Quick Answer

Connect payout infrastructure to SAP ERP by defining the SAP boundary first, separating payment acceptance from payout orchestration, and proving event-to-posting traceability before automating postings. Confirm the exact SAP edition, gather a minimum evidence pack of posting rules, exception paths, and reference mapping, then phase rollout from read-only visibility to low-risk posting automation and later payout batches once idempotency, retries, and reconciliation controls are stable.

How SAP Fits Into Your Payout Stack#

Define the SAP boundary before you choose integration tooling. For payout work, an early decision is whether SAP S/4HANA is only the destination for postings or whether it also sits inside payment acceptance, payout state tracking, and reconciliation control.

That boundary matters because ERP is the shared system for core business processes. When SAP ownership is vague, scope drifts. This guide takes a decision-first path: confirm your SAP offering, separate acceptance from payout orchestration, and phase automation only after event-to-posting traceability is clear.

Name the SAP edition first#

Name the exact SAP offering in scope first. SAP states that SAP S/4HANA Cloud Public Edition, SAP S/4HANA Cloud Private Edition, and SAP S/4HANA are distinct offerings with different characteristics and purposes. That distinction affects operating constraints and change handling.

For on-premise SAP S/4HANA, SAP says the customer is responsible for installation, upgrades, and operations. For SAP S/4HANA Cloud Private Edition, SAP states a new software version is released every two years with seven years of maintenance for that release. A simple quality check is whether your architecture note names the exact edition and operating model, not just "SAP."

Follow a practical sequence#

- Confirm the SAP market. Document the ERP variant, environments, and change-approval owners.

Verification point: explicitly state Cloud Public Edition, Cloud Private Edition, or on-premise SAP S/4HANA.

-

Separate acceptance from payouts. SAP digital payments add-on connects SAP and non-SAP consumer applications with external PSPs, and SAP documents out-of-the-box integration for listed consumer applications. That can fit payment acceptance, but payout orchestration, retries, status handling, and finance exceptions can be a separate design problem.

-

Build a minimum evidence pack. Gather current PSPs, SAP posting rules, known exception paths, and existing reconciliation workarounds.

Verification point: confirm how an external provider reference maps to an SAP posting reference today.

- Phase implementation. Start with visibility, then controlled posting automation, then broader payout handling after controls stabilize. SAP Activate is relevant here because SAP positions it as a structured phased approach to reduce risk and support business continuity.

Watch the early red flags#

Do not treat commercial setup as separate from technical readiness. If SAP digital payments add-on is in scope, SAP states you need a contract with the PSP you plan to use. Confirm contracts and test access before connector evaluation moves forward.

Also avoid collapsing everything into a single "payments integration" scope too early. If phase one only needs standard acceptance and posting, keep it narrow. If payout status orchestration or provider-specific exception handling is already in scope, document that early and design for it directly.

If you're assessing whether SAP is the right fit, read SaaS Accounting Software Evaluation: What Payment Platforms Need Beyond Standard GL Features for a closer look at the finance requirements behind that decision.

Start by scoping the integration boundary#

Set the boundary early and keep it firm. Use SAP digital payments add-on for an acceptance-first scope, and treat payout operations as a separate layer unless your requirements are truly narrow. If phase one is only credit card acceptance and standard digital payment processing, keep scope tight. If phase one also needs onboarding controls, batch payouts, or payout-state control, plan a broader platform layer.

Separate acceptance from payout responsibilities#

Separate acceptance and payout responsibilities before you compare tools. SAP describes SAP digital payments add-on as a service that connects a consumer application to a non-SAP PSP for secure digital payment processing. SAP also describes a baseline market of three parts: the add-on, at least one consumer application where payment is initiated, and at least one non-SAP PSP.

Use this checkpoint: your architecture note should name the payment-initiating app and the PSP. If either is still just labeled "payments," the boundary is still too vague.

Classify phase-one money movement#

Classify phase-one money movement explicitly as in scope, out of scope, or later phase: collect, hold or track, and payout. In many designs, collect fits the add-on boundary, while holding funds, payout timing, and payout operations tracking belong in a platform layer.

Hidden scope usually appears here. Adyen documents holding funds until payout, and Stripe-hosted onboarding includes document upload plus validation and verification support. If you need those controls, keep them explicit instead of folding them into a generic "SAP payments integration" label.

Use one decision rule for phase one#

Use one decision rule for phase one. If the release is credit card acceptance, start with SAP digital payments add-on. For SAP S/4HANA Cloud for customer payments, SAP also notes that only direct capture can be initiated through the add-on, which is a practical fit check.

If you need mass payouts, API or webhook payout tracking, onboarding controls, or held-funds controls, design for a broader payout platform from day one. A clear red flag is a design that demonstrates collection but has no clear way to track payout status operationally.

Prepare the inputs before any architecture decision#

Do not compare connectors or payout platforms yet. First lock down your SAP estate, the posting evidence SAP must receive, and the operating constraints you will not relax. That is the clearest way to see whether you are solving a narrow acceptance integration or a broader payout-and-reconciliation design.

Confirm the exact SAP deployment#

Confirm the exact SAP deployment, not the shorthand used in meetings. SAP Cloud ERP, formerly SAP S/4HANA Cloud Public Edition, is the ready-to-run public cloud option. SAP Cloud ERP Private keeps more company-specific configuration and customization. SAP S/4HANA on-premise means your team operates the software on your own infrastructure. If internal docs still say "SAP S/4HANA Enterprise Management," resolve what deployment that maps to before vendor evaluation.

| Deployment | Article description | Extra note |

|---|---|---|

| SAP Cloud ERP (formerly SAP S/4HANA Cloud Public Edition) | Ready-to-run public cloud option | Distinct offering with different characteristics and purposes |

| SAP Cloud ERP Private | Keeps more company-specific configuration and customization | New software version released every two years with seven years of maintenance for that release |

| SAP S/4HANA on-premise | Your team operates the software on your own infrastructure | Customer is responsible for installation, upgrades, and operations |

This choice sets hard constraints. For electronic payments with SAP S/4HANA Cloud, SAP requires the SAP digital payments add-on, and that add-on has a separate license. Checkpoint: your brief should explicitly name the SAP edition, operating model, add-on license status, and whether fit-to-standard validation has started.

Build a minimum evidence pack#

Build a minimum evidence pack from real transactions, not vendor slides. You need enough data to prove an integration can post, trace, and reconcile in SAP ERP. Include at least:

| Evidence item | What to collect | Article example |

|---|---|---|

| Payment service providers | Current payment service providers and the business flows each supports | Use real transactions, not vendor slides |

| Posting rules | Current SAP ERP posting rules for authorization, capture, refund, fee, and any payout or reversal events in scope | Prove the integration can post, trace, and reconcile in SAP ERP |

| Exception paths | Failed settlements, duplicate events, delayed confirmations, and manual write-offs | Use concrete current exception paths |

| Reconciliation pain points | Missing references, timing mismatches, or spreadsheet joins | Describe monthly pain points in concrete terms |

| Reference mapping sample | PSP name, payment reference, and the corresponding clearing-document payment data in SAP | If you cannot pull this sample, architecture selection is premature |

Prioritize reference mapping. For digital payments processing, SAP documents that the feeder system or convergent invoicing must provide PSP and payment reference values, and that SAP stores this in clearing-document payment data. For each provider, confirm you can pull a sample with PSP name, payment reference, and the corresponding clearing-document payment data in SAP. If you cannot, architecture selection is premature.

Turn non-negotiables into testable rules#

Write non-negotiables as measurable rules. "Fast settlement" is vague. "Payout must land within X business days" is testable. Settlement timing is provider-specific, not universal: Adyen documents a default two-day payout delay and a sales day window of 00:00 to 23:59, while Stripe describes payout schedules using delay days.

Apply the same standard to retries and auditability. Stripe states webhook endpoints can receive duplicate events, and Adyen documents automatic webhook retries for up to 30 days. Your retry policy should therefore include idempotency and a defined replay window. For audit trail, define how each external payment or payout event maps to an SAP reference. For data residency and security, do not assume they are automatically satisfied. Confirm what your integration logs, where it runs, and how identity and access are controlled.

Turn unknowns into evaluation criteria#

Turn known unknowns into evaluation criteria before the first demo. In fit-to-standard, SAP guidance is to examine requirements not covered by standard processes directly.

Ask vendors and internal teams for concrete answers on:

- connector mechanics: how references, statuses, and retries enter SAP and where they are stored

- failure handling: behavior on duplicate webhooks, late events, and partial payout failures

- measurable outcomes: which reconciliation steps can be reduced and how that will be tested against current month-end pain points

Treat "supports SAP" as insufficient if it does not include verifiable reference mapping, failure handling, and proof against your sample data.

If you're comparing ERP options, see Microsoft Dynamics 365 for Payment Platforms: Finance Module Setup and Payout Integration Guide for how a similar payout integration works in a different stack.

Compare the three architecture options side by side#

If you expect multi-provider growth, favor the option with cleaner long-term ownership boundaries, even if launch is slower. In this comparison, that often points to option C. Option A fits narrower SAP-led payment acceptance, and option B is safest when the certified SAP target matches your estate.

Anchor the comparison on ownership, not the demo#

Use this table to separate what each option owns from what your team still needs to build or validate.

| Option | SAP S/4HANA depth | Payout batch support | Webhook and retry ownership | Reconciliation effort | Change cost | Lock in and unwind |

|---|---|---|---|---|---|---|

| A. SAP digital payments add-on | SAP lists out-of-the-box coverage for SAP S/4HANA Cloud Private Edition and SAP S/4HANA Cloud Public Edition, and notes API implementation may be required depending on backend choice. | Do not assume end-to-end payout batch orchestration from DPA alone. | Validate per PSP and integration path; SAP states PSP process coverage varies by provider. | Can be simpler for supported authorization, settlement, and refund flows; harder when payout states remain external. | Includes direct PSP contracts; effort varies by PSP scope and backend implementation. | PSP replacement is possible, but postings and ops can still become DPA-path dependent. |

| B. SAP-stack plugins (for example, Novalnet, eBizCharge) | Product-specific. Novalnet is SAP-listed as certified and fully integrated with DPA, including SAP ERP via FIN-DP 1.0. EBizCharge evidence here is for SAP B1 HANA 10 Cloud, not SAP S/4HANA. | Can exist in specific products; confirm exact SAP target before assuming coverage. | Connector behavior should be tested directly for retries and duplicate-event handling. | Can be lower early if mapping is bundled, but complexity can grow with added providers or custom posting logic. | Can be lower at launch when connector fit is exact, and can rise if operations depend on connector-specific behavior. | Lock-in risk rises when exception handling and status mapping are connector-specific. |

| C. Payout platform plus your orchestration layer | Less SAP-native, broader scope. Tipalti positions SAP S/4HANA integration and also offers file integration for other ERPs. | Strong fit when batch payouts are central; Tipalti claims 200+ countries and territories, 120 local currencies, and 50+ payment methods. | Your orchestration layer owns retry, dedupe, and replay rules. | Higher upfront design to normalize references and posting outcomes before SAP posting. | Higher initial design/build effort for the orchestration layer. | Lower lock-in risk if you keep a canonical model outside vendors; higher if vendor-native payout states flow directly into SAP postings. |

Verification check: when someone says "SAP-certified," ask which SAP product and where the certificate is. The eBizCharge certification claim is for SAP Business One HANA 10 Cloud, not SAP S/4HANA.

Test the boundary where each option usually breaks#

Each option tends to fail at a predictable boundary. Test that boundary before you commit.

Option A breaks when teams stretch DPA beyond its intended scope. SAP defines DPA as connecting SAP and non-SAP consumer applications to non-SAP PSPs, and PSP process support is provider-specific. If your scope includes payout orchestration, treat DPA as one component, not the whole design.

Option B breaks when a strong connector fit is mistaken for long-term architecture. Novalnet has clear SAP evidence, but replacement effort can grow once exception handling and operating procedures depend on connector behavior.

Option C breaks when orchestration is underspecified. A payout platform can widen rails and ERP options, but sending vendor-native payout states straight into SAP can make later provider changes harder. Keep SAP postings tied to normalized references and accounting events.

A practical check for all options: run one duplicate-event case and one delayed-event case against sample data, then verify SAP document references and traceability.

Choose the option that survives your next expansion#

Choose the option that still works after the next scope increase, not just the first demo.

Pick option A when scope is mostly payment acceptance in SAP S/4HANA and stays close to authorization, settlement, and refund.

Pick option B when the plugin's certified or documented SAP target matches your estate and the use case stays inside that boundary.

Pick option C when your roadmap includes multi-provider growth, payout batches, or ERP portability. It can be slower to launch, but it gives you cleaner ownership boundaries between payout operations and SAP accounting evidence.

Before locking in a connector, map your ownership boundaries and failure-handling assumptions against Gruv integration patterns in the developer docs.

Set canonical records and posting rules before writing integration code#

Lock record ownership before you write mappings: SAP ERP and SAP S/4HANA should receive normalized accounting events, not raw provider states. That keeps provider-specific status names and duplicate deliveries from leaking into finance postings.

Assign the system of record for each object#

Assign the system of record for each object. Define in writing which layer owns each state and which layer owns booked accounting outcomes.

| Object | Recommended system of record | What SAP should store |

|---|---|---|

| Transaction state | Provider-facing platform or orchestration layer | Normalized status, amount, key provider references, posting outcome |

| Payout state | Payout platform or orchestration layer | Batch or payout reference, completion or reversal posting references |

| Accounting balance view | SAP ERP or SAP S/4HANA for booked balances | Posted accounting position, not raw provider balance states |

If you use SAP digital payments add-on for card flows, SAP can receive a token after card registration. SAP documentation describes using that token in downstream authorization and settlement and transferring it to SAP Financial Accounting. Treat that as card-flow integration evidence, not proof that SAP should own every upstream provider state.

Normalize provider events before you map postings#

Normalize provider events before you map postings. Run posting logic on a small normalized status model that you control. Provider event names are inputs, not your accounting model.

For example, PayPal exposes distinct events for capture completion (PAYMENT.CAPTURE.COMPLETED), capture refund (PAYMENT.CAPTURE.REFUNDED), and payout batch success (PAYMENT.PAYOUTSBATCH.SUCCESS). Map those to your own canonical states, for example capture_completed, capture_refunded, and payout_batch_completed, before posting to SAP S/4HANA.

Apply the same rule to wallets. SAP Open Payment Framework includes Apple Pay, but wallet support does not by itself create one universal event vocabulary for posting logic. Normalize PSP events into your common state model first.

Separate posting triggers by accounting meaning#

Keep posting triggers aligned to accounting meaning, not transport progress. Acceptance flows and payout flows should not share the same trigger family.

Card or wallet acceptance events belong to authorization, capture, settlement, and refund logic. Payout events need their own completion and reversal triggers. In PayPal Payouts, sender_batch_id duplicate checks over 30 days help with request deduplication, but they should not be treated as completion proof. Keep submission, completion, and reversal in separate states with separate posting rules.

Make every state transition traceable before go live#

Require a full trace chain for every status that can create or reverse a posting. At minimum, persist provider event ID, provider object or capture or batch reference, internal payment or payout ID, posting timestamp, and SAP document reference.

Build this for replay safety. Stripe states webhook endpoints can receive duplicate events and retries undelivered events for up to three days. Your handler should prove a replay resolves to the same internal record and the same SAP posting decision. Use provider request linkage where available, including PayPal-Request-Id on supported POST calls and Stripe request or related object references.

For a step-by-step walkthrough, see SOC 2 for Payment Platforms: What Your Enterprise Clients Will Ask For.

Implement in phases that limit rollback risk#

Do not enable acceptance postings, payout postings, and operator handling all at once. A practical rollout pattern is to phase scope so validation and rollback stay manageable, in line with phased transformation and cutover-simulation guidance. Big-bang releases are generally framed as a better fit for smaller, simpler implementations.

Start with read-only visibility into SAP S/4HANA#

Start with visibility in SAP S/4HANA, not automated payout postings. In this stage, keep payout posting decisions manual and focus on consistent payment-state and reference data in SAP-facing reporting or staging views.

The core checkpoint is traceability, not message volume. For each key event, you should be able to follow the same reference chain from provider object to integration record to SAP-side record.

For acceptance scope, keep boundaries explicit. SAP digital payments add-on can connect SAP and non-SAP consumer applications with PSPs, but that does not by itself mean your payout lifecycle is ready for automated ERP posting.

Automate low risk postings for one provider cohort#

Once read-side visibility is stable, automate only low-ambiguity posting families for one provider cohort. Keep payouts out of scope here.

Choose postings with clear accounting meaning and clean reconciliation paths, then verify them end to end from provider reference to internal record to SAP document. Keep a short signoff pack with enabled rules, excluded edge cases, rollback criteria, and named engineering and finance approvers.

Enable payout batches only after exception handling has an owner#

Treat payouts as a separate phase because failure handling is different. In SAP terms, the payment batch is the grouping object for collective processing, and batch posting can use a grouped total with a clearing item.

Before you enable payout-batch automation, require an exception queue and explicit operator ownership. SAP advanced payment management describes semi-automated exception handling and business-user batch approval. Use those controls deliberately for rejected transactions and rejected batches, not just as UI workflow.

Run dual path validation when cutover risk is high#

When cutover risk is high, run old and new paths in parallel for a defined validation window before full switch. Treat this as a cutover simulation: compare outputs, log variances, and refine the cutover plan with what you learn.

If prior QAS migration findings exist, incorporate them into production cutover planning. Do not fully switch until material variances are explained.

Design webhook, retry, and idempotency handling before go-live#

Phased rollout only works if the event path is replay-safe. Before any provider event can create or change postings in SAP S/4HANA or SAP ERP, design for duplicates, delays, and out-of-order delivery as normal operating conditions.

Accept webhooks fast and process asynchronously#

Do not make provider delivery wait on SAP posting. Receive the webhook, validate it, persist the payload with key identifiers, return success quickly, and continue processing asynchronously.

This matches provider behavior. Adyen recommends acknowledging before business logic, marks webhooks as failing if no response arrives within 10 seconds, and retries failed deliveries. In SAP Integration Suite asynchronous flows, the sender can receive HTTP 202 (Accepted) while downstream processing runs later. Your checkpoint: for any event ID or provider reference, you can show receipt time, persistence time, and SAP processing result time.

Define one durable idempotency key across the full path#

Use one stable processing key from webhook receipt through SAP-facing posting. If the key changes between hops, retries can still create duplicate finance documents.

In SAP Integration Suite, Idempotent Process Call can detect an already-processed message ID and skip or mark duplicates. That only protects you if reprocessing uses the same message ID. Treat transient transport IDs or delivery-attempt IDs as insufficient when they do not map cleanly to the final SAP ERP posting reference.

Retention is a go-live gate: SAP's idempotent repository deletes stored IDs by default after 90 days. Keep a clear record of key format, storage location, retention period, and reprocessing ownership.

Recover with explicit ordering rules, not last-write-wins#

When event order breaks, reconcile using the ordering fields your event schema guarantees, often provider reference and event timestamp, before applying updates. That avoids overwriting newer state with a delayed event.

Adyen explicitly calls for timestamp checks to preserve chronological processing. In practice, that means classifying each incoming event as newer, older, or already applied, then applying only the valid state transition. For already-processed events, return success to suppress additional retry noise.

Test failure modes before enabling posting#

Do not rely on happy-path tests. Run explicit drills for:

| Provider | Documented event behavior | Window |

|---|---|---|

| Stripe | Retries undelivered webhook events; duplicate webhook delivery can occur | Up to 3 days |

| PayPal | Retries non-2xx deliveries | Up to 25 times over 3 days |

| Adyen | Can retry from queue for failed deliveries | Up to 30 days |

- duplicate webhooks for the same event

- delayed confirmation arriving after a later state change

- provider timeout followed by successful retry

- partial batch failure where one payout item fails but the batch record exists

- downstream SAP posting failure after webhook acknowledgment

Expected result for every drill: one auditable status, one posting outcome, and no duplicate documents in SAP ERP. Validate against real retry behavior where possible: Stripe retries undelivered events for up to 3 days, PayPal retries non-2xx deliveries up to 25 times over 3 days, and Adyen can retry from queue for up to 30 days. Related: SAP Business One for Mid-Market Companies: ERP Capabilities and Payment Integration.

Build reconciliation controls finance will actually use#

Reconciliation controls only work when finance can answer daily and month-end questions in SAP without calling engineering. The practical minimum is an auditable trail for payout and fee events, plus clear daily and close views.

Preserve one traceable record from provider event to SAP posting#

Keep one identifier chain intact from provider event receipt to the final SAP ERP posting. For payouts, fees, reversals, and adjustments, finance should be able to follow the same record across the full lifecycle.

In SAP digital payments add-on, each digital payment transaction is linked to one specific merchant ID, and once the PSP and merchant ID are determined, they remain the same for the rest of the process. Use that stability as the anchor for traceability.

For each event, keep these fields together in one searchable record:

- provider event ID and provider reference

- PSP and merchant ID

- payout or batch reference

- gross amount, fee amount, currency, and event timestamp

SAP ERPposting document number or clearing reference- processing status and status-change timestamps

Your control check is simple: start from one bank-statement payout line and trace it back to provider reference, merchant ID, event history, and final posting outcome without manual reconstruction. Use SAP audit trail events to show what happened and when, rather than reconstructing the story manually.

Expose daily and close views inside SAP S/4HANA#

Finance should work from SAP-native views for daily operations and period close. Do not make reconciliation depend on engineering-owned exports.

For daily monitoring, use Bank Statement Monitor for recent statement status and reconciliation issues, including records over the last 14 days. For broader coverage, use the SAP bank-statement overview across house bank accounts with drill-down into statement detail.

For close, use the Bank Reconciliation report to gather account-item data, check statement errors, and review beginning and end-of-period balances and turnovers for main bank and related clearing accounts. That gives finance what they need to separate timing differences, posting errors, and unresolved exceptions.

If finance still needs engineering to interpret exceptions or close balances, this layer is not done.

Split exceptions into auto-resolved and operator queues#

Split exceptions early into no-touch matches and human-reviewed investigations. A single blended exception bucket hides ownership and slows close.

Model your routing on confirmed matches, which need no further action, versus suggested matches, where a user confirms or discards. Then run two queues with explicit owners and internal SLA targets:

- Auto-resolvable queue: items that rules can close after references, amounts, or statement data align

- Operator queue: missing references, amount breaks, clearing-account issues, or other cases requiring finance judgment

For queue hygiene, every open item needs a reason code, owner, opened timestamp, and last action timestamp. Publish queue definitions and aging reports as audit evidence. For sensitive-data investigations, Read Access Logging (RAL) supports answering who accessed particular data within a specified time frame. Related reading: Solving Esports Prize Payment Distribution: How Tournament Platforms Pay Winners Globally.

Handle compliance and data boundaries explicitly#

Set payout-release gates in the provider or orchestration layer first, then record outcomes in SAP ERP or SAP S/4HANA. Keep only truly blocking checks as release gates. Store advisory checks as informational signals so finance can monitor risk without creating unnecessary holds.

Classify provider checks into blockers vs records#

Use each payment service provider's documented gating rules, not a generic SAP checklist. Adyen requires user verification before payments or payouts, and Stripe requires verification information before enabling charges and payouts. Stripe capabilities also control what connected accounts can do.

For each payee or merchant, keep two explicit statuses: release_blocking_status and informational_status. Put verification-complete state, required capabilities, and country-based payout eligibility (where applicable) in the blocking status. Keep advisory follow-ups in informational status inside SAP ERP. Validation check: for one released payout, you should be able to show provider account ID, status timestamp, and the evidence used to allow release.

Keep logs masked but reconstructable#

Keep audit trails chronological and traceable, but exclude sensitive payloads from routine logs. Log references instead of raw payloads: provider event ID, provider reference, payout batch ID, amount, currency, event timestamp, and SAP posting reference.

If card data appears in support views, display no more than first 6 and last 4 digits. If investigations frequently require full payload dumps, treat that as a sign logging boundaries may be too permissive. SAP digital payments add-on has PCI DSS verification status in SAP Trust Center, but your custom integration logs still need their own masking and redaction discipline.

Confirm coverage caveats before commitments#

Confirm market, payment-method, and feature coverage before contracts, cutover dates, or finance signoff. SAP digital payments add-on is an integration boundary to non-SAP PSPs, and PSP process support varies by provider. Stripe payment-method support varies by country, currency, product, and API option, and Connect country availability can also depend on enabled features. PayPal Payouts support is segmented into 4 levels, including countries where merchants cannot send payouts.

Maintain a versioned provider coverage sheet and re-check it when onboarding or expansion changes. Revalidate verification requirements regularly, because provider KYC requirements can change over time.

Plan migration and coexistence for legacy SAP estates#

Coexistence should be an explicit architecture decision with clear boundaries, not an open-ended transition state. If you are moving payout logic toward SAP S/4HANA, define what stays in the legacy estate, what moves next, and what condition allows the old connector to be retired.

Define coexistence boundaries before migration work starts#

For SAP Business Suite, anchor planning to SAP's maintenance timeline: mainstream maintenance for Business Suite 7 core applications, including SAP ERP 6.0, runs through end of 2027, with optional extended maintenance through end of 2030. Use that window to set ownership boundaries, not to defer them.

If you are not doing a full system conversion, include SAP's SAP S/4HANA Selective Data Transition in your options, since SAP documents it as an alternative path. For SAP Business One, document boundaries even more tightly: the Integration Framework is optional, and each service unit needs its own dedicated instance.

Verification point: validate one live payout flow end to end and confirm provider reference, payout batch ID, amount, currency, and posting reference are traceable across both estates without changing status meaning.

Normalize payout status meaning across ERPs before connector tuning#

Cross-ERP rollout can stall when each connector keeps its own status semantics. NetSuite exposes customer payment records via REST web services, Microsoft Dynamics distinguishes synchronous and asynchronous integration patterns, and Acumatica tracks payment processing with document statuses and unique reference numbers.

Define one shared payout status model for reporting and operations, then map each ERP into it. The goal is consistent operational meaning for states like release and failure, even when source objects differ. That is what keeps month-end reporting comparable during coexistence.

If you need deeper cross-ERP implementation detail, use the companion guide. ERP Integration for Payment Platforms: How to Connect NetSuite SAP and Dynamics to Your Payout System.

Use capability parity checks to choose migration order#

Migration order should follow proven capability parity, not preference. Rather than assuming a fixed sequence, prioritize posting, reconciliation, and payout orchestration based on dependency and operational risk in your environment.

For each capability, confirm:

- the target estate reproduces the same reference chain and accounting outcome

- finance can close on target outputs without fallback workarounds

- operators can resolve exceptions without returning to the legacy connector

If parity is not met, pause at that boundary.

Set decommission criteria at the beginning#

Set the retirement trigger up front or coexistence will drift into permanent connector debt. Use phased routing consistent with the Strangler Fig pattern, and retire legacy components only after dependencies are removed. Pair that with explicit stakeholder approval before decommissioning.

Document the decommission trigger in the migration plan from the start: dependency inventory cleared, approvals captured, and finance plus engineering confirmation that the new path is the operational path. Without that trigger, coexistence tends to persist as long-term connector debt.

If SAP is one of several ERP paths you're evaluating, Acumatica for Payment Platforms: How to Integrate This Cloud ERP with Your Payout Infrastructure covers a comparable integration pattern in a cloud ERP environment.

Avoid the integration mistakes that create platform debt#

The fastest demo path can create costly unwind work later. Platform debt often starts when teams optimize for plugin speed, over-assign scope to SAP digital payments add-on, and only then confront duplicate or out-of-order events in production.

Add an exit-cost review before signing the plugin route#

If a connector wins on demo speed, add an exit-cost check before you sign. eBizCharge markets easy implementation, and Novalnet markets broad lifecycle coverage, but that does not by itself show replacement effort after your SAP ERP posting flows and operations depend on the connector.

Include a short evidence pack in contract review:

- exportable transaction and status history

- provider reference, internal payment reference, and posting reference fields

- documented error codes and retry behavior

- a clear replacement condition for ending connector use

Verification point: ask for one completed payment event export with the exact references needed to recreate posting and reconciliation outside the plugin. If that chain is unclear during procurement, it can be harder after go-live.

Write down what SAP digital payments add-on does not own#

Treat SAP digital payments add-on as a defined digital-payments connector scope, not a full payout-orchestration layer. SAP positions it as a connection layer between consumer applications and PSPs, with learning materials centered on incoming credit-card payment flows, and SAP also notes PSP process support varies by provider.

Document the remaining responsibilities explicitly: payout state tracking, batch release logic, reversal handling, exception ownership, and reconciliation rules into SAP S/4HANA or legacy SAP ERP. If you skip this, gaps can appear in exception paths rather than in demo happy paths.

Make event handling replay-safe before auto-posting#

Do not enable auto-posting until event handling is replay-safe. Safe retries require durable idempotency-key handling, and webhook consumers should assume duplicate delivery and possible ordering issues.

If recovery is needed, use a staged sequence: pause auto-posting, reprocess idempotently, then re-enable in controlled phases. Start with one provider cohort and confirm duplicate events do not create duplicate postings, while update-before-create cases are routed to exception handling instead of silently changing state.

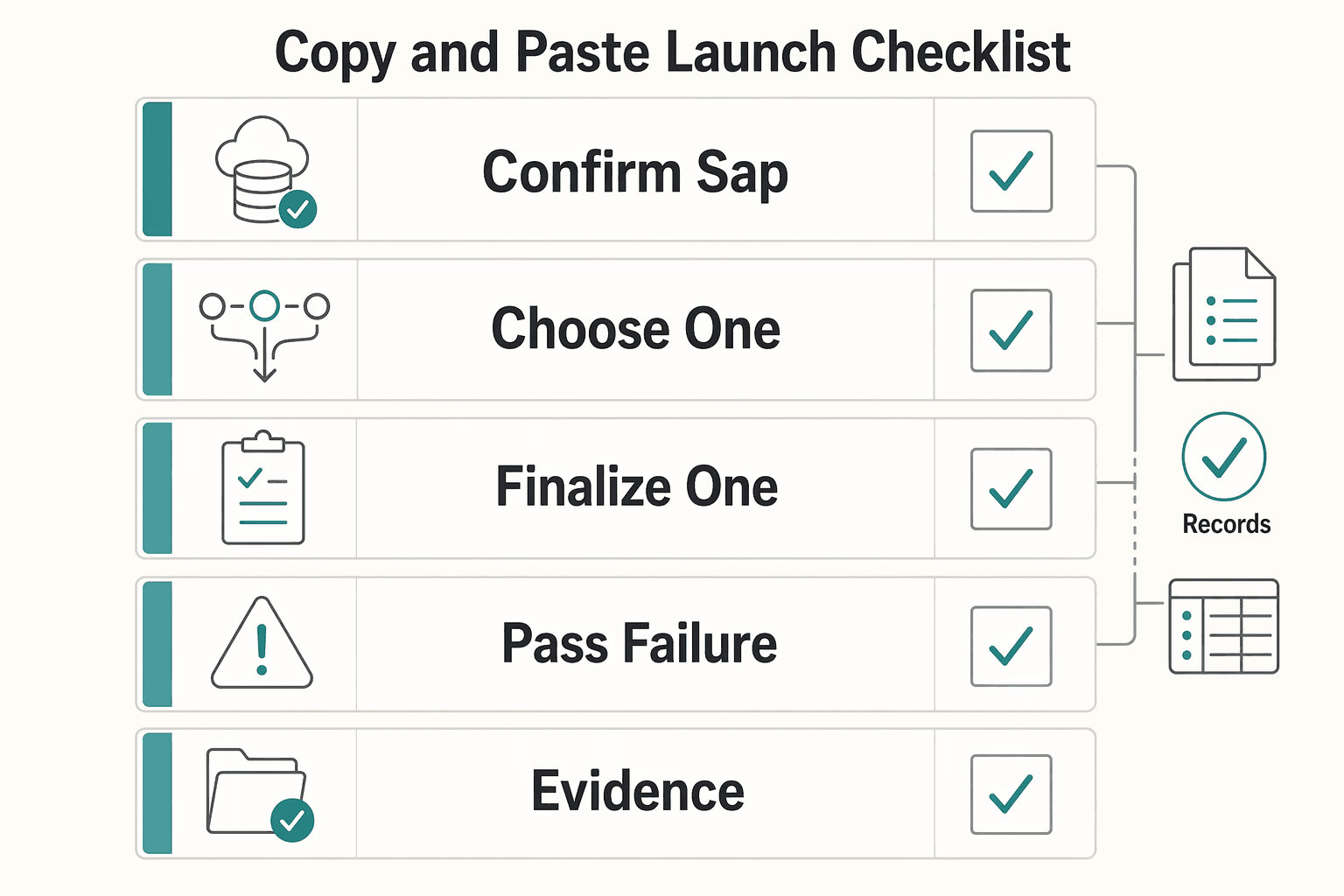

Copy and paste launch checklist#

Use this as a go or no-go gate, not a nice-to-have list. If any item is still vague, especially status mapping or retry handling, do not enable automated posting into SAP ERP.

- Confirm the SAP target market and ownership model first.

Document the exact estate: SAP Cloud ERP (formerly SAP S/4HANA Cloud Public Edition), SAP S/4HANA Cloud Private Edition, or another legacy SAP market that needs separate validation. Record who owns integration, finance signoff, exception queues, and posting-rule approvals.

- Choose one architecture path and define the exit criteria up front.

Pick one route: SAP digital payments add-on, a plugin path such as Novalnet or eBizCharge, or a payout-platform integration. Use SAP digital payments add-on when scope fits SAP's documented consumer-application and PSP model; require written product-fit evidence for plugins, since Novalnet is SAP-certified while eBizCharge evidence is specific to SAP Business One.

- Finalize one canonical status model and posting rules before build.

Map provider events from your selected payment service providers into one normalized internal state model before posting to SAP ERP. For each event path, define provider event, normalized status, posting trigger, reversal behavior, provider reference, internal transaction or payout reference, and resulting SAP posting reference so operators can trace every transition end to end.

- Pass failure-path tests before go-live.

Run production-like tests for retries, duplicate events, delayed webhooks, and reconciliation exceptions. Happy-path demos are not enough. Stripe is a useful benchmark because it warns duplicate webhook delivery can occur and retries undelivered events for up to three days, but validate each provider's behavior directly.

Minimum pass criteria:

- replaying the same event does not create a second posting in

SAP ERP* update-before-create cases route to an exception queue * delayed confirmations reconcile by provider reference and event time * idempotency keys, or equivalent duplicate protection, are enforced across API and posting layers

- Publish operator documentation that is usable in live operations.

Include daily checks, month-end reconciliation steps, escalation paths, and rollback steps for disabling auto-posting while preserving inbound event capture. Specify required screens and reports, exception definitions, reprocessing authority, and evidence needed before manual correction.

Conclusion#

Use a phased sequence: define scope first, choose architecture second, prove controls third, and scale only after those pieces hold under real exceptions in SAP ERP. That order helps keep a workable integration from turning into finance-side cleanup later.

Anchor the project to fit and scope#

Start by defining what phase one must do. SAP digital payments add-on is positioned for secure end-to-end digital payment processing and PSP connectivity, but that documented scope is not, by itself, proof of full payout-orchestration coverage. If you need batch payouts, payout status handling, and provider-specific exception processing, require explicit ownership and flow details.

Push every "native SAP support" claim against your actual deployment and market. The real answer should cover connector mechanics, posting ownership, and out-of-order or delayed provider events.

Choose the path your team can operate#

Choose the path your team can run month after month, not just the one that demos well. SAP Activate defines 6 phases, with core project delivery between Prepare and Deploy. That is a practical check against trying to validate architecture, controls, and scale all at once.

Prefer the option with clear ownership boundaries, even if release one is narrower. A plugin demo can look efficient, but if posting rules, exception handling, and finance procedures become hard to unwind later, long-term change cost can rise. SAP guidance also notes that a fit-to-standard approach helps minimize delivery risk and lower total implementation and operation cost.

Prove controls before widening rollout#

Scale only after retries, duplicate delivery handling, and reconciliation are proven. For payment APIs, idempotency should be enforced end to end so retries do not create or post duplicate operations.

Reconciliation needs the same rigor. Payout reconciliation is batch-oriented in provider documentation, so require a payout reconciliation report, or equivalent evidence, that ties each settlement batch back to SAP ERP postings. At minimum, trace provider reference, event timestamp, internal transaction or payout reference, and resulting SAP posting reference. If that chain fails under delayed events or partial batch failures, keep automation scope bounded.

Use this outline as a working evaluation checklist in vendor conversations, and keep pressure on the parts that are easiest to gloss over: market fit, replay safety, payout batch handling, and operator visibility. If you are selecting across multiple ERPs as well as SAP, this companion guide may help frame broader tradeoffs. ERP Integration for Payment Platforms: How to Connect NetSuite SAP and Dynamics to Your Payout System.

If you want a practical review of your SAP payout architecture, request a scoped walkthrough focused on controls, reconciliation, and rollout risk via Gruv contact.

Frequently Asked Questions

Is `SAP digital payments add-on` enough if we also need complex payout operations?

Usually not by itself. SAP positions SAP digital payments add-on as a service that connects consumer applications to PSPs and frames it as a hub for incoming credit-card payment processing. If you also need full payout operations with exception ownership, treat that as separate scope.

What should we decide before selecting between native SAP integration and a payout platform?

Decide the scope boundary first: incoming payments only, or full payout operations with exception handling. Then confirm your SAP estate, required PSPs, and regional fit. Before selection, lock a short evidence pack with posting rules, exception paths, and phase-one provider coverage.

How do we connect payout infrastructure to `SAP ERP` without locking ourselves into one provider?

Aim for portability, but validate it provider by provider. Confirm early which flows are actually portable in your market and where backend-specific API implementation is required. Keep normalized references and accounting events outside provider-specific payout states.

Which controls are table stakes for `SAP S/4HANA` plus payout integrations?

Use idempotency keys for retry-safe POST calls, verify webhook signatures, and make webhook consumers replay-safe. Retries, duplicates, delays, and out-of-order events should not create duplicate postings. Add reconciliation controls for cases where journal entries can post even if PSP transmission fails, and route later advice items like fees, returns, or manual payments into exceptions.

What implementation details are usually missing from vendor pages and must be validated directly?

The biggest gaps are process coverage, regional availability, and failure-path behavior. Validate exact process support, any backend API work, duplicate-event handling, and delayed confirmations. Ask for live proof, not just happy-path demos.

How should teams phase rollout to reduce cutover risk and reconciliation surprises?

Use phased rollout based on organizational readiness and risk tolerance. Start with a narrow provider or process scope, validate idempotency, webhook verification, and reconciliation controls, and then expand coverage. Treat rollout as ready only when reconciliation differences are explainable and exception handling is clearly owned.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 6 external sources outside the trusted-domain allowlist.

- docs.stripe.com/api/idempotent_requeststrusted

- docs.stripe.com/webhooks/process-undelivered-eventstrusted

- cheatsheetseries.owasp.org/cheatsheets/Logging_Cheat_Sheet.htmlexternal

- docs.adyen.com/development-resources/webhooks/troubleshootexternal

- docs.adyen.com/platforms/quickstart-guide/payoutsexternal

- help.sap.com/docs/DIGITALPAYMENTS/62bf12232b35472b90d531f...external

- help.sap.com/docs/SAP_S4HANA_ON-PREMISE/c9b5e9de6e674fb99...external

- mas.owasp.org/MASWE/MASVS-STORAGE/MASWE-0001external

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: