Quick Answer

Yes - platforms can offer instant payouts platform feature no float risk only when exposure is contractually shifted and operationally enforced. In practice, that means clear Liability Allocation and Fraud-Loss Responsibility terms, explicit downgrade paths to ACH, and no release before confirmed states. If your team cannot show contract clauses plus reconciled evidence for delayed or exception cases, the no-float claim is not ready for launch.

Why this decision is harder than most payout feature launches#

Step 1 Treat instant payouts as an infrastructure decision#

The hard part is not moving money fast. It is being honest about the risk you take on when you do. You can market Instant Payouts in a headline, but the speed promise only holds up when liquidity, routing, liability, and controls line up in the same sequence.

That is why this is a platform decision, not a feature toggle. In practice, real-time payment optimization is the coordination of liquidity, data standards, and routing logic, not just a faster send button. Fast rails can settle obligations in seconds rather than days, but that speed also forces you to handle irrevocability and liquidity directly. If your review is still centered on UX speed alone, you are evaluating the wrong thing.

Use a simple checkpoint: ask your team to describe, in one page, what funds the payout, what route it takes, and what happens if the payout instruction succeeds before your underlying funds position is final. If that answer lives partly in a product spec, partly in a provider sales deck, and partly in someone's Slack assumptions, you are not ready for a launch decision.

Step 2 Define the promise before you define the product copy#

Do not start with the headline. Start with the promise you can actually keep. The real decision is how to balance speed with fraud prevention, capital preservation, and clear risk ownership.

That means separating speed from risk ownership. A payout can be fast and still create exposure for your platform if the funding sequence is wrong, if fraud checks lag behind settlement speed, or if your contracts and internal controls leave responsibilities unclear. The recurring failure mode is simple: teams approve the speed promise first, then discover finance is carrying the capital and ops is cleaning up the exceptions.

Keep the real tradeoff in view from the start. It is not "fast versus slow." It is "fast with verified funding and clear liability and control decisions" versus "fast with hidden exposure." If you cannot verify the first condition, the responsible answer is to narrow rollout or delay go-live.

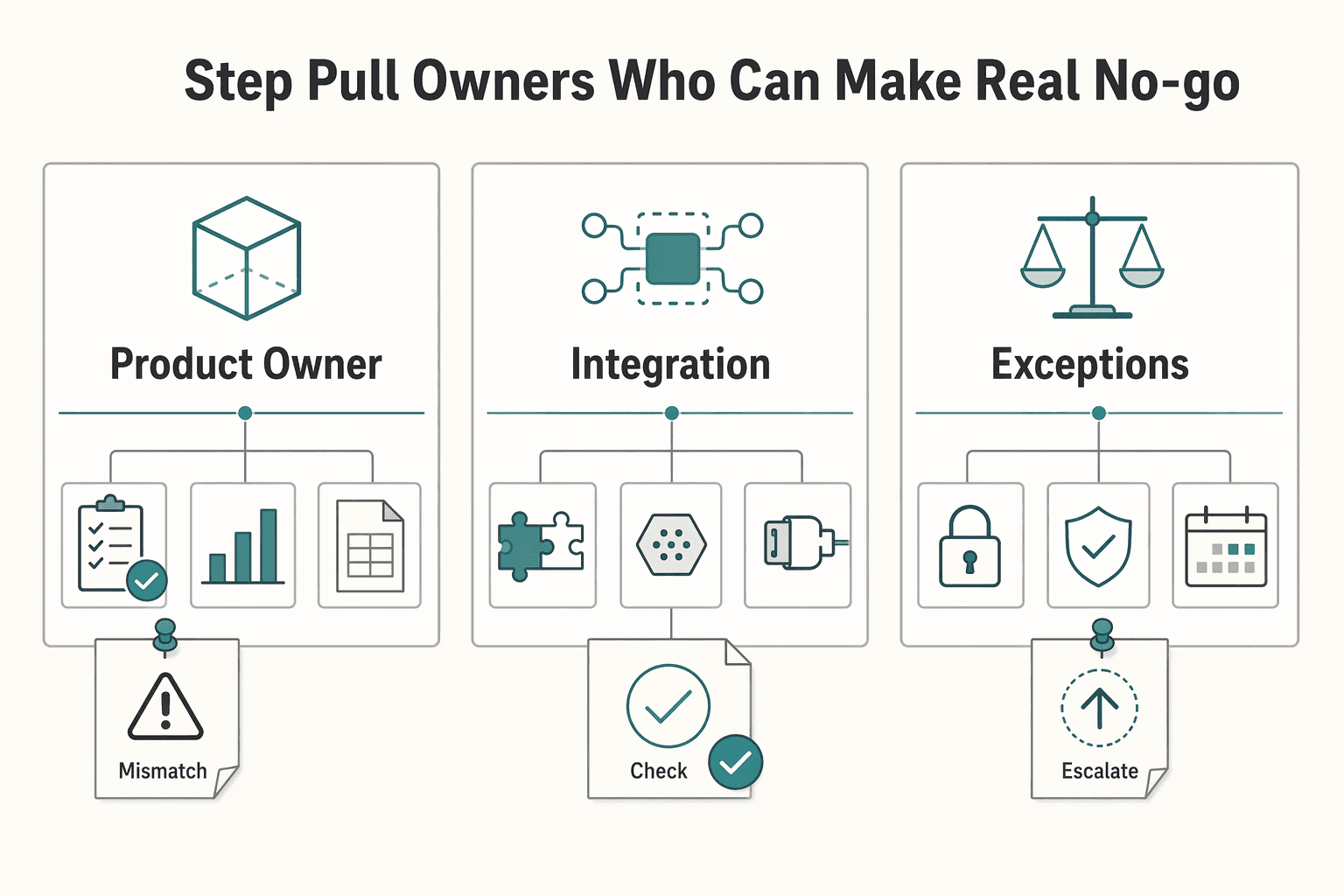

Step 3 Pull in the owners who can make a real go or no-go call#

You need a decision, not inspiration. Product, engineering, finance, and ops all own part of the answer because the scope includes compliance and liability, funding, payout methods, and integration needs, not just implementation effort.

In practice, you should expect at least four named owners before approval:

- A product owner for eligibility rules and customer promise

- An engineering owner for routing, state handling, and integration behavior

- A finance owner for liquidity, reconciliation, and capital preservation

- An ops or risk owner for exception handling and fraud prevention

If one of those seats is missing, the review usually skews toward speed and away from the costs that surface later. The rest of this article is built to help that group make a grounded call on whether your payout design truly aligns speed, funding, and controls, or only looks that way from the front end.

For a step-by-step walkthrough, see How Availability Heuristic Distorts Risk Assessment for Freelancers. If you want a quick next step, try the free invoice generator.

What no float risk actually means in payouts#

Step 1 Define float risk in funding terms#

No float risk means you do not disburse before funds are truly settled and available. Float risk is the timing gap between when you pay out and when incoming funds through ACH, Wire Transfers, cards, or other rails are final. If payouts go out while incoming funds can still be delayed, returned, or disputed, your platform is carrying exposure even if the user sees "paid."

Use a simple check for each payout path: document the funding source, the rail, and the exact point finance treats funds as final enough to release.

Step 2 Separate speed from settlement reality#

"Instant" describes speed, not risk removal. The OCC treats ACH, wires, cards, and Real-Time Payments as separate payment types with product-specific risks, and it separately identifies fraud, credit, and liquidity risk. Faster rails can reduce delay, but they do not automatically remove reversal exposure or the consequences of irrevocability.

Also, availability is conditional in practice. Stripe states the first payout has a 7-14 day waiting period, says that delay cannot be waived, and notes some countries can see waits up to 30 days (such as Brazil).

Step 3 Name the party carrying the loss#

Use one hard go-live rule: if your team cannot name who holds Liability Allocation and Fraud-Loss Responsibility for each payout route, you do not yet have no float risk. "The processor handles it" is not a control; ownership needs to be explicit in contracts and in your exception process.

Related: Integrated Payouts vs. Standalone Payouts: Which Architecture Is Right for Your Platform?.

What to prepare before you turn on Instant Payouts#

Do not turn on Instant Payouts until ownership, launch evidence, and fallback routing are explicit. Fast delivery can happen in seconds, but control failures still create timing and reversal exposure.

Step 1: Lock owners and eligibility rules. Assign one owner for eligibility policy, one for finance reconciliation, and one for engineering webhook/idempotency handling. Then document eligibility in plain language: who qualifies for instant delivery, which checks must pass, and when a payout routes to a slower path. If product, finance, and engineering give different answers for the same test recipient, do not launch.

Step 2: Build an approval evidence pack. Before go-live, collect the provider documents your team would rely on during exceptions: Settlement Guarantees, Reserve Requirements, reversals/returns, and dispute handling. The key test is simple: can you point to exact documents and internal owners when a payout is challenged? If not, the launch boundary is still unclear.

Step 3: Map instant and fallback routing end to end. Define the primary instant route and the fallback route for ineligible or unavailable instant cases. Make downgrade rules explicit in both ops policy and user-facing messaging, since card payout timing can still run up to 5 days in some flows. For each route, align engineering events and finance reconciliation expectations so retries do not create duplicates.

Step 4: Start with a narrow cohort and hard exclusions. Launch first with high-trust recipients and operationally complete profiles. Exclude recipients missing KYC/KYB readiness where your provider flow requires it, and require named approval for overrides. If instant eligibility fails, route cleanly to the fallback path instead of forcing instant coverage.

Choose the payout model and assign who holds exposure#

Choose the model by exposure first, speed second. If signed agreements do not clearly assign Reversal Exposure, timing-gap funding, and Liability Allocation, assume the platform is exposed.

| Model | Who funds timing gaps | Who carries Reversal Exposure | How Liability Allocation is documented | Practical fit |

|---|---|---|---|---|

| Provider-prefunded Instant Payouts | Provider/PSP | Usually the provider, only if contract language is explicit | Provider agreement, payout terms, Settlement Guarantees, reserve/reversal/dispute clauses | Best fit when your goal is to keep timing-gap exposure off your balance sheet |

| Platform-prefunded payouts | Platform | Platform, unless explicitly backstopped | Customer terms, provider contract, treasury/reserve policy, internal prefunding approvals | Fast customer promise, highest chance of recreating float risk |

| Delayed release via Escrow plus Split Logic | No early advance; release is conditional | Lower timing-gap exposure; release/operations risk remains | Escrow terms, release conditions, split rules, exception policy, user terms | Slower UX, often cleaner for refunds, holds, and multi-party flows |

Use a hard decision rule: if the provider will not contractually own timing-gap exposure and Settlement Guarantees are vague, do not market the feature as "no float risk." A fast UI or "real-time" label does not answer who absorbs a later reversal.

For marketplaces with volatile refund behavior, bias toward provider-funded rails and stricter Transaction Rules over the fastest possible disbursement. Then align product copy to the actual architecture: if instant is eligibility-based or conditional, say that plainly in the interface and help content. If you need help framing that promise, use pricing and UX design for instant payouts as a product decision input, not just a messaging pass.

Set contract and policy terms before launch#

Before launch, make risk ownership explicit in writing or assume the platform still carries it. Your provider agreement, payout policy, and exception rules should align on who absorbs loss, who can slow or stop payouts, and how incidents are handled.

Step 1 Write the provider non-negotiables into the contract packet#

Put the core exposure terms in one signed packet: Liability Allocation, Fraud-Loss Responsibility, Reserve Requirements, return handling, and outage obligations. Do not treat sales collateral or dashboard help text as binding evidence.

Use a simple cross-functional check: legal, finance, and ops should each be able to point to the exact clause that answers the same five questions. If answers vary by team, the launch position is not settled.

Keep third-party risk management practical, not abstract. The OCC payment-systems guidance explicitly frames payment-systems risk through operational risk, liquidity risk, third-party risk management, and policies, procedures, and internal controls. Apply that standard: if a term affects funding timing, reversals, or exceptions, it must be written and reviewable.

Step 2 Define eligibility gates as policy, not product copy#

After contract terms are clear, codify operating gates in policy. State when payouts are instant-eligible, when they downgrade to Same Day ACH, and when they are held for review, then mirror customer-facing outcomes in UX and terms.

The key is consistency across systems and teams: API behavior, support responses, and ledger treatment should follow the same rule set. If manual overrides can bypass holds without an audit trail, you have a control gap and potential exposure.

Step 3 Require explicit exception and reversal language#

Exception handling is where unclear risk allocation usually surfaces. Require explicit terms for reversals, delayed statuses, processor outages, and network incidents; if handling is left to "commercially reasonable efforts" or "case by case," treat ownership as unresolved.

Use an exceptions matrix attached to the contract or operating policy. For each exception type, define the action path (pause, downgrade, retry, pending) and assign ownership of any resulting loss or funding gap. If your bank partner or processor references payment-systems membership or notice requirements under 12 CFR 7.1026, keep that documentation in the launch packet.

If exceptions and reversals are not explicitly assigned, do not position the feature as no-float-risk in launch materials.

Build control gates in product and ops#

Control gates, not feature copy, determine whether instant payouts stay off your balance sheet. After contracts are set, make product logic, ops handling, and reconciliation enforce the same decision. If Fraud-Loss Responsibility sits with your platform, favor denial over speed.

The operating check is straightforward: policy is only real when eligibility rules, exception handling, and audit records all match. Use separate controls for regulatory/oversight adherence, scheme-rule handling, and risk management so one gap does not override the others.

Step 1 Build a control matrix that routes risk, not just payments#

Use one matrix across product, risk, support, and finance so each payout request gets one outcome: instant, slower rail, or hold.

| Risk level | Recipient verification status | Payment method | Transaction history | Payout rail | Required action |

|---|---|---|---|---|---|

| Low | Verified with no unresolved identity concerns | Known method with successful prior use | Established pattern with no active review flags | Instant-eligible rail (for example, Visa Direct) | Allow Instant Payouts |

| Medium | Verified but recently changed details, or pending additional review | Valid method but newly added or changed | Limited or mixed history | Slower rail (for example, ACH) | Auto-route to slower rail |

| High | Failed, missing, or inconsistent identity or risk signals | Method not yet trusted or still needs confirmation | New, unusual, or flagged activity | Hold by default; use separately approved rail paths only where policy allows (for example, wire) | Block instant path and require review |

Treat this as a control document, not a presentation artifact. Every row should have a named owner, a customer-facing outcome, and matching ledger treatment.

Set one hard rule: if identity or risk signals fail, do not return to the instant path through manual override.

Step 2 Assign queue ownership and escalation before exceptions happen#

Define exception operations before launch so delays and status conflicts are handled consistently, not ad hoc.

At minimum, define:

- A named owner for each hold/exception queue

- An internal review/disposition timing target

- An escalation path for webhook failures or conflicting provider statuses

Run a simple test on a held payout: who owns it now, what evidence clears it, and when it escalates. If answers differ, the queue is not controlled.

When Fraud-Loss Responsibility is yours, accept more false holds to avoid false approvals.

Step 3 Reconcile every status change to auditable records#

Require every payout status change to map to a ledger entry and a durable provider reference. Dashboard views can support triage, but they are not sufficient reconciliation evidence.

For every state change, record:

- What changed

- Which system or actor reported it

- What durable record proves it

If a provider reference cannot be matched to the internal payout record, keep the payout unresolved until it can.

Implement the technical sequence from request to reconciliation#

Treat the payout flow as a sequence of distinct states, not one event. Otherwise, you will create duplicate attempts and false completion signals.

Step 1 Validate before submission. Keep a fixed order: payout request, idempotency validation, policy gate evaluation, provider submission, webhook confirmation, ledger posting, then export-ready reconciliation state. If the same request appears twice, replay the prior outcome or keep it pending instead of creating a new disbursement attempt.

Before any provider call, require traceability: one internal payout ID, one idempotency reference, and one recorded policy decision (instant, ACH fallback, or hold). That gives ops and finance a clear reason for each routing decision later.

Step 2 Submit once and wait for confirmation. Instant-payment rails are described as real-time and 24/7, while ACH settles in business-hour batches. Because timing differs by rail, keep payout-request state separate from finance-complete state until confirmation arrives.

Do not resend blindly when confirmation is delayed. Keep explicit statuses such as requested, submitted, pending confirmation, confirmed, failed, and held.

Step 3 Post the ledger from confirmed events only. Ledger entries should follow confirmed payout-state changes, not optimistic UI updates or dashboard impressions. Wallet and recipient views can be useful projections, but audit and close should rely on the ledger trail.

A practical check is sampling completed payouts and confirming each chain is intact: request ID -> provider reference -> ledger entry -> reconciled status.

Step 4 Export only reconciled records. Define an export-ready state finance can use without manual cleanup. Include internal payout ID, provider reference, amount, recipient, current status, and the confirming-event timestamp tied to ledger posting.

This is where fragmented stacks create drag: in one cited travel context, reconciliation cycles were reported as ~20% longer when teams had to manually align transactions across platforms. If exports still depend on dashboard checks, support notes, or spreadsheet joins, tighten the sequence before expanding eligibility.

Related reading: Named Perils vs. All-Risk Insurance Policies: How Burden of Proof Shapes Claims.

Common mistakes that recreate float risk and how to recover#

Float risk usually comes back through policy and ownership gaps, not through a lack of payment-rail options.

| Mistake | Recovery |

|---|---|

| Promising "instant for everyone" before eligibility logic exists | Narrow eligibility now, and make payout timing rules explicit anywhere users make decisions |

| Treating provider marketing language as risk allocation | Pause expansion until legal and ops confirm what your executed agreements actually assign |

| Treating delayed webhook signals as failed payouts and resending blindly | Treat delay as uncertainty, enforce idempotency on retry paths, and reconcile references before any second submission |

| Leaving exception queues without clear ownership | Assign joint finance-ops and engineering ownership, then define the evidence required to close each item |

Mistake 1: Promising "instant for everyone" before eligibility logic exists. Recovery: narrow eligibility now, and make payout timing rules explicit anywhere users make decisions. Keep your public promise aligned with your actual rules, consistent with transparency and public-disclosure expectations.

Mistake 2: Treating provider marketing language as risk allocation. Recovery: pause expansion until legal and ops confirm what your executed agreements actually assign. This is a third-party risk management control, not a copywriting decision.

Mistake 3: Treating delayed webhook signals as failed payouts and resending blindly. Recovery: treat delay as uncertainty, enforce idempotency on retry paths, and reconcile references before any second submission. Keep ledger movement tied to confirmed state changes.

Mistake 4: Leaving exception queues without clear ownership. Recovery: assign joint finance-ops and engineering ownership, then define the evidence required to close each item. That aligns with policies, procedures, internal controls, and broader scheme-rule and risk-management governance expectations.

If your process spans multiple rails, keep control design specific to each one rather than assuming one generic flow covers all cases; the OCC framework separates product-specific risks for ACH, payment cards, and real-time payments.

Make the decision and launch in controlled phases#

For a no-float Instant Payouts claim, launch only when exposure ownership is documented, enforceable, and reconcilable. If that proof is unclear, do not launch.

- Confirm the launch model and name the risk owner.

Document the exact first payout path, including fast rail and fallback rail (such as ACH). For each path, assign one owner who can clearly state timing-gap exposure, Fraud-Loss Responsibility, and Reversal Exposure.

- Confirm contract terms and your control matrix in one approval session.

Review one shared pack with product, finance, and engineering: executed contracts/addenda, control matrix, eligibility rules, and exception ownership. Treat provider capability and provider liability as separate checks.

- Confirm reconciliation proof before broad rollout.

Validate a reconciled sample from payout request through provider reference, status changes, ledger posting, and final money state, including delayed or exception cases.

- Enable the smallest cohort that can validate the claim.

Start narrow so exceptions can be inspected end to end, including fast-rail behavior and fallback behavior.

- Keep rollout phased and expand only on stable outcomes.

Use a fixed review cadence (for example, weekly) and expand only when risk outcomes, ops load, and reconciliation accuracy remain stable without ownership ambiguity.

Frequently Asked Questions

Can a platform offer instant payouts without float risk?

Potentially, but only if the timing-gap exposure is actually shifted away from your platform in signed agreements and then enforced in product policy. Fast recipient access is not enough on its own. If finance cannot show both contractual risk allocation and reconciled payout evidence, do not market the feature as no-float.

Who holds float risk when funds move instantly?

"Instant" describes payout speed, not loss ownership. The ECB describes the shift toward intra-day or near-real-time payments, and the OCC frames payment activity around operational, fraud, credit, and liquidity risk, so you need to read the rail design and provider agreement together. The party holding risk is typically the one named, or left exposed, in liability, reversal handling, reserve, and exception language.

Is starting with receiving-side capabilities safer than sending first?

It can be safer, because your team can learn reconciliation, delayed event handling, and support escalation before you add fast outbound disbursement risk. A good checkpoint is simple: take a sample of delayed transactions and confirm each one ties from your internal payout ID to the provider reference to the final reconciled state without a resend. If you cannot prove that path yet, keep outbound instant access narrow.

What contract clauses matter most before launch?

Start with Liability Allocation, Fraud-Loss Responsibility, Reserve Requirements, reversal handling, and Settlement Guarantees. Then read for the failure cases, not just the happy path: network outage language, processor delay treatment, return timing, and whether the provider can push losses back to you after provisional payout. Vague wording here can be a red flag, because it may hide platform exposure.

When should we downgrade from instant to ACH?

Downgrade when eligibility checks fail, when provider confidence is low, or when policy gates require more review than an instant rail can safely tolerate. Finix notes that Visa Direct can send funds to eligible debit or prepaid cards within minutes, even as little as one minute, but that is an eligibility-based speed claim, not a universal promise. If the recipient or transaction does not clearly qualify, route to ACH and state the timing plainly instead of forcing a risky exception.

What proof should finance request before calling this no float risk?

Ask for the executed contract set, including the payout product addendum, the sections covering Liability Allocation, Fraud-Loss Responsibility, Reserve Requirements, reversals, and any Settlement Guarantees. Then ask for operational proof: a reconciled sample showing payout request time, provider reference, webhook or status confirmation, ledger posting, and the final money state for at least one delayed or exception case. If the evidence stops at a provider dashboard screenshot, the claim is not strong enough yet.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bis.org/cpmi/publ/d154.pdftrusted

- ecb.europa.eu/pub/pdf/scpops/ecb.op229~4c5ec8f02a.en.pdftrusted

- fastpayments.worldbank.org/sites/default/files/2025-07/FPS_Governance%2...trusted

- federalreserve.gov/newsevents/pressreleases/files/US-path-to-fa...trusted

- leginfo.legislature.ca.gov/faces/billTextClient.xhtmltrusted

- mn.gov/deaf-hard-of-hearing/rest/rss/Newstrusted

- occ.gov/publications-and-resources/publications/comp...trusted

- sec.gov/Archives/edgar/data/1524566/0001628279250004...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Platforms Can Offer Instant Payouts as a Premium Feature Without Margin Surprises

Treat instant payouts as a paid acceleration option, not a blanket promise that money always arrives immediately. Teams tend to get better results when they package it as a Premium feature with clear scope limits, then make those limits visible before pricing, copy, or rollout decisions harden.

What Instant Payouts Really Cost Platforms for Same-Day and On-Demand Pay

Fast access can improve worker experience, but speed is not the core decision. The real question is whether you can move money earlier without losing margin discipline, record clarity, or control over exceptions. Instant payouts are an economics and controls choice first, and a UX feature second.

Integrated Payouts vs Standalone Payouts for Platform Architecture Decisions

**Treat integrated and standalone payouts as an architecture decision, not a product toggle.** The real split is the same one you see in payment processing more broadly: either payments are connected to the core platform experience, or they are not. [Lightspeed](https://www.lightspeedhq.com/blog/payment-processing-integrated-vs-non-integrated) puts that plainly in POS terms: your payment terminal either speaks to your point of sale, or it does not. For platform teams, the equivalent question is whether payment flows run through one connected system or sit in separate lanes you manage independently.