Quick Answer

Start with a period-specific AP subledger-to-General Ledger tie-out, then test transactions in order for completeness, accuracy, validity, and cutoff. Require each sample to include the invoice, approval evidence, settlement report reference, journal entry, and reconciliation result. Escalate any broken handoff as a control failure, not a paperwork gap. Re-test after remediation before sharing the file set for investor due diligence or an external auditor request.

What Auditors and Investors Need to See in an AP Self-Audit#

Before you start#

Step 1. Set the bar higher than a clean dashboard. The goal is not to make AP look organized. It is to run a self-audit that leaves you with an evidence set you can hand to investor due diligence and an external auditor without scrambling to backfill support. Financial due diligence helps investors judge financial integrity, and auditors can only conclude on what they can support with sufficient appropriate audit evidence. If your review ends with "the numbers seem right," you are not done.

Accounts Payable (AP) is a short-term liability, often due within 30 to 90 days, but timing pressure is only part of the risk. Risk grows when payment activity scales faster than the evidence around it. A report can show settled payouts and balanced totals while still hiding missing source support, late reconciliations, or period cutoff errors that matter the moment someone asks for proof.

Step 2. Test the places that fail quietly. The surface can look clean while the real control breaks sit in audit trail continuity, reconciliation timing, or cutoff support. Your checkpoint is simple and unforgiving: can you trace a transaction from source document to accounting entry to reported financials, without a gap? If you cannot link the invoice, approval, payment or settlement reference, journal entry, and final balance, treat that as a control issue, not a paperwork issue.

Reconciliation timing matters for the same reason. Monthly reconciliations are a practical minimum because delays make errors harder to isolate and explain later. Cutoff is less forgiving still. To prove liabilities sit in the right period, you need supporting documents such as invoices and receiving reports, not just a posting date in the ledger.

Step 3. Keep the scope on platform AP controls that move money and numbers. This guide is for operators managing AP controls tied to ledgers, settlements, payout execution, and reporting at scale. It is not a full company audit manual. The focus is the chain that starts with an obligation to pay and ends in posted balances and financial reporting, especially where asynchronous events, status changes, or manual adjustments can break continuity.

By the end, you should have three things: a repeatable cycle for self-testing, explicit checkpoints for pass or escalation, and a closeout checklist you can drop into period end. The working rule is straightforward. If any handoff in that chain cannot be proven end to end, do not call the area audit-ready. Rebuild the evidence pack first, then test again.

You might also find this useful: Internal Controls for Accounts Payable on Platforms: How to Prevent Fraud and Ensure Accurate Disbursements.

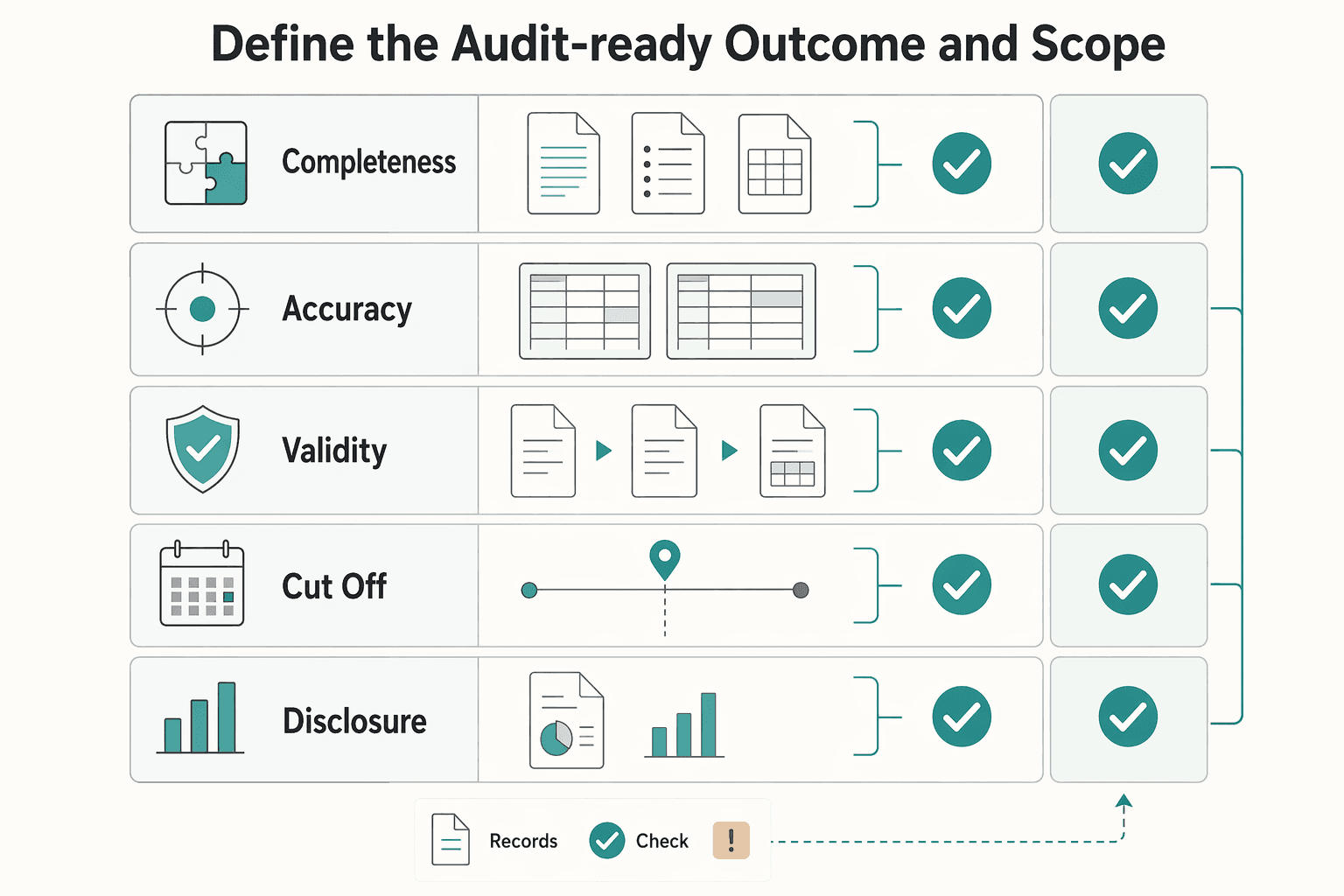

Define the audit-ready outcome and scope#

Before you start sampling, define what "ready" means in a way another reviewer can verify from the file alone.

| Control objective | What it asks |

|---|---|

| Completeness | Whether all liabilities that should be recorded are recorded |

| Accuracy | Whether amounts, dates, and account coding are right |

| Validity | Whether the obligation is real and properly approved |

| Cut-off | Whether transactions are recorded in the correct period |

| Disclosure | Whether reporting is supportable for investors and other capital providers |

Step 1. Define "audit-ready" in evidence terms. Call AP audit-ready only when you can prove three things for a defined accounting period: the AP subledger ties to the General Ledger, sampled invoices trace from source to posting, and the resulting balances support financial reporting prepared for investors, lenders, and other resource providers. Anything less is progress, not readiness. If the subledger-to-GL comparison does not reconcile for that period, stop there and fix that before you expand testing.

Keep one period-specific tie-out file that shows the General Ledger balance, the AP subledger balance, every reconciling item, and the linked source support for each item. If you cannot hand that file to Finance leadership or an external auditor without extra explanation, the area is not audit-ready yet.

Step 2. Draw the system boundary before you test. Decide early which records are authoritative across the AP subledger, payment operations, settlement data, and reporting outputs. In practice, different systems may serve as the authoritative record for the underlying obligation, the payment activity, and the posted accounting result. Write that down before sampling, or you will end up comparing records that were never meant to agree line for line.

A common failure mode is boundary drift. Teams pull screenshots from different tools, but no single evidence chain proves the transaction end to end. For each handoff, name the source of truth and where the retained evidence lives.

Step 3. Set control objectives inside the Internal Control System. Use table-stakes criteria: completeness, accuracy, validity, cut-off, and disclosure. Completeness asks whether all liabilities that should be recorded are recorded. Accuracy asks whether amounts, dates, and account coding are right. Validity asks whether the obligation is real and properly approved. Cut-off asks whether transactions are recorded in the correct period. Disclosure asks whether reporting is supportable for investors and other capital providers. Do not stop at transaction checks alone. Weak approvals, master data, or journal logic can still break the result.

Related: Finance Automation and Accounts Payable Growth: How Platforms Scale AP Without Scaling Headcount.

Prepare prerequisites and ownership before testing starts#

Before you test a single transaction, assign owners and freeze the evidence boundary. If nobody clearly owns a control, an Exception Queue, or the documents behind your Financial Statements, the review will be harder to defend in a self-review, investor diligence, or an external auditor request.

| Prerequisite | Details |

|---|---|

| Owner matrix | List the control, primary owner, backup owner, related Exception Queue, and escalation path |

| Artifact pack | Gather chart of accounts mapping, AP policy documents, prior remediation logs, settlement report exports for the period under review, and representative payout batch files |

| Period and change window | Anchor scope to the most recent fiscal year-end or exact period under review and use separate evidence sets if changes are active |

| Evidence hygiene | Require versioned files, timestamped exports, restricted access, and one retained final copy for each item |

Step 1#

Build a named owner matrix with authority, not just awareness. Management is responsible for establishing and maintaining internal control over financial reporting, so your matrix should show who executes each control, who reviews it, and who can approve fixes when something breaks. Cover Finance, Ops, and Product explicitly, because gaps often show up at the handoff between teams rather than inside one function.

At minimum, list the control, the primary owner, backup owner, related Exception Queue, and escalation path. Use a real exception type to test the matrix, such as a failed payout posting. If the matrix does not tell you who investigates it, who can correct the logic or data, and who signs off that it is closed, ownership is still fuzzy.

Step 2#

Assemble the prerequisite artifact pack before sampling. You are trying to support balances, activity, and disclosures presented in the Financial Statements, so gather the records that explain how amounts move and how prior issues were handled. A practical starter pack might include chart of accounts mapping, AP policy documents, prior remediation logs, settlement report exports for the period under review, and representative payout batch files.

Do not wait until testing to discover that one export is generated differently each week or that a policy changed mid-period without version history. The failure mode here is evidence drift. You pull records later, the fields no longer match, and you cannot prove what existed at the time of posting. Keep a dated index of every artifact you plan to use, with file owner and storage location.

Step 3#

Lock the accounting period and define the change window. If you are testing year-end readiness, anchor the scope to the most recent fiscal year-end or the exact period covered by the balances under review. Then decide whether core posting logic, reconciliation rules, or payout configuration changes are happening during that same window.

If those changes are active, either pause the affected releases for the test period or split the scope into pre-change and post-change populations with separate evidence sets. Change-control discipline matters here. Proposed changes to controlled systems should be reviewed and approved or disapproved. If you mix transactions produced by two different versions of posting logic without marking the cutover date, you contaminate the sample and create avoidable retesting.

Step 4

Set evidence hygiene rules before the first export leaves the source system. Require versioned files, timestamped exports, and restricted access for any artifact that ties directly to Financial Statements. Name one retained final copy for each item, and keep earlier drafts only when they explain a revision.

Close the evidence pack on a defined completion date rather than letting it sprawl. Audit standards use a fixed documentation assembly discipline, with AS 1215 requiring a complete and final set of audit documentation to be assembled for retention within 14 days after report release. You can borrow that rigor even for an internal review. If teams keep replacing files in place, you lose the trail of what was tested, and the whole exercise becomes harder to defend.

If you want a deeper dive, read SOC 2 Type II Certification for Payment Platforms: What Auditors Look For.

Map control points from transaction to ledger posting#

Once your evidence pack is fixed, draw the posting path before you test it. If you cannot prove one transaction from invoice through payment activity into the General Ledger and reconciliation output, treat that control as not operating effectively until the missing evidence is repaired.

Step 1#

Trace the real order of operations, including delayed status changes. Start with what creates the accounting event, not with the ledger entry you hope to see later. In a common AP platform flow, that means documenting the sequence from invoice, approval, payment release, provider response, settlement update, journal creation, transfer to the General Ledger, and final reconciliation closeout.

Do not map only the happy path. Payment and settlement updates can happen asynchronously, outside the immediate payment flow, so your diagram needs separate lines for the initial action and the later event that changes status. That matters because stale status data can be processed after the business event has already moved on, and settlement timing can drift by country and payment method. A two business day interval may be normal in one case and a red flag in another.

Use one paid invoice as a trace test and write down every identifier that should survive each handoff. At minimum, you want a request identifier, the provider reference, the journal entry identifier, and the reconciliation output or match result. If any one of those disappears between teams or tools, your audit trail is broken even if the ending balance looks right.

Step 2#

Build a control matrix that names the owner, evidence, and re-test method. Keep it in a documented procedure or policy set, not just a shared sheet living outside controlled documentation. The point is to show what each control is meant to prevent or detect, who owns it, what evidence proves it ran, what failure looks like, and how you will confirm the fix.

| Control objective | System owner | Evidence artifact | Common failure mode | Re-test method |

|---|---|---|---|---|

| Approved invoices only move to payment release | Finance Ops | Invoice approval log, payment release report | Unapproved invoice released after manual override | Select a sample of released payments and confirm matched approval evidence |

| Each provider event is processed once | Product or Engineering | Event log with processed event IDs, request ID record | Duplicate event delivery causes duplicate posting or duplicate status change | Re-send or inspect a known duplicate event and confirm no second posting occurred |

| Settlement updates post to the correct period and account | Finance Systems | Settlement report export, journal entry, GL posting report | Settlement timing drift causes cutoff error or unmatched recon item | Trace a sample settlement to its journal date and account mapping |

| Exceptions are investigated and closed before close signoff | Finance Ops | Exception Queue export, owner notes, closure proof | Aged unresolved item remains open with no disposition | Re-open the sample queue, verify resolution evidence, and confirm related posting outcome |

A good matrix is specific enough that another operator could re-run the test without asking what file to pull.

Step 3#

Verify end-to-end traceability at every handoff, then flag breakpoints fast. In platform environments, common breakpoints include duplicate webhook-like events, stale statuses from snapshot data, settlement timing drift, and Exception Queue items that never reach a real conclusion. You are not trying to prove that every event arrives in neat order. You are proving that your controls can still prevent or detect misstatements on a timely basis when timing is messy.

Use one sample packet per tested transaction. Put the invoice, approval evidence, payment request, provider request identifier, provider reference, journal entry, and reconciliation result into one chain. If the provider event log shows the request but Finance cannot tie it to a posted journal entry, stop there and mark the handoff failed. If the journal exists but cannot be tied back to the originating invoice or payment request, that is also a failed handoff.

The practical red flag is an unresolved Exception Queue item attached to a posted balance. It may not always mean a material weakness, but it does mean your control evidence is incomplete until the item has an owner, disposition, and closure proof. Under the AS 2201 deficiency idea, a control that cannot prevent or detect timely misstatements in normal operations is deficient. Use that standard for your own judgment before an investor or external auditor does it for you.

For a step-by-step walkthrough, see Accounts Payable Outsourcing for Platforms When and How to Hand Off Your Payables to a Third Party.

Execute core AP self-audit tests in a fixed sequence#

Once the posting path is mapped, keep the test order fixed so a failure tells you where to look next. Use completeness, accuracy, validity, then cutoff testing. That order is a practical operating choice, not a universal rule from one standard, but it keeps re-test work clean.

| Test | Focus | Main evidence |

|---|---|---|

| Completeness | All transactions and accounts that should appear in the financial statements are included | Match invoice, payment, settlement, and journal evidence back to the ledger |

| Accuracy | Amounts, dates, account coding, and period assignment are correct | Compare selected journals to the source invoice, settlement report, and chart of accounts mapping |

| Validity | Transactions are authorized, supported, and not duplicated, fabricated, or posted after an override | Inspect approval evidence, manual override logs, duplicate event handling, and exception closures |

| Cutoff | Liabilities are recorded in the correct accounting period | Review subsequent cash disbursements and invoices received after period end |

Step 1#

Start with completeness, because missing activity makes later checks look cleaner than they are. Under AS 1105, the completeness assertion is whether all transactions and accounts that should appear in the financial statements are included. In AP, that means proving your ledger contains the liabilities and disbursements that should be there, not just that the items already posted look reasonable.

Run two populations in parallel. First, take a sampled population from normal-period AP activity and match invoice, payment, settlement, and journal evidence back to the ledger. Second, run targeted selections for high-value items, high-risk flows, and aged balances sitting in Accrued Liabilities. Aged accrued items matter because they can hide timing breaks, missing reversals, or liabilities that never cleared to the underlying invoice.

The checkpoint is whether each selected item can be tied from source evidence into the posted account and period. If an accrued liability cannot be connected to a supporting invoice, receiving report, or later disbursement, do not call that a documentation gap and move on. Treat it as a potential completeness and liability recognition issue until resolved.

Step 2#

Now move to accuracy and validity. At this point, you know the population is not obviously incomplete, so the next question is whether the transactions are right and whether they should exist at all. Accuracy asks whether amounts, dates, account coding, and period assignment are correct. Validity asks whether the transaction was authorized, supported, and not duplicated, fabricated, or posted after an override that bypassed policy.

For accuracy, compare the amount and account mapping on selected journals to the source invoice, settlement report, and chart of accounts mapping you locked earlier. For validity, inspect approval evidence, manual override logs, duplicate event handling, and any exception closures linked to the item. A common failure mode is a transaction that looks financially correct in amount but is still invalid because it was released without support or because a duplicate provider event drove a second posting.

This is also where targeted testing should get less predictable. PCAOB AS 2301 says the auditor should incorporate an element of unpredictability in procedure selection from year to year, and that is a good self-audit discipline too. If you always pull the same vendor types or the same payment lane, fraud-sensitive control gaps can sit untouched.

Step 3#

Run the cutoff test after the core assertion work, using subsequent disbursements as your main proof point. A practical AP cutoff step is to review subsequent cash disbursements and invoices received after period end, then determine whether the related liability belonged in the closing period. This test can expose items buried in Accrued Liabilities that never should have stayed there.

Anchor the review to post-period cash activity and the supporting invoices or receiving documents behind it. For each selected disbursement, determine whether the underlying obligation related to the period under audit and whether the liability was recorded in the correct accounting period. Where the posting date and the supporting documents disagree, follow the support rather than assuming the ledger timestamp is enough.

If the support shows the liability belonged in a different period, treat it as a cutoff exception and assess it before close. Cutoff is not a cosmetic clean-up step. It is part of proving that liabilities were recognized in the period they relate to.

Build the investor-ready AP closeout packet#

Before a 2025 or 2026 diligence review starts, package the accounts payable file so another reviewer can retest it quickly. The closeout packet should show the exact close period, every open exception, every cleared exception, and the balance a controller or CFO signed off.

Weekly evidence checklist#

Start with the evidence every investor, lender, or external reviewer asks for first.

- A dated AP subledger-to-GL tie-out for the exact close period.

- An aged payables report by vendor, currency, and due-date bucket such as current, 30 days, 60 days, and 90+ days.

- An open Exception Queue export with owner, created date, aging, and planned resolution.

- A vendor master change log covering bank-detail edits, tax-form updates, and approval history.

- A subsequent-disbursement sample pack linking invoice, approval, payment, and posting evidence.

Escalation thresholds for unresolved AP items#

Use explicit monetary and timing thresholds so the team does not improvise under pressure.

- Escalate any unmatched item above 10000 USD, 10000 EUR, or 8000 GBP unless leadership approved a different threshold.

- Escalate duplicate-payment indicators that remain open for more than 2 business days.

- Escalate manual journal overrides tied to AP balances on the same day they are posted.

- Escalate vendor bank-detail changes that bypass maker-checker review.

- Escalate any cutoff exception that changes period expense recognition.

What the investor or auditor file should show#

The review file should answer who approved, what changed, when it changed, and how the final balance was cleared.

- One summary memo naming the tested population, the risk areas, and any unresolved items.

- A reconciliation schedule tying the AP subledger, cash disbursement log, and general ledger.

- Evidence that stale exceptions were cleared, waived, or escalated with approver names.

- A bridge for foreign-currency vendors showing source amount, booked amount, and FX treatment.

- A final sign-off page dated before the board pack, lender update, or 2026 fieldwork window.

Questions to ask before external fieldwork starts#

Use a short challenge list before you claim the file is audit-ready.

- Can a reviewer trace one transaction end to end in under 30 minutes?

- Can finance explain every reconciling item without reopening production systems?

- Are all vendor bank changes supported by approvals and callback controls?

- Do subsequent-disbursement samples prove the right period was charged?

- Is every open exception assigned to one owner and one target date?

AP self-audit FAQ#

These questions help controllers answer the follow-up points investors and auditors usually raise.

How many transactions should we trace before calling the AP file review-ready?#

There is no universal sample size, but the first pass should cover normal volume, unusual vendors, and manual overrides. Many teams start with at least 5 traces, then expand to 10 or more when exceptions cluster around one workflow or one approver.

What is the fastest way to prove the AP subledger matches the general ledger?#

Use one dated reconciliation packet that shows the AP subledger balance, the GL balance, every reconciling item, and the owner for each difference. If that packet cannot be reproduced inside 1 business day, the file is not ready for investor or auditor review.

When does an exception queue item become an investor-level issue?#

Treat it as investor-level when it affects a reported balance, stays unresolved beyond the close calendar, or points to a repeat control failure. A single stale exception is manageable; a pattern across 3 or more similar breaks usually signals a process problem that needs a formal escalation memo.

Should we freeze vendor master changes during AP self-audit week?#

Freeze nonessential vendor master edits during the critical testing window whenever possible. If business operations require a change, route it through an emergency approval path with maker-checker evidence and same-day review.

What should we show when approvers bypass the normal workflow?#

Show the reason for the bypass, the approving authority, the amount involved, and the follow-up control that confirmed the payment was still valid. Reviewers care less about the existence of an override than about whether the override was documented and re-tested.

How do we evidence cutoff testing when payments settle after month-end?#

Anchor the test to the invoice date, receipt evidence, approval timing, and the subsequent cash event. When settlement crosses month-end, show why the liability belonged in the reported period and keep the support in the same packet you use for 2025 and 2026 close reviews.

Frequently Asked Questions

How many transactions should we trace before calling the AP file review-ready?

There is no universal sample size, but the first pass should cover normal volume, unusual vendors, and manual overrides. Many teams start with at least 5 traces, then expand to 10 or more when exceptions cluster around one workflow or one approver.

What is the fastest way to prove the AP subledger matches the general ledger?

Use one dated reconciliation packet that shows the AP subledger balance, the GL balance, every reconciling item, and the owner for each difference. If that packet cannot be reproduced inside 1 business day, the file is not ready for investor or auditor review.

When does an exception queue item become an investor-level issue?

Treat it as investor-level when it affects a reported balance, stays unresolved beyond the close calendar, or points to a repeat control failure. A pattern across 3 or more similar breaks usually signals a process problem that needs a formal escalation memo.

Should we freeze vendor master changes during AP self-audit week?

Freeze nonessential vendor master edits during the critical testing window whenever possible. If business operations require a change, route it through an emergency approval path with maker-checker evidence and same-day review.

What should we show when approvers bypass the normal workflow?

Show the reason for the bypass, the approving authority, the amount involved, and the follow-up control that confirmed the payment was still valid. Reviewers care less about the existence of an override than about whether the override was documented and re-tested.

How do we evidence cutoff testing when payments settle after month-end?

Anchor the test to the invoice date, receipt evidence, approval timing, and the subsequent cash event. When settlement crosses month-end, show why the liability belonged in the reported period and keep the support in the same packet you use for 2025 and 2026 close reviews.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- controller.berkeley.edu/accounting-and-controls/division-key-controlstrusted

- controller.berkeley.edu/accounting-and-controls/internal-controlstrusted

- ecfr.gov/current/title-21/chapter-I/subchapter-A/part...trusted

- guides.gaoinnovations.gov/greenbook/2025/principle-3-establish-structu...trusted

- guides.gaoinnovations.gov/greenbook/2025/principle-12-implement-contro...trusted

- sao.wa.gov/sites/default/files/2023-05/Best-Practices-f...trusted

- sec.gov/rules-regulations/2003/03/managements-report...trusted

- sec.gov/interps/account/sab99.htmtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

What Payment Platform Auditors Actually Test in SOC 2 Type II

If buyers are asking for SOC 2 Type II, the real question is simple: can you show that controls operated over time, with clear scope and clear evidence ownership?

How Platform Teams Scale AP Volume Without Adding Headcount

Use this as a decision list for operators scaling Accounts Payable, not a generic AP automation explainer. In these case-study examples, invoice volume can grow faster than AP headcount when the platform fit is right, but vendor claims still need hard validation.

Internal Controls for AP Platforms to Prevent Fraudulent Disbursements

Start here: your AP control design should reduce fraudulent disbursements and payment errors without turning every payout into a bureaucratic exercise. In practice, that means clear escalation points at the moments where money can move incorrectly, not extra approvals added just to look controlled.