Quick Answer

Yes - treat forecasts as a screening input, then commit only after operator proof is in place. For this topic, the go/no-go standard is three checks: billing health in your own data, jurisdiction readiness, and reliable money movement under failure conditions. The article points to concrete tests such as renewal and decline behavior, VAT and KYC/KYB/AML scoping, and payout feasibility by country. It also flags involuntary churn risk from failed recurring payments, including a benchmark sample showing 7.2% of subscribers at risk monthly.

What Platform Operators Should Plan For Through 2027#

The point of future subscription commerce predictions platform operators 2027 is not to admire a growth curve. It is to turn broad forecasts into country-by-country, vertical-by-vertical go or no-go decisions that still hold up when billing starts, renewals hit, and compliance review begins. If a market looks attractive on paper but you cannot confirm payment fit, retention durability, and jurisdiction requirements, it is still a risky bet.

That matters because macro growth claims do not always show where execution breaks. In subscription commerce, recurring payment failure can be a major source of risk, not just weak demand. Recurly's research describes involuntary churn as subscriber loss caused by declined or failed recurring payments, and its benchmark sample found 7.2% of subscribers at risk each month from that issue. You should not treat that number as universal across every vertical or country, but it is a strong reminder that revenue continuity can fail even when acquisition looks healthy.

The same limitation shows up in market forecasts. Research products can be useful, especially when they offer a country readiness index or a 2025 to 2030 view of the subscription economy, but they are still directional inputs. They tell you where to investigate, not where to commit launch resources on their own. A practical check is simple: if a prediction does not connect to evidence you can verify in your own funnel, billing data, or country compliance review, treat it as a weak input.

Jurisdiction detail is where many expansion plans go from promising to blocked. Payment authentication rules and other local compliance requirements can change the shape of a launch, even inside markets that look commercially similar. For example, some PSD2 transactions may be out of scope for extra authentication only when they are flagged correctly. That kind of operator detail never appears in a topline market slide, yet it can affect the authentication flow and whether your recurring setup works as intended.

This article separates useful signals from noisy headlines, compares first markets through a country-and-vertical lens, pressure-tests retention economics before paid expansion, and maps the compliance and money-movement constraints that can stop a rollout late. Then it closes with launch checkpoints that force proof before scale. If you are choosing where to place product and go-to-market bets next, that sequence gives you something more durable than optimism. It gives you a way to fund only the opportunities you can actually execute.

Define the operating terms before making any 2027 bet#

Before you rank markets, define the operating terms you are actually betting on. Here, the core is recurring payments, meaning charging customers on a recurring basis, not just tracking topline demand.

This section is for platform operators making real allocation choices: which verticals to prioritize, which countries to enter, and where go-to-market spend goes first. Use inputs you can verify in your own operating reality, and treat high-level growth claims as incomplete on their own.

Cross-border ecommerce also needs a strict definition. OECD measures selling to customers in other countries separately from overall ecommerce activity, and customs guidance treats cross-border transaction or shipment elements as distinct from domestic online selling. So a domestic playbook is not automatically portable across jurisdictions, especially where payment and AML/CFT implementation differs by country.

Keep scope discipline on forecasts. Projections to 2030 can help with direction, and the 2025 OECD revision is useful because it explicitly covers subscriptions and digital intermediaries, but neither replaces operator evidence for go or no-go decisions.

If you want a deeper dive, read Media and Digital Publishing Subscription Billing: Paywalls Metering and Bundling for Platform Operators.

Separate reliable signals from noisy growth headlines#

For 2027 planning, treat headline growth as directional and make funding decisions from operator evidence you can verify: payment declines, retention and renewal patterns, and onboarding friction.

Published forecasts can align on direction and still be weak for execution decisions. One estimate projects subscription e-commerce platform market growth of USD 407.31 billion from 2022 to 2027, while another projects 14.28% CAGR through 2031. The spread is not the core problem. The risk is treating topline forecasts as decision-grade when they do not show how renewals hold up, where payments fail, or where signup breaks.

| Signal | What it helps answer | Strength | What to verify |

|---|---|---|---|

| Headline market forecast | Is there broad category demand? | Weak alone unless method and sourcing are explicit | Confirm the publisher clearly explains inputs and methodology |

| Payment decline-rate trend | Can revenue collect reliably? | Strong early operator signal for collection risk | Track decline rate over time and analyze unique declines, excluding failed retries |

| Retention and renewal trendline | Do customers keep paying after signup? | Stronger than acquisition growth for durable demand | Check renewal success and failure patterns in billing data and CRM |

| Onboarding friction | Will prospects convert without heavy support? | Strong leading signal for launch readiness | Review drop-off in signup, verification, and first-payment steps |

| Customer lifetime value movement | Is unit economics holding as cohorts mature? | Useful but more lagging than onboarding and decline shifts | Watch movement as a confirmation signal, not an early trigger |

Use a simple rule: if a prediction lacks method transparency, treat it as a weak input until it matches your CRM and first-party data. First-party data is collected directly from your own audience, so it is the clearest operator evidence base. If an external report says a vertical is expanding but your funnel shows high abandonment before first payment, the report may still be useful, just not sufficient.

Before you fund a new market or vertical, require one evidence checkpoint: external opportunity and internal signals should agree. In practice, confirm three things: outside demand is supported by transparent methods, onboarding does not show severe friction, and unique decline plus renewal-failure patterns are explainable rather than noisy. If you cannot show that evidence pack, keep the market on a watchlist instead of committing rollout budget.

Pick first markets with a country and vertical decision matrix#

Prioritize first launches where VAT handling, verification scope, payout feasibility, and document readiness are already clear; if those prerequisites are unclear in a jurisdiction, pause and run discovery before you build.

Use a decision matrix to rank country-vertical options by execution risk, not headline market size.

| Country and vertical pattern | Demand signal | Local payment fit | Compliance burden | Operational complexity | Expected time-to-live |

|---|---|---|---|---|---|

| Familiar European Union market, known vertical | Strong when you already see first-party demand | Easier to validate when provider coverage and your billing model are already known | Moderate: OSS can allow registration in one EU member state; apply the EU-wide EUR 10,000 threshold correctly | Lower relative complexity when similar onboarding and support flows already exist | Shorter relative path because key assumptions are testable early |

| New EU market, adjacent vertical | Medium until CRM and funnel data confirm segment demand | Often workable, but renewal behavior can still differ by vertical | Moderate to high: VAT treatment and evidence requirements still need explicit review | Medium: localization, invoicing, and verification edge cases often appear late | Medium path if compliance and coverage are confirmed before build |

| Less-known market where coverage and policy gates vary by program | Weak to medium unless you have direct first-party demand evidence | Unclear until country support and payout capability are confirmed for your use case | High: requirements vary by location, business type, and requested capabilities; AML/CFT implementation differs by country context | High: charge setup can pass while payout and verification remain blocked | Longer and less predictable until discovery closes gaps |

Prelaunch evidence pack (required before engineering)#

| Check | What to confirm | Specific detail |

|---|---|---|

| VAT handling | Whether OSS applies to your model | How you will operate once cross-border sales pass EUR 10,000 in the EU context |

| KYC/KYB/AML mapping | Required fields and checks | Match the exact jurisdiction, entity type, and capability set |

| Payout feasibility | Payout availability by country/program and capability tier | Do not treat availability as binary; some programs use 4 payout feature levels |

| Document readiness | Which records are needed | Include beneficial-owner verification inputs and tax forms such as Form W-9 or W-8BEN |

A common expansion failure is assuming checkout readiness means market readiness. Charge acceptance can work while payout and verification still fail later on policy or documentation gates.

For a familiar EU launch, the operating path is often more knowable because VAT routing and thresholds are explicit. In less-known markets, ambiguity is the main risk: coverage may exist in principle while required capabilities or documents do not match your model. For a related operating-model discussion, read The Future of the Agency Model in the Age of AI.

Build retention economics before scaling acquisition#

Scale acquisition after retention economics are stable, not before. If LTV is unstable in your core market or churn cohorts are getting worse, prioritize retention fixes before new-country go-to-market.

Recent subscription reporting supports that priority: acquisition rates were reported down from 4.1% in 2021 to 2.8% in 2025, and a 2025 report based on 67 million subscribers across more than 2,200 merchants described retention, personalization, and loyalty tactics as a central focus for operators. The operating implication is straightforward: more paid traffic will not fix weak lifecycle performance.

Make "retention first" operational by unifying CRM, email, SMS, and loyalty data into one lifecycle system. You need one customer view that combines events and traits across site, app, and back-end systems, so post-purchase, renewal, and win-back actions trigger from the same record instead of disconnected channel tools.

Tie that setup to economics. Track LTV (total predicted revenue across the customer relationship) and churn (how many customers leave over time) by cohort, and use both signals before increasing paid spend.

Before expansion, confirm you can answer from one shared view:

- Which cohort is churning?

- What event happened before churn?

- Which intervention changed behavior?

Define ownership for execution, not just strategy. Each post-purchase and renewal trigger needs a named owner, timing rule, and success measure, including:

- Post-purchase triggers: first payment success, onboarding not started within a set window, first usage milestone, loyalty enrollment.

- Renewal triggers: card expiring, renewal approaching, failed renewal payment, grace-period entry, cancellation intent.

If those triggers and owners are unclear, retention work is incomplete. If LTV is unstable in your strongest market, fix renewal messaging, save flows, and loyalty-linked interventions before funding expansion into the next country.

For a step-by-step walkthrough, see Future of Financial Identity for Nomads Seeking Loans.

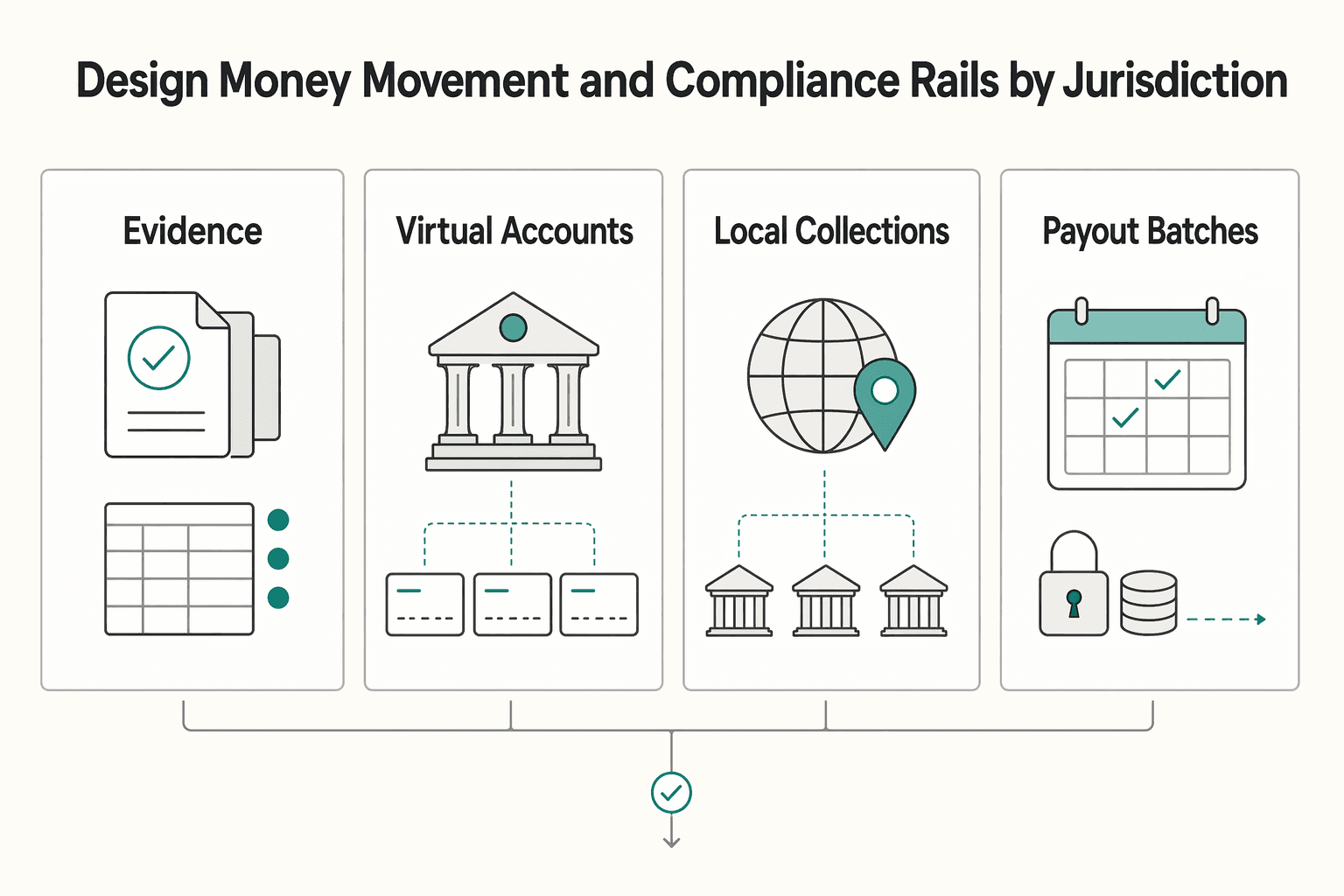

Design money movement and compliance rails by jurisdiction#

If you cannot confirm collections, compliance, and payout capability for the target country and your specific program setup, do not commit a launch date.

Start with four building blocks, and verify each one at country level before product work begins:

| Building block | What it does | What to confirm first |

|---|---|---|

| Merchant of Record | Handles transactional tax duties such as calculating, collecting, and remitting sales tax, VAT, or GST | Whether your MoR setup also covers the compliance scope you expect, including KYC and AML responsibilities |

| Virtual Accounts | Use unique account numbers linked to a wallet and currency for collections and reconciliation | Country and currency support, and whether the structure fits your local collection path |

| Local collections | Lets customers pay with market-specific payment options | Which region-specific payment methods are supported in that country, on your account, now |

| Payout batches | Sends funds out efficiently, including bulk API requests where available | Whether batch payouts are supported for that corridor and currency, and any local-currency payout rules |

The most common launch blocker is compliance intake. KYC requires collecting and maintaining account-holder information, and required data differs by country. KYB is the separate step of verifying the business is legitimate and safe to work with. AML design should align with recognized anti-money-laundering standards, so onboarding often needs more than basic profile fields.

Collect tax profile data in the same intake flow. Where relevant, you may need Form W-9 to provide a correct TIN to payers or brokers for IRS information returns, and Form W-8BEN when requested by the withholding agent or payer. If onboarding does not gather the required legal entity details, tax identifiers, and supporting documents for that jurisdiction, you are not launch-ready.

Set one architecture rule early: ledger journals are the audit source of truth. Use an append-only, double-entry record of monetary events, not provider dashboards, webhook payloads, or CSV exports, as your financial record.

Then enforce idempotency on every retry path that can move money. If a provider succeeds but your app times out, retries must not create duplicate charges or payouts. Before launch, replay a sample day from ledger journals, reconcile balances per account, and confirm retries with the same idempotency key produce one financial outcome.

One caveat: local payment methods, platform availability, virtual account support, and payout behavior vary by market and program, and can change over time. Confirm country coverage, currency constraints, and compliance availability before locking your launch calendar. Related: State of Subscriptions 2026: Key Benchmarks Platform Operators Need to Know.

Sequence rollout with failure modes and verification checkpoints#

Scale only after a controlled pilot proves that collections and payouts are stable under real retry and exception conditions. A practical sequence is: market validation, compliance scoping, payment rail setup, controlled pilot, then broader go-to-market.

Use a staged order that reflects launch risk#

| Stage | What to confirm |

|---|---|

| Market validation | Confirm the country and vertical are worth integration effort |

| Compliance scoping | Confirm onboarding and KYC requirements early, since payout eligibility can depend on completed verification |

| Payment rail setup | Complete rail configuration and test payments plus webhooks in sandbox before live traffic |

| Controlled pilot | Run limited traffic with manual review capacity so failures are visible and recoverable |

| Scale GTM | Expand only after pilot behavior is repeatable |

Test the failure modes that create financial damage first#

| Failure mode | What to test |

|---|---|

| Webhook lag and retries | Delivery retries can continue for up to three days; track failed events, retry timing, and eventual state convergence |

| Duplicate execution without idempotency | Webhook events can be delivered more than once, so fulfillment and money movement paths must execute once per intended payment outcome |

| Payout exceptions | Test incomplete onboarding/KYC, invalid account details, and corridor readiness before rollout |

| Batch payout duplicate protection | If you use payout batches, verify duplicate controls; reused sender_batch_id values can be rejected within a 30-day window |

| Renewal decline spikes | Check whether local payment methods, retry timing, or issuer behavior create renewal-failure patterns during pilot |

Gate each phase with an evidence pack#

Require a small, reviewable evidence pack at each phase gate:

- Policy decisions for retries, fulfillment, refunds, and payout exception handling.

- Reconciliation outputs derived from ledger journals, then matched to bank records.

- Webhook event audits covering duplicate handling, retry outcomes, and unresolved failures.

- Proof that collections and payout batches behave consistently for the target program.

No scale-up until pilot KPIs and exception handling are stable across collections and payouts. If you cannot replay pilot activity from ledger journals, reconcile it, and explain exception paths, hold the rollout.

Related reading: A Comparison of Dubai Free Zones for E-commerce Businesses.

Use channels for discovery without losing margin control#

Once the pilot is stable, treat channel strategy as a margin-control decision: use marketplaces for discovery and initial conversion, then move repeat lifecycle value into channels you control. The practical pattern is reach on third-party surfaces, with owned onboarding and renewal paths capturing loyal-customer behavior over time.

The upside is clear. Marketplaces put you in front of shoppers who are already browsing and ready to buy, and live shopping can deepen discovery and engagement. The tradeoff is just as clear: as marketplace dependence rises, fee and policy changes can capture more of your margin while limiting your control over retention touchpoints.

Before you increase channel spend, verify that discovery is turning into owned lifecycle control:

- First-time buyers can enter your owned onboarding path with low friction.

- Repeat purchase and refund behavior are visible in your reporting, not only marketplace dashboards.

- Channel fees and required ad spend still leave acceptable contribution margin after support and churn costs.

The failure mode is dependency without transfer. If marketplace or live-shopping growth does not strengthen your owned lifecycle touchpoints, you are renting demand on terms you do not fully control. As one marketplace operator put it, "eliminating selling fees can strengthen our marketplace by lowering the barriers to C2C selling," which underscores how quickly fee policy can shift channel economics. Published comparisons also show how wide the spread can be, including take-rate differences of 11 percentage points versus a typical 15% referral-fee baseline. If channel policy risk starts driving margin more than product performance, redirect investment to owned onboarding, retention messaging, and direct renewal control before buying more channel volume. You might also find this useful: Subscription Benchmark Report for Platform Operators: Churn Trials Payment Declines and LTV.

Conclusion#

The main call is simple: winning in 2027 depends less on confidence in a forecast headline and more on whether each target market is operationally ready. A projection like USD 407.31 billion of growth from 2022 to 2027 can justify attention, but it should not justify spend on its own.

The decision standard is stricter than "demand looks good." Expand only when three things are already true in evidence, not in slideware. First, your retention economics must be stable enough to trust, using the exact subscription signals you report internally: MRR, churn, and active subscribers. Those definitions are configurable, so keep the calculations consistent before you compare one market to another. Otherwise you risk funding expansion off a reporting artifact.

Second, jurisdiction checks have to be market-specific. Cross-border VAT is not a single setting because national VAT systems interact, and compliance implementation has to be adapted by country. If you are evaluating a European Union launch, OSS may materially reduce admin burden, in some cases by up to 95%. That is only useful after you confirm your offer and target-market scope actually fit the program. Treat any plan that assumes one country's setup can be copied unchanged into the next as a stop signal.

Third, money movement has to be reliable under failure, not just in a happy-path demo. Your event pipeline should be able to handle duplicate webhook deliveries safely, and your team should verify recovery for missed deliveries as well. One concrete checkpoint is whether core payment and reconciliation logic still lands correctly when undelivered events are resent for up to three days. If duplicate retries can create double actions, or delayed events break your payment records, you are not ready to scale go-to-market.

A practical next step is to run your market matrix on the top candidates you are already debating, then force a proof pack before any product or go-to-market commitment. For each market, gather:

- Retention evidence: current MRR, churn, active-subscriber trend, and the exact internal definitions used for each metric.

- Jurisdiction evidence: written VAT and compliance confirmation for that specific market, including whether any EU OSS path really applies.

- Reliability evidence: duplicate-event handling, undelivered-event recovery, and reconciliation outputs that show your payment records stay clean under retry conditions.

That is the real filter. If the market looks attractive but one of those three pillars is still unproven, keep it in discovery, not delivery. The operators who win are usually the ones who delay the wrong launch early enough to fund the right one.

Frequently Asked Questions

What should platform operators prioritize first for subscription commerce through 2027?

Start with billing health, not market headlines. The first checks should be your own MRR, churn, active subscribers, and customer MRR changes, because those show whether recurring revenue is actually getting more stable. If those signals are weak in your core market, fix retention and subscription payment processing before funding a new-country push.

Is projected market growth enough reason to expand into a new country?

No. Published forecasts can be huge. One projects USD 1043.05 billion of growth at 68.3% CAGR from 2024 to 2029, and another projects growth from $536.72 billion in 2025 to $859.52 billion in 2026 at 60.1% CAGR. That range is exactly why you should treat them as directional. If a country looks attractive on paper but VAT handling, compliance scope, or recurring collections are still unclear, delay the launch.

Which prediction signals are reliable enough to influence budget decisions?

Use signals you can verify in your own billing analytics. Customer MRR changes, churn movement, and active subscriber trends are reliable because they show upgrades, downgrades, reactivations, and churn at customer level rather than broad demand claims. A good checkpoint is whether those trends stay healthy over time in your own billing data.

How should operators choose the first vertical-country combinations to test?

Pick combinations where you already understand the recurring-payment model and the jurisdiction burden is scorable upfront. For cross-border ecommerce, that means checking VAT interaction early, since national VAT systems can interact in ways that may slow launch. If you cannot document the tax and compliance path before build work starts, it is not your first test market.

What do most subscription predictions miss about execution risk?

They usually miss the fact that demand does not remove jurisdiction friction. In digital markets, sellers often have no physical presence in the customer’s country, yet can still face obligations there, so the failure mode is assuming expansion is mostly a marketing problem. The real evidence pack should include verified billing metrics plus written confirmation of country-specific tax and compliance requirements.

Where do payment constraints and compliance gates usually derail expansion plans?

They usually break at the handoff between commercial intent and country reality: recurring collections, VAT setup, and customer or business due diligence. KYC and CDD are applied using a risk-based approach, which means there is flexibility, but not uniformity, across jurisdictions. If your team has treated KYC, KYB, AML, and VAT obligations as standard across markets, that is a red flag to stop and re-scope before budget is committed.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ftc.gov/news-events/news/press-releases/2024/10/fede...trusted

- goingdigital.oecd.org/en/indicator/72trusted

- irs.gov/forms-pubs/about-form-w-9trusted

- irs.gov/forms-pubs/about-form-w-8-bentrusted

- oecd.org/en/publications/the-2025-oecd-definition-of-...trusted

- oecd.org/en/data/indicators/composite-leading-indicat...trusted

- stripe.com/globaltrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Media Subscription Billing Decisions for Paywalls, Metering, and Bundling

**A metered paywall is only a good business decision if your billing operations can support it.** For platform founders, the real question is not whether reader revenue sounds attractive. It is whether digital publishing subscription billing and paywall metering can survive the messy parts of launch: failed renewals, entitlement sync, invoicing, tax treatment, and local payment movement.

State of Subscriptions 2026 Benchmarks for Platform Operators

Subscription benchmarks matter only if they help you make a better launch decision. For platform operators looking at the 2026 subscription benchmark cycle, the job is not to repeat market trends. It is to separate signals that justify investment from signals that only sound reassuring.

Subscription Benchmark Report for Platform Operators: Churn Trials Payment Declines and LTV

Use benchmark data as a filter, not a launch order. The real decision is not which market shows the highest headline LTV. It is which market can support your trial design, absorb payment friction, and clear compliance checks without turning early churn into noise.