Quick Answer

Start with a written termination trigger and place payout on hold until three proofs exist: access removal, contract-level payment terms, and a reconciled rail outcome. Treat missing tax records as a hard stop, because backup withholding can apply at 24% when IRS conditions are met. For mixed jurisdictions, route timing conflicts to legal review instead of forcing auto-release, then record who approved release, hold, or stop with timestamps.

Final Payment Controls During Contractor Offboarding#

Contractor offboarding is a compliance and money movement risk event, not an admin cleanup task. If you treat a departure like a simple HR ticket, contract status, access rights, tax reporting, and payout controls can all fail at once.

That risk grows when a single payout stack spans multiple markets. In the US, digital platform operators are expected to classify workers correctly and meet information reporting, tax withholding, filing, and depositing requirements. Form 1099-NEC may also be required for independent contractor payments. In the EU, DAC7 has imposed reporting obligations on platform operators since 1 January 2023, with the first exchange for calendar year 2023 at the end of February 2024. An exit decision can therefore change what you must report, retain, and prove later.

Payment timing is also jurisdiction-sensitive. US federal law does not require immediate final payment in every case, while states may require faster timing. Singapore shows a stricter employer-termination baseline: final salary on the last day of employment, or within 3 working days if same-day payment is not possible. These are not universal contractor rules, so your controls should follow the actual contract and jurisdiction, not a generic "offboarded" status.

Data and access controls belong in the same flow. Offboarding includes removing access to systems and data, and CISA guidance calls for immediate removal when access is no longer required. Where personal data processing is outsourced, UK GDPR accountability requires a written controller-processor contract, including end-of-contract return or deletion terms and audit or inspection rights. If payment release does not wait for those checks, you can release funds before closeout is complete.

This article stays focused on practical controls. It covers:

- a decision-oriented comparison of platform patterns for termination notification, final payment status, and payment cessation per contract

- a pre-release payment sequence so ops, finance, legal, and risk act in the right order

- a minimum evidence checklist for audit-trail readiness when a payout is held, released, or stopped

Prioritize proof over speed. You should be able to show who changed final payment status, who approved the decision, and what evidence supported release or hold, with records retained so they can be produced for review. For US employment-tax records, the IRS says to keep records for at least four years after filing the fourth quarter for the year. Even where that exact rule does not govern your contractor model, the same evidence discipline still matters.

Market rules vary, so this guide stays concrete where obligations are clear. Where contract terms, local payout timing, classification questions, or cross-border reporting duties conflict, the right next step is specialist legal or tax review.

Related reading: IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments.

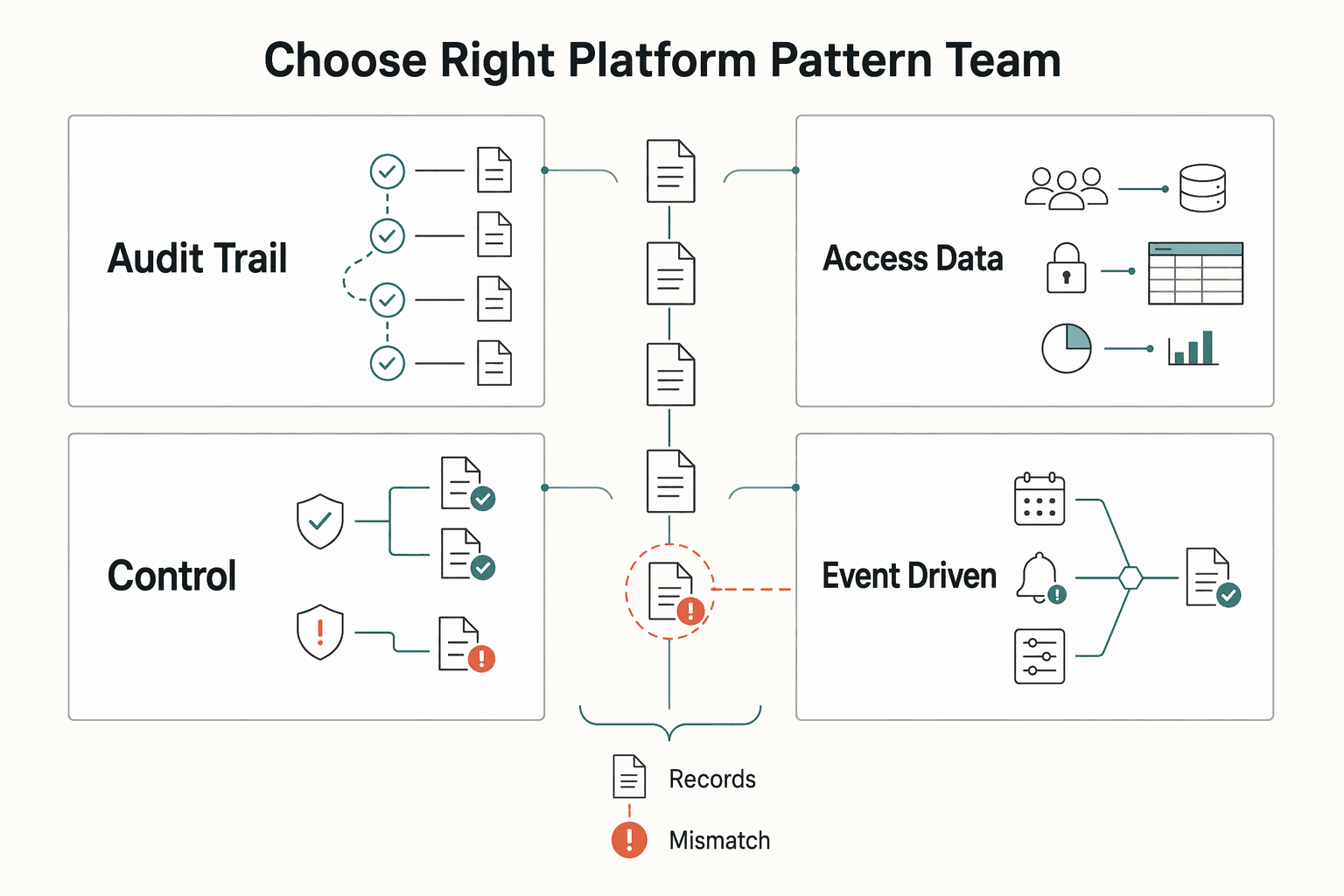

How to choose the right platform pattern for your team#

Start with one question: can the platform stop payment when evidence is incomplete, then prove the decision with exportable records? If compliance, legal, finance, and risk all share ownership, checklist UX matters less than whether you can show a defensible sequence from termination notice to final payment status to payout outcome.

| Criterion | What to prefer | Grounding |

|---|---|---|

| Audit trail depth | Status changes, review steps, and supporting records | Termination notifications, documented review or activation flow, and a full documentation and audit trail |

| Access and data closeout | Closeout evidence instead of ticket comments | Explicit attestations for data privacy and destruction requirements so the evidence is reviewable later |

| Final payment controls | Exportable history of status changes and payment cessation per contract | Post-decision reconciliation evidence such as payout reconciliation exports and bank-linked reconciliation status |

| Event-driven operations | Webhooks and idempotent requests where available | Webhooks are designed for high volumes of business-critical events; idempotency keys can be up to 255 characters and systems may prune stored keys after at least 24 hours |

Use these criteria in this order.

- Audit trail depth

Prefer platforms that show status changes, review steps, and supporting records. A stronger offboarding pattern includes termination notifications, a documented review or activation flow, and a full documentation and audit trail.

- Access and data closeout evidence

Make payment release depend on closeout evidence, not ticket comments. Prioritize explicit attestations for data privacy and destruction requirements so the evidence is reviewable later.

- Final payment status and payment cessation controls

Rule out options that cannot prove final payment status changes and payment cessation per contract with exportable history. Also require post-decision reconciliation evidence, for example payout reconciliation exports and bank-linked reconciliation status, so you can verify the operational result, not just the approval event.

- Event-driven operations and safe retries

If your process still depends heavily on manual tickets, prefer event-driven workflows and webhooks where available. Webhooks are designed for high volumes of business-critical events, and idempotent requests support safe retries without repeating the same operation. Idempotency keys can be up to 255 characters, and systems may prune stored keys after at least 24 hours. Still require payout and bank reconciliation, because idempotency alone does not prove downstream systems stayed aligned.

A practical filter is to ask each vendor to show you one complete offboarding record with termination details, review status, required notifications, final payment status, and reconciliation exports. If they cannot show that evidence clearly end to end, treat it as a disqualifier. For providers with mixed published signals on offboarding depth, verify capability directly before selection.

For a deeper dive, see Construction and Trades Platform Payments: How to Pay Subcontractors with Lien Waiver Compliance.

Quick comparison of platform options for offboarding and final payment compliance#

For mixed-market, higher-exposure offboarding, choose the pattern that gives you the strongest evidence and approval chain, not just the fastest setup.

| Option | Best for | Control depth | Evidence quality | Operational burden | Escalation support | Pros | Cons / Unknowns |

|---|---|---|---|---|---|---|---|

| Aravo-style TPRM systems | Teams that need lifecycle governance through termination | High for documented offboarding controls (termination notification routing, attestations, payment finalization or cessation tied to contract) | Strong in the reviewed materials for audit-trail-oriented offboarding controls | Can be higher due to setup and process ownership | Strong where review or activation and documentation are part of flow | Clear audit trail, explicit privacy or destruction attestations, contract-linked payment cessation language | May require a heavier cross-functional operating model |

| Employment suites (for example, Deel) | Teams managing mixed worker types and market-specific offboarding steps | Medium to high, but flow depends on employment type and local context | Moderate in the reviewed materials (clear variation by employment type; local date adjustments may be required) | Medium | Present when local adjustment is required | Handles variation and local compliance adjustments in process | No evidence here of one uniform offboarding path across all contexts |

| Payout tool sets (Slash / Remofirst / Remote) | Teams optimizing payout operations and payment-status handling | Variable by provider; strongest published signals here are around approvals, payout status, and dashboard visibility | Mixed: strong for specific features, thin for end-to-end offboarding evidence chains | Variable based on enabled controls | Variable, often operational rather than full governance escalation | Slash: configurable approval counts. Remofirst: payout status visibility and payment-cycle controls. Remote: structured PEO flow with final-pay handling and offboarding dashboard visibility | Unknowns remain for unified evidence chains (request -> approval -> payment cessation -> exportable outcome), and for consistent contractor coverage across all jurisdictions in these materials |

| Hybrid stack (Gruv + internal controls) | Teams that want payout infrastructure plus custom policy gates and internal governance | Potentially high if you implement internal termination, approval, and attestation controls on top of payout rails | Gruv capability evidence is from product context here, so validate in your environment | Medium to high (integration + internal control design) | Can be strong if internal legal or compliance escalation rules are explicit | API and webhook-driven operations, compliance-gated payouts, idempotent retries, audit trail, reconciliation-oriented model | You must design and enforce your own offboarding governance layers. |

If legal exposure is high and markets are mixed, prioritize evidence quality and approval controls over faster setup.

For more detail, see Build a Contractor Payment Flow for Home Services Marketplaces.

Option 1 unified payouts and compliance controls in one operating stack#

This is a strong option when you need offboarding decisions and money movement to stay tightly aligned. A unified stack works best when you can hold funds, verify offboarding status, and export a time-sequenced record of what changed and when.

The key benefit is not automatic compliance. The real benefit is control proximity. Payout holds, request logs, and reconciliation outputs can sit close enough to the payout event to reduce the risk that final payment status drifts from the offboarding decision. It does not remove jurisdiction-specific final-pay obligations, which can differ between federal baseline rules and stricter state requirements.

What makes this option worth choosing#

Choose this option when policy-gated payouts are a hard requirement. If you can hold funds in the same environment where payout execution occurs, you reduce the chance of paying while legal or security still has open offboarding actions.

Evidence quality improves when the same stack provides reconciliation and request-level logs. From one record set, or from a clearly linked internal approval record, you should be able to answer:

- What was the contractor's final payment status at each step?

- Which release, hold, or stop decision state changed, and when?

- Did the provider outcome match the recorded internal decision?

If you cannot export those records in order, the "one stack" model is mostly cosmetic.

Where teams still get this wrong#

A common failure is weak termination initiation, not weak payout rails. If the trigger is an unstructured email, Slack message, or spreadsheet edit, the platform can still execute an incomplete or incorrect instruction.

A second failure point is retry handling. Offboarding flows are often asynchronous, and payout calls get retried when responses are delayed or unclear. Without idempotent payout actions, retries can create duplicate disbursements or hold-state mistakes.

The operator rule that matters most#

Tie account and access controls to termination events before payout release. If access disablement is a prerequisite, require logged confirmation on the same offboarding record before funds move.

For a marketplace offboarding a contractor, use a defensible sequence:

- A formal termination notification enters the platform and places payout on hold.

- Security or operations confirms access removal and logs completion.

- Finance or legal checks contract terms for cessation, offsets, or remaining amounts due, including any jurisdiction-specific final-pay timing rules.

- An authorized reviewer records the decision to release, continue hold, or stop, with rationale and timestamp.

- Payout executes, and reconciliation confirms the provider outcome.

Used with disciplined initiation and retry controls, this pattern is a credible choice for final-payment control. Used casually, it concentrates failure in one place.

For a step-by-step walkthrough, see What Is RegTech? How Compliance Technology Helps Payment Platforms Automate Regulatory Reporting.

Option 2 TPRM-first systems for vendor termination governance#

A TPRM-first model is often a defensible choice when third-party exits require cross-functional signoff. Its core strength is governance evidence: why the relationship ended, who reviewed it, and which obligations were closed before completion.

It fits best for enterprises that already run a formal TPRM program. In U.S. federal banking guidance issued June 06, 2023, termination is explicitly part of the third-party lifecycle alongside planning, due diligence, contracting, and ongoing monitoring. That guidance is sector-specific, but the operational takeaway travels well. Treat termination as a governed stage, not a post-invoice cleanup step.

Where this option earns its keep#

TPRM-first systems are strong for vendor termination and end-of-contract evaluation. They are built to manage post-contract exposure, route reviews, and keep review chains visible across teams.

What matters most is the evidence attached to each approval. Your termination record should require, at minimum, contract context, confirmation of vendor access and credential removal, final payment terms to confirm, and named reviewers with a clear review trail. If those details sit in email or meeting notes, the governance control is weaker than it looks.

What to verify before you trust it#

This model is only sufficient when the governance decision can be tied to the payment outcome. TPRM tools are built for lifecycle governance, so do not assume they natively execute payout holds, stops, or ledger postings.

Run one real trace before rollout:

- Start from a completed termination approval.

- Confirm the same case ID, or equivalent, appears in finance or payments handling.

- Confirm reconciliation shows the provider outcome or ledger event that matches the decision.

If you cannot complete that trace, you have governance evidence but not final-payment control evidence. If risk can approve termination while finance can still pay from an unlinked queue, TPRM alone is not sufficient.

Limits and failure modes#

A common failure is handoff fragmentation across teams, including HR, legal, and IT. When each team closes its own ticket without a linked final-payment state check, the process can look complete while payment risk stays open.

Accountability is the second failure mode. Third-party use does not transfer responsibility for the compliance outcome, even when every reviewer signs off. For payment-processing relationships, termination governance should be linked to payment operations. Otherwise, the record shows that a decision was made, but not whether payment execution matched it.

For regulated or regulator-influenced teams, termination-rights detail deserves extra legal review when a vendor supports critical operations. Used well, this is a credible component. Used alone, it often proves approval discipline, not payment control.

For the full breakdown, see How to Build a Contractor Payment System for a Nursing or Allied Health Staffing Agency.

Option 3 contractor suites with built-in offboarding guidance#

Contractor suites can be a practical adoption path when you need prescriptive offboarding steps without building the process from scratch. A suite such as Deel can simplify handoffs by packaging termination and offboarding into a defined workflow.

The main benefit is the built-in flow. Deel supports immediate or future-dated contractor end dates, and offboarding can start from either an automatic contract-end trigger or a manual termination. It also makes escalation boundaries explicit. It tells teams to check with Payroll or Legal when the last working day is unclear, and it notes that requested end dates may be adjusted after local-law review.

The limit is final-payment control depth. Do not assume a suite can make every jurisdiction-specific final-payment decision on its own. In the U.S., federal law does not require immediate final payment in every case, and some states may require faster timing, so internal legal or payroll review should still govern exceptions.

What to verify before rollout#

Before rollout, test whether the built-in flow gives you evidence you can actually defend later. Focus on the record, not the interface.

- Trace one real offboarding case end to end, and confirm it was triggered the way you expect, whether by automatic contract end or manual termination.

- Export the offboarding record (CSV, PDF, or Excel) and verify it works as evidence without relying on extra UI screenshots.

- Confirm exception outcomes are preserved outside the UI, including legal date changes.

- Validate that disputed worker status is escalated to internal review using control-and-independence evidence, not contract labels alone.

Option 4 lightweight payment tools with manual legal and compliance overlays#

This pattern works when you intentionally choose simple payment operations and add manual controls to make exits defensible. For smaller teams, it can work if you can prove payment cessation per contract, preserve termination notification records, and assign clear approval ownership.

Best for#

Use this when offboarding volume is low enough for human review. It fits early-stage teams with payment-focused operations where payout handling is the immediate need, not a full lifecycle suite. Some tools focus mainly on contractor payments, while others cover broader compliance workflows, so a lighter tool choice means you must supply the missing controls yourself.

A practical use case is a platform operating in a few markets with a named ops owner and a written escalation rule for legal or tax uncertainty. In that setup, a standardized checklist is a real control because it centralizes who did what and when.

Why teams choose it#

Teams choose this for operational simplicity. It can be simpler to roll out than a heavier model and can reduce dependence on paper checks or spreadsheet tracking, which are associated with delays and data-entry errors.

It also preserves flexibility. You can manually enforce stop-work instructions, stop new payment initiation, and collect final invoice documentation while a stronger control layer is still being built.

Where it breaks#

The weak point is evidence quality. An audit trail must be chronological and strong enough to reconstruct what happened, including the trigger, termination notification, payment hold or release decision, approver, payout outcome, and exception notes.

Termination handling is where gaps can appear first. A stronger provider-led pattern can include an immediate Stop Work Order, a 21 calendar day window to submit a final invoice, and continued access to historical records and invoices after termination. If your setup does not provide this structure, you need to recreate it manually and retain records outside the provider UI.

Non-negotiable overlays#

The tool alone is not the control here. What makes this pattern work is a short overlay with named owners and retained records.

- Cross functional ownership: define who handles legal or HR steps, who verifies contract terms, and who removes access with IT or OT where relevant.

- Checklist with timestamps: record each task, who completed it, and when. Include termination notification sent, access removed, final invoice received or outstanding, and payment hold or release decision.

- Jurisdiction first review: route unclear country-specific exits to legal before final release, since local legislation can take precedence over company policy.

- Evidence pack outside the tool: retain notice records, contract end terms, invoice or release documents, approval records, and provider outcomes showing stop, hold, or release.

Before rollout, run one real offboarding case end to end and export the evidence file. If you cannot show notification date, approver, invoice status, and hold rationale, this pattern is too light for your risk profile. A specific U.S. federal example shows the logic. GSAM 532.905-70 (effective 01/15/2026) ties final payment to required contract documentation and requires higher-level approval if documentation is missing and no response is received within 60 calendar days. That rule is not universal, but the documentation-and-escalation pattern is still useful.

Final payment release checks in the exact order operations should run#

Run final payment as a gated sequence, not a cleanup task. Treat this as an internal control sequence because legal requirements can vary by jurisdiction. If a required artifact is missing, set the case to hold, route it to legal or risk, and wait for written evidence. Do not release on verbal confirmation alone.

| Stage | What to verify now | Hold if this is missing or unclear | Evidence to retain |

|---|---|---|---|

| Trigger received | Capture the offboarding trigger in a durable written record (termination or contract-end notice, internal ticket, timestamp, named owner). The instruction must be savable as a record. | No written trigger, no identifiable owner, or conflicting instructions | Notice record, case ID, timestamp, source, actor |

| Access and data checks | Confirm IT system access revocation across relevant systems, credentials, tokens, and shared tools. CISA recommends immediate access removal for exiting personnel. Confirm data privacy handling at contract end (delete or return), and collect written deletion or return confirmation where required. | Any active access remains, privacy action is unconfirmed, or deletion or return proof is absent | Access logs, identity records, privacy review note, deletion or return confirmation |

| Contract checks | Verify payment cessation terms, final invoice requirements, and the intended final payment status. Check whether contract terms or local rules affect timing. For U.S. reportable payments, confirm TIN collection and written certification where applicable; backup withholding can apply at 24% when IRS conditions are triggered. | Ambiguous contract language, possible timing conflict, unknown final invoice status, or incomplete tax documentation | Contract excerpt, invoice status record, tax form or certification, jurisdiction review note |

| Approval routing | Route by case type: routine to finance, exceptions to legal or risk. Keep approvals written and timestamped. | Verbal-only approval, skipped exception path, or unclear approver authority | Approval record, approver name, timestamp, exception notes |

| Payout decision | After prior checks clear, issue release, stop, or hold. Then reconcile provider and ledger status, and record the resulting final payment status. | Unknown transaction status, unresolved prior hold, or unreconciled provider response | Provider response, internal status log, ledger reconciliation note |

| Record retention | Build one end-to-end evidence pack (notice, access logs, privacy records, approvals, tax artifacts, provider outcome). | The file cannot show who decided what, when, and based on which record | Case export, attachment list, retention location, audit trail export |

The checks most teams leave too late#

Run access and data controls before money moves. If credentials or system access are still live at release, payment and security decisions are happening out of sequence.

Privacy controls belong in the same gate. In controller-processor relationships, current ICO guidance (under review) says there should be a written contract, processor action on documented instructions, and records that can be saved. That is why written deletion or return evidence is a core release artifact.

What should force a hold#

Use a clear internal control rule: if written trigger evidence, IT system access revocation proof, privacy confirmation, or validated final payment status is missing, hold and escalate. Verbal confirmation is not enough for release.

Timing is another escalation point. U.S. federal law does not require immediate final payment, and state rules can be stricter. If contract timing and local rules do not align, pause automation and route for legal review before release.

The async failure mode that causes duplicate or conflicting payouts#

Add a retry checkpoint for asynchronous payout calls. After a timeout, check the latest transaction status tied to the original request ID before sending any new payout action. Stripe documents idempotent requests for retry safety, and PayPal supports PayPal-Request-Id on supported POST calls to return the latest status for the same request.

Also prevent retries from overwriting manual holds. Make hold dominant until explicitly cleared. Read the current decision state before posting, reuse the same idempotency key where supported, and block any new release action when the case is still marked hold.

Related: The Gig Economy in 2026: Payment Volume Trends Contractor Growth and Platform Consolidation.

If you are turning this sequence into system controls, map each hold or release decision to explicit status events in the Gruv docs.

Minimum evidence pack for audit and dispute readiness#

Your process is only as defensible as the case file you can export after close. The minimum pack should let a reviewer reconstruct what happened, who approved it, what was revoked or destroyed, and why payment was released, held, or stopped.

| Evidence item | What to keep | Key details |

|---|---|---|

| Termination record | Written notice plus receipt or acknowledgment | Include notice date, sender, recipient, contract or case ID, and effective date; keep a signed copy if policy or contract requires it |

| Access and data evidence | IT system access revocation records and deletion or return confirmation | Show account deletion or privilege changes, timestamps, and affected accounts; link identity logs and data closeout records to the same case |

| Payout decision chain | Audit trail from request through pre-payment review, approval, exception notes, and payment outcome | Keep chronological evidence; for any exception path, document what was bypassed and who accepted that risk |

| Closeout evaluation | End-of-contract evaluation record and retention note | Capture discontinuance rationale, relevant performance issues, unresolved disputes, and re-engagement status; a 5-year baseline appears in multiple regimes but is not universal |

- Termination record with receipt proof

Keep the written termination notice and proof the contractor received or acknowledged it. If your policy or contract requires a signed termination notice, retain the signed copy; otherwise, retain a written notice plus receipt evidence. At minimum, include notice date, sender, recipient, contract or case ID, and effective date. Avoid keeping only an internal summary when the actual notice is left in email or chat and not linked to the case.

- Access and data evidence that stands on its own

Keep verifiable IT system access revocation records, not a generic note like "access removed." The evidence should show account changes such as deletion or privilege changes, with timestamps and affected accounts. Add a data destruction attestation or equivalent deletion or return confirmation when your contract or data role requires it. If identity logs and data closeout records live in different tools, link them to the same case so the event chain is still auditable.

- Linked payout decision chain from request to outcome

Preserve a full audit trail from request through pre-payment review, approval, exception notes, and payment outcome. The standard is chronological evidence that can reconstruct the sequence of events. If approval and payout outcome records are stored in disconnected systems, defensibility drops quickly. For any exception path, document what was bypassed and who accepted that risk.

- End-of-contract evaluation and retention note

Keep a completion-stage end-of-contract evaluation record where your framework requires closeout evaluations, not just a payment status. Capture discontinuance rationale, relevant performance issues, unresolved disputes, and re-engagement status. Add a retention note in the same file. A 5-year baseline appears in multiple regimes, but do not assume one universal retention period across all payment flows.

If you need to prioritize, choose linkage over volume. One complete, connected file is more useful than a large set of disconnected attachments.

Escalation points that must trigger legal or tax review#

If offboarding facts fall outside your approved rules, pause the payout and escalate to legal or tax before money moves. In practice, these cases should not move through a standard release path without review.

| Case | Escalate when | Grounded details |

|---|---|---|

| Pay timing or status conflict | Contract terms conflict with governing pay-timing rules or the status determination in the case file | Federal baseline rules on final pay can differ from state requirements, and California requires immediate payment at discharge for employees |

| U.S.-Canada treaty claim | A request would reduce or bypass withholding under the U.S.-Canada tax treaty | Article XV analysis can turn on facts including $10,000 Canadian, 183 days in any twelve-month period, and whether Form 8233 is appropriate |

| Construction lien waiver issue | Lien-waiver enforceability is uncertain before release | In Texas, a waiver is unenforceable unless it substantially complies with the statutory form; review the signed document, governing state, and the invoice or draw it covers |

- Contract language conflicts with local pay timing or status facts

Escalate when contract terms conflict with governing pay-timing rules or the status determination in the case file. Federal baseline rules on final pay can differ from state requirements, and California requires immediate payment at discharge for employees. Do not rely on contract labels alone. Check governing law, work location, and documented status rationale against the offboarding record.

- U.S.-Canada treaty treatment or Article XV questions before final payout

Escalate any request to reduce or bypass withholding under the U.S.-Canada tax treaty until tax review confirms the position. Article XV analysis can turn on specific facts, including thresholds such as $10,000 Canadian and 183 days in any twelve-month period, and whether Form 8233 is appropriate for the claim. Do not treat a "treaty exempt" note as a decision; require a reviewed determination. For more depth, see US-Canada Tax Treaty and Contractor Payments: Article XV and Platform Compliance.

- Construction payouts with lien waiver compliance issues

Escalate construction-related payouts when lien-waiver enforceability is uncertain. In Texas, a waiver is unenforceable unless it substantially complies with the statutory form, so review the signed document, governing state, and the invoice or draw it covers before release. A polished but noncompliant template is still a legal risk.

Related: Contractor Misclassification at Platform Scale: Legal and Financial Risks.

Mistakes that create regulatory surprises after offboarding#

Regulatory surprises often show up when teams mark offboarding complete before payment status and evidence are actually settled. Risk drops when finance controls, records, and exception handling stay connected through the final payout decision.

Mistake 1 treating offboarding as admin cleanup instead of a finance control#

This mistake creates exposure because access removal can finish while payment controls lag. Teams may remove access but miss payment cessation per contract, leave recurring payouts active, or release funds before contractual conditions are met.

The control objective is to link termination actions to account and payment controls, not run them as separate tracks. If your process can disable credentials but cannot show who stopped future payouts, who approved that stop, and which contract term governed it, the case is still risky.

Mistake 2 capturing task completion but not a defensible audit trail#

A completed task is not the same as defensible evidence. Accountability expectations focus on whether you can demonstrate compliance with records, not whether a ticket says "done."

In practice, keep one retrievable chain for the offboarding decision path: request, review, approval, and payout outcome. Retention quality matters because disputes and reviews often happen after the event, and weak records make your position harder to defend.

Mistake 3 closing the case without verified final payment status#

Closing before verified final payment status raises payment-error risk. The gating check is not just "termination approved" or "invoice received" on its own, but confirmed payment status supported by the required payment documents.

If payment status is unknown, do not mark the case as fully settled. Verify the invoice or voucher, approval, and payout-rail outcome before the record is marked complete.

Mistake 4 automating edge cases that need market or tax exceptions#

Automation helps on standard exits, but it can fail when rules vary by jurisdiction or tax status. Final-pay timing is not uniform, so a single baseline rule can create timing mistakes.

Tax-data exceptions are another hard stop. If required tax inputs are missing or invalid in scenarios that require immediate backup withholding, auto-release logic should halt and route to legal or tax review instead of pushing payout through.

Conclusion#

The practical win is not more software. It is clear decisions about what blocks money movement, what evidence is required before release, and what must escalate.

-

Gate money at exit. Treat contractor offboarding as a lifecycle control event that includes termination, not an admin handoff. Following OCC Bulletin 2023-17 (June 6, 2023), keep controls proportionate to risk and criticality. Higher-impact relationships need stricter release approvals, clearer hold criteria, and stronger records. Final payment should not move while access removal, contract checks, or tax-status questions are unresolved.

-

Keep one audit-ready evidence chain. A closed ticket is not enough. Maintain retrievable proof of access removal, approvals, and final payout outcomes, with clear timestamps for key decisions. CISA's immediate access-removal guidance and GDPR Article 28's requirement to demonstrate compliance point to the same baseline. If you cannot export the decision trail, your control is weaker than it appears. For asynchronous payouts, use idempotency protection so retries do not create duplicate payment actions after hold or release decisions.

-

Escalate uncertainty early. Do not let automation guess when worker status or market facts are unclear. U.S. IRS guidance treats employee and independent-contractor tax handling differently, and Topic 762 points to Form SS-8 when formal worker-status determination is needed. The U.S. Department of Labor also identifies misclassification as a serious problem, with its current rule effective March 11, 2024. Strong teams automate routine exits, then stop and escalate when classification evidence is unclear, terms conflict, or tax questions remain open.

If you are evaluating a platform for contractor offboarding and final-payment compliance, score options in this order: evidence quality, final-payment control depth, and escalation support first, then market coverage. That prevents you from choosing the smoothest interface and finding out later that you cannot prove why a payment was released, held, or stopped.

If you cannot verify the gate, prove the record, and name the escalation path, the exit process is not ready to scale. Before rollout, confirm market coverage and control ownership for your offboarding flow in a scoped review with Gruv.

Frequently Asked Questions

What must a platform verify before releasing a contractor’s final payment?

Before release, confirm the termination trigger, that future payouts were actually stopped, and the final payment outcome on the payment rail, not just in a ticket. Confirm tax-data readiness, including a valid Form W-9/TIN record and backup-withholding handling where required, since backup withholding can apply at 24 percent. If required artifacts are missing or payout status is still pending, hold the release.

Is contractor offboarding mainly an HR task or a compliance and finance control process?

Treat it primarily as a compliance and finance control process, with HR as an input. The core risk is legal status and money movement, especially across markets with different timing and worker-rule requirements. In the U.S., federal law does not require immediate final pay, and state rules may be stricter.

What proof should exist to show offboarding was completed correctly?

You need one retrievable evidence chain: termination notice, review or approval record, data-handling completion evidence, and the final payout decision with outcome. The standard is demonstrable compliance, not a ticket marked done. For U.S. employment-tax records, keep records for at least four years after filing the fourth quarter for the year.

When should a team stop automation and escalate to legal counsel?

Stop automation when classification or jurisdiction facts are unclear instead of routine. If independent-contractor status is uncertain, use escalation rather than assumptions; Form SS-8 exists for worker-status determination when needed. Also stop on missing or invalid tax data where backup withholding could apply.

Can one global process handle every market, or do we need jurisdiction-specific exceptions?

Use one core process with jurisdiction-specific exception branches, not a single universal rule. Requirements differ: British Columbia sets employee final-pay timing at within 48 hours in one scenario and within 6 days in another, while U.S. federal timing is not immediate and state rules may tighten it. UK IR35 adds another branch when services are provided through an intermediary but would otherwise be employment.

How do we compare offboarding tools when vendor pages are vague on compliance depth?

Compare tools by control evidence, not feature labels. Ask for documented lifecycle coverage through termination, exportable approval history, and clear records of payout holds or releases. Treat SOC 2 as general control assurance, not proof that the tool can evidence your specific final-payment compliance decisions.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cisa.gov/news-events/cybersecurity-advisories/aa22-137atrusted

- csrc.nist.gov/glossary/term/audit_trailtrusted

- dol.gov/general/topic/wages/lastpaychecktrusted

- dol.gov/agencies/whd/flsa/misclassificationtrusted

- eba.europa.eu/activities/single-rulebook/regulatory-activi...trusted

- fdic.gov/news/financial-institution-letters/2023/fil2...trusted

- irs.gov/businesses/small-businesses-self-employed/in...trusted

- irs.gov/businesses/small-businesses-self-employed/em...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: