Quick Answer

Separate customer held balances, reserve holds, settlement payables, and Accounts payable, then release funds only after proof in ledger journals. For balance sheet payment platforms held funds reserves liabilities, treat delayed or duplicate webhooks as open items, not payout-ready states. Require a documented trigger for each reclassification, keep blocked KYC/AML amounts visible, and tie payout batch totals to approved release entries before money moves.

Where held funds, reserves, and liabilities show up on the balance sheet#

If you own payouts, the core question is not what sits on the balance sheet. It is what obligation you can prove, what amount should stay held, and what can safely move. For finance, ops, and product teams dealing with balance sheet treatment for payment platforms - held funds, reserves, and liabilities - that distinction matters more than tidy labels. If your team cannot explain that distinction at release time, your close process is weaker than it looks.

A balance sheet shows assets, liabilities, and shareholders' equity. A liability is a present obligation from past events that is expected to result in an outflow of resources. In platform money movement, that gets practical fast. Once cash is received, credited, held for release, reserved for risk, or queued for payout, classification should follow the obligation reflected in your records, not just a dashboard label. Use this article as an operating tool, not an accounting lecture. Every item supports one of four decisions:

- What to classify

Separate customer held balances, reserve amounts, and other payable buckets instead of combining everything into one broad "funds held" bucket. If you cannot clearly state who is owed the money and what event changes that status, the classification is too loose. We recommend forcing your team to name that event before it changes the bucket.

- What to reconcile

Journal entries matter, but they are not enough on their own. Payment operations are asynchronous, so status updates and cash movement do not always land at the same time. The real checkpoint is whether ledger journals tie to event evidence and transaction-level settlement reporting, not just to an internal balance summary.

- What to hold

A common control is to keep owed balances recorded as liabilities until release conditions are met. That can include funds held pending release conditions and reserves set aside for potential reversals or claims risk. A useful distinction is that reserves are risk buffers, while held funds are often tied to a customer or merchant obligation waiting on a release trigger.

- What to release

Treat payout readiness as something you verify, not assume. If an event is delayed or duplicated, or if a release condition is still pending, keeping the liability open is often the safer call. A practical failure mode is a product-layer "paid" state that is not backed by reconciled settlement evidence. We would rather keep your liability open than let your team release against a status your books cannot support.

Two control themes run through the rest of this article. Platforms may hold balances across product and currency states, and event handlers can receive duplicate deliveries. Your process should prevent duplicate posting and show that each payout release was triggered only once.

If your team cannot produce a liability roll-forward, supporting ledger journals, and reconciliation evidence for a bucket at close, treat that as an operating gap. The rest of this list is built to surface those gaps early, before they turn into payout failures, trapped funds, or close exceptions. For related operating detail, see Liquidity Management for Payment Platforms: How to Make sure You Always Have Funds Ready to Pay.

How to use this list and who it is for#

Use this list as a close prompt for teams that need to explain why funds are held, moved, or still pending. It is not a standalone accounting or legal determination. The aim is to help frame questions like, "Who may be owed this amount, why is it still here, and what evidence would support release under our policy?" We recommend using it the same way your team reviews payout readiness at close.

- Classify obligations based on documented evidence and policy, not interface labels alone.

For each item, identify who may be owed the amount, what appears to have changed the status, and which internal record supports that status today.

- Apply it alongside your own accounting policy, legal guidance, and internal rules.

This is an operating aid, not a replacement for formal accounting or legal advice.

- Prioritize traceability over presentation.

A useful check is whether you can follow each balance from opening amount, through period movements, to closing amount, with supporting transaction-level evidence.

- Treat missing close support as a signal to investigate.

If support is incomplete at close, flag it for review; it may indicate a process, control, or reporting gap. Do not treat it as a formatting issue alone.

Top 5 liability buckets you should track separately#

Keep these liabilities in separate buckets. Once you collapse them into one held-funds line, ownership, release triggers, and supporting evidence start to blur, and close quality drops with them.

| Bucket | Use | Key support |

|---|---|---|

| Customer held balances pending release | Customer amounts that are recorded but still pending settlement | Move out only when settlement moves them to available balance |

| Risk and reserve holds | Temporary hold meant to cover anticipated losses, for example disputes, refunds, chargebacks, or reversals | Show why the hold exists, what population it covers, and what releases it |

| Processing and settlement payables | Amounts already initiated through payment rails after EFT initiation but not fully settled | Reconcile initiated payouts to settlement reports, then to final ledger movement |

| Operational payables and fees | Provider fees, vendor charges, and operating obligations in Accounts payable | Tie each AP balance to an invoice, fee statement, contract charge, or accrual support |

| Compliance and tax-related withholdings | Amounts held because tax documentation or withholding conditions are not complete | Track Form W-9 or Form W-8 BEN status; backup withholding may apply at 24 percent |

- Customer held balances pending release

Use this for customer amounts that are recorded but still pending settlement. If funds are pending, they are not yet spendable or payout-ready, and they should move out of this bucket only when settlement moves them to available balance.

Run a daily roll-forward: opening pending, inflows, releases to available, reversals, closing pending. If pending balances go stale, first check for a missing or broken release event.

- Risk and reserve holds

Keep reserves separate from pending customer funds. A reserve is a temporary hold meant to cover anticipated losses, for example disputes, refunds, chargebacks, or reversals, so it is not free operating cash.

Reserve support should show why the hold exists, what population it covers, and what releases it. If those points are unclear, the reserve turns into a blunt control that traps capital and creates close disputes.

- Processing and settlement payables

Use a distinct payable bucket for amounts already initiated through payment rails after Electronic Funds Transfer (EFT) initiation but not fully settled. EFT is broad by definition, which is why this bucket gets complicated in multi-rail flows.

Timing alone justifies the split. ACH processing runs 23 1/4 hours each business day and settles four times daily. FedACH publishes distinct settlement windows such as 1:00 p.m. ET (1300 ET) - current day and 8:30 a.m. ET (0830 ET) - future business day. Reconcile initiated payouts to settlement reports, then to final ledger movement, so "sent" does not get mistaken for "settled."

- Operational payables and fees

Put provider fees, vendor charges, and operating obligations in Accounts payable, not in customer-held or reserve buckets. Accounts payable is a current liability for short-term obligations owed to suppliers or vendors.

Tie each AP balance to an invoice, fee statement, contract charge, or accrual support. A key red flag is netting fees against customer obligations before close, which can distort both liability reporting and margin visibility.

- Compliance and tax-related withholdings

Use this bucket for amounts held because tax documentation or withholding conditions are not complete. Form W-9 provides taxpayer identification data to payers filing information returns, and Form W-8 BEN is provided by foreign beneficial owners when requested by the payer or withholding agent.

If required certification data is missing or incorrect, backup withholding may apply at 24 percent. Keep reporting classification separate too. Certain card and third-party network transactions are reported on Form 1099-K. IRS guidance describes $20,000 and more than 200 transactions and recipient copies by January 31, but filing-year rules can change.

Classify by ownership, release trigger, and supporting evidence, not just by where cash appears to sit. That is what keeps these five buckets useful at close.

For the reporting side of this work, see our guide on What Is RegTech? How Compliance Technology Helps Payment Platforms Automate Regulatory Reporting.

Held funds, reserves, and payables are not interchangeable#

Do not swap these labels at close. If ownership or release conditions are unclear, classify the amount conservatively as a liability until a release event is documented in your accounting records.

- Held funds stay customer obligations until release

Money your platform holds on someone else's behalf stays a customer obligation until the release condition is actually met, even if cash is already in your bank account or payout seems close. Public platform filings show this gross presentation. One disclosed balance was $8.7 billion as of March 31, 2024 for bookings held before check-in.

Ownership and control are central classification tests. Do not automatically treat these amounts as operating cash or as unrelated Accounts payable. Before you book a release, tie it to the exact eligibility-changing event and the related entry in your records, not just an expected settlement state.

Balance sheet reservesneed a clear purpose, trigger, and release rule

A reserve helps only when its hold-and-release logic is explicit. Platform tooling often uses rule-based reserve mechanics, such as withholding part of transaction flows and releasing holds after predefined timing windows.

Trigger quality drives reserve quality. Define what population the reserve covers, what starts the hold, and what releases it. Vague labels like "general risk" are hard to test. Keep provider language in mind as well. Reserve terms are not uniform, and some providers describe reserves as merchant-owned and retrievable.

Accounts payableis for operating obligations, not customer money

Accounts payable is for amounts owed to suppliers of goods and services your entity consumes in operations. It is not a catch-all bucket for customer-held balances awaiting settlement or payout.

The key distinction is who you owe and why. Netting held funds against provider fees without a legally enforceable setoff right and settlement intent can reduce balance sheet clarity. Keep AP support tied to invoices, fee statements, or accruals, and keep held-funds support tied to participant balances plus release status.

- Use

Incurred but not reported (IBNR) reservesonly as an estimation analogy

IBNR is an insurance concept. Here, it works only as an analogy for estimation discipline, not as a direct accounting mapping for payment-platform held funds.

Use the analogy to enforce rigor in exposure definition, review cadence, and evidence. Do not use it as a shortcut label for unclear ownership or release logic. If those remain unclear, classify conservatively as a liability and require a specific release event in your accounting records.

For a step-by-step walkthrough, see Goodwill and Intangible Assets on a Balance Sheet for Payment Risk.

The order of operations that keeps books and payouts aligned#

Sequencing is the control. Do not run payouts ahead of the ledger state that proves an amount is releasable. The cleanest close usually comes from a simple rule: post, classify, verify, release, then reconcile.

- Inflow: post journals first, then absorb async status updates

Post ledger journals from a durable payment reference at confirmation time, even when full status arrives later by webhooks. Webhook events are asynchronous, can be stale at processing time, and can be replayed for up to three days if undelivered. Handlers should be duplicate-safe, and books should tolerate timing gaps. If a status update could change liability treatment, fetch current state before reclassifying.

- Hold: classify by ownership, purpose, and payout eligibility

Classify funds into held balances versus balance sheet reserves based on who the funds belong to, why they are restricted, and whether payout conditions are met. A reserve is a temporary hold for potential losses. That is different from customer obligations still awaiting release. Keep reserve logic explicit: covered population, trigger, and release event.

- Eligibility: clear verification and

AMLcontrols before release

If verification is pending or failed, keep the liability held and visible. Funds become payout-usable after settlement into available balance, and payout capability can be disabled when required information is missing. Treat verification deadlines as real operational gates. Some programs use grace periods such as 14 days. Beneficial-owner requirements can vary by institution in 2026.

- Release: execute

payout batcheswith idempotent controls

Use idempotent payout requests so retries do not create duplicate disbursements. A payout instruction is not always proof of settlement, so close the liability only on terminal success. Monitor statuses like processing, failed, returned, and canceled. If a payout fails or is returned, re-open the liability state immediately. Retries are not always automatic.

- Close: reconcile cash, liabilities, and status events together

Close quality depends on matching three views at once: cash movement, liability movement, and operational event history. Use payout reconciliation reporting to tie each payout batch to included transactions, and use balance-transaction records as the movement trail. As an internal control, keep timing breaks visible as tracked exceptions with a named owner and SLA in your close process. If your team cannot show all three views together, your reviewer should treat the batch as not ready.

The evidence pack you should demand at month-end#

If your month-end file cannot show what you owe, why amounts are still blocked, and which breaks are still unresolved, the close is not payout-ready. Keep the pack tight. You need evidence for liability movement, operational exceptions, compliance gates, and tax status, and you need it in records someone else can test.

| Evidence item | What it should show | Checkpoint |

|---|---|---|

| Liability roll-forward by bucket | Opening balance, period movements, and closing balance, tied to ledger journals | Sample any closing line and trace it to journals that created, reclassified, released, or re-opened the amount |

| Exception log that keeps contradictory evidence visible | Unresolved posting breaks and webhook exceptions, including duplicate deliveries and undelivered or late events | Include root-cause tag, owner, opened date, and target remediation date |

| Compliance gating report with release decisions | Which items stayed blocked by KYC or AML status, who approved any release, and what evidence supported that release | Every held amount here should tie to the same held amount in the liability roll-forward |

| Tax and documentation artifacts where your program requires them | Status for W-9, W-8 including W-8BEN, and relevant Form 1099 or Form 1099-K indicators | Preserve evidence that supports recipient status ahead of the January 31 furnishing date |

- Liability roll-forward by bucket

Use a roll-forward for each liability bucket you manage, with opening balance, period movements, and closing balance, tied to ledger journals. This opening, movement, closing pattern is a recognized reconciliation structure and gives a clearer test trail than reporting only an ending total. Checkpoint: sample any closing line and trace it to journals that created, reclassified, released, or re-opened the amount. If ownership or release status is disputed, keep it visible as a liability instead of netting it away.

- Exception log that keeps contradictory evidence visible

Track unresolved posting breaks and webhook exceptions, including duplicate deliveries and undelivered or late events. Include root-cause tag, owner, opened date, and target remediation date. This is evidence quality, not admin overhead. Unresolved exceptions belong in close documentation, including items that contradict your asserted state. Webhook retries can continue for up to three days, so the log should show both the operational event and the accounting impact, with an explicit treatment decision when close ends before retries do.

- Compliance gating report with release decisions

Show which items stayed blocked by KYC or AML status, who approved any release during the period, and what evidence supported that release. For banks under 31 CFR 1020.220, specified customer identifying information is required before account opening. Related records are retained for five years after account closure. Regardless of model, blocked or pending items should remain in the evidence pack. Checkpoint: every held amount here should tie to the same held amount in the liability roll-forward. If monitoring flags suspicious activity or incomplete customer data under your policy, document the decision to keep funds held or release them.

- Tax and documentation artifacts where your program requires them

Where payout holds depend on tax setup, retain status for W-9, W-8 including W-8BEN, and relevant Form 1099 or Form 1099-K indicators. W-9 supports correct TIN collection for information returns, and W-8BEN supports foreign-status documentation for eligible individuals. If your U.S. flow includes 1099-K, preserve evidence that supports recipient status ahead of the January 31 furnishing date. Do not rely only on threshold logic. IRS guidance notes a recipient may still receive Form 1099-K below the familiar $20,000 and more than 200 transactions statement.

Decision rules for reserve sizing without freezing growth#

Reserve changes should be narrow, driven by evidence, and reversible, not portfolio-wide reactions. Broad, vague changes can trap capital without clearly improving risk coverage.

- Raise reserves only where volatility is rising

Increase protection only for the specific corridor, partner, or flow where you are seeing more failed refunds, returns, claims, or disputes. Keep this case by case, because reserve decisions are not one-size-fits-all. For Visa card lanes, track the VAMP ratio (fraud plus disputes over settled transactions) and account for program-threshold updates effective 1 June 2025. Your approval trigger should be tied-out evidence by lane, not a general risk narrative.

- If utilization stays low, narrow scope before releasing capital

Consistently low reserve use is a signal to tighten scope first, not remove coverage everywhere. Compare reserve usage to the actual loss window in the affected flow. Some programs use 30-90 days to allow refunds and chargebacks to be processed. In practice, a rolling or fixed reserve tied to one risky segment can be more controlled than lifting protection across the full book.

- Keep routine payables separate from uncertain held obligations

Use reserve logic for uncertain exposures, and track routine payables separately under your accounting policy. Keep unresolved failed refunds, disputed deposits, or unresolved negative balances visible as held obligations until they are resolved. This matters operationally. Some reserve programs apply aging rules to unresolved negative balances and may auto-clear aged balances after 180 days, which is a different pattern from routine payables.

- Approve reserve changes with rail-specific evidence, not intuition

Require a short pack with failed refunds, return rates, aged exceptions, and the exact corridor or partner affected. For ACH or debit lanes, keep thresholds in-lane: 0.5% unauthorized, 3.0% administrative, and 15.0% overall return-rate inquiry levels. Do not apply those thresholds to card programs. Define the reserve type, target or threshold, start date, and release condition up front, and avoid broad unspecified contingency buffers.

Failure patterns that make liabilities look right but behave wrong#

Once reserve logic is stable, the next problem is state drift. Liabilities can look right at close and still be wrong for release because event, compliance, or settlement state is out of sync.

- Missed or misordered webhooks

Liabilities can be understated when teams treat webhook delivery as single-path and in order. Stripe documents duplicate and out-of-order events, and retries undelivered events for up to 3 days. A missed status-change event can leave ledger journals showing funds as available when they are still pending.

Approve release only when the event ID and journal entry match for that payout or hold transition. Late or missing de-duplication can create duplicate postings or hide a missing status update until after funds are sent.

- Stale compliance status that keeps a hold alive after the user is ready

Liabilities can be overstated when compliance status and payout capability drift apart. Even after some verification is complete, payout capability can remain restricted while requirements.currently_due is not empty, leaving funds in a held state.

Use provider capability state as the control point, not a UI badge or manual note. If review is marked complete, confirm payout-relevant status in the provider record before moving the liability bucket.

- Provider settlement lag mixed into customer-held balances

Settlement timing needs its own visibility. Funds can be pending and not payout-usable, and provider settlement is batch-based, so provider timing, bank movement, and customer liability are related but not the same state.

Keep separate views for customer-held balances, provider settlement timing, and reserve holds. If cash is still pending or the provider batch has not closed, treat it as not payout-ready, and make that explicit in journals.

- Old reconciliation breaks treated as "timing" forever

A break that survives your close window should be handled as a controlled incident, not routine timing noise. Reconciliation standards require differences to be investigated, resolved, and documented, and Regulation E's 10 business days is a useful seriousness benchmark for prompt error determination after notice.

Enforce aging discipline. If an exception is older than close and still blocks a clean tie between cash, status events, and ledger journals, treat release readiness as unproven until it is resolved and checked again. We recommend giving your team one rule here: aging breaks do not become acceptable just because the queue is busy.

Product and engineering choices that cut reconciliation pain#

The fastest way to reduce recurring reconciliation breaks is to make a few product decisions explicit in the system design. Good accounting support usually starts as a product and engineering choice, not a month-end rescue.

- Idempotent webhook handling

Treat every webhook as replayable from day one. Webhook delivery can duplicate, and event-driven payment flows are asynchronous, so each provider event_id should produce at most one ledger journal effect. If your app writes payout-related objects through an API, use idempotency keys on those write calls so retries do not execute twice.

The practical checkpoint is traceability: event_id, provider object ID, posting timestamp, and journal entry ID should all tie. If one is missing, treat the retry path as unsafe until reconciled.

- Explicit liability states in APIs and UI

Keep liability and payout states explicit so ops does not have to infer meaning from a generic "ready" label. Many providers separate not-yet-settled funds from spendable funds, and in Connect setups balances can move from pending to available on a 2-day rolling basis.

This matters for Virtual Accounts and payout batches. If state labels blur settlement timing and customer obligations, close breaks become manual. In manual payout flows, your platform also needs its own reconciliation logic because the provider may not identify which transactions are in each payout.

- Derived balances separate from the ledger of record

Show derived balance views for speed, but keep the ledger as the source of truth. A ledger account can carry liability balances, and the same underlying ledger entries can support pending, posted, and available views.

This separation makes timing differences explainable. If a displayed balance cannot be traced back to specific ledger entries, it is not reliable close evidence.

- Explicit ownership definitions for

Merchant of Record (MoR)flows

In Merchant of Record (MoR) models, do not leave who is treated as the seller implied. Define the event boundaries your business uses, then stamp each movement with ownership state and counterparty at that boundary.

That record should make handoffs auditable: event type, prior owner, new owner, amount, and linked journal entry. If payout activity and recorded ownership state diverge, treat it as a reconciliation risk to resolve.

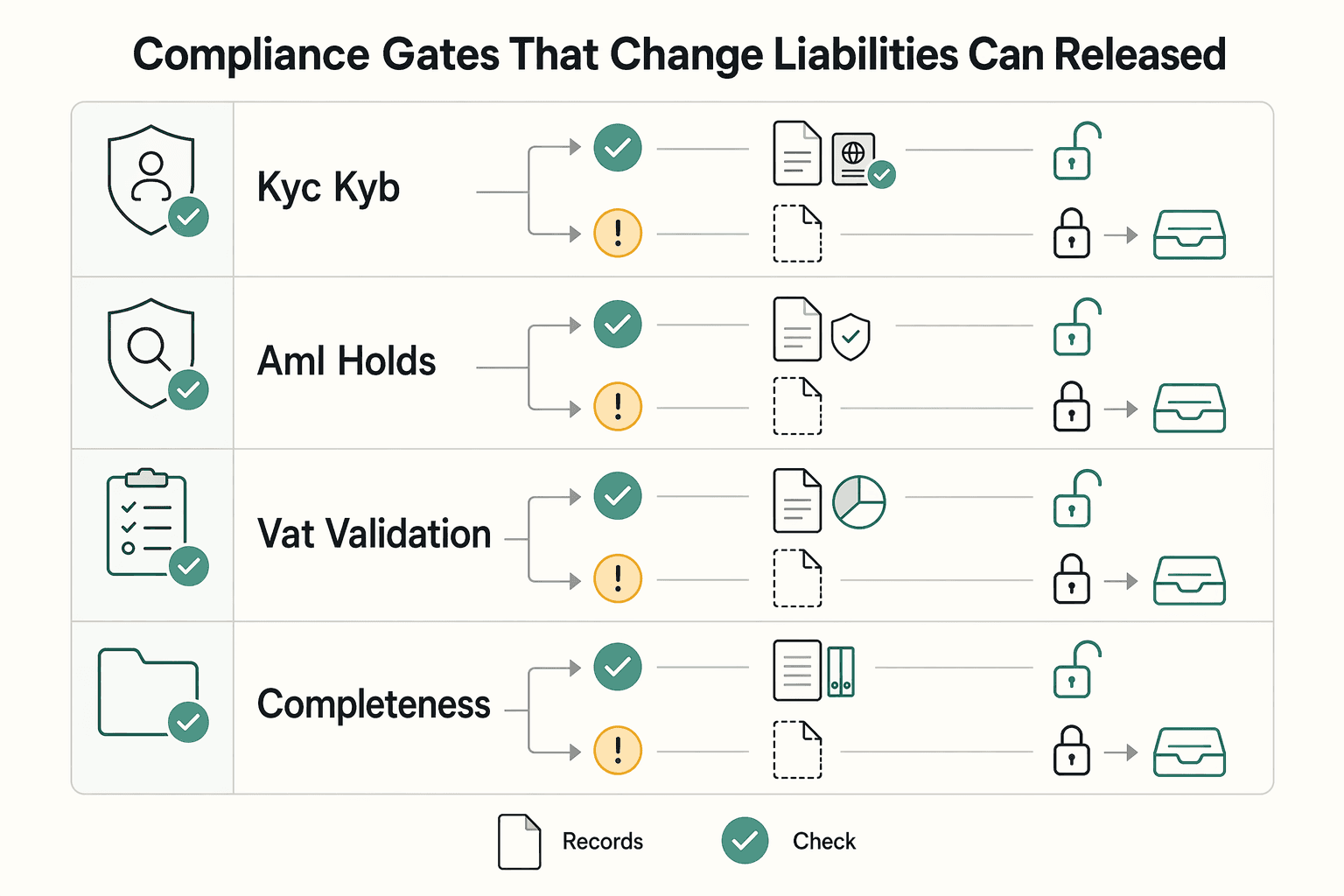

Compliance gates that change when liabilities can be released#

Liabilities should be released only when compliance gates are explicitly cleared, not just when cash is received. Treat KYC, KYB, AML, VAT, and tax-document status as payout gates with evidence. If status is pending or unknown at payout time, keep funds on hold and route them to an exception queue with clear ownership.

| Gate | Release impact | Record to keep |

|---|---|---|

| KYC and KYB outcomes | Verification status can directly gate payout capability; failed verification keeps payouts disabled | Current verification status, decision timestamp, and approved payout account |

| AML holds with a real path forward | Need a defined release, escalation, or cancellation path; in-flight payouts can remain pending for up to 10 days | Hold reason, open time, current owner, and requested remediation evidence |

| VAT validation where your program requires it | Use VAT validation as a gate when VAT registration is a payout prerequisite; VIES returns valid or invalid | VAT number, country code, VIES result, and lookup timestamp |

| W-8 and W-9 completeness | Missing after configured processing volume can block payouts; missing or incorrect TIN details can trigger backup withholding; certain foreign-payee payments can be 30% | Separate missing, received, and validated-for-payout states |

- KYC and KYB outcomes

Verification status can directly gate payout capability, so funded does not mean payout-eligible. Stripe requires connected accounts to satisfy KYC requirements before they can accept payments and send payouts, and KYB checks are part of business onboarding. Adyen similarly requires verification before payouts, and failed verification keeps payouts disabled.

Funds can sit in balance accounts until they are paid out, so keep the liability visible and blocked until release criteria are met. At minimum, record current verification status, decision timestamp, and approved payout account on the release decision.

- AML holds with a real path forward

AML holds need a defined release, escalation, or cancellation path, not a queue that just stays open. Firms may request information for AML checks, and regulated governance includes named escalation responsibility, for example MLRO accountability. Stripe also supports pausing payouts, both manual and automatic, and in-flight payouts can remain pending for up to 10 days.

Track hold reason, open time, current owner, and requested remediation evidence. Work the queue with explicit checkpoints so held liabilities remain explainable at close.

- VAT validation where your program requires it

When your program makes VAT registration a payout prerequisite, use VAT validation as a gate with stored evidence. VIES returns a binary outcome, valid or invalid, which makes it suitable for a clear pass or fail control in those programs.

Store VAT number, country code, VIES result, and lookup timestamp with the payout decision. Avoid manual-only "VAT checked" notes that cannot support later audit or reconciliation.

- W-8 and W-9 completeness

Tax-document completeness can be a payout gate when your platform policy enforces it. The IRS describes W-9 for taxpayer identification details and W-8 BEN for foreign beneficial-owner documentation when requested. Stripe supports threshold-based enforcement, including blocking payouts if required W-8/W-9 is missing after configured processing volume.

Separate missing, received, and validated-for-payout states. Missing or incorrect TIN details can trigger backup withholding on reportable payments. For certain foreign-payee payments, withholding can be 30%. Stripe also notes potential IRS penalties up to 310 USD per incorrect 1099 submission.

When compliance status is unknown at payout time, do not force release just to clear the operations backlog. Keep the amount on hold, keep it out of payout-ready totals, and route it through exception handling. For cross-border flows, see International EFT Payments: How Platforms Can Send Electronic Funds Transfers Across Borders.

A close checklist before you approve payout batches#

Approve a payout batch only when these four controls are all clear. If one is still open, the batch is not ready.

- Batch total tied to reconciliation records

Tie the bank-facing payout amount back to the settlement batch and underlying transactions. Use reconciliation outputs to prove the batch total matches settled transactions, not a dashboard balance or export estimate.

- Unresolved

webhooksand unmatcheddepositsexplicitly cleared

Treat asynchronous breaks as open risk until they are resolved or explicitly signed off. Because IPN or webhook delivery can be delayed or retried, close only when open webhook and deposit exceptions are within your internal tolerance or documented in an exception log with an approver, owner, and follow-up date.

KYCand other compliance-blocked funds excluded from payout-ready totals

Keep blocked amounts out of payout-ready calculations until verification and compliance gates are cleared. Keep those funds visible in hold or exception reporting until they are cleared.

- Tax forms and reporting flags checked before release

For payouts with tax gating, verify W-9 or W-8 BEN status in the same record used for payout authorization. If required TIN or form status is missing where backup withholding applies, handle it before release. Do not rely on stale Form 1099-K threshold logic when IRS references conflict.

For implementation detail, see Microsoft Dynamics 365 for Payment Platforms: Finance Module Setup and Payout Integration Guide. Then turn this checklist into an operating runbook by mapping each control to implementation details in the Gruv docs.

Conclusion#

Keep one operating rule: release logic must be stricter than cash visibility. A liability is a present obligation, and under IFRS 9 it is removed only when that obligation is extinguished, discharged, cancelled, or expired. In practice, that means classify first, then release only with evidence in records, reconciliations, webhook handling, and close controls. We recommend treating that as your default release rule, not an exception policy.

- Classify by who is owed and what ends the obligation

Separate customer held funds and operational payables into distinct liability buckets with their own release condition and reconciliation path.

This is operating and reporting discipline, not a formatting preference. IAS 1 supports separate liability classifications. Public filings show the difference in practice: one major payment-company 10-Q reports "Accounts payable" separately from "Funds payable and amounts due to customers," with 133 and 139 versus 41,727 and 41,935.

- Treat evidence as stronger than status

Webhooks support operations, but they are not enough to justify release on their own. Stripe documents asynchronous events and automatic retries of undelivered events for up to three days, so payout readiness should be proven in your books, not inferred from one event feed. If your team sees one clean webhook and no reconciliation support, we would rather hold the batch.

Tie each payout batch total to approved liability-release entries. Keep unresolved webhook items cleared or explicitly signed off in the exception log. Use idempotent payout-creation controls and handle retries with your provider's key-retention window in mind, for example keys retained for at least 24 hours.

- Keep customer-funds obligations separate until they are truly gone

In UK payment or e-money contexts, safeguarding under the Payment Services Regulations 2017 and Electronic Money Regulations 2011 protects customer funds received for payment services or e-money. Treat money held for users as distinct from operating cash and ordinary trade payables until the obligation is actually extinguished.

Your month-end checkpoint should show the liability position, supporting entries, and evidence that the contractual obligation ended. If the obligation still exists, keep the amount classified as held. Your reviewer should be able to see that decision without asking your team for a second explanation.

No liability is payout-ready without evidence, ownership, and a verified release event. If settlement, event confirmation, or another release condition is still unresolved, keep it visible as held. We would rather keep your exception visible than let your team explain an avoidable release error later.

Related reading: SOC 2 for Payment Platforms: What Your Enterprise Clients Will Ask For. If you are refining release governance and disbursement execution, review how Gruv Payouts supports compliance-gated payout operations.

Frequently Asked Questions

Are held funds assets or liabilities for a payment platform, and when does that status change?

Held funds can map to both sides of the balance sheet. Cash may be recorded as an asset, while the obligation to the customer may be treated as a liability until release conditions are met. In at least one SEC payment-company disclosure, those customer obligations are presented within current liabilities as funds payable and amounts due to customers. Operationally, many teams treat status as changed only when a release event is supported in ledger journals, not just when a dashboard shows money received.

What is the practical difference between held funds and `balance sheet reserves` in day-to-day operations?

Held funds are owed amounts that are not yet release-ready because settlement, compliance, or payout timing is still open. Reserve balances are narrower: funds cannot be paid out or transferred until the reserve hold period ends, and the hold is used for expected dispute or refund loss coverage. Keeping these separate avoids confusion in aging, release logic, and exception ownership.

Why can over-reserving hurt payout performance even when it looks conservative?

Over-reserving reduces what is actually available to pay out. Payout execution depends on available balance, not total inflow recorded in the ledger. That can slow batch execution even when reported balances look strong.

What minimum controls prove liabilities are actually payout-ready, not just reported as such?

Use controls that tie payout readiness to evidence, not labels: batch totals tied to approved liability-release journals, unresolved webhooks cleared or formally signed off, and CIP/AML-related holds excluded from payout-ready totals. Apply idempotency on payout creation so retries do not create duplicate financial operations. If you cannot produce sufficient appropriate evidence for release, keep the amount classified as held.

How should teams classify amounts when `webhooks` are delayed or settlement is still pending?

Classify them as held or pending, not payout-ready. Webhook updates are asynchronous and failed deliveries are retried, so timing gaps are expected; pending funds become available at available_on timing, with one Connect example using a 2-day rolling basis that varies by country and account. If settlement state or webhook confirmation is unresolved, keep the amount in the liability roll-forward and in the exception log with an owner and follow-up date.

Which checks should run before releasing funds in cross-border payouts with `KYC` and `AML` gates?

Before release, confirm risk-based customer identity verification procedures are complete under your CIP program. For legal entities, apply your current beneficial-owner requirements and avoid assuming repeat verification is always required in every case after the Feb. 13, 2026 exceptive-relief change in scope. Also run sanctions controls that support OFAC reporting obligations for rejected transactions, and confirm tax-status handling, including backup withholding at 24 percent where required.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- federalreserve.gov/paymentsystems/fedach_about.htmtrusted

- irs.gov/forms-pubs/about-form-w-9trusted

- irs.gov/businesses/understanding-your-form-1099-ktrusted

- ncua.gov/newsroom/press-release/2026/fincen-issues-ex...trusted

- occ.treas.gov/topics/supervision-and-examination/bsa/index...trusted

- sec.gov/about/reports-publications/investorpubsbegfi...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: