Quick Answer

The best platform choice depends on your invoice size and risk tolerance, not a fixed income cutoff. Build a two-rail "get-paid system": default to bank-transfer rails (Wise or SWIFT) where possible, keep a client-friendly backup (PayPal or card via Stripe), and track your effective fee % per invoice by including fees, FX spread, and deductions. Store a consistent audit packet (invoice, proof-of-receipt, FX record, bank credit) every time.

You're not picking a "best platform"-you're building a get-paid system that doesn't break at the worst time#

Stop searching for the "best platform" and build a two-rail system, with one primary rail and one backup, that protects cashflow, FX, and reversals. As a freelancer, you're running a business of one. Getting paid is a core ops system, not a preference.

Treat the question of "indian freelancer payment platforms by income" as an operations problem: terms, invoicing, payment rail, documentation. One tool won't cover every failure mode.

Design around the failures that show up at the worst time, right before payroll, taxes, or a big vendor bill:

- Payment holds: PayPal explicitly uses holds and reserves to manage risk, and funds can get held for up to 21 days in typical scenarios. That's an operating constraint, not an edge case.

- FX spread hiding inside the rate: PayPal states its conversion rate "includes a currency conversion spread applied and retained by us." If you only compare upfront fees, you miss the real cost.

- SWIFT uncertainty: With SWIFT transfers, correspondent fees can be deducted at any stage of processing, including by intermediaries. You can't fully predict the net amount received unless you plan for it.

- Chargebacks (card rails): Stripe notes a dispute (chargeback) can pull the payment amount plus dispute fees. If you accept cards, you need a dispute-ready workflow.

Your income-based framework (low / mid / high) without fake thresholds#

You don't need a specific INR cutoff to act like an operator. Use invoice size and cashflow fragility:

| Band | Invoice pattern | Rail approach |

|---|---|---|

| Low income / small invoices | Small invoices; optimize for client will actually pay | Keep PayPal as an acceptance rail if clients insist, and pair it with a bank transfer rail (including SWIFT, where relevant) as backup |

| Mid income / mixed invoice sizes | Mixed invoice sizes | Default to bank transfer rails for most clients; keep PayPal as a backup for urgency or client preference |

| High income / large invoices | Large invoices | Default to bank transfer rails first, then add a backup rail; treat card acceptance (Stripe) as an intentional product decision with dispute handling |

Break-even math you can do in 60 seconds#

Run this quick "effective fee" check per client:

- Effective fee % = (All fees + FX spread + expected deductions) ÷ invoice amount.

- If a rail charges fixed-ish costs, like potential SWIFT deductions, it punishes small invoices more.

- If a rail hides cost in FX spread, it punishes every invoice until you price for it.

Verdict: Build a primary rail that fits your typical invoice and risk tolerance. Keep a backup rail your client can use if the first one fails. If you want a deeper FX lens for payment optimization, use Financial Analysis of Foreign Currency Transactions for the Indian Freelancer Economy.

At-a-glance: which platform fits your invoice size + risk tolerance? (quick comparison table)#

Now that you're committing to a two-rail system, use this table to shortlist a primary rail and a sane backup based on invoice size and the failure mode you can tolerate. Think like an operator. You're choosing the FX mechanism, the reversal mechanics, and the compliance friction.

A few definitions to keep you sharp while you scan:

- Mid-market rate is the midpoint between buy and sell prices for a currency (a benchmark). Wise says this is the rate it gives you when you send money to over 140 countries.

- Currency conversion spread is a markup baked into an exchange rate. PayPal explicitly says its rate "includes a currency conversion spread applied and retained by us."

- Correspondent (SWIFT) fees can get deducted during processing by banks in the chain. Wise notes "the correspondent fee can be deducted at any stage of this process."

- Chargebacks (card disputes) reverse the payment. Stripe notes the dispute "immediately reverses the payment" and pulls the payment amount plus dispute fees.

Use the table as a quick filter, then turn it into defaults in the next section.

| Criteria (what actually matters) | Wise | PayPal | Payoneer | SWIFT wire to bank account | Stripe (card checkout) | Upwork (and similar marketplaces) | Skydo / EximPe / Xflow / Razorpay (IN-focused options) |

|---|---|---|---|---|---|---|---|

| Common fit (operator shorthand) | When you care about FX transparency against a benchmark | When a client insists on PayPal | When a client wants this rail | When a client mandates bank wires | When you need card acceptance and can run a dispute workflow | When you're using a marketplace that bundles discovery + payments | Varies by provider; validate capabilities before you depend on it |

| Effective cost drivers | Fees + FX vs mid-market rate benchmark | Fees + FX rate that can include a conversion spread | Cross-border fee (Payoneer says up to 3.5%) plus FX | Sending bank fees + correspondent fees that can be deducted during processing | Processing fees + disputes (which can reverse payments and pull dispute fees) | Platform take-rate (Upwork says 0% to 15% per contract) plus payout/withdrawal costs (where applicable) | Fees + FX + provider/corridor rules. Razorpay claims: "Settle funds in INR within 24 hours, with automated eFIRC for tax compliance." |

| Cashflow reliability (what breaks first) | Timing can depend on bank processing and any account verification steps | Holds. PayPal says holds can last up to 21 days | Documentation requests. Payoneer says account holders may need to submit documentation | Net received can change if fees get deducted mid-chain | Card disputes can reverse funds | Payment collection is handled by the platform; timing and rules vary | Varies by provider and setup |

| Biggest hidden cost | You underprice if you ignore FX and only look at the headline fee | Holds plus FX spread, which may be larger than the visible fee | Compliance friction plus the cross-border fee ceiling | Fee arrangement surprises; fees can get deducted at any stage | Chargebacks; disputes can reverse the payment and pull dispute fees | Service fees that reduce net earnings | Details vary; don't assume fees, settlement timing, or documentation requirements without verifying |

| Risk profile (operator view) | FX benchmark is clear; other operational requirements can still apply | Hold risk (funds availability) | Documentation + cross-border fee exposure | Ops complexity + potential deductions in transit | Dispute risk: disputes can immediately reverse the payment and can pull dispute fees | Margin compression from platform fees | Varies by provider-treat as "verify first," not "set-and-forget" |

| Best "backup rail" role | Strong backup to card and wallet rails | Backup for clients who won't use anything else | Backup if the client already uses it | Backup for clients that mandate wires | Only with strict terms and a tight dispute workflow | Not a backup rail. It is a business model | Potential backup if your primary option is blocked (confirm details first) |

Verdict (safe default): If you're cost-conscious and optimizing for more predictable net receipts where you can, shortlist one bank-transfer-first rail (Wise or SWIFT) plus one client-friendly acceptance rail (PayPal or card via Stripe). Then pick the pair based on which risk you want to eliminate first: FX opacity, holds, correspondent deductions, or chargebacks.

What income band are you in-and what should your default rail + backup rail be?#

Pick your band by operating load, then set one default rail and one backup rail that keep receipts predictable. This turns a shortlist into a weekly system.

Define your band with triggers (not ego)#

Forget monthly totals. Use these operator triggers:

- Invoice count: Do you send a few invoices per month, or dozens?

- Average invoice size: Mostly small tickets, or chunky retainers?

- Audit pressure: How often do you need proof-of-receipt for India work? FIRC (Foreign Inward Remittance Certificate) is a bank-issued proof you received an international payment for export of goods/services. e-FIRA serves the same purpose as proof of foreign payment receipt in electronic form.

- KYC friction: Do you have documents ready before the first receipt? Platforms can start KYC "at the moment of your customer's first transfer," not only at signup.

Safe defaults by operational band (and why)#

Use this as a working decision table. It stays consistent even as clients change.

| Your operational reality | Default rail (optimize for) | Backup rail (optimize for) | Controls to add |

|---|---|---|---|

| Many small invoices | Consider Wise or Payoneer (optimize for fees and FX clarity; Wise is described as popular for low fees and fair exchange rates) | PayPal only when the client insists (PayPal's higher fees can take away a larger share from smaller payments) | Consolidate into fewer invoices when possible. Keep KYC ready (PAN, Aadhaar or passport, plus business docs if applicable). |

| Repeat clients, monthly closes (retainers, predictable billing) | Consider Wise or Payoneer (optimize for repeatability) | Bank wire transfer for clients who only pay wires | Set one billing cadence per client inside your SOW and payment terms. Ask clients to include the invoice number in the transfer reference. Store any remittance advice alongside the invoice. |

| Multiple clients, currencies, exceptions (you spend time "chasing payments") | Account-first workflow (an account-based rail such as Wise/Payoneer where it fits, or your bank process) | Dual rail: one account-based rail plus one wire option | Build a monthly audit pack: invoice + proof-of-receipt (FIRC/e-FIRA or equivalent where available) + payout record. Pre-collect KYC once and reuse it. Share the pack with your CA. |

Verdict: Many Indian freelancers receive international client payments via options like PayPal, Wise, Payoneer, and bank wire transfers, so pick one account-based rail you can run consistently and keep a client-driven backup, often PayPal or a wire transfer. Then lock it into contract language with a simple payment clause inside your MSA. Use this guide for that: How to Write a Master Service Agreement (MSA) for Long-Term Client Engagements.

"Fees" are a trap-what's your effective fee % at $200 vs $10,000?#

Stop comparing "fees" in isolation. Compare your effective fee percentage per invoice, because the winner changes as invoice size changes. Once you do this, "cheap" and "expensive" stop being opinions.

Use one consistent metric (and log it like an operator)#

Payment processors call this concept an effective rate: total fees divided by total sales volume. For Indian freelancers, turn it into a per-invoice habit:

Effective fee % (your ops definition) = total costs you can observe on that payment ÷ invoice amount.

Capture four buckets in your ledger notes, or a simple spreadsheet, every time money lands:

- Platform fees: what the provider charged, or what the client paid if you reimburse.

- FX cost: the gap between a reference exchange rate you track and the rate you actually got.

- Bank and intermediary fees: wires can pick up intermediary bank fees, and those fees may be deducted "along the route," creating a short receipt.

- Withdrawal fees: anything charged to move funds out to your bank.

Operational detail that saves you later: log the invoice number and any reference codes your bank/regulator requires (rules vary by jurisdiction). Store the FX-rate record you used, with timestamp + reference, alongside the payment confirmation for traceability.

Copy/paste scenario table (model $200 to $10,000)#

Use the same columns for every provider you actually use. Fill them with real values from your last 3 payments.

| Scenario | Provider | Stated fee (flat/%/min) | FX spread vs reference rate (estimate) | Withdrawal/receiving fee | Intermediary/SWIFT fee risk | Effective fee % (calc) |

|---|---|---|---|---|---|---|

| $200 | Wise / Payoneer / PayPal / SWIFT | Note min + % | Note rate gap | Note payout fee | For SWIFT: possible deductions | Total ÷ 200 |

| $1,000 | Wise / Payoneer / PayPal / SWIFT | Total ÷ 1,000 | ||||

| $5,000 | Wise / Payoneer / PayPal / SWIFT | Total ÷ 5,000 | ||||

| $10,000 | Wise / Payoneer / PayPal / SWIFT | Total ÷ 10,000 |

Break-even logic (no math heroics):

- Minimum or flat fees punish small invoices. When transactions run small, providers can add a flat fee alongside the percentage, or enforce it as a minimum charge.

- Percentage fees (and FX spreads) punish large invoices. Percentage fees hit harder as amounts rise, and FX spreads can add percentage cost on top of stated transaction fees. PayPal explicitly states its transaction exchange rate "includes a currency conversion spread applied and retained by us." If you can't get transparent FX, treat that rail as a premium, client-driven exception.

Verdict: Your effective fee % becomes your truth. Run this table quarterly, then use the cheapest transparent rail as default and keep the more expensive or less transparent rail as backup only when it prevents a lost deal.

Wise vs PayPal vs Payoneer vs SWIFT: which one breaks least often in real life?#

None of these wins every time. You win by choosing the rail whose failure mode you can diagnose and recover from fastest, without turning it into a week-long support loop.

The reliability comparison that matters: failure modes + recovery path#

When wallets "break," they usually pause the transfer until you finish verification or provide more information.

Wise states it plainly: "We won't be able to send your transfer until we finish verifying you." Payoneer also warns that once you actively start receiving payments, "we may ask you to provide additional information via email."

PayPal goes further into holds and restrictions: "PayPal may place a hold or restrict your account activity if we need a little more information from you about a transaction, your business, or your account activity." Disputes can freeze funds too. PayPal says: "All cases result in a temporary hold on transaction funds."

When SWIFT "breaks," the wire can be rejected during processing because of incorrect or missing details. One explainer puts it like this: "Incorrect or missing information on a foreign wire transfer increases the chance it may be rejected during the funds transfer process."

Your recovery tool here is sender-bank documentation. If details went wrong, the sender's bank can correct them and provide updated proof. For example: "your bank can provide a copy of the amended SWIFT MT103 or PACS008 message."

| Rail | What "breaks" looks like | What you control | What you need to recover fast |

|---|---|---|---|

| Wise | Transfer cannot send until verification finishes | Complete verification early | Identity and business details ready before first invoice |

| PayPal | Holds/restrictions; dispute/claim/chargeback cases create a temporary hold on transaction funds (and PayPal notes some holds may be up to 21 days in rare cases) | Reduce disputes with clear acceptance | Signed SOW, delivery proof, client confirmation trail |

| Payoneer | Requests for additional info after you start receiving | Keep profile consistent and current | Fast response to questionnaires and document requests |

| SWIFT wire | Rejection due to incorrect or missing wire info | Tight wire instructions | Wire confirmation, corrected details, MT103 or PACS008 |

Operator defaults (cost-conscious and resilient)#

- Prebuild a "verification pack" (KYC or KYB basics): ID, address proof, and a one-paragraph description of the services you sell. Do it before you need it.

- If you accept card payments (or PayPal), treat disputes as a system risk. Stripe defines it cleanly: "A dispute (also known as a chargeback) occurs when a cardholder questions your payment with their card issuer." Tighten your scope and sign-off language, and store evidence per client. Use How to Write a Master Service Agreement (MSA) for Long-Term Client Engagements.

- Run two live rails, not one. Keep one wallet-based option (Wise Business or Payoneer) and one bank-wire option (SWIFT). Test both with a small payment before a high-stakes invoice.

Verdict: In the usual Wise vs PayPal debate, and in broader payment optimization, pick the rail with the clearest recovery path for the deal. Then keep a second rail warm so a hold or a rejected wire never turns into a cashflow crisis.

What's the simplest way to make every payment audit-ready in India (FIRC/e-FIRC/e-FIRA) without losing your mind?#

Build a repeatable evidence packet per payment, so your bank, your CA, and your future self can trace one invoice from contract to INR credit fast.

Your audit-ready packet (a practical baseline)#

FIRC is "a certificate issued by a bank as proof of international payment for the export of goods and services." You may also see FIRA in the mix. Wise describes it plainly: "FIRC) or a Foreign Inward Remittance Advice (FIRA) is a document that acts as proof of a foreign transfer to India." (In practice, names and formats can vary by bank.)

Treat those as outputs. Your job is to keep the inputs consistent.

Use a folder per invoice, because it reduces searching, not because any rule forces it. Name it like: ClientName_Invoice123_USD_2026-03. Store:

- Invoice PDF (final version you sent)

- MSA / SOW / PO (whatever governs scope and pricing)

- Payment confirmation (platform receipt, remittance advice, or email from client)

- Any available FX record (platform conversion details, rate, fees)

- Bank credit proof (the statement line item that shows the inward credit)

Then add one file called README_Recon.txt with the platform reference number and the matching bank statement date. That single text file prevents hours of "which receipt matches which credit?"

Purpose Code hygiene + reconciliation mapping (the part that stops back-and-forth)#

Purpose codes matter because "these codes are mandated by the Reserve Bank of India (RBI) to monitor and regulate foreign exchange transactions." Pick the right code with your CA, then keep your service description consistent across the invoice, SOW, and the payment request message.

Consistency doesn't guarantee zero questions, but mismatches do create them.

Run a single reconciliation table for all clients:

| Field | What to record | Example |

|---|---|---|

| Invoice # | Your internal ID | INV-123 |

| Amount/Currency | As invoiced | 2,000 USD |

| Platform ref | Transfer ID (if applicable) | TFR-XXXX |

| Bank statement line | Date + UTR/narration (if available) | 2026-03-18 NEFT/UTR... |

| FX reference | Rate, fees, converted amount | 1 USD = X INR, fee Y |

| Settlement INR | Net INR received | 1,64,000 INR |

Reality check: terminology varies. As one explainer puts it, "Your chartered accountant asks for an FIRC, the bank says they issue FIRA." When that happens, you still win if you can show the trace end-to-end.

Also note that "Payment advice is evidence that a business has received export payments that originated outside India," and Stripe's guidance says: "Present the payment advice to your bank to obtain a Foreign Inward Remittance Certificate (FIRC)."

Read next for the FX math behind payment optimization: Financial Analysis of Foreign Currency Transactions for the Indian Freelancer Economy.

If a payment gets stuck (or reversed), what's the runbook to get it released fast?#

Treat a stuck payment like an ops incident: freeze inputs, assemble a tight evidence packet, then escalate on the correct rail with the correct ID. If you already keep an audit-ready packet per invoice, you're ahead.

Day 0: freeze variables before you escalate (quick, no drama)#

Your goal on Day 0 isn't to solve it. It's to stop new confusion.

- Confirm identity and KYC status on the platform. Wise explicitly says verification usually needs "a photo ID, proof of address, and/or a picture of you holding your ID." If Wise asks for documents, Wise also says review "usually takes around 2 working days." Upload first, escalate second.

- Capture the current state. Save the transaction ID, status text, timestamps, and any remittance advice or transfer confirmation you can download.

- Confirm the client-side send details match what you invoiced. Amount, currency, and recipient details. If anything differs, stop and correct it before you open tickets.

Evidence pack to attach to every ticket (reduces ping-pong)#

Attach a single bundle every time, as a zip or folder link:

- Invoice PDF

- SOW or written acceptance proof (email approval works)

- Client proof of payment initiation (platform confirmation or bank receipt)

- Your bank statement snippet showing missing or partial credit

- If it traveled via SWIFT, ask the client for MT103. Razorpay's explainer states, "An MT103 is a payment instruction that confirms a SWIFT transfer has been initiated."

- If your client's bank mentions a UETR, keep it. Deutsche Bank notes: "All cross border transactions processed via the SWIFT network require a unique identifier called the Unique End-to-End Transaction Reference (UETR)."

Escalation path that actually works (by rail)

| Rail | Start here | What to provide | Next escalation |

|---|---|---|---|

| Wise | Wise support ticket | Transfer ID + what you've already completed for verification + invoice | If verification is pending, complete docs first, then re-open with the same ID |

| PayPal | Resolution Center | Transaction ID + the documents PayPal requests (as listed in the Resolution Center) | If "limited," PayPal says it may ask for documentation "to help us confirm you or your business" |

| SWIFT (bank wire) | Your client | Ask for MT103 and any UETR (if their bank provides it) | Client asks their bank to trace the payment using the available SWIFT tracking references |

| Payoneer | Payoneer support | Transaction reference + any relevant documentation you have | Ask what information or documents they need to move it forward |

Common failure modes and prevention (build once)

- Verification delays: Pre-complete KYC before sending larger amounts (Wise notes it may need additional documents showing how you got the money).

- Proof gaps on digital work: For PayPal disputes on intangible/digital work, keep "compelling evidence" that the item was delivered or the purchase order was fulfilled (deliverable links, handoff emails, timestamps).

- Partial payments: Ban them by default in your MSA unless you schedule milestones explicitly. Use this once: How to Write a Master Service Agreement (MSA) for Long-Term Client Engagements.

Verdict: If money gets sticky and deadlines loom, stop retrying the same method. Move the next invoice to your backup rail immediately, document the change in the client thread, and keep the incident isolated to one transaction.

When should you graduate from "solo tools" to a real money-ops stack (and where does Gruv fit)?#

You graduate when "getting paid" stops being a single action and becomes a repeatable process that needs controls, traceability, and clean reconciliation. The goal is fewer edge-case fires and a faster month-close.

The 3 scaling pain points that signal "ad-hoc" broke#

You don't need a specific revenue milestone to feel this. You'll recognize it by friction:

| Pain point | What it looks like | Why it matters |

|---|---|---|

| Multi-client, multi-currency chaos | You collect via Wise, PayPal, SWIFT, maybe Payoneer, then manually match receipts to invoices and hunt FX rates | Payment reconciliation means matching and comparing transaction records, and accuracy does not scale with copy-paste |

| Recurring compliance questions | Platforms and banks can ask KYB and AML-style questions as part of due diligence | If you answer the same questions across vendors, you are paying the vendor-sprawl tax |

| More hands touching money | A VA sends invoices, a teammate triggers payouts, and you approve in DMs | Separation of duties matters because no individual should perform two consecutive tasks in an accounting procedure |

Those are the common failure points. Here's what each one means in practice:

- Multi-client, multi-currency chaos: You collect via Wise, PayPal, SWIFT, maybe Payoneer, then manually match receipts to invoices and hunt FX rates. Stripe defines payment reconciliation as "matching and comparing transaction records," which is exactly the job you're doing by hand. Accuracy does not scale with copy-paste.

- Recurring compliance questions: Platforms and banks can ask KYB and AML-style questions as part of due diligence. ComplyAdvantage defines KYB as "the process of verifying the ownership of a company and the legitimacy of its activities." If you answer the same questions across vendors, you're paying the vendor-sprawl tax.

- More hands touching money: A VA sends invoices, a teammate triggers payouts, and you approve in DMs. That setup invites mistakes. The OJP internal controls guide puts it bluntly: "Separation of duties is a critical element of internal control, meaning no individual should perform two consecutive tasks in an accounting procedure."

Design the stack as modules (collection, FX, payout, ledger)#

Think in modules so you can swap rails without breaking your books:

| Module | Solo-tool behavior | Money-ops behavior (safe default) | Where Gruv can fit (where supported) |

|---|---|---|---|

| Collection | Each client uses a different rail | Standardize intake via virtual accounts where available | Gruv Virtual Accounts can sit here when enabled |

| FX | Convert whenever, note rates manually | Convert with auditable quotes and references | Gruv can support FX workflows depending on program |

| Payout | One-off sends, no batching | Batch payouts with approvals and status tracking | Gruv Payouts can sit here where enabled |

| Ledger | Spreadsheet as "truth" | A single source of truth tied to invoice IDs | Gruv can help centralize logs and exports |

Controls that reduce risk, not admin work: enforce payout approvals, lock naming conventions (invoice ID as the primary key), and keep an exception queue for held or returned deposits.

If you automate, use idempotent retries. Stripe explains: "A client generates an idempotency key... to recognize subsequent retries of the same request." That approach helps you handle retries without accidentally duplicating work. And when you process webhooks, build for re-deliveries: Stripe notes that when your endpoint receives an already processed event, you should ignore it and return a successful response to stop future retries.

Reconciliation exports (audit-friendly): export a pack that ties each receipt to an invoice, keeps conversion references, and preserves an audit trail of who approved what. Keep it structured enough that you can reuse it for audits and documentation requests (requirements vary). For deeper cost and FX thinking, pair this with Financial Analysis of Foreign Currency Transactions for the Indian Freelancer Economy.

Verdict: Low complexity favors "two rails plus discipline." Higher complexity favors a money-ops stack. Gruv fits when you want an infrastructure approach that reduces vendor sprawl, without pretending one provider solves every corridor or compliance edge case.

Decision checklist: pick your platform(s) in 10 minutes (and reuse it every new client)#

Use this as your default selection workflow. Start with the rail your client can actually send, then optimize for effective cost and risk controls. Finally, store an audit pack you can reuse. This is how you stay consistent as clients and corridors change.

The 10-minute decision flow (copy into Notion)#

1) Client constraints (non-negotiables first) Start with what the client can do, not what you prefer.

| Step | Focus | What to capture |

|---|---|---|

| 1 | Client constraints | Check whether bank transfer is possible, whether the client is card-only, or whether payment must go by SWIFT; for SWIFT, ask for the fee charge code in writing (OUR/SHA/BEN) |

| 2 | Invoice profile | Compute effective fee % per rail: (explicit fee + FX spread + expected deductions) divided by invoice amount |

| 3 | Risk controls | Set partial upfront, milestones, a stop-work clause, acceptance criteria, invoice number in the payment reference, and prepare KYC documents before invoice #1 |

| 4 | Compliance pack | Store invoice, MSA/SOW/NDA, payment confirmation, FX record, bank statement line item, and RBI Purpose Code mapping |

| 5 | Resilience rule | Maintain two rails: a primary and a backup; if feasible, run a small test payment on the backup rail when onboarding a new client or changing bank details |

A few practical notes under that flow:

- Bank transfer possible? If the client can pay by ACH (where available), you can treat it as a bank-to-bank transfer (CFPB defines an ACH transaction as an electronic transfer between banks and credit unions over the Automated Clearing House network).

- Card only? Expect chargeback exposure if you take card payments. Stripe explains that chargebacks function as a consumer protection mechanism for disputes or fraud on card transactions. That should change your terms (see controls below).

- SWIFT only? Ask for the fee charge code in writing (OUR/SHA/BEN). Banks can charge at multiple points (initiating, intermediary, receiving), so you need to control who eats surprise deductions.

2) Invoice profile (what drives effective fee %) You can't optimize "fees" without context. Compute an effective fee % per rail: (explicit fee + FX spread + expected deductions) divided by invoice amount. Flag these:

- Small invoices: fixed charges can dominate.

- Large invoices: FX spread risk dominates.

- Multi-currency: you need clean FX records every time.

3) Risk controls (reduce holds and disputes) Put the controls in your MSA/SOW, not in frantic emails.

- Take partial upfront and bill milestones.

- Add a stop-work clause tied to overdue invoices.

- Write acceptance criteria (what counts as "delivered").

- Require the invoice number in the payment reference.

- Prepare KYC documents before invoice #1 so you don't scramble mid-payment (KYC means verifying identity via baseline identity attributes).

4) Compliance pack (store this every time) Create one folder per client per month:

- Invoice

- MSA/SOW/NDA (as relevant)

- Payment confirmation

- FX record (rate, date, reference)

- Bank statement line item

- RBI Purpose Code mapping (for inbound transfers to India-these codes categorize the reason for an inbound transfer)

If you want a deeper workflow for FX documentation, keep this handy: Financial Analysis of Foreign Currency Transactions for the Indian Freelancer Economy.

5) Resilience rule (no single point of failure) Consider maintaining two rails: a primary and a backup (for example, a platform payout option plus a direct bank wire option). If feasible, run a small test payment on the backup rail when you onboard a new client or change bank details.

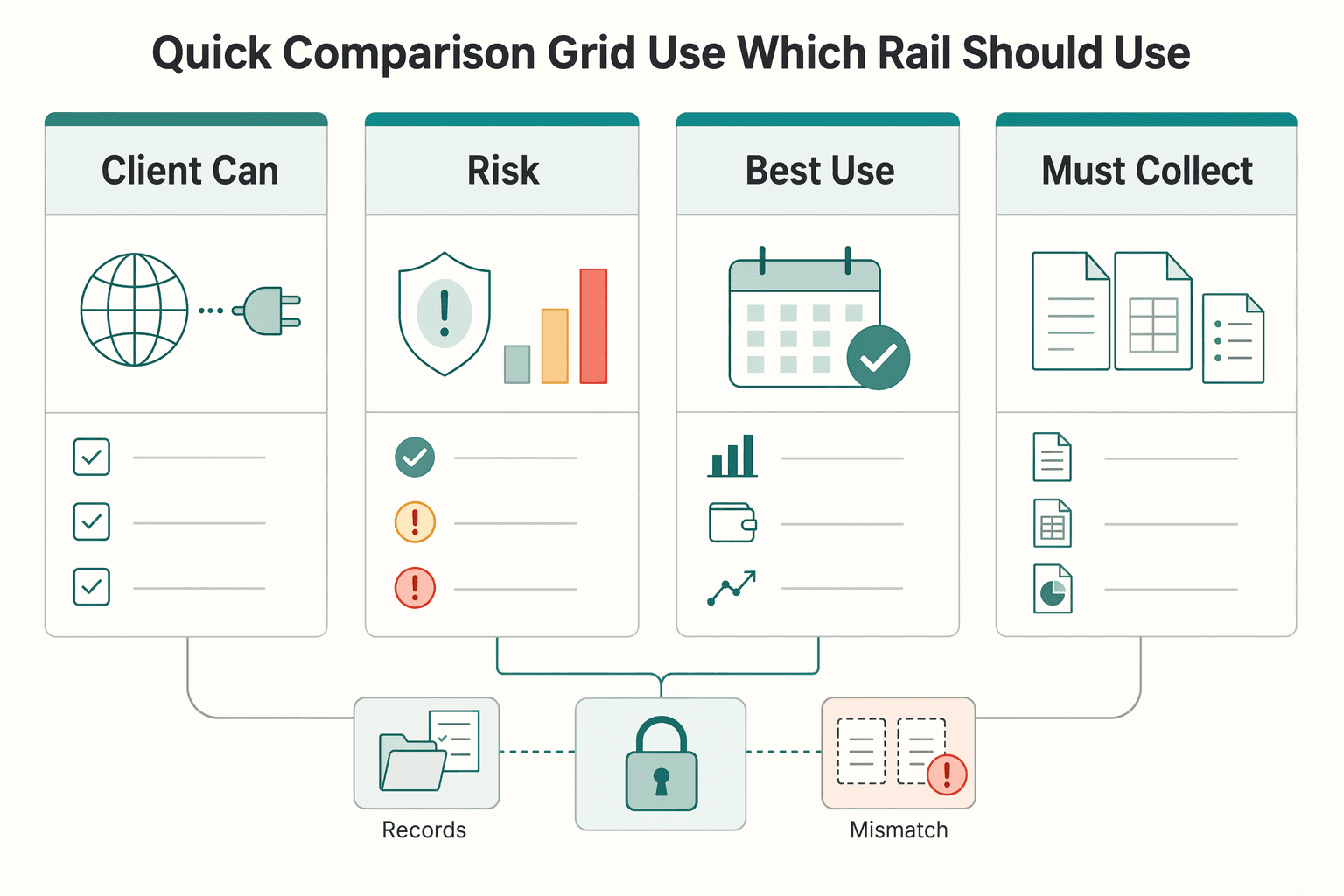

Quick comparison grid (use for "which rail should I use?" decisions)#

| Decision factor | Bank transfer (local rails like ACH, where available) | Card payments | Platform-mediated transfers | SWIFT bank transfer |

|---|---|---|---|---|

| Client can pay via | Bank-to-bank transfer | Card rails | Provider's available transfer routes | Bank-to-bank international wire |

| Main risk to plan for | FX spread plus process variance | Chargebacks and disputes | Compliance checks and process variance | Multi-bank fees and deductions |

| Best use in your system | Bank-rail default when the client can send it | When the client insists on card | When the client already uses the platform | Backup rail and procurement-heavy clients |

| What you must collect | KYC plus FX record | Evidence for disputes | KYC plus payout proof | Fee code (OUR/SHA/BEN) plus payment trace |

Verdict: Pick the rail your client can execute, then choose the option with the lowest effective fee % for your invoice profile. Lock it in with two rails plus one audit pack.

Want a quick next step? Try the free invoice generator.

Conclusion: your safe default is two rails + one audit pack + one fee model#

Your safest default here is not one "best" tool. It's redundancy plus records. You're building a system that still gets you paid when a provider pauses funds or compliance asks questions.

The safe default system (what to standardize)#

Use this table as your standard operating procedure. Keep it boring. Boring gets paid.

| Component | Your rule | Why it survives real life |

|---|---|---|

| Primary rail | Pick the rail you want clients to use most of the time | Consistency reduces reconciliation errors and "where did the money go?" loops |

| Backup rail | Set up a second route you can switch to quickly | Providers can pause access. PayPal calls this "funds availability," and it can delay access to funds; PayPal says funds are usually held for up to 21 days. Wise also says it may suspend an account while it performs a mandatory regulatory compliance check |

| One fee model | Track your "effective fee" per common invoice size using the same method every time | PayPal states its transaction exchange rate includes a currency conversion spread it applies and retains. Wise defines the mid-market rate as what banks and money transfer services use to trade between themselves. Translation: you need a consistent way to see total cost, not just visible fees |

| One audit pack | Store the same proof bundle per payment | Wise describes FIRC/FIRA as proof of a foreign transfer to India. ClearTax describes a FIRC as a bank-issued proof of international payments for exports with remittance details |

Your "audit pack" checklist (copy/paste)#

Create a folder per invoice, then drop in:

- Invoice (PDF) plus your client's PO or SOW reference if you have one.

- Payment proof (platform receipt, bank credit advice, or transfer confirmation).

- FX record (conversion confirmation, rate used, and date).

- FIRC/FIRA (when you obtain it) or any inward remittance advice your bank/platform provides.

- SWIFT specifics (if applicable): capture the MT103 and the "Details of Charges (Field 71A)" where OUR/SHA/BEN can appear.

If you want a deeper lens on payment optimization and FX math, keep one internal reference handy: Financial Analysis of Foreign Currency Transactions for the Indian Freelancer Economy.

Verdict: Run two rails, measure total cost consistently, and file the same audit pack every time. That system scales cleanly as your client mix, invoice sizes, and scrutiny increase.

Frequently Asked Questions

What is the best payment platform for Indian freelancers based on income?

No single tool wins for indian freelancer payment platforms by income. Choose based on two levers: invoice size (effective fee %) and dispute risk. Lower freelance income usually means small invoices where fixed charges hurt, so prioritize a bank-rail option your client can actually send. Higher income usually means larger invoices where FX spread and documentation can matter more than a headline fee.

Wise vs PayPal for Indian freelancers: which is cheaper and safer?

Treat this as payment-rail behavior (and how your client funds the payment), not brand loyalty. PayPal explicitly states that when it performs currency conversion, "the transaction exchange rate will also include a currency conversion spread," so your cost can hide in FX, not just visible fees. Safety also means reversals, since card-linked flows carry chargeback exposure as a consumer protection mechanism for disputes or fraud. If your client insists on PayPal, protect yourself with milestone billing, acceptance criteria, and a clean evidence trail.

How can Indian freelancers reduce international payment fees (FX spread, minimum fees, bank charges)?

Track effective fee % per invoice: (explicit fee + FX spread + deductions) / invoice amount. For SWIFT wires, confirm who pays which fees (often shown as a fee-charge arrangement like OUR/SHA/BEN, depending on the bank) because banks may charge at initiation, intermediary, or receiving points. Avoid unnecessary conversions, convert once, and store the FX record (rate, date, reference) with the invoice.

What documents do I need for foreign remittance receipts in India (FIRC / e-FIRA)?

Start with what banks issue and what you can reliably store. FIRC is "an official document issued by a bank or authorized financial institution in India," and it's commonly used as proof of foreign funds received. e-FIRA stands for "Electronic Foreign Inward Remittance Advice." Also capture your RBI Purpose Code because the referenced guidance presents it as a mandatory identifier for payments received from abroad.

Is PayPal safe for receiving freelance payments in India?

Define "safe" as low reversal risk plus clean records. PayPal can work, but card-style dispute mechanics can reverse funds via chargebacks, so treat every delivery like you may need to prove it. Operationally: signed SOW, acceptance email, dated proof of delivery, and invoice number in the payment reference.

Should I use SWIFT wire transfers or a platform like Wise/Payoneer?

Use SWIFT as a backup rail or when your client requires a wire. SWIFT can surprise you on net received amount because multiple banks may charge fees along the path. If you use a platform, keep your records tight so reconciliation and audits are straightforward.

What's the best way to get paid from US/UK/EU clients in India (ACH vs SWIFT vs card)?

There isn't one universal "best," but here's a practical starting point based on rails and risk: | Client can send | Common starting point | Why it's a reasonable default | |---|---|---| | ACH | Bank transfer route | CFPB defines ACH as an electronic bank-to-bank transfer; it generally avoids card chargeback mechanics | | SWIFT | Wire transfer (backup) | Works broadly, but manage intermediary fee deductions (fee-charge arrangements vary by bank) | | Card | Card only when required | Chargebacks exist as a dispute and fraud mechanism, so tighten terms and evidence |

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- consumerfinance.gov/ask-cfpb/what-is-an-ach-transaction-en-1065trusted

- consumerfinance.gov/ask-cfpb/what-is-an-ach-transaction-en-1065trusted

- oacp.upenn.edu/audit/audit101/internal-controls-guidance/op...trusted

- oacp.upenn.edu/audit/audit101/internal-controls-guidance/op...trusted

- ojp.gov/ovc_fmrc_guide_sheet_internal_control_separa...trusted

- karboncard.com/blog/indian-freelancers-payment-platformsexternal

- xflowpay.com/blog/freelancer-payment-methodsexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Indian Freelancer Payment Analysis That Protects Net INR

For freelancers in India, the number that protects cash flow is the net INR credited to your bank, not the USD amount on the invoice. Start from that outcome and work backward through every payment decision.

How to Use a Nominee Director in an Offshore Company Without Losing Control

Privacy and cleaner operations are valid goals, but control and compliance come first. A structure only helps if authority, approvals, and records are clear enough to survive outside review.

Master Service Agreement for Freelancers in Long-Term Client Engagements

If you expect repeat work with the same client, set the contract architecture first: one reusable MSA for standing terms, then project documents for each engagement. The point is not just speed. It is making sure your baseline terms are set before they repeat across future projects. Treat each document as a separate layer: