Quick Answer

Start with a two-stage evidence packet: a minimal first-pass proof set and a full fallback file. For the future of financial identity, AI is most useful as a packaging layer that turns uneven freelance records into verifiable income summaries reviewers can check quickly. That helps in mortgage and compliance queues, especially when you meet self-employed thresholds such as 25% business ownership and lenders examine a two-year earnings pattern. Required documents still apply; the gain is fewer avoidable clarification cycles.

The Sovereign Professional: A Framework for Owning Your Financial Identity#

You do not need a manifesto. You need an evidence stack you control: records that are easy to verify, easy to reuse, and limited to what each reviewer actually needs.

The credibility gap shows up in routine work: mortgage underwriting, repeated client onboarding checks, and payment-platform risk reviews. In some transfer workflows, verification checks can delay completion by 5 to 14 working days, and reserves can hold funds to cover refunds, disputes, and reversal risk. The goal is practical: reduce avoidable friction without pretending underwriting, KYC, or risk rules have disappeared.

Where the credibility gap shows up#

The problem is usually not that you lack evidence. It is that review systems still expect standardized inputs, and independent professionals rarely fit those defaults cleanly. A salaried employee with one payroll source often fits the template. A professional with several clients, uneven monthly income, or a business entity behind the work often does not, even when the underlying records are solid.

| Profile | Income/source pattern | Fits the template? |

|---|---|---|

| Salaried employee | One payroll source | Often fits the template |

| Professional | Several clients | Often does not |

| Professional | Uneven monthly income | Often does not |

| Professional | Business entity behind the work | Often does not |

If you own 25% or more of a business, Fannie Mae treats you as self-employed. For Fannie Mae loans, lenders generally expect a two-year prior earnings history, plus analysis of income stability and business continuance before approval.

The same pattern shows up in onboarding and payments. US banks must run risk-based Customer Identification Program procedures to form a reasonable belief they know the customer's true identity. Payment platforms also run risk reviews tied to fraud, disputes, and chargebacks. In practice, the bottleneck is often format and verification speed, not a total lack of proof. A reviewer may have enough evidence in theory, but not in a form that is easy to scan, compare, and confirm on first pass.

That is why the fix is not more paperwork. It is better-prepared inputs. When your first packet is clear, matched, and scoped to the exact question, you lower the odds of a second round spent explaining inconsistencies that were really packaging problems.

A better input model#

A useful approach is a dual-track model: required documents plus verifiable, minimal-disclosure proofs. A verifiable credential is a standardized digital claim from an issuer that can be checked for tampering. The W3C Verifiable Credentials Data Model v2.0 is now a Recommendation, published 15 May 2025.

The key is sequencing. Lead with the smallest proof set that answers the reviewer's immediate question, and keep the deeper file set ready if the case moves to manual review. That does not replace required filings. It can improve the odds that the first reviewer understands your profile quickly enough to move the file forward without avoidable back-and-forth.

| Review point | Legacy input model | Verifiable credential input | First-pass review speed | Documentation burden | Privacy exposure |

|---|---|---|---|---|---|

| Mortgage review | Full tax returns, transcripts, bank statements, manual explanations of variable income | Signed income or stability proof with required tax documents behind it | May speed first-pass review when facts are easy to verify; does not replace required filings | Less upfront back-and-forth, though full returns may still be requested | Lower if initial sharing is limited to needed income facts |

| Client compliance onboarding | Repeated uploads of ID, address, tax, and vendor forms | Reusable identity and compliance attributes from an issuer | May reduce re-verification time across clients because proofs are checkable | Fewer duplicate uploads | Lower through field-level sharing |

| Payment risk review | Contracts, invoices, explanation emails, historic statements after a flag | Prebuilt identity, ownership, or income-pattern proof | Can shorten response prep when a review starts; reviews still happen | Smaller emergency packet during triggered checks | Lower if only relevant fields are disclosed |

In practice, separate three things that often get mixed together: the underlying record, the proof derived from it, and the workflow packet for a specific counterparty. Once you treat those as separate layers, you stop rebuilding the same evidence from scratch every time someone asks for it in a slightly different format.

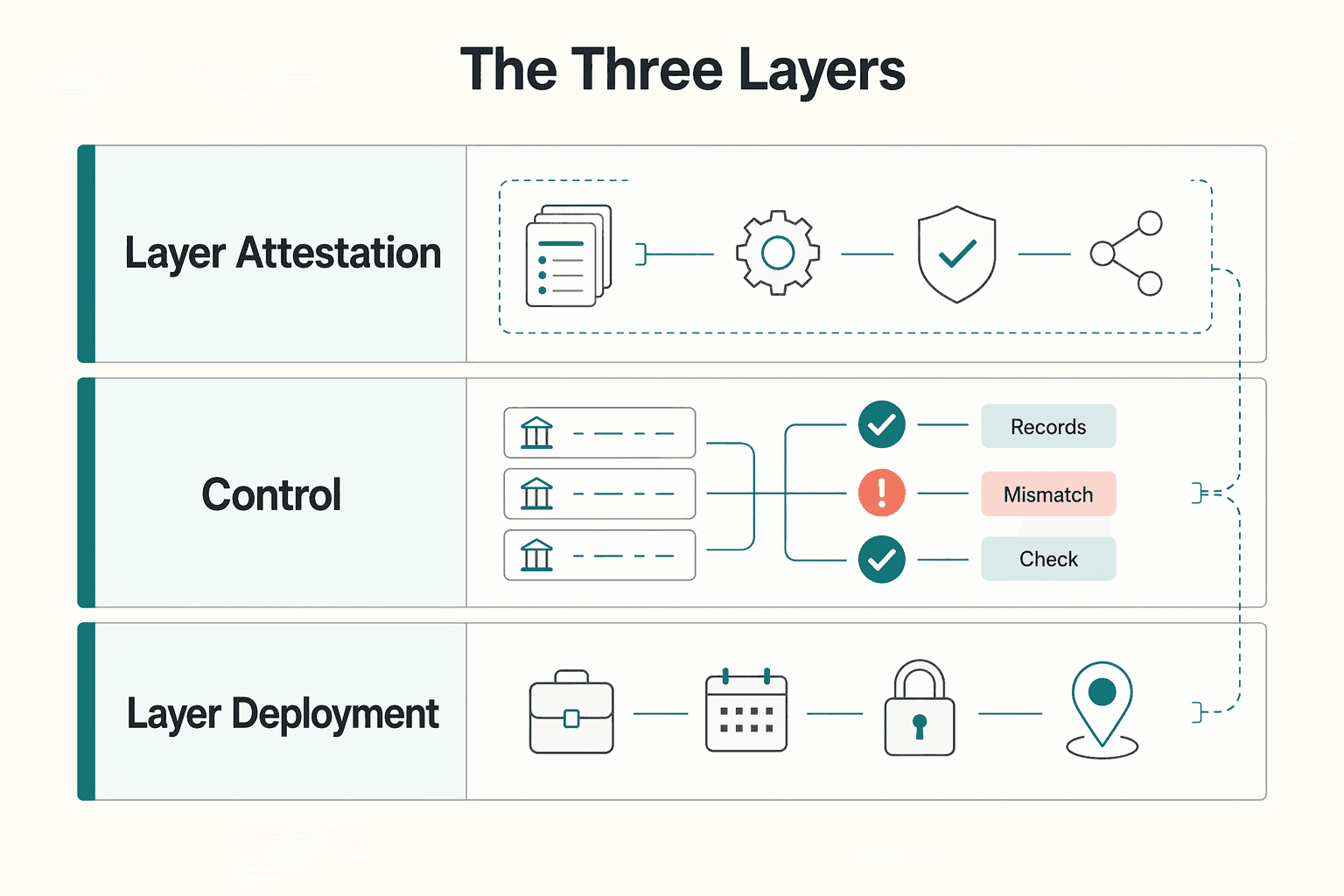

The three layers#

A practical setup has three layers. First, build strong underlying records. Then turn those records into reusable proofs. Finally, package them for the workflows where delays cost the most.

| Layer | Prepare | Generate | Deploy first |

|---|---|---|---|

| Layer 1: Attestation | Tax transcripts or returns, business bank statements, invoice history, and payout records that reconcile | Proof artifacts for reviewer questions, for example verified income history, stability proof, and core identity fields | Mortgage workflow; if transcript detail is insufficient, expect fallback to full returns, schedules, or forms |

| Layer 2: Control | Identity and compliance attributes you repeatedly share | Credentials you hold and present from your own wallet | Client onboarding and platform checks where selective disclosure helps |

| Layer 3: Deployment | Scenario-based packets before reviews start | A ready first-response bundle per workflow | Mortgage; client compliance; payment risk |

Layer 1: Attestation (prepare -> generate -> deploy). This is where you turn raw records into proof artifacts a reviewer can use quickly.

- Prepare: tax transcripts or returns, business bank statements, invoice history, and payout records that reconcile.

- Generate: proof artifacts for reviewer questions, for example verified income history, stability proof, and core identity fields.

- Deploy first: mortgage workflow, where self-employed documentation pressure can be high. If transcript detail is insufficient, expect fallback to full returns, schedules, or forms.

The operational test for this layer is simple: can a reviewer look at your packet and understand the income story without hunting through unrelated files? If not, the records may be accurate but still hard to use. Your summary proof should point clearly to the supporting records behind it, and those records should reconcile in sequence.

If a reviewer opens the packet and sees gaps between deposits, invoices, and reported income, you are likely headed for manual review. That can happen even when each document is technically valid on its own.

Layer 2: Control (prepare -> generate -> deploy). This matters if you keep answering the same identity and compliance questions across different counterparties.

- Prepare: identity and compliance attributes you repeatedly share.

- Generate: credentials you hold and present from your own wallet.

- Deploy first: client onboarding and platform checks where selective disclosure helps. SSI and DID-based models are designed around holder control, and selective disclosure lets you reveal only specific fields instead of entire files.

The practical win here is not novelty. It is reuse. If you repeatedly send the same identity, address, tax, or vendor information, holder-controlled presentation can reduce duplicate handling and limit over-sharing. The core discipline is deciding in advance which attributes you commonly disclose, which ones require a fallback document, and which ones you share only when a reviewer specifically asks. That keeps you from sending a full document set by default when only a narrow fact is needed.

Layer 3: Deployment (prepare -> generate -> deploy). This is where preparation starts paying off. The goal is a ready first-response packet for each common review path.

-

Prepare: scenario-based packets before reviews start.

-

Generate: a ready first-response bundle per workflow.

-

Deploy first:

-

Mortgage: send summary proof with formal documents so the income shape is clear early. - Client compliance: lead with reusable identity and tax attributes. - Payment risk: keep contracts, invoices, delivery evidence, and core identity and earnings proofs ready for sudden reviews.

This layer is less about storage and more about timing. Under pressure, you can send too much, send the wrong version, or forget the one record that ties the story together. A scenario-based packet avoids that. For a mortgage review, the packet should make it easy to trace the business context, the income pattern, and the supporting records in one pass. For client onboarding, it should answer routine compliance questions without forcing you to rebuild the same set each time.

For a payment risk review, it should let you respond quickly with records that show who you are, what was sold, and how the activity fits your normal earnings pattern.

Build each packet to work in two stages: first-pass review and fallback review. The first-pass set is narrow and easy to verify. The fallback set is heavier and ready if the reviewer escalates. That structure reduces panic when a request suddenly expands from "send proof" to "send the full file."

Guardrails#

This only works if the records underneath are clean and current. Start with these guardrails:

| Guardrail | What to check | Note |

|---|---|---|

| Data quality | Names, dates, entity names, and account identifiers match across returns, invoices, and bank records | Check before issuing anything |

| Credential refresh | Refresh credentials when underlying facts materially change | There is no universal cadence |

| Fallback document pack | Keep transcripts, full returns or schedules, statements, contracts, invoices, or delivery records ready | Wallet-based proofs can open the process, but some reviewers still require these documents |

It also helps to test your own packet the way a reviewer would. Open the files in order. Confirm that the naming is consistent, that the dates make sense together, and that the packet answers a concrete question rather than just dumping records into a folder. If a reviewer has to infer the timeline, the relationship between entities, or which account belongs to which activity, expect delay.

The fallback pack matters for a second reason: acceptance is still uneven. Even where selective disclosure is possible, some counterparties still want the familiar document set because that is what their workflow accepts. If you prepare only the credential layer and ignore the conventional documents, you have not reduced friction. You have only postponed it.

Built this way, your financial identity becomes a reusable process: cleaner inputs up front, full documentation in reserve when deeper review is required. If you want a deeper dive, read Should Your Freelance Business Accept Credit Cards?. Before you apply for financing, organize your residency and compliance evidence in one place with the Tax Residency Tracker.

Conclusion: Your Identity Is Not a Liability - It's Your Leverage#

Treat verification as an operating discipline, not a last-minute scramble. This will not guarantee approvals or instant onboarding. It can reduce avoidable friction, make your profile easier to verify, and strengthen your position when lenders, clients, or platforms ask for proof. The practical shift happens in three places:

- From reactive to prepared: Prepare before the request arrives. For lending, keep an up-to-date income summary, business context, and issuer-backed records ready. For onboarding and payment-risk reviews, make sure names, dates, entity details, and account identifiers match across files so your materials are consistent for review.

- From over-sharing to selective disclosure: Send the minimum evidence that answers the exact question. Where supported, verifiable credentials and selective disclosure let you share specific claims without exposing full records. Where not supported, use your fallback document set.

- From applicant to asset holder: Manage your records as reusable verification assets. If you meet self-employed thresholds such as 25% ownership, expect continued focus on income stability, business viability, and generally a two-year earnings history. Keep both a credential pack and traditional documents ready.

In practice, that means maintaining a reusable credential pack, reviewing and refreshing it regularly, and keeping fallback documents for institutions that are not yet credential-ready. Before each new client, platform, or financing request, run your checklist and send only the minimum proof needed. The less you improvise under deadline, the easier it is to present a financial identity that is coherent, verifiable, and ready for real-world review.

Related: What is a 'Financial Identity' and Why Do Nomads Need One?.

If you want a more reliable collect-to-payout workflow with clear status visibility and audit-ready records, review Merchant of Record for freelancers.

Frequently Asked Questions

How do you prove income for a mortgage when your income is uneven?

Use the reviewer’s stated requirements as the source of truth, then provide a clear summary of your income pattern with matching supporting records. A clear summary can help first-pass review, but it does not replace required documentation. Before submitting, check that names, dates, entity details, and account identifiers line up across files. Organize the packet so each summary figure is traceable to underlying records for the same review period.

What is self-sovereign identity for finance?

Avoid treating any one workflow as universal. Use it only where a verifier supports that format, and keep standard documents ready for fallback. Also keep the acronym clear: in SSA materials, SSI means Supplemental Security Income. SSA updates key Social Security figures yearly, including Social Security Update 2025.

Can you use this approach for tax residency proof?

Treat it as a packaging workflow, not a guaranteed acceptance path. Define the exact period under review, align each record to that period, and confirm acceptance criteria in advance with the reviewer. Clear period labeling keeps the scope explicit.

Why do payment platforms freeze or review freelancer accounts?

The practical response is to keep a ready packet so you can answer review requests quickly with consistent records and context. To reduce avoidable back-and-forth, keep contracts, invoices, payout history, and your timeline organized together before a review starts.

Is this actually secure?

Security depends on operational controls, not labels. If your setup relies on cloud services, Treasury identifies monitoring, auditing, and testing as a practice area, and flags insufficient transparency and exposure to potential operational incidents as challenges. Treasury also states its cloud report does not create new requirements and is not intended to endorse or discourage specific providers. So the practical step is to verify each tool’s access controls, recovery process, and incident handling before trusting it with core records.

What is the difference between eKYC and self-sovereign identity?

Use this as an operating comparison with caution. Confirm performance, privacy, and adoption outcomes with the relevant authority before relying on either model. | Aspect | eKYC | Self-sovereign identity | | --- | --- | --- | | Grounded technical definition | Confirm with the relevant authority | Confirm with the relevant authority | | Verified performance/adoption outcomes | Verify with the verifier | Verify with the verifier | | Operational decision point | Follow verifier requirements | Use only where verifier supports it, with fallback documents ready | | Acronym caution | SSI in SSA context means Supplemental Security Income | Do not use SSI here to mean self-sovereign identity | The practical decision is compatibility: use the reviewer's required process and preserve fallback records.

Will this work everywhere yet?

Plan for mixed requirements and confirm acceptance criteria with each counterparty before submission. A reusable process still helps: keep one consistent evidence backbone, then package it to match each reviewer's stated requirements.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- consumerfinance.gov/compliance/circulars/circular-2022-03-advers...trusted

- consumerfinance.gov/rules-policy/final-rules/required-rulemaking...trusted

- digital-strategy.ec.europa.eu/en/factpages/european-digital-identity-wallettrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- selling-guide.fanniemae.com/sel/b3-3.5-01/underwriting-factors-and-docum...external

- w3.org/news/2025/the-verifiable-credentials-2-0-fam...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Should Your Freelance Business Accept Credit Cards?

Offer card payments, but stay in control of how money reaches you. The goal is not a smoother checkout screen. It is predictable cash you can use to run the business.

What is a 'Financial Identity' and Why Do Nomads Need One?

Your financial identity should function as portable proof. It can help you get paid across borders, clear reviews faster, and control risk when your life does not fit the one-address, one-employer, one-country model many institutions still assume.

No Official Stability Report for a Freelance Mortgage

If you are looking for a "stability report," pause here. In the Fannie Mae Selling Guide materials shown here, there is no borrower document labeled a "stability report." What you do see is the Selling Guide itself, with a downloadable PDF, plus Ask Poli and Guide Resources for policy questions and related forms.