Quick Answer

Start with one closure rule: an invoice is closed only when Accounts receivable and the Ledger journal both show zero for the same invoice reference. Then reconcile posted cash from the Payment processor or Bank deposit, apply any Credit memo, Debit memo, or Write-off, and verify no unapplied balance remains. If Purchase order or Receiving report evidence is missing, keep it out of auto-close and send it to manual exception review.

Why Invoice Settlement Gets Complicated on Platforms#

Invoice settlement is a closure problem, not just a payment event. In practice, an invoice is operationally settled when the related balances in Accounts payable and Accounts receivable are zeroed out. Money can move and the work can still be unfinished if the invoice shows an open balance, a credit memo or fee adjustment, or an unresolved dispute.

That distinction matters even more on platforms because you may sit on both sides of the flow. Accounts payable is the short-term obligation you owe suppliers or vendors for goods or services already received. Accounts receivable is the money owed to your business for goods or services provided on credit. A payout adds another layer. It is simply the transfer of funds from a merchant account to the business bank account. Useful signal, yes. Proof that an invoice is closed, no.

This guide is for platform operators handling AP, AR, payouts, and invoice disputes together. It is not a freelancer invoicing primer, and it is not a card-processing explainer with accounting terms added afterward. That scope matters because invoice settlement is not the same as online invoice payment processing. In real AP and AR work, settlement can involve more than a payment. It can also require invoices, credit memos, and fees to be applied correctly before anyone should call the record closed. If you own those queues, you need one closure rule your team can apply the same way every time.

Disputes make that gap obvious. A disputed invoice exists when a customer challenges the invoice's accuracy, the services performed, or the agreed terms. Money movement and invoice truth can diverge. You may have a completed transfer, but if the amount is contested, you still need an accounting outcome that clears the remaining position.

Use one working checkpoint for the rest of this article. Before you automate anything, make sure finance, ops, and engineering can all answer the same question for a single invoice: "What exact event or document makes this closed?" The test is simple. Pull one invoice and confirm that you can trace the invoice record, the payment or payout reference, any adjustment, and the remaining AP or AR balance without guesswork. If you cannot answer that quickly, do not automate the close yet.

A red flag is when teams use paid, settled, and closed as if they mean the same thing. If that language is still loose, keep the process manual until you define it properly.

For the broader workflow around invoices, payouts, and disputes, see How to Build a Vendor Portal for Platforms: Tax Forms Invoices Payouts and Disputes in One Workspace.

Define the close state before you automate anything#

Define closure in one sentence before you automate it: an invoice is closed only when the outstanding balance is zero in both Accounts receivable tracking and your platform Ledger journal. A payment event can confirm funds moved, but it does not by itself prove the invoice is closed.

Write the zero-balance rule#

Document the close condition in plain language and align finance, ops, and engineering on the records that must reconcile before status changes. Settlement can involve multiple balance-affecting transaction types, so your rule should require invoice-level application, not just payment activity.

Use one checkpoint: trace a single invoice from invoice record to applied payment and journal impact, then confirm zero remaining balance. If Payment processor activity exists but AR still shows an open or unapplied amount, the invoice is not closed.

Separate money movement from accounting closure#

Treat money movement and closure as separate tests. You may need a Credit memo to reduce what is owed or a Debit memo to reflect an additional valid amount owed before the invoice can be settled cleanly.

Apply payments and memo adjustments directly to the invoice. Unapplied payments or unapplied adjustments create the common failure mode where cash moved but the invoice remains open.

Assign owners before you add auto-close logic#

Assign responsibilities in writing before you enable auto-close paths. A practical split is finance owning accounting outcomes, ops owning triage and exceptions, and engineering owning system state transitions and controls.

If close criteria are still unclear in real cases, keep automation narrow and route exceptions through manual review until the rule is consistent.

Related: Improving Credit Card Reconciliation for Platforms: How to Auto-Match Card Charges to Invoices.

Prepare the evidence pack and system prerequisites#

Set a hard gate before settlement starts: no evidence pack, no matching. This keeps automation reconciling records instead of guessing across incomplete data.

Gate settlement on minimum evidence#

Require these artifacts before an invoice enters settlement:

Purchase order- Invoice record

Receiving reportwhen receipt confirmation is required

This aligns with standard invoice matching that checks invoice, PO, and receipt information, and it reflects real settlement scope, which can include invoices, payments, Credit memo entries, and fees. If receipt proof is contract-critical, keep the invoice out of auto-settlement until the receipt record is attached or linked.

Run a small pre-queue sample check: confirm each invoice traces cleanly to its required matching records. If a lane still depends on inbox threads or manual memory, keep that lane on manual review.

Define reconciliation inputs by rail#

Define evidence by payment rail instead of relying on one generic paid signal:

| Rail | Evidence |

|---|---|

| Bank-funded flows | Bank deposit files or bank statements |

| Card flows | Credit card/Debit card processor confirmations |

| Platform disbursements | Payout status events and payout reconciliation reporting |

For payouts, use the report that ties what reached the bank account back to settlement-batch transactions, then review grouped transaction categories for exceptions. For cards, document which processor event counts as settlement evidence in each integration.

Configure control surfaces and choose the matching mode#

Before broad automation, configure these control surfaces:

- Dispute intake in the

Vendor portal - Clear ownership for the exception queue

- Audit export from

Ledger journalentries

Then choose matching mode by use case:

- Use

2-way matchingby default for low-complexity service scenarios - Require

3-way matchingwhen delivery confirmation is contract-critical, because it adds receipt-quantity validation

If there is no meaningful receipt event, forcing 3-way checks usually creates noise. If proof of delivery is required, skipping 3-way checks is the larger control risk.

For the payout operations side, see Mass Payouts for Gig Platforms That Teams Can Actually Operate.

Step 1 map matching rules from invoice to payout#

Set identity-first matching rules before amount tolerance, or you will auto-close the wrong items.

Define deterministic match keys#

Document a fixed key order for each settlement lane. A practical sequence is invoice ID, then payee entity, then currency, and only then an amount tolerance policy for partial settlement or minor variance. Use that as a lane policy, not a universal rule.

| Order | Match element |

|---|---|

| 1 | Invoice ID |

| 2 | Payee entity |

| 3 | Currency |

| 4 | Amount tolerance policy |

Apply tolerance only after identity fields match. Matching discrepancies should be checked against configured tolerance limits, and anything above the allowed amount or percentage should be flagged for resolution. If you use a percentage rule, record the exact policy by lane or legal entity; 5 percent is an example policy in common finance tooling, not a default.

Use a hard checkpoint for auto-close eligibility: one invoice reference, one payee entity, one currency, and the exact tolerance rule applied.

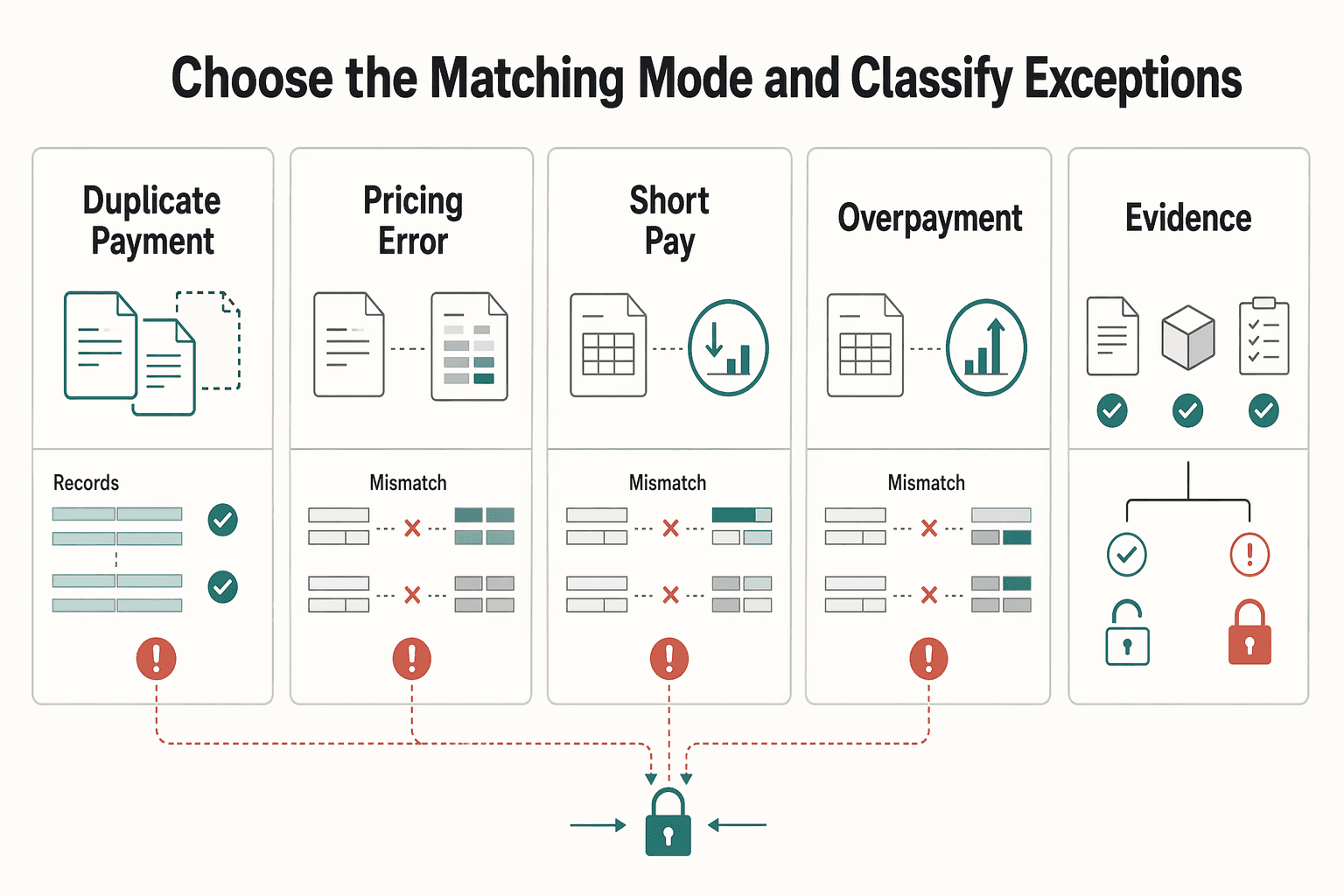

Choose the matching mode and classify exceptions#

Pick the matching mode based on payment-release evidence. Use 2-way matching when you only need invoice price vs. Purchase order price, and escalate to 3-way matching when Receiving report evidence is required because quantity matching must also pass. If receipt proof is required, unresolved line-level exceptions should block payment.

Make exception categories explicit so ops can route them fast:

| Exception category | What failed | Next action |

|---|---|---|

| Duplicate payment | Invoice appears already paid or attached to another payout | Hold settlement and confirm duplicate vs. replacement posting |

| Pricing error | Invoice price vs. Purchase order is outside tolerance | Route for price review and approved correction |

| Short-pay | Paid amount is below invoice amount | Keep invoice open for the outstanding balance with amount/currency context |

| Overpayment | Paid amount is above invoice amount | Hold close and decide refund, credit, or adjustment path |

| Missing evidence | Required Purchase order or Receiving report is absent | Block payment release until evidence is attached or linked |

If the first pass cannot classify the mismatch, route it to manual ops review instead of forcing auto-close.

Record each decision in a journal-linked trail#

Capture every match decision as a Ledger journal-linked event so audits can trace why an invoice stayed open or settled. At minimum, store the invoice reference, payout reference, exception or tolerance result, decision timestamp, and posted journal entry identifier.

This keeps batch-level "paid" status from hiding invoice-level exceptions and gives finance a usable review export for investigation. We cover related payout operating patterns in Crypto Payouts for Contractors: USDC vs. USDT - What Platforms Must Know.

Step 2 reconcile money movement before invoice closure#

Do not close an invoice on match status alone. A safer pattern is to reconcile the cash leg first, then reconcile invoice application against that posted cash, because money movement and invoice settlement can be separate events. Dynamics 365, for example, allows posting a customer payment before settling it to invoices.

Run payment reconciliation against posted cash#

Start with the Payment processor or Bank deposit record and confirm funds arrived and were posted. Stripe's Payout reconciliation report is built to match bank-received payouts to batches of payments and other transactions, which makes batch-level reconciliation a practical first pass. PayPal frames its payouts reconciliation report similarly for end-to-end money flow and notes the report is generated on SFTP by 9:00 AM daily, which can affect close timing.

Do not use payout amount alone as proof. Adyen notes that processing fees are deducted from payout totals, so a lower net deposit can still be correct. Keep evidence tied to each posting: payout or deposit reference, batch (or settlement-batch) identifier, posted amount, fee component where relevant, and the Ledger journal reference.

Then reconcile invoices to that posted cash#

After cash posting is confirmed, run Invoice reconciliation on open Accounts receivable items. Apply funds to the correct invoices and verify what remains open by payee and currency. In settlement terms, the goal is to bring invoice-linked balances to zero.

This is where partial payments and mixed batches create risk. A payout can be posted while an invoice is still short-paid, overapplied, or applied to the wrong payee. Check invoice-level residuals, and use journal-linked settlement evidence for each application, not only the original deposit posting.

Reconcile batches in two passes#

For batch operations, a practical control is two passes: reconcile the Payout batch first, then reconcile invoice lines inside it. This helps catch the common blind spot where a batch total looks right while one invoice still fails. Your team should be able to identify the bad invoice without reopening the whole batch.

Use a clear closure checkpoint as an internal control: confirm payment posting, invoice application posting, and no unresolved balance mismatch between Accounts receivable and the Ledger journal for that item. If evidence is incomplete, hold closure and route to exceptions.

Step 3 resolve disputes with explicit decision rules#

When cash posting and invoice application already match, the remaining items are usually dispute decisions, not reconciliation errors. Require a documented outcome, with evidence, before changing close status on any Invoice dispute.

Classify the dispute before you post anything#

Do not leave disputes in vague states while balances age. Use a clear internal triage so each case has a next action:

- Valid invoice: issued amount stands; continue collection or defend the payment challenge.

- Valid customer objection: invoice is wrong, so reduce or reverse the receivable.

- Mixed fault: part stands and part does not; calculate the net effect and document the split.

If the issue is a payment dispute, treat it as a bank-led process. The account owner challenges the payment through their bank, and the bank decides the outcome. The processor can facilitate, but that is not closure evidence by itself. Keep the invoice record, original calculation, supporting delivery or procurement records, payment or dispute reference, and finance-approved corrected amount together.

Post the right adjustment document#

After classification, post the document that matches the corrected economics. A Credit memo reduces an invoice amount while preserving auditability. A Debit memo increases what the customer owes.

| Dispute scenario | Primary action | Close only when |

|---|---|---|

| Overstated price or quantity | Post Credit memo | Adjusted balance in Accounts receivable matches the Ledger journal |

| Understated price or quantity | Post Debit memo | Additional amount is posted and either collected or left as an approved open receivable |

| Duplicate payment with expected future activity | Hold as account credit | Credit is visible for future invoice application and ownership is assigned |

| Evidence still incomplete at SLA deadline | Keep invoice open and escalate | Finance approves next step; no shortcut posting used |

Checkpoint: one approved corrected calculation, tied to one journal-backed adjustment record. If you cannot show both, the dispute is not resolved.

Handle duplicate payments and missing evidence conservatively#

Confirm true duplicates first: invoice IDs, remittance details, prior applications, and unapplied cash position. If the customer is active, holding duplicate funds as account credit can be a clean path. If credit is not applied after three months, refunding is a documented fallback. If the relationship or scope is ending, refund is often the cleaner close. We recommend keeping the duplicate-funds path explicit so your team does not improvise credits under pressure.

Set evidence-owner SLAs for disputes and pre-disputes. Delayed responses can weaken formal dispute outcomes. If evidence is still incomplete at SLA expiry, keep the invoice open and escalate. Do not use Write-off to clear unresolved cases; write-offs are for uncollectible receivables after collection attempts.

Related reading: A Guide to Invoice Factoring for Freelancers. Want a quick next step? Try the free invoice generator.

Step 4 post adjustments and close invoices with audit trail integrity#

Close an invoice only after the approved accounting adjustment is posted. Post the approved Credit memo, Debit memo, or Write-off to the Ledger journal, let approval complete, and then move the invoice to closed.

Settlement is complete when accounting balances are zero, not when an ops status changes. Apply the related memos or adjustments to the invoice, then confirm the balance is actually cleared in accounting records.

Post first, then verify zero balance#

Use the same invoice reference across all settlement records. After posting, verify that invoice reference shows zero remaining balance in both Accounts receivable and the finance settlement view, including Accounts payable workflows where relevant. If either side still carries balance, keep it open.

| Close checkpoint | What must exist | If it fails |

|---|---|---|

| Adjustment posted | Approved Ledger journal entry tied to the Credit memo, Debit memo, or approved Write-off | Keep invoice open and resolve posting or approval |

| Balance cleared | Same invoice reference is zero in Accounts receivable and the settlement view finance uses | Reconcile unapplied payments or adjustments |

| Trace preserved | Source event, approver, and resulting journal entry ID linked to the settlement action | Block close until the record trail is complete |

To validate auditability, trace from subledger transaction detail to the posted journal entry. That GL-to-subledger path is what makes closure defensible.

Tie close status to immutable evidence#

Treat closure as an auditable record, not just a UI state. For each settlement action, retain the source event, approver, and resulting journal entry ID in a history that remains traceable after commit.

A common failure mode is closing in the application layer before posting is final. That creates closed invoices without posted accounting, or duplicate effects after retries.

Make retries safe#

Retries are expected; duplicate postings are not. Enforce idempotent close operations so repeated requests return the same result instead of creating duplicate settlement effects.

Use an idempotency key when creating or updating close-related objects, and keep the close rule strict: no posted adjustment, no zero balance, no closure.

For cross-border payout routing, see When Platforms Should Use Wires vs Local Rails for Cross-Border Payouts.

Common failure modes and how to recover fast#

Most settlement failures are recovery problems, not mysteries: one record moved ahead of the proof needed to close.

| Failure mode | Recovery check |

|---|---|

| Payout marked complete, invoice still open | Re-run Invoice reconciliation against the specific Payout batch, not only aggregate balances |

| Overpayment parked with no clear resolution | Assign a finance owner immediately, then resolve the excess as either a refund or invoice credit based on expected future activity |

| Missing PO or receipt evidence | Do not auto-close when required matching artifacts are missing |

| Dispute closed in ticketing, not in accounting | Treat ticket status as workflow state, not settlement proof |

- Payout marked complete, invoice still open: Re-run

Invoice reconciliationagainst the specificPayout batch, not only aggregate balances. Settlement-batch reconciliation is strongest at payout level, where a batch can look complete while an invoice line is still unmatched.

Recovery check: if cash movement exists but the invoice balance is still open, route it back to the missing accounting proof and complete that step before closing.

- Overpayment parked with no clear resolution: Assign a finance owner immediately, then resolve the excess as either a refund or invoice credit, for example via

Credit memo, based on expected future activity.

Recovery check: if you issue a refund, reconcile it to the bank statement line; if the overpayment is invoice-specific, attach claim details to the invoice application record.

- Missing PO or receipt evidence: Do not auto-close when required matching artifacts are missing. Missing

Purchase orderevidence breaks a clean2-way matchingflow, and where required, missing receipt evidence breaks3-way matching.

Recovery check: send discrepancies beyond configured tolerance to manual exception review with a clear requester action.

- Dispute closed in ticketing, not in accounting: Treat ticket status as workflow state, not settlement proof. Mark disputes resolved only when linked accounting evidence, such as a

Ledger journalrecord or transaction audit history, shows what changed, by whom, and when.

Recovery check: if that evidence is missing, keep the accounting side open and the invoice unsettled.

Close invoices faster without losing control#

You close invoices faster by tightening close controls, not by skipping them. If your team cannot trace a closed invoice from request and evidence to the final Ledger journal details, treat that as a design gap and fix it before scaling automation.

- Define the close state in writing.

An invoice is closed only when the balance is properly zeroed out in Accounts receivable or Accounts payable, and journal-side records reflect the same outcome. A payment event alone is not closure.

- Collect required evidence before settlement starts.

Keep the invoice and supporting documents together from the start. Where configured, include Purchase order data for 2-way matching and receipt evidence such as a Receiving report for 3-way matching, and compare discrepancies to your set tolerances.

- Settle the payment, then settle the invoice balance.

Confirm the payment was actually settled, then apply payments and any needed adjustment documents to the invoice so you do not leave unapplied balances behind. If payment activity is complete but the invoice is still open, post the missing accounting action before closing.

- Resolve disputes with explicit outcome rules.

Decide whether the original invoice stands, an adjustment is required, or the result is split. When the amount changes, post the correct adjustment document, for example Credit memo or Debit memo, and keep dispute evidence linked to the invoice.

- Post journal-impacting adjustments before marking closed.

Approved adjustments should post first, then status flips to closed. Your close record should preserve who approved the action and the journal-linked transaction details. Make close actions idempotent so retries do not create duplicate postings. If your reviewer cannot see who approved the action and which journal posted it, the invoice is not ready to close.

- Pilot narrowly, then expand with review gates.

Start with one payout lane and one dispute lane, prove normal-case accuracy and broken-case recovery, then widen automation. Auto-approve only invoices that meet criteria, and route the rest to authorized review. Your team should prove both the easy path and the ugly path before you scale automation.

For a step-by-step walkthrough, see Accounting Automation for Platforms That Removes Manual Journals and Speeds Close.

Frequently Asked Questions

What is `Invoice settlement` for platforms versus standard payment collection?

For platforms, Invoice settlement is broader than collecting money. In Accounts receivable and Accounts payable, settlement can involve any balance-affecting transaction, including invoices, payments, Credit memo entries, and fees. A payout or payment event may move cash while the invoice still needs an accounting adjustment before it is settled.

What is the difference between payment completion and invoice closure in `Accounts receivable`?

Payment completion means the money movement finished. Invoice closure means the invoice balance is zero in Accounts receivable and the accounting transaction history shows why. If one side says paid and the ledger still shows an open balance, treat it as unsettled until you post the missing adjustment.

When should teams use `2-way matching` instead of `3-way matching`?

Use 2-way matching when approval only depends on the invoice matching the Purchase order. Use 3-way matching when payment should also depend on delivery or receipt evidence, usually a Receiving report or product receipt.

How should we match payouts to invoices when amounts do not exactly match?

Match the invoice against the supporting records, then apply your configured amount tolerance. If the difference stays within tolerance, document the reason and keep the audit trail attached to the invoice. If the discrepancy exceeds tolerance, surface it as a variance and route it to manual review instead of auto-closing it.

When should we issue a refund versus a `Credit memo` after an `Invoice dispute`?

Issue a Credit memo when you need to reduce what the customer owes and the balance can stay on account. Issue a refund when cash must go back to the customer. Customer accounts may not show the refund for 5-10 business days, so reconcile against the processor or bank record while it is in flight.

What evidence is required before marking a disputed invoice as closed?

You need the dispute outcome, the supporting documents behind that decision, and the accounting proof that changed the balance. Depending on the matching flow, that can include invoice, Purchase order, and receipt records, plus the related balance-affecting adjustment (such as a Credit memo or refund posting). Mark the dispute closed only after the balance update is posted in the accounting record.

What minimum controls should exist before enabling auto-close logic?

At minimum, separate vendor setup, invoice approval, and payment processing responsibilities. Require evidence-backed matching before payment, block closure when core documents are missing, and stop auto-close when discrepancies exceed configured tolerances. If your automation cannot show who approved the action and which entry closed the balance, keep that case in manual review.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- docs.stripe.com/reports/payout-reconciliationtrusted

- docs.stripe.com/api/idempotent_requeststrusted

- finance.cornell.edu/accounting/topics/accountsreceivable/writeoffstrusted

- law.cornell.edu/wex/accounts_payabletrusted

- law.cornell.edu/wex/accounts_receivabletrusted

- oc.finance.harvard.edu/faq/what-happens-if-my-customer-makes-duplic...trusted

- ojp.gov/ovc_fmrc_guide_sheet_internal_control_separa...trusted

- stripe.com/resources/more/credit-memostrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Build a Vendor Portal for Platforms: Tax Forms Invoices Payouts and Disputes in One Workspace

Treat the **vendor portal for platforms** as an operating surface, not a file drop or message inbox. If it cannot support onboarding checks, invoice and payment visibility, clear access boundaries, and a reliable record of status changes, it will not take real work off finance and ops.

Improving Credit Card Reconciliation for Platforms with Auto-Match Invoice Controls

Auto-match works at scale only when you treat it as a control layer across invoices, the general ledger, approvals, and payout decisions, not as a convenience feature. At its core, credit card reconciliation is still a financial-control task. You are comparing card activity to internal accounting records to confirm transactions are accurate, authorized, and posted correctly.

Payment Reconciliation for Freelancers: How to Match Invoices to Bank Deposits

Payment reconciliation on freelancer platforms breaks down when a bank deposit cannot be tied, with confidence, to the right internal transaction. Your operating goal is simple: route each deposit into the right path, auto-match, manual review, or exception handling, and keep a record that can be traced from bank transfer through GL posting.