Quick Answer

Use a dual-view close: manage liquidity from cleared cash, then evaluate results from earned revenue and incurred costs. For an accrual vs cash basis accounting agency workflow, keep AR for delivered but unpaid work and AP for received but unpaid costs, and align both to the service period before approving spend. If cash and profit tell different stories, pause major commitments until the timing gap is explained.

Cash vs. Accrual: What's the Real Difference for Your Agency's Bottom Line?#

This is a control choice, not a theory debate. You need one view for liquidity, cash in and out, and another for performance, work earned and costs incurred. Treat those as the same signal, and a strong month can look weak, while a weak month can look stronger than it is.

Your bank balance answers, "Can we pay people and vendors?" Your books also need to answer, "Did this month's work actually make money?"

What each method tells you at close#

The difference comes down to timing. Cash-basis accounting records revenue when cash is received and expenses when cash is paid. The timing follows bank movement. Accrual accounting recognizes revenue when earned and expenses when incurred, regardless of when cash moves.

| Term | Article definition |

|---|---|

| Revenue earned | Service has been delivered. |

| Expense incurred | You already received the vendor or subcontractor service. |

| AR (accounts receivable) | Completed and invoiced work that is still unpaid. |

| AP (accounts payable) | Received costs that are still unpaid. |

Accrual uses revenue recognition and matching to keep related revenue and costs in the same period, which can make month-to-month margin easier to read. Cash basis tracks movement, while accrual ties performance to delivery timing and obligations.

Workflow example across two months#

Say you deliver a strategy sprint on May 21 and invoice $10,000 that day. The client pays on June 1. A specialist's bill for May work is paid on June 15.

| Scenario item | Cash basis | Accrual |

|---|---|---|

| Strategy sprint revenue | Revenue appears when payment clears, June 1. | Revenue is recorded when earned, at May delivery. |

| Unpaid client invoice after May delivery | The timing follows bank movement. | Unpaid amounts are in AR until payment. |

| Specialist cost for May work | Specialist cost appears when paid, June 15. | Specialist cost is recognized when incurred, for May service. |

| Unpaid specialist bill before payment | The timing follows bank movement. | Unpaid amounts are in AP until payment. |

Under cash basis:

- Revenue appears when payment clears, June 1.

- Specialist cost appears when paid, June 15.

- May can look quieter than the work you actually delivered.

Under accrual:

- Revenue is recorded when earned, at May delivery, with unpaid amounts in AR.

- Specialist cost is recognized when incurred, for May service, with unpaid amounts in AP until payment.

- Activity stays tied to the period when the work happened.

The tradeoff is more timing discipline. Accrual requires tighter tracking of delivery dates, invoices, and vendor records.

Side-by-side for agency decisions#

| Decision area | Cash basis | Accrual basis |

|---|---|---|

| Pricing confidence | Can be harder to read when client payments lag or bunch together | Clearer view of whether delivered work is earning enough in the period performed |

| Margin visibility | Profit can shift between months based on payment timing | Revenue and related costs are aligned more closely by period |

| Cash planning | Strong for near-term liquidity tracking | Should be paired with a separate cash view so liquidity stays visible |

| Reporting readiness | Simple internal cash view | Aligned with GAAP framing for formal performance reporting |

| Tax-timing risk | Timing generally follows cash movement | Timing differences can affect reported performance and tax outcomes when earned amounts are recognized before cash arrives |

What to check at your next close#

Before you compare one month to another, make sure you are using one method consistently. Then run this check:

- Confirm unpaid completed client work is captured in AR.

- Confirm received but unpaid vendor or subcontractor costs are captured in AP.

- Check that revenue sits in the service-delivery period and related costs align to that period where possible.

If this is messy in practice, tighten your records first with How to Manage Bookkeeping for Your Freelance Business. For broader context, see GAAP for Small Businesses Choosing Between Cash and Accrual.

From Financial Guesswork to Strategic Command#

Once you separate cash from performance, the next move is to use both on the same monthly cadence. Check performance and cash together, then make commitments only from records you can defend. Use this to run operations, not to replace your CPA or tax adviser.

Set one evidence standard before planning: every input is confirmed, pending, or disputed. Confirmed means the record set is complete now: invoice or vendor bill, service or receipt support, and bank or approval trail where applicable. Pending means work happened but documentation or approval is incomplete. Disputed means scope, amount, timing, or collectibility is contested and should stay out of optimistic planning.

Decision table#

| Lens item | Evidence standard | Action now | Failure mode if you skip this |

|---|---|---|---|

| Liquidity | Confirmed cleared cash and known due dates | Approve payroll and core obligations first; pause optional spend if one payment is carrying the month | You treat profit like runway and commit cash before it arrives |

| Receivables | Confirmed invoiced balances; pending delivered-but-not-invoiced work; disputed scope or collection items | Escalate overdue invoices, bill completed work, and exclude disputed balances from growth decisions | Forecasts rely on cash that may slip or never collect |

| Payables and commitments | Confirmed bills and agreed subcontractor costs; pending expected costs not yet documented | Approve costs tied to active delivery; delay upgrades or expansion until collections support them | Margin looks stronger than reality, then liquidity tightens mid-cycle |

| Borrowing pressure | Confirmed near-term obligations and realistic repayment capacity | Escalate early with your lender if liquidity may tighten | Lender delinquency responses vary by institution, and tight conditions near lender limits can trigger collateral valuation and repayment disputes |

Three-step close routine#

A workable monthly close can stay simple:

| Step | Owner | Action |

|---|---|---|

| 1 | You or your finance lead | Review liquidity first using cleared cash and near-term required payments. |

| 2 | Bookkeeper, or whoever closes | Reconcile receivables and payables, then tag each line confirmed, pending, or disputed. |

| 3 | You | Test every new commitment against collection risk, not booked revenue alone. |

If you cannot produce those three statuses cleanly each month, fix your bookkeeping process first with How to Manage Bookkeeping for Your Freelance Business.

For compliance questions, verify against full IRS text rather than bulletin highlights. Internal Revenue Bulletin 2026-1 (dated December 29, 2025) states its synopses are not authoritative interpretations, and Rev. Proc. 2025-1 was superseded by Rev. Proc. 2026-1 on page 1.

If late or inconsistent invoicing is skewing your cash view, tighten your billing workflow with the Free Invoice Generator.

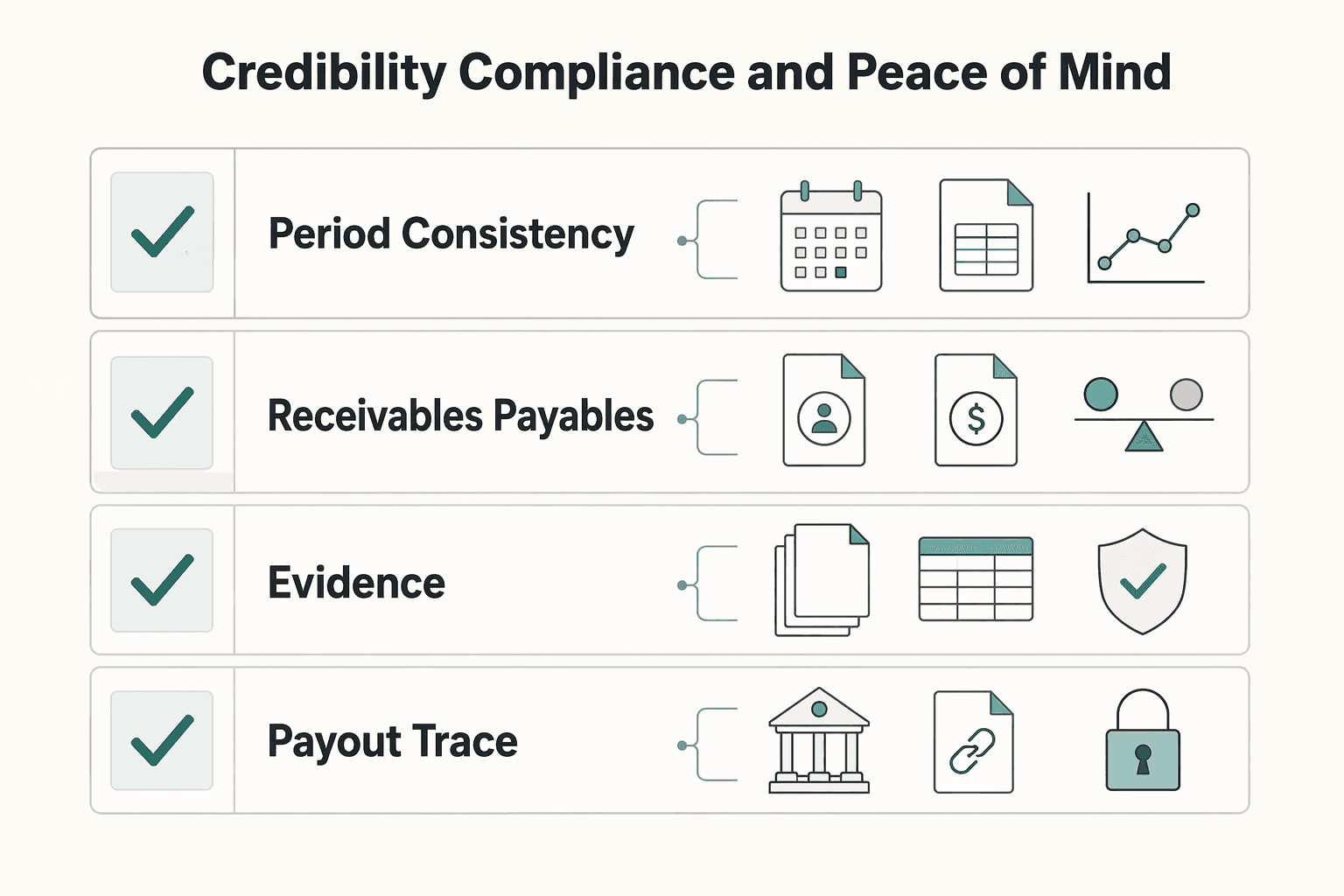

Your Professional Shield: Credibility, Compliance, and Peace of Mind#

If your file may be reviewed, period-based records can be easier to defend because they show the service period and open balances, not just money movement. Cash tracking still matters for liquidity, and period context with receivables/payables visibility can make the file easier to review.

| Reviewer intent | Cash records can show | Accrual-style records can show | Review impact |

|---|---|---|---|

| Period consistency | Deposit and payment dates | Revenue and costs tied to service period, plus period-end balances | You can explain period performance without cash-timing noise |

| Receivables and payables visibility | What cleared the bank | Billed-but-unpaid receivables and incurred-but-unpaid payables | Reviewers can see exposure that has not settled in cash |

| Document package completeness | Bank activity, plus manually assembled support | P&L, balance sheet, AR/AP detail, and linked source records | The file reads as one system, not disconnected transactions |

| Cross-border traceability | When funds moved | Service dates, invoice date, payment date, and open items in one timeline | You can map financial activity to where and when work occurred |

For compliance workflows, keep your accounting records stable and refresh filing requirements before submission. Leave any current-year requirements, filing thresholds, and agency-specific checklist items marked for advisor review until they are verified.

If FEIE or foreign tax treatment may apply, keep one project timeline map per engagement: service dates, invoice date, payment date, and location support you can substantiate. The IRS states FEIE-related benefits require foreign earned income and a foreign tax home, plus a qualifying test. Under the physical presence test, the checkpoint is 330 full days in a 12 consecutive month period, and a full day is 24 consecutive hours beginning and ending at midnight.

For foreign tax treatment, choose either a credit or a deduction for all qualified foreign taxes. Then confirm filing mechanics with your advisor before submission, including Form 1116 for the credit path or Schedule A (Form 1040) for the deduction path.

Use this defensibility routine:

- Reconcile your bank, AR, and AP on a fixed monthly cadence, with a visible close date.

- Keep one audit trail per project: contract, invoice, delivery support, period mapping, and location support.

- Apply one accounting method consistently across periods, and confirm any filing-method change with your advisor before filing.

If your structure is still loose, tighten it first in How to Manage Bookkeeping for Your Freelance Business. If you want a deeper dive, read Hiring Your First Subcontractor: Legal and Financial Steps.

You're the CEO: It's Time for a CEO's Financial System#

Run the business with two views, not one: use cash to manage near-term liquidity, and use an accrual-style view to judge whether the month was actually healthy. That is how you get a usable operating picture when invoicing, delivery, and payment land in different periods.

The distinction is straightforward. Cash accounting records activity when money moves. Accrual accounting records revenue when it is earned and expenses when they are incurred, even if cash lands earlier or later. In practice, liquidity decisions usually rely on cash visibility, while pricing and margin decisions usually rely on delivery-period visibility.

Cash view vs accrual view#

| Decision area | Cash view tells you | Accrual view tells you | What you do this week |

|---|---|---|---|

| Invoicing and earned revenue | What you have collected | What you have earned for work delivered | Review items where delivery, invoicing, and payment fall in different periods |

| Bills and delivery costs | What has been paid | What costs were incurred for delivered work this period | Check whether current-period costs are aligned to current-period delivery |

| Project profitability | Which clients paid this month | Which projects made money after matching revenue and related costs | Recheck projects where delivery and payment landed in different months |

| Planning and runway | Cash available right now | Whether operations are producing healthy margins | Read period performance and cash position side by side before approving new spend |

This matters most when timing gets messy. If work was delivered in December, treat it as December activity in your management view even if invoicing or payment happened later. A cash-only read can make one month look stronger or weaker than the work actually was.

The practical risk is overcommitting. A cash-framed month can make spendable cash look higher than operational reality, especially when timing gaps are not clearly mapped.

Your month-end risk checkpoint#

Before any margin or runway decision, review four items together: cash received and paid, work delivered in the period, costs incurred for that work, and what is still outstanding. If those are not clear, your monthly profit number is not ready to use.

Use one practical test: can you clearly explain what was delivered this month, what it cost to deliver, what has been billed, and what is still outstanding?

Keep decision context in the loop#

Use each view for the decision it supports. Cash helps you manage near-term spending capacity. Accrual-style reporting helps you judge period performance. Reporting quality depends on the specific decision you are making.

What this changes for you now#

Turn that into a repeatable close sequence each month:

- Reconcile cash so your bank position is accurate.

- Identify what was delivered in the month.

- Match the related costs to that same delivery period.

- Compare period profitability and cash position side by side.

- If those views conflict, pause major spending until you can explain the timing gap.

If your software cannot show delivery date, invoice date, payment date, and open balances in one client record, fix that next. See A Guide to the Best Accounting Software for Small Agencies.

You might also find this useful: Choosing Value Pricing for Accounting and Bookkeeping Services.

When you are ready to operationalize these controls in your finance stack, review the Gruv Docs for integration and reconciliation workflows where supported. ---

Frequently Asked Questions

How does the accounting method choice affect FEIE timing?

What it does support is timing mechanics: cash accounting records transactions when payment occurs, while accrual records revenue and expenses when goods or services are delivered or performed. Keep an internal management view for delivery timing, and confirm tax-filing treatment with your CPA.

What FEIE checkpoint do agency owners miss most often?

A common timing-control issue is weak documentation when delivery timing and payment timing differ. Before filing, verify current requirements with your CPA and keep one file with service dates, invoice dates, payment dates, contracts, and delivery proof.

How should I handle a client retainer or advance payment?

Record the cash receipt when it is paid, and keep it separate from the service period until work is performed. For internal management, track advances clearly in the client ledger. For tax filing, confirm treatment with your CPA based on your method and contract language, and do not assume day-one cash is day-one earned revenue.

Can I use accrual for internal books but cash for taxes?

It can be possible, but treat it as a confirmed setup, not an automatic one. For internal management, accrual-style records can give you a clearer period view when timing differs. For tax filing, use the method your CPA confirms for the return, and keep a simple monthly bridge showing why book timing and cash movement differ.

If I use the foreign tax credit, does the accounting method matter there too?

Timing can still matter when a filing position depends on when items are recognized. Keep consistent records (service dates, invoice dates, payment dates, and related tax documents), then confirm with your CPA which year each item belongs in.

Is it worth adopting accrual-style reporting early if my agency is still small?

It can be worth it, especially if you invoice before payment or carry costs across months. Cash accounting may be easier to run, while accrual-style reporting can give a more accurate view when delivery and payment land in different periods. Use this checkpoint: your month-end close should show open balances, not only bank activity.

What should I look for in software if I want this method to hold up?

Pick software that keeps service date, invoice date, payment date, and open balances together in each client record. The practical test is simple: can you pull one clean file that shows delivered work, billed amounts, paid amounts, and open items without rebuilding it in spreadsheets? Treat tools that only mirror bank activity as a warning sign for period-based reporting.

When is an agency legally required to switch methods?

Do not rely on older summaries for this decision. Check current IRS Publication 538 and review its "Future Developments" note. The edition surfaced here is Publication 538 (01/2022) and may not reflect current-year updates. If tax-year setup is part of your case, review the publication's Change in Tax Year section. Then ask your CPA whether your facts require a method change and which filing step applies after verification.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- circabc.europa.eu/sd/a/707cefe5-e3a3-43a6-ae65-4ad96dd51d88/It...trusted

- courts.ca.gov/system/files/2026-03/tcfppm_full_manual_2024...trusted

- irs.gov/irb/2026-01_IRBtrusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- k-state.edu/kams/resources/kams/New%20Mediator%20Trainin...trusted

- repository.upenn.edu/bitstreams/d808a148-5784-459d-acbf-770e73cc9...trusted

- instagram.com/reel/DTK7DVvAc3iexternal

- instagram.com/popular/accrual-accounting-vs-cash-based-acc...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Hiring a Subcontractor for the First Time Without Costly Surprises

**Start with a risk-control sequence, not an ad hoc handoff.** As the Contractor, your goal is simple: deliver cleanly, control scope, and release payment only when the work and file are complete.

Freelance Bookkeeping for Faster, Safer Client Payments

Control over cash starts with records you trust. When entries are current, categorized, and easy to trace, you spot risk earlier and make calmer decisions about follow-up, spending, and month close.

Best Accounting Software for Small Agencies That Protects Cashflow

Pick the platform that protects cash timing, not the one with the longest feature list. For most agencies, three controls deserve early attention: dependable invoicing, project-level profitability visibility, and billing steps that match contract terms without constant exceptions.