Quick Answer

Start by selecting the reserve model that matches your payout risk pattern, then enforce release with dual controls. For reserve policy design for platforms, the practical baseline is rolling holds for variable timing risk, fixed minimum balances for stable programs, and a hybrid only when finance, ops, and engineering can govern exceptions together. Before funds move from hold to payable, confirm payout eligibility plus a reconciliation-backed ledger check rather than trusting one provider status.

Set hold, release, and evidence rules up front#

Reserve policy for a platform comes down to three things: decide what gets held, when it gets released, and how you will prove later that the release was justified. For embedded payments, that is usually the hard part. A good reserve policy is less about abstract risk theory and more about controls your finance, ops, and engineering teams can verify from event history and payout records.

This article is for platform operators who own contractor, creator, or marketplace payouts and need decisions they can implement. The clearest way to approach the problem is to split it into three jobs:

- Reserve model

This is the structure of the hold itself. A reserve plan can automatically hold a percentage of each charge to cover refund and dispute exposure, which fits when risk appears continuously rather than as a one-off event. The main distinction is whether you use ongoing protection tied to charge activity, such as a rolling reserve, or an account-level reserve approach.

- Release logic

Release rules matter as much as the hold. Supported release behavior can follow a fixed date or a rolling schedule based on a set number of days after the associated charge, and reserve duration cannot exceed 180 days. The tradeoff is predictability versus responsiveness. A fixed release is easier to explain, while rolling release tracks transaction age more closely when payout timing and reversals do not line up neatly.

- Auditability

A reserve policy is only credible if your team can reconstruct what happened. In practice, that means your internal accounting records, webhook event history, and payout reconciliation need to line up. Webhooks capture payment events that happen outside the direct payment flow, and payout reconciliation ties each bank payout back to the batch of transactions it settles. The key test is whether your control can be verified at transaction level, not just described in a policy doc.

This is where many teams get exposed. If release depends on one provider status flag, a missing webhook or stale payout state can turn a sensible rule into an early-release mistake. Use a simple checkpoint. Before you relax a hold, confirm at least one event-driven signal and one accounting-verifiable signal. Then make sure your payout reconciliation can trace the money to the settled transaction group.

As you read the rest, treat every reserve choice as an operating tradeoff. If your biggest issue is timing mismatch, start by choosing the right model. If your bigger problem is uncertain user behavior, start with stricter release gates and require an evidence pack for exceptions. That pack should include the reason, approver, related accounting entries, and the next review date.

For more background, see What Is a Balance Sheet? How Payment Platforms Account for Held Funds Reserves and Liabilities. If you want a quick next step, try the free invoice generator.

Choose the reserve model before you tune thresholds#

Choose the reserve structure first, then tune thresholds. You need the hold-and-release logic to be clear before any percentage or floor is meaningful.

| Consideration | What to check | Grounding detail |

|---|---|---|

| Wallet balance volatility | Balance-movement patterns around payout timing and reversal timing | Choose timing-based holds such as rolling behavior, or an account-level floor, based on what is easier to operate and defend from your records |

| Refund and dispute exposure | Whether exposure is temporary or tied to a specific date | If exposure is temporary or tied to a specific date, fixed reserve plans are the better starting point; fixed-release plans require a release date 3 to 180 days in the future, and connected-account reserves cannot exceed 180 days |

| Payout batch maturity | Whether reserve deductions reconcile to payout records and ledger journal entries | In Adyen, the amount needed to fill the reserve threshold is deducted from payable balance when the payout batch closes |

This section is for platform and marketplace payout operators running multi-party flows with embedded payments and KYC gating. If you cannot reliably trace holds and releases in your ledger journal, or you lack enforceable payout and AML controls where those obligations apply, fix that before threshold tuning.

- Wallet balance volatility

Use balance-movement patterns around payout timing and reversal timing to choose the model. Decide whether timing-based holds, such as rolling behavior, or an account-level floor are easier to operate and defend from your records.

- Refund and dispute exposure

Reserves are meant to keep funds available for refunds, chargebacks, and related operational expenses. If exposure is temporary or tied to a specific date, fixed reserve plans are the better starting point; Stripe fixed-release plans require a release date 3 to 180 days in the future, and connected-account reserves cannot exceed 180 days.

- Payout batch maturity

Treat payout-batch behavior as a hard readiness check before tightening thresholds. In Adyen, the amount needed to fill the reserve threshold is deducted from payable balance when the payout batch closes, so every deduction should reconcile to payout records and ledger journal entries.

Use a simple rule: if your biggest risk is timing mismatch, start with structure; if your bigger risk is uncertain behavior, tighten release gating and improve disclosure before loosening payout access.

For a step-by-step walkthrough, see Merchant of Record for Platforms and the Ownership Decisions That Matter.

Rolling reserve is best for variable risk and uneven payout timing#

If your main risk is ongoing timing mismatch, a rolling reserve is usually a better structure than a fixed minimum balance. It withholds part of each new transaction and releases on a rolling schedule, for example a 30-day rolling window, so release timing follows transaction timing instead of one static floor.

- Best fit: variable inflows and ongoing exposure

Use rolling logic when credits, refunds, disputes, or returns do not land on the same timeline as payouts. This structure is designed for ongoing risk, not one-off holds.

- Why it works operationally: event-linked holds and releases

Rolling holds map cleanly to payout operations because each held amount can be traced to its originating transaction, hold rule, and release event. Your control point is simple: you should be able to trace every hold and release in ledger journal history.

- Main tradeoff: predictability for sellers and creators

The model can feel unpredictable when users only see gross inflows and available balance, without reserve deductions and expected release timing. Clear reserve visibility is what keeps support and trust issues from growing.

A practical use case is a marketplace that gives customers dedicated Virtual Accounts for inbound transfers, then sends payouts by API. In that flow, credits and payout-status updates can arrive asynchronously by webhook, so rolling reserve timing is typically a better match than a static balance floor.

Do not release funds on the first positive payout event alone. Webhooks are useful for status changes, but a payout status update on its own does not confirm final bank settlement. Set release triggers using both event state and ledger evidence that funds are actually releasable.

If reversals regularly appear after credits already look available, choose the rolling structure first and tune percentages second.

If you want a deeper dive, read Accounts Payable Workflow for Platforms: How to Design an Efficient End-to-End Payables Process.

Minimum balance is best for stable programs with predictable risk#

If your risk profile is steady, a fixed minimum balance is usually the cleanest reserve shape. It works best in mature payout programs with consistent account behavior and documented KYC, KYB, and AML controls, but it is still a policy choice, not a guarantee.

- Best fit: stable accounts with known behavior

A minimum balance keeps a set amount in the account and pays out only what is above that floor. Eligibility depends on whether available funds exceed the threshold, not on transaction-by-transaction aging. A common starting point is 4 to 5 times average daily processing volumes, then tuning from observed refunds, disputes, and fees.

- Why operators choose it: easier payout checks and cleaner reconciliation

The rule is mechanical and auditable. Reserve-threshold funding can be deducted from payable balance at payout-batch close, which makes payout logic easier to verify from ledger and reconciliation records. For each batch, you should be able to confirm the opening balance, configured floor, payout amount, and ending retained balance.

- Main tradeoff: one floor can become too rigid

A fixed floor can over-restrict healthy accounts during growth or seasonality while still under-covering higher-risk cohorts. It can also fail operationally if reserve coverage is too thin, including refund failures when funds are insufficient. If refunds, fees, or disputes are concentrated in a narrow cohort, one account-wide floor may hide segmentation issues instead of fixing them.

A strong use case is a recurring-payments platform with steady activity, documented AML review paths, and routine finance reconciliation. In that environment, minimum-balance rules are usually easier to explain and enforce than rolling reserves.

One practical recommendation: use a fixed floor only when you can show post-payout liabilities are predictable enough to size it, and confirm the feature is supported in your market. One published minimum-balance implementation excludes Brazil, India, and Thailand.

Hybrid reserve is best when you need both baseline protection and adaptive control#

A hybrid reserve makes sense when you need a fixed floor for predictability and rolling controls for changing risk. Keep a minimum balance as the default for stable cohorts, and apply rolling holds only where timing risk or behavior still needs extra protection.

- Baseline floor for stable cohorts

Use a standing reserve threshold so each eligible account keeps a known buffer before payout. In threshold-based setups, the amount needed to refill the reserve is deducted from payable balance when the payout batch closes, which keeps reconciliation straightforward. If an account passes your stability checks, release toward that baseline instead of leaving it in a permanently restrictive state.

- Rolling hold for accounts or periods with active risk

Rolling reserves are for ongoing risk management and can automatically hold a percentage of each charge. Typical reserve periods are often 30-90 days, and connected-account reserve plans cap duration at 180 days. Use a clear if-then rule: if behavior is stable, release toward the floor; if refunds, disputes, or review signals rise, tighten release triggers before you expand payouts.

- Tax and reporting gates for cross-border payout programs

Hybrid policies are useful when payout eligibility depends on both risk and documentation status. Form W-9 provides payer-side TIN data for IRS information returns, while specific W-8 forms can exempt foreign persons from backup withholding and Form 1099 reporting. Keep reporting paths distinct: payment card and third-party network transactions are reported on Form 1099-K under section 6050W, not on Form 1099-MISC or Form 1099-NEC.

The main tradeoff is governance overhead. Finance should own reserve sizing and reconciliation checks, ops should own cohort changes and exception handling, and engineering should own ledger and payout implementation so reserve logic does not drift.

Before you loosen controls, require an evidence pack: cohort reason, W-8/W-9 status, linked payout batch IDs, and ledger entries showing the account can move from rolling treatment back to baseline without creating reconciliation gaps.

Set reserve release triggers that survive audits and incidents#

After you pick a reserve model, release logic becomes the real control. Do not release funds from a single status flag. Use at least two proofs: the account is eligible for payout, and finance can tie the release to settled activity in your ledger journal.

| Gate | Evidence to require | Purpose |

|---|---|---|

| Compliance | Confirm KYC and compliance review before calculating what is releasable | Answers whether you can pay the account at all |

| Transaction integrity | Map each release or payout request to one logical action and one idempotency key | Reduces duplicate payout attempts caused by retries, delayed jobs, or replayed requests |

| Settlement confirmation | Treat provider webhook events as required evidence, not standalone truth | Helps catch missing provider events and stale local payout states before release |

| Finance reconciliation | Tie payout or settlement batches back to booked transactions in the ledger journal | Provides the accounting-verifiable gate |

A practical gate order is compliance, transaction integrity, provider settlement evidence, then finance reconciliation.

- Compliance gate before payout eligibility

Confirm KYC and your compliance review before calculating what is releasable. Stripe says connected accounts must satisfy KYC before they can accept payments and send payouts, and Adyen also ties verification to payout capability. This gate answers whether you can pay the account at all.

- Transaction integrity gate with an

idempotency key

Map each release or payout request to one logical action and one idempotency key. Stripe idempotency supports safe retries, and repeated requests with the same key return the same result. This gate reduces duplicate payout attempts caused by retries, delayed jobs, or replayed requests.

- Settlement confirmation from

webhookstate

Treat provider webhooks as required evidence, not standalone truth. Stripe documents duplicate webhook deliveries and automatic retries of undelivered events for up to three days, including cases where retries continue after manual processing. This gate helps catch missing provider events and stale local payout states before release.

- Finance reconciliation against the

ledger journal

Require a reconciliation check that ties payout or settlement batches back to booked transactions. Stripe payout reconciliation is designed to match bank payouts to payment batches, and Stripe provides payout.reconciliation_completed for completed reconciliation. This is the accounting-verifiable gate.

Recommendation: never release on one signal. Require at least one compliance gate plus one accounting-verifiable gate before funds move from hold to payable.

For manual exceptions, require a consistent evidence pack:

- reason code

- approver

- linked

ledger journalentries or payout batch references - expected re-check window

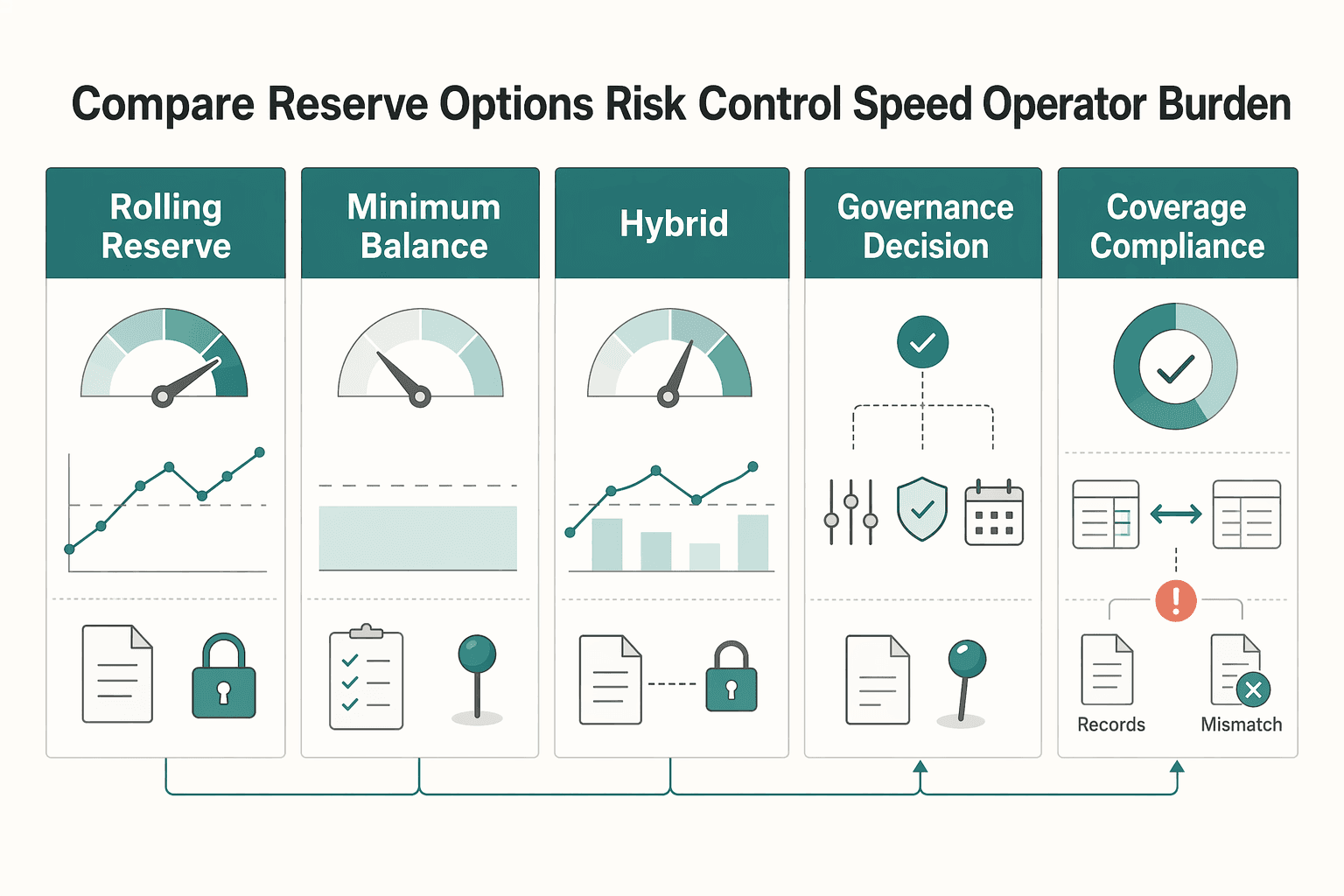

Compare reserve options by risk control speed and operator burden#

Choose rolling reserve when risk changes quickly, choose minimum balance when operational simplicity matters most, and use a hybrid only if you can govern it tightly. The right model is the one your team can explain and verify in each payout batch without creating avoidable exceptions.

| Model | Best for | Protection strength | Payout friction | Support burden | Implementation complexity | Auditability artifacts |

|---|---|---|---|---|---|---|

| Rolling reserve | Variable risk, uneven settlement timing, cohorts with changing refund or dispute exposure | Built for ongoing risk over time; Stripe describes rolling reserve plans as for automated management of ongoing risk | Can be higher when fund availability depends on moving hold windows | Can rise when release timing is harder to explain | Higher, because release trigger logic must combine timing, settlement evidence, and reconciliation state | Time-based hold rules, webhook settlement evidence, reserve balance history, linked ledger journal entries |

| Minimum balance | Stable programs with predictable behavior after KYC and KYB checks are consistently passed | Baseline protection from a fixed floor; PayPal defines it as a specific minimum amount you are required to keep available | Often lower when the floor is explicit in balance calculations | Often lower when release decisions are based on one visible threshold | Lower, because payout eligibility can check one floor before release | Floor policy, balance snapshots, payout eligibility checks, finance reconciliation records |

| Hybrid | Mixed cohorts, segmented programs, or setups that need both a floor and time-based withholding | Can be stronger for some cohorts, but only when rule precedence is explicit and controlled | Can be higher because both floor and time-window rules can affect availability | Can be higher when exceptions cross finance, ops, and engineering | Highest, because you must define and enforce precedence between hold types | Policy version history, exception approvals, ledger journal support for both hold types, release evidence pack |

| Governance decision | Any platform changing controls after launch | Control strength depends on how hard it is to loosen policy without evidence | Some friction is intentional before loosening controls | Manageable when one owner coordinates finance, ops, and engineering | Medium, but required | Named approver, review cadence, change reason, payout-batch exception review, and proof compliance and reconciliation gates still hold |

| Coverage and compliance caveats | Programs spanning markets, products, or tax setups | Varies by provider, market, and enabled features | Can increase when onboarding or tax checks block payout eligibility | Often appears during expansion or reclassification | Medium to high when market or program rules differ | Verify platform-country and connected-account country eligibility, KYB collection status, and tax-validation dependencies, including VAT validation differences by market |

A quick operational check is to review payout-batch exception rates, refund outcomes, and journal tie-outs together. If refunds fail because reserve funds are missing or insufficient, treat that as a policy-design signal, not only a treasury issue; Adyen documents that refunds can fail when no reserve is set or funded enough.

Before you loosen controls, require evidence instead of assumptions: recent ledger journal matches, payout-batch exception trends, current compliance status for affected cohorts, and the exact policy version being changed. Also verify market and program coverage directly, since connected-account country availability depends on platform location and enabled features, and some platform financial-account programs are US-only.

Do not assume tax or entity checks transfer cleanly across markets. Your platform is responsible for collecting required KYC and KYB onboarding data, and VAT validation is not uniform; in the EU VIES context, UK (GB) VAT number validation ceased on 01/01/2021.

You might also find this useful: Payout Status Page Design: How Platforms Reduce Where-Is-My-Money Support Tickets.

Implement in 90 days with clear owners and verification checkpoints#

A 90-day rollout can work when each phase has a single owner and you advance only on verified evidence from finance, ops, and engineering.

- Days 1 to 30: define policy objects and state evidence

Define the policy objects your team will operate: reserve type, payout hold, release trigger, exception reason, manual override, and recheck window. For each hold and release state, map the expected ledger journal entry and the webhook outcome that supports it. If a release cannot be tied to clear accounting and event evidence, keep the rule out of production. Finance signoff here should confirm the state map reconciles before live changes.

- Days 31 to 60: run shadow mode and test retry safety

Replay production traffic in shadow mode so candidate logic runs without changing live payouts. Validate that retries with the same idempotency key return the original result instead of creating duplicate payout behavior, and test keys both inside and beyond the 24-hour retention horizon. Include temporary endpoint failure cases, because webhook redelivery can continue for up to three days.

- Days 61 to 90: phase rollout by risk tier

Roll out by cohort instead of switching all accounts at once, with explicit phases such as 25% -> 50% -> 100% across payout batch runs. At each phase, review release latency, payout failures, and manual override frequency together. Pause progression if override load rises or release outcomes become harder to explain operationally.

- Verification checkpoints: require three function-level approvals

Finance signs off on reconciliation and journal tie-out. Ops signs off that exception queues are understandable and manageable. Engineering signs off that event handling is replay-safe and rollback paths work. Keep an evidence pack per checkpoint with sample exceptions, linked journals, duplicate-request replay results, and the approved policy version.

For a related workflow view, read Figma Design Handoff for Freelancers and Small Design Teams.

Conclusion#

If you are still choosing between models, the practical answer is simple: do not chase a universally right reserve structure. Choose the one that fits your risk profile, payment-channel mix, and the level of operating discipline your team can actually sustain.

- Choose the model you can defend in operations

Different reserve models fit different payout and reversal timing, and different operating patterns. A rolling reserve, a minimum balance, or a hybrid can each be workable depending on your channel mix and how much control overhead your team can run reliably. What matters is fit: the right design matches the complexity of your products, services, and payment channels, not the one that sounds most sophisticated on paper.

- Make release logic prove eligibility, not assume it

Your release rule should rely on multiple verifiable signals, not a single status change. A practical baseline is a compliance gate, an accounting-verifiable check, and a replay-safe payout control before money moves. In practice, that means checking payout eligibility, confirming the relevant state, matching the release to the expected ledger journal, and using an idempotency key so retries do not create duplicate payout effects. The control is only real if you can verify it before and after a payout run. If a hold is released because one provider status flipped, you are one stale event or retry bug away from a bad payout.

- Treat policy, evidence, and governance as one decision

A reserve policy is not complete when the thresholds are written down. It is complete when the process is documented, exceptions are reviewable, and each transaction record preserves who created it, what it did, and when it happened. For any manual override, keep an evidence pack with the reason, approver, linked ledger journal entries, and the next re-check date. Review cadence matters. A strong benchmark is management checking adherence at least quarterly, with board-level review of risk information at least semi-annually.

The point is not to pick the most conservative model forever. It is to start with controls that fit your current maturity, then tighten or relax them only when the evidence supports it. If you cannot explain a payout hold or release all the way from policy rule to ledger journal, do not loosen thresholds yet. Fix the documentation, replay safety, and approval path first, and the rest of the policy will scale with far fewer surprises.

Frequently Asked Questions

What is a reserve policy for a platform, in practical payout terms?

It is the set of rules that decides what portion of funds stays on hold, why it stays there, and when it becomes eligible for payout. In practical terms, the point is to buffer transaction liabilities such as chargebacks and refunds, not to create a vague risk bucket. In practice, teams should tie each hold or release to a clear reason code and matching accounting record so the policy is easier to operate and audit.

What is the difference between a rolling reserve and a minimum balance?

A rolling reserve holds a percentage of daily transactions and releases those funds later on a schedule. One published example is 10% of money received on day 1 being released on day 91, which shows how delayed availability works over time. A minimum reserve instead keeps a fixed amount in reserve balance, so it can be easier to explain while being less responsive to transaction-volume changes.

What should count as a valid reserve release trigger?

Completion of the configured holding period can be one valid trigger, but it should not be the only one you trust. A release is safer when the hold period has ended and additional controls confirm the account is still payout-eligible and the release matches accounting records. If your ops team is releasing based on one provider status flag alone, you can create audit and incident risk.

How often should we review and adjust reserve policy rules?

Use quarterly as the minimum management review cadence, because that is a supported governance benchmark for checking whether operations still match policy. Review sooner when risk patterns change, especially after notable shifts in disputes, refunds, or exception handling. During rollout or after a rule change, review more frequently than quarterly rather than waiting for quarter end.

Who should approve reserve policy changes across finance, ops, and engineering?

Keep approval separate from day-to-day execution. The governance model that matters most is periodic approval and review at the board or risk committee level, with senior management monitoring compliance with the policy at least quarterly. Inside the platform team, a common split is finance reviewing reserve-accounting impact, ops confirming exception handling, and engineering verifying payout behavior before anything ships.

What breaks first when release triggers are too strict or too loose?

When triggers are too strict, payout friction usually shows up first. A very hard posture can look like holding 100% of processed transaction funds for 7 days, which may protect risk but creates clear payout delay. When triggers are too loose, the more dangerous failure is that disputed amounts can exceed the funds left in the account, leaving your platform short at exactly the wrong moment.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/manualtrusted

- docs.stripe.com/connect/connected-account-reservestrusted

- docs.stripe.com/webhooks/process-undelivered-eventstrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-12/chapter-II/subchapter-A/par...trusted

- federalreserve.gov/frrs/regulations/section-25234-liquidity-ris...trusted

- federalreserve.gov/frrs/guidance/interagency-policy-statement-o...trusted

- irs.gov/instructions/i1099mectrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Designing an End-to-End Accounts Payable Workflow for Platforms

Start with the process, not the product demo. Full-cycle Accounts Payable (AP) runs from purchase order through payment and reconciliation. Weak design usually shows up later as invoice delays, duplicate payments, missed due dates, and supplier disputes.

What Is a Balance Sheet? How Payment Platforms Account for Held Funds Reserves and Liabilities

If you own payouts, the core question is not what sits on the balance sheet. It is what obligation you can prove, what amount should stay held, and what can safely move. For finance, ops, and product teams dealing with balance sheet treatment for payment platforms - held funds, reserves, and liabilities - that distinction matters more than tidy labels. If your team cannot explain that distinction at release time, your close process is weaker than it looks.

Payout Status Page Design That Reduces Where-Is-My-Money Tickets

Many examples of **payout status page design** focus on visual inspiration instead of operating guidance. Layout ideas can help, but they do not answer the question your finance or support team asks most: where is the money, who owns the next step, and what proof do we have?