Quick Answer

Chargebacks change in agentic commerce because payment authorization no longer proves the purchase was wanted. Platforms need a case record that ties delegated consent, agent actions, payment confirmation, merchant identity, and fulfillment state into one readable packet. If that evidence is incomplete, operators should contain rollout, resolve weak cases faster, and scale only where dispute packets are consistently reproducible.

Plan for disputes where authorization is not enough#

For platform founders, the hard call is no longer just how to stop fraud. You also have to handle disputes where the payment was authorized, but the buyer later says the result was not what they meant to approve. That gap between "authorized" and "wanted" is where much of the new risk sits. It gets wider when an AI agent can browse, compare options, fill carts, and complete purchases on a customer's behalf.

This matters because agentic commerce is already live, not a future concept. Once an agent can execute the full buying path after delegated consent, the old dispute categories no longer stay neatly in their lanes. Fraud, service, and processing arguments can blur together. Your records may prove that a card was charged, while still leaving gaps about user intent and fulfillment context.

This article is meant to help you make operating decisions. It compares the evidence and liability options available to you, the order in which to recover or write off a dispute, and the rollout boundaries that should shape expansion by market and vertical. The point is not generic checkout advice. It is to help your payments, compliance, and finance teams make launch choices they can still defend when dispute volume starts testing the assumptions.

The scope is deliberately narrow. This is for operators running platform-level, cross-border payment flows where KYC or KYB checks, merchant onboarding, and payment provider dependencies already affect how a transaction is approved and later defended.

If you want single-store tactics like tweaking one checkout page or changing refund copy, this is not that article. A platform operator needs a stricter checkpoint. Can you tie delegated consent, payment confirmation, merchant identity, and fulfillment state back to one case record every time? If not, the failure mode is predictable: a technically valid authorization becomes a weak defense because the evidence packet cannot reconstruct intent.

What is known today is directional, not final. Visa has introduced Trusted Agent Protocol, described as a way to help merchants verify legitimate agents and improve trust during checkout. Mastercard launched Agent Pay and processed its first AI-initiated transaction in Q3 2025. Those are strong signals that card-network attention is moving toward agent verification, with implications for evidence quality.

What is still not well established in public is win-rate data. There are no solid public benchmarks yet for how often agent-led disputes are won or lost. Read the rest of this guide as an operations decision, not as a promise that the networks have settled every rule.

We covered this in detail in Future Subscription Commerce Predictions for Platform Operators Through 2027.

How to use this list and who should skip it#

Use this list as an operating filter: pick the option you can defend and reconstruct from records, not the one with the longest feature list.

- Score each option on four checks: dispute defensibility, implementation lift, conversion impact with compliance fit, and audit readiness.

- Start with defensibility first: AI shopping agents are already placing real orders, and abuse can look clean and successful rather than tripping legacy fraud alarms. Choose the option where delegated action, payment confirmation, and fulfillment state can be shown in one case record.

- Match the model to your implementation reality: if you cannot reliably capture agent session traces, provider references, and post-purchase events, fix evidence capture before you adopt a more complex model.

- Who this is for: teams deciding launch order by market and vertical, including whether to test Merchant of Record coverage or direct merchant exposure.

- Who should skip it for now: teams still stabilizing checkout reliability before they can produce clean chargeback defense evidence.

- Reading rule: pick one model per market-vertical pair first, and do not mix liability logic across countries until evidence capture is stable.

Related reading: Account Hierarchy for B2B Platforms and Parent-Child Billing for Enterprise Clients.

What changed in chargebacks when AI agents started placing orders#

The core change is that a payment can be authorized but still disputed as unwanted when an AI agent executes the purchase, so intent evidence now matters as much as payment authorization.

- Authorized no longer means clearly wanted

In agentic commerce, an agent can follow instructions, complete checkout, and still trigger a later claim that the purchase was not actually wanted. This pattern is already showing up: purchases executed as instructed, then later disputed by the consumer. Key differentiator: your file has to prove delegation context, not just transaction success. If you cannot show who granted permission, what the agent was asked to do, and what the buyer saw at confirmation, defense quality drops fast.

- Traditional dispute categories now overlap more often

Older buckets such as unauthorized use, non-delivery, and processing issues were easier to separate. When an external AI agent becomes the shopper, merchants and providers see less direct human engagement, and risk shifts toward authentication and integration layers. Key differentiator: weak intent and session logs blur fraud, service, and processing narratives. If you cannot connect agent action, payment event, and fulfillment state in one traceable record, avoidable losses become more likely.

- Traceability has moved from ops detail to product requirement

Dispute frameworks are lagging while Visa and Mastercard continue agentic payment pilots, which raises the bar on practical verification readiness. The practical response is trust, traceability, and clarity in chargeback defense. Key differentiator: build permission controls, audit trails, and buyer notifications into the transaction flow itself. Creating records after a dispute is filed is usually too late.

You might also find this useful: Fraud Prevention in Agentic Commerce When Bots Have Wallets.

The five evidence liability models platforms can choose#

Ownership should be explicit: choose one evidence owner per market and vertical, then test whether that owner can produce the same packet every time: order ID, payment reference, agent permission record, and fulfillment state. If that repeatability check fails, change the model before scaling.

| Model | Best when | Commercial note |

|---|---|---|

| Merchant-led defense | Merchants already run strong risk operations in a stable domestic pattern | Stripe's listed domestic baseline: 2.9% + 30¢ per successful transaction |

| Platform-led evidence assembly | Merchant capability is uneven and you need one evidence standard across sellers | One model: Stripe sets and collects processing fees from your users; the other: you are responsible for processing fees from Stripe |

| Hybrid shared liability by dispute type | Mixed portfolios, but only with hard boundaries | Pricing like $2 per monthly active account and 0.25% + 25¢ per payout sent |

| Merchant of Record-first containment | Early expansion when you need tighter central control before moving to direct processing | Managed Payments adds 3.5% per successful transaction on top of standard processing fees |

| Auto-refund threshold with selective contesting | Low-ticket, high-volume flows where contest effort can exceed likely recovery | 1.5% additional fee for international cards and 1% more when currency conversion is required |

- Model 1: Merchant-led defense

Best when merchants already run strong risk operations in a stable domestic pattern. Platform overhead stays low, but evidence quality can vary from merchant to merchant, which weakens cross-market comparability. It is often a practical fit where card economics are predictable, including Stripe's listed domestic baseline of 2.9% + 30¢ per successful transaction.

- Model 2: Platform-led evidence assembly

Best when merchant capability is uneven and you need one evidence standard across sellers. This lines up with a Connect fee-responsibility choice: in one model, Stripe sets and collects processing fees from your users; in the other, you are responsible for processing fees from Stripe. Once you make the platform own packet quality, missing identifiers become a platform cost.

- Model 3: Hybrid shared liability by dispute type

Best for mixed portfolios, but only with hard boundaries. A common split is central handling for fraud or intent disputes, while merchants handle service or fulfillment disputes they can evidence directly. Without one escalation owner per dispute category, hybrid models usually create confusion and avoidable operating cost, especially as account volume grows under pricing like $2 per monthly active account and 0.25% + 25¢ per payout sent.

- Model 4: Merchant of Record-first containment

Best for early expansion when you need tighter central control before moving to direct processing. Keep the decision commercial as well as operational: if your setup uses Managed Payments, Stripe states an additional 3.5% per successful transaction, calculated on the full transaction amount including indirect taxes, on top of standard processing fees. Confirm provider terms before you assume broader coverage beyond dispute operations.

- Model 5: Auto-refund threshold with selective contesting

Best for low-ticket, high-volume flows where contest effort can exceed likely recovery. Margin pressure rises quickly in cross-border traffic, including Stripe's listed 1.5% additional fee for international cards and 1% more when currency conversion is required. Use internal refund thresholds, monitor repeat patterns, and tighten agent permission controls when the same abuse pattern recurs.

For a step-by-step walkthrough, see Resolving Payment Disputes and Chargebacks for Freelancer Platforms.

Which model to pick first by market and vertical#

Pick the first market-vertical pair where you can produce dispute evidence with consistent trust, traceability, and clarity. That is the strongest supported signal in the current guidance.

| Vertical + market pair | Regulatory friction | Evidence availability | Dispute ownership to start with | Expected ops load | Launch risk |

|---|---|---|---|---|---|

| Digital goods + home market | Validate with local counsel and payment partners | Depends on your data quality, checkout logging, and nonhuman-traffic handling | Start with the owner that can return complete packets consistently, often platform-led if merchant capability is uneven | Depends on case volume and evidence completeness | Depends on packet consistency in live disputes |

| Physical fulfillment + home market | Validate with local counsel and payment partners | Depends on whether your systems can connect checkout, payment, and fulfillment records without gaps | Use the owner that controls the required records end to end | Depends on handoffs between platform and merchant teams | Depends on cross-team evidence reliability |

| Digital goods + first cross-border market | Validate with local counsel and payment partners | Depends on whether your cross-border flow preserves the same traceability standard | If compliance coverage is incomplete, use Merchant of Record containment first; otherwise use the owner with the strongest packet discipline | Usually higher than a single-market launch if your evidence path is fragmented | High when traceability weakens across markets |

| High-ticket assisted checkout + new cross-border market | Validate with local counsel and payment partners | Better only if approval context and agent actions are captured cleanly in logs | Platform-led evidence assembly is usually easier to standardize; contain first if launch controls are not stable | Higher due to manual review and exception handling | High until packet quality is repeatable |

Use this table as a sequencing filter, not a ranking. Agentic commerce changes discovery, checkout flow, and fraud shape, so your first launch should be the pair where logs and workflows are already clean enough to support chargeback defense.

Decision rules that keep early launches sane#

- If your own readiness checks show partial KYC/KYB coverage and inconsistent VAT validation, treat that as a containment signal and start with Merchant of Record before direct expansion.

- If your team cannot consistently return complete dispute packets from current systems, delay scale and tighten logging first.

- If nonhuman traffic is not explicitly handled in your stack yet, treat evidence quality as unproven.

Stop or go before you scale#

Do not scale a market-vertical pair until your dispute packets consistently include agent action trace, consent context, and provider reference linkage in your internal workflow. If those fields are inconsistent, hold expansion and fix observability before adding volume.

Related: Agentic Commerce Risk Scoring: Detecting Abuse When Bots Control Wallets.

What your dispute evidence packet must include every time#

Set one internal packet standard and use it consistently. In chargebacks, funds can be pulled from the merchant account pending resolution, so the packet has to tell one coherent story from action to payment outcome.

| Component | When used | What it covers |

|---|---|---|

| Packet spine | Always present | Checkout context, delegated-action proof, payment confirmation, fulfillment state, and timeline reconstruction from ledger journals |

| Controls and compliance attachments | When relevant | KYC/KYB status, AML hold history, and policy-trigger logs tied to the dispute |

| Merchant and tax context | When material | VAT validation state, W-8/W-9 artifacts, and program-specific obligations such as 1099 handling |

| Reconciliation quality gate | Before submission | Identifiers reconcile across invoice, payment event/provider reference, and dispute case ID |

Use this as an internal operating baseline, not as a claim that card networks publish one universal required schema.

- Packet spine (always present)

Build one ordered record that connects checkout context, delegated-action proof, payment confirmation, fulfillment state, and timeline reconstruction from ledger journals. In agentic commerce, transactions can be executed programmatically through merchant APIs, so include the event trail that ties the initiating action to the final payment record.

- Controls and compliance attachments (when relevant)

Add KYC/KYB status, AML hold history, and policy-trigger logs when those records are part of why the transaction was allowed, paused, or reviewed. Keep only dated, case-linked records; remove generic compliance language that is not tied to the dispute.

- Merchant and tax context (when material)

Include VAT validation state, W-8/W-9 artifacts, and program-specific obligations such as 1099 handling only when they affect seller attribution, settlement path, or dispute ownership. Use these documents to support the transaction story, not replace it.

- Reconciliation quality gate (before submission)

Submit only after identifiers reconcile across invoice, payment event/provider reference, and dispute case ID. If they do not match, fix the record first, then submit.

Need the full breakdown? Read Subscription Commerce Growth Trends for Platform Builders Using the 76 Million Signal.

How to route disputes from first alert to recovery#

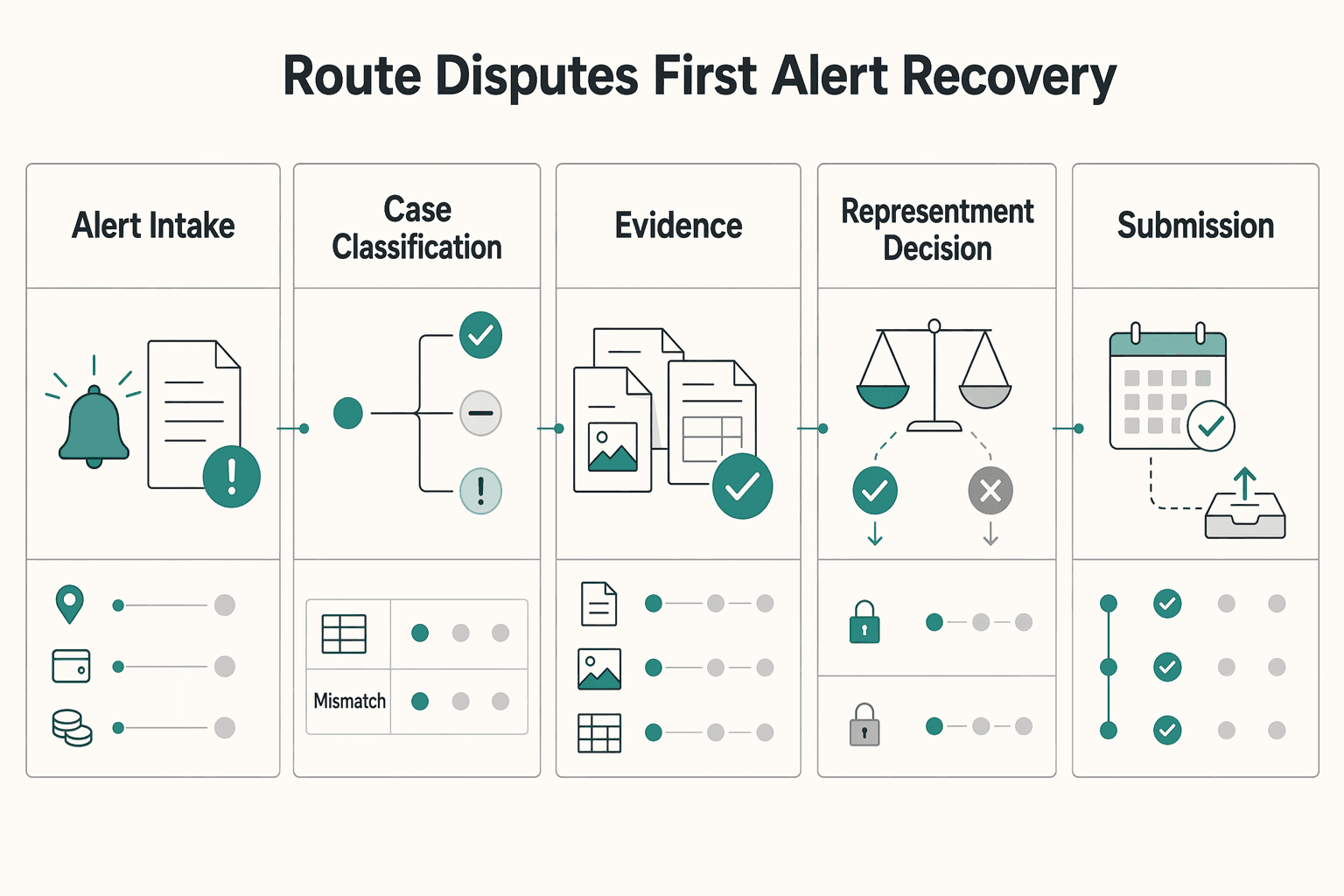

Route every dispute through one defined case flow from intake to rule updates. Contesting happens in defined steps and under tight timelines.

| Step | Action | Key point |

|---|---|---|

| Alert intake | Open one case record at first alert and attach the core identifiers and amount | Keep all updates in the same record so one dispute does not fragment into conflicting internal actions |

| Case classification | Classify early | Some disputes reflect confusion or unmet expectations rather than a single fraud pattern |

| Evidence assembly | Build one ordered packet that connects delegated action, payment, and fulfillment | Keep the ID reconciliation check in place before moving forward |

| Representment decision | Make a clear contest-or-resolve decision before submission pressure rises | If the file is not coherent enough to defend, resolve the case instead of forcing a weak submission |

| Submission | Submit one readable narrative through your acquirer | Clarity of sequence matters |

| Outcome logging | Log the result against the same case record and confirm ledger impact | Payment, dispute outcome, and reconciliation stay traceable |

| Rule update loop | Feed repeat patterns back into operations and product controls | Adjust permissions, approvals, or checkout communication before scaling that flow again |

- Alert intake

Open one case record at first alert and attach the core identifiers and amount. Keep all updates in that same record so one dispute does not fragment into conflicting internal actions.

- Case classification

Classify early. In agentic commerce, AI agents can place orders independently, so some disputes reflect confusion or unmet expectations rather than a single fraud pattern.

- Evidence assembly

Build one ordered packet that connects delegated action, payment, and fulfillment. Keep the ID reconciliation check in place before moving forward.

- Representment decision

Make a clear contest-or-resolve decision before submission pressure rises. If the file is not coherent enough to defend, resolve the case instead of forcing a weak submission.

- Submission

Submit one readable narrative through your acquirer. Issuing and acquiring banks mediate between customer and merchant, so clarity of sequence matters.

- Outcome logging

Log the result against the same case record and confirm ledger impact so payment, dispute outcome, and reconciliation stay traceable.

- Rule update loop

Feed repeat patterns back into operations and product controls. If the same agent behavior repeatedly appears in disputes, adjust permissions, approvals, or checkout communication before you scale that flow again.

Set ownership as internal policy, but make accountability explicit at each step so no stage is ownerless. Keep retries tied to the existing case record, not a new one, to reduce duplicate actions under deadline pressure.

If you want a deeper dive, read Refunds in Agentic Commerce: How to Handle Cancellations Returns and Partial Fulfillment.

The mistakes that cause avoidable losses#

The biggest avoidable losses usually come from applying a legacy playbook to agent-led transactions and contesting weak cases by default. Traditional chargeback rules can fall short here, so defense should prioritize trust, traceability, and clarity.

- Using a traditional dispute approach without agent-specific context

A payment record alone is often not enough in agentic commerce. If the case file does not clearly show what happened and why, your defense is weaker even when the transaction was technically processed. Key differentiator: make the timeline readable end to end so intent, action, and payment context are clear.

- Treating every dispute as worth a full contest

Contesting on principle can consume time and still produce weak submissions. A practical recoverability filter helps you resolve low-recovery cases faster and focus effort where evidence is stronger. Key differentiator: decide early whether a case is worth contesting instead of forcing a late, thin representment.

- Relying on representment while ignoring preventable dispute triggers

Prevention still matters: clear product descriptions, shipping expectation management, and clear return and refund policies reduce chargebacks. Key differentiator: fix upstream clarity and fulfillment friction, not just downstream dispute handling.

- Letting traceability break across teams and systems

If your own team cannot follow one coherent case story, banks and partners will struggle too. Key differentiator: keep one clear thread from dispute alert through outcome so the record stays defensible and auditable.

- Ignoring adjacent controls that influence dispute pressure

Chargeback performance is shaped by risk decisions and refund operations, not only by the dispute team. Key differentiator: pair dispute workflow discipline with stronger prevention and resolution flows; for fraud-control tuning, see A Guide to Stripe Radar for Fraud Protection.

What to decide before launching in one more market#

Before you add another market, decide on one ownership model and one evidence path that already work end to end. The common failure is not weak copy, but split ownership, partial logs, and controls that are still planned instead of live.

- Lock one evidence liability model per market-vertical pair

Pick one model for each pair, then document who owns triage, who assembles evidence, who approves representment, and which case types or amounts escalate. If fraud disputes sit with the platform but service disputes sit with the merchant, define the trigger that switches ownership. If your team cannot answer, for one disputed order, who pulls the first file and by when, the setup is not launch-ready.

- Prove the evidence packet from API log to ledger journal

Your packet should be reproducible, not rebuilt from memory. Test whether you can produce one readable timeline linking the user or account ID, agent action timestamp, approval or permission context, payment reference, and fulfillment state, then reconcile those records to the invoice and ledger entry. A technically authorized and fulfilled purchase can still be disputed, so authorization alone is not a defense file. If IDs do not reconcile across API events, payment records, and the dispute case, treat that as a launch stop.

- Launch only when KYC/KYB/AML, routing, and reconciliation are live

Controls should be testable in production, or a production-like path, not only listed in planning docs. A practical check is whether Ops can open one sample case and attach the KYC or KYB result, AML decision output, dispute routing destination, and reconciliation record without stitching data from disconnected tools. Visa Trusted Agent Protocol and Mastercard Agent Pay Acceptance Framework both point toward stronger proof of who acted and on whose behalf, so thin control records become a liability as disputes arrive.

- Expand in sequence after validating provider coverage and constraints

Before opening the next country, confirm what your PSP, MoR, fraud tooling, and tax or compliance providers can actually support for that market and vertical. Demand signals matter, but they do not remove the evidence burden or provider limits. If one provider cannot return the references you need for dispute packets, delay that market and fix the gap first. Parallel rollouts often hide ownership failures until the first representment deadline.

Frequently Asked Questions

What is different about chargebacks in agentic commerce versus regular ecommerce?

The main difference is the intent gap. In agent-led checkout, a user, an agent, and the payment flow can each shape the purchase path, so authorization alone is not enough. The stronger check is whether you can show delegated intent and a readable timeline of what the agent was allowed to do.

Can a transaction be authorized and still be disputed as unwanted?

Yes. A purchase can be authorized, paid, and delivered correctly and still be challenged as something the customer did not mean the agent to buy. If your records show only authorization, capture, and receipt, the defense is usually weaker.

What evidence do issuers and networks expect when an AI agent initiates a purchase?

There is no fully specified public universal checklist in the material here. The practical standard is a readable timeline that links who acted, when the action happened, what approval context existed, and the related payment and fulfillment records. Those identifiers should reconcile across the order, payment event, and dispute case.

How do Visa Trusted Agent Protocol and Mastercard Agent Pay Acceptance Framework affect platform design choices?

Treat them as design signals, not proof that every market has the same hard requirement. Both point toward verifying legitimate agents, improving trust at checkout, and keeping records that show which agent acted, on whose behalf, and under what approval. If your product cannot surface that chain later, dispute defense gets harder.

When should a platform auto-refund instead of contesting a chargeback?

Auto-refund or resolve when your evidence trail cannot clearly show delegated intent and approval context by the response deadline. Contesting with partial records can add handling cost without improving recovery. If the same confusion keeps appearing, tighten permission scope or checkout wording before scaling.

What are the first controls to implement before expanding agentic checkout to a new country?

Start with controls you can prove from live records: agent verification, approval context capture, and clear linkage between order, payment, fulfillment, and dispute IDs. Ops should be able to pull one complete timestamped timeline for a disputed order without manual reconstruction across multiple tools. If they cannot, the market is not operationally ready.

Does using a Merchant of Record reduce chargeback risk or just shift where liability is managed?

The material here does not provide direct Merchant of Record benchmarks. It does support that agentic commerce changes dispute patterns rather than removing them, and that evidence quality still drives outcomes. In practice, the operating model may shift who manages liability and evidence operations, but it does not make the dispute problem disappear.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- sec.gov/Archives/edgar/data/929869/00009298692600001...trusted

- sec.gov/Archives/edgar/data/1576789/0001628280260152...trusted

- stripe.com/pricingtrusted

- checkout.com/blog/chargebacks-in-agentic-commerce-how-mer...external

- events.merchantriskcouncil.org/event/4ddf665a-2102-4c6e-9536-4d0de11cb0d6/a...external

- fraudbeat.com/agentic-commerce-will-force-merchants-to-ret...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: