How OFAC screening fits into every payout flow#

Sanctions control in payouts is a release decision, not a search-box task. If your platform moves funds quickly, you need a defensible way to stop, review, and document risky payouts before money leaves your control.

Before you start#

This guide focuses on Office of Foreign Assets Control controls in payout operations. It is for compliance, legal, finance, and risk owners deciding when screening happens, how exceptions are handled, who approves edge cases, and what evidence needs to survive audit or examination. It is not a substitute for jurisdiction-specific legal advice, and legal determinations still belong with specialist counsel.

Step 1. Anchor on risk, not vendor claims#

A risk-based approach is the baseline for sanctions controls in fast payment environments. Treasury guidance on instant payment systems (bulletin sent on 09/30/2022 01:01 PM EDT) emphasizes managing sanctions risk with a risk-based approach and encouraging sanctions-compliance features in system design. For payout teams, the question is not "Do we have screening?" but "Which payout flows carry which sanctions risk, and what control applies before release?"

Risk is not uniform across products, services, customers, entities, transactions, and geographic locations. A single blanket rule can create the wrong tradeoff: too much noise in lower-risk flows and too little review where speed or geography raises exposure.

Step 2. Use OFAC list search as an input, not proof#

OFAC's list search tools support screening, but they do not replace due diligence or reduce civil or criminal liability. OFAC administers and enforces U.S. economic and trade sanctions, and its Sanctions List Search is built to help users work with the SDN List and other OFAC-administered lists. OFAC is also explicit that search results are not a compliance safe harbor.

For each held or released payout after a possible match, your team should be able to show the screening inputs, returned results, analyst notes, decision rationale, approver, and timestamp. If that evidence is incomplete or overwritten, the control is weaker than it looks.

OFAC also notes that its search uses approximate string matching, so false positives should be expected. Without clear ownership for match adjudication, teams can clear alerts too quickly or freeze legitimate payouts.

Step 3. Design for investigation, escalation, and records#

Screening alone is not the control. The control is what happens after an alert. FFIEC procedures look for investigation and escalation processes for potential matches, plus processes to block and reject transactions.

Build the operating model around four decision points: screening, exception handling, escalation, and audit trail. If identity data changes after review, consider re-screening before release. If a potential match is ambiguous, route it to the named compliance or legal approver instead of resolving it under speed pressure.

Record retention should be designed early, not bolted on later. FFIEC procedures refer to a five-year requirement for relevant OFAC records, with longer retention for blocked property. The sections that follow focus on making those operator decisions consistent, reviewable, and defensible.

Related: Invisible Payouts: How to Remove Payment Friction for Contractors Without Sacrificing Compliance.

What to prepare before you screen a single payout#

Set scope and evidence first. If you cannot show who is in scope and which payout paths touch U.S. banking, alert and release decisions are harder to defend.

Step 1. Confirm OFAC scope#

Confirm OFAC scope based on how your payout model actually runs. At minimum, map your entities and U.S.-linked touchpoints, including U.S. banks in the payout chain, and program scenarios that may involve foreign persons handling U.S.-origin goods.

Write a short scope note that lists each legal entity, its payout role, and each bank or provider connection that introduces U.S. exposure.

Step 2. Inventory every payout flow#

Inventory every payout flow and split it into domestic and cross-border, because OFAC rules apply to both domestic and international payments. Do not scope only the primary product path. Include normal rails and exception paths, for example urgent manual releases, so your controls reflect how payments are really sent.

Step 3. Collect current program artifacts#

Collect your current sanctions program artifacts before changing tools: risk assessment, screening and reporting controls, independent testing or audit evidence, and training logs. Use FFIEC risk dimensions as a completeness check: products, services, customers, entities, transactions, and geographic locations.

Step 4. Document the screening setup you run today#

Document the screening setup you actually run today, whether manual, software-based, or both. Name the OFAC Sanctions List Search if used, note any additional watchlist provider you use, and assign ownership for list updates.

Track list freshness and version evidence in your records. OFAC provides regularly updated downloadable lists, and the SDN page shows a visible last-updated date. If you want a deeper dive, read Sanctions Screening for Payment Platforms: How to Run OFAC SDN and Global Watchlist Checks.

Map your payout risk profile before selecting controls#

Do not pick screening settings until you map payout risk by flow. Your risk profile should drive the controls, not the other way around.

Step 1. Classify each payout flow#

Classify each payout flow with the same risk categories used in your broader assessment: products, services, customers, transactions, and geographic locations. That gives you a defensible structure before you design controls.

For payout operations, capture at least the payment rail or type, instant-payment usage, settlement speed, destination jurisdiction, bank relationships in the chain, and institution-defined value bands. Keep domestic and cross-border flows separate, and split out exception paths such as urgent manual releases or fallback providers.

Checkpoint: every payout path from your prior inventory should appear in one risk-map row, with no catch-all "miscellaneous" bucket. Do not treat one provider integration as one flow when it supports both domestic and cross-border payouts with different exposure.

Step 2. Apply a risk-based approach to control selection#

Apply a risk-based approach when selecting controls. Secondary summaries of the Instant Payment Systems guidance, published September 30, 2022, describe institution-specific design, not one universal control pattern.

Those summaries also report that domestic and cross-border instant payments carry different sanctions risk, and that payment nature and value are relevant factors. If a flow involves non-U.S. bank relationships, assess that exposure directly instead of inheriting domestic settings.

Using one rule set for every path can create the wrong tradeoff: unnecessary friction on lower-risk flows or weaker controls on faster cross-border flows.

Step 3. Set explicit tiers and attach control decisions#

Set explicit tiers, then attach a control decision to each tier. The goal is documented, repeatable decisions where exposure is higher and reversal is harder.

| Risk tier | Typical profile | Control decision |

|---|---|---|

| Lower | Domestic payouts, U.S. bank only, slower settlement, lower internal value band | Standard screening and ordinary exception review |

| Elevated | Cross-border involvement, faster settlement, higher value band, or non U.S. bank relationship | Enhanced screening and tighter internal controls |

| Highest | Cross-border plus high velocity, instant or near-instant release, limited ability to stop or recall | Enhanced pre-release review, senior approval, and documented release rationale |

For cross-border, high-velocity flows, the highest tier is often the starting point, then confirmed or adjusted by documented assessment. Also document ownership of name-match threshold decisions. OFAC's Sanctions List Search uses approximate string matching and does not recommend a specific confidence rating.

Step 4. Make management commitment visible in operations#

Make management commitment visible in operating decisions, not only in policy text. Secondary summaries describe five essential components: management commitment, risk assessment, internal controls, testing and auditing, and training.

Show ownership clearly: policy owner, sign-off authority for risk-tier changes, and accountable escalation owner when payouts cannot be auto-released. Keep the evidence concise and current: approved risk-tier matrix, version date, approver, and change log. If exception authority and accountability are unclear, control selection is still incomplete. For broader context, see A Guide to OFAC Sanctions Screening for Global Businesses.

Decide when screening happens in payout operations#

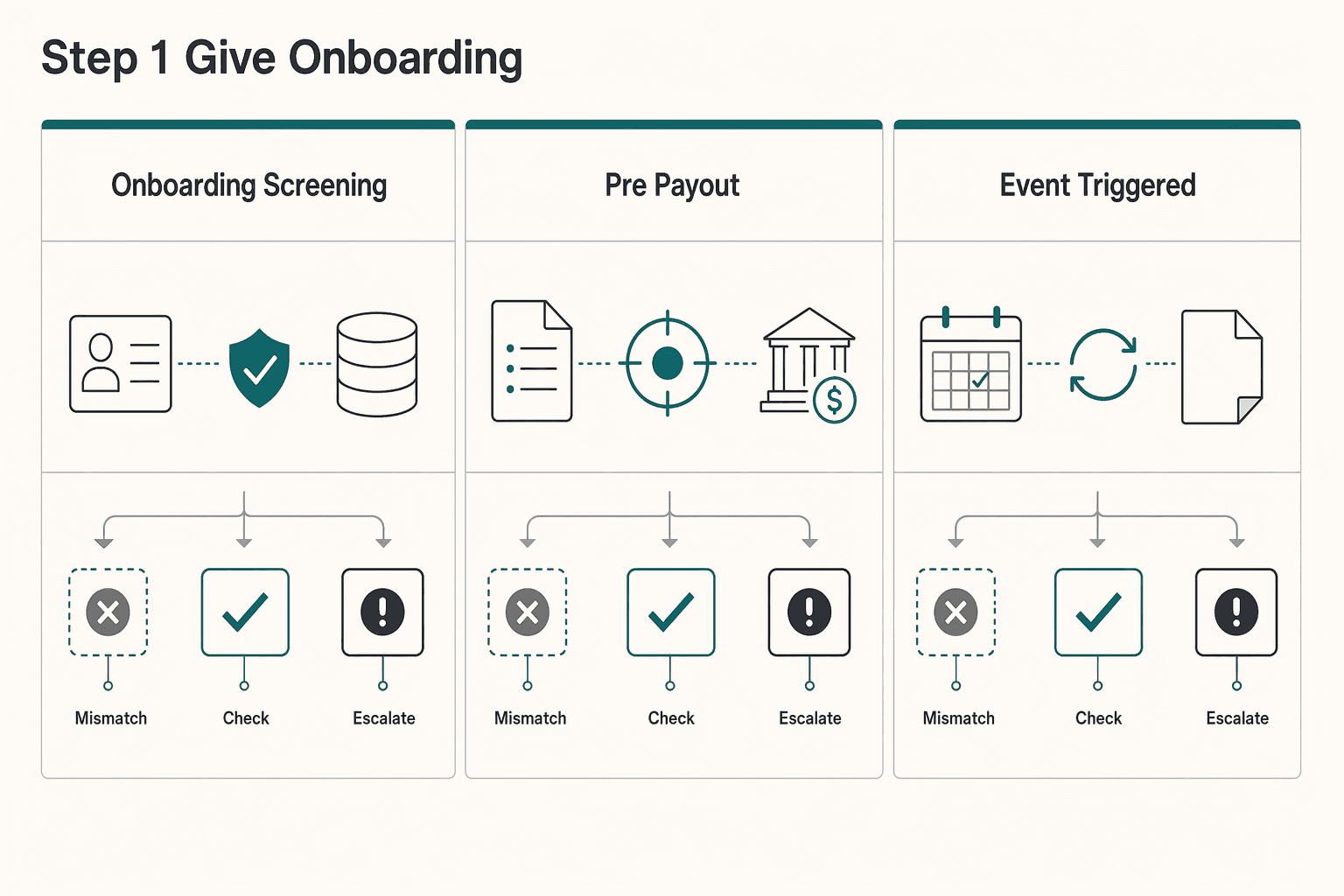

Put the sanctions gate before provider submission, and use onboarding, pre-payout, and event-triggered re-screening as layered controls. Onboarding checks can catch issues early, but pre-payout screening is typically the release decision point, with re-screening when list data changes and, by policy, when key party data changes.

Step 1. Give onboarding, pre-payout, and re-screening different jobs#

Use both customer screening and transaction screening, but give each one a clear job. Wolfsberg's distinction is practical for payout operations: onboarding screening helps control who enters your system, while pre-payout screening controls who gets paid now.

| Timing option | What it catches well | Main limitation | When to use it |

|---|---|---|---|

| Onboarding screening | Obvious sanctioned parties before profile activation | Can become stale as party details or list data change | Use at payee or beneficiary setup |

| Pre-payout screening | Current party and payment context at release time | Adds latency if exception handling is weak | Use as the release gate for domestic and cross-border payouts |

| Event-triggered re-screening | New risk from OFAC list updates and other policy-defined trigger events | Depends on reliable triggers and monitoring | Use on OFAC list updates (including Delta Files) and other policy-defined data-change events |

Pre-payout screening carries the most weight because it sits closest to the transfer decision. OFAC's Sanctions List Search covers the SDN List and other OFAC-administered lists. It uses approximate matching and does not recommend a specific confidence rating. That means timing and exception design matter as much as threshold settings.

Verification point: for each payout flow, identify the screening point that can still stop release. If screening happens only after instruction submission, the gate may already be too late.

Step 2. Keep a fixed payout sequence#

Keep a fixed payout sequence so exceptions stay inside control. A practical order is:

- Intake the payout request and freeze decisioning data.

- Run sanctions screening on relevant names and identifiers.

- Decide hold or release.

- Submit to the provider only after release approval.

- Track provider status and resolve exceptions.

The freeze point is critical. If beneficiary data can change after screening but before submission, the approved and transmitted records can diverge. Your exception branch also needs a true hold state. A legal summary of OFAC's September 30, 2022 instant-payment guidance highlights the need for exceptions to automatic processing so potential sanctions concerns can be investigated. The expected outcome is simple: each payout is released, held for review, or rejected before provider submission.

Step 3. Re-screen when data or list coverage changes#

Set a clear internal policy rule: if identity or beneficiary data changes after approval, re-screen before release for both domestic and cross-border payouts. This is a defensibility choice, not a claim that OFAC prescribes that exact trigger.

Define trigger events in operational terms so your team does not debate them mid-queue, and include OFAC list updates, including Delta Files, in that trigger set. Record the screened input data, when screening ran, which list source or update was used, and the hold or release decision with reviewer or rule attribution.

Also keep reporting in view. If you reject a prohibited transaction, 31 CFR 501.604 ties reporting to the rejection event. A secondary CFR text source states a 10-business-day filing window. Screening only after provider submission can increase unwind pressure, delay resolution, and make decision-point evidence harder to maintain. For implementation detail, read Webhook Payment Automation for Platforms: Production-Safe Vendor Criteria.

Build the match decision path your ops team can execute#

Once pre-payout screening is your release gate, decision ownership becomes the control that keeps releases defensible. Approximate name matching is triage input, not a yes-or-no tool output, so your team does not release on weak evidence or hold legitimate payouts without cause.

Step 1. Build a triage matrix your analysts can apply fast#

Use an internal three-bucket triage model for potential matches from Sanctions List Search results. This is a policy choice, not an OFAC-mandated taxonomy. It gives operations and compliance a shared handling path when approximate matches appear against the SDN List or other OFAC-administered lists.

| Internal triage bucket | Typical signals | Default action |

|---|---|---|

| Likely false positive | Name similarity exists, but available identifiers do not align well enough to support a true match | Hold briefly, document the mismatch basis, then release only if policy permits |

| Possible match | Name similarity remains plausible and identifiers are incomplete or mixed | Move to manual review and do not release until resolved |

| Likely true match | Name similarity plus overlapping identifiers suggests the listed party may be the same person or entity | Stop release and escalate immediately |

Do not let a match score decide the case by itself. OFAC provides sanctions list data and search infrastructure, but your team still has to decide whether your payout party is the listed party.

Step 2. Assign stop, review, and release authority by risk level#

Set explicit ownership by risk in your policy. Reporting accountability under 31 CFR 501.603 rests with the actual holder, transferrer, or releaser of the property, so case ownership should be unambiguous. For example, trained operations may clear well-supported false positives, while ambiguous or higher-risk cases route to compliance and, when needed, legal. This matters most in faster payment flows, where exception handling needs to be explicit before release decisions are made.

If identifiers are not enough to resolve identity, keep the payout out of straight-through processing. That aligns with exception-processing language in legal commentary on OFAC's September 30, 2022 instant-payment guidance, which describes removing transactions from automated flow to investigate potential sanctions concerns.

Define owner states in your policy and tooling:

- release after documented false-positive clearance

- hold pending review

- stop and escalate for potential sanctions concern

Step 3. Require a minimum evidence pack before release#

A clearance should hold up later, not just in the moment. Require a minimum case file before release:

- sanctions search results used in review

- screened input data and identifiers compared

- analyst notes explaining why the listed party is not your payee or beneficiary

- explicit decision rationale

- approver identity

- review and approval timestamps

- transaction references tying the case to the payout record

Capture enough detail to reconstruct the event if needed. If a transaction is rejected, 31 CFR 501.604 requires reports to include identifying information to the extent available, including reference numbers, account numbers, dates, or other transaction-identifying details.

Design records for retention, not just queue handling. Under 31 CFR 501.601, records must be available for examination for at least 10 years after the transaction.

Step 4. Add escalation triggers that force a second look#

Define internal escalation triggers so analysts do not clear edge cases in isolation. For example, your policy can require compliance review when the same beneficiary triggers repeated hits, identifiers conflict across sources, or SDN-list similarity remains unresolved after first-line review.

These are internal control triggers, not OFAC-mandated trigger text. The goal is consistent second-level review before release whenever pattern risk or unresolved identity risk remains.

Related: SOC 2 for Payment Platforms: What Your Enterprise Clients Will Ask For. If you are translating stop, review, and release rules into system behavior, map them to idempotent payout states and webhook handling in the Gruv docs.

Configure list coverage and name matching without drowning in alerts#

Start with OFAC coverage as your baseline, then add non-U.S. lists only where legal obligations or clear risk justify the extra alert load.

Step 1. Keep OFAC list coverage in your baseline#

Your baseline should include the Specially Designated Nationals (SDN) List and the OFAC Sanctions List Search process. OFAC's search application is designed to facilitate use of the SDN List and other OFAC-administered lists, and OFAC provides downloadable SDN and Consolidated (non-SDN) data.

To avoid quiet coverage gaps, confirm exactly which OFAC datasets your tool ingests and make sure reviewers can see returned program codes. OFAC specifically recommends close attention to program codes because they affect how a true hit should be handled.

Do not treat OFAC search as a legal shield. OFAC states the search tool is not a substitute for appropriate due diligence and does not limit civil or criminal liability.

Step 2. Separate legally required lists from risk-enhancing lists#

If your payout flow touches other jurisdictions, classify each non-U.S. list as either:

- Required by law or jurisdictional nexus

- Risk-enhancing but not strictly required

This keeps alert volume tied to obligation and business risk, not list sprawl. For example, the UK Sanctions List covers UK-designated targets. The EU states financial sanctions obligations apply to both public and private sectors, and UN member states are obliged to implement measures tied to listed names.

If a list is only risk-enhancing, document why it is included, which risk it addresses, and who approved the expected alert volume.

Step 3. Tune approximate matching to real payout patterns#

OFAC Sanctions List Search uses approximate string matching and can return near matches for misspellings or incorrectly entered text. OFAC also does not recommend any specific confidence rating.

That means your matching thresholds and alias handling are internal control decisions, not regulator-provided defaults. Tune them to your actual payout-name patterns, and keep test packs built from your own historical false positives, alias-heavy cases, and common spelling variants.

Before promoting any matching change, compare old and new logic on the same historical sample for alert volume, escalation rate, and true-match capture.

Step 4. Measure alert quality before and after tuning changes#

Use a stable internal metric set so you can show you reduced noise without weakening detection. Typical controls include false-positive rate, escalation rate, review time, and confirmed matches found in review.

Validate changes in controlled testing and audit trails, not just vendor demos. Evidence from a Federal Reserve study shows model choice can materially change outcomes. It reported 92 percent fewer false positives and 11 percent more matches versus its highest-performing fuzzy baseline. You still need proof in your own environment.

If alerts drop sharply after a threshold change, require evidence that true-positive capture did not fall. Keep the prior and new settings, test dataset, sample outcomes, approver sign-off, and effective date.

Assign ownership across compliance legal finance and ops#

Once you change thresholds or list coverage, assign decision rights before the next urgent payout forces an ad hoc call.

| Function | Core role | Notes |

|---|---|---|

| Compliance | Maintains policy and case standards | Name a designated OFAC compliance officer, or the equivalent person responsible for OFAC monitoring, and make the reporting line explicit |

| Legal | Supports hard-interpretation questions | Provide input when facts or jurisdiction are unclear |

| Finance or ops | Executes hold, release, reject, and reporting steps | Keep a direct handoff into compliance for reporting obligations |

Step 1. Name one accountable sanctions owner#

Name a designated OFAC compliance officer, or the equivalent person responsible for OFAC monitoring, and make the reporting line explicit. FFIEC examiner materials look for a named owner and clear assignment of responsibilities.

One workable operating split can be this: compliance maintains policy and case standards, legal supports hard-interpretation questions, and finance or ops executes hold, release, reject, and reporting steps. Your policy, escalation contacts, and approval records should point to the same owners.

Step 2. Tie responsibilities to risk and control changes#

Assign ownership across four areas: risk assessment, internal-control changes, case adjudication, and regulator response. You do not need to call it RACI, but each area should have a clear responsible owner and approver.

Control changes are safer when they are not pushed by ops alone. Route matching, list, and release-rule changes through your documented risk-assessment process, with compliance and legal input when facts or jurisdiction are unclear.

Step 3. Set escalation timing so unresolved cases do not auto-release#

Define internal escalation timing that matches payout speed, and keep a hold path when a potential match cannot be cleared in time. The point is to stop release pending review, not bypass review to meet payout cutoffs.

Keep regulatory timing separate from internal timing. Blocked-property reports are due within 10 business days, and primary reporting responsibility rests with the actual holder, transferrer, or releaser of the property. Rejected prohibited transactions also carry OFAC reporting obligations for covered U.S. persons, so finance and ops need a direct handoff into compliance.

Step 4. Show management commitment in recurring governance records#

Make management oversight visible through periodic review of blocked or rejected transactions, material control changes, and filing timeliness. Keep documented approvals, including approval dates in minutes where that governance structure exists.

As a governance benchmark, U.S. examiner guidance places internal-control accountability at board level through senior management. In practice, keep current risk-assessment records, recent approvals, and evidence that management was informed of significant sanctions issues. For a broader lens, see Why RegTech Creates a Compliance Moat for Gig Platforms.

Keep the evidence pack examiners and auditors will expect#

Once ownership is clear, make every payout decision reconstructable. If you cannot show what was screened, which list version was used, who approved the outcome, and what happened next, you may struggle to demonstrate your controls in review.

Under 31 CFR 501.601, parties subject to OFAC recordkeeping rules must keep a full and accurate record of each covered transaction and make it available for examination for at least 10 years. FFIEC examination procedures still reference a five-year baseline in places, so document that your retention standard follows current eCFR text and apply it consistently.

Step 1. Define the minimum record set for every payout#

Keep one evidence packet or linked case record per payout. At minimum, include:

| Record item | What to keep | When |

|---|---|---|

| Beneficiary and payment data | Beneficiary and payment data screened | Every payout |

| Sanctions source | Sanctions source used, including list or update reference | Every payout |

| Match outcome | Match outcome and analyst notes, if reviewed | If reviewed |

| Approver | Approver identity and timestamp | Every payout |

| Final action | released, rejected, or blocked | Every payout |

| Blocked-property additions | Filing date, the 10-business-day initial filing deadline, and any OFAC Reporting System (ORS) identifier when available | If the case becomes a blocked-property filing |

Be strict on identifiers. 31 CFR 501.604 requires rejected-transaction reports to include reference numbers, account numbers, dates, or other details needed to identify the transaction. Use that as your design floor. If a case becomes a blocked-property filing, add the filing date, track the 10-business-day initial filing deadline, and include any OFAC Reporting System (ORS) identifier when available.

Step 2. Preserve cross-system traceability from request to ledger#

You do not need to claim OFAC mandates a specific architecture, but durable links across the records you keep make reviews and responses more defensible. Tie together payout request ID, internal case ID, screening-provider result or search reference, processor or bank reference, ledger posting, and any exported review log.

This supports 31 CFR 501.602, which allows OFAC to require books and electronic documents tied to transactions before, during, or after the transaction. Fragmented IDs across tools can become a failure point: teams can show a match existed but cannot prove which transaction was held, released, or reported.

If you use OFAC's Sanctions List Service, keep the update date or Delta File reference as a traceability signal. It is supporting context, not a substitute for the transaction record.

Step 3. Split operating logs from restricted case files#

Separate day-to-day operating logs from restricted case files, especially where sensitive identifiers may appear. Some OFAC-related records may include data such as a social security number or employer identification number, so broad access increases exposure.

Use a simple pattern: keep a PII-light operations log for status, timestamps, handoffs, and final action, and keep the full case file in restricted storage. Link both with the same case ID so compliance can trace an ops event to underlying evidence during review.

Step 4. Snapshot the broader sanctions compliance program, not just single cases#

Examiners review more than single payout files. FFIEC OFAC procedures also examine training adequacy, independent testing and audit follow-up, and timeliness of list updates and filtering criteria.

Keep dated records of training completion, approved control changes, before-and-after filtering settings, testing and audit results, and remediation evidence. The sources do not support a fixed snapshot cadence, so capture these artifacts when controls change, after testing cycles, and before audits or exams.

For a step-by-step walkthrough, see OFAC, PEP, and Adverse Media Screening Decisions for Payment Platforms.

Test the program and retrain teams before controls drift#

Good records are not enough if controls fail under pressure. Run ongoing, risk-based testing on realistic screening scenarios, then retrain the teams who handle alerts and release decisions when weaknesses appear.

Step 1. Build test cases that reflect real payout risk#

Use scenario-based testing and auditing, not just clean-record matches. Independent testing is part of a risk-based OFAC program, and difficult-match cases are often where control gaps appear. Include scenarios such as:

- subtle name variations, including reordered name elements

- plausible name or address deviations that simulate difficult screening matches

- sanctioned-entity records drawn from multiple country contexts

- near-match cases that require reviewer judgment

For each scenario, verify both outcomes: the screening result and the reviewer decision.

Step 2. Test exception handling end to end#

Do not stop at whether the tool returns a match. Follow each test case through triage, escalation, and final hold or release to confirm that people and process are working with the technology.

The control objective is straightforward: the case is surfaced, escalation triggers are applied consistently, and the final decision matches policy.

Step 3. Set recurring training with a clear minimum cadence#

Make training a standing control, not a once-a-year scramble. A practical baseline is periodic training for appropriate teams, with annual training as the minimum floor, plus targeted refreshers after control changes or repeated test failures. Keep training practical: sanctions-list handling, escalation triggers, release authority, and short case walkthroughs that test decision quality, not attendance alone.

Step 4. Pause weak release paths when failures repeat#

Use a practical internal threshold: if the same control fails repeatedly in testing, escalate and, where warranted, temporarily pause the related release path until remediation is verified.

That matters most for faster payment flows. Speed is not a basis for weaker risk-based sanctions controls, so rerun failed scenarios after fixes and document who approved the control to resume.

Recover from common mistakes without freezing payouts#

When controls break, fix the recurring gap rather than locking down every payout flow. Focus recovery on four points: risk-based timing, analyst adjudication, clear decision ownership, and one complete record per case.

| Control gap | Recovery step | Operational check |

|---|---|---|

| Onboarding-only screening in higher-risk flows | Keep onboarding screening, then re-screen before release and when key payout or beneficiary data changes after approval | Confirm that changes to name, country, bank, or beneficiary identifiers route the payout back into review before submission |

| Fuzzy-name hits handled without analyst adjudication | Require documented analyst review before indefinite holds on fuzzy name matches | Use a standard evidence pack and escalate repeated alerts on the same party |

| Release authority is unclear on urgent payouts | Define and publish who does first review, who makes the final decision on ambiguous matches, and who is backup | Teams should be able to state who can release, who must escalate, and what happens after hours |

| Evidence is scattered across screenshots and chat threads | Build one audit packet per case in one place | Centralize screening inputs, screening outputs, analyst notes, escalation steps, approver identity, final action, and linked payout references |

Step 1. Add pre-payout and change-triggered re-screening#

Onboarding-only screening may be insufficient in higher-risk flows. A risk-based approach and Part 501's before, during, and after transaction reporting context support adding checks at multiple points, not just at account creation.

Keep onboarding screening, then re-screen before release and when key payout or beneficiary data changes after approval. As an operating check, confirm that changes to name, country, bank, or beneficiary identifiers route the payout back into review before submission.

Step 2. Require analyst adjudication for fuzzy matches#

A screening hit is not a final block decision. Sanctions due diligence includes investigating potential hits, then deciding whether to block or reject as appropriate.

Require documented analyst review before indefinite holds on fuzzy name matches. Use a standard evidence pack for each decision: screened name, matched entry, identifiers reviewed, analyst notes, rationale, approver, and timestamp. If the same party repeatedly triggers alerts, escalate the pattern instead of clearing each alert in isolation.

Step 3. Publish the final-approver chain#

Urgent payouts can bypass controls when release authority is unclear. Define and publish who does first review, who makes the final decision on ambiguous matches, and who is backup when the primary owner is unavailable.

Keep this in the same policy set tied to management OFAC ownership. Validate it with live alerts: teams should be able to state immediately who can release, who must escalate, and what happens after hours.

Step 4. Consolidate one audit trail packet per case#

Scattered screenshots and chat threads often do not provide a full and accurate record. Build one audit packet per case in one place, and retain it for the applicable period, including the Part 501.601 expectation that records be available for examination for at least 10 years.

At minimum, centralize screening inputs, screening outputs, analyst notes, escalation steps, approver identity, final action, and linked payout references. This supports faster audits and more consistent decisions because each reviewer can see prior reasoning.

Implement this in Gruv with policy gates and traceable payout controls#

Sanctions screening is a hard release gate, not a side check. In Gruv, design payout flows so a payout moves to released only after a screening pass or a documented analyst decision, and keep every retry, hold, and override tied to one case record.

Step 1. Put the screening decision before payout release#

Make the sanctions decision final before any payout instruction is sent. The flow should be: payout requested, screening run, analyst review if needed, then release. If your flow has U.S. nexus, a true SDN match is not a normal delay because U.S. persons are generally prohibited from dealing with SDNs.

Keep list data current through OFAC Sanctions List Service pulls on a controlled schedule for SDN data and, where your policy requires it, consolidated non-SDN data. For retry safety, a replayed payout request should return the same hold or release outcome rather than create a second action. Use idempotent requests for hold and release operations. Screening after provider submission can shift control to reversal or exception handling instead of preventing execution.

Step 2. Expose a small set of states and publish them consistently#

Use a small status set with clear operational meaning: hold, under review, released, and rejected or blocked when legal analysis requires it. Keep the same payout ID and case ID visible across compliance, finance, and ops so teams act from one source of truth.

If your Gruv setup supports webhooks or similar event delivery, push each state change to the teams that must act. Include at least payout reference, prior state, current state, actor or service, and timestamp. Make handlers idempotent so repeated deliveries do not advance a case twice. Exception handling can fail when state views drift across teams, so close that gap before volume scales.

Step 3. Link the case record to the money movement#

Keep one record that connects sanctions decisions to payout movement end to end. Reviewers should be able to move from payout to case, and from case to a ledger or balance-transaction equivalent, without searching email or chat.

Store screening inputs, matched names or identifiers, analyst notes, approver, final action, and payout or batch reference together in an exportable packet. This supports the full-and-accurate record expectation and retention readiness for examination for at least 10 years.

Step 4. Apply the same controls to Virtual Accounts and payout batches where supported#

Use the same escalation path and approval standard for Virtual Accounts and payout batches where those programs are supported. Do not create a lighter path because a batch file or account type sits between review and release. Unresolved items should not auto-release in batch flows.

State market qualifiers explicitly. Coverage and payout behavior vary by country, industry, and program setup, and legal obligations can differ by jurisdiction. Operate one documented sanctions program with local qualifiers, clear ownership, and the same evidence standard wherever the feature is supported.

Final takeaway and copy-paste checklist#

A defensible sanctions program for payouts comes down to three controls: a documented risk assessment tied to your payout model, clear stop/review/release rules where risk warrants them, and records you can produce without reconstructing decisions from chat and email.

For any payout you release, hold, block, or reject, keep a decision trail: who reviewed it, what data they reviewed, what they decided, and when. If a case becomes blocked property, the initial report under 31 CFR 501.603 is due within 10 business days.

Copy-paste checklist#

- Confirm scope under OFAC regulations.

Identify the U.S. nexus points in your payout chain, including U.S. persons and U.S. financial-institution touchpoints. Your policy should name the legal entities, products, and payment partners in scope.

- Map payment flows by risk profile.

Separate domestic and cross-border flows where risk differs, and use a risk-based design instead of one blanket control set. Treasury guidance for instant payments emphasizes a risk-based approach, and FFIEC procedures expect policies and processes to follow the institution's risk assessment.

- Set screening timing checkpoints explicitly.

Decide and document where screening happens (for example, at onboarding, before payout release, and after material data changes). If screening starts only after submission, controls become more reactive.

- Define match triage and escalation before alerts start arriving.

FFIEC procedures call for a defined investigation and escalation process for potential matches and a defined process to block or reject transactions. Because OFAC Sanctions List Search uses approximate matching and is not a substitute for due diligence, treat fuzzy-name hits as triage alerts and document the identifiers reviewed and the final disposition.

- Assign approvers and backup coverage.

Name who handles lower-risk alerts, who makes final sanctions decisions, and who covers when the primary reviewer is unavailable to avoid coverage gaps.

- Document every case in one evidence pack.

Keep screening inputs, the source checked, list version or "last updated" reference when available, match outcome, analyst notes, approver identity, timestamps, and final action. At minimum, include SDN coverage and, where relevant, OFAC consolidated non-SDN list data.

- Retain records to the current OFAC baseline.

Under 31 CFR 501.601, full and accurate transaction records must be available for examination for at least 10 years. If internal procedures or vendor settings still reflect five-year retention, update them to the current 10-year standard effective March 12, 2025.

- Run periodic testing and auditing, then retrain after failures.

Test real decision paths, not only whether a tool generates alerts. Sample closed cases for complete evidence, correct escalation, and consistent decisions; retrain and re-test when you find repeat gaps or undocumented overrides.

Once your checklist is drafted, confirm market coverage and policy-gate fit for your rollout through Gruv Payouts.

Frequently Asked Questions

Do payment platforms need to screen every payout against OFAC-related sanctions lists?

OFAC does not prescribe one universal screening rule for every platform and payout type. The grounded standard is risk-based, including decisions on whether and how to screen based on your exposure profile. OFAC also states that Sanctions List Search is not a substitute for due diligence and does not limit civil or criminal liability.

What does a risk-based sanctions compliance program look like for instant payment systems?

Use a risk-based design that matches controls to your payment model instead of forcing one pattern across all flows. A commonly cited structure uses five components: management commitment, risk assessment, internal controls, testing and auditing, and training. For instant payments, legal summaries of OFAC guidance describe domestic systems as typically lower exposure than cross-border systems, so your documented controls should reflect that difference.

When should we screen in the payout lifecycle to avoid both delays and missed risk?

If your goal is to stop risky payouts before execution, screen before release rather than only after submission. eCFR allows reporting requirements before, during, or after transactions, so timing design should be explicit in your program. Document how alerts are handled at each stage so post-submission cases can still be managed consistently.

How should teams handle fuzzy logic name matching alerts without stopping all payouts?

Fuzzy-name results are triage alerts, not automatic blocks. OFAC states its tool uses approximate string matching and does not recommend a single confidence rating, so your review standard should go beyond name similarity alone. Document the matched record, program codes, identifiers reviewed, analyst notes, and the final hold or release decision with timestamps.

What is the minimum escalation workflow for potential sanctions matches?

A practical minimum is to capture the alert and identifiers, route ambiguous or higher-risk cases to a named reviewer, and record the final decision before payout movement. If the case becomes blocked property, reporting obligations apply quickly: under 31 CFR 501.603, primary responsibility sits with the actual holder, transferrer, or releaser, and the initial report is due within 10 business days. Build backup approver coverage so escalation does not depend on one person being available.

Who should own final sanctions decisions across compliance, legal, finance, and operations?

OFAC regulations do not provide a universal RACI, so ownership has to be assigned in your policy. A defensible model is to assign clear adjudication ownership, define when legal review is required, and have execution teams carry out only approved actions. Whichever team carries reporting responsibility should also be able to retrieve a complete record for at least 10 years.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/manual/OfficeOfForeignAssetsControl/01_eptrusted

- bsaaml.ffiec.gov/manual/OfficeOfForeignAssetsControl/01trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-V/part-5...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-V/part-5...trusted

- federalregister.gov/documents/2025/03/21/2025-04864/reporting-pr...trusted

- federalreserve.gov/econres/feds/files/2025092pap.pdftrusted

- sanctionslist.ofac.treas.gov/Home/index.htmltrusted

- sanctionslist.ofac.treas.gov/Home/SdnListtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: