Quick Answer

Define the offer first: instant payout should be a bounded Premium feature, not a blanket delivery promise. Set eligibility and exclusions in one policy, separate “request accepted” from “delivered,” and make fee impact visible before submission. Then choose structure before price point (per-withdrawal, subscription, hybrid, or pilot) and test it by cohort. Finally, tie every visible status to API webhooks and Ledger journals, and expand only through staged rollout gates with prewritten rollback triggers.

Why Instant Payouts Wins and Where Teams Get Burned#

Treat instant payouts as a paid acceleration option, not a blanket promise that money always arrives immediately. Teams tend to get better results when they package it as a Premium feature with clear scope limits, then make those limits visible before pricing, copy, or rollout decisions harden.

Step 1. Define the promise narrowly before you define the price. Your core offer should read more like a policy than a slogan: available where supported, when enabled, and with coverage that varies by market or program. That wording matters because "instant" can describe the request experience, while actual delivery can still depend on factors outside the moment of request. If your homepage says "instant payouts" but support has to explain caveats in tickets, you do not have a messaging problem. You have an offer-definition problem.

A quick consistency check helps here. Put the same one-sentence promise in the product spec, pricing page draft, support macro, and launch brief. If any version quietly drops "where supported" or "when enabled," fix that before you ship. That single check can prevent avoidable disputes and exception handling later.

Step 2. Align the internal tension early, because each team is optimizing for a different win. Product wants adoption and a reason for users to upgrade. Finance wants margin control and clear limits on what gets subsidized. Ops wants fewer edge cases and fewer manual explanations. Engineering wants retries, failures, and state changes to behave predictably. All four priorities matter, and instant payouts can go sideways when one of those goals is treated as the only goal.

That is also why pricing cannot be separated from packaging. A Premium feature can be sold through usage-based billing, recurring billing, or sales-negotiated contracts, and each choice can shift cost, support load, and user expectations in different ways. Freemium-style access can reduce CAC and create upsell paths, but it also raises the cost of serving free users and can create user-volume pressure if demand outruns controls. If one group sees this as a growth perk while another treats it as a tightly bounded revenue feature, you end up with confusing UX and weak margin discipline.

Step 3. Treat UX and launch controls as economic decisions, not polish. UX is not just the screen where a user taps "withdraw." It is a business-performance lever, not only a design layer. The fee explanation, availability message, and status wording can shape trust and conversion behavior. Good design here is a performance tool, not decoration.

The guide that follows is built for that reality. You will get concrete pricing choices, UX decisions, and rollout controls that still hold up as volume grows and exceptions become more common. A good launch standard is simple. If you cannot explain who gets the feature, what they pay, when it appears, and when it does not, you are not ready to call it instant.

If you want a deeper dive, read How to Offer Instant Payouts as a Platform Feature Without Taking on Float Risk.

What to Prepare Before You Price or Build#

Before you debate fees or copy, lock the commercial structure first: who each plan is for, how tiers scale, and how the paywall explains value.

Step 1. Segment users before you segment price. Use clear buyer personas so product, finance, and ops are designing for the same customer types. If the team cannot explain which persona each plan serves, pricing decisions will drift and UX copy will become inconsistent.

Step 2. Decide tier logic early, then keep it readable. Build pricing that scales with customer needs instead of forcing one flat offer across very different use cases. A simple tier structure is usually easier to compare and buy; many teams use three pricing tiers as a practical starting point.

Step 3. Define the paywall job as value communication, not access blocking. Your paywall should make the upgrade benefit obvious at the decision moment. If it only gates access without clarifying value, you should expect more abandonment.

Step 4. Pressure-test the conversion path, not just the pricing table. The full flow should feel smooth and trustworthy from plan comparison to upgrade action. When that experience is unclear, conversion drops even if the underlying offer is sound.

For a step-by-step walkthrough, see Reserve Policy Design for Platforms with Rolling Holds and Release Controls.

Define the Offer So Legal, Ops, and UX Say the Same Thing#

Define the instant-payout promise in one shared policy before pricing it: if legal, ops, and product cannot describe the same eligibility and status path in the same words, the offer is not ready.

| Status | Meaning | Evidence |

|---|---|---|

| Requested | submit action recorded | pending internal journal intent |

| Accepted for processing | processing started | initiation event (balancePlatform.transfer.created) |

| Updated | transfer status-change event | balancePlatform.transfer.updated |

| Delivered | credited outcome | provider money-movement record reconciled to Ledger journals |

| Failed | failure event | reversal/exception journal path |

Step 1. Write eligibility in plain language. State who can request instant payout, then list the checks in order: supported country/program, eligible external bank account or debit card, and required identity or business verification. If you operate in the EU, specify where VAT validation applies. VIES can help verify whether a VAT number is valid and associated with a name/address, but it is a validation step, not blanket approval.

Include one testable account-history or readiness rule (for example, completed onboarding or required tax status present). Keep this explicit because payouts can be paused when required tax information is missing, even if payment acceptance continues.

Step 2. Separate "accepted" from "delivered." Treat request acceptance and funds delivery as different milestones in UX and ops language. "Request accepted" means processing started, not that funds arrived.

Map each visible status to both webhook evidence and internal ledger handling:

- Requested: submit action recorded, pending internal journal intent.

- Accepted for processing: initiation event (for example,

balancePlatform.transfer.created). - Updated: transfer status-change event (for example,

balancePlatform.transfer.updated). - Delivered: credited outcome plus provider money-movement record reconciled to Ledger journals.

- Failed: failure event plus reversal/exception journal path.

Validate this with one traced payout across UI, support tooling, webhook logs, and ledger view.

Step 3. Publish exclusions before confirmation. List instant-payout exclusions up front: unsupported markets, unsupported payout methods, or profiles under review. Show the fallback status clearly (instant unavailable, under review, or standard payout only) so users see the path before they confirm.

This matters because policy screening can occur after booking and before funds leave.

Step 4. Use one internal status dictionary. Set a single dictionary and enforce it across support macros, product copy, engineering enums, webhook handlers, and Ledger journals: eligible, requested, accepted, under_review, credited, failed. Put longer explanations in one evidence pack, not scattered documents.

Need the full breakdown? Read Xero Multi-Currency for Payment Platforms: How to Reconcile Foreign Currency Payouts.

Choose a Pricing Model That Matches Margin and Risk#

Choose the model before the price point: your structure will shape adoption, support load, and how predictable the feature is to operate.

Map the model first#

Use three lenses when you evaluate your Premium feature: cost-based, competitor-based, and value-based. Cost tells you what is viable, competitor patterns can guide packaging style, and value helps you decide what each cohort is likely to accept.

| Model | When it fits | Primary upside | Primary tradeoff |

|---|---|---|---|

| Per-withdrawal fee | Usage is uneven or you need tighter cost recovery per request | Charge stays tied to usage | Frequent users may resist per-use friction |

| Subscription tier | You want a cleaner upgrade path and more predictable recurring revenue | Simpler plan story | Weak caps can create margin pressure |

| Hybrid | You want an upgrade narrative plus guardrails on heavy usage | Balances recurring and usage-based monetization | Rules can feel complex if not explicit |

| Platform-subsidized pilot | You need real demand and support data before long-term packaging | Fast learning cycle | Pilot scope can drift without clear stop rules |

Run one real scenario per cohort through each row. If finance, product, and support each choose a different model, tighten the rules before launch.

Set decision rules before internal debate#

If usage is high and economics are tight, keep pricing closer to usage. If retention and plan expansion are the priority, test bundled packaging with explicit limits and explicit over-cap behavior.

For pilots, define the cohort, owner, review date, and exit criteria before launch. Temporary pricing often becomes a perceived promise if these boundaries are not clear.

Segment the logic, not just the label#

Do not default every cohort to identical fee logic. New users, high-usage sellers, and enterprise accounts can justify different packaging, but the product promise still needs one consistent language for eligibility, limits, and fallback behavior.

Validate this in practice: the same account state should resolve to matching explanations in UI copy, support macros, and your finance model.

Use analogs for packaging, not for economics#

Gumroad and tiered patterns like Figma Professional are useful for naming, plan framing, and feature separation. They are not direct evidence for your payout economics.

Use those analogs to improve clarity, then finalize pricing from your own cost and support data. For a deeper cost-side check, pair this step with Instant Payouts Economics: What It Really Costs Platforms to Offer Same-Day and On-Demand Pay.

This also connects with Invoice Settlement for Platforms That Match Payouts and Close Disputes.

Design the Payout UX So Users Trust the Fee and the Timeline#

Trust comes from clarity, not speed claims. keep the UX tied to your actual payout policy and system states, and avoid language that reads like a delivery guarantee.

| Stage | What users see | Key details |

|---|---|---|

| Option selection | Standard and instant options side by side | fee, expected timing window, and current availability |

| Pre-submit review | Review card | gross amount, fee impact, net amount, and any policy caveats that can still affect completion |

| After submit | Status updates | map to real internal processing states in plain language |

| Failure state | Next action | retry, switch to standard, or contact support with a request reference if one is available |

Use a simple, consistent payout flow:

- Show standard and instant options side by side at payout, with fee, expected timing window, and current availability.

- Before submit, show a review card with gross amount, fee impact, net amount, and any policy caveats that can still affect completion.

- After submit, show status updates that map to real internal processing states in plain language.

- On failure, offer a clear next action: retry, switch to standard, or contact support with a request reference if one is available.

If your product, support, and operations teams use different wording for the same state, users will see one promise while your team works from another. Keep those labels aligned across UI, support replies, and internal tooling.

Related: Embedded Wallet Design Patterns: How Platforms Build In-App Balance and Spend Features.

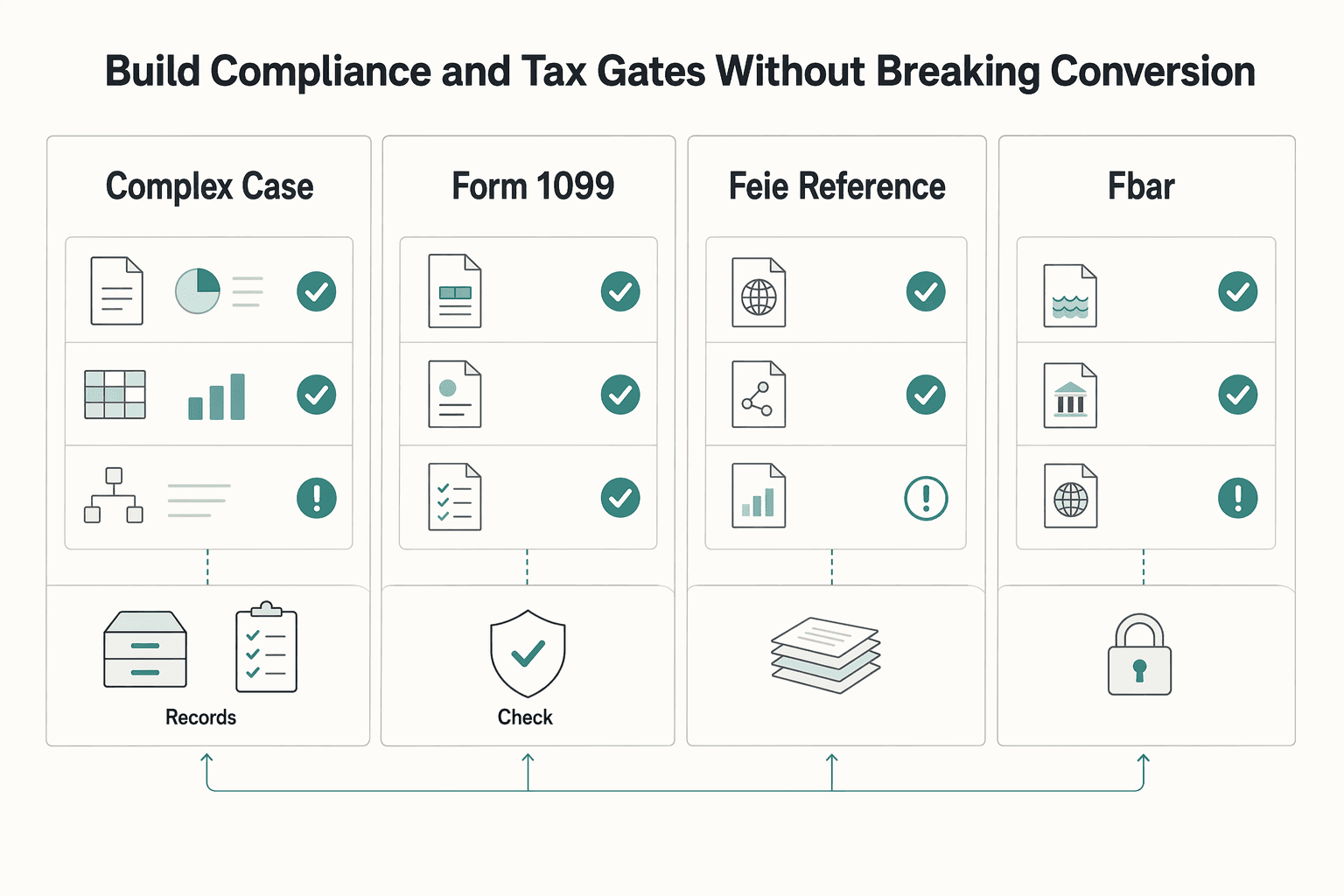

Build Compliance and Tax Gates Without Breaking Conversion#

Prevent late surprises by enforcing compliance and tax eligibility before payout confirmation, not after. The faster path feels trustworthy when users can see eligibility early and fix issues before they choose instant payout.

| Item | How to handle | Key note |

|---|---|---|

| Identity and business checks | Move to the start of the flow before payout confirmation | Do not let users review fees and confirm instant payout while internal KYC or KYB status is incomplete |

| W-8 or W-9 | Show as a visible program prerequisite before certain payouts, if required | Keep one shared status model across product, support, and finance: not collected, collected, under review, rejected |

| Form 1099 workflows | Document downstream handling once a tax profile is collected, if enabled | Keep an auditable trail for each block: current status, submission timing, who changed it, and which payout request was affected |

| FEIE reference support | Keep separate from payout eligibility decisions | The physical presence test uses 330 full days in a 12 consecutive months window; if you surface FEIE values, keep tax-year context explicit |

| FBAR | Use FinCEN due-date and extension notices to guide export timing and date-range clarity | Do not treat it as an automatic payout block unless your own policy says so |

Step 1 Move identity and business checks to the start of the flow. Do not let users review fees and confirm instant payout while your internal KYC or KYB status is incomplete. Make eligibility labels in the UI match the same internal statuses ops uses to clear or block accounts.

If required data is missing, show what is missing before confirmation and keep standard payout separate when your policy allows it. Avoid the failure mode where users select a premium option that was never actually available.

Step 2 Treat tax form status as a visible program prerequisite. If your program requires a W-8 or W-9 before certain payouts, show that dependency clearly instead of handling it only in back-office review. Keep one shared status model across product, support, and finance (for example: not collected, collected, under review, rejected).

If Form 1099 workflows are enabled, document downstream handling once a tax profile is collected. Keep an auditable trail for each block: current status, submission timing, who changed it, and which payout request was affected.

Step 3 Keep FEIE and FBAR support separate from payout eligibility decisions. If you provide reporting helpers, label them as reference support, not legal determinations. For FEIE context, the physical presence test uses 330 full days in a 12 consecutive months window, and those days do not need to be consecutive; excluded foreign earned income still must be reported on a U.S. tax return.

If you surface FEIE reference values, keep tax-year context explicit (for example, $130,000 for 2025 and $132,900 for 2026) and version content as limits change. For FBAR, use FinCEN due-date and extension notices to guide export timing and date-range clarity, not as an automatic payout block unless your own policy says so.

Step 4 Document fallback behavior for incomplete data. When a payout is blocked, show the reason, the missing item, and the next action. Internally, define who can clear holds, what evidence is required, and when to retry instant payout versus route to standard payout or manual review.

Implement in Order and Verify Each Layer Before Rollout#

Roll this out from the money path outward, then expose it in the UI after each lower layer is verified.

Step 1 Build core layers before screens: eligibility, fee calculation, payout orchestration, eventing, reconciliation, then UI rollout. A useful benchmark is the marketplace sequence that places Step 6. Implement Marketplace Payments before Step 9. Launch Your Marketplace MVP, with Step 10 focused on scale. Use that sequencing logic so launch does not outrun operational readiness.

Step 2 Define duplicate-handling rules at every handoff before launch. Set clear identifiers for request, orchestration, webhook event, and journal reference, then test replay scenarios against those rules across API webhooks and Ledger journals. The goal is straightforward: retries should be predictable for product, ops, and finance.

Step 3 Add integration checkpoints for adjacent modules before expanding scope. If Virtual Accounts are part of funding, confirm which balance state is used for eligibility and payout decisions. If Merchant of Record is enabled for some flows, document in-scope and out-of-scope paths so product, finance, and ops are aligned before broader rollout.

Step 4 Use staged release gates with explicit rollback triggers: internal sandbox, limited cohort, then monitored expansion. Define the exact signals that pause or reverse rollout, and make sure support coverage matches the risk window. Enterprise tooling often highlights 24x7 Support and a First Response Time: 4 Hours; treat that as a practical benchmark for money-movement incident readiness.

The target outcome is predictable expansion: each layer is validated before the next one is exposed, and rollback decisions are pre-defined instead of improvised.

We covered this in detail in Account Reconciliation for Payment Platforms: How to Automate the Match Between Payouts and GL Entries.

Common Launch Mistakes and How to Recover Fast#

When rollout issues appear, recover by fixing the decision logic and flow clarity first, not just UI polish. In payment flows, late friction is costly: Nuvei reports that 70% of cart abandonment happens after users enter the transaction flow.

Mistake 1: Pricing copied from SaaS seat plans. Recover fast: Rebuild pricing on payout-unit economics. Use one margin table by payout size band, expected usage, support touch rate, and subsidy cap so finance can validate margin by segment, not just tier names. If you need a reset, start with unit economics.

Mistake 2: Speed promises that hide processing dependencies. Recover fast: Make statuses explicit in both UX copy and internal operations: "request accepted," "processing," and "completed." Each label should map to a real event your team can explain.

Mistake 3: Compliance checks too late in the flow. Recover fast: Move KYC/AML gating earlier and make the unblock path explicit before final submission. Show the hold reason, what the user needs to provide, and what happens next.

Mistake 4: Weak exception operations. Recover fast: Run a daily review queue for failed payout runs and unresolved event deliveries, with an owner, aging, and a required next action for every case. This is where "minimize errors" and "remove friction" become real operating practice.

You might also find this useful: How Platforms Should Design Loyalty Reward Payouts for Margin and Control.

Want a quick next step for "offer instant payouts premium feature pricing ux design platforms"? Try the free invoice generator.

Rollout Checklist You Can Copy Into Your Launch Doc#

Use this as a go/no-go gate, not launch admin: if any line has no owner, no evidence, or still needs major edits, pause rollout.

Apply a requirements-breakdown approach: translate the feature promise into buildable phases, then verify each phase with proof before you turn it on.

Step 1. Confirm the offer definition. Lock eligibility, exclusions, timing language, and market caveats in one shared source. Make sure product copy, support language, and status labels stay aligned.

Step 2. Confirm the economics. Select the pricing model and document the margin logic by segment before launch. Keep subsidy limits explicit so rollout decisions are tied to cost reality, not packaging clarity.

Step 3. Confirm the UX in staging. Verify fee transparency, net amount visibility, timing expectations, and status tracking in the live flow. Test failure paths so users get a clear next action instead of a dead-end state.

Step 4. Confirm controls with evidence. Collect staging evidence for compliance, tax, idempotency, and reconciliation checks based on your market/program requirements. Include test outputs and exception handling references your ops team will use.

Step 5. Confirm go-live and rollback criteria. Run a phased release (internal, limited cohort, broader rollout), define alerting and on-call ownership, and set rollback triggers in advance. Ask one readiness question before each phase: can you go live now without major edits or manual patches?

Step 6. Run a limited cohort review before expanding. Use week one as an early decision checkpoint, not proof of long-term stability. Expand only if margin, trust, and operations metrics remain inside target.

Related reading: ACH Payment Processing Platforms for U.S. Collections and Payouts.

Frequently Asked Questions

How should a platform price instant payouts as a premium feature?

The provided material does not validate any instant-payout fee benchmark, surcharge, or margin target. It only supports that pricing structures can vary and may be packaged in different ways (for example, hourly, fixed-price, or retainer models in agency work). Use those as structure analogies, then set payout pricing from your own cost, risk, and margin data.

What must users see before they choose instant payout?

Keep the offer transparent before selection: clear option names, what each option includes, and the price attached to each option. The approved examples support plan-and-seat clarity, not payout timing or status-language standards.

When should instant payouts be unavailable or delayed?

Any hold/delay criteria should be defined in your own policy and shown clearly to users.

What are the minimum controls needed before launch?

The minimum defensible requirement is transparent packaging and pricing communication. Specific operational controls (for example, ledger handling, idempotency, exception queues, or webhook workflows) must be specified internally.

Should we bundle instant payouts into a subscription or charge per use?

The excerpts do not show that per-use or subscription is better for payout economics. What they do support is clear packaging: named options and explicit inclusions or limits. Figma Starter/Professional and seat options, including a $3/mo Collab seat, are useful packaging analogies, not payout-pricing proof points.

How do we reduce support tickets when an instant payout fails?

Keep claims limited to transparency: define options and pricing clearly up front, and avoid promising failure-resolution flows that are not documented in your own operating policy.

Which metrics tell us the feature is working without harming margin?

Use internal finance and operations data to define success metrics, and avoid presenting external agency pricing ranges or plan-packaging examples as proof of payout-margin performance.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cga.ct.gov/2024/gldata/TMY/2024SB-00002-R000229-Bastian...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- europa.eu/youreurope/business/taxation/vat/check-vat-n...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- sandiego.gov/sites/default/files/2025-08/k-25-2371-db2-3-...trusted

- stripe.com/gb/resources/more/freemium-pricing-explainedtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Offer Instant Payouts Without Taking on Float Risk

The hard part is not moving money fast. It is being honest about the risk you take on when you do. You can market Instant Payouts in a headline, but the speed promise only holds up when liquidity, routing, liability, and controls line up in the same sequence.

What Instant Payouts Really Cost Platforms for Same-Day and On-Demand Pay

Fast access can improve worker experience, but speed is not the core decision. The real question is whether you can move money earlier without losing margin discipline, record clarity, or control over exceptions. Instant payouts are an economics and controls choice first, and a UX feature second.

Embedded Wallet Design Patterns for In-App Balance and Spend Features

Choosing an embedded wallet is not just a UX call. It is an operating model choice. The moment you keep wallet actions inside your product instead of sending users to a separate interface, you are also deciding how compliance handling, balance accuracy, and payout timing will work when a spend succeeds in one place and fails in another.