Quick Answer

Choose the route that fixes today’s constraint first: bounded horizontal integration when near-term GTM access is limited, and selective vertical integration when payout and reconciliation dependencies are compressing unit economics. Require a one-page memo with take rate, gross margin, and contribution margin baselines tied to named owners. If approval risk or post-close execution is still unclear under the December 18, 2023 merger guidance context, delay scope expansion.

How Integration Strategy Affects Payment Margin#

For payment platforms, the decision is simple in principle: choose the integration path that protects margin with execution risk your team can carry in the near term, not the one that sounds bigger. That pressure is higher now because, as of September 2025, investors are pushing payments operators for sharper margin discipline.

Use the labels precisely. Horizontal integration means combining with rivals at the same competitive level. Vertical integration means combining firms or assets at different stages of the same supply chain. In payments, that is an operating choice, not a branding choice.

The right path also depends on market conditions, not just product ambition. In payments, system conditions include infrastructure, plus legal and regulatory environments, and cross-border planning has to account for the fact that jurisdictions regulate and supervise PSPs differently. A strategy that looks strong in one market can be hard to execute in another.

So treat this as a judgment call, not a mechanical exercise. Even formal merger guidance warns that mechanical application can mislead, and these sources do not establish a universal winner between horizontal and vertical integration for payment platforms.

This article is meant to help you decide in operator terms. You will get:

- A comparison table focused on value-chain control, integration burden, speed to revenue, and margin path.

- Decision rules for when horizontal expansion is more defensible and when vertical depth is more defensible.

- A pre-commit checklist and an early-phase execution sequence to allocate product and GTM resources with fewer blind spots.

Related reading: 5 AP Principles for High-Growth Platforms That Need Control and Speed.

At a glance comparison for next quarter decisions#

Use horizontal integration when next-quarter GTM speed is the priority and you can keep integration scope tight. Use vertical integration when margin pressure is tied to third-party payout or reconciliation dependencies and your team can carry the added build and operating load.

| Criteria | Horizontal integration | Vertical integration |

|---|---|---|

| Value chain control | Expands at the same stage by combining with peers. Focuses control on a single stage rather than adding supply-chain stages. | Adds ownership across more stages of the supply chain under one company. Usually increases control over how value is created and delivered. |

| Speed to revenue | Can be faster if an acquisition brings existing customers, products, or market access. Timing can slip when approvals or post-close integration expand. | Can be slower at first because revenue impact depends on building capability and stabilizing operations. |

| Integration complexity | M&A integration complexity is high. Leadership, governance, and target-state decisions are critical to capture deal value. | Technical and operational complexity is high in a different way. Webhook event handling, payout operations, and reconciliation become core internal work. |

| Execution risk | Includes deal risk and integration risk. In the US, horizontal M&A has explicit antitrust review exposure under the December 18, 2023 merger guidelines, and multi-jurisdiction approvals may be required before close. | Includes build risk and operating risk. Asynchronous events, market-specific payout timing, and manual payout reconciliation can add finance and support overhead. |

| Take rate path | Can change, but definitions vary by platform and metric naming. | Can change as more stages are handled in-house, but results and metric definitions are company-specific. |

| Gross margin path | Can change, but not necessarily on the same timeline as other margin lines. | Can change, but not necessarily on the same timeline as other margin lines. |

| Contribution margin path | May move differently from take-rate and gross-margin lines during integration. | May move differently from take-rate and gross-margin lines during buildout and stabilization. |

| Implementation burden | M&A requires strong integration leadership, governance, and clear ownership from day one. | Supply-side buildout requires clear ownership for payout flows, event handling, and close-process reconciliation. |

| Best fit now | Better fit when GTM pressure is high and your team can constrain acquisition integration to critical surfaces. | Better fit when recurring margin pressure sits in supply-chain dependencies and your team already handles payment exceptions reliably. |

Before you commit, validate where the first margin movement should show up. On February 18, 2026, a live platform disclosure reported 13.3% net revenue margin, 6.4% gross profit as a percentage of GOV, and 4.7% contribution profit as a percentage of GOV. Those lines can move differently, so do not treat "margin uplift" as one number.

For a step-by-step walkthrough, see Retainer Subscription Billing for Talent Platforms That Protects ARR Margin.

What horizontal and vertical integration actually mean in payments#

In payments, these terms are useful only if you can name the layer you are controlling and the day-to-day work your team will own. Horizontal integration expands at the same value-chain stage. Vertical integration adds control across more stages involved in moving funds, events, and payouts.

Horizontal integration#

Horizontal integration is expansion at the same industry stage, not across multiple stages. In merger guidance, regulators frame horizontal deals as transactions between actual or potential competitors in the same market.

For a payment platform, that can mean expanding at the platform layer rather than taking ownership of additional downstream or upstream payment operations. You may still depend on the same processors, payout providers, and reconciliation setup you run today.

Vertical integration#

Vertical integration means one firm controls more stages of the value chain. In payments, that can mean taking on stages that third parties previously handled, including more direct responsibility for how funds movement and payout operations are executed.

This is where strategy language becomes operating reality. If your model includes accepting funds and transmitting them to another person or location, you may be entering money transmission services territory under 31 CFR 1010.100. That can add formal compliance obligations, including FinCEN MSB registration timelines and AML program requirements. In the UK, authorized PIs and EMIs must meet safeguarding requirements.

The operator test#

The real test is operational, not conceptual. Many payment events are asynchronous. Webhook handling requires accepting, storing, and processing messages. Failed delivery retries can continue for up to 30 days, and payout reconciliation can remain a platform responsibility.

Before you fund either path, require a concrete operating plan: which webhook flows change, who owns payout reconciliation, and what compliance determines about money movement. If those answers are unclear, execution risk is still high.

We covered this in detail in SOC 2 for Payment Platforms: What Your Enterprise Clients Will Ask For.

How each strategy changes margin mechanics#

Horizontal integration often moves distribution first. Vertical integration often targets cost control first. That pattern is useful, but it does not guarantee the margin outcome. If your constraint is customer access, horizontal can make sense despite near-term drag. If your constraint is thin unit economics in the supply chain, vertical can be a stronger thesis, but only if you can carry the added execution load.

Start with a clean margin bridge#

Start with a clean margin bridge, not one blended "margin improvement" number. Split the analysis into:

| Margin line | Definition | Article caution |

|---|---|---|

| Take rate | What you keep relative to payment volume or transaction activity | Definitions vary by platform and metric naming |

| Gross margin | What remains after direct processing and delivery costs | Can change, but not necessarily on the same timeline as other margin lines |

| Contribution margin | What remains after variable and semi-variable costs your company classifies below gross margin | May move differently from take-rate and gross-margin lines |

Public reporting already uses different lenses. PayPal reports transaction margin dollars. Block has reported transaction-based gross profit as a percentage of GPV, including 1.16% in Q2 2023. Before you compare strategies, lock one internal definition set and one baseline period.

Then build a bridge that isolates price, direct payment costs, integration costs, support costs, and compliance or operations additions. If each cost is not mapped to a margin line, you cannot tell whether an apparent gain is real or just shifted lower in the P&L.

Horizontal integration usually lifts reach before margin quality#

In merger terms, horizontal integration combines actual or potential competitors in the same relevant market. In payments, the first upside is often distribution and installed-base expansion. Global Payments described its April 17, 2025 Worldpay transaction in that way.

The margin case usually takes longer to prove. Take rate may stay flat if inherited pricing and concessions remain. Gross margin can dip first because integration creates explicit costs, including disclosed deal and integration-related expenses. Contribution margin can compress further when teams run duplicated systems and operating models during harmonization.

Before you approve the plan, require a dated harmonization plan for pricing, processor relationships, reporting definitions, and ERP mappings. Without that, the market-share case may be credible while the margin case stays speculative.

Vertical integration often targets direct-cost control first#

Vertical integration means controlling more stages of the supply chain. In payments, the margin thesis is strongest when you can point to specific direct cost layers you expect to reduce or control more tightly.

Early effects may appear in direct-cost economics before pricing. Company-specific management commentary around Capital One and Discover explicitly linked vertical integration to stronger margins in a thin-margin business. Treat that as directional evidence, not a universal rule.

The counterweight is execution burden. The same reporting described operating the network as a "very complex, high-stakes activity." Added compliance and operational load can pressure contribution margin even if direct cost per transaction improves. Take rate may not move in the near term unless pricing changes.

Set a stricter verification bar here. Ask for line-item proof of expected direct cost reduction using current invoices, fee schedules, incident logs, and reconciliation exception data.

Knowns and unknowns#

| Margin question | What current evidence supports | What remains unknown |

|---|---|---|

| Horizontal effect on distribution | Horizontal moves are often framed as distribution and installed-base expansion | No verified benchmark delta for take rate, gross margin, or contribution margin after horizontal integration |

| Horizontal near-term cost impact | Integration can create explicit expense drag, including disclosed integration-related expenses | No sourced benchmark for how long harmonization drag typically lasts |

| Vertical effect on cost/control | Vertical integration can strengthen margins in a thin-margin business in company-specific commentary | No generalizable proof of which margin line moves first across payment platforms |

| Vertical execution burden | Vertical integration can be very complex and high-stakes; evidence is mixed rather than one-directional | No verified benchmark quantifying contribution-margin pressure from added operations or compliance |

| Decision certainty | Merger decisions are made with incomplete information | No support here for deterministic margin promises for either path |

The evidence supports direction, not guaranteed deltas. Underwrite horizontal on bounded integration scope. Underwrite vertical on provable cost removal. If you cannot show either with current documents and dates, do not commit to a margin outcome you will not be able to verify later.

If you want a deeper dive, read Maverick Spend in Platforms: How to Stop Off-Contract Contractor Payments Before They Drain Margin.

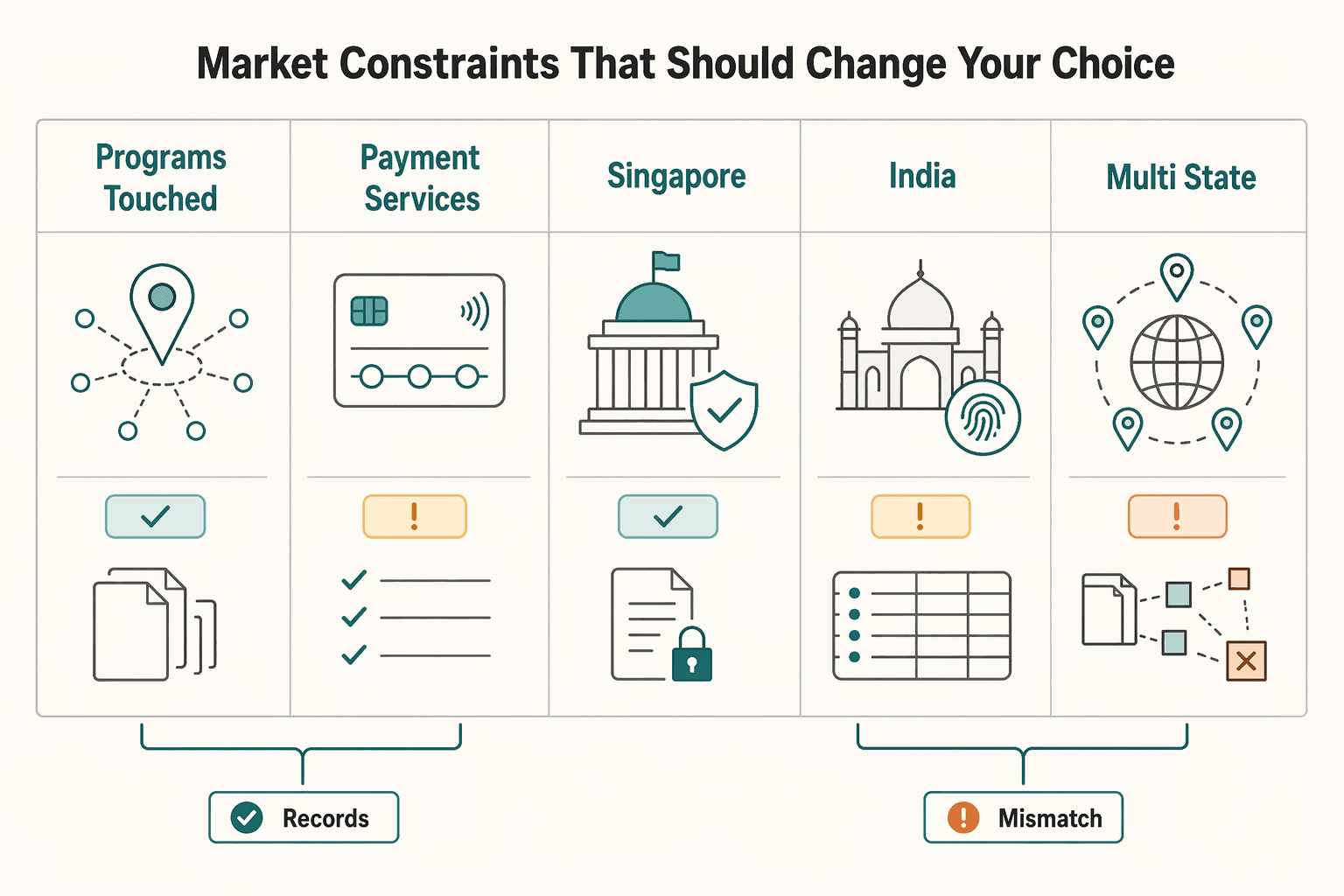

Market constraints that should change your choice#

Start with local reachability, not the strategy label. If regulation, authentication, or resilience obligations are the real gate, headline market-share upside is secondary.

Cross-border payment regulation is still fragmented across jurisdictions for banks and non-banks, and the FSB has flagged legal, regulatory, supervisory, and data-framework frictions in cross-border payments. There is still no complete global supervisory standard for payment-service provision, especially for non-bank PSP oversight. That is why the same strategy can perform differently market by market.

| Market or constraint | What it changes in the choice | What you should verify before GTM spend |

|---|---|---|

| EU programs touched by PSD2 | If launch depends on digital-wallet card enrollment or similar flows, SCA under PSD2 Article 97(1)(c) can be a gate. Horizontal expansion does not remove that gate. | Test the enrollment journey, failure reasons, exemption logic, if any, and ownership of support for authentication failures. |

| UK payment services and e-money activity | UK rules define which payment activities are regulated and who is affected. If important business services cannot stay within tolerance, adding vertical scope can raise execution risk. | Confirm regulated-activity mapping, named operational owners, incident escalation, and ability to operate within resilience tolerances expected after 31 March 2025. |

| Singapore | The Payment Services Act 2019 is the core statute for licensing and regulation of payment service providers and oversight of payment systems. Coverage without a clear licensing-perimeter answer is not real coverage. | Get a written activity map for the planned service, identify the licensed entity or dependency, and check support coverage for exceptions and complaints. |

| India | The RBI Master Direction on Regulation of Payment Aggregator (PA) dated September 15, 2025 indicates a defined authorization and risk-control environment for aggregators. Wrong operating-model assumptions can become costly. | Verify authorization status, ownership of risk controls, and whether phase one needs deep processing changes or only distribution. |

| US multi-state money transmission | Progress is real but not uniform. Thirty-one states have enacted MTMA in full or part, covering 99% of reported money transmission activity tied to licensees in at least one adopting state. Nationwide assumptions can still fail. | Build a state coverage map, identify non-adopting-state gaps, and confirm whether support, compliance, and failure handling vary by state footprint. |

That leads to a practical rule. Choose vertical integration only where owning more of the supply chain removes a repeated, documented bottleneck. The evidence should come from recurring processor exceptions, reconciliation breaks, dependency-driven outages, or repeated policy-gate delays.

Choose horizontal integration when timing and distribution access are the real constraint, and keep phase one tightly bounded. Do not pair customer-base expansion with deep payment-operations rewrites when local policy gates, authentication requirements, or resilience obligations are still unresolved. Before committing campaign spend or sales targets, require a market-by-market readiness pack with:

- regulated-activity and policy-gate mapping for that country or program

- named support owners, coverage hours, and escalation path

- recent failure-handling evidence, including incident logs, exception queues, and service-unavailability records

- a clear phase-one scope and explicit out-of-scope items

Verdict: let local reachability determine sequence. If compliance and banking dependencies dominate, go vertical only for provable bottleneck removal. If access and timing dominate, go horizontal only with bounded integration scope and clear proof that support and failure handling can absorb launch.

Where horizontal expansion fails in practice#

Horizontal expansion often underperforms after close, not at signing. You can buy geography or adjacent capability, but margin protection usually depends on how quickly systems and operating policies converge so duplicate costs do not linger.

That is often a post-merger integration execution problem, not just a deal-selection problem. In payments, two stacks can each work independently yet stall together when APIs, data models, and operating policies do not align. Post-merger integration is complex, and under-addressing technology and data can create near-term business-continuity risk. If integration is treated as side work for already-loaded product, finance, and ops teams, delay is likely.

The convergence problem is usually visible early#

You can usually spot the risk before Day 1 if you request the right artifacts. Ask for the API inventory, sample payloads for high-volume payment events, exception and retry logic, and current ERP finance mapping. Then compare settlement timing, refund handling, reserve logic, dispute ownership, support escalation, and cut-off rules. If those differ, revenue can be additive on paper while operations stay split.

The data layer is where costs can compound. Without a plan for a common schema, reporting and reconciliation can stay duplicated and consolidation decisions slip. You do not need full Day 1 unification, but you do need a clear target-state architecture and a named owner for how data gets there.

The hidden cost layers that hit contribution margin#

Post-close drag usually tracks the degree of change more than headline deal size. That is why margin erosion can come from "temporary" integration layers that never really go away.

| Post-close issue | What it can look like in practice | How it can erode contribution margin | What you should verify |

|---|---|---|---|

| API and data-model mismatch | Separate adapters, manual transforms, duplicated reporting logic | More engineering support and slower consolidation | API inventory, event samples, field mapping, top exception paths |

| Duplicated tooling | Two monitoring stacks, two ticket queues, two reconciliation tools | Ongoing software spend and duplicated operator effort | Tool overlap list, contract end dates, consolidation sequence |

| Duplicated workflows | Different refund, dispute, onboarding, and incident paths | More support effort and slower resolution | SOP comparison, queue volumes, escalation ownership |

| Delayed ERP harmonization | Manual journal mapping, separate close calendars, custom exports | Longer close cycles, more finance effort, weaker performance visibility | ERP dependency map, chart-of-accounts mapping, named harmonization owner |

| Weak integration governance | Decisions made ad hoc by functional leaders | Priority drift, rework, missed synergies | Tech IMO or equivalent, decision rights, weekly issue cadence |

In payments, this can get worse when integration attention is already crowded out by regulatory or data-standard work. If either side is in the middle of those changes, plan for post-close integration capacity to be lower than the deal deck implies.

Founder red flags before you approve the plan#

Before you approve the plan, watch for founder red flags. If you see any two of these together, treat it as a signal to narrow scope and reprice the integration burden:

| Red flag | What is missing |

|---|---|

| No target-state architecture | Written plan for API, data, and operating-policy convergence |

| No ERP harmonization owner | Single owner for post-merger ERP harmonization and finance mapping |

| No Tech IMO | Clear decision rights |

| No duplicate-tooling evidence pack | Contract end dates and shutdown order |

| No policy-difference log | Recorded differences for disputes, refunds, reserves, and support escalation |

Do not fund broad horizontal expansion until the convergence path is explicit, not just the commercial upside. If architecture is still vague, keep the thesis narrow, preserve partial separation where needed, and make finance integration an early requirement. If you need a deeper finance check, use this ERP integration architecture guide. For the webhook side, read Webhook Payment Automation for Platforms: Production-Safe Vendor Criteria.

Where vertical integration backfires operationally#

Vertical integration backfires when operational control expands faster than event discipline. Owning more of the value chain can improve control, but it also creates more points where API responses, webhooks, payout state, and monitoring can conflict.

This failure mode can appear inside your own stack because you now own more execution paths end to end.

More control means more execution risk#

As you move deeper into collection, orchestration, or payout integration, you inherit more asynchronous outcomes across providers and internal systems. Adyen notes many flows are asynchronous, and Stripe documents that most event types are asynchronous while some require a response path.

So an API success response is not enough on its own. Your webhook handling, storage, retry logic, and monitoring all have to agree on final state. If they do not, downstream systems can drift out of sync and leave finance and support with conflicting records.

| Area you deepen | Control you gain | Operational burden that grows | What to verify first |

|---|---|---|---|

| API request handling | More direct control over payment and payout actions | Retry safety and duplicate-action risk | Idempotency design, including key retention rules, for example Adyen's minimum 7-day validity window |

| Webhook processing | Faster event-driven updates | Duplicate deliveries, failed acknowledgements, backlog recovery | Ability to return 2xx, store first, then process, as Adyen requires |

| Payout integration | Better visibility into fund movement | Matching bank payouts to transaction batches and settlement activity | Reconciliation evidence, exception ownership, bank-to-ledger matching rules |

| Incident response | More direct control during failures | More branches to triage and contain | An immediately practical incident response plan |

Payout integration is where finance feels failures first#

Payout integration is where vertical-scope failures usually become visible to finance. Finance still has to match bank payouts to underlying transaction batches and settlement activity, even when the product flow looks successful.

| Provider | Documented webhook detail | Ops note |

|---|---|---|

| Adyen | Many flows are asynchronous; return 2xx, store first, then process; example idempotency minimum 7-day validity window | Webhook handling, storage, retry logic, and monitoring have to agree on final state |

| Stripe | Most event types are asynchronous; duplicate deliveries can occur; undelivered events are resent for up to three days | Recovery workflow is limited to events from the last 30 days |

| PayPal | Retries non-2xx deliveries up to 25 times over 3 days | Without idempotent handlers and defined exception ownership, reconciliation can degrade into manual recovery |

When webhook endpoints become unstable, retries and duplicate deliveries can quickly increase load. Stripe notes duplicate deliveries can occur, and undelivered events are resent for up to three days. PayPal retries non-2xx deliveries up to 25 times over 3 days. Without idempotent handlers and defined exception ownership, reconciliation can degrade into manual recovery.

Use a go or no-go check before expanding scope: trace recent failed or retried payout events from provider event ID to internal ledger record to bank payout reference. If the trace breaks, do not widen vertical ownership yet.

Event discipline protects close quality#

Weak event discipline does not just create support noise. It can delay reconciliation and reporting. Stripe documents that failed event generation can leave downstream systems out of sync with provider state.

The baseline controls are straightforward: acknowledge with 2xx, store raw events, process idempotently, and maintain a recovery workflow for undelivered events. Stripe's recovery workflow is limited to events from the last 30 days, so delayed cleanup increases risk. Also, not every reconciliation delay is a webhook problem. Finance workflow states can block reconciliation too. Do not expand vertical scope until incident response and reconciliation are already reliable at current volume.

Scenario based recommendation rules founders can use#

If your go or no-go check showed weak operational resilience, do not answer that with a bigger expansion bet. Use bounded horizontal moves when market access is the bottleneck. Use selective vertical moves only when recurring cost or control failures sit inside your own supply chain and current operations are already stable at today's load.

Decision matrix#

| Situation | Typical signal | Recommended move | Verify before you commit |

|---|---|---|---|

| Early stage, small team, high GTM urgency | Reach, channel access, or product adjacency is the constraint, not infrastructure depth | Start with bounded horizontal integration | Keep scope narrow: one product line, one target data model, one accountable integration owner, and a written post-close timeline if acquisition is involved |

| Growth stage, moderate team, medium GTM urgency | Repeated margin drag from controllable processing, orchestration, or payout friction | Prioritize selective vertical integration in one module | Confirm critical operations and incident response are already reliable at current volume |

| Multi-country expansion, larger team, high GTM urgency | Demand exists, but rollout is blocked by country-specific authorization or licensing | Expand horizontally only in markets with evidenced readiness. Avoid broad vertical build that assumes fast approvals | Check the specific gate first: FCA authorisation or registration where relevant, EU national competent authority status, or US NMLS licensing path |

| Any stage, finance already strained | Slow close, manual exceptions, and unowned fit assumptions | Defer broad acquisition activity and broad dual-track expansion | Make ownership, timeline, staffing, and margin assumptions explicit before signing or building further |

Horizontal expansion is most defensible when distribution or market share is the bottleneck, but it is not low risk by default. M&A can expand markets and improve efficiency, yet underperformance is common. If success depends on broad convergence across products, teams, finance processes, and architecture, it is no longer bounded.

Selective vertical integration is most defensible when one module creates repeated operational drag. Sequence matters. Deepen only the module tied to a proven pain point, and only after critical operations are reliable at current load. If critical operations are unstable, deeper ownership can increase integration risk instead of improving outcomes.

Market gates matter more than strategy labels#

If market-entry gates are not evidenced, you do not have an executable expansion plan. In the UK, firms providing payment services or issuing e-money may need FCA authorisation or registration. In the EU, authorisation remains with national competent authorities. In the US, NMLS is the system of record for many non-depository financial services licenses and registrations. As of Feb 26, 2026, thirty-one states had enacted MTMA in full or in part, covering 99% of reported money transmission activity.

Rule: if next-quarter targets depend on new geographies before those gates are confirmed market by market, do not fund a large vertical build on parallel approval assumptions. Take a smaller horizontal step where access is already supportable, or pause until readiness evidence is complete.

When a hybrid path is the right answer#

A hybrid path makes sense when one module needs deeper ownership but distribution expansion is still time-critical. A practical pattern is one vertical lane, for example payout handling, plus one horizontal lane, such as one adjacent product or one new channel, with strict scope boundaries.

Keep one module under vertical expansion, one commercial expansion lane, one accountable leader per lane, and one written margin hypothesis per lane. Do not let hybrid execution become hidden scope creep where finance absorbs post-merger integration and a core stack rewrite at the same time. PMI is complex by definition, and delayed integration staffing can erode expected savings. A six-month delay in selecting nonexecutive talent is associated with double-digit percentage savings losses.

Stop conditions#

Use stop conditions when execution risk rises faster than expected margin recovery:

- Resilience testing under severe but plausible scenarios exceeds your stated tolerance for disruption for a critical operation.

- Critical operations still require manual reconstruction to reconcile key payment flows.

- Market entry depends on unresolved authorisation or licensing status, whether FCA, an EU national competent authority, or US state licensing via NMLS.

- Acquisition value case still relies on vague savings language while integration ownership, staffing, and first post-close milestones remain undefined.

Choose the smallest move that attacks the real bottleneck your current operating discipline can support. If ownership, jurisdiction readiness, or operational resilience is not evidenced, defer the bigger bet.

This pairs well with our guide on How to Build a Float Management Strategy for Marketplace Platforms.

The pre commit evidence checklist#

Use one evidence standard for every option before you commit budget. If you cannot show margin baselines, architecture constraints, operating readiness, and downside assumptions, you are still funding unknowns.

A one-page memo is enough if it is strict. Start with current take rate, gross margin, and contribution margin, then state which assumptions move each line for each option. Define terms clearly. Gross margin is net revenue minus cost of sales, and contribution margin is selling price minus variable cost per unit. Reject vague claims like "efficiency gains" unless the mechanism and owner are explicit.

| Evidence area | What must be shown | Verification checkpoint | Red flag |

|---|---|---|---|

| Margin baseline | Current take rate, gross margin, contribution margin, plus explicit assumptions for each option | Finance can trace baselines to current reporting and identify which cost lines move first | Margin case relies on broad savings language with no line-item owner |

| Architecture | Current ERP dependencies, API inventory, and event-driven sync readiness | Named systems of record, maintained host and deployed API version inventory, and clear producer, router, and consumer boundaries | Unknown API versions, deprecated endpoints, or hidden ERP touchpoints discovered late |

| Operations | Reconciliation capacity, payout exception handling, incident ownership | Proof that payout transactions reconcile to payout batches and internal ledger; named incident commander | Manual reconstruction is still required after failures, or duplicate events are not handled |

| Commercial | GTM timeline, effort sizing, and downside if rollout slips | Cross-functional launch timeline plus schedule with staffing assumptions and slip scenario | Revenue case assumes launch dates without a credible schedule or downside case |

Architecture proof that changes the real answer#

Architecture evidence can be where both horizontal and vertical plans fail. Name every ERP dependency touched by post-change operations, because ERP finance and operations systems should be treated as integration constraints. If you cannot map journal, settlement, payout, or refund flows to current ERP dependencies, do not widen scope.

Your API inventory is a control, not documentation overhead. OWASP flags inventory management in API9:2023. In practice, you need a maintained list of hosts and deployed API versions before integration starts. This is where teams can otherwise discover deprecated versions or exposed debug endpoints late. If event-driven sync is in scope, verify readiness at producer, router, and consumer boundaries, since those components are decoupled and can operate independently.

If helpful, see ERP Integration Architecture for Payment Platforms: Webhooks APIs and Event-Driven Sync Patterns.

Operations proof that finance will trust#

Operations proof should answer one question: can you reconcile and recover from exceptions at current volume without a finance fire drill? For payout integration, test the real reconciliation path, not just happy-path ledger entries. In Stripe-based setups, payout-batch reconciliation reporting is available with automatic payouts enabled, and automatic payouts preserve transaction-to-payout associations. If your plan depends on payout-batch reconciliation, validate that setup before approving expansion.

Exception handling also needs explicit controls. Stripe notes webhook endpoints can receive duplicate events, and undelivered events can be resent for up to three days. Your proof pack should show duplicate-event handling, replay handling, and a named incident commander accountable for payout, refund, and settlement event response.

Commercial proof that survives delay#

Commercial proof should read like an executable plan, not a target statement. A GTM timeline should be a cross-functional coordination artifact with clear responsibilities and deadlines. Pair it with effort sizing backed by credible staffing assumptions, since weak schedules are early signs of budget and delivery risk.

Include a downside case aligned with the spirit of 17 CFR 229.303 on known trends and uncertainties. If launch slips, show expected impact on demand, tooling cost, support load, and the margin line you expect to improve first. If that cannot be stated on one page, hold the decision until the evidence is stronger.

Before you lock the memo, map your assumptions for retries, reconciliation, and status visibility to the implementation details in the Gruv docs.

Execution sequence for the first two quarters#

Use Q1 to lock boundaries and reliability. Let Q2 expand only after payout and reconciliation flows are stable under real-world failures.

| Quarter | Primary objective | Minimum viable work | Verification checkpoint | Red flag |

|---|---|---|---|---|

| Q1 | Lock scope and integration boundaries | Fix in-scope products, countries, and payment flows; limit API and webhook changes to first-release needs | Teams can trace one payment, refund, and payout event end to end with no undocumented handoffs | New modules are added before one core flow is fully mapped |

| Q1 | Align finance operations early | Map ERP posting touchpoints for journals, refunds, payouts, and vendor transactions; where relevant, confirm Dynamics 365 Finance posting setup (including vendor posting profiles) and whether Dual-write is in scope | Finance confirms each transaction type has a defined posting path and owner | ERP mapping starts after integration build has already spread |

| Q2 | Scale payout and reconciliation flows | Expand payout integration and reporting only after current flows reconcile cleanly at live volume | Reconciliation output matches bank movement and internal ledger on recent payout batches | Manual reconstruction is still needed after retries, duplicates, or delayed events |

| Q2 | Expand coverage cautiously | Add countries, payment methods, or modules only after event handling is reliable | Exception queues stay manageable and incident ownership is explicit | Coverage expands while event backlogs or duplicate handling are still unstable |

In Q1, boundary control is the main risk control. For Stripe, most event types are sent asynchronously to webhook endpoints. Duplicate deliveries can happen, and undelivered events can be resent for up to three days. The minimum bar is idempotent handling and replay-safe operations before you widen scope.

Finance mapping belongs early in Q1, not after build starts. If you use Dynamics 365 Finance, confirm posting behavior, including vendor posting profiles, early, and decide whether Dual-write is in scope or explicitly deferred for the first release.

Q2 is for scaling what already reconciles, not broad parallel expansion. If duplicate, delayed, or replayed events still create manual cleanup, pause expansion and stabilize core event-driven sync first.

Related: Microsoft Dynamics 365 for Payment Platforms: Finance Module Setup and Payout Integration Guide.

How to verify the strategy is protecting margin#

Shipped scope is not proof that margin is protected. Verify reliability signals first, then confirm finance outcomes on a fixed cadence. If operational failure rate or integration cycle time worsens, treat that as early margin risk before month-end reporting catches up.

| Signal | Practical proxy | What to verify | Red flag |

|---|---|---|---|

| Operational failure rate | Change fail rate | How many releases required rollback or hotfix work after deployment | Releases continue, but rollback and remediation work keep rising |

| Integration cycle time | Change lead time | Time from committed change to production for integration work | Small payment or payout changes take longer each sprint |

| Fee capture | Take rate | Whether fee revenue as a percentage of transaction value is improving | Take rate rises, but mostly in segments with heavier downstream cost |

| Real margin outcome | Transaction margin (and gross margin, if that is your operating line) | Whether higher fee capture survives transaction expense, transaction and credit losses, and third-party costs | Margin stays flat or falls while delivery effort rises |

Take rate is useful, but it is only one line. In payments, margin can still compress as cost layers, funding-source mix, such as credit versus debit or bank-funded flows, and transaction or credit losses shift. When take rate improves, confirm transaction margin, or your primary margin line, moved with it.

Keep the evidence pack small and specific. Use release logs for rollbacks and hotfixes, current exception counts, and one finance view showing take rate plus your margin line for the exact module, country, or partner you expanded. If you cannot isolate the change set, you cannot credibly attribute the margin result.

Set rollback triggers before launch. A defensible pattern is error-budget-style gating. If the service exceeds its error budget over the preceding four-week window, halt changes and releases except critical fixes. If one incident burns more than 20% of that budget, require a postmortem. If that happens while margin is flat or down for your review window, narrow scope before adding the next country, payment method, or module.

You might also find this useful: How to Build a Currency Reserve Strategy for Marketplace Platforms Operating in Volatile Markets.

Conclusion#

Choose the path that improves margin with execution risk your team can actually carry. In payments, that bar is higher now: growth is expected to slow from 8.8% to 4.0%, performance varies sharply by segment, and investors are pushing for sharper margin discipline. This is not a theoretical horizontal-versus-vertical debate. It is an operating decision you should be able to verify in take rate, gross margin, or contribution margin before complexity outruns benefit.

The practical rule is simple. If your main constraint is distribution, market access, or share at the same layer, a tightly bounded horizontal move can fit. If your constraint is recurring cost, control gaps, or repeated supply-chain bottlenecks, selective vertical expansion can fit. If you cannot name the first margin line you expect to move and the mechanism that moves it, you are not ready to fund either route.

Use the comparison table, scenario rules, and evidence checklist to force one defensible view across product, finance, and operations. That view should cover the current margin baseline, expected movement by option, scope, integration implications, reconciliation ownership, and downside if rollout slips. If finance and operations cannot explain the impact in the same terms, pause and close that gap before committing.

Apply extra caution to acquisition decisions. U.S. merger guidance issued December 18, 2023 is explicit that agencies do not predict merger effects with certainty, and it also notes that in concentrated markets, internal growth rather than acquisition can benefit competition. Combined with post-merger integration complexity and mixed evidence on M&A value outcomes, that is a reason to treat deal-led expansion as risk-based, not automatically faster.

Apply the same discipline to vertical buildout. Owning more of the stack can improve control, but it also increases what you must monitor, reconcile, and support. If core monitoring, exception ownership, or transaction-level reconciliation are still unstable at current volume, adding supply-chain responsibility may be premature.

The practical decision is to pick the option that solves your current bottleneck with the least unproven operational expansion. If evidence is incomplete, delay scope growth and close the unknowns before committing irreversible build or acquisition moves. If country coverage or compliance gates are the deciding factor, confirm rollout constraints early in a focused scoping conversation.

Frequently Asked Questions

Which strategy usually protects margin faster for payment platforms?

There is no universal winner. Horizontal expansion can help when the constraint sits at the same industry stage, while vertical integration can help when margin pressure comes from stages you do not control. Before committing budget, define the exact margin outcome you expect and how you will verify it.

When does horizontal expansion hurt margin instead of helping it?

Horizontal expansion hurts when integration work and deal uncertainty outweigh the upside. It can also raise regulatory risk because horizontal integration can reduce competition, and U.S. merger review is explicitly handled case by case based on law and facts, with guidelines issued December 18, 2023. If approvals or integration quality are uncertain, margin timelines can become less predictable.

When does vertical integration create more operational risk than value?

Vertical integration becomes riskier when you add more payout and event states than your team can reliably operate and reconcile. Payout lifecycles can include initiated, authorised, booked, pending, and failed states, and weak handling of those states creates avoidable operational load. Webhook reliability is not automatic: PayPal may redeliver up to 25 times over 3 days after non-2xx responses, and Adyen can keep failed deliveries in a retry queue for up to 30 days.

How should founders choose by country constraints and market maturity?

Start with country-level capability, not a global availability headline. PayPal payout support is split into 4 levels, and some markets are receive-only for payout users, so send assumptions can fail early. For payment methods, scope by country or region and currency support first, then pick the strategy that removes that specific market constraint.

Can a platform run horizontal and vertical integration at the same time?

Yes, but only with narrow scope and clear ownership. Running both broadly in parallel is not a safe default without explicit operating controls. Keep one path tightly bounded while you validate operational stability and margin impact.

What minimum evidence should be collected before committing product and GTM budget?

There is no single universal checklist threshold, but the evidence must be specific enough to support a go or no-go decision. A practical evidence set includes a country capability map for payouts and payment methods, a clear webhook failure-handling plan, and transaction-level reconciliation visibility for the scope you are changing. If ownership and verification are unclear, delay commitment until they are.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- congress.gov/crs_external_products/LSB/PDF/LSB11027/LSB11...trusted

- eba.europa.eu/publications-and-media/press-releases/eba-cl...trusted

- eba.europa.eu/risk-and-data-analysis/data/registers/paymen...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- eur-lex.europa.eu/EN/legal-content/summary/guidelines-on-the-a...trusted

- federalreserve.gov/supervisionreg/topics/operational-resilience...trusted

- ftc.gov/system/files/documents/public_statements/804...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: