Quick Answer

Use three operator metrics: KYB completion, time to first payout, and stage drop-off. Mark KYB complete only when the case is payout-eligible under active AML policy, including beneficial-owner verification obligations under 31 CFR 1010.230. Measure stage movement from asynchronous webhook receipts, then confirm first-payout success against ledger postings, settlements, and bank-statement matching. Keep separate timers for compliance review, payout-rail setup, and manual queue aging so fixes go to the right owner.

Many widely shared onboarding reports are written for Customer Success and implementation teams#

Many widely shared onboarding reports are written for Customer Success and implementation teams. Recent examples say that directly. OnRamp's 2026 report surveyed 161 customer success, onboarding, and implementation leaders, and Rocketlane's 2025 report is framed as a "State of Customer Onboarding Report" based on over 950 leaders and practitioners. That perspective is useful, but it is not enough if you own payouts, compliance operations, or finance controls.

For a platform, onboarding succeeds only when the business can actually operate. The hard questions are not just whether a business signs up. They are whether it completes KYB, whether it becomes eligible for payouts under current KYC, KYB, and AML policy, and how long it takes to reach a first successful payout without creating audit problems later. Those are payment ops questions. They live inside your API flow, your asynchronous webhooks, and your reconciliation checks.

That is the lens for this explainer. If you use API onboarding, your platform owns the user interaction and verification collection. In practice, that means you are not just designing screens. You are deciding what evidence gets collected up front, what blocks a case, what can wait for manual review, and how you prove the process met legal and regulatory requirements in the regions where you do business.

Measurement matters as much as experience. Webhook events exist because payment lifecycles are asynchronous, so a clean onboarding metric cannot rely only on what your frontend thinks happened. A business may look complete in your product while a required verification event is still pending, or a payout capability has not actually been activated. If you do not anchor your numbers to event receipts and downstream status changes, your drop-off and time-to-payout benchmarks can look better than reality.

The same caution applies after the first money movement. Reconciliation is not a reporting extra. It is the control that matches and compares transaction records, including your internal records against bank statements and transaction data, so you can tell whether a successful first payout was truly successful in your books. If onboarding speed improves but those records do not line up, you have moved work downstream rather than fixed the process.

The goal here is practical and narrow. Define a small set of benchmarks you can trust, tie them to the control points you already operate, and use them to improve conversion and speed without loosening compliance discipline. The sections that follow focus on three measures operators can actually act on: KYB completion, time to first payout, and stage drop-off.

If you want a deeper dive, read What Is a Subscription Lifecycle? How Platforms Manage Trial Active Paused and Churned States.

Define the three benchmarks and measurement boundaries#

Define the boundary first, then calculate the metric. For platform onboarding benchmarks, count only status changes tied to compliance decisions, payout state events, and records that Finance can reconcile.

| Benchmark | Start boundary | End boundary | What to exclude or flag |

|---|---|---|---|

| KYB completion rate | A started business onboarding case, such as an account application submitted by API | Case passes required KYB checks and is eligible for payouts under current AML policy | Do not count a case as complete if documents were only uploaded or review is still pending |

| Time to first payout | First onboarding intent event | First successful payout status | Keep provider and country effects visible. A provider may document an initial payout window such as 7 to 14 days after first successful payment, but that is not universal |

| Stage drop off | Entry into each defined onboarding stage | Progression to the next stage | Measure loss at each boundary, not just final abandonment |

For KYB, completion means payout eligibility, not just activity in the queue. In U.S. AML context, 31 CFR 1010.230 requires procedures to identify and verify beneficial owners of legal entity customers, so a case with incomplete beneficial ownership verification is not complete. A practical checkpoint is a case record that shows both the verification outcome and the policy decision that enabled or blocked payouts.

For time to first payout and stage drop off, anchor measurement to webhooks and ledger events, not frontend assumptions. Webhooks can show payout status changes, but they do not by themselves prove success in your books. Confirm against settlements, bank statements, and accounting records so your benchmark reflects operational reality.

Set one shared glossary across Product, Ops, and Finance. Your data dictionary should define each metric, allowed values, and the event that closes each stage so reconciliation and reporting use the same boundary definitions.

Map onboarding stages to control points and owner handoffs#

Map each onboarding stage to one owner, one evidence set, and one stop rule. If any of those are missing, teams will close cases on effort instead of auditable proof.

Onboarding spans multiple teams and vendors, and weak ownership is linked to process gaps, misaligned priorities, and higher fraud risk. Use a stage map that Finance, Ops, and Product can all verify.

| Stage | Primary owner | Required evidence | Blocking policy gates | System-of-record fields | Escalation rule |

|---|---|---|---|---|---|

| Intake | Product or Ops intake team | Submitted business profile and contact details | Document completeness at submission | API request ID, internal case ID, idempotency key | Auto-retry transient submission errors; pause if core fields are missing |

| KYB or KYC | Compliance or Risk | Business and identity verification results | AML hold rules, unresolved verification failures | Provider reference, webhook status, review outcome | Route higher-risk cases to manual review; pause for corrected docs |

| Tax profile | Tax Ops or Onboarding Ops | W-9 for U.S. TIN collection, or W-8BEN when requested for foreign beneficial owners | Missing or invalid tax form, VAT validation where applicable | Tax form status, VAT check result, provider reference | Pause until corrected form or VAT details are supplied |

| Payout method setup | Payments Ops | Verified payout destination, including traditional or virtual accounts where supported | Incomplete destination setup or failed verification | Provider reference, webhook status, payout rail type | Auto-retry technical failures; manual review for destination mismatches |

| First payouts | Payments Ops with Finance visibility | Successful payout event and downstream posting evidence | AML block still active, payout failure, missing posting trail | Webhook status, provider payout reference, ledger journal link | Retry processor failures per policy; escalate repeated failures |

| Post-payout reconciliation | Finance or Reconciliation | Matched payout, settlement, and ledger evidence | Unmatched cash movement or missing ledger entry | Ledger journal link, settlement reference, bank statement match ID | Hold further activity pending investigation if cash and ledger diverge |

Make the evidence pack explicit#

For KYB/KYC, require the verification outcome, the policy decision, and the approving owner before progression. A document upload alone is not enough evidence.

For tax, tie the rule to the form's actual use: W-9 provides a correct TIN to payers required to file IRS information returns, and W-8BEN is submitted by a foreign beneficial owner when requested by the withholding agent or payer. If VAT applies in EU flows, record whether the number was checked through VIES.

Record the fields you need when something breaks#

Store trace fields, not just UI status labels: API request ID, provider reference, your idempotency key, the webhook status that moved the stage, and the ledger journal link once money movement has accounting impact.

Do not close a payout setup stage without provider and webhook evidence of the status change. Do not close first payout without a link from payout event to ledger posting, since the ledger entry is the accounting line item inside the parent transaction.

Escalate by failure type#

Use only three escalation paths: automatic retry for transient technical faults, manual review for higher-risk or ambiguous cases, and pause pending corrected documents when the user can fix the blocker.

| Path | Use | Examples |

|---|---|---|

| Automatic retry | Transient technical faults | Transient submission errors; technical failures; processor failures per policy |

| Manual review | Higher-risk or ambiguous cases | Higher-risk cases; destination mismatches |

| Pause for corrected docs | When the user can fix the blocker | Core fields missing; corrected docs; corrected form or VAT details |

Tie AML escalation to case risk, not queue pressure. If a webhook is missing, VAT validation is unresolved, or corrected tax forms were requested but not received, keep the case open and close it only when evidence is complete. This also keeps downstream reconciliation cleaner.

Instrument the data contract before chasing benchmarks#

Treat benchmarking as a data-contract problem first: onboarding metrics are trustworthy only when transitions are complete, retries are replay-safe, and outcomes can be traced into settlement and bank reconciliation evidence.

Onboarding status changes are often asynchronous, so each stage transition should be captured from Webhooks. But webhook visibility alone is not proof of operational truth. You still need to reconcile those transitions to Ledger impact, Settlements, and Bank Statements before calling the process improved.

Make completeness a hard gate#

If a transition is not observable, do not count it. For KYC/KYB/AML, require a recorded review outcome before stage completion. For payout setup, require an async status event instead of inferring success from UI confirmation or manual notes.

Use stage-level checks:

- transition received via

Webhooksand stored on the case - status can be matched to

Ledgerimpact once funds movement exists - downstream settlement and bank-reconciliation evidence exists before marking first payout success

Replays should never change the answer#

Retries are normal, so replay behavior must be idempotent. The same POST retried with the same Idempotency Key should resolve to the same business result, not create duplicate side effects.

Validate this with a known retry path. If a timeout-driven resend can produce a second record or a second completion count, your completion and drop-off metrics are measurement artifacts, not performance signals.

Keep separate clocks for separate delays#

Track separate timers for distinct bottlenecks: compliance review (KYC/KYB/AML), payout-rail setup (Virtual Accounts/Payouts), and internal queue latency. Different clocks map to different owners and fixes.

Keep payout-speed timing separate from compliance timing. Payout availability varies by risk and geography, and some providers note initial payouts are typically scheduled in about 7-14 days after the first successful live payment. Blending those delays into one timer hides root cause and misroutes escalation.

Related: State of Platform Payments: Benchmark Report for B2B Marketplace Operators.

Diagnose drop-off with a failure taxonomy and decision rules#

When drop-off shifts, classify failed or stalled cases before you change controls or redesign UX. Use four practical buckets: document mismatch (KYB/KYC), policy mismatch (AML/VAT), integration defects (API/Webhooks), and user confusion.

| Bucket | Examples | Check next |

|---|---|---|

| Document mismatch | KYB / KYC; missing or unreadable files; name/identifier mismatches | Compare uploaded evidence, entered form data, and rejection reasons |

| Policy mismatch | AML / VAT; policy-scope or reviewer guidance changes | Review policy changes and reviewer guidance |

| Integration defects | API / Webhooks; delayed async confirmation | Confirm a later webhook event, matching request identity, and the expected accounting trail |

| User confusion | Unclear tax-step instructions; form understanding | Make the tax step explicit about which form is required and what data is needed |

This prevents false fixes. A blurry document, a policy-scope change, and a delayed webhook can all look like abandonment in the same chart, but they require different actions.

Start with document quality before policy changes#

If verification pass rate falls, check document quality first. Compare failed KYB/KYC cases across uploaded evidence, entered form data, and rejection reasons to separate missing or unreadable files from name/identifier mismatches.

If document quality is stable, review policy changes next. AML review scope is risk-sensitive, so pass-rate movement can come from policy or reviewer guidance changes even when the user flow is unchanged.

Treat tax-step exits as an evidence and instruction problem first#

If drop-off clusters after tax collection, audit W-8/W-9 handling before tightening risk rules. W-9 is used to provide the correct taxpayer identification number to a payer filing IRS information returns, and W-8BEN is submitted by a foreign beneficial owner when requested by the withholding agent or payer.

In practice, make the tax step explicit about which form is required and what data is needed to complete it correctly. Unclear instructions often look like policy failure when the blocker is form understanding.

Keep a red-flag list for false drop-off#

Before labeling a case as abandoned, clear these red flags:

| Red flag | Observed issue | Checkpoint |

|---|---|---|

Delayed Webhooks | Asynchronous events can arrive late; retries in live mode can continue for up to three days | Confirm a later webhook event |

Missing Ledger postings | Status may have changed before the downstream reporting record is complete | Confirm the expected accounting trail |

Duplicate retries with inconsistent Idempotency Key | The same action can be counted twice instead of returning the first result | Confirm matching request identity and keep retry handling idempotent |

Use one checkpoint consistently: confirm a later webhook event, matching request identity, and the expected accounting trail. Because webhook endpoints can receive the same event more than once, deduplicate by event identity and keep retry handling idempotent so integration lag is not misread as user abandonment.

Cut time to first payout without weakening compliance controls#

The fastest compliant improvement is usually better sequencing, not looser controls. Cut time to first payout by running independent setup work in parallel, while keeping KYB, AML, and payout-eligibility gates in the required order.

Parallelize prep work, not approval decisions#

Run concurrent steps only when they do not determine each other's outcome. In practice, that can include KYB document collection, payout method setup, and tax-profile intake in parallel where your program and jurisdiction allow it. The goal is to remove idle time, not bypass approval logic.

Use one hard checkpoint: the first successful payout should map to the required approval status, not just completed intake forms. If payout initiation can happen before the governing AML or KYB decision, you have shifted risk downstream instead of reducing onboarding friction.

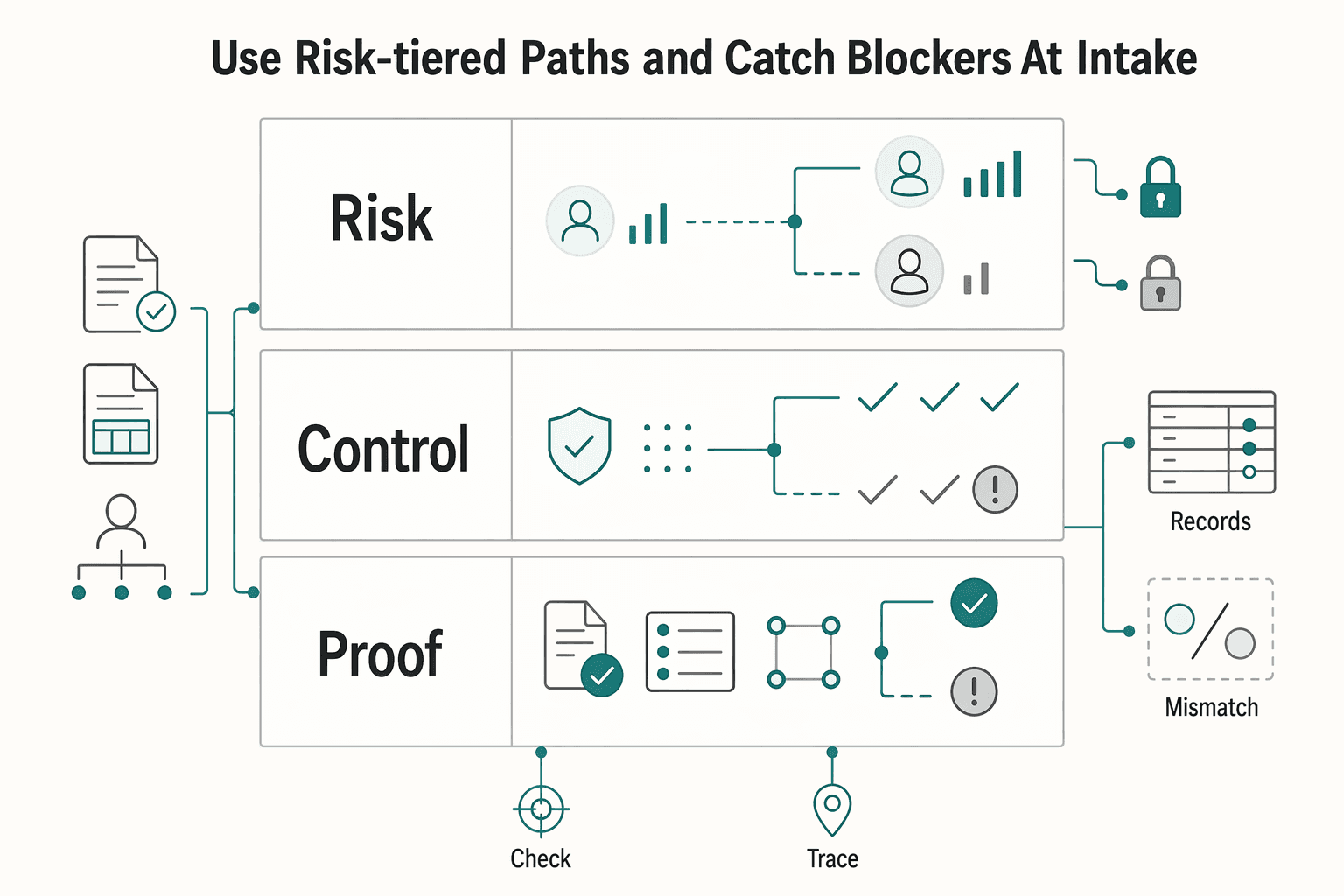

Use risk-tiered paths and catch blockers at intake#

Use a standard route for lower-risk accounts, and a stricter route for higher-risk or higher-volume profiles with tighter AML review and manual approval before payouts are enabled. That aligns speed with risk-proportionate controls instead of forcing one path for every account.

Pre-validation should happen at intake. Under 31 CFR 1010.230, beneficial owners for each legal-entity customer must be identified at account opening and verified with risk-based procedures. So collect beneficial-owner information early and check core entity details against KYB evidence before final review. If ownership details are incomplete or entity data does not match documents, stop the case early rather than rejecting it late.

Speed only counts if payout integrity still holds. Treat a gain as real only when the first successful payout still matches ledger records and reconciliation checks. Reconcile each payout with the batch of transactions it settles, and watch whether exceptions rise as time to first payout falls.

For a step-by-step walkthrough, see How to Automate Client Onboarding with Notion and Zapier.

Handle country and program variance without breaking comparability#

Comparability only holds if you keep one global schema and tag every case by jurisdiction and program. That keeps KYB, KYC, and AML differences visible instead of averaging unlike cases into one benchmark.

Use a shared structure, then require filters that map each cohort back to the rule set that governed it. FATF's risk-based approach is country-context dependent, so a published completion or drop-off metric is only trustworthy if you can trace it to the applicable market policy.

Treat availability as a qualifier, not a constant. Virtual Accounts, Merchant of Record (MoR), connected-account setups, and payout rails can vary by country and program, and virtual account provisioning can have market-specific limits. Even if a payout program can send funds to more than 50 countries, that does not make every rail or account path available in every onboarding flow.

Keep tax and reporting variance on a separate axis from onboarding completion. VAT, FBAR (FinCEN Form 114), and Form 1099-NEC are different reporting tracks, so mixing them into one completion metric makes cross-cohort comparisons less fair. When policy changes mid-trend, update the definition and annotate the trend break before you publish deltas, including dated changes such as those taking effect on 1 January 2025.

Run a weekly operator checklist and month-end control review#

Run this control cadence every cycle: clear operational friction weekly, then prove onboarding outcomes against cash movement and tax evidence at month-end.

Weekly reviews should prioritize issues that can misstate onboarding speed or completion. Onboarding and payment status changes are asynchronous, and undelivered webhook events can retry for up to three days. Before you label a case as operational delay or drop-off, check whether it is actually an undelivered-event backlog with no matching ledger or status update yet.

| Review area | Cadence | What to verify | Red flag |

|---|---|---|---|

| Stage drop-off hotspots | Weekly | Exact stage boundary losing cases by segment | "General drop-off" with no stage-level cause |

First Payouts latency | Weekly | Median and outliers by segment, separated from manual-review time | Faster onboarding reported, but no improvement in first successful payout |

Unresolved Webhooks / Ledger mismatches | Weekly | Missing or delayed event handling and unmatched journal links | Cases aging past the retry window with no resolution |

Manual-review aging for KYB / KYC / AML | Weekly | Oldest open blockers and breaches of documented escalation SLAs | Queue growth with no owner action |

Settlements, Bank Statements, and Reconciliation tie-out | Month-end | Cohorts that reached payout also appear in payout and bank reporting | Unexplained variance between onboarding output and cash movement |

For manual review, track queue aging and blocked onboarding separately. KYB/KYC/AML exceptions often get buried in blended backlogs, which hides first-payout blockers. If a case is aging and blocking payout, escalate under your documented SLA instead of waiting for the next batch review.

Month-end is the control proof point. Tie onboarding cohorts to payout reconciliation output, then to bank-level reporting that shows payout impact on cash. If successful onboarding does not map cleanly into Settlements, Bank Statements, and Reconciliation, treat it as an investigation item before publishing gains. If you need a fuller close workflow, use this month-end close checklist.

Run tax-document completeness as a separate month-end pass. Confirm domestic payees have W-9 records on file and retained for four years. For foreign payees, confirm appropriate W-8 evidence is present to establish foreign status. For contractor payments, review whether Form 1099 reporting may apply. The evidence-pack test is practical: for any sampled onboarded account, you should be able to pull the tax form, status history, and payout trail without manual reconstruction.

Conclusion#

A credible report should leave you with controls you can operate, not observations you can admire. If your benchmark set does not tell you where onboarding slows, who owns the block, and whether the account can actually reach payouts, it is not useful enough for Finance, Ops, or Product.

In practice, it still comes back to the same three metrics: verification completion, time to first payout, and stage drop off. What makes them decision-grade is the diagnostic layer underneath. You need stage boundaries anchored to real status changes, owner handoffs that explain queue aging, and a measurement rule that ties progress to money movement and compliance gates, not just form submissions or frontend events.

That matters even more in API-led onboarding, where your platform owns the account interactions and the collection of verification information. Baseline instrumentation starts with event visibility. For connected account setups, webhook coverage is not optional, and payout progress should be tracked from the webhook stream as well. If your first payout metric stops when a user finishes onboarding screens, rebuild it around the first successful payout outcome instead. Otherwise, you are measuring application completion, not operational readiness.

The checkpoints that separate a credible benchmark article from soft commentary are straightforward. First, segment by the factors that change requirements in the real world, especially legal entity type and operating country. Those differences can change what verification data is required, so pooled averages are easy to misread. Second, keep compliance integrity explicit: verification happens before payment processing and payouts, so speed work should focus on earlier collection, cleaner evidence, and fewer avoidable loops, not on weakening verification gates.

Two operator details are worth carrying forward. One is verification discipline: review requirement changes on an ongoing basis, at least once every six months, if you run custom onboarding collection. The other is a failure check. When drop off spikes, do not assume user abandonment first. Check webhook event delivery and verification-stage status changes before you label the problem as friction in the user experience.

If this article did its job, you should now be able to test your own onboarding with a sharper standard. Can you show, for a given cohort, what was required, what was collected, what was verified, when the account became payout ready, and why any case stalled? If the answer is yes, the state of platform onboarding becomes something you can manage week to week while keeping audit quality intact.

Frequently Asked Questions

What is a good benchmark set for platform onboarding beyond generic SaaS onboarding?

Use measures that map to compliance and payout eligibility, not just sign-up completion: KYB completion against required onboarding fields, first-payout readiness, and stage drop-off at asynchronous boundaries. A generic activated-account metric is too soft if the account still cannot send payouts. The checkpoint is simple: the benchmark should line up with requirement state, webhook-confirmed status changes, and payout capability state.

How should we define KYB completion rate so teams do not report inflated success?

Define completion against the provider’s requirement state, not just uploaded documents. If you use incremental collection with currently_due fields only, report that separately from a stricter up-front view that includes eventually_due, or your completion rate can overstate future readiness. A good red flag is any case counted as complete while required fields still sit in eventually_due.

What is the cleanest way to measure time to first payouts across API and manual review paths?

Use one explicit start and end definition across both paths, and treat verification completion as a gating condition before first payout is considered reachable. Pair elapsed time with requirement state and capability state (payouts_enabled, charges_enabled) so you can interpret the number correctly. If those states are missing, time-to-first-payout reporting is easy to misread.

How do we calculate stage drop-off when statuses come from asynchronous webhooks?

Count stage movement when asynchronous status is confirmed by webhooks, not when a form is submitted or a request is merely accepted. Keep a temporary pending bucket for cases where the webhook has not arrived yet, and deduplicate retries with the same idempotency key so repeat requests do not create fake exits. A common failure mode is labeling delayed async confirmation as user abandonment.

What usually causes first-payout delays: compliance review, banking setup, or internal ops queues?

There is no universal single cause, so do not assume one. Start with unmet verification requirements and account capability state (payouts_enabled / charges_enabled), then investigate operational handling for async updates and retries. This keeps diagnosis tied to observable account state instead of guesswork.

How do we speed onboarding without relaxing AML or KYC controls?

Move earlier, not looser, and keep the verification gate before payouts. The main tradeoff is collection mode: up-front collection of eventually_due requirements can reduce later interruptions, while incremental collection of currently_due requirements lowers initial friction. Whichever mode you choose, track requirement state explicitly so progress reporting stays accurate.

Which metrics must be segmented by jurisdiction or program before comparing cohorts?

At minimum, segment KYB completion, time to first payout, and stage drop-off. Also segment by onboarding requirement mode (currently_due vs eventually_due) and capability state so cohorts are comparable on like-for-like conditions. Without that, pooled averages can hide where readiness is actually blocked.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- docs.stripe.com/connect/api-onboardingtrusted

- docs.stripe.com/webhookstrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- europa.eu/youreurope/business/taxation/vat/vat-rules-r...trusted

- federalregister.gov/documents/2016/05/11/2016-10567/customer-due...trusted

- irs.gov/businesses/small-businesses-self-employed/fo...trusted

- irs.gov/individuals/international-taxpayers/forms-fo...trusted

- stripe.com/resources/more/payment-reconciliation-101trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

What Is a Subscription Lifecycle? How Platforms Manage Trial Active Paused and Churned States

Subscription lifecycle states matter only when they tell your team what happens next. In **subscription lifecycle states platform management**, a label like `Active` or `Suspended` should tell finance, billing ops, and product what changes in charges, access, edits, and reconciliation.

Month-End Close for Payment Platforms with PSP Settlement Control

Month-end close often breaks down when PSP settlement is treated as a side reconciliation. For payment platforms, settlement is often the clearest record of what cash should have moved, so it should drive the close rather than being checked after journals are drafted. If you run close across multiple PSPs, you need that settlement record to lead the review before your team starts defending journal entries.

State of Platform Payments Benchmark Report for B2B Marketplace Expansion

This article translates broad payments narratives into expansion decisions: where a B2B marketplace operator should launch first, what to delay, and what to validate before committing product and GTM budget in 2026.