Quick Answer

Start by sequencing five control decisions: supplier activation, high-risk approval gates, exception status ownership, compliance fallback behavior, and audit evidence retention. For a high-growth AP operation, that means validating IRS tax ID, W-8/W-9, and payout eligibility before release, then applying tighter review to payee changes and first payouts to new destinations. Use one hard checkpoint to confirm readiness: trace a completed payout from approval record to ledger entry and bank reconciliation without relying on chat threads or spreadsheet reconstruction.

Why AP breaks first in high-growth platforms#

AP breaks early because growth turns invoice handling into a control problem. As invoice volume rises and more people join approvals, invoice processing stops being straightforward. It becomes a series of decisions about who can be paid, when, which checks must happen first, and how you prove the payment was valid after the fact.

Volume exposes weak spots. Manual, disconnected AP work creates payment errors, missed discounts, fraud risk, and vendor strain. High invoice counts and multi-person approvals also open the door to mistakes, duplicate payments, and unauthorized transactions. In practice, teams often do not feel the full impact until an audit, a cash flow issue, or a vendor dispute forces someone to reconstruct what happened.

The terms that matter#

For this article, internal controls means the policy rules and approval gates that govern how invoices are received, reviewed, approved, and paid. They are not just finance paperwork. They are the checkpoints that can stop an unapproved invoice or duplicate payment before money moves.

A platform AP operating model is the full path from purchase orders and invoice receipt through approvals, payment, and reconciliation. Traditional full-cycle AP already covers purchase orders, invoice receipt, approvals, payment, and reconciliation. Core steps often include three-way matching, approvals, and general-ledger integration. On a high-growth platform, that same core usually means more handoffs and more exception handling across teams.

A simple early checkpoint works well. Can your team trace one payment from supplier record to approval, payment outcome, and ledger entry without stitching together spreadsheets and chat messages? If not, growth will usually widen the gap faster than headcount can absorb it.

What this article will help you decide#

This article is meant to help you make operating decisions, not just absorb theory. The next sections lay out five principles with clear tradeoffs, common failure modes, and implementation checkpoints that finance, ops, product, and engineering owners can use. The point is not to tell you to "automate AP" in the abstract. It is to help you decide where control belongs, where speed matters, and where a missing check will create expensive cleanup later.

One boundary matters from the start. These examples are operational and are not jurisdiction-specific compliance determinations. If your team operates across entities or markets, confirm local requirements before launch.

Related: Internal Controls for Accounts Payable on Platforms: How to Prevent Fraud and Ensure Accurate Disbursements. Want a quick next step? Try the free invoice generator.

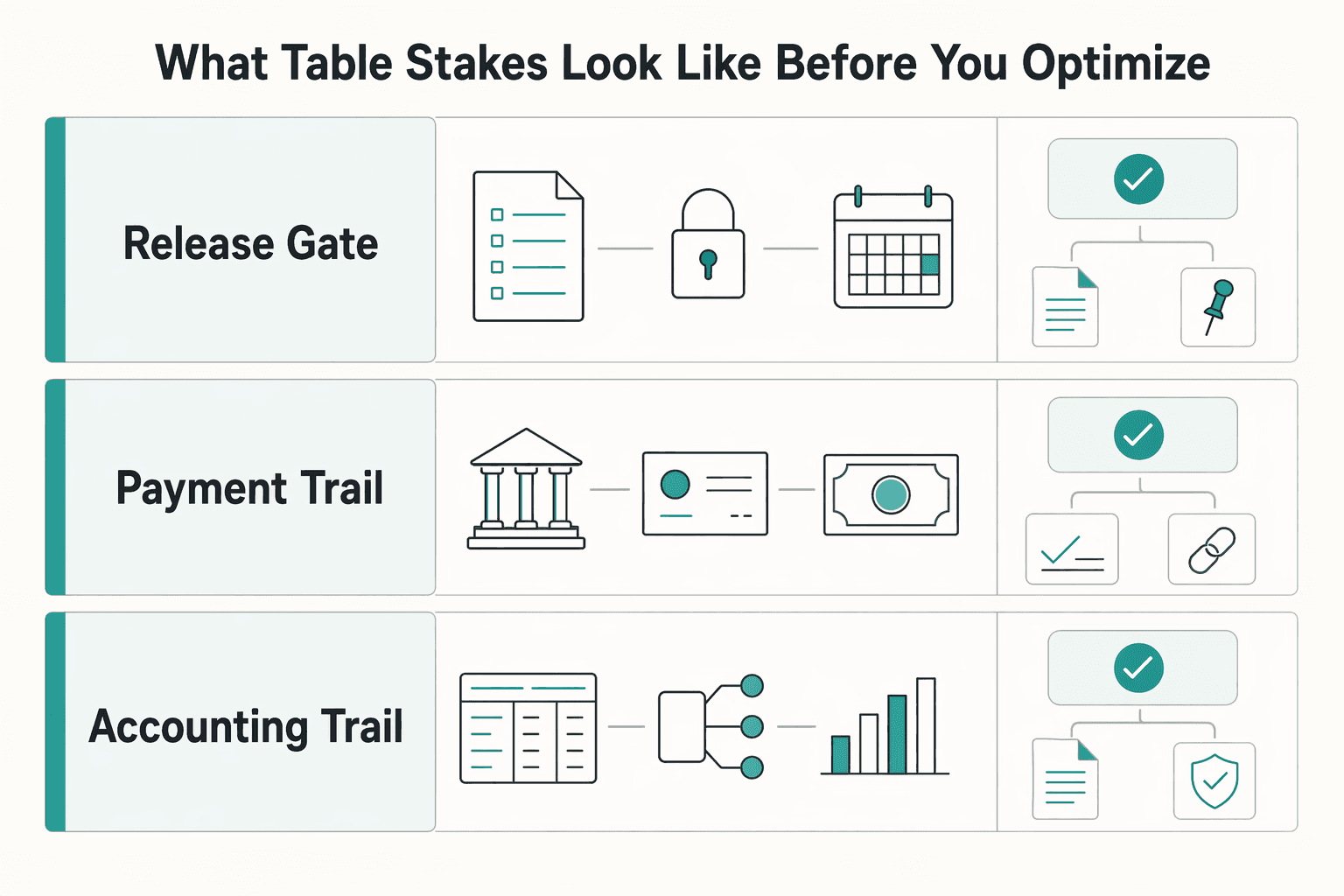

What table stakes look like before you optimize#

Before you optimize, make the foundation repeatable: a clean Chart of Accounts (CoA), clear ownership, connected accounting systems, and monthly bank reconciliation before close.

| Trail | What to confirm |

|---|---|

| Approval trail | who approved, when, and for what obligation |

| Payment trail | payee, amount, reference, and status |

| Accounting trail | CoA posting, export status, and bank-statement alignment |

Basic AP advice often under-delivers for platforms because it focuses on process steps you can see, but not the accounting structure that keeps records trustworthy as volume grows. A well-structured CoA gives each transaction a specific account home, and connecting that structure to accounting software or ERP reduces manual work and errors. Early governance also matters: regular reviews, consistent communication, and clear documentation are what protect data integrity over time.

Use a quick self-check before scaling payout batches: can you trace one completed payout from approval to accounting export and bank reconciliation without stitching together spreadsheets or chat history? Check the approval trail, payment trail, and accounting trail. If that trace breaks at any point, fix that control first and optimize second.

For a step-by-step walkthrough, see Accounts Payable vs Accounts Receivable for Freelancers.

The 5 guiding principles and the tradeoffs behind each#

As volume and exception rates rise, standardize early where errors compound, and stay flexible only where the business truly needs it.

| Principle | Focus | Tradeoff |

|---|---|---|

| Standardize supplier identity and activation early | Collect a consistent legal-entity profile, and run IRS tax ID and VAT checks where they apply before payout activation | Onboarding friction now versus remediation debt later from payout failures, tax-document cleanup, and duplicate records |

| Place internal controls only at high-risk moments | Focus review gates on approval rights, payee changes, and final release, and assign clear owners for each control point | Loss exposure if controls are too light versus queue delays if controls are too heavy |

| Design cross-border money movement for exceptions, not just happy paths | Define the statuses your teams actually use for cases like holds, returns, or investigations, and assign who acts next | More upfront product and engineering effort versus downstream support and reconciliation chaos |

| Treat compliance checks as product logic with fallback behavior | For checks such as KYC, KYB, AML, and OFAC, decide in advance what the platform does when checks fail or stay pending, who is notified, and what evidence is retained | Implementation complexity versus inconsistent handling across support, ops, and finance |

| Make traceability non-negotiable | Your record should connect the operational event, the control event, and the accounting effect so one payout can be explained end to end | Heavier recordkeeping now versus expensive reconstruction later during disputes, diligence, or audits |

- Standardize supplier identity and activation early.

Collect a consistent legal-entity profile, and run IRS tax ID and VAT checks where they apply before payout activation. You are trading some onboarding friction now for less remediation debt later from payout failures, tax-document cleanup, and duplicate records.

- Place internal controls only at high-risk moments.

Focus review gates on approval rights, payee changes, and final release, and assign clear owners for each control point. The tradeoff is loss exposure if controls are too light versus queue delays if controls are too heavy. IRS IRM 1.33.4's explicit focus on "Funds Control Responsibilities" and "Program Controls" is a useful model: controls work when ownership is named.

- Design cross-border money movement for exceptions, not just happy paths.

Define the statuses your teams actually use for cases like holds, returns, or investigations, and assign who acts next. The tradeoff is more upfront product and engineering effort versus downstream support and reconciliation chaos.

- Treat compliance checks as product logic with fallback behavior.

For checks such as KYC, KYB, AML, and OFAC, decide in advance what the platform does when checks fail or stay pending, who is notified, and what evidence is retained. The tradeoff is implementation complexity versus inconsistent handling across support, ops, and finance.

- Make traceability non-negotiable.

Your record should connect the operational event, the control event, and the accounting effect so one payout can be explained end to end. The tradeoff is heavier recordkeeping now versus expensive reconstruction later during disputes, diligence, or audits. The IRS 2025 financial report's "Analysis of Systems, Controls, and Legal Compliance" is a clear example of this control posture.

If one payout cannot be supported with its approval trail, payee history, status history, and accounting impact, pause added complexity and fix that first.

Related: The Best High-Interest Checking Accounts for Freelancers.

Decide what to implement now by growth stage#

Treat implementation as a staged plan, not one flat backlog. As platforms move from growth to scaling, the decision rules need to change, and AP controls are usually where that shift shows up first.

| Growth stage | Required controls now | Minimum integrations now | Primary owner | Not yet |

|---|---|---|---|---|

| Early scale | Standard supplier record, approval matrix, payout release gate, basic audit trail, 3-way matching where invoices apply | Supplier intake, approvals, general ledger integration | Finance ops lead | Extra payment methods, custom dashboards, country-by-country exceptions |

| Active expansion | Named owner for exceptions, payee-change review, documented status handling, retained approval history | Early-scale stack plus reliable status visibility for payouts and exceptions | Finance ops + product | FX tuning, long-tail payment rails, partial automation of edge cases |

| Multi-entity complexity | Entity-level approval rights, consistent coding across entities, centralized evidence retention, tighter reconciliation review | Entity-aware ledger mapping and common approval records across entities | Controller or finance lead with engineering partner | Local one-off flows that bypass common records |

Keep your minimum stack anchored to core AP steps that do not disappear as you grow. In the cited full-cycle AP model, approvals, 3-way matching, and general-ledger integration remain core steps; if those are weak, adding breadth usually adds failure points.

If payout volume is rising faster than finance headcount, prioritize the approval matrix and a clean release path before broadening payment-method coverage. Define who can approve what, which events always require review, and how release is recorded so accounting can tie back to it. A practical check is to take one recent payout and verify you can show the supplier record, approval, release decision, and ledger effect without piecing evidence together across multiple teams.

If cross-border expansion is first, prioritize clear intake and eligibility decision rules before FX optimization. The key test is whether ops can quickly explain why a payee is eligible for a given program and market, and point to the supporting record trail.

Keep the Not yet column explicit. Clear deferrals are safer than silent gaps.

If you want a deeper dive, read Finance Automation and Accounts Payable Growth: How Platforms Scale AP Without Scaling Headcount.

Build supplier onboarding that prevents downstream rework#

Treat onboarding as your first payout control, not a separate intake queue. If payout is enabled before identity, tax, and approval records are complete, rework usually shows up at the worst time: first live disbursement, a return, or a support escalation.

Set and document a clear internal sequence for activation. A practical flow is: collect legal entity and beneficiary details, validate tax identifiers and form status (including IRS tax ID and W-8/W-9 where your program requires them, plus VAT details where relevant), run KYC/KYB checks, then enable payout. Keep status separation explicit: profile created is not the same as payout eligible.

Use a hard gate before money moves#

Use a release gate for incomplete validation. Let a supplier profile exist, but block live disbursement until required checks are complete, with clear statuses such as onboarding in progress and payout eligible.

Define control terms so decisions are defensible. IRS guidance includes explicit sections for Program Controls and Terms/Definitions, and the IRS 2025 agency financial report includes Analysis of Systems, Controls, and Legal Compliance. In practice, your team should be able to define approved, validated, and eligible in one sentence each.

Design for predictable failure modes#

Most downstream cleanup comes from known misses:

- Duplicate supplier entities with slight naming variation.

- Beneficiary name mismatches between onboarding and payout destination.

- Missing or stale W-8/W-9 records.

- Manual overrides that bypass the gate without clear ownership.

Require an evidence pack on each supplier record: validation outcomes, approval timestamps, masked document references, and audit-log links for status changes or overrides. This aligns with the control-first approach used in payment risk management, where internal controls are a core part of the operating model.

Tie onboarding quality to payout reliability reviews. Trace returns, holds, and exception tickets back to onboarding root causes, then tighten the gate before expanding payment reach.

Related reading: How to use 'First Principles Thinking' to solve client problems.

Reduce fraud risk without slowing payouts#

Put tighter controls on the events where loss exposure jumps, and let clean payouts move. In practice, focus on payee change events, the first payout to a new destination, and payout batches that are unusually fast or concentrated for your operation, instead of routing every release through the same manual review.

Once a supplier is valid and payout eligible, the trigger should be the event, not the existence of the payee. Re-approving unchanged, already-cleared payouts adds queue time without much added protection.

Put the gate on the risky event#

Use stronger controls when money-routing details change or risk rises:

| Event | Controls named | If unresolved | If cleared |

|---|---|---|---|

| Payee or bank destination changes after onboarding | OFAC and AML screening, role-based approvals, and an exception path with clear ownership | hold release and route to ops | let it continue automatically without a second manual signoff |

| First live payout to a newly added destination | OFAC and AML screening, role-based approvals, and an exception path with clear ownership | hold release and route to ops | let it continue automatically without a second manual signoff |

| Payout batches that move faster or look more concentrated than normal | OFAC and AML screening, role-based approvals, and an exception path with clear ownership | hold release and route to ops | let it continue automatically without a second manual signoff |

For those events, use layered controls: OFAC and AML screening, role-based approvals, and an exception path with clear ownership. OFAC administers and enforces U.S. sanctions, and prohibitions can vary by program, including blocked-property restrictions, so an unresolved screening state is a release decision, not a cosmetic warning.

Keep the rule set explicit: if screening is unresolved or a risk signal remains open, hold release and route to ops. If the event clears screening and policy checks, let it continue automatically without a second manual signoff.

Keep humans for exceptions, not for everything#

The tradeoff is simple: too many manual checks increase handoffs, delays, and avoidable errors; too few gates increase fraud exposure and recovery burden when payments must be traced, recalled, or written off.

Validate the control at the event level. For a payee change or first payout, one record should show prior destination, new masked destination, screening outcome, approver, timestamp, and any override. If that proof is scattered across chat, tickets, and inboxes, the control is not operationally reliable.

Tune the system with standing reviews rather than widening gates blindly: monitor false positives, review override patterns, and tag failed payouts by root cause so you can separate sanctions or AML holds from beneficiary-data errors, duplicate release attempts, or batch handling mistakes.

Need the full breakdown? Read High-Earners vs. Low-Earners: A Breakdown of Platform Choices for Indian Freelancers.

Make cross-border execution traceable end to end#

For cross-border AP, make traceability a system requirement. Every payout should be reconstructable from invoice confirmation to final ledger reconciliation.

Map one transaction chain and keep a single internal payout ID across each lifecycle event: invoice confirmation, FX quote acceptance (when conversion applies), conversion, disbursement submission, provider status updates, and reconciliation. If a step can occur without writing back to that record, you lose end-to-end visibility.

Align that design with current cross-border interoperability direction. The G20 Roadmap explicitly includes cross-border data exchange and message standards as a work area, and ISO 20022 is widely treated as the go-to format for cross-border payments and reporting. In practice, keep structured provider fields intact instead of collapsing key references into free text.

Pick a traceable path, not just a fast one#

Where supported, choose flow designs that improve inbound and outbound traceability (including virtual-account or merchant-of-record paths when they fit your model). Use them selectively to reduce reconciliation ambiguity, not as a replacement for internal controls.

Apply the same principle to retries: payout submission and webhook handling can be retried operationally, but each business event should map to one accounting outcome in your internal record.

Make status meaning explicit#

Define status semantics and ownership in your own operating model so ops, support, engineering, and finance handle transitions consistently.

| Status | Meaning in your operation | Primary owner |

|---|---|---|

| Pending | Accepted internally, waiting on next processing step | AP or payments ops |

| Held | Paused for review | Risk, compliance, or ops |

| Returned | Sent out and rejected back by provider/receiving side | Payments ops |

| Failed | Could not be processed or submitted successfully | Engineering and ops |

| Settled | Provider completed payout; reconciliation can be finalized | Finance or reconciliation |

For each payout, keep export-ready audit records tied to lifecycle events, including provider references, ledger journal IDs, timestamps, and status history. If one payout cannot be reconstructed cleanly, fix that before expanding to more markets.

Handle GAAP and tax obligations before audit pressure hits#

Audit readiness here is mostly about consistency and evidence. Finance should be able to explain how a payout was recorded and which records supported that decision without rebuilding the story from chat threads.

For day-to-day AP operations, apply the same posting logic to the same fact pattern every time, then keep the supporting trail attached to the transaction. In practice, that means the payout basis, approver identity, approval timestamp, payee record, change history, and final journal reference stay linked in one place.

Turn policy into evidence#

Run a simple spot check on a completed payout:

- What was it?

- Why was it coded that way?

- Which record authorized it?

If those answers depend on tribal memory, your retention and posting discipline are too loose.

Keep tax intake separate from tax advice#

Store tax-document status clearly (for example, which payees have W-8 or W-9 on file, and which payments may feed 1099 workflows), but do not assume one rule set works across every entity or country.

FBAR and FEIE can appear in cross-border operations, but they are not platform-wide shortcuts. The IRS describes FEIE as eligibility-based: for example, one path includes a foreign tax home and physical presence in foreign countries for 330 full days during any 12 consecutive months; those days do not have to be consecutive, and income excluded under FEIE is still reported on a U.S. tax return. Coverage varies by jurisdiction, program design, and entity structure, so confirm obligations with legal and tax advisors before hard-coding collection or reporting rules.

You might also find this useful: Accounts Payable Audit for Platforms: How to Run a Self-Audit Before Your Investors or Auditors Do.

The next 90 days that will actually de-risk growth#

Over the next quarter, de-risk growth by assigning one accountable owner across finance, ops, and engineering, then sequencing controls before expansion. Shared ownership often leaves gaps between onboarding, release controls, and reconciliation.

Pick one owner and lock scope#

Give one owner a written 90-day scope tied to the five principles from earlier: onboarding, high-risk controls, cross-border exceptions, compliance logic, and auditability. Be explicit about what will not ship yet. If payee-change approvals, payout status definitions, or retained evidence are still inconsistent, new rails or new markets should wait.

Use one practical verification test: can that owner walk a single payout end to end without pulling screenshots or email threads from multiple teams? You should be able to see who was onboarded, what approved the payment, which control gates applied, which statuses changed, and what finally posted.

Ship the control baseline before coverage#

Ship a plain control baseline first, then expand coverage. Start with internal controls for payee changes, first payout to a new destination, and payment execution, then stabilize exception handling before adding countries or payout methods.

That order aligns with how OCC payment-systems guidance separates governance areas, including fraud risk, compliance risk, internal controls, and third-party risk management. It is also a reminder that provider dependencies are core risk, not cleanup work for later.

For sanctions-sensitive flows, define coverage and escalation before launch. OFAC has stated in the Venezuela sanctions context that a specific license may still be required even where general licenses exist, so exceptions need a real legal-review stop rather than an ops guess.

Review one monthly pack#

Use one monthly checkpoint pack so recurring issues surface early.

| Checkpoint | What to verify | Red flag |

|---|---|---|

| Supplier onboarding quality | Incomplete tax or identity records, duplicate payees, blocked payout eligibility | Live payouts enabled before onboarding is complete |

| Control overrides | Who overrode approval or screening gates, why, and what evidence was retained | Repeat overrides by the same role with no review |

| Payout failure taxonomy | Returned, failed, held, duplicate attempt, provider rejected counts with root-cause tags | "Miscellaneous" is your biggest category |

| Reconciliation completeness | Provider reference, approval trail, payout status, and journal linkage for sampled payouts | Exceptions sitting open with no named owner |

Practical next step: confirm market and program coverage first, especially where third parties or sanctions exceptions can change the path. Then review docs or demo the modules you can enable now, and defer nice-to-have expansion until traceability is stable.

This pairs well with our guide on The Best High-Yield Savings Accounts for Freelancers.

Frequently Asked Questions

What are the five guiding AP principles for a high-growth platform?

The grounding for this section does not define five platform-specific AP principles. It does support a clear control foundation: standardize and document the workflow, implement strong internal controls, and run AP across three sequential categories, obligation to pay, data entry into the system, and payment execution. Together, those practices help balance speed, fraud risk, and audit readiness.

What is table stakes in platform AP versus a real differentiator?

Table stakes are the basics of a documented workflow and strong internal controls. A real differentiator is maintaining those controls consistently when volume and exceptions increase, especially under time pressure. That consistency is what helps reduce duplicate payments, fraud risk, compliance gaps, and human error.

What should we implement first when headcount is flat but payout volume is climbing?

Start with standardization and internal controls before adding complexity. In practice, document the AP workflow and enforce checks and balances across obligation, system entry, and payment execution. The red flag is bypassing review to move faster, because rushing AP can increase duplicate-payment risk.

How do we lower fraud risk without delaying legitimate payouts?

Use checks and balances at each AP stage rather than relying on one final review step. Keep controls strong in obligation, data entry, and payment execution, and supervise performance continuously so controls stay effective as volume changes. This approach helps reduce fraud risk without adding unnecessary manual friction that can introduce new errors.

How does GAAP relevance change for a platform operating across multiple markets?

These sources do not establish GAAP or jurisdiction-specific accounting requirements. What they do support is consistent control discipline and documentation across the AP process so decisions remain auditable as operations scale.

Which controls belong in product logic versus finance operations?

The sources here do not prescribe ownership by team. They do indicate that AP controls must be clear across obligation to pay, system entry, and payment execution, with a standardized workflow and strong internal controls. Whatever the ownership model, continuous supervision is needed to keep performance and audit readiness intact.

What evidence should we keep so investors or auditors can verify AP decisions quickly?

Keep records that show the full AP control path: the obligation to pay, what was entered into the system, and how payment was executed under documented controls. Maintain enough workflow and review history that a later audit can verify decisions without relying on memory alone.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Platform Teams Scale AP Volume Without Adding Headcount

Use this as a decision list for operators scaling Accounts Payable, not a generic AP automation explainer. In these case-study examples, invoice volume can grow faster than AP headcount when the platform fit is right, but vendor claims still need hard validation.

Internal Controls for AP Platforms to Prevent Fraudulent Disbursements

Start here: your AP control design should reduce fraudulent disbursements and payment errors without turning every payout into a bureaucratic exercise. In practice, that means clear escalation points at the moments where money can move incorrectly, not extra approvals added just to look controlled.

Run an AP Self-Audit Your Investors and Auditors Can Verify

**Step 1. Set the bar higher than a clean dashboard.** The goal is not to make AP look organized. It is to run a self-audit that leaves you with an evidence set you can hand to investor due diligence and an external auditor without scrambling to backfill support. Financial due diligence helps investors judge financial integrity, and auditors can only conclude on what they can support with sufficient appropriate audit evidence. If your review ends with "the numbers seem right," you are not done.