Quick Answer

Treat contractor status as a gated operating decision, not a contract label. If classification support is incomplete, stop onboarding or payout activation until legal review, tax handling, and control evidence all line up.

Contractor Misclassification at Scale Is an Operating Risk#

At platform scale, contractor misclassification is an operating risk, not a legal edge case. As programs expand across countries and teams, risk can build through many day-to-day classification decisions rather than one obvious mistake.

Misclassification is not new, and it is not limited to gig platforms. What changes with scale is how many points of drift you need to monitor across onboarding, relationship changes, and local rules.

Status decisions are multifactor. No single checkbox, contract clause, tax form, or hours signal settles worker status everywhere. Common factors include control and how permanent the relationship becomes over time, so an independent contractor agreement shows intent but does not end the analysis.

Cross-border growth raises the stakes because countries apply different tests, and state-level rules can also shift the analysis. California AB 5, signed in September 2019, is a useful reminder that one market can apply stricter employee-versus-contractor criteria.

If you own legal, compliance, finance, or operations, set ownership and escalation rules before volume makes decisions inconsistent. In practice, answer three questions clearly:

For current baseline language, review the U.S. Department of Labor's misclassification FAQs alongside California DIR's independent contractor FAQ before you set platform-wide worker-status rules.

- What signals are we actively monitoring?

- When does a borderline case move from ops to legal or compliance review?

- What evidence do we retain so later decisions can be explained and defended?

Evidence quality is central. If you cannot reconstruct why someone was treated as a contractor, you likely have an assumption, not a defensible process. The file can stay simple, but it should consistently capture what the team relied on at onboarding and what changed later.

Use a basic checkpoint before first payout, then re-check when operating facts change. Waiting until a complaint, audit request, or finance exception can turn a fix into legal, tax, and operational disruption, including forced pauses.

This explainer stays focused on that operating goal: what to monitor, when to escalate, and how to document decisions without overbuilding process. The anchor throughout is practical reality over labels.

For a step-by-step walkthrough, see How to use 'Deel Shield' to mitigate contractor misclassification risk.

Misclassification at platform scale means operational dependence not contract labels#

At platform scale, misclassification risk turns on how the relationship works in practice, not what the contract calls it. Under the Fair Labor Standards Act (FLSA), the core question is employee versus independent contractor status under an economic realities analysis, not whether an independent contractor agreement exists.

That distinction matters operationally. Labels are easy to standardize, but day-to-day working reality is where risk appears. The U.S. Department of Labor’s 2024 final rule revised guidance for this FLSA analysis. It was published 01/10/2024 and took effect March 11, 2024, so agreement collection alone is not a sufficient control.

At scale, misclassification risk can grow through pattern drift. A few contractors may look distinct, while a large contingent workforce program can create employee-like patterns through consistent management and review practices. Scale alone does not prove employee status, but it can normalize dependence patterns and make them harder to spot.

Use a simple checkpoint before approval:

- Compare contract terms with real operating practice.

- Tie status review to FLSA analysis, not just paperwork completion.

- Track active legal-change checkpoints (for example, WHD-2026-0001 is a proposed rule process, not final law).

- Escalate cases where contractors are treated as interchangeable with employees.

If you need one operator rule, use this: when paper and practice diverge, treat practice as the stronger signal and escalate. California’s ABC test is not the federal FLSA test, but its contract-and-in-fact framing is a practical reminder to check both documents and real behavior.

There will still be gray areas. Economic realities analysis is often criticized for inconsistent outcomes and limited employer clarity, so keep a defensible record of what was reviewed and why.

Related: Platform Invoicing at Scale: How to Auto-Generate Compliant Invoices for Thousands of Contractors.

Legal baseline you must anchor to before building controls#

Anchor your controls to the current federal baseline. Tie your internal criteria to the analysis currently set forth in 29 CFR part 795, not to legacy checklists or vendor intake forms.

If you reference the 2024 final rule internally, use exact identifiers so teams can locate the right record. That means 89 FR 1638, document number 2024-00067, published 01/10/2024 under Employee or Independent Contractor Classification Under the Fair Labor Standards Act.

Do not assume this baseline is static. In 2026, the Wage and Hour Division (WHD) issued a notice of proposed rule that would replace the current Part 795 analysis with the analysis from the prior final rule dated January 7, 2021. It is a proposal, not final law, but it is a concrete sign that classification criteria can go stale.

Keep a practical change log with at least:

- rule or notice title, citation, and document number

- status (proposed vs. final), including docket WHD-2026-0001 and RIN 1235-AA46 where relevant

- owner, review date, and the specific criteria changes made internally

Use the Federal Register and, for proposed rules, the Federal eRulemaking Portal to review dockets and comments. Before changing controls, verify against an official edition rather than relying only on the FederalRegister.gov display.

Contract terms and day-to-day reality drift apart#

This is where programs get into trouble. The independent contractor agreement may say autonomy, but day-to-day operations can still show employee-like control. If actual signals show schedule control, company tool dependence, manager reporting, or ongoing work central to the business, treat that as an escalation trigger, not a drafting issue.

Use a paper-versus-practice check. Teams can write contractor-friendly language, then run workers through day-to-day workflows with employee-like direction. That mismatch is where risk grows, often because business teams optimize for speed or cost while classification analysis turns on structure and control.

What to compare in a paper versus practice review#

Start with the contract, then test each autonomy clause against operating evidence. Use a short review against four signals:

- Schedule control

Contract says the contractor controls timing. In practice, are set hours, standing meetings, shift coverage, or time-off approvals required?

- Tool and system access

Contract says independent methods. In practice, is work dependent on core internal tools, company logins, internal chat, or employee-style workflows?

- Supervision and reporting

Contract says outcome delivery. In practice, does the worker report into managers, receive detailed task direction, or follow employee-style check-ins?

- Assignment duration and integration

Contract says defined scope. In practice, is the worker doing ongoing labor central to how the business runs?

A scoped engagement can still drift into dependence if day-to-day control and integration keep increasing.

Escalate on employee-like operating patterns#

Escalate when records show employee-like operating patterns, even if contract language looks clean. A well-written agreement does not override operational evidence.

Use primary records, not summaries: the agreement, access history, meeting cadence, manager direction, assignment history, and performance notes. If those records show schedule control, company tool dependence, manager reporting, and central business work, contract edits alone will not fix the risk.

Where teams usually miss the drift#

A common failure mode is optimizing for speed or cost while operations become employee-like. A contractor may start with a defined outcome, then get pulled into recurring internal workflows and employee-like management because it is operationally convenient.

Treat classification as an ongoing risk assessment, not a one-time onboarding step. Controls should detect shifts in control and dependence after signature, not just at intake.

A simple rule you can use now#

If the agreement promises autonomy but your evidence shows employee-like control, pause and escalate to legal or compliance before the pattern hardens. Use a dedicated classification gate in your evaluation workflow so exceptions are reviewed consistently.

For escalation, keep a compact document pack: current agreement, scope, access profile, reporting line, meeting cadence, assignment history, and any performance or correction records. That keeps review anchored in evidence rather than labels.

Related reading: Build a Platform-Independent Freelance Business in 90 Days.

Build an intake classification gate before first payout#

A practical place to catch misclassification risk is before money starts moving. Put the classification gate before activation in Payouts or Virtual Accounts, not after someone is already in recurring payout batches.

Do not activate payouts until the intake file shows a plausible contractor model. Opening the pay rail first can turn classification into remediation work later.

Put the gate at activation, not remediation#

Place the check in onboarding approvals so payment setup cannot proceed until classification review is complete. Keep it lightweight: a first-gate questionnaire, a required artifact check, and a clear escalation path for mixed signals.

Use plain operational questions tied to your existing signal types. Are you buying deliverables or fixed schedule time? Who controls methods and tools? Can the person work for others? Will they be supervised like an employee?

What has to be in the case record#

A yes-or-no form is not enough. Before first payment, require supporting artifacts and store them in an audit-ready file. At minimum, include:

- the independent contractor agreement with scope and autonomy terms

- representation on multi-client work and whether long-term exclusivity is expected

- tax intake and invoice records

- an access log once provisioned

If you cannot produce a complete file on demand, you do not just have missing documents. You have a repeatable process gap.

Also watch for drafting drift. A contract can look careful but still prescribe how work must be done. If the document reads like supervision instead of deliverable definition, flag it at intake.

Decision rule for mixed signals#

Use a hard routing rule: if onboarding signals are mixed, stop automatic activation and escalate the case for review before enabling recurring payouts. A common mixed pattern is outcome-based language in the file while the role still requires fixed hours, close supervision, or long-term exclusivity.

Run a 15-minute spot audit on an approved file. Confirm questionnaire answers match the contract, access setup, and payment design. Treat invoicing through AP as process design, not proof that classification is sound.

If you want a deeper dive, read Healthcare Accounts Payable Automation: How Staffing Platforms Pay Clinical Contractors at Scale.

Set reassessment triggers that auto-escalate legal review#

An intake gate is only the start. Reassessment should fire when operating facts change, not just when a calendar reminder comes due. Route those changes to legal or compliance automatically so status decisions stay aligned with the real working pattern.

Rule status belongs in that trigger set too. The Federal Register entry published on 01/10/2024 with document 2024-00067 is a baseline reference. A WHD Proposed Rule published on 02/27/2026 indicates the Department is proposing to rescind prior analysis, with a comment period shown through 04/28/2026. Treat that as a reason to review your internal decision logic when rule status changes, including references tied to 29 CFR Parts 780, 788, and 795.

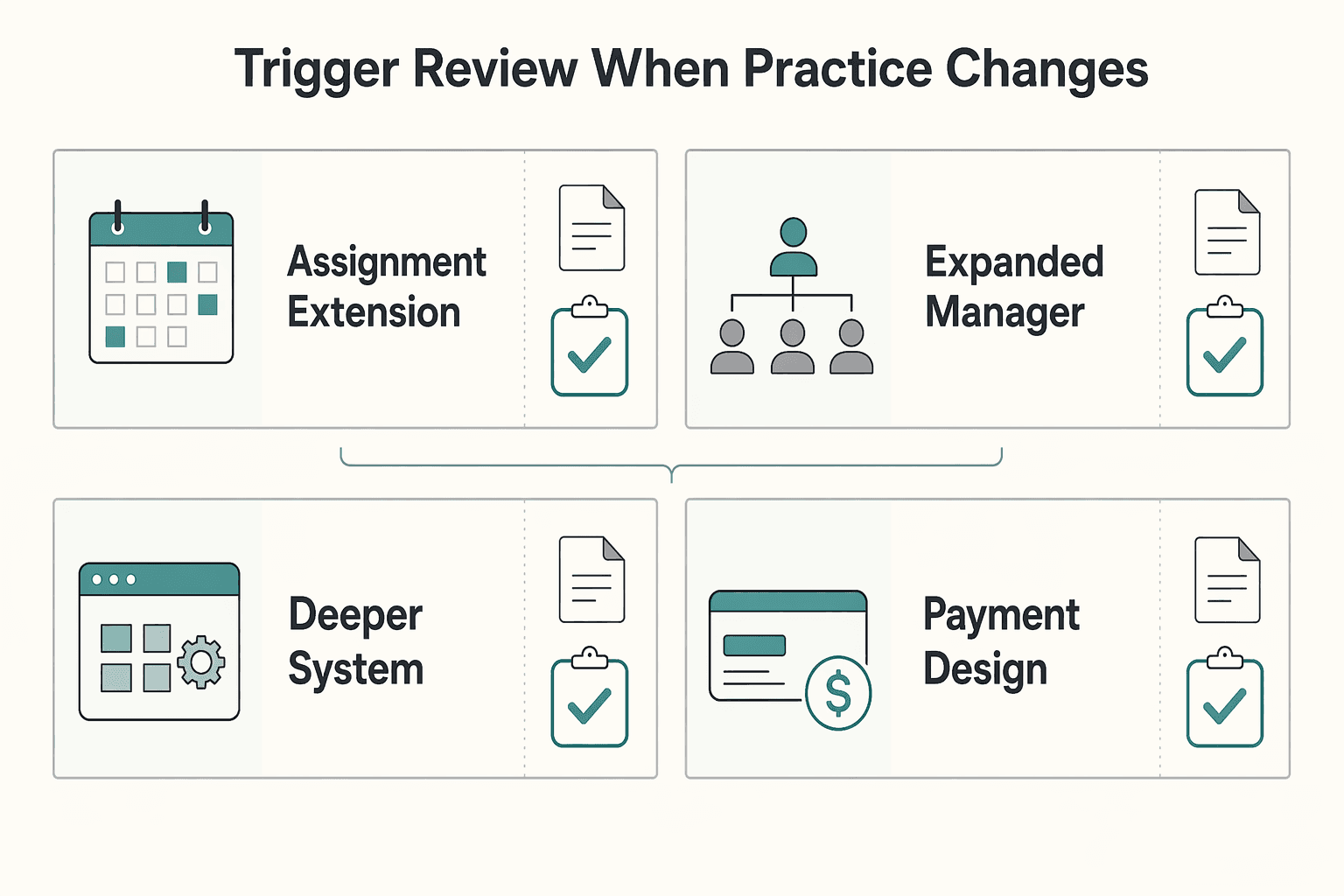

Trigger review when practice changes#

A signed contractor agreement is a starting point, not an end state. If day-to-day work shifts toward tighter control or greater dependence, consider reopening classification review even if no complaint exists.

Use this as an internal trigger framework, not a WHD-mandated checklist.

| Example operations event | Why it matters | What to retain in the case file |

|---|---|---|

| Assignment extension or repeat renewal | Longer duration can change the operating profile | Extension record, updated scope, current invoice pattern |

| Expanded manager oversight | More day-to-day direction can change autonomy in practice | Tasking records, meeting cadence, relevant performance notes |

| Deeper system or tool access | Access changes can show deeper integration | Access request, permissions, provisioning record |

| Payment design change | Payout pattern changes can alter how the relationship functions operationally | Updated payout setup, frequency change, approval trail |

Use a clear routing rule: if the operating pattern changes in a way that may affect status, escalate to legal or compliance.

Tie escalation to records you already use#

The goal is not more forms. It is reliable routing. For each material trigger event, require one checkpoint: either confirm no classification-impacting change or open a legal review task.

A practical internal spot check is to compare three records: the latest contract or amendment, the current access profile, and the live payout pattern. If they do not tell the same story, treat that as a review trigger.

When citing federal rule status, do not rely only on the FederalRegister.gov display. Use the corresponding official Federal Register edition or PDF on govinfo.gov in the determination record. That gives later review a verifiable legal baseline.

Track outcomes by market and rule version#

Track trigger volume, escalations, and outcomes by market and by rule version used at decision time. At minimum, log jurisdiction, whether legal cleared the case, and the authority or version applied.

When interpretation or enforcement questions remain, escalate through counsel. Where appropriate, use the WHD channel identified in the rule materials, the nearest WHD district office.

We covered this in detail in How to Handle Termination of an International Contractor.

Assign ownership across legal compliance finance and ops#

Without explicit ownership, even a good control design can break down. A practical split is for legal to interpret classification status, compliance to run the gate and records, finance to track exposure, and ops to make sure the process happens. This split is not a legal requirement by itself, but it helps keep structured assessments, ongoing monitoring, and auditable processes reliable at scale.

| Function | What it can own | Verification checkpoint | Evidence to retain |

|---|---|---|---|

| Legal | Classification interpretation and calls on mixed or borderline cases | Case file documents the rationale used and the review date | Assessment notes, contract terms reviewed, operating facts reviewed |

| Compliance | Intake gate, exception handling, and audit-ready records | Required assessment and contract artifacts are present before approval | Intake questionnaire, approval trail, exception log, review records |

| Finance | Exposure visibility and payment traceability for reviewed populations | Sampled payouts tie back to worker, period, and review status | Payout records, invoice references, exposure assumptions used in reporting |

| Ops | Intake completeness, trigger reliability, and remediation turnaround | Trigger events open review tasks and close with a named owner | Intake checklist, trigger logs, remediation tickets, closure notes |

Keep legal as the interpretation owner#

Legal should own how your organization applies its classification standard in practice. Each determination should clearly show what facts were reviewed and when the decision was made so later reviews are auditable.

A common risk is treating a signed contract as the full answer after day-to-day conditions change. Legal should be able to reopen a decision when operating reality no longer matches the original assessment.

Put compliance in charge of the gate and the paper trail#

Compliance is the control point between policy and execution. The gate should require complete review artifacts, and exceptions should be formally accepted, rejected, or escalated rather than passed informally.

For new workflows, add a pre-deployment checkpoint and define ongoing monitoring so adverse impacts can be identified over time.

Give finance the exposure view, not just the spend view#

Classification issues can create legal and financial downside, so finance needs visibility into which populations are under review, what has been paid, and which periods are affected. The goal is not false precision. It is explicit assumptions tied to real payment evidence.

The key checkpoint is traceability from worker to payout to review status. If reporting only shows aggregate contractor spend, finance cannot isolate exception-driven exposure.

Make ops accountable for execution quality#

Ops owns whether intake is complete, whether reassessment triggers fire, and whether remediation closes on time. If these handoffs fail, the policy exists on paper but not in operations.

Track open review and remediation items by owner and age so legal, compliance, finance, and ops are working from the same queue.

You might also find this useful: California Meal and Rest Break Laws and Contractor Misclassification Risk.

Create a monthly evidence pack regulators and auditors can follow#

A monthly evidence pack is what turns all of the above into something a reviewer can actually follow. A fixed format is not stated as a legal requirement in the cited materials, but it is a practical control for consistent, reviewable decisions.

One practical approach is to keep the pack in a stable order: worker population changes, risk-tier changes, open exceptions, legal escalations, and closed remediations. For each change, show the prior state, current state, effective date, owner, and approval trail so an independent reviewer can reconstruct a case without side-channel context.

Attach the legal references used that month#

Include the exact legal materials used in determinations, not a generic "DOL guidance" label. The 2024 record is a Wage and Hour Division rule published on 01/10/2024, with citation 89 FR 1638, document number 2024-00067, and listed CFR parts including 29 CFR Part 795.

Also separate active standards from watchlist items. The WHD item in Docket WHD-2026-0001 is a proposed rule, so treat it as monitored change, not current law. If you track it, record the posted date, Feb 27, 2026, and comment deadline, Apr 28, 2026 at 11:59 PM EDT, in a watchlist appendix.

FederalRegister.gov also states that its web display is not an official legal edition and that its XML does not provide legal or judicial notice. Keep the Federal Register page. Also retain the linked official printed PDF used for verification.

Tie legal decisions to payment evidence#

If your compliance controls include payment testing, include sampled traceability from case file to payment records so exposure reporting is testable. For sampled cases, you can track payout state, provider or payee reference, payment period, and ledger-linked reconciliation output tied to worker and review status.

| Tier / event type | Suggested evidence in pack | Verification checkpoint |

|---|---|---|

| Low-risk onboarding | Intake questionnaire, contract/scope terms, review date, approver | Complete record before first payout |

| Medium-risk trigger review | Prior determination, trigger event, updated operating facts, signoff | Reassessment reflects current operating reality |

| High-risk escalation | Determination memo, cited references (including 29 CFR Part 795 and WHD materials), decision date, owner | Legal basis is explicit and fact-linked |

| Closed remediation | Operational change made, effective date, owner, sampled payout trace | Status closure matches payment and operating records |

If you standardize one thing, standardize completeness by tier and event type. That removes ambiguity about what "done" means and gives legal, compliance, finance, and ops one defensible record.

Score risk tiers and choose actions with explicit if-then rules#

Risk tiers should drive action, not just document concern. Define low, medium, and high as internal control bands tied to control signals, then bind each band to a default internal action.

Keep tiers internal and fact-based#

Treat these tiers as triage logic for your team, not universal legal thresholds. Focus on how much control is showing up in practice and whether those facts are changing over time.

Analysis of misclassification-related contract provisions found them generally predictive of estimated litigation risk, but that result came from a small sample. Use that as a signal, not proof of causation or a standalone legal conclusion.

Use one if-then table for every case#

Use a single internal table so case handling stays consistent; this is an internal control framework, not an FLSA-mandated matrix.

| If the case shows... | Then assign tier... | Then take action... | Before closing the step, confirm... |

|---|---|---|---|

| Limited control, with facts consistent over time | Low | Proceed | Intake and approval records are complete |

| Mixed or changing control signals | Medium | Proceed with controls and reassessment | Reassessment reflects current operating facts |

| Strong control signals that persist in practice | High | Route for legal determination and status review before proceeding | Legal rationale is documented and tied to case facts and payment status |

For high-risk cases, escalate instead of relying only on contract language changes. Keep legal analysis anchored to the current materials your team uses for FLSA determinations. Do not treat the 2020 WHD Federal Register item as final law by itself because it is a proposed rule entry, and verify against an official Federal Register edition when needed.

Match remediation to the failure mode#

When a case moves tiers, name the remediation path explicitly in the file so everyone knows what is being fixed.

- Contract correction: use when operating reality is contractor-like but documentation is inconsistent.

- Operating model change: use when daily controls are the issue and the workflow must change.

- Status change: use when control patterns are sustained and cannot be reduced without changing the role.

Only downgrade risk after both decision evidence and operating evidence are updated.

Publish SLAs by event trigger#

If you publish internal SLAs, define them as internal policy choices and document escalation ownership clearly. Control-based triage and documented decisions are sound practice, but they do not set required escalation or remediation timelines.

Need the full breakdown? Read Are You an Employee or a Contractor? A Self-Assessment Checklist.

If you need to turn your risk-tier table into enforceable payout controls and exception handling, see how Gruv structures Payouts workflows.

Model financial exposure without fake precision#

Once you have a risk tier, model financial exposure as a range, not a single exact loss number. The current evidence supports direction and scale of risk, but it does not support a universal per-worker penalty benchmark.

Use the Maryland report as an anchor for scale, not as a pricing table: agencies identified 7,767 misclassified workers in Fiscal Year 2025, a nearly 39% increase over 2024. That supports serious scenario planning, but it does not represent national prevalence or your platform's exact liability.

| Scenario | Population basis | Duration basis | Wage stress test |

|---|---|---|---|

| Narrow | Confirmed high-risk cases only | First clear trigger to remediation date | Test whether payouts could create pay-compliance issues if employee status is found |

| Working | High-risk plus unresolved medium-risk cases | Activation date or last clean review, whichever is earlier | Add additional pay-liability implications where operating patterns and records make that plausible |

| Stress | Everyone in the affected operating model or team | Full internal lookback used for exposure reporting | Assume missing records cut against you until evidence narrows the range |

Keep assumptions explicit and reviewable in the case file or monthly evidence pack: affected cohort, lookback window, jurisdiction, hour-data quality, exclusions, and approver. If records are incomplete, say so plainly and widen the range.

Use one verification checkpoint before reporting: reconcile modeled headcount and dates to payout ledger data, first and last payout dates, contract amendments, and extension records. Potential misses include excluding prior paid workers under the same operating facts or relying on contract dates when operating reality changed earlier.

If assumptions remain weak, increase the reserve range and label uncertainty clearly. For legal-research inputs, verify FederalRegister.gov material against an official Federal Register edition before treating it as a legal anchor.

Connect classification controls to tax and cross-border documentation#

Treat this as a linkage control. Keep classification, tax documentation, and payout setup connected in one workflow, but do not treat them as the same decision. A complete tax file shows how someone is being paid and reported, not whether the classification is correct.

Keep tax paperwork aligned, not confused#

Keep the classification record alongside the tax record for the same worker or supplier profile. In U.S. contractor flows, that usually means a Form 1099 path, commonly 1099-MISC or 1099-NEC, rather than a W-2 employee setup. For cross-border programs, use the same alignment approach with the local tax-document path on file.

Tax-form completeness is not classification proof. Tax paperwork covers reporting and withholding, while classification asks whether operating reality reflects contractor status, including whether company control stays limited. If operating facts point to employee-like control, escalate review even when the document set is complete.

Put jurisdiction notes in the case file#

Make jurisdiction notes mandatory because classification rules vary by country and can diverge across markets. In stricter U.S. states, meeting 1099 standards can be harder, so escalation discipline matters more.

For each case, capture:

- country and, for U.S. cases, state

- current tax path on file, for example 1099 path, W-2 path, or equivalent local documentation path

- short note on the local risk concern

- local-counsel trigger and escalation date

- key operating facts tied to control and how work is performed

Keep it concise, but clear enough that finance, compliance, and ops can see where a single-market analysis may fail.

Make remediation hit invoicing and payout setup#

A classification fix is incomplete until invoicing and payout settings change with it. Otherwise, a contractor setup can stay in place after legal or compliance updates.

Before the next payment cycle, run one checkpoint: confirm classification status, tax-document path, invoicing state, and payout profile all match across case records and payment systems. Validate the first post-remediation payout, or block, by worker ID, profile type, and document status, not contract name alone.

If you need deeper tax-operations detail, use this tax-operations guide for high-volume contractor programs.

Conclusion#

The core control is operational, not contractual. Classification decisions are strongest when current evidence shows how work is actually performed and when you escalate as practice drifts. At scale, weak decisions can get repeated across teams, roles, and markets, and the risk compounds.

If you implement one control set, make it enforceable:

- Run a classification check before an engagement starts.

- Define the operating changes that trigger reassessment.

- Assign clear internal owners for exceptions.

- Keep an evidence record for changed or disputed cases.

Use a simple test in every review: does current evidence show an independent business relationship, or increasing economic dependence on your platform? If the answer depends on stale onboarding notes or contract language that no longer matches day-to-day operations, treat that as a live risk signal.

In practice, review who sets schedules, whether the role performs core business functions, what systems and tools are used, and whether extensions or deeper integration have shifted control. As your cross-border footprint expands, verify local requirements early and route borderline cases before volume ramps.

A repeatable initial classification check, trigger-based reassessment, clear ownership, and consistent evidence review can reduce surprises more effectively than contract text alone. Before expanding to more markets, map each classification checkpoint to traceable system events and records using the Gruv docs.

Frequently Asked Questions

What is contractor misclassification at platform scale?

It is classifying someone as an independent contractor when the real working relationship looks like employment in practice. At platform scale, that risk can compound if one flawed operating pattern is repeated across many workers. The core check is how work is actually controlled and performed, not just the profile label.

Does a signed independent contractor agreement prevent misclassification?

No. The distinction between employee and contractor goes beyond paperwork, and California guidance looks at both contract terms and what happens in fact. A signed agreement helps document intent, but it does not override employment-like control in day-to-day operations.

What factors matter most in an economic reality test review?

Center the review on actual operating facts, not only the contract file. The provided materials do not give a full federal factor list or weighting, so avoid inventing a scoring model. At minimum, test whether the worker is genuinely independent in practice and whether control resembles an employee relationship.

When should a platform re-assess contractor status after onboarding?

The excerpts do not support a fixed reassessment cadence. A practical trigger is a material change in the real working relationship, especially if control or direction shifts in practice. If contract terms and day-to-day reality start to diverge, escalate review.

Who should own misclassification risk across legal, compliance, finance, and ops?

The provided materials do not establish a legally mandated single owner across those functions. Treat this as a cross-functional risk with clear decision rights, named accountability, and an escalation path. Avoid split responsibility without clear authority to pause or correct setup.

Can tax documents like Form W-8 or Form 1099 substitute for classification analysis?

No. A Form 1099 path does not prove classification is correct, and documented tax treatment can still coexist with employment-like control. For Form W-8, the provided excerpts do not establish that it can substitute for classification analysis. Use tax documentation and classification analysis as separate checks.

How should we act when evidence is incomplete but risk signals are rising?

Do not treat missing evidence as neutral when control-related risk signals are increasing. Escalate for legal or compliance review and document what is known versus unknown in the case record. Keep the record focused on jurisdiction, current contract status, and whether actual practice matches documented terms.

Does California change the analysis?

Yes. California’s ABC framework starts from a presumption that workers are employees unless all three conditions are satisfied. Its control analysis explicitly tests both the contract and real-world practice, and roles comparable to existing employee roles are a strong risk signal.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- crptr.nv.gov/uploadedFiles/crptrnvgov/content/meetings/20...trusted

- cslb.ca.gov/Resources/BoardPackets/2023/Sunset%20Review%...trusted

- dir.ca.gov/dlse/faq_independentcontractor.htmtrusted

- dol.gov/sites/dolgov/files/WHD/flsa/IC_NPRM_092220.pdftrusted

- dol.gov/agencies/whd/flsa/misclassification/rulemaki...trusted

- federalregister.gov/documents/2024/01/10/2024-00067/employee-or-...trusted

- federalregister.gov/documents/2024/01/10/2024-00067/employee-or-...trusted

- irs.gov/pub/irs-access/p2104_accessible.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: