Quick Answer

Start by fixing scope and ownership, then choose DAC7 compliance platforms that can prove record lineage from onboarding through payout and export. The article anchors decisions to Council Directive (EU) 2021/514 and stresses evidence quality over feature breadth. It recommends testing legal-entity coverage, validating handling for fields such as TIN and VAT ID, and requiring clear correction workflows. Teams should run an annual checkpoint calendar, escalate unresolved exceptions early, and avoid tool selection until accountability and filing artifacts are explicit.

DAC7 compliance platforms only work when your operating model is clear first#

Start with operating reality, not feature grids. This section is for compliance, legal, finance, and risk owners who need a defensible decision, not a generic explainer. The goal is practical: make a faster scope call, choose an approach that fits your entity and data setup, and get through reporting with fewer surprises.

1. Decide who actually owns the compliance decision#

Set ownership first. You need to know which legal entity owns the reporting obligation, which team can evidence the underlying records, and who approves edge cases when facts are incomplete.

A useful discipline check comes from EU VAT operations. VAT and DAC7 are not the same, but cross-border obligations become entity-specific very quickly. Under OSS, businesses register in one Member State of identification. For VAT Cross Border Rulings, requests are filed in the participating EU country where the requester is VAT-registered. When several group companies are involved, one company files on behalf of the others. Get to that level of entity clarity before you compare tools.

2. Define "working" before procurement#

A platform works only if it reduces unresolved questions at reporting time. In practice, that means faster scope decisions, clear ownership of seller and transaction records, and evidence you can reproduce later without rebuilding the story from raw data.

Use concrete checks. Do you need one reporting owner across multiple EU Member States? Where do source records actually live: product, finance, or payments? What reporting rhythm do you already run? OSS guidance is a useful benchmark for operational discipline because it spans registration, declaration, and payment. It also includes quarterly returns for Union and non-Union schemes and monthly returns for the import scheme. Your tooling should match that operating rhythm and exception load, not just a feature list.

Since 1 July 2021, EU VAT rules for cross-border B2C e-commerce changed, and online marketplaces also face record-keeping requirements beyond deemed-supplier cases. The operational takeaway is simple: obligations expand around records, ownership, and evidence.

3. Treat escalation paths as a hard requirement#

Do not assume you have a clean benchmark for country-by-country DAC7 enforcement exposure or vendor performance. Build escalation paths early, with named owners for borderline scope questions, late data remediation, and specialist review when needed.

Pressure-test lock-in and failure modes before selection. In OSS, choosing a Member State of identification can bind that choice for the current calendar year plus the two following calendar years. A Member State can also exclude a taxable person or intermediary from an OSS scheme. These are VAT examples, but the control lesson carries over. Test governance and exit risk up front.

Before you make a shortlist, assemble a short evidence pack: entity map, registration summary, record-keeping owner, and escalation contacts by function. If that pack does not exist, pause procurement.

If you want a deeper dive, read FATCA Compliance for Marketplace Platforms: Identifying and Reporting Foreign Account Holders.

Selection criteria that separate usable DAC7 tools from marketing claims#

Choose the tooling you can evidence end to end. Feature count is secondary. If you cannot trace the filing pack back to source records, the tool is not usable.

- Legal fit before product breadth

Score tools against your legal interpretation of DAC7 requirements, not feature grids. In vendor walkthroughs, separate what works now, what is configurable, and what still needs legal judgment on your side. Ask vendors to state country-level dependencies plainly. If they cite EU guidance, verify it is on the europa.eu domain.

- Evidence quality over dashboard polish

Prioritize controls you can reproduce: record history, timestamped changes, and exports that can be regenerated from source data. The standard is an audit-ready file, not a clean UI. OSS is a practical benchmark for control completeness because EU materials explicitly cover registration, declaration and payment, and record keeping and audits. If a tool shows only a current-state profile without a change trail, treat that as a control gap.

- Implementation detail for tax-identifier data

Require the actual data model for tax-identifier handling: ownership, validation, null handling, jurisdiction tags, and exception routing. Do not accept screenshots instead of data design. As a concrete OSS example, non-Union onboarding uses an allocated VAT ID format, EUxxxyyyyyz. Treat DAC7 field-level TIN or VAT ID rules as a legal-and-product decision you need to validate directly with your legal and tax advisers.

- Clear filing handoff and ownership

If your operating model depends on one filing authority before onward exchange, require a concrete handoff design for preparation, export, correction, and retention. In OSS, submitted returns and VAT paid are transmitted onward by the Member State of identification through a secure communications network. Confirm DAC7 XML and transmission specifications with your legal and technical advisers. Use OSS as a clarity benchmark, not proof that DAC7 is identical. Exclude tools that cannot assign ownership for final exports, correction history, and late-data handling.

Scope test before procurement so you do not overbuild#

Write the scope memo first. If you cannot explain, for each legal entity, what is in scope and what remains legally unresolved, pause procurement and settle that classification before buying tooling.

- Entity status first

Assess scope at the legal-entity level, not the brand level. Record, for each entity, who onboards sellers, who controls the transaction flow, and who pays out. For OSS planning, confirm which entity will register in one Member State of identification and whether that choice could create lock-in. If answers to DAC7 terms such as "reportable platform operator" or "non-EU platform operator" differ across legal, finance, and product, treat that as an unresolved legal issue requiring a written legal determination.

- Test activity coverage on real transactions

Use production samples to test your scope logic against actual transaction patterns, not demo assumptions. If an entity opts into an OSS scheme, verify that all supplies falling under that scheme are declared via the OSS return from the Member State of identification. If your team uses DAC7 activity labels as a working taxonomy, keep them clearly marked as internal assumptions rather than confirmed scope from these materials.

- Run explicit checks and document the decision trail

For VAT-specific cross-border uncertainty, you can use VAT Cross-Border Rulings (CBR) to seek advance VAT treatment on complex transactions. Submit CBR requests under the national VAT-ruling conditions of the participating country, and when multiple companies are involved, have one company submit on behalf of the others. Keep DAC7-specific exclusion logic and final scope calls marked as unconfirmed here, and do not treat VAT or OSS mechanics as a DAC7 scope determination.

For a step-by-step walkthrough, see How to Build a RegTech Stack for Payment Platforms: Tools and Vendors by Compliance Function.

Best DAC7 compliance platform options by operating model#

Once scope is settled, choose the operating model that gives you defensible records with the least extra process. When comparing DAC7 compliance platforms, prioritize a setup that preserves seller evidence, reconciles to payouts, and works across legal entities without creating a second manual workflow beside your ledger.

| Model | Fits when | Main concern |

|---|---|---|

| DAC7 specialist tax platform | Reporting readiness is the main risk and payout execution is already stable elsewhere | Traceability can weaken when onboarding, payouts, and tax prep sit in separate systems |

| Payout platform with DAC7 module | Payouts are the core system and compliance needs to attach directly to money movement | If payout outcomes are stored with weak supporting history, control quality is thinner than it looks |

| ERP or AP-led compliance add-on | Finance-led organizations with strong back-office controls and moderate seller churn | The common weakness is front-end data capture |

| In-house orchestration with API vendors | Your legal perimeter is unusual and engineering already owns core seller and ledger logic | It gives you maximum ownership for interpretation, monitoring, and yearly updates |

| Hybrid model with managed filing support | Internal compliance capacity is thin and timelines are volatile | The risk is dependency |

There is no universal winner. A practical stress test is your adjacent EU VAT operating reality: OSS can centralize registration in one Member State, and OSS returns are additional filings that do not replace domestic VAT returns. These VAT points are control benchmarks, not DAC7 legal scope, and if a platform choice ignores those control habits, year-end workload can go up.

DAC7 specialist tax platform#

This can be a strong fit when reporting readiness is the main risk and payout execution is already stable elsewhere. You are buying depth in data preparation, validation, and export controls while keeping existing payout rails.

The key test is whether the tool handles records by legal entity and can produce a repeatable filing pack without depending on your payout provider to fill gaps. Run one messy production sample end to end. Check validation results, correction history, final export, and audit trail. If a vendor promises an XML reporting file, verify it as a product feature rather than treating it as proof of legal completeness.

The tradeoff is clear. Reporting discipline can improve, but traceability can weaken when onboarding, payouts, and tax prep sit in separate systems.

Payout platform with DAC7 module#

This can be a practical choice when payouts are the core system and compliance needs to attach directly to money movement. It can simplify execution for high-frequency seller or creator payouts because transaction and payout data already live together.

Your main checkpoint is evidence depth, not feature labels. As a nearby benchmark, VAT workflows may still require record-keeping even when a platform is not treated as the deemed supplier. If your system stores payout outcomes but weak supporting history, control quality is thinner than it looks. Validate by reconciliation, and confirm onboarding status, payout mapping, correction events, and year-end totals remain linked after changes.

ERP or AP-led compliance add-on#

This can fit finance-led organizations with strong back-office controls and moderate seller churn. If finance already owns reconciliations, close calendars, and retention, this route can reduce tool sprawl.

The advantage is control familiarity, especially where teams already handle additive filing obligations. In VAT OSS, for example, OSS returns do not replace domestic VAT returns, and that mindset helps avoid the assumption that one export solves everything.

The common weakness is front-end data capture. Define the evidence pack early: seller master data, payout mapping, transaction classification, correction log, and legal-entity filing outputs.

In-house orchestration with API vendors#

Build-first is usually most relevant when your legal perimeter is unusual and engineering already owns core seller and ledger logic. It gives you maximum control, and it also gives you maximum ownership for interpretation, monitoring, and yearly updates.

The design priority is to keep jurisdiction decisions explicit and reviewable. In VAT OSS, Union-scheme Member State choices can create operational lock-in for the current calendar year plus the next two years, so policy decisions should stay visible rather than buried in service code.

When facts are ambiguous, add a legal checkpoint before automation. For VAT questions, CBR can be requested under national ruling conditions, and where multiple companies are involved one can file on behalf of others.

Hybrid model with managed filing support#

This can be a fast, defensible option when internal compliance capacity is thin and timelines are volatile. You keep part of collection or payout operations in-house and rely on a partner for validation or filing support.

The benefit is speed. The risk is dependency. Define the service boundary in writing: cutoffs, correction handling, evidence retention, and who can reproduce the filing package without the vendor.

If a provider claims transmission readiness, ask for the exact handoff model and the internal artifacts you retain. If that chain is unclear, the control risk still sits with you.

You might also find this useful: FATCA and W-8 Tax Compliance for Platforms: When to Release, Hold, or Withhold Foreign Payouts.

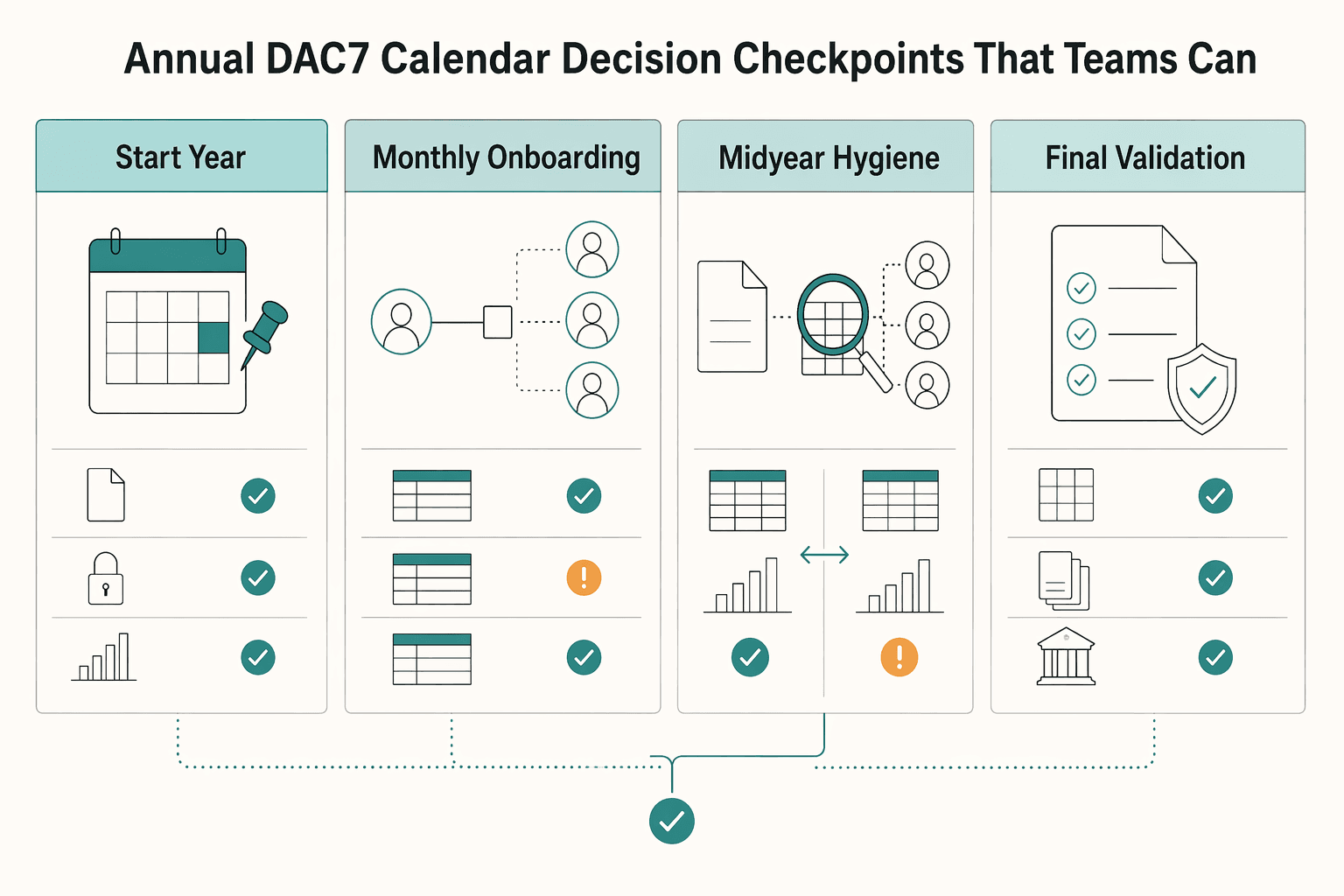

Annual DAC7 calendar with decision checkpoints that teams can actually run#

Run this as a control calendar, not a last-week filing task. Set internal cutoffs ahead of any external filing timeline that applies to your program, and treat authority handoff as the end of execution, not the start of cleanup. If your team already runs OSS, reuse the operating discipline even though the legal regime is different: prepare the OSS VAT return, submit it electronically, and track onward transmission by the Member State of identification.

| Checkpoint | Main action | Evidence or escalation |

|---|---|---|

| Start-of-year freeze and due diligence completion | Freeze the prior-year seller population and reconcile it to payouts, onboarding status, and legal-entity ownership | Keep a dated evidence pack for each in-scope seller |

| Monthly onboarding quality checks | Review newly onboarded and recently changed sellers monthly, then route exceptions to named owners immediately | Track missing or conflicting TIN or VAT ID values early |

| Midyear hygiene and pre-close rework window | Run a midyear dry run against year-to-date data to catch structural issues while rework is still cheap | Document who can reopen records, who approves overrides, when late partner files stop auto-inclusion, and who owns escalation |

| Final validation and hard go/no-go before the reporting file | Before generating the final reporting file, enforce a hard internal stop rule for unresolved identity exceptions | Final sign-off should include a validation report, unresolved-exception log, seller-to-total reconciliation, correction history, and named approvers |

- Start-of-year freeze and due diligence completion

Freeze the prior-year seller population and reconcile it to payouts, onboarding status, and legal-entity ownership. The goal is a reproducible filing population with clear inclusion logic, not just a seller count. Keep a dated evidence pack for each in-scope seller: identity snapshot, payout mapping, activity classification, and remediation notes, so later legal or compliance review can trace changes.

- Monthly onboarding quality checks

Review newly onboarded and recently changed sellers monthly, then route exceptions to named owners immediately. Focus on whether identity and account data are complete, consistent across systems, and linked to the correct seller and payout profile. If your internal policy relies on fields such as TIN or VAT ID, track missing or conflicting values early so they do not sit unresolved until filing prep.

- Midyear hygiene and pre-close rework window

Run a midyear dry run against year-to-date data to catch structural issues while rework is still cheap. Compare seller master data with payout totals, correction events, and partner or regional data feeds to surface duplicates, broken links, or classification drift. Document the rework window: who can reopen records, who approves overrides, when late partner files stop auto-inclusion, and who owns escalation. For complex cross-border VAT interpretation, use a formal path such as CBR, and submit requests under the national VAT-ruling conditions of the participating EU country.

- Final validation and hard go/no-go before the reporting file

Before generating the final reporting file, where your process uses one, enforce a hard internal stop rule for unresolved identity exceptions. This is an internal control choice, not a statement of DAC7 statutory field law. Final sign-off should include a validation report, unresolved-exception log, seller-to-total reconciliation, correction history, and named approvers. If late data arrives from business units or payment partners, route it through a predefined rework path with a clear decision to amend, defer, or hold submission.

Seller data checklist for reportable sellers and audit evidence#

Your filing is only as defensible as the evidence behind it. Build each reportable seller record as four linked packs you can explain later: identity, activity, verification, and privacy.

- Identity pack

Start with one frozen seller profile per reportable seller and link it to the payout record used for money movement as an internal control. As an internal checklist, you may capture fields such as legal name, address, jurisdiction, TIN, VAT ID where relevant, and payout account mapping, but treat that as an internal control list, not a complete statutory field list from the excerpts. For each relied-on field, keep source traceability and a last-confirmed date, for example onboarding data, finance master data, or remediation updates. If identity values change late in year, retain the prior value, reason, and approver so you preserve history instead of overwriting it.

- Activity pack

Make the category decision explicit and evidence-backed for every in-scope seller. The excerpt-supported categories are sale of goods, personal services, immovable property rental, and transport rental, and coverage is described as both domestic and cross-border. Store a short evidence reference behind each classification: listing type, contract language, transaction description, service metadata, or booking object. If a seller spans multiple activities, record your split logic rather than forcing a single broad tag. Use threshold-style examples as review triggers, not automatic exclusions, unless jurisdictional implementation is confirmed, for example less than 30 sales and annual consideration not exceeding EUR2,000, or at least 2,000 rentals per year in the property example.

- Verification pack

Keep a dated decision trail, not just a final status. As an internal control, record what was checked, what exception was found, what remediation was requested, and the final seller status. When a seller moves from exception to cleared, run one final identity-to-payout mapping check before reporting prep. If documents arrive after an annual freeze point, append correction history rather than replacing prior records so your audit path remains intact for later exchange-of-information questions.

- Retention and privacy pack

Define and document how reporting data is held and controlled under your GDPR posture. The excerpts do not prescribe detailed GDPR settings, so your policy should still clearly state why data is retained, who can access unmasked values, what is masked in routine workflows, and how deletion or archiving decisions are applied. Avoid both extremes: retaining everything indefinitely without rationale, or deleting remediation and source snapshots too early to defend reporting decisions. If privacy and reporting teams disagree, align a joint retention decision before scaling DAC7 process tooling.

Need the full breakdown? Read DAC7 for Platform Operators: Scope, Seller Data, and Controls for EU and Non-EU Platforms.

Before locking your year-end data pack, if you collect VAT identifiers, run a quick consistency pass with the VAT Number Validator.

Control ownership by function so gaps are visible before filing week#

Assign named owners before filing week. The provided excerpts do not define a DAC7-specific ownership model, so treat this as internal control design, not a legal requirement.

| Function | Owns | Control detail |

|---|---|---|

| Compliance | Interpretation decisions and exception approvals | Set one approval path for borderline scope decisions, with a dated exception register linked to seller identity and activity records |

| Legal | Policy text, jurisdiction caveats, and incomplete-facts escalation | Use a hard escalation rule when minimum facts are missing by the internal cutoff |

| Finance and Ops | Data quality, payout reconciliation, and evidence readiness | Run a pre-file reconciliation for seller totals, payout totals, and manual adjustments |

| Engineering | Repeatable pipelines, file validation, and override logging | Own deterministic reruns, required-field validation before export, and complete logging for manual overrides |

- Compliance owns interpretation decisions and exception approvals.

Set one approval path for borderline scope decisions, with a dated exception register linked to seller identity and activity records. As an operational analogy, VAT Cross-border Rulings says that when multiple companies are involved, one company submits on behalf of the others. Every exception record should show approver, decision date, facts considered, and affected seller records.

- Legal owns policy text, jurisdiction caveats, and incomplete-facts escalation.

Legal should maintain the written policy for how decisions are applied across relevant EU Member States and what happens when facts are incomplete. Use a hard escalation rule when minimum facts are missing by the internal cutoff. As an operational analogy, CBR requests are filed in the participating EU country where the requester is VAT-registered, and in specified OSS Union-scheme cases, a Member State choice can bind the current calendar year plus two following years. That is not a DAC7 rule, but it shows why jurisdiction choices need deliberate ownership.

- Finance and Ops own data quality, payout reconciliation, and evidence readiness.

Finance and Ops should own whether report figures can be tied back to payout records, seller records, and retained support. The OSS materials group registration, declaration and payment, record keeping, and audits as connected responsibilities. Use the same control discipline in your reporting process. Run a pre-file reconciliation for seller totals, payout totals, and manual adjustments, and escalate unresolved breaks before file generation.

- Engineering owns repeatable pipelines, file validation, and override logging.

Engineering should own deterministic reruns, required-field validation before export, and complete logging for manual overrides: who, when, why, and before or after. This is not stated as a DAC7 legal requirement in the excerpts, but it is a filing-week control worth enforcing. A practical check is rerunning the same frozen population twice and investigating any output change without an approved input change.

If you do one thing next, publish a one-page ownership matrix that lists primary owner, backup owner, approval right, and evidence artifact per control, and keep it with the filing pack.

Related reading: OFAC Compliance for Payment Platforms: How to Screen Every Payout Against the Sanctions List.

Build vs buy rules for DAC7 compliance platforms#

Treat this as a control decision under reporting pressure. Choose the path that gets you to a defensible, explainable reporting process quickly without losing accountability.

Industry commentary describes platforms of different sizes changing onboarding and verification before the first DAC7 reporting deadline on January 31, 2024. The same commentary also states there is no small-platform exemption and warns that persistent non-compliance can lead to severe enforcement exposure, including possible loss of the ability to operate in the EU. So this is not a side workflow.

Buy first#

A vendor-first path can be a practical option when speed to compliance is your main risk and your operating model fits common platform patterns. The core question is whether the tool can produce evidence, not just outputs: clear record history, changes over time, and data prepared for automatic exchange of information (AEOI). If exception handling still depends on offline workarounds, your team still owns significant control risk.

Build first#

A build-first path can fit when you need direct control over how your internal data and decisions translate into reportable outputs. The key quality check is reproducibility: same frozen input, same output, and explainable differences only when approved inputs changed. If compliance cannot explain inclusion, exclusion, or reclassification decisions from the resulting data trail, the build may not be filing-ready.

Hybrid#

A hybrid path can help when you need near-term filing support but want to keep long-term control of core records and approvals. Keep the external scope narrow and time-bound, and define up front what data and history you can extract each cycle so your team can rerun and challenge outcomes later. If your team cannot yet pressure-test AEOI readiness and exception handling, treat build-first as higher execution risk rather than a default choice.

Related: GDPR for Marketplace Platforms: How to Handle Contractor and Seller Personal Data Compliantly.

Rollout sequence for a live platform without breaking payout operations#

After you choose build, buy, or hybrid, stability comes from sequence. Roll out in narrow slices, keep payout continuity non-negotiable, and expand only when records reconcile and evidence is reproducible.

- Consider piloting one market and one activity type first

Treat this as an operational choice, not a legal requirement. A narrow pilot gives you a contained defect list and makes it easier to catch where seller records, transaction classification, and payout data stop matching. Expand across EU Member States only after repeated checks pass: seller counts tie out, payable totals reconcile to the payout ledger, and your evidence trail shows who changed what and when.

If you also run VAT processes through OSS, keep that lane separate from DAC7. OSS allows registration in one Member State of identification for covered VAT returns, and supplies that fall under a chosen OSS scheme are declared through that scheme's OSS return. OSS does not replace DAC7 obligations. In some Union-scheme cases, the Member State choice can bind you for the current calendar year plus the next two.

- Connect onboarding, verification, and payout in that order

Start with onboarding so the durable seller record is created first. Add verification next so identity and status checks attach to the same seller ID. Bring payout mapping live only after those two are stable, because payout joins are where traceability failures can become costly.

Your control test is simple: one persistent seller identifier should survive all three steps and still map to the transaction classification used in your reporting process.

- Run parallel dry runs before production submission

Run dry runs alongside live operations to test both output generation and exception handling. Confirm records map correctly into your expected reporting output, then test who reviews exceptions, how overrides are approved, and whether corrected records re-enter cleanly.

For OSS lanes, use return cadence as an operational checkpoint: quarterly for non-Union and Union schemes, monthly for the import scheme. Validate queue ownership as strictly as data transforms, and test escalation paths before the cycle closes.

- Add controls that produce a reusable audit pack

Put approval gates on reclassifications, final signoff, and manual overrides. Use masked data views where supported so reviewers can validate quality without broad personal-data exposure. Standardize one export pack each cycle: source extract, transformed output, exception report, approval log, and a masked reviewer version retained under your privacy controls.

Repeatability is the test. For OSS-related operations, include record-keeping evidence (including marketplace/platform cases, even when not treated as deemed suppliers) and an escalation path for exclusion risk, since scheme participation can end by exclusion from the Member State.

This pairs well with our guide on 8 Resilient Compliance Controls for Payment Platforms in 2026.

Failure patterns that trigger escalation instead of silent risk#

Treat these as escalation events, not cleanup tasks, because they affect record integrity, legal interpretation, or your ability to defend what was filed.

- Conflicting TIN and VAT ID values during reporting prep

Escalate when tax identifiers are missing, duplicated, or contradictory. The grounding pack does not establish DAC7-specific TIN or VAT ID remediation rules, so a conservative move is to freeze the affected seller set, preserve field-level provenance, and route a decision on reportability to the accountable owner. Keep one evidence packet with the original value, corrected value, timestamp, and approver.

- Activity coding that flips between personal services and sale of goods labels

Escalate when the same seller can be interpreted both ways from product text, invoice labels, or payout metadata. Operations should not reclassify on their own; confirm DAC7 treatment differences for ambiguous categories with legal. Require one classification path across onboarding, transaction records, and tax logic. For complex cross-border VAT treatment uncertainty, route to legal and use VAT Cross-border Rulings as an available escalation path.

- Corrected records without a complete audit trail

Escalate when you cannot reproduce the before-and-after state of a corrected record. Under OSS, record keeping and audits are explicit operational components, and return and payment data is transmitted by the Member State of identification to Member States of consumption through a secure communications network. Minimum pack: source extract, corrected extract, exception note, approval log, and change executor.

- Unclear ownership during remediation

Escalate when legal, compliance, and engineering ownership is ambiguous. Assign one decision owner for legal interpretation, one data owner for seller records, and one technical owner for change execution and logging as an internal control checkpoint. This is more critical when your broader EU reporting design includes lock-in choices, since some OSS Member State of identification decisions can bind the current calendar year plus the two following calendar years.

DAC7 overlap with GDPR and parallel tax regimes your team already manages#

Keep the boundary explicit. DAC7 reporting and GDPR controls run in parallel, but they do not serve the same control objective. Use shared records where useful, and keep the control purpose clear.

- Separate objectives, shared records

Directive 2021/514 (DAC7) introduces reporting obligations for digital platform operators, and reports are submitted to one EU member state and then exchanged through AEOI. In practice, that can make completeness and traceability important priorities for reporting data, even when privacy controls are managed separately.

- Design for consistency across workflows

A practical risk is not the existence of separate controls, but letting separate controls create conflicting seller records. Use one canonical seller record with clear provenance and ownership so updates can be reconciled if questioned.

- Reuse existing tax ops carefully

Existing W-8, W-9, and 1099 workflows may provide useful operational structure, but they do not automatically satisfy DAC7 requirements. Treat them as supporting processes, then validate DAC7 reporting outputs on their own terms, including in your broader contractor tax operations.

Choose the smallest compliant design you can defend under audit#

Start with scope, then choose the operating model. For DAC7, the most defensible design is the one that matches your legal perimeter, entity map, and how seller income data moves through your business.

That order matters because reporting rules are internationally aligned, but implementation details are still jurisdiction-specific. If you buy broad tooling before scope is settled, you can over-cover low-risk areas while leaving material gaps unresolved.

If your platform facilitates services, for example taxi, food delivery, freelance work, or accommodation letting, or facilitates goods sales, treat that as a trigger for a written scope review. Do not use it as a shortcut to procurement. Tax administrations are handling rapidly increasing data volumes and more automatic information exchange, so assumptions without evidence are hard to defend later.

-

Scope decision record. Create one record of what is in scope, out of scope, and unresolved across entities, business lines, and transaction flows. Tie each conclusion to current operating facts: entity names, product surfaces, seller journey, payout path, and real transaction examples, so the decision is auditable.

-

Reporting checkpoint calendar. Build checkpoints backward from each relevant reporting window, with internal cutoffs before submission. Include onboarding quality checks, data hygiene reviews, completeness review, and pre-submission validation that seller income details are reportable to both tax authorities and sellers.

-

Escalation matrix. Assign named owners for scope ambiguity, missing or conflicting seller data, and post-review corrections. Keep the trail usable under pressure: affected records, issue date, approver, and final disposition.

Before vendor commitment, have legal and tax specialists confirm two points: your coverage matches operating reality, and control ownership is assigned to named people. If either changes, resize the design before signing.

We covered related operating controls in How to Handle Unclaimed Payouts: Escheatment Rules and Dormant Funds Compliance for Platforms. If your team needs to map DAC7 controls to payout operations and confirm market-specific coverage, talk to Gruv.

Frequently Asked Questions

Who must comply with DAC7 if our company is outside the EU?

Treat DAC7 scope as unresolved for non-EU companies until you have a written legal determination mapped to your entities, transaction flows, and EU-linked activity. Save that decision memo before you lock tooling or filing workflows.

Which activities are reportable under DAC7 and which are usually excluded?

This evidence pack does not confirm a DAC7 list of reportable activities or exclusions. Do not treat a vendor checklist as authoritative without legal review. Classify each business line against real transaction examples, and keep supporting screenshots and contract terms with each decision.

What is the practical difference between EU and non-EU platform operator obligations?

This evidence pack does not support a DAC7-specific EU versus non-EU comparison. If you need a definitive answer, get jurisdiction-specific advice. As an operational parallel only, EU VAT OSS shows that a non-EU business can register through one Member State of identification, but that VAT pattern is not a DAC7 determination.

What seller data is mandatory before year-end reporting?

Define the mandatory DAC7 seller data fields, including whether TIN or VAT ID is required in your case, with legal and tax. Then require your vendor to prove source, validation, and exception handling for each field. Minimum control: you can export each seller record with provenance, timestamps, and current exception status.

How should we handle missing TIN or VAT ID data close to filing?

This evidence pack does not provide a DAC7 remediation rule for missing TIN or VAT ID close to filing. Escalate each gap to a named owner and document outreach plus counsel-approved disposition. If you cannot produce an exception report with seller ID, missing field, contact history, and final disposition, treat it as an audit-trail failure, not only a data gap.

How does DAC7 reporting interact with GDPR obligations?

Avoid absolute statements on the DAC7-GDPR boundary, and align tax reporting and privacy handling through one controlled seller record model with documented collection purpose reviewed by counsel. If tax and privacy teams keep separate seller records, reconcile ownership and data lineage before filing periods.

What should we do first if our current vendor cannot prove filing readiness?

Treat inability to prove filing readiness as an immediate control risk. Ask for a concrete evidence pack: field mapping, validation rules, exception workflow, sample exports, submission procedure, and remediation ownership. If those artifacts are missing, run a documented manual or hybrid fallback while you re-evaluate the vendor. In EU VAT OSS contexts, participants can be excluded from a scheme by the Member State.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- data.consilium.europa.eu/doc/document/ST-15829-2022-ADD-2/en/pdftrusted

- eac.gov/sites/default/files/eac_assets/1/6/2010-04-2...trusted

- europarl.europa.eu/RegData/etudes/STUD/2021/662603/EPRS_STU(202...trusted

- single-market-economy.ec.europa.eu/system/files/2022-11/SWD_2022_350_2_EN_impac...trusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- taxation-customs.ec.europa.eu/system/files/2024-01/2023_CRM_Guide.pdftrusted

- vat-one-stop-shop.ec.europa.eu/one-stop-shop_entrusted

- vat-one-stop-shop.ec.europa.eu/index_entrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: