Quick Answer

Addressable spend in a platform payout operation is the portion of recurring external payouts your team can control, standardize, and automate. It usually includes contractor, creator, seller, and marketplace disbursements where you set release rules, apply compliance checks, track payout status, handle retries safely, and reconcile outcomes into finance records, rather than employee spend programs or one-off invoice-based AP workflows.

What Counts Toward Addressable Spend for Platform Payouts#

The useful question is not whether you should automate payouts. It is which spend is actually controllable, repeatable, and risky enough to automate first. For platform operators, that usually means isolating the share of contractor, creator, and marketplace disbursements you can actively influence, then pairing automation with controls that keep retries, status tracking, and payout outcomes reliable.

That is the practical meaning of addressable spend here. In procurement language, addressable spend is the portion of total spend your team can control, influence, or optimize. In a platform payout operation, the highest-value slice is rarely all spend. It is the recurring external payout volume where your product, finance, and ops teams can define who gets paid, when they get paid, what checks must pass first, and how the result is recorded.

Three categories matter most at the start:

- Controllable payout lanes

Focus on flows where your team owns the payment decision, not just the accounting aftermath. Marketplace payout automation is built around programmatic recipient creation, one-time or recurring payouts, and outcome tracking. Repeatability is the real dividing line: if the same flow happens every day or every week, it is a better candidate for automation than a one-off exception.

- Embedded product payments

When payments are built natively into your software product, they stop being a back-office concern and become part of the user experience. Embedded payments are presented as improving customer experience and retention, but that only helps if payout execution is dependable. What matters is where the failure shows up: a missed seller payout or contractor payment hits customer trust directly, not just finance workload.

- Retry-safe execution controls

High-volume payout automation fails fast when retries are not handled safely. Idempotency exists for a simple reason: if a request is retried, it should not create the same side effect twice. This is about operational safety, because duplicate disbursements are much harder to clean up than a delayed payment.

That is why generic finance software roundups miss the point. AP automation and payout orchestration are not the same job. One is centered on invoices and payable workflows; the other has to handle recipient onboarding, payout release, outcome tracking, and recovery when something breaks midstream. Use Guide to Bulk Payment Processing Platforms when you need a closer comparison of payout-first tooling.

A good early verification step is simple: pick one recurring payout flow and confirm you can trace the request, the approval or business trigger, and the payout outcome without relying on a spreadsheet. A strong red flag is any setup that promises automation but cannot explain how retried requests avoid duplicate payments or how payout status is surfaced after submission.

The sections that follow are built for that decision. They will help you sort the payout lanes worth automating now, the ones to defer, and the controls you should verify before you scale.

Who this list is for and how to choose#

Use this list if your pain is recurring external disbursements, not employee spend. The right buyers are teams handling Marketplace payouts or Embedded payments where finance ops and engineering both own part of the outcome, especially once a single batch can send funds to many recipients at once.

- Best fit: recurring payout lanes with shared ops and engineering ownership

If you release contractor, seller, or creator funds on a schedule, you are in scope. A mass payment is a single batch to multiple recipients, so the selection question is less about "can it send money?" and more about whether the product can survive retries, exceptions, and status tracking when that batch goes wrong.

- Poor fit: employee card and reimbursement programs

If your main need is corporate credit card management, card issuance, spend controls, and expense reconciliation, this list is probably not your first stop. Brex and Rippling are clearly positioned around employee spend governance; Rippling, for example, describes issuing corporate cards, controlling spend, and reconciling expenses. That is a different job from orchestrating high-volume external payouts.

- Choose on concentration, reconciliation, and compliance gates

Start with the payout lane where volume is concentrated and mistakes are expensive. Then check whether you can tie payout activity back to posted GL entries in Intacct or NetSuite, because reconciliation is where weak tooling shows up first. If you pay across borders, also verify how KYC and AML checks gate payout release, since KYC is a regulatory requirement and not just an onboarding checkbox. If that proof is missing, Account Reconciliation for Payment Platforms is the right next check.

- If spreadsheets still handle failures, move status and retry controls to the top of your list

Spreadsheet-heavy reconciliation is a real warning sign because it adds error risk and delays close. Prioritize products that expose explicit Payouts status states, status-change events, idempotent retries, and audit trails. One practical check: ask to see the status history for a failed payout and the evidence that a replayed request will not create a duplicate disbursement. The self-service layer in Supplier Portal Self-Service Contractor Payment Hub Best Practices is a useful reference point.

Where your addressable spend actually sits#

Start by mapping spend by flow type, not by whoever currently owns the process. The useful split is simple: invoice-based AP on one side, recurring external payouts on the other. If you mix them together, you usually buy for approval screens and miss the harder part, which is payout status, retries, and reconciliation when a batch fails.

- One-off AP invoices

Treat supplier bills, invoice approvals, and standard payable cycles as AP automation, not payout orchestration. That lane is about bill capture, approvals, payment status, posting details, and audit trails, which lines up with how Sage Intacct presents AP visibility and traceability. The source record is the invoice or bill, and the evidence trail should start there. If your team can point to the bill, the approval, and the posting details, this flow belongs in AP first, even if the money in the end moves through a bank or payment rail.

- Recurring contractor payouts

Put repeated contractor or creator payments in a separate lane, especially when the payout is triggered by platform activity rather than a fresh invoice each time. NetSuite does position payment processing as connecting AP and AR with third-party payment systems and financial institutions, but that is not the same as proving full payout-state behavior for high-volume external disbursements. Score this flow on operational friction, not just dollars. If exceptions are common, finance is hand-keying corrections, or reconciliation back into Intacct or NetSuite takes real effort, you are already outside a clean AP-only pattern. If the lane already looks batch-heavy, Mass Payouts for Gig Platforms: Complete Guide is a strong comparison read.

- Marketplace disbursements

This is usually where automation value concentrates first, because the flow is frequent, repeatable, and exposed to failure at scale. Your minimum evidence pack per disbursement should include four items: the source event that created the obligation, the approval or release record, the payout status history, and the posted GL entries. The General Ledger is the accounting layer where accounts, journals, and financial reports are maintained, so if you cannot trace a payout into posted entries, you do not yet have a dependable operating view. The checkpoint here is traceability. Ask for one failed payout example and verify that you can follow it from source event to provider reference to GL posting without leaving spreadsheets. If that chain breaks, the flow is more manual than it looks.

- Compliance-gated flows

If a payout lane is blocked or released based on KYC or AML checks, treat it as prime automation territory. In at least one major platform setup, users must complete full verification before they can process payments and receive payouts, and missing or unverified identity information can temporarily pause payouts. Use a hard decision rule here: if the flow is frequent, repeatable, and payout release depends on verification or monitoring, move it to the front of your automation queue. A common failure mode is assuming compliance is just onboarding data collection, when in practice it can be the gate that stops funds from moving at all. The tax-document side of that gate belongs with How to Automate W-9 Collection for a 1099 Contractor Pool.

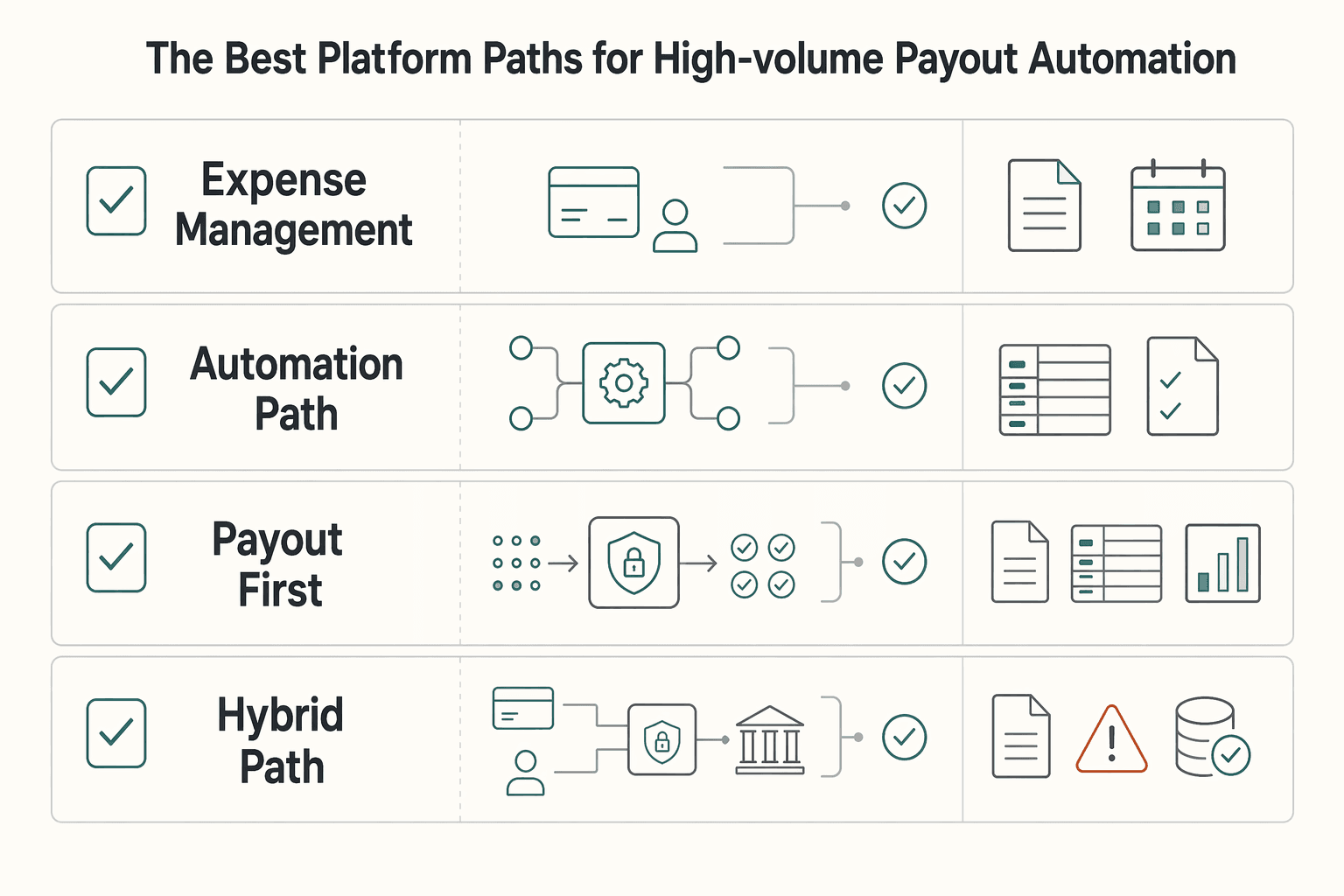

The best platform paths for high-volume payout automation#

If your payout lane is recurring, external, and exception-prone, do not force it into an employee spend or invoice tool just because finance already owns that software. The practical split is simple: use expense tools for employee spend, AP tools for invoice governance, and payout-first rails when you need batch status, retries, compliance gates, and reconciliation evidence.

| platform path | best for | key pros | key cons | required controls | when to avoid |

|---|---|---|---|---|---|

| Expense management path (Brex, Rippling) | Employee cards, reimbursements, internal spend controls | Fast finance adoption; strong spend visibility; Brex emphasizes real-time control of company spending; Rippling centers employee cards, spend control, and reconciliation | Unclear fit for high-volume external marketplace payouts and multi-recipient payout operations | Clear separation between employee spend and external payee payouts; reconciliation into ERP; approval policy by spend type | Avoid if funds are going to contractors, creators, sellers, or other external recipients at scale |

| AP automation path (Yooz, CashFlo) | Invoice-based AP and payable workflows | Strong invoice routing and approval depth; Yooz markets configurable approval criteria; CashFlo markets 95% straight-through invoice booking and 100% compliance in its AP message | Current public evidence here is invoice-first, not payout-batch recovery, status-state depth, or reversal handling | Invoice source record, approval matrix, posting controls, ERP sync, exception handling for payable workflows | Avoid if your core pain is batch payouts, failed recipient transfers, or payout-state visibility |

| Payout-first infrastructure path (Gruv Payouts + Virtual Accounts) | Recurring external disbursements with compliance and reconciliation needs | API, webhook, file import/export options; batch status reporting; item-level breakdowns; downloadable reconciliation files; Virtual Accounts in 30+ currencies where supported | More implementation ownership across engineering, finance ops, and operations | Idempotency keys for retry safety, webhook endpoint, payout status history, reconciliation file review, policy gates before release | Avoid if you only need basic employee spend control or low-volume invoice payments |

| Hybrid path (AP + payout infra) | Companies running both invoice AP and marketplace or contractor payouts | Keeps invoice governance in AP while routing external disbursements through payout-oriented rails; cleaner control model for mixed flows | Two tools to govern, more integration work, more ownership boundaries to define | Clear source-of-truth rules, ERP posting logic, exception queue ownership, end-to-end audit trail | Avoid if your volume is low enough that one lane clearly dominates and the second tool adds more overhead than value |

- Expense management path

Brex and Rippling make sense when your problem is internal company spend, not marketplace disbursement orchestration. Brex positions spend management around real-time control over company spending, and Rippling frames its finance lane around issuing corporate cards, controlling employee spend, and reconciling expenses. That is useful, but it is not the same as proving you can manage a failed batch of 2,000 external payouts.

The red flag is a payee-type mismatch. If the recipient is not your employee, ask the vendor to show the payout status trail, retry behavior, and reconciliation output for a multi-recipient external batch. If that demo turns back into card controls or employee reimbursements, you are in the wrong product category.

- AP automation path

Yooz and CashFlo fit best when the source record is an invoice and the core control is an approval path. Yooz explicitly markets invoice routing according to set criteria, such as a customized AP approval matrix, and CashFlo's public AP message centers invoice straight-through processing with a 95% booking claim.

That strength becomes a trap if you treat it as proof of payout capability. Public evidence in this set supports AP depth, not batch-failure recovery, explicit payout status changes, or replay-safe retries for external disbursements. If your finance team wants approval discipline but your ops team is living in spreadsheet-based payout exceptions, AP automation alone is usually not enough.

- Payout-first infrastructure path

This is the right path when external payouts are frequent and operationally sensitive. Gruv positions its integrations around APIs, webhooks, file imports, and exports, and its mass-payout message includes real-time batch status reports, item-level breakdowns, and downloadable reconciliation files compatible with major ERPs. Virtual Accounts add local account details in 30+ currencies where supported, which matters when inbound and outbound money need a cleaner ledger trail. That operating shape is also covered in Global Payment Processing Platforms: Complete Infrastructure Guide.

Your must-have controls here are not optional extras. Use idempotency so retries do not create duplicate disbursements, and require a webhook endpoint because payout integrations need event-driven status updates. A good verification checkpoint is simple: ask for one failed payout example and confirm you can trace request, webhook status change, provider reference, and reconciliation output without manual patching.

- Hybrid path

Most growing platforms land here. Keep invoice governance in AP, and route recurring external payouts through payout-first rails. That gives finance the approval structure it expects while giving ops and engineering the control surface needed for real payout behavior.

If you choose this path, define ownership early. Decide which record is authoritative for release, which record is authoritative for status, and what document closes the loop into the ERP. If that is still fuzzy, the failure mode is predictable: approvals look clean, but exceptions and reconciliation pile up off-book.

The decision checkpoints that prevent an expensive wrong choice#

Once you have narrowed the path, stop comparing logos and start forcing proof. The right decision rule here is simple: if a vendor cannot demonstrate replay-safe retries, status visibility through API or webhooks, and reconciliation outputs your finance team can post into Intacct or NetSuite, treat it as a no-go for high-volume Embedded payments.

Payout operations look manageable in a demo, then get messy fast when transaction counts rise and fund flows become more complex. That is why your selection meeting should end with evidence, not promises. Ask the vendor to show a failed payout, a retried payout, and the accounting output that closes the loop.

| checkpoint | what you should ask for | go signal | no-go signal |

|---|---|---|---|

| Throughput evidence | "Show the largest production-like batch or payout volume you can credibly support, and tell us what is still unknown." | Vendor is explicit about tested volume ranges, caveats, and what needs validation in your use case | Hand-waving about "scalability" with no test evidence or refusal to discuss unknowns |

| Batch controls | "How do batch states work, and what happens when only part of a batch fails?" | Clear item-level status, batch-level status, and a visible path for partial failures | Only a binary batch success/fail answer, or no explanation of partial failure handling |

| Exception workflow | "Where do failed payouts go, who works them, and what evidence is preserved?" | Named ownership, traceable status history, and a defined exception queue | Failures are handled manually in email or spreadsheets, or ownership is unclear |

| Retry semantics | "How do you prevent duplicate payouts when requests are retried?" | Explicit idempotent or replay-safe behavior for payout creation or update requests | Retries can re-run the payout without duplicate protection, or the answer is vague |

| Reconciliation outputs | "What file or event output will let us reconcile into Intacct or NetSuite?" | Downloadable or exportable reconciliation data that ties request, status, and provider reference together | Finance must manually stitch payout events back to ERP postings |

Four checkpoints worth treating as hard gates#

- Make replay safety a hard stop

If the answer on retries is fuzzy, you already have your answer. Stripe's API documentation defines idempotent requests as a way to safely retry without accidentally performing the same operation twice, and that is the standard you should use when judging payout creation behavior. For high-volume payouts, duplicate execution is not a small bug. It becomes a customer trust problem, a reconciliation mess, and sometimes a recovery project with real cash exposure.

Your verification step is concrete: ask the vendor to trigger the same payout request twice and show why only one payout is created. The common failure mode is that sales says retries are "handled," but engineering later reveals that protection only exists for some API calls, not batch imports or adjacent actions.

- Require real status visibility, not summary reporting

A payout tool needs real-time status updates made available through the API or webhooks, not just an end-of-day report. You want to see the request accepted, the payout progressing, the failure if it happens, and the reference that lets finance trace it back. If a vendor can only show a dashboard screenshot, that is not enough for operating at scale.

This matters most when your team closes the month in Intacct or NetSuite. The evidence pack should include the source event, payout status history, provider reference, and the reconciliation output finance uses to support the posting. If you need more detail on that handoff, see Account Reconciliation for Payment Platforms: How to Automate the Match Between Payouts and GL Entries.

- Do not let compliance gating sit outside payout release logic

If KYC, KYB, or AML checks are performed by another provider or another team, confirm exactly how those decisions control payout release. Adyen's verification guidance is clear on the principle: users must be verified before you can process payments or pay out funds, and capability access should depend on verification outcomes. In practice, that means you need a rule that blocks payout initiation until the required checks pass.

The red flag is "compliance is handled elsewhere." That often means the payout engine has no direct enforcement link to the verification result, so money can move before controls are applied. Controls that happen after funds move are the ones that usually break first.

- Force explicit answers on the unknowns

Current SERP claims often say plenty about approvals, automation, or speed, but stay quiet on the details that matter when payout volume grows. Ask four direct questions: What throughput limits are known today? How are batch failures handled? What is the process for reversals? Who owns exceptions operationally on both sides? You are not looking for perfection. You are looking for honesty about what has been proven and what still needs testing.

If a vendor cannot answer those questions in writing, assume your team will discover the answers during production incidents. That is usually the expensive wrong choice.

Compliance and tax gates that change rollout order#

The rollout order here should be strict: verify the payee, monitor the activity, collect the right tax documents, then release funds. If your KYC, KYB, AML, and tax checks are still happening in side tools or spreadsheets, do not widen payout volume or add countries yet.

| Step | Primary owner | What must be true before you advance | Evidence to keep |

|---|---|---|---|

| Map the payout lane | Finance ops + product | The recurring payout flow is clearly separated from AP and employee spend | Named lane, monthly volume, and exception rate |

| Prove payout controls | Engineering + ops | Idempotent retries, status visibility, and replay handling work on one real flow | Request ID, webhook history, and provider reference |

| Verify compliance gates | Compliance + ops | KYC, KYB, AML, and tax-document rules can actually block payout release | Hold or release states with timestamps and reviewer actions |

| Close the finance loop | Finance controller | One payout can be traced into reconciliation output and posted GL entries | Batch output, reconciliation file, and ERP posting evidence |

- Gate activation on KYC and KYB, not after the first payout

KYC is not a nice-to-have for external payees. Stripe's verification guidance states that connected accounts must satisfy KYC requirements before they can accept payments and send payouts, and U.S. customer due diligence rules require beneficial owners of legal-entity customers to be identified when a new account is opened. The operator check is simple: try to create a payout for an unverified individual and for a business missing beneficial ownership details. Both should fail before money moves. The common break is that onboarding marks a profile "approved" in one tool, while the payout engine has no direct block tied to that status. For tax-ID control points, TIN Matching Platforms Validate Contractor Tax IDs is a practical companion.

- Treat AML as an ongoing hold-and-review control

AML does not stop at onboarding. FFIEC guidance points to ongoing monitoring to identify and report suspicious transactions, so your payout policy needs a state that can pause or queue disbursements when monitoring flags activity. Ask the vendor to show one alert that changes a payee or payout state and preserves the reason code, timestamp, and reviewer action in the audit history. A frequent failure mode is screening only at signup, then letting a previously approved payee continue receiving payouts with no ongoing review path.

- Make W-8 and W-9 collection part of payee readiness

Do not activate a payee and hope tax paperwork catches up later. Form W-9 gives the payer the Taxpayer Identification Number needed for information returns, Form W-8BEN should be collected when requested by the payer or withholding agent, and Form 1099-NEC is the IRS form used to report nonemployee compensation. Your evidence pack should include the exact form collected, the receipt date, the payee record it is tied to, and the rule that decides whether the payee can move to "payable." If the first payout goes out before the form is on file, year-end reporting usually turns into a chase exercise.

- Document cross-border tax scope before market expansion

For cross-border programs, write down where VAT handling starts and where it does not. The EU frames VAT as a general tax that applies in principle to commercial activities, but that does not mean every payout flow has the same treatment, so you need a country-by-country operating note before launch. Keep FEIE and FBAR in the right lane too: FEIE is an individual tax filing concept, with a 2026 maximum exclusion of $132,900 per person, while FBAR is FinCEN Form 114 and can apply when aggregate foreign financial accounts exceed $10,000 at any point in the year, due April 15 with an automatic extension to October 15. These are not blanket rules for every payee, so document when they may matter and where your support team should stop short of tax advice.

- Keep PII controls explicit and tied to payout decisions

Compliance data quickly turns into a privacy problem if you are vague about access. NIST's baseline is straightforward: PII should be protected from inappropriate access, use, and disclosure. In practice, store sensitive fields masked by default, limit unmask rights to named roles, and keep audit logs for data addition, modification, deletion, and exports. If you use log tooling that supports restricted unmask permissions, such as CloudWatch's logs:Unmask, make that permission rare and reviewable. The red flag is a support or ops user being able to view full identity or tax data without a business reason tied to a payout decision.

The implementation sequence finance and engineering should follow#

Once your compliance gates can actually stop money movement, the next decision is sequencing. For your first live lane, keep it narrow and opinionated: create the payee, run policy checks, trigger Payouts, wait for webhook status, then post GL entries. Do not let finance posting key off the initial API request alone. Before rollout, compare the posting model in Real-Time Ledger vs Batch Settlement Architecture for Platform Volume.

- One-lane rollout first

Start with a single payout lane such as domestic contractor payouts, not every payee type at once. The point is a strict order of operations: payee record first, policy result second, payout request third, webhook-confirmed status fourth, ledger and GL entries last. That gives you one traceable chain to test end to end before you add cross-border rules, multiple funding paths, or ERP-specific posting logic.

A practical checkpoint here is to force a failed state on purpose. Create one payout for a payee that passes checks and one for a payee that should be held, then confirm your downstream entries only appear for the successful case. A common failure mode is posting the liability or cash movement when the payout is merely requested, then spending days unwinding journal entries after a downstream failure or reversal.

- Use Virtual Accounts when the product and geography support them

If Virtual Accounts are enabled, use them to simplify inbound collection and make entity-level routing clearer. They are sub-ledger account identifiers linked to a physical demand deposit account, and implementations can assign them by subsidiary legal entity. The benefit is cleaner operational segmentation without opening a new physical bank account for every flow or business unit.

This matters most when inbound funds and outbound disbursements share the same operating stack. You want each receipt tied to a virtual account identifier, then mapped into the ledger before release to outbound payouts. If finance cannot trace an inbound collection to the virtual account, the payout record, and the resulting GL entry, do not broaden rollout yet.

- Make retries replay-safe before volume arrives

Idempotent requests are not optional if you expect timeouts, user retries, or provider retries. Stripe documents idempotency keys up to 255 characters long, and keys can be pruned only after they are at least 24 hours old. The payoff is that retries become safe operationally instead of a hidden source of duplicate disbursements.

Handle webhooks with the same discipline. Providers may deliver the same webhook event multiple times, so store event IDs and check for duplicates before you run business logic. Your ledger should be the source of truth for payout state, not whatever the client retried last.

- Reconcile daily, but investigate before trusting the report

Set up a daily reconciliation report and an explicit exception queue before you expand lanes. The point is operational closure: reports show what settled in the day window, but daily transaction reporting does not always reflect final status, and production reconciliation should expose failed-payout breakdowns rather than hide them in raw logs.

Give exceptions a named owner and a documented investigation path. Route mismatches into a queue or worklist, compare the payout batch to the underlying transactions it settles, and only then release broader volume. If you need a deeper model for that last mile, this companion piece on matching payouts and GL entries is the right next read.

Red flags that signal you should pause rollout#

If these show up in selection or testing, pause. They usually mean you are about to scale ambiguity, not payout operations.

- The demo stays glossy and dodges batch mechanics

If a vendor cannot walk through payout batches, reversals, failed-settlement handling, and what happens when you retry the same request, treat that as a real no-go, not a sales gap. You need concrete answers on how a payout is grouped, what reference comes back from the provider, and how exceptions are surfaced when a batch only partially clears.

- You cannot trace one payout end to end into the ERP

Pick a single payout and force the team to show the full chain: request ID, provider payout reference, settlement batch, and posted GL entries in Intacct or NetSuite. This matters because payout reconciliation depends on linking the bank payout to the transactions it settles, and NetSuite's Transaction Audit Trail can drill into transaction history and GL Impact while Intacct keeps audit-relevant user actions centrally. If that chain breaks anywhere, your reconciliation report is decoration, not control.

- "Compliance is handled" is the whole answer

That phrase is not enough when money release is involved. For connected-account payouts, KYC requirements must be satisfied before accounts can send payouts, and in the U.S. an MSB AML program is a maintained obligation under 31 CFR § 1022.210. What matters is whether policy gates are tied to payout release logic, with observable hold and release states, not just a vendor promise.

- Finance and engineering disagree on status truth and exception closure

If finance trusts the ERP status while engineering trusts webhook status, you do not yet have one accountable record. The failure mode is predictable: duplicate retries, unresolved exceptions, and journal entries posted before the payout is actually final. Your checkpoint is simple: name one source of truth for status, one owner for exception closure, and one evidence pack every team can read.

Conclusion#

If you take one thing from this guide, make it this: do not buy on logo familiarity. Choose based on the spend lane you are actually operating, then prove that lane is controlled before you scale it.

- Map the lane before you pick the tool.

AP automation software is for receiving, approving, and paying supplier invoices. High volume payout infrastructure is built for sending large numbers of external disbursements to payee networks. The real difference is the operating shape: if your work looks like invoice governance, use AP tooling; if it looks like recurring creator, contractor, or marketplace payouts, treat it as payout infrastructure, especially once you are nearing 1,000+ monthly payments, where published guidance says manual and traditional AP approaches start to fall short.

- Treat compliance gates as release controls, not paperwork.

A payout operation is not ready just because funds can move. Your go live threshold should include identity and AML checks that are enforced before release, because compliance is part of core operating control, not an optional add on. The test is enforcement: if KYC, KYB, or AML decisions sit outside the payout decision and someone can still push money out manually, you have not really controlled the lane.

- Insist on replay-safe execution, not vague promises about reliability.

At payout scale, retries are normal. What matters is whether the same request can be retried without accidentally creating a second disbursement, which is exactly what idempotency is for. The proof is concrete: ask the vendor to retry the same payout request with the same idempotency key and show that only one operation occurs. If they cannot demonstrate that behavior, or they will not document what happens on timeout, partial failure, or reversal, pause the rollout.

- Scale only when one payout is traceable end to end.

The final test is not a polished demo. It is whether you can trace a single payment from source event to approval record, payout status history, provider or bank reference, settlement, and posted GL entries in Intacct or NetSuite. The deciding evidence is reconciliation: accounting reconciliation is the act of comparing records for consistency, and bank reconciliation ties payout records back to actual deposits and cash movement. If finance and engineering cannot agree on that chain of evidence, growth will expose the gap fast.

That is the real decision rule behind how addressable spend platforms automate high-volume payouts. Use the comparison and checklist sections to narrow the model, confirm unknowns early, and only expand after your payout loop is traceable, replay-safe, and reviewable by finance without guesswork.

Frequently Asked Questions

What is addressable spend in a platform payout operation?

Addressable spend is the controllable subset of total spend that your team can actively influence. In payout operations, that usually means disbursements where you can set release rules, collect required payee data, and trace the payment into finance records. The dividing line is control, not just dollar volume.

How is addressable spend different from total spend and tail-end spend?

Total spend is everything the business pays. Addressable spend is only the portion procurement, finance, or ops can actually manage. Tail-end spend is usually the small, fragmented end of spend categories; some of it may be addressable, but the real test is whether you can standardize controls and evidence on it.

When should we use AP automation instead of payout-first infrastructure?

Use AP automation when the job is invoice to pay: capture invoices, route approvals, and remove manual entry from accounts payable. Shift toward payout-first infrastructure when you are sending recurring external disbursements at scale, especially once you approach 1,000+ monthly payments, where published guidance says manual and traditional AP-only approaches start to fall short. The real question is whether you are managing invoices or operating a payout network.

What must be automated first when marketplace payout volume spikes?

Automate payee gating and replay-safe payout execution first. That means identity checks before release, then idempotent request handling so a retry does not create a second payout if the first request timed out. Your checkpoint is simple: retry the same request with the same idempotency key and confirm only one operation is performed.

What controls are non-negotiable before scaling embedded payouts across countries?

You need risk-based identity procedures that let you form a reasonable belief you know the customer's true identity, plus the right tax-document collection for the payee type. In the U.S., that often means Form W-9 for a correct TIN, or Form W-8BEN for a foreign individual establishing foreign status. If you pay nonemployee compensation of $600 or more, you may trigger 1099-NEC reporting, which is generally due by January 31.

What usually breaks first at high payout volume: approvals, retries, compliance, or reconciliation?

Do not assume there is one universal first failure. The evidence here supports a different conclusion: at scale, manual handling and AP-only tooling become insufficient, and the first visible break is usually wherever control is weakest. If you have limited test time, pressure-test retries and reconciliation together, because duplicate operations and unmatched payout records are both expensive to unwind.

How do we validate vendor claims when throughput and batch behavior are not publicly documented?

Ask for proof, not positioning. You want a concrete walkthrough of batch creation, partial failures, reversals, and retry behavior, plus one payout traced end to end through request ID, provider payout reference, settlement batch, and posted GL entries in Intacct or NetSuite. If the vendor will not document unknowns or show replay behavior, treat that as a real buying risk.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/manual/AssessingComplianceWithBSARegulatoryR...trusted

- bsaaml.ffiec.gov/manual/AssessingTheBSAAMLComplianceProgram/01trusted

- csrc.nist.gov/pubs/sp/800/122/finaltrusted

- docs.stripe.com/api/idempotent_requeststrusted

- docs.stripe.com/api/idempotent_requeststrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1022trusted

- fdic.gov/federal-register-publications/modern-treasur...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: