Quick Answer

Match by accounting period, not by bank movement. Recognize revenue when the service event is satisfied, recognize payout-side cost when incurred, and treat settlement lag, reserve holds, and disputes as separate timing states that may cross closes. Start with transaction-date logic when timing is stable, then move to settlement-lag accrual, reserve-aware posting, or dispute-adjusted reversals if period results keep swinging from cash timing differences.

Why this matters for platform operators now#

For platform operators, cash timing often does not match accounting timing, so payout date should not be your default anchor for revenue or payout-cost recognition.

- Accounting rules point to accrual timing, not cash timing. IAS 1 requires accrual-basis financial statements except for cash flow information. IFRS 15 ties revenue to the transfer of promised goods or services. IRS Publication 538 says income is reported when earned and expenses are deducted when incurred. In practice, the first timing question is simple: when was the obligation satisfied?

Your accounting records therefore need a clear economic event date, such as service completion or order fulfillment, not just a settlement or bank payout date. A useful close check is to compare source-event timestamps to posting dates.

- Platform funds move through operational states before cash is usable. Provider balances can sit in pending status until settlement, and payout frequency settings do not change how long pending funds take to become available. Stripe's example of daily payouts with a 3-business-day payout speed shows the point: cash paid today can reflect activity from earlier days.

In practice, you are often managing three different dates at once: accounting event date, settlement date, and payout date. Keep separate evidence for each, including pending-versus-available balance reporting and payout or batch records.

- Reserves and disputes can stretch timing gaps across periods. PayPal describes reserves as held funds for risk coverage, including a rolling-reserve example of 10% held for 90 days, and notes reserve reviews can occur in 180 days. Stripe notes disputes can immediately reverse a payment, response windows are usually 7 to 21 days, and full dispute lifecycles can run 2 to 3 months.

Because these items can stay open across multiple closes, treat them as explicit accounting states at cutoff, with links back to the original transaction or payout entry. Without that linkage, period attribution for reversals and true-ups becomes hard to verify.

Related reading: Accrual vs Cash Basis Accounting for Small Agencies.

Who this list is for and how to pick your matching method#

This list is for teams that need to explain timing differences at close, not just move cash. Use it if you need a matching method you can trace and defend during tie-outs.

- Best fit: teams accountable for close tie-outs, record integrity, and payout reporting.

If you need to prove records agree and resolve discrepancies, this is your lane. In practice, that means tracing a transaction across event date, settlement date, payout or batch reference, and any later reversal.

- Weak fit: cash-method bookkeeping or occasional manual payouts without batch-level close discipline.

If you recognize activity when cash is received or paid, stricter matching may be unnecessary complexity right now. Operating pattern matters here. Payout setups can be manual or automatic, and automatic weekly payouts run at least once a week.

- Choose your method using three signals: settlement-delay volatility, dispute frequency, and close noise.

Settlement timing can vary by connected-account country and may use business-day or calendar-day counting, with override values up to 31. More variability means more period-matching risk. Dispute timeframes differ by issuer and can stay open long enough to cross multiple closes: in general up to 120 calendar days, and in some Visa and Mastercard cases up to 540. Chargebacks can also debit both the payment amount and a processing fee, so reversals and related fees should stay linked to the original entries.

- Decision signal: if cash timing keeps driving period-to-period profit swings, consider tighter matching.

You do not need a perfect model on day one. But if service timing and cash timing regularly land in different periods, and close explanations keep repeating, consider moving to a stricter accrual-based match.

That choice leads directly to method selection: start with the lightest approach that works, then add complexity only when your close actually needs it.

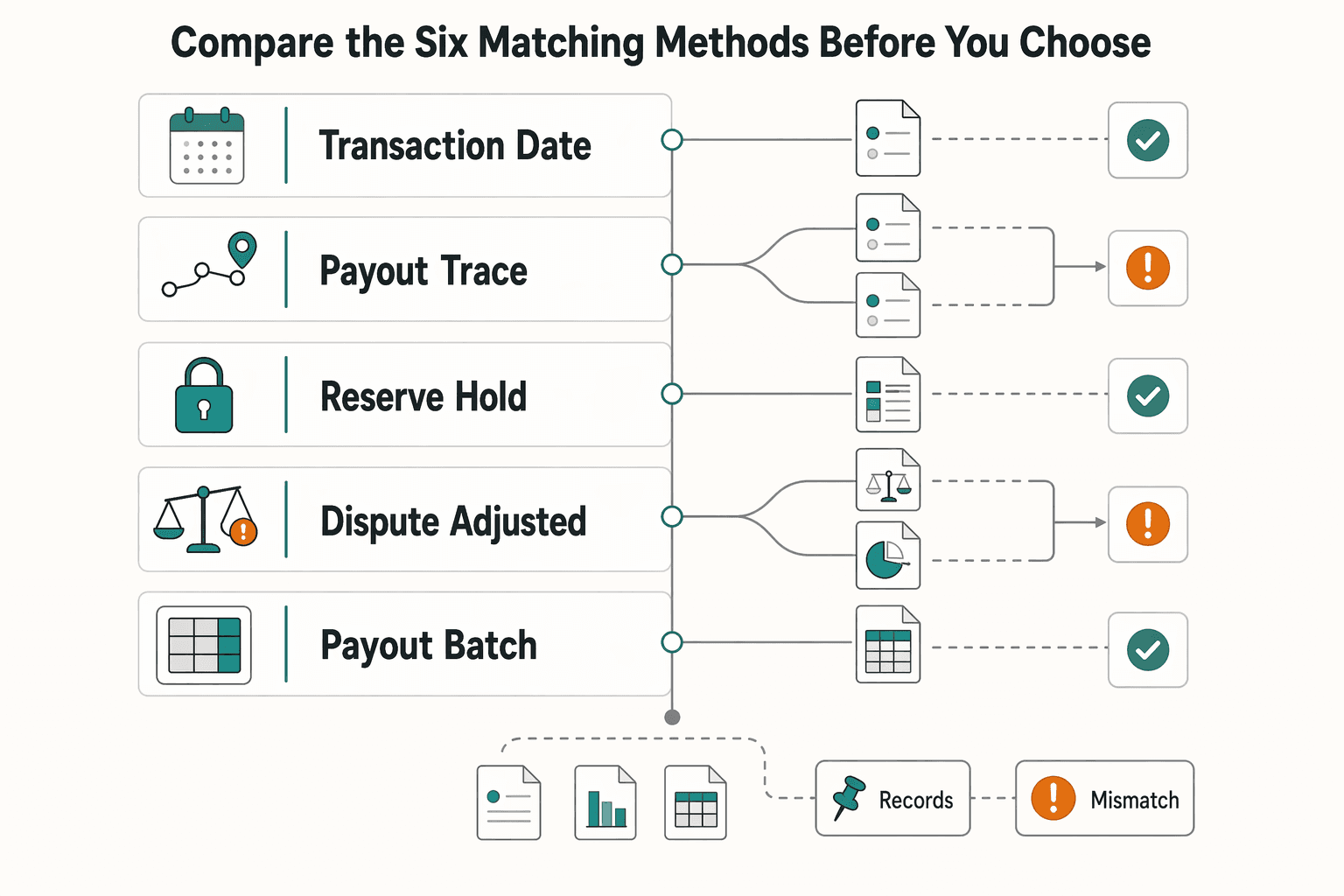

Compare the six matching methods before you choose#

Use the simplest method that keeps revenue and payout costs in the same period, then add complexity only when reserve activity, disputes, or cutoff noise become material at close. This table compares six operational patterns for planning, not a formal accounting standard.

Under accrual accounting and the matching principle, revenue and expenses are recognized when earned or incurred rather than when cash moves. In payout operations, revenue is typically tied to service transfer, while expense timing also has to account for settlement lag, payout scheduling, reserve holds, and later reversals. Payout frequency and fund availability are separate controls. Even daily payouts can reflect transactions captured three working days earlier.

| Method | Best for | Revenue Recognition trigger | Expense Recognition trigger | Reserve Holds | Rolling Payouts | Processor Fees | Chargebacks | Payment Disputes | Required controls | Key pros and cons | Failure risk |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. Transaction date matching | Low-volatility flows with few exceptions | Service transfer (often proxied by transaction event) | Same transaction event date | Usually treated as exception if immaterial | Assumes timing is stable enough not to distort periods | Recognize at transaction level where itemized fee data exists | Post on event; often later-period adjustment | Event-triggered only | Idempotent transaction keys, period cutoff checks, basic exception queue, audit link from event to posting | Simple and fast to close; weaker when holds or reversals grow | Period margin swings when cash timing diverges from event timing |

| 2. Settlement lag accrual | Stable, known settlement delay | Service transfer date | Transaction date plus accrual for expected lag | Usually separate unless reserve program exists | Decouples recognition from payout date; useful when daily payouts still lag capture by three working days | Accrue transaction-linked fees, then true up to provider reports | Adjust when chargeback posts | Usually event-triggered with strict period-end cutoff | Idempotent accrual and reversal journals, unsettled-item cutoff controls, mismatch exception queue, accrual rollforward evidence | Better matching without full reserve logic; requires disciplined true-ups | Misstated accruals if lag assumptions drift |

| 3. Reserve-hold aware matching | Contracts or cohorts with routine held balances | Service transfer date | Policy-based recognition that separates held amounts; recognize held portions when release is evidenced | Core treatment; reserve is a temporary hold for potential dispute or refund losses | Handles rolling releases better than simple lag accrual | May require split timing across transaction and reserve movement | Link to original payout and reserve history | Conservative treatment when reserve or dispute status is unclear at cutoff | Idempotent reserve-state postings, release-signal exception queue, held-versus-released cutoff controls, reserve notices or report evidence | Avoids overstating margin while funds are restricted; more operational overhead | Premature release recognition or unsupported reserve balances |

| 4. Dispute-adjusted matching | Frequent reversals crossing periods | Service transfer date | Initial recognition, then reversal or adjustment on dispute outcomes | May offset exposure but not primary driver | Works if original transaction linkage is intact | Keep transaction-level fee mapping and reverse where required | Explicit reversal tied to original posting | Must handle long windows; disputes are commonly initiated within 120 days, sometimes longer | Idempotent reversal keys, dispute-state exception queues, open-versus-resolved cutoff rules, linked audit trail across original entry and reversal | Improves comparability when disputes are common; harder to govern across closes | Double counting, broken links, inconsistent open-dispute treatment |

| 5. Payout batch matching | Batch-driven payout operations | Service transfer date | Batch approval or execution date, with separate handling for cutoff misses | Often carved out and tracked separately | Fits operationally batch-driven rolling payouts | Can allocate by batch if reports support it; transaction detail is still better for variance | Can fall outside original batch period; separate reversals needed | Usually handled outside original batch unless included in adjustments | Idempotent batch IDs, partial or failed exception queues, approved-versus-sent-versus-settled cutoff controls, batch-file and status-log evidence | Aligns accounting to payout operations and batch tie-outs; can hide bad line items inside clean batches | Batch timing can mask transaction-level errors and cutoff issues |

| 6. Hybrid by rail or product | Multi-rail or product platforms with different risk and timing profiles | Policy by rail or product, anchored to service transfer | Rail-specific policy, such as transaction, lag accrual, reserve-aware, or batch | Explicit only where relevant | Lets stable rails stay simple and volatile rails use tighter logic | Fee mapping follows each rail's matching policy | Rail-specific reversal rules | Rail-specific event-triggered or policy-based treatment | Idempotency by rail and event, owned exception queues, rail cutoff matrix, evidence of policy mapping and exceptions | Practical for mixed models; governance load is high | Comparability drift if similar events get different treatment without clear policy |

Start with transaction date matching when operating complexity is low and close maturity is early. Move to settlement lag accrual when timing lag is the main source of close noise. Add reserve-aware, dispute-adjusted, batch, or hybrid models only after you can run four controls reliably each close. Those controls are idempotency, exception queues, cutoff controls, and audit evidence tied to each posting.

Use transaction date matching when payout timing is predictable#

Transaction-date matching works best when settlement timing is consistent enough that cutoff differences do not regularly move period results. Revenue is recognized when earned, and payout cost can be recognized on the same transaction event, even if cash lands later.

- Use it when settlement lag is stable and understood.

Under accrual accounting, income is recognized when earned and expenses when incurred, not when cash moves. That makes this method workable when payout timing differences are operationally real but still manageable at close. One documented pattern is daily payouts with delay_days. Stripe examples include a 3 business day payout speed and funds becoming available 2 business days later in one case. If timing varies by rail, country, or cohort, this method can hide variance instead of reducing it.

- It is easier to apply when fees are predictable and event-level mapping is clean.

The practical benefit is tighter posting logic tied to the underlying transaction. When processor fees are stable and itemized, you can book expense on the same transaction key as revenue. Stripe publishes 2.9% + 30¢ per successful domestic card transaction for one pricing case. Keep the assumption anchored to consistency, not payout speed. Instant payouts can settle within 30 minutes for eligible accounts, but new users are not immediately eligible.

- Validate it each close with two checks.

First, confirm a complete trace from event timestamp to processor reference to posting to payout or balance movement. Second, tie the processor payments balance to the external bank account and isolate unsettled items at cutoff. Stripe explicitly states the payments balance can be used to reconcile transactions and payouts to an external bank account. Keep lightweight evidence: provider statements, payout status logs, transaction-level fee detail where available, and a period-end exception list.

- Move off this method when reserves, rolling payouts, or disputes become recurring close drivers.

Reserve balances are funds you cannot pay out until the hold period ends, and reserve periods are commonly 30-90 days. Disputes and refunds also reduce the payments balance after the original transaction. If later deductions, held balances, or rolling releases keep forcing manual true-ups, shift to settlement-lag, reserve-aware, or dispute-adjusted matching.

Add a settlement lag accrual layer when cash lands later#

When revenue is earned before funds are available for payout, add a settlement-lag accrual layer. This is often the practical next step when timing differences are material at period end.

Under the accrual method, you record income when earned, not when cash arrives. If revenue is recognized when the performance obligation is satisfied under IFRS 15, settlement timing can be handled separately through balance sheet accruals and later clearing entries.

1. Best fit#

Use this when settlement delays are known, recurring, and measurable at close. A common case is card-heavy flow where transaction events occur before funds become available.

The key is explicit delay tracking between transaction date and settlement availability. Adyen documents configured settlement delay days and gives an example where sales on Monday, January 1 settle two business days later on Wednesday, January 3. Stripe also exposes payout timing through settlement_timing.delay_days, and timing can vary by country and payment method.

2. Why it improves matching#

This approach is meant to keep revenue and related payout cost or payable in the same accounting period even when cash settles later. You book the accrual at period end, then reverse or clear it when settlement posts.

A key benefit is cleaner cutoff discipline. Period-end cutoff drives recognition, not bank-arrival timing. At period end, ask two questions: was the service delivered before close, and is the settlement delay known? Then compare pending versus available balances.

3. What you must control#

This method works best with strong cutoff and close controls. You need a trace from revenue event to processor reference to posting to settlement or payout movement. A practical close pack should include:

- provider statements or balance reports showing pending versus available funds

- the settlement-delay setting or schedule used in accrual logic, such as

settlement_timing.delay_days - a period-end unsettled-items report tied to posted entries

- a tie-out file explaining differences between provider records and accounting records

Payment matching means comparing transaction records across statements and accounting records, and timing differences are a common source of discrepancies. At month-end, confirm each pre-close earned transaction is either settled, in pending balance, or listed on the unsettled exception report.

4. Main tradeoff and failure mode#

The tradeoff is operational discipline. If delay rules change without finance visibility, reports are incomplete, or pending and settled funds are mixed, accruals can be misstated and reverse in the wrong period.

Treat configuration changes as accounting-relevant. Stripe allows eligible accounts to set delay_days_override up to 31, so payout timing changes can shift the accrual population. Use this method when delay assumptions are documented, pending balances are tied out, and unsettled cutoff items are fully explained. Related: Recurring Revenue Recognition vs Cash Accounting for Platform Teams.

Use reserve hold aware matching for held funds#

If your processor can place funds in reserve, treat those held amounts separately from normal settlement lag. Reserve releases are tied to risk exposure or a stated release date, not just transfer timing.

| Reserve check | Confirm |

|---|---|

| Reserve type | Rolling, fixed, or single hold |

| Held amount | Held amount and affected account or cohort |

| Timing | Reserve start date and stated release date or schedule |

| Offsets | Offsets already applied, such as refunds or disputes |

| Provider records | Provider records that separate available funds from reserve-held funds |

1. Best fit#

Use this when reserve-held balances are a recurring part of operations, including higher-risk cohorts and connected accounts with heavier refund or dispute exposure. A reserve is a temporary hold on a portion of funds, and reserve size is based on business risk rather than a single uniform rule.

Reserve structure affects payout-side accounting. Rolling reserves hold part of daily transactions and release later on schedule, such as PayPal's 10% held for a 90-day rolling period. Providers also use fixed reserves and single-amount holds, and Stripe Connect reserve plans cannot hold funds longer than 180 days. Stripe also notes many reserve windows are 30 to 90 days.

2. Recognition rule#

Split payout-side accounting between funds available for payout and funds still restricted by reserve. Even when held money is still economically yours, do not clear it as ordinary settled cash while it remains unavailable for use or withdrawal.

In practice, keep a separate posting bucket for reserve-held balances instead of netting everything into one pending-settlement line. That helps preserve period matching when releases happen later or when held amounts are applied to refunds or disputes.

3. What to verify at cutoff#

At close, confirm reserve status from provider evidence rather than assumptions, and verify at minimum:

- reserve type: rolling, fixed, or single hold

- held amount and affected account or cohort

- reserve start date and stated release date or schedule

- offsets already applied, such as refunds or disputes

- provider records that separate available funds from reserve-held funds

If release status is unclear at cutoff, keep the amount classified as held until status is confirmed. If you also need a reserve-related loss accrual under US GAAP, accrue only when loss is probable and reasonably estimable. If no amount in a range is a better estimate, accrue the minimum amount in that range.

A defensible close pack can include the provider reserve statement or plan export, a balance report with held versus available funds, and an exception report for items missing a release signal.

4. Main tradeoff and failure mode#

The tradeoff is added operational detail. Reserve levels can change with risk, and release behavior can be staged, so a single settlement-date rule may not be enough. If finance only sees net payouts, it becomes hard to tell whether funds were released, still held, or used for dispute coverage.

One failure mode is clearing held reserves too early. That can create reversals and close noise later when the provider applies held funds to losses instead of releasing them in cash.

5. Concrete use case#

A high-dispute connected-account cohort is a practical example. Stripe Connect explicitly identifies heavy disputes as a case for rolling reserves, and processors may require rolling reserves for higher-risk businesses. In that setup, keep the reserve-held portion segregated until release or offset.

Need the full breakdown? Read Accounts Payable vs. Accounts Receivable for Platforms and the Two-Sided Ledger.

Adjust for chargebacks and payment disputes without distorting margin#

Once disputes and chargebacks become a normal part of operations, they need their own matching logic. A practical split is to use accrual estimates for stable cohorts and event-triggered reversals when patterns are not predictable.

| Dispute check | Verify |

|---|---|

| Dispute state | Per transaction: opened, responded, won, lost, or chargeback booked |

| Original link | Link to the original posting and related accounting entries |

| Provider debit evidence | Chargeback amount and processing fee |

| Response deadline | Deadline status, since missing the deadline can auto-lose the dispute |

| Event timestamps | Webhook or event timestamps showing when status changed |

1. Best fit#

Use this approach when chargebacks and payment disputes are recurring operating realities, not rare exceptions. Timing is the core issue. Cardholders generally have up to 120 calendar days to dispute a transaction, and in some Visa and Mastercard scenarios that can extend to 540 calendar days. The financial impact can land well after the original payment period.

If dispute behavior is stable across a large cohort with similar characteristics, estimation can be reasonable. If behavior is volatile or driven by one-off spikes, event-triggered adjustments are usually safer.

2. Recognition rule#

Anchor recognition to the underlying economics, then choose the adjustment method based on the quality of your evidence. A dispute is the bank-level contest. A chargeback is the reversal initiated by the issuing bank. Leaving the original period untouched can weaken period-to-period comparability when losses are part of normal activity.

For predictable cohorts, estimate expected dispute impact at period end and true up as outcomes resolve. IFRS 15 allows an expected value approach for large numbers of similar contracts, but only where it remains highly probable that a significant reversal will not follow.

For less predictable flows, post reversals when provider events confirm the dispute or chargeback.

3. What to verify at cutoff#

At close, validate dispute-state evidence, not just net processor balances, and verify at minimum:

- dispute state per transaction, such as opened, responded, won, lost, or chargeback booked

- link to the original posting and related accounting entries

- provider debit evidence for chargeback amount and processing fee

- response deadline status, since missing the deadline can auto-lose the dispute

- webhook or event timestamps showing when status changed

Traceability is the control point. If your books cannot tie chargeback journals, debits, and dispute events back to the original postings, period analysis gets noisy fast.

4. Main tradeoff and failure mode#

The benefit is cleaner period comparability and clearer Cost Per Payout analysis. The tradeoff is operational overhead: explicit reversal logic and reliable event-to-posting linking.

A failure mode is double counting: booking an estimate at close, then expensing the later chargeback debit and fee without clearing the estimate. Another is relying only on delayed settlement summaries when funds are pulled at dispute initiation.

5. Concrete use case#

For a large cohort with stable dispute behavior, accrue expected dispute loss at month end and adjust as cases are won or lost. For a new or volatile cohort, wait for dispute or chargeback events and post the impact when the provider debit occurs. This split approach preserves matching discipline without pretending you have more predictability than you do.

For a step-by-step walkthrough, see PO Matching Exceptions for Platforms with Partial Receipts and Variances.

Use payout batch matching when operations run in cycles#

When payouts run on a schedule, the batch is often the cleanest accounting anchor. If approval, execution, and settlement happen at different times, batch-level matching can produce a cleaner close than forcing everything back to individual transaction dates.

| Batch check | Verify |

|---|---|

| Batch identifier | Provider batch identifier, such as Adyen Batch Number |

| Batch totals | Batch totals for credits, debits, and transaction counts |

| Input vs output | Submitted batch input versus provider output |

| In-flight items | Failed or still in-flight payments |

| Spot checks | Transaction-level cost detail for spot checks |

1. Best fit#

This approach fits teams that intentionally process payouts in grouped batches with scheduled approval or routing windows. Stripe, for example, separates payout availability from payout execution in its schedule settings. Weekly payouts can run on specified weekly_payout_days, while availability timing is driven by delay_days, and delay_days_override can be set up to 31.

When those timelines differ, transaction-date matching can add noise to period results. Batch matching is often cleaner because it follows how operations actually run.

2. What to anchor on#

Do not force a universal rule for approval date, execution date, or settlement date. Pick the batch milestone that best represents when payout cost is operationally committed in your environment, then apply it consistently.

Tipalti's flow shows why that matters. Instructions are submitted and validated before payer or provider approvals. Submitted payments can remain in flight for several days. Processing date is also distinct from value date, for example US wires PD+1; ACH PD+1/PD+2. If execution reliably follows approval, approval-window matching can be reasonable. If execution frequently stalls, anchor to the later confirmed batch state.

3. What to verify at cutoff#

Batch matching only works if you can prove the batch and monitor the exceptions around it. At close, verify:

- provider batch identifier, such as Adyen Batch Number

- batch totals for credits, debits, and transaction counts

- submitted batch input versus provider output

- failed or still in-flight payments

- transaction-level cost detail for spot checks

Adyen's batch-level report helps prove batch totals in a date range. Its settlement details report supports transaction-level cost checks when totals look right but specific lines do not.

4. Main tradeoff and failure mode#

The benefit is faster, clearer period matching tied to a single operational key. It can also simplify some downstream accounting sync workflows, such as this Xero integration process. The risk is false confidence: a batch can tie out at total level while individual payouts are delayed, failed, or unresolved.

Treat batch tie-outs and transaction-failure monitoring as separate controls, not substitutes for each other.

5. Concrete use case#

Weekly contractor payouts are a good example. Approval date, provider processing timing, and recipient receipt timing can all differ. Routing windows create real timing gaps, such as a same-day ACH window with a 10:30 a.m. ET deadline and 1:00 p.m. ET settlement slot, but those timings are provider- and rail-specific, not universal.

In that pattern, batch matching is usually the most practical anchor for cost recognition and close checks, as long as outliers are reviewed between cycles.

Choose a hybrid model when products and rails differ#

Use a hybrid model when rail or product-path behavior differs enough that one matching rule could distort timing. The order matters: standardize policy definitions first, then apply different methods by rail or product path.

In multi-rail setups, FedNow supports near-real-time transfers at any time, any day, while RTP is also always on and describes settlement as final and irrevocable. ACH and cross-border routes follow different timing patterns, so one cutoff rule across all rails can create avoidable exceptions.

1. Standardize definitions before you split methods#

Hybrid works best when policy language is consistent. IFRS 15 requires consistent treatment for similar contracts in similar circumstances, and IAS 8 defines accounting policies as the principles and practices used in financial reporting. In practice, finance, ops, and product need one shared dictionary before posting logic diverges.

Lock the terms that drive entries: earned revenue, payout initiated, payout executed, settled, reserve-held, disputed, reversed, and retried. Then compare provider status mappings to journal templates so identical labels do not hide different meanings across rails.

2. Split only where accounting risk actually changes#

Split methods only when timing or reversal mechanics are materially different. ACH can settle on a future business day. Same Day ACH's March 19, 2021 expansion added a two-hour submission window, but it did not make ACH equivalent to always-on instant rails. Cross-border timing can vary from less than five minutes to more than two days by route.

That is where hybrid logic earns its keep. It separates real operating differences from arbitrary policy variation.

| Rail or product path | Matching method | Core ledger rule | Month-end close checkpoints |

|---|---|---|---|

| FedNow or RTP payouts | Transaction-date matching | Post payout cost on execution plus accepted provider event; keep reversal handling separate because RTP settlement is final and irrevocable | Verify provider-reference completeness, check duplicate postings, review exceptions to separate failures from timing noise |

| ACH scheduled payouts | Settlement-lag accrual or batch matching | Accrue at the chosen execution or batch milestone, then clear on provider settlement evidence | Check items still pending future-business-day settlement, confirm cutoff against ACH windows, tie batch totals to posted journals |

| Cross-border payouts by route or corridor | Settlement-lag accrual by route | Use route-specific accrual timing and clear only on settlement confirmation | Review aging by corridor, inspect unmatched settlements, flag routes crossing period end beyond expected timing |

| Flows with reserve holds or high dispute variance | Reserve-hold-aware matching plus dispute adjustments | Separate held or disputed amounts from standard payout-expense postings | Confirm reserve status at cutoff, list unreleased held balances, carry disputed items in a true-up queue |

3. Govern hybrid as a policy, not a workaround#

The benefit is better fit by segment. The cost is governance overhead, and that overhead is real if you want reliable external reporting under ICFR expectations and a recognized control framework.

Set one core guardrail: similar products in similar circumstances should not use different recognition rules just because different teams own them. IFRS 15 allows portfolio treatment only when the result is not materially different from contract-level application.

To prevent policy drift, require an evidence pack before adding any new rail or product path. That pack should cover settlement-timing characteristics, provider status definitions, finality or reversibility behavior, sample provider reports, and the exact journal templates. If management reporting already runs by rail or product line, keep the accounting map aligned to that same view so the operating and financial story stays consistent.

Build event to ledger posting rules your team can audit#

Once methods vary by rail or product, posting ambiguity becomes the next close risk. Make each accounting event explicit, traceable, and retry-safe so finance can trust the period result.

1. Lock one accounting trigger to one journal template#

Define one exact trigger for revenue recognition and one exact trigger for expense recognition, then map each trigger to a fixed journal template. Accrual logic should place revenue when earned and costs when incurred in the correct accounting period, not when cash moves.

For each payout path, keep a posting map with the event name, accounting date rule, amount basis, provider reference, currency, journal template, and idempotency key. One event should not produce different journal behavior because of retries or team handoffs.

Idempotency is the control that keeps retries from creating duplicate execution. If you want one convention across providers, 64 characters or less is a conservative key length, and you should not assume old keys are retained indefinitely for duplicate protection.

2. Make drilldown possible from request to reconciliation output#

Every posted payout entry should be traceable end to end: internal request ID, provider reference, journal ID, and matching export line. If one link is missing, exception analysis and cutoff decisions become harder to defend.

Treat drilldown as a close control, not a nice-to-have. A reviewer should be able to start at a GL journal line and reach the underlying payout transaction without engineering help.

At period end, test both directions: journal line to source payout, and provider-side item to accounting records and matching export. If either direction fails, treat it as a control gap before close.

3. Set a fixed failure flow and keep unresolved items visible#

Use one documented handling flow for accounting-impacting events. A common pattern is to block duplicates, route posting failures to a reviewable failure queue (such as a dead-letter queue), and require unresolved items in close review before sign-off. Consistency matters more than improvising case by case.

Failed postings need an owner, age, root cause, and next action. Silent retries without visible queue records create period risk.

If a payout executed but posting failed, finance needs a clear accrual or true-up path before month-end. If provider execution never happened, do not recognize until evidence supports posting.

4. Build the evidence pack at posting time#

Audit-ready posting depends on linked evidence captured when the event is processed. Do not wait until audit season to reconstruct support from screenshots.

For each payout path, store the artifacts that support the posting decision: provider statements, payout status logs, batch files where relevant, matching exports, and posting diffs for corrections or replays. Keep actor and timestamp history for create or modify activity in the transaction trail.

Also store both the original event payload and the normalized accounting record used to post. That is what lets your team explain why a specific journal template and accounting date were applied.

Run a month end close that catches mismatches early#

Month end should force timing mismatches into view before journals are treated as final. The checklist below is meant to surface unsettled payouts, held funds, fees, and disputes early enough to act on them.

-

Start cutoff controls with timing, not bank cash. If payouts follow a schedule, such as T+3, and initial payouts can take 7-14 days after first live payment, bank cash alone is not a reliable period boundary. Review unsettled items, reserve holds, processor fees, chargebacks, and payment disputes against provider status and accounting date using payout matching, reserve, fee, and dispute reporting, not just net payout totals.

-

Use practical close checkpoints before sign-off. Check posting completeness against provider activity, then test variance between operational and accounting totals, then review unresolved exception queues with owner, age, and next action. If an exception remains open at close, document the accounting treatment. Treat "ties at net payout only" as a red flag, because fee and dispute movements can be missed there.

-

Split ownership so separation of duties is real. One workable split is finance owning expense recognition and cutoff treatment, ops owning payout status integrity, and product owning event taxonomy changes that affect posting behavior. Internal-control guidance is explicit that one person should not perform two consecutive tasks in an accounting procedure. Keep dated approvals and effective timestamps when taxonomy changes affect journal mapping.

-

Connect close fixes to matching and unit economics. Push cleared items into your Xero bank-reconciliation workflow so bank transactions are confirmed in accounting records. Feed recurring mismatch patterns into Cost Per Payout analysis using the same close dimensions, including payments, payouts, fees, and balance changes, so control improvements also show up in unit economics.

You might also find this useful: Accounting Automation for Platforms That Removes Manual Journals and Speeds Close.

If you want to operationalize this checklist with clear status surfaces and reconciliation-friendly workflows, review the implementation patterns in Gruv Docs.

Pick one model now and tighten it each close#

If two people on your team would date the same payout cost differently, your method is not reliable yet. Pick one accrual posting approach, write it into your posting rules, and enforce it with the same cut-off controls every close.

- Choose one posting logic and document the trigger.

Publication 538 sets the baseline: under accrual accounting, income is reported when earned and expenses when incurred, regardless of cash timing. The matching principle applies the same logic in reporting: related expenses belong in the same period as related revenue. Document the exact trigger for each entry type, including which date drives revenue, which date drives payout-cost recognition, and which source record controls when dates conflict.

- Make cut-off a control, not a monthly debate.

Cut-off means transactions and events are recorded in the correct accounting period. Define what proves period ownership under your policy, apply it consistently, and test boundary items before sign-off. If month-end treatment keeps changing case by case, the policy is still incomplete.

- Run reconciliation every month and use exceptions as feedback.

Reconciliation compares record sets to check consistency and accuracy, with the goal of finding and resolving discrepancies. Monthly is often a practical baseline. Compare accounting records to provider and operational records, then track exceptions by category, owner, root cause, and status so repeated issues become process fixes instead of recurring cleanup.

- Judge each close on consistency, explainability, and evidence.

Target consistent income-statement logic, not artificially smooth results. Business volatility should remain. Noise from timing drift and unresolved breaks should not. At close, confirm you can trace sample transactions from source to accounting records, explain period movement without relying only on cash timing, and show dated support for unresolved items. That gives you a cleaner base for performance review and a stronger audit trail where your systems support it.

If your team needs to pressure-test which matching model fits your payout rails and controls, you can talk through your setup with Gruv.

Frequently Asked Questions

What does matching revenue and payout costs in the same period mean in practical terms for payment platforms?

It means recognizing revenue when earned and payout-related costs when incurred, instead of waiting for bank cash movement. In practice, the same reporting period should show the related revenue and the fees, reversals, and dispute impacts tied to that activity. If margin swings only because payout timing shifted, the process is probably too cash-led.

What is the difference between payout date and expense recognition date?

The payout date is when funds move through the provider or bank. Expense recognition follows when the cost is incurred under your accrual policy. Those dates can differ because provider balances move through pending and available states before bank settlement, and settlement timing varies by location and payment method. Compare provider balance states and payout matching reports to journal dates, especially when initial live payouts may take 7-14 days.

How should failed payouts, reversals, and retries affect accrual accounting entries?

Update entries when payout outcomes change. Do not leave the original posting untouched. If a payout fails, funds can be returned and the pending transaction voided, so the accounting records should reverse or reclassify to reflect the new state. Also account for method-specific retry behavior, since automatic retries are configurable in some flows and not universal by default.

When should processor fees be accrued versus recognized on settlement?

There is no single universal rule across all rails and jurisdictions, so use a written policy and apply it consistently. If fee impact is visible and tied to the transaction before bank settlement, earlier recognition can be supportable because pending balances can already reflect charge amount minus fee. If timing is uncertain until settlement, recognize at settlement and verify the rule each close so fee movement is not missed.

What should a month-end close checklist include for payout cost matching?

Include unsettled payouts, pending versus available balances, processor fees, disputes, and failed automatic payouts. Use payout matching reporting to preserve transaction-to-payout linkage, and review failed payout sections explicitly rather than assuming they net out later. A close that only ties to bank cash can miss dispute debits, fee movements, or returned payouts that are typically returned in 2-3 business days.

Which records are required to make matching entries audit-ready and defensible?

Keep records that trace each transaction from event through settlement outcome: provider statements, payout matching exports, balance transaction detail, dispute notices, failed payout records, and journal entries with dates, amounts, and reference IDs. Audit-ready support requires sufficient, appropriate evidence and books and records that reflect transactions in reasonable detail. A defensible file links the payment, payout or reversal, fee impact, and close-period journal to the same provider reference.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- canons.sog.unc.edu/blog/2024/04/08/the-bank-reconciliation-a-ke...trusted

- ecfr.gov/current/title-17/chapter-II/part-240/subpart...trusted

- ecfr.gov/current/title-26/chapter-I/subchapter-A/part...trusted

- federalreserve.gov/paymentsystems/fednow_about.htmtrusted

- irs.gov/publications/p538trusted

- irs.gov/taxtopics/tc305trusted

- ojp.gov/tfmc/guidesheets/internal_controls.pdftrusted

- sec.gov/spotlight/fcpa/fcpa-recordkeeping.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Xero Integration for Payout Platforms: How to Sync Contractor Payments with Your Accounting System

A strong Xero integration launch is not just about moving data. It is about creating a sync finance can trace and reconcile early in the close process. Treat this as an accounting integration with clear posting logic and review paths so it reduces manual entry and double handling instead of pushing cleanup downstream.

Unit Economics for Payment Platforms: How to Calculate True Cost Per Payout

---

Bad Payouts Are Costing Your Supply in Two-Sided Platforms

Payout issues are not just an accounts payable cleanup task if you run a two-sided marketplace. They shape supply-side trust, repeat participation, and fill reliability. They can also blur the revenue and margin signals teams rely on.