Quick Answer

Start with a confidence screen: use state of subscriptions 2026 benchmarks platform operators input to frame demand, then require pilot proof on retention, payout reliability, and compliance before launch. RevenueCat and Recurly provide useful market signals, but they do not replace market-specific checks on Merchant of Record responsibility, settlement timing, and exception handling. If those gates are incomplete, treat expansion as a test, not a rollout decision.

How to Use These 2026 Subscription Benchmarks#

Subscription benchmarks matter only if they help you make a better launch decision. For platform operators looking at the 2026 subscription benchmark cycle, the job is not to repeat market trends. It is to separate signals that justify investment from signals that only sound reassuring.

Two widely used reports in this discussion are RevenueCat's State of Subscription Apps 2026 and Recurly's 2026 State of Subscriptions report. RevenueCat's report, published March 18, 2026, presents itself as benchmark guidance for subscription app growth and says its dataset covers more than 115,000 apps and over $16 billion in revenue. Recurly's report says it analyzes data from 76 million unique subscribers and 2,200 global merchants, and it explicitly frames retention as a growth engine. Those are meaningful datasets, but they do not answer the same operator questions in the same way.

That matters because platform operators are often deciding across multiple constraints at once: vertical fit, country readiness, and payment operations. A benchmark can be strong on demand-side signals and still be weak for launch planning. If a benchmark shows growth momentum but says little about how your target market collects funds, pays out users, handles tax documents, or absorbs support load, you do not have a go decision yet. You have a hypothesis that still needs operational proof.

Before you commit product or go-to-market resources, ask three questions. First, what exactly is known from the source itself: sample size, report scope, and the lens the publisher is using. Second, what is still unknown: market-level execution constraints, payment friction, compliance burden, and whether a benchmark applies cleanly to your business model. Third, what evidence closes that gap: pilot retention, channel mix, onboarding completion, payout reliability, or a documented compliance review.

One checkpoint will save you a lot of bad extrapolation: verify what the benchmark actually covers before you use it in a market decision. RevenueCat is clearly speaking from subscription app data. Recurly is clearly speaking from subscriber and merchant data. Neither report excerpt, by itself, proves that a country expansion is viable. A common mistake is treating broad benchmark momentum as permission to launch, then discovering too late that execution risk lives in settlement, payouts, tax handling, or support exceptions rather than conversion.

So read this article as a decision document, not a thought piece. Where the evidence is strong, we will treat it as usable guidance. Where it is partial, we will say so directly. And where the evidence is weak, the recommendation is simple: treat expansion as a testable assumption, not a launch plan.

If you want a deeper dive, read State of Platform Onboarding: KYB Completion, Time to First Payout, and Drop-Off Benchmarks.

What the 2026 benchmark cycle really tells operators#

Use 2026 benchmarks to frame decisions, not to approve a launch. The strongest signals here describe market pressure; the weakest signals tell you whether a specific country and vertical rollout will work.

| Signal | Published detail | How to use it |

|---|---|---|

| Competition | App growth is increasingly polarized, and store competition is getting more crowded | Directional market pressure, not launch approval |

| Growth pace | Overall subscription growth is described as slower at 12.6% | Context for planning, not proof a rollout will work |

| Cancellation pressure | 52% canceled at least one subscription in the past year due to lack of use | Retention warning before acquisition-heavy expansion |

| Reporting window | Recurly's 2026 report is described as reflecting activity through the end of 2025 | Check the metric time basis before using it in planning |

From the provided excerpts, RevenueCat gives a clearer starting scope and points to two concrete dynamics: app growth is increasingly polarized, and store competition is getting more crowded. Recurly adds useful pressure signals, especially on retention and churn, but you should confirm exact metric definitions, segment cuts, and reporting windows before using those numbers in planning.

The reporting window check is essential. Recurly's 2026 report is described as reflecting activity through the end of 2025, so a 2026 label should not be treated as proof of current-year run rate on its own.

Read the combined signals as directional: more competitive markets, slower growth (12.6%), and higher cancellation pressure (52% canceled at least one subscription in the past year due to lack of use). Platform movement across Google Play and the App Store, including Android/iOS UA shifts, can refine channel planning, but it is not enough on its own for a country launch decision.

If a benchmark cannot be tied to a specific launch choice in Software, Digital Media, Healthcare, or Education, treat it as context, not guidance. Then define what your pilot still needs to prove. For adjacent signals, see Gig Economy Payment Trends 2026: What Platform Operators Should Expect.

How to compare benchmark sources before you trust them#

Treat a benchmark as decision input only when you can verify the sample, the metric time basis, and the segmentation you need. If any of those are unclear, label it directional at best and use it to generate validation questions, not a go/no-go decision.

| Source | Sample definition | Time window clarity | Segmentation depth | Missing fields | Confidence label |

|---|---|---|---|---|---|

| RevenueCat public benchmark page and methodology notes | States the report draws on apps that use RevenueCat's platform; public page cites 115,000+ apps, $16 billion in revenue, and 1 billion+ transactions | Partial: shows year-over-year framing and historical coverage references, but not exact dates for every metric | Public slicing includes category, platform, trial length, paywall strategy, AI vs. non-AI | Full inclusion/exclusion rules, exact per-metric dates, full metric formulas | Directional (upgrade only after verifying the detailed method for the exact metric/segment) |

| Recurly 2026 report landing and related materials | States 76 million unique subscribers and 2,200 global merchants | Mixed: 2026 materials include prior-period evidence (for example, 2025 recovery figures), so metric basis needs checking | Not clear enough in public excerpts | Metric formulas, segmentation method, exact time basis by finding | Directional |

| Third-party recap (for example, Data Analysis Journal or Substack interpretation) | Typically inherits publisher sample | Often summarized rather than specified | Usually shallower than original publisher material | Original methodology, caveats, exact metric wording, exclusions | Commentary-only |

| Known unknowns for your launch decision | Is your vertical, channel, country, and plan mix represented? | Does the period match the cycle you are forecasting? | Can you isolate the slice you need? | Your pilot evidence, retention definition, cohort window | Must validate before market commitment |

Use a strict decision rule: if sample rules or metric definitions are unclear, do not treat the source as decision-grade. Large sample size can still mislead if method clarity is missing.

A practical review pass before leadership sees the deck: answer each column in one sentence using source-backed wording. If you cannot, downgrade confidence and add the gap to the known-unknowns row so it becomes an explicit pre-launch validation item.

Which benchmarks should drive go or no-go by vertical#

Use retention and churn as the primary go or no-go signals by vertical, and treat conversion as supporting context. Recurly frames retention as a growth engine, while also noting that 52% of consumers canceled at least one subscription in the past year due to lack of use, which is a clear warning against acquisition-heavy expansion without durable retention.

RevenueCat shows why conversion alone is not enough: hard paywalls can outperform freemium on trial-to-paid conversion (10.7% vs. 2.1%), but that advantage can fade over time, with one-year retention ending up nearly identical. Early churn can also hide behind strong conversion, including the pattern that 55% of 3-day trial cancellations happen on Day 0.

A vertical matrix that keeps benchmarks in their lane#

| Vertical | Benchmarks to prioritize for go/no-go | Evidence seen in benchmark | Must validate in pilot |

|---|---|---|---|

| Software | Retention and churn first; trial behavior; annual-plan durability; App Store vs Google Play mix | Recurly includes Software churn/retention comparisons. Recurly also reports annual plans can deliver 50-60% higher revenue per user with higher renewal risk. RevenueCat benchmarks behavior across Apple App Store and Google Play Store. | Whether trial-to-paid holds after early churn, whether annual buyers renew reliably, and whether store mix changes outcomes enough to alter GTM pacing. |

| Digital Media | Retention and early churn; trial behavior; annual-plan durability; store mix | Recurly includes Digital Media churn/retention comparisons. RevenueCat shows strong upfront conversion can coexist with weaker long-run durability. | Whether early cancellations, renewal behavior, and store mix support scaling assumptions. |

| Healthcare | Retention before paid scale; trial behavior; annual-plan durability; store mix | Recurly includes Healthcare in its churn/retention benchmark set. Annual-plan uplift still carries renewal-risk tradeoffs. | Whether onboarding and value realization are stable enough to support retention, and whether shorter commitments outperform annual plans. |

| Education | Retention and early churn first; trial behavior; annual vs shorter-term durability; store mix | Recurly includes Education in its vertical comparisons. RevenueCat supports reading conversion alongside long-run retention, not in isolation. | Whether cohort durability after onboarding and renewal supports expansion, and whether store channel differences require different execution. |

Those checkpoint columns keep the benchmarks in bounds. Use "evidence seen in benchmark" to set hypotheses and test order, and use "must validate in pilot" before those assumptions enter market forecasts.

What should stop scale#

If your trial-to-paid looks strong but early churn is unstable, delay GTM scale and fix onboarding and value realization first. If annual-plan performance is weaker than expected, test shorter commitments before you build expansion forecasts around annual-heavy assumptions.

Where app subscription benchmarks fail for platform operators#

App subscription benchmarks are strong demand signals, but they are not operations-readiness signals. Use them to estimate trial and conversion behavior, then separately validate whether your transaction and settlement model can support rollout in the target market.

RevenueCat's 2026 report is explicitly scoped to subscription app behavior, built from a large in-app dataset (115,000+ apps; $16B+ revenue). Appsflyer's subscription reporting similarly centers on funnel metrics such as trial adoption, conversion, and install-to-paid. That is useful for market demand, but it does not directly answer platform execution questions.

What these reports can tell you, and what they cannot#

| What app benchmarks can tell you | What they do not directly tell you |

|---|---|

| Trial starts, conversion, early cancellations, retention patterns | Who is legally and operationally responsible for transactions |

| Demand differences by category or channel | How tax and compliance responsibility is assigned in your model |

| Funnel performance trends | How cross-border settlement timing affects downstream fund movement |

Merchant of Record is the clearest boundary line. A MoR is responsible for calculating, collecting, and remitting sales tax, VAT, or GST, and carries financial, legal, and compliance responsibility for transactions. That is a different decision layer than paywall conversion performance.

The failure mode operators walk into#

Teams often over-weight the cleanest funnel chart and under-scope execution constraints. The practical check is to confirm transaction ownership and settlement mechanics before treating benchmark demand as rollout-ready.

Cross-border timing is one concrete example: traditional correspondent banking flows can take 3-5 business days to settle. For a platform that must move funds onward and reconcile balances, that timing can materially affect launch design and operator workload.

Before you commit rollout, confirm:

- your transaction model, including whether Merchant of Record applies and who owns tax/compliance obligations

- required payout capabilities in the target market

- expected settlement timing, exception paths, and responsibility for delayed or unmatched funds

If those are still assumptions, treat app benchmarks as hypothesis input, not a launch decision. This is where State of Platform Payments: Benchmark Report for B2B Marketplace Operators is the better companion read.

Country readiness checks before you commit product and GTM#

Country selection should be an operations decision, not a demand-only decision. Use this check sequence as a working gate for commit decisions: collection viability, withdrawal rails, payout reliability, then support burden.

| Gate | What to verify | Why it matters |

|---|---|---|

| Collection viability | Provider country support, accepted payment methods, settlement currency options, and whether Merchant of Record fits your transaction model | Country support is a prerequisite. If support is missing, launch is blocked; broad charging coverage does not replace country-specific settlement checks. |

| Withdrawal rails | Whether Payouts are supported for your target country and program, plus recipient bank-account requirements | Demand can look strong while funds movement still fails operationally. |

| Payout reliability | Expected arrival timing, return scenarios, and reissue handling | After initiation, payouts can still take up to 5 business days to arrive, which affects seller experience, support load, and cash timing. |

| Support burden | Ownership for unmatched deposits, returned payouts, manual reviews, and escalations | Scale depends on exception handling, not just happy-path flows. |

Start with hard availability checks. For each target market, verify directly whether Merchant of Record, Virtual Accounts, and Payouts are available where supported and enabled for your specific program. Do not assume that charging customers in over 135 currencies means your settlement setup, payout route, or legal transaction model is ready in that country.

Exception design is usually where plans break. Virtual accounts are sub-ledgers tied to a physical account, and unique virtual account numbers can improve payer identification and reconciliation. If your model depends on incoming transfers, define unmatched-deposit handling up front: required reference data, how long unmatched funds can sit, who investigates, and what support evidence is needed before crediting funds.

Set explicit payout-failure checkpoints before approval. Banks and issuers may screen payouts for regulatory reasons, so treat returns as expected scenarios. Confirm what typically triggers returns in that market, how quickly failure is visible, who reissues or reroutes funds, and when escalation starts. Repeated returns are a concrete risk: in Adyen's documented flow, 3 returned payouts can trigger a blocked payout account.

If two countries show similar demand, use cleaner operational coverage as your tie-breaker. Starting where settlement and payout unknowns are lower gives you a clearer baseline cohort before expanding. For related expansion framing, see Build a Platform-Independent Freelance Business in 90 Days.

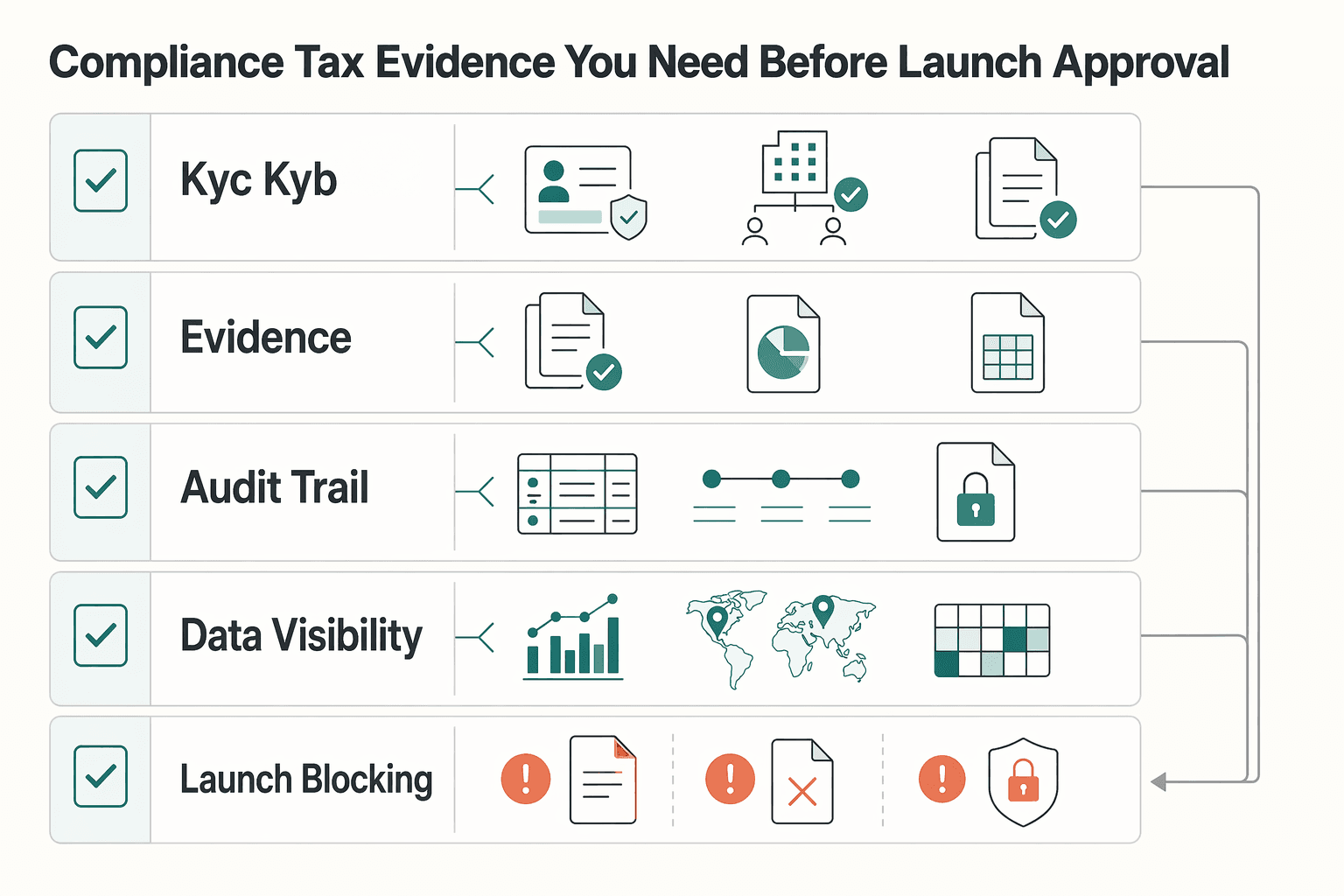

Compliance and tax evidence you need before launch approval#

Treat this as a hard gate: if you cannot produce market-specific compliance and tax evidence in writing, do not approve launch, even when demand benchmarks look strong.

| Evidence area | What to document | Specific detail |

|---|---|---|

| KYC, KYB, AML, VAT | How controls differ by market and program | KYC and AML controls are risk-based; for legal entities, KYB should include written procedures to identify and verify beneficial owners |

| Tax documents | Which documents are collected, from whom, and what triggers collection | Separate W-9 and W-8BEN logic; W-9 supports correct TIN collection, and W-8BEN is submitted when requested by the payer or withholding agent |

| Audit trail | Which records prove each decision and status change | Decision and status events should be timestamped, attributable, and tied back to the underlying transaction or ledger context |

| Data visibility | How sensitive data is masked or restricted in internal tools | PAN display should be limited to the first six and last four digits for non-authorized viewers |

| Launch-blocking tax checks | Market-specific tax readiness before sign-off | EU VAT must be market-by-market; FBAR uses aggregate foreign-account value exceeding $10,000 at any time during the year; 2026 Form 1099 revisions separate address fields into individual entry boxes |

Build the approval packet by market and by program, not as a single global checklist. KYC and AML controls are risk-based, and identity verification is expected to be done to a reasonable and practicable standard. For legal entities, KYB should include written procedures to identify and verify beneficial owners.

What has to be in the packet#

At minimum, include:

- how

KYC,KYB,AML, andVATcontrols differ by market and program - which tax documents are collected, from whom, and what triggers collection

- which audit trail records prove each decision and status change

- how sensitive data is masked or restricted in internal tools

For tax readiness, separate W-9 and W-8BEN logic. W-9 supports correct TIN collection for information-return workflows, while W-8BEN is submitted when requested by the payer or withholding agent. A generic note like "tax forms collected at onboarding" is not enough for approval.

The evidence that makes audits survivable#

Your audit trail should let reviewers reconstruct what happened and why, including record-level change history where needed. In practice, that means decision and status events are timestamped, attributable, and tied back to the underlying transaction or ledger context.

For card data visibility, confirm masking in actual tools, not just policy text. Display should be limited to the first six and last four digits of PAN for non-authorized viewers.

Tax edge cases that should block approval#

Two checks should be explicit before sign-off:

- EU VAT setup must be market-by-market, because Member States set the number and level of VAT rates within the EU framework.

- FBAR exposure should be assessed on aggregate foreign-account value exceeding

$10,000at any time during the year, not a single-account test.

Also include Form 1099 data readiness before launch. IRS Publication 1099 notes 2026 revisions that separate address fields into individual entry boxes, so loosely structured address capture can create downstream reporting cleanup. For stack planning, see Choosing a Safer Fintech Stack in 2026.

A practical sequence for the first two market launches#

Once the compliance packet exists, sequencing should come before expansion ambition. A practical approach is to run the same five-step check for both markets, use launch one to validate assumptions in a lower-complexity environment, and treat launch two as a controlled contrast case.

| Stage | What to do | Article detail |

|---|---|---|

| 1. Source confidence check | Weight benchmark inputs by transparency and depth | RevenueCat publishes explicit scope signals, including data informed by 115k apps making $16bn in revenue; use Recurly's 2026 report primarily as readiness framing for retention and payment strategy |

| 2. Vertical benchmark fit | Confirm the benchmarks match your model, retention pattern, and plan mix | If the case only looks strong on acquisition or trial conversion, test whether retention still holds once onboarding and payment friction appear |

| 3. Country operations fit | Verify payout timing, settlement handling, and exception paths before launch | Payout readiness is expansion-relevant in operator finance practice |

| 4. Compliance sign-off | Attach the market-specific approval packet, not just a status note | If a required milestone is open, treat that market as unready |

| 5. Stop conditions | Set one owner and clear thresholds where possible | Use a retention floor for the pilot cohort, a payout-failure level you will not accept, and a hard stop for unresolved compliance exceptions |

- Source confidence check. Weight benchmark inputs by transparency and depth. RevenueCat publishes explicit scope signals, including data "informed by 115k apps making $16bn in revenue" and a reported 338-page report depth, which supports deeper segmentation checks. Use Recurly's 2026 report primarily as readiness framing for retention and payment strategy, not as a direct substitute for source-depth signals.

- Vertical benchmark fit. Confirm that the benchmarks match your model, retention pattern, and plan mix. If the case only looks strong on acquisition or trial conversion, test whether retention still holds once onboarding and payment friction appear.

- Country operations fit. Verify payout timing, settlement handling, and exception paths before launch. Payout readiness is expansion-relevant in operator finance practice.

- Compliance sign-off. Attach the market-specific approval packet, not just a status note. If a required milestone is open, treat that market as unready; compliance milestones can determine whether a market is operationally open.

- Stop conditions. Set one owner and clear thresholds where possible. Use a retention floor for the pilot cohort, a payout-failure level you will not accept, and a hard stop for unresolved compliance exceptions.

If launch one fails those conditions, pause before proceeding to launch two.

Need the full breakdown? Read Choosing Creator Platform Monetization Models for Real-World Operations.

Conclusion#

The right move is not to pick the loudest benchmark. It is to build a decision path that tells you which signals are strong enough to act on, which are only directional, and which unknowns still make a launch too risky.

That matters more in 2026 because the market is not forgiving loose assumptions. Recurly describes a more mature, more competitive subscription economy, with acquisition rates stabilizing around 3% and overall subscription growth slowing to 12.6%. RevenueCat shows the same pressure from a different angle: a winner-take-more market where the top 25% of apps grew 80% year over year while the bottom 25% shrank by 33%. Those numbers are useful, but they are context, not launch approval.

Your practical rule is simple: use benchmarks to frame demand, then force the market through operations gates before you commit product and GTM spend. That means checking whether the source is decision-grade, verifying the metric window, and then asking whether your actual launch conditions match the benchmark population. A March 18, 2026 report can still reflect earlier behavior, so the freshness check is not optional if you are using it to justify expansion now.

The operator lens is lifecycle, not just acquisition. Recurly's underlying point is the one to keep: conversion, payment, and retention need to connect into one continuous loop. If trial conversion looks promising but you have not validated payment and early cohort retention in the target market, you do not have a launch case yet. You have a demand hypothesis with execution risk attached.

When evidence is incomplete, scale down before you scale up. Google Play gives you a controlled release checkpoint because you can choose the percentage of users who receive the rollout. Apple gives you another with its 7-day phased release. Use those controls to test a narrower cohort, inspect the first failure points, and close the unknowns. The common mistake is reading benchmark upside as permission to expose the full market before payment and retention signals have proved stable together.

So the final recommendation is straightforward. Treat the 2026 subscription benchmark cycle as a strong starting point, not a substitute for launch evidence. If the data source is thin or key launch evidence is still incomplete, delay scale, run the pilot, and earn the right to expand. That is slower than a headline-driven rollout, but it is usually faster than cleaning up a market launch that never should have gone wide.

Related reading: Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

Frequently Asked Questions

Which subscription benchmarks matter most for platform operators in 2026?

Retention and churn should usually sit above acquisition optics. Recurly explicitly frames retention as a growth engine, and that is a strong operator lens: if users convert but do not stay, your country or vertical expansion case is weak.

Can I use app-subscription benchmarks to decide cross-border expansion?

Not on their own. RevenueCat is clear that its insights come from a subscription app dataset, so use those numbers for demand-side patterning. Then pair them with payout, settlement, tax, and compliance checks before calling a market launch-ready.

How do I compare RevenueCat and Recurly if their methods are not equally transparent?

Start with scope, then downgrade confidence where definitions are thinner. RevenueCat publicly discloses over 115,000 apps, $16 billion in revenue, and more than 1 billion transactions. Recurly discloses 76 million unique subscribers and 2,200 global merchants. Both are useful, but if you cannot verify inclusion rules, metric windows, or segmentation depth, treat that source as directional rather than go or no-go evidence.

What should I do when benchmark sources disagree on retention or churn direction?

Do not average them. Check whether the reports are measuring the same population, the same plan mix, and the same time window, especially because at least some 2026 reporting reflects activity through the end of 2025. If the disagreement survives that check, run a pilot and make your own early-cohort retention the tiebreaker.

How much should I trust annual-plan benchmarks when market behavior is shifting?

Use annual-plan performance as a hypothesis, not a forecast anchor. Benchmark behavior may not transfer cleanly to a new market when onboarding friction or price sensitivity is different. If you see that risk, test shorter commitments before you bake annual-plan economics into launch targets.

What is the minimum compliance and tax evidence needed before launch?

You need a real evidence pack, not a status note. At minimum, that usually means documented controls for W-9 collection when a U.S. Taxpayer Identification Number is required and W-8BEN collection when requested by the payer or withholding agent. It also means AML review where your regulated exposure requires it, and VAT readiness for cross-border digital sales where non-resident supplier or platform registration may apply. Add one explicit threshold check for FBAR exposure if relevant: the IRS states the trigger at an aggregate foreign account value above $10,000 at any time during the calendar year.

How should I prioritize Google Play versus App Store signals in country selection?

Prioritize the store that matches your real channel mix, but verify both before greenlighting a country. Google Play gives a practical checkpoint because its country tables show app availability, supported currency, and price range information. Apple gives you a parallel check because it lets you release in up to 175 countries or regions where the App Store is available. If your Android share is meaningful, do not score a market as open until the Google Play country, currency, and pricing constraints are checked.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- federalregister.gov/documents/2024/08/09/2024-16546/anti-money-l...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/forms-pubs/about-form-w-9trusted

- sec.gov/about/divisions-offices/division-trading-mar...trusted

- stripe.com/resources/more/merchant-of-recordtrusted

- taxation-customs.ec.europa.eu/taxation/vat/vat-directive/vat-rates_entrusted

- appsflyer.com/resources/reports/subscription-marketingexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

State of Platform Payments Benchmark Report for B2B Marketplace Expansion

This article translates broad payments narratives into expansion decisions: where a B2B marketplace operator should launch first, what to delay, and what to validate before committing product and GTM budget in 2026.

State of Platform Onboarding Benchmarks for KYB and First Payout

Many widely shared onboarding reports are written for Customer Success and implementation teams. Recent examples say that directly. OnRamp's 2026 report surveyed 161 customer success, onboarding, and implementation leaders, and Rocketlane's 2025 report is framed as a "State of Customer Onboarding Report" based on over 950 leaders and practitioners. That perspective is useful, but it is not enough if you own payouts, compliance operations, or finance controls.

Gig Economy Payment Trends 2026 for Platform Operators

One report frames 2026 as a shift year for the gig economy, but platform expansion decisions should still be driven by operations, not headlines. Reported market signals matter, but market sizing is still directional, with global estimates ranging from $455 billion to $646 billion.