Keep the service description accurate and specific to the engagement, but do not overcomplicate it. AP generally needs enough detail to connect the invoice to the work approved under the contract, SOW, or PO. If the buyer uses internal coding or a required reference, place it where their intake process expects it instead of burying it in a narrative paragraph.

A clean invoice should read as if it was built to match the buyer's workflow rather than your own shorthand.

Take a verification-first approach to VAT. Swiss VAT changes took effect on 1 January 2025, and ESTV English pages are informational only. Until official-language wording is verified for the engagement, mark the VAT line as VAT treatment pending official-language tax/legal verification. After validation, freeze the approved wording in the client template. If your facts indicate Swiss VAT exposure, check the foreign-company rule: VAT liability can arise at worldwide turnover of CHF 100 000 p.a. with Swiss-taxable supplies, and registration is due within 30 days once liability starts.

The practical point is to separate invoice drafting from legal wording. Draft the invoice structure first, then insert the verified VAT line once you know the correct treatment for that engagement. Do not improvise tax text on the day you send the invoice, and do not rely on an English summary if you have not confirmed the official-language position.

Once verified, reuse the exact approved wording for that client so you are not reopening the same question on every billing cycle.

Keep one payment identity on the page#

Payment instructions should say the same thing everywhere they appear. If the client pays on Swiss domestic rails, consider using a QR-bill path when your invoicing stack supports it. The QR-bill carries payment data in both QR and plain-text form, and payer-side manual entry remains possible when needed.

Apply one canonical payment identity rule: one beneficiary, one account, one reference. If QR generation is unavailable, use plain text with only those same details plus amount and currency.

In practice, choose one source for payment instructions and reuse it everywhere without editing by hand. Problems often appear when the PDF carries one beneficiary line, the email body contains a shortened version, and an attachment or footer shows an older account. Each version may look close enough to you while still creating doubt for the payer.

AP should never have to decide which payment block is current. Your job is to remove the choice.

Fail pre-send if any channel conflicts with that identity set:

- Invoice PDF

- Email body

- Footer or remittance note

- Attachments

This matters most when payment details change or when you use more than one receiving setup. If you invoice in CHF for one client and USD for another, or if you keep different receiving accounts for different use cases, build a pre-send habit that checks the final package as a bundle. Open the PDF, compare the email draft, and review any remittance note.

Confirm that all visible payment instructions point to the same beneficiary, account, amount, currency, and reference. If you are using a QR-bill, make sure the plain-text payment details mirror the QR data rather than introducing a second version.

Control the cash trail after sending#

Once the invoice is sent, the job shifts from formatting to proof and follow-up. Your goal is simple: keep evidence and follow a set cadence. Keep one invoice-level file trail containing the signed contract or SOW, final invoice, upload proof or sent email, acknowledgment, requested W-8, acceptance evidence, and payment confirmation.

Think of this file trail as your dispute kit and your payment-status record at the same time. If the client later says the invoice was never received, you need the submission proof. If they say the amount was not approved, you need the signed contract or SOW and any acceptance evidence. If they question who should have been paid, you need the final invoice and the payment instructions that were actually in force.

Keeping these documents together turns a vague follow-up into a fast, evidence-based escalation.

Use the same follow-up format every time: invoice number, amount, currency, original send date, due date, and submission route. If you used a portal, store screenshots or status emails as they appear.

Consistency matters because follow-up is easier when you do not have to reconstruct the facts each time. Your first check can be a receipt check if intake confirmation does not arrive after a few business days. Your due-date follow-up can then reuse the same core fields and add only the current status.

That rhythm helps you distinguish three different failure modes quickly: the invoice was never received, the invoice was received but is missing something, or the invoice is approved and simply delayed in processing.

Retain the full trail for ten years under the Article 958f baseline, counted from fiscal year-end. That gives you a fast dispute path: what was agreed, what was delivered, what was submitted, and which payment instructions were valid.

Do not reduce the record to the invoice PDF alone. The PDF shows what you billed, but not whether the client received it, whether they asked for a W-8, whether a portal accepted the upload, or whether a payee change was verified. The stronger your trail, the less likely a late-stage dispute turns into a memory contest.

If you want a deeper dive, read The Silent Profit Killer: How to Stop Margin Erosion in Your Freelance Business. Before you lock currency and fee ownership, run your scenario in the payment fee comparison tool.

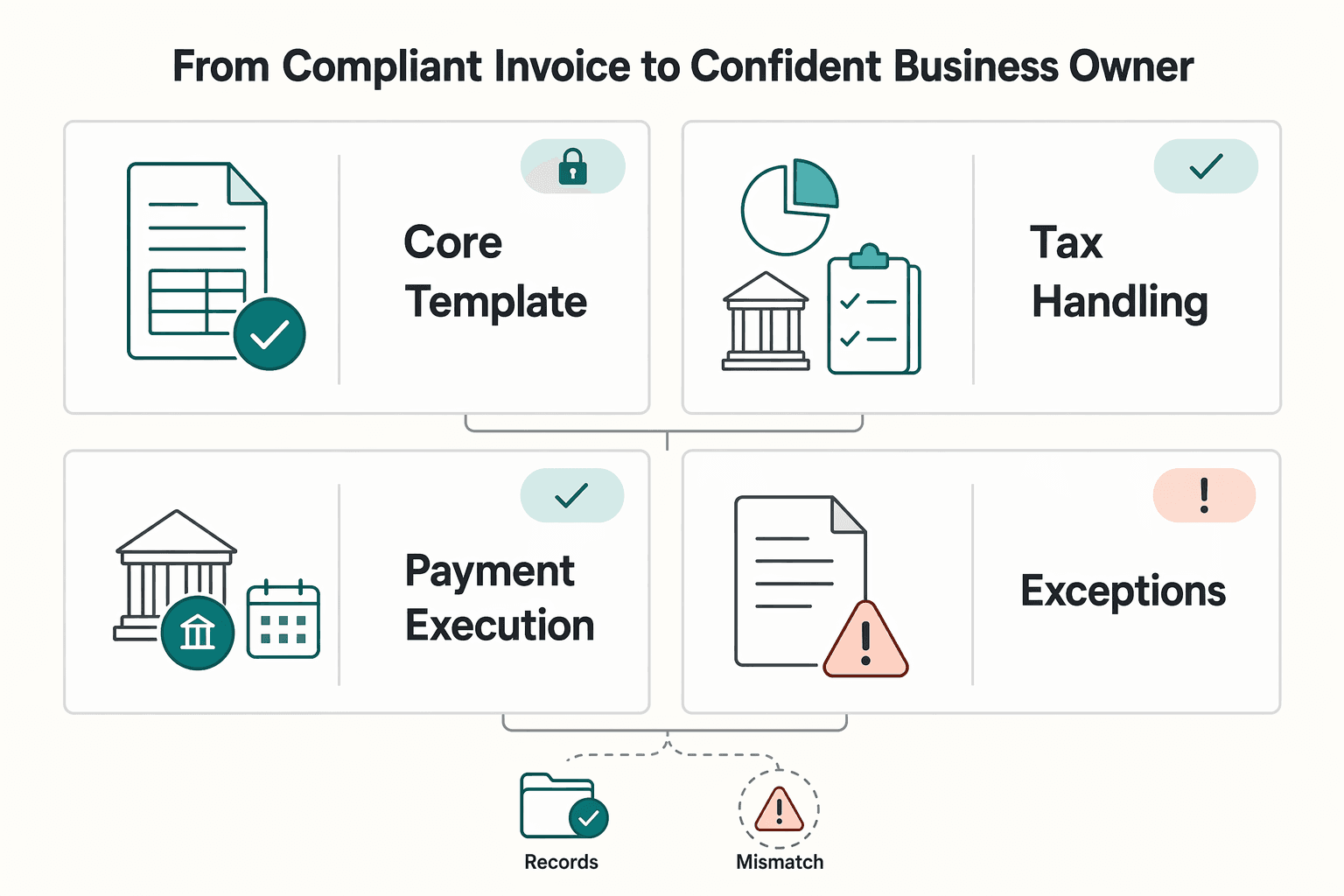

From Compliant Invoice to Confident Business Owner#

The point of this playbook is simple: keep invoicing predictable by locking what should not change and checking what can. Run invoicing as a control system, not a one-off task. Standardize the stable details, verify the variables, and escalate mismatches before they turn into payment holds.

| Dimension | Reactive invoicing | Controlled invoicing | Decision trigger |

|---|---|---|---|

| Core template | Fields are rebuilt each cycle, then fixed after submission | One approved template keeps identity and payment fields stable | Standardize supplier identity on the template now, and include recipient name and address when the receipt is over CHF 400 |

| Tax handling | W-8 and VAT issues surface late in email threads | Tax setup is decided before send and reused | If the payer or withholding agent requests documentation, use the form that matches payee type; VAT treatment pending official-language verification until wording is confirmed |

| Payment execution | AP rekeys details and flags inconsistencies | Payment data is structured for quick checks | If using a QR-bill, make the payment section and receipt complete, and keep payment data consistent in QR and plain text before send |

| Exceptions | Conflicts drift across contract, PO, portal, and bank records | Conflicts pause the invoice and route to one check path | Escalate any mismatch across contract, PO, vendor profile, or payment details before resubmission |

Keep the definitions tight so reviews move faster. Withholding documentation means Form W-8BEN when you invoice as a foreign individual, or Form W-8BEN-E when you invoice as a foreign entity. Provide it when requested by the payer or withholding agent. VAT positioning means the invoice reflects verified Swiss treatment and, where applicable, required supplier identity, VAT number, VAT rate, and VAT amount treatment. Because Swiss VAT changes took effect on 1 January 2025, unresolved VAT text should state that VAT treatment is pending official-language tax/legal verification until legal wording is confirmed. QR-bill execution means the payment section and receipt are complete and internally consistent so payment data can be checked before approval.

If you want this to work in real life, reduce the process to a repeatable loop. Before the engagement starts, lock identity, tax-form path, currency, and receiving setup. Before each invoice goes out, run the same short pre-send review against the contract, PO, onboarding record, and payment details. After submission, save proof and follow the same cadence for receipt checks and due-date escalation.

That rhythm is what turns compliance guidance into a billing system you can actually operate.

Close every invoice with the same loop: review, document, improve. Review mismatch points first: name, address, VAT number, amount, currency, and payment data. Keep one retrievable invoice folder with the contract or SOW, final invoice, PO or buyer reference, requested W-8 form, submission proof, acceptance evidence, and payment confirmation. Then retain the record trail for 10 years from fiscal year-end (Art. 958f baseline).

Improve by mapping each delay to a process fix for the next cycle. Missing recipient data should update the template. Failed payment execution should update the payment block. Sudden payee-detail changes should stay paused until the approved record is verified.

Related: Tbilisi, Georgia: The Ultimate Digital Nomad Guide (2025). Once your controls are set, turn them into a repeatable template with the free invoice generator.

Frequently Asked Questions

What should you validate before sending the invoice?

Before sending, validate four things: identity, PO or reference, currency and payment instructions, and tax-form status. Make sure your legal payee name, the client legal name, addresses, and any required VAT number match the contract and onboarding records. If any of those checks fails, pause and verify before submitting.

What counts as required versus just helpful?

Required means anything needed to release payment under the contract, the buyer's AP intake rules, or Swiss invoice criteria when VAT applies. Helpful details can speed approval but are not release conditions. Verify requirements by intake channel, because a field that is optional by email may be mandatory in a portal.

Do you need the client's UID on the invoice?

Include the client's UID if the buyer requires it in onboarding or intake instructions. Copy it exactly from the client record in the format provided, such as CHE-123.456.789 or CHE123456789, rather than retyping from memory. If documents show conflicting UID values or formats, verify the correct record and save that source in the invoice file.

Do you need special VAT wording?

Do not finalize VAT wording until you verify the current official-language position for the engagement. If the rule, wording, or threshold is unresolved, mark the VAT line as pending official-language tax/legal verification, then lock the final language into the client template once verified. If your facts indicate possible exposure, verify the CHF 100 000 p.a. worldwide-turnover trigger, the 30-day registration timing from liability start, and the Swiss tax representative requirement for foreign registrants.

Should you send a PDF, a portal submission, or a QR-bill?

Use the buyer's required intake channel first, then match the file format to that channel. Use a QR-bill only when your setup supports it and payment is within Switzerland or Liechtenstein, with beneficiary, account, currency, and reference kept identical across all steps. Store submission proof with the final invoice.

My client asked for a W-9 or another tax form. What should you send?

First confirm whether the request is actually for withholding documentation from the payer or withholding agent. If W-8 documentation is requested, use W-8BEN when you bill as an individual and W-8BEN-E when you bill through an entity, and submit it to the requester as instructed. If the requested form does not match your legal payee setup, pause and resolve that mismatch before the invoice reaches AP.

Should you invoice in CHF or USD?

Use the currency stated in the contract or PO and keep it consistent in both the invoice totals and payment instructions. If currency is still open, align the choice with your contract terms for fees and FX exposure and lock it in writing before work starts. Pause if any document or remittance detail conflicts.

How long should you keep records?

Keep records for 10 years, not just the invoice PDF. Store the contract or SOW, final invoice, PO or reference, submission proof, requested tax forms, acceptance evidence, relevant accounting records, and payment confirmation in one retrievable folder. If an e-invoice lacks signature proof, keep alternative evidence such as POs, delivery notes, accounting entries, or proof of payment.

What if the payment instructions or payee suddenly change?

Treat any sudden change as a payee change verification event. Verify it through a trusted existing contact and a phone number you looked up independently, not one provided in the change request. Do not redirect payment based on a single email alone, and file the request, verification notes, callback record, and approved revised invoice together before applying the change.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 5 external sources outside the trusted-domain allowlist.

- fbi.gov/how-we-can-help-you/scams-and-safety/common-...trusted

- irs.gov/individuals/international-taxpayers/forms-fo...trusted

- irs.gov/pub/irs-pdf/fw8ben.pdftrusted

- estv.admin.ch/en/vat-liability-foreign-companiesexternal

- estv.admin.ch/en/vat-changes-from-1-january-2025external

- kmu.admin.ch/kmu/en/home/concrete-know-how/finances/taxes...external

- kmu.admin.ch/kmu/en/home/concrete-know-how/finances/accou...external

- postfinance.ch/en/support/payments/invoices/qr-bill-explain...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Stop Freelance Profit Margin Erosion Before It Hits Cashflow

Revenue can hold steady while the business underneath it gets weaker. What comes in matters, but what you keep after the work is delivered is the clearer signal of health.

Tbilisi Digital Nomad Guide for 2026 Long Stays in Georgia

Start with sequence, not excitement. If your income depends on delivering work on schedule, secure your legal footing, assemble your documents, and keep month one reversible before you optimize comfort.

How US Financial Consultants in Switzerland Use the Tax Treaty

As a U.S. financial consultant in Switzerland, your biggest risk may not be a market downturn. It may be one misunderstood treaty line that costs you thousands. Building a successful business around your expertise is hard enough. Cross-border compliance adds a steady layer of uncertainty.