Quick Answer

Choose based on operating fit, not the cheapest package. For dubai free zones for e-commerce, compare how each option supports your actual sales model, documentation quality for account checks, processor readiness, and expansion path. DMCC, IFZA, and Dubai CommerCity can all work, but only when their activity scope, paperwork sequence, and cost breakdown match how you plan to run the business after incorporation.

Introduction: Moving Beyond the Brochure#

When you compare dubai free zones for e-commerce, start with operating risk, not branding. The real question is whether the setup will support bank account onboarding, satisfy your payment processor's verification demands, keep total setup cost clear, and still hold up as the business gets more complex.

That friction often shows up during onboarding, sometimes after incorporation. UAE financial institutions must verify customer identity under CDD and KYC rules. Payment providers such as Stripe may ask for UAE-issued licensing documents, owner details, and proof of an active business bank account. If your paperwork is incomplete, outdated, or mismatched to what the business actually does, onboarding can slow down quickly. Stripe also notes that payouts or processing can be paused if renewed verification documents are not provided.

That is why the cheapest-license question is often the wrong place to start. A lower headline fee can become expensive later. You may find the activity scope is too narrow, a third-party approval is required, or your bank wants a fuller compliance pack than you prepared. Before you apply, confirm the exact licensed activity, the shareholder and UBO details you will need to maintain, and whether any owner at 25% or more will need separate identity documentation for payment onboarding.

This guide is structured to help you decide in the right order. First, audit your business model. Next, use a scorecard to judge each zone on bankability, payment fit, cost, and scale. Then compare the main zone options side by side. Last, match the choice to your 5-year growth plan so you do not overpay for credibility you do not need or underbuy the structure your business will soon require. If you want a deeper dive, read Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers.

Step One: Audit Your Business Model#

Audit your operating model before you compare zones, because most delays come from mismatch: your licensed activity, your documents, and your payment setup are not aligned. Your goal is simple: keep one consistent business story from application to invoicing so you can move from legal formation to a running company with banking in place.

Audit what you sell#

Start with how you actually earn revenue, not a broad label. That affects licence wording, logistics needs, and the documents you should prepare early.

| Operating model | Ask yourself first | What this changes | Keep ready now |

|---|---|---|---|

| Digital services | Are you selling your expertise, delivery time, or managed execution? | Activity wording, scope clarity, and invoicing consistency become the priority | Service descriptions, proposals, sample invoices, matching website copy |

| Digital products | Are you selling downloads, software access, or subscriptions? | Payment flow, refund handling, and product terms matter more than warehousing | Product descriptions, terms, refund policy, ownership details |

| Physical goods | Do you hold stock, dropship, or use third-party fulfillment? | Logistics becomes central; some zones market warehousing, logistics, and digital payment support, so verify fit directly | Supplier details, product list, fulfillment model, shipping and returns process |

| Hybrid | Are you combining products, services, and digital add-ons? | Activity mismatch risk increases, so your activity set must reflect each revenue line | One plain-English summary covering every revenue stream |

Write one two-sentence description of your business and reuse that exact wording everywhere: forms, emails, website, invoices, and bank conversations. Small wording changes can trigger extra questions.

Audit where your customers pay from#

Map customer geography before setup. Your customer mix drives which payment rails, settlement currencies, and gateway options you need to confirm directly with providers.

Use a simple planning sheet:

| Customer region | Expected payment methods | Preferred settlement currency | Gateway/provider status |

|---|---|---|---|

| Region 1 | Payment methods pending provider verification | Settlement currency pending provider verification | Confirm current availability directly with provider |

| Region 2 | Payment methods pending provider verification | Settlement currency pending provider verification | Confirm current availability directly with provider |

| Region 3 | Payment methods pending provider verification | Settlement currency pending provider verification | Confirm current availability directly with provider |

Do not assume a zone choice automatically gives you the rails you want.

Audit founder path and documentation readiness#

Choose your founder path early, then prepare documents to match.

- Resident-founder path: align identity and address details across visa, company, and banking records.

- Non-resident-founder path: build a complete, internally consistent documentation pack from day one and keep your business description identical across channels.

Audit your financial stack before setup#

Run this checklist before you speak with a formation agent:

| Check | What to pin down |

|---|---|

| Bank account capabilities | Which bank account capabilities are non-negotiable for your operations? |

| Primary and fallback gateway | Which gateway is mission-critical, and what is your fallback if onboarding is declined or delayed? |

| Chargeback/refund pattern | Is your chargeback/refund pattern low, moderate, or high? |

| Marketplace or partner onboarding | Do your target marketplaces or partners require specific company documents for onboarding? |

If you may operate in a zone with higher audit expectations, build document discipline early. For example, one DMCC-focused audit-preparation source lists trade licenses, financial transaction records, bank statements, and tax registrations as documents auditors may request.

Take those answers into Step Two and convert them into a weighted scorecard so your decision is evidence-led rather than brochure-led.

Step Two: The CEO's Scorecard for Vetting a Free Zone#

Use your Step One audit to score each zone the same way. If a zone is cheap but weak on bankability or payment onboarding, eliminate it early.

Start with one hard gate before scoring: can the zone issue the right licence for what you actually sell? UAE guidance requires an appropriate e-commerce licence, and Federal Decree-Law No. 14 of 2023 covers both digital and physical goods and services sold through technology platforms. If activity fit is unclear, stop and clarify before you proceed.

Then score the zone across four pillars.

| Pillar | What you are testing | Weight |

|---|---|---|

| Bankability | Whether your company file will look complete and credible to UAE banks | 35 |

| Payment-gateway readiness | Whether your primary and backup processors can onboard you with your real model | 25 |

| True cost | What setup, renewal, and scale-up actually cost beyond headline pricing | 20 |

| Operational substance and stability | Whether you can show the business is active, consistent, and document-ready | 20 |

Score each pillar from 1 to 5, convert to weighted points, and total to 100. Use this formula: (pillar score ÷ 5) × weight. As a practical rule, treat scores under 70 as weak unless the zone solves a specific non-negotiable need.

Make bankability and payment readiness evidence-based#

For bankability, score document readiness, not brochure reputation. CBUAE rules require institutions to identify and verify customers using reliable, independent sources and to collect proof of an active licence. Build your file around that.

| Review area | What to verify | Article detail |

|---|---|---|

| Bank onboarding documents | Which incorporation documents are issued at setup, and whether they are typically accepted for business account onboarding | CBUAE rules require institutions to identify and verify customers using reliable, independent sources and to collect proof of an active licence |

| Founder and UBO KYC | What founder KYC is usually requested for your nationality and residency status | Identity, address, and beneficial-owner/control details |

| Address or workspace evidence | What proof-of-address or workspace evidence is expected | ADCB and Mashreq NeoBiz list items like a trade licence, constitutional/incorporation documents, address proof, and authorized-signatory paperwork |

| Payment processor onboarding | What exact entity and owner documents are required, what manual-review triggers are common, and what fallback provider you have | Stripe may require ownership/control verification; PayPal Business activation includes identity and bank-account verification |

Use these verification prompts:

- Which incorporation documents are issued at setup, and are they typically accepted for business account onboarding?

- What founder KYC is usually requested for your nationality and residency status (identity, address, beneficial-owner/control details)?

- What proof-of-address or workspace evidence is expected?

- What extra review friction is common for your model?

For practical document planning, bank pages such as ADCB and Mashreq NeoBiz list items like a trade licence, constitutional/incorporation documents, address proof, and authorized-signatory paperwork.

For payment gateways, verify current onboarding requirements directly. Stripe lists the UAE in supported countries and may require ownership/control verification. PayPal Business activation includes identity and bank-account verification. Your score should drop if your licence wording, website, invoices, and terms do not match, because that often triggers manual review.

Use these gateway prompts:

- What exact entity and owner documents are required at onboarding?

- What are the common manual-review triggers for your business model?

- What is your fallback provider if your first-choice processor declines?

- Do your product pages and refund terms support a clean compliance review?

Model cost in three buckets, not one headline number#

| Cost bucket | Include in your model | Current fee range |

|---|---|---|

| One-time setup costs | Licence issuance, incorporation/registration docs, establishment/immigration file setup, visa processing if needed | Current fee range pending official/free-zone verification |

| Recurring compliance costs | Licence renewals, facility/desk renewals if applicable, document reissue charges, required annual admin or audit-related administration where applicable | Current fee range pending official/free-zone verification |

| Optional operating costs | Extra activities, visa quota expansion, workspace upgrades, insurance, logistics/warehouse services, payment setup-related service costs | Current fee range pending official/free-zone verification |

Insist on an itemized quote. DMCC states its fees can change without prior notice, so old quotes are not decision-grade. Also verify activity limits and add-on pricing. Dubai CommerCity states a base licence includes three activities from the same group, with paid add-ons, and also describes a DET dual-license path without separate physical office space.

Define operational substance before approvals test you#

Operational substance means showing a real operating business, not just a registered shell. In practice, that usually means:

- A workspace/address setup that fits your licence path

- A live website and business materials that match your stated activity

- Clear founder/staffing intent for how operations will run

- Organized records and a consistent document narrative across licence, banking, and gateway files

This matters because approvals are easier when your file is coherent and verifiable.

Quick risk-flag filter#

| High-risk signals | Favorable signals |

|---|---|

| Vague or mismatched activity wording | Clear licence-to-business fit |

| No clear proof-of-address/workspace path | Named document pack and readiness checklist |

| Hidden mandatory add-ons | Itemized quote with setup vs renewal clarity |

| No concrete fallback if first bank/gateway declines | Explicit fallback bank/gateway path |

| Website, invoices, and application tell different stories | Consistent story across all documents and channels |

Apply this same scorecard to DMCC, IFZA, and Dubai CommerCity in the next section so your comparison stays consistent.

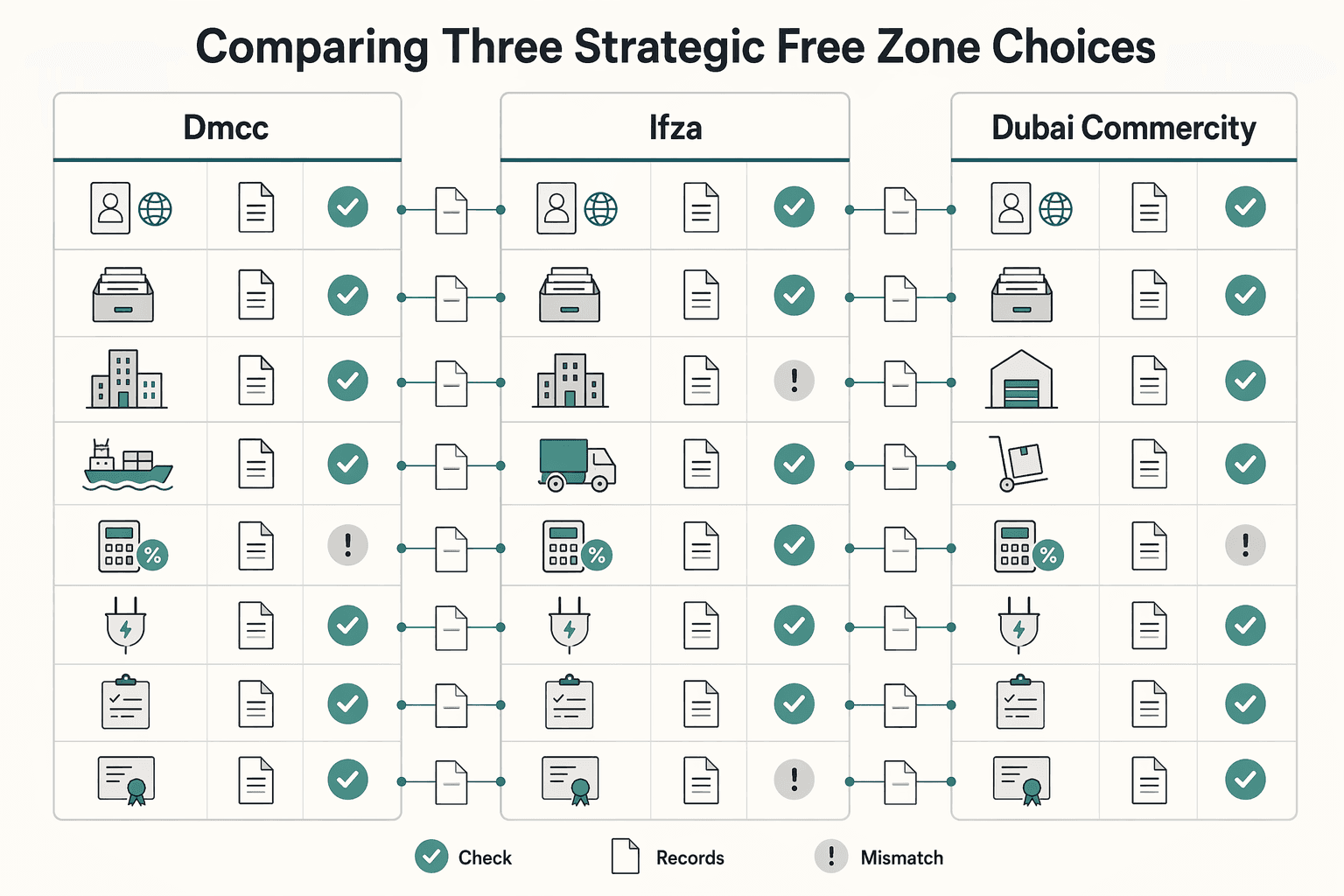

The Playbook: Comparing Three Strategic Free Zone Choices#

Keep your scorecard open. Do not pick the zone with the strongest pitch. Pick the one that gives you the clearest, verifiable fit for your licence scope, onboarding file, and operating plan.

A useful benchmark is EY's SEZ cost-competitiveness framework (13 Dec 2024). It does not rank DMCC, IFZA, and Dubai CommerCity for e-commerce, but it shows the right method: compare multiple cost buckets, not a headline fee. The framework looks at labor, facility acquisition, office space, transport and logistics, taxes, utilities, business registration, and licensing.

| Zone | Business model fit | Onboarding friction | Operational flexibility and scaling path | Cost buckets to build | Proof points to request | Choose this if / Avoid this if |

|---|---|---|---|---|---|---|

| DMCC | Ask for exact activity wording and match it to your real sales flow, website, and invoices. | Request the full incorporation document pack and the expected KYC/UBO checklist before payment. | Get written clarity on workspace options, adding activities, and scaling from founder-only to staffed operations. | Setup, recurring, and expansion cost bands pending official/free-zone verification. | Bank introduction process, payment-provider onboarding expectations, office/substance options, and logistics compatibility if you ship goods. | Choose if you get specific answers in writing that score well on your framework. Avoid if answers stay high-level and verification is weak. |

| IFZA | Confirm the proposed activity wording covers what you sell now, not only future plans. | Test whether the quote and checklist are complete before formation fees are paid. | Ask how visas, added activities, and team growth change your operating setup over time. | Setup, recurring, and expansion cost bands pending official/free-zone verification. | Itemized quote, sample document pack, realistic KYC expectations for your profile, and fallback path if first-choice onboarding fails. | Choose if transparency and documentation quality are strong. Avoid if low entry pricing is clear but ongoing add-ons are vague. |

| Dubai CommerCity | Check that the licence path matches your model, especially if fulfillment and returns are part of operations. | Ask what additional documents are expected when inventory movement is involved. | Map what changes as you add warehousing, staff presence, or wider distribution. | Setup, recurring, and expansion cost bands pending official/free-zone verification. | Logistics partner compatibility, workspace/substance options, onboarding document expectations, and payment-provider requirements for your category. | Choose if your model needs a clearly documented logistics path. Avoid if your operation is mostly digital and extra operating layers do not support your plan. |

A common mistake is deciding from sales calls alone. Before you commit, reconcile your real operating model with the exact activity wording and checklist you are being asked to sign against. If those do not align, treat that as unresolved risk and pause.

Also model your staffing path early. EY's framework includes labor, and it explicitly flags employee cost of living as a hiring and retention factor. If you expect UAE hiring in the next 12-24 months, ask each zone how your operating footprint changes with headcount.

Shortlist by scorecard fit, not headline price. Move forward with the zone that gives you verifiable licence fit, clear documentation, and transparent cost buckets. Cut options that stay vague. For a step-by-step walkthrough, see How to Get a Business License in Dubai as a Freelancer.

Step Three: Align Your Choice with Your 5-Year Growth Plan#

Choose the zone that creates the least rework in your next growth phase, not the easiest year-one setup. In practice, rework usually shows up when you hire, change operating footprint, or move from fully digital sales into hybrid or physical operations.

| Growth check | What to confirm | Article detail |

|---|---|---|

| Visa capacity path | What changes when you move from founder-only to employees, what extra quota route exists, and whether workspace upgrades are tied to headcount | DMCC publicly refers to additional visa quota, and Dubai CommerCity includes employee visa processing in its setup flow |

| Admin complexity | Which growth steps trigger new documents or approvals | Added activities, extra visas, workspace upgrades, and any mainland operating step |

| Cost model | Current cost requirement for each growth event, pending official/free-zone verification | Extra visas, workspace changes, activity amendments, warehouse space, and any DET licensing or permit requirement |

Map your most likely next move before you commit:

- If you plan to stay digital: prioritize licence wording that still fits when your offer expands, plus practical banking support and a clear team-scaling path.

- If you may go hybrid: validate in advance how added activities, staffing, and operating scope are handled.

- If you expect warehousing or fulfillment: treat legal route and logistics fit as early-stage decisions, not later clean-up.

UAE guidance requires the appropriate e-commerce licence and applies to both digital and physical goods and services, so a narrow setup can become a constraint faster than expected.

Use this expansion checklist before you sign:

- Visa capacity path: confirm what changes when you move from founder-only to employees, what extra quota route exists, and whether workspace upgrades are tied to headcount. DMCC publicly refers to additional visa quota, and Dubai CommerCity includes employee visa processing in its setup flow.

- Admin complexity: confirm which growth steps trigger new documents or approvals, including added activities, extra visas, workspace upgrades, and any mainland operating step.

- Cost model: build line items for each growth event and leave each current cost requirement pending official/free-zone verification: extra visas, workspace changes, activity amendments, warehouse space, and any DET licensing or permit requirement.

Your biggest risk is not growth itself; it is changing operating model without confirming the legal path. If you may operate outside your free zone later, ask directly about Executive Council Resolution No. (11) of 2025 and the Free Zone Mainland Operating Permit launched by DET on 8 October 2025, then get the route, exclusions, and required documents in writing.

| Zone | Stronger fit for your next phase | Network outcomes to verify | Future-fit risk |

|---|---|---|---|

| DMCC | You expect a broader build with more staff, higher bank scrutiny, or a more formal operating footprint. | DMCC states it has more than 26,000 businesses and offers banking support that can fast-track account applications. Verify the exact bank-introduction path, team-scaling process, and whether warehouse options up to 700 sqm matter for your model. | You may pay for a more structured setup earlier than needed if you remain lean and mostly digital. |

| IFZA | You want remote setup now with broad activity coverage and a path from shared desk to private office as you grow. | IFZA states remote setup, over 800+ activities, and partnerships with UAE banks and EMIs. Verify which growth steps remain partner-led under its B2B model and what support looks like as complexity increases. | Low-friction entry can turn into added admin later if hiring or operating footprint expands quickly. |

| Dubai CommerCity | You expect hybrid or physical-commerce operations where warehousing, fulfillment, and returns are core. | DCC is positioned as a dedicated e-commerce free zone, lists employee visa processing and bank account opening support, and highlights logistics infrastructure for warehousing, fulfillment, and last-mile delivery. Verify whether its DET dual-license route matches your mainland plan. | If you stay mostly digital, you may carry extra operational structure before you need it. |

Use one decision prompt: which option has the lowest expected rework across your next phase, including likely licence, staffing, workspace, and mainland-operating changes.

Conclusion: Make the Confident, De-Risked Decision#

The costly mistake is usually not choosing a zone with a higher headline fee. It is choosing the cheapest-looking setup before you know whether your company can clear banking and payment onboarding once it is live. That is where a small saving can turn into delays, rework, and lost revenue.

Keep the decision sequence simple. First, confirm business-model fit. If you are a digital business, prioritize smoother banking review and a clean fit between your activity and documents. If you sell physical goods, check logistics depth first, because a zone like Dubai CommerCity is purpose-built for e-commerce logistics. Among dubai free zones for e-commerce, the right answer is the one that matches how you actually operate, not the one with the lowest entry price.

Next, test bankability and payment-rail readiness before you sign anything. Banks and payment gateways may not assess every zone the same way, so pressure-test how your model is likely to be reviewed before you commit. A good sign is clear, specific guidance. A red flag is broad reassurance with no detail.

Then confirm the full setup scope and true costs. You want clarity on what is included at setup and what may surface after incorporation, rather than relying on a bundled headline number.

The comparison itself is straightforward. Prioritize credibility when cleaner banking is critical. Treat speed claims as zone-dependent and verify timelines for your case. Prioritize logistics depth when inventory, fulfillment, or returns are part of the business. Before you sign, run one final check: business-model fit confirmed, bank and payment scrutiny reviewed, true costs clarified, and scalability pressure-tested.

Frequently Asked Questions

How do you check the real setup cost before you pay?

Start by asking what is actually included in the package, not just the headline license fee. For example, Meydan’s FAQ says its 0 visa license includes a Lease Agreement and an LLC-FZ Trade License with three groups of business activities, while Shams says it currently accepts 100% upfront payments. Ask for a line-item quote that separates the license, lease, and any immigration-card or visa-allocation related charges. If the quote stays bundled, stop and ask for a revised breakdown. | Use case | Better first check | Evidence to request | |---|---|---| | You want visa-linked setup clarity | Meydan | Written confirmation of immigration card and visa allocation sequence, plus the visa route that applies to your shareholding | | You need to protect cash flow before filing | Shams | Written payment schedule confirming the 100% upfront policy and whether any bank-based installment option is outside the free zone | | You are setting up with a corporate shareholder | Meydan | Full parent-company document list, including Certificate of Incorporation, Certificate of Incumbency, Memorandum and Articles of Association, and Board Resolution |

What should you verify about banking support?

Check the process, not the promise. Shams states that it provides a bank contact list and has Sharjah Islamic Bank and RAK Bank representatives in office for queries. Ask for that list before you submit anything, and ask which documents banks typically pre-screen first. If the zone cannot explain the expected UBO paperwork, treat that as a red flag rather than assuming the account will sort itself out.

Does residency change what you need to do?

If residency matters to your timeline, verify the order of steps in writing. Meydan states you can apply for a visa after incorporation only if you have the immigration card and visa allocation. It also says Investor or Partner visa eligibility applies if you have invested AED 50,000 share capital or more in the company. If you are below that threshold, ask what visa route applies instead of assuming the partner visa route will work.

How do you judge logistics fit without relying on marketing claims?

Ask the zone to map your actual operating model: digital only, stock holding, returns, third-party fulfillment, or your own delivery chain. Then request the exact license activity wording, any lease requirement, and any extra approvals or documents for physical goods if relevant. If they answer with a generic “e-commerce is covered,” but cannot show the document path, assume the setup may be too narrow for your model.

How do you reduce payment gateway surprises?

Check the provider’s current UAE eligibility page and compare it against your proposed activity wording before incorporation. Then ask the free zone what post-incorporation documents you will receive. At Meydan, the FAQ lists Certificate of Formation, Share Register, Business License, Lease Agreement, and MOA, which gives you a concrete document checklist to confirm in writing. If your activity wording is vague or your UBO file is incomplete under Cabinet Decision No. (58) of 2020, fix that before you apply.

What should you do before you apply?

Do this in order. Get the exact activity wording and visa sequence in writing. Request the full document list for your ownership structure, especially if a parent company is involved. Ask for the post-incorporation document pack you will receive. Reconfirm all requirements immediately before submission, because Shams notes that terms can change on UAE government instruction.

Try a related tool

An international business lawyer by trade, Elena breaks down the complexities of freelance contracts, corporate structures, and international liability. Her goal is to empower freelancers with the legal knowledge to operate confidently.

Priya is an attorney specializing in international contract law for independent contractors. She ensures that the legal advice provided is accurate, actionable, and up-to-date with current regulations.

Sources

Includes 6 external sources outside the trusted-domain allowlist.

- investindubai.gov.ae/en/business-setup/free-zone-companies/free-z...trusted

- support.stripe.com/questions/uae-account-activation-requirementstrusted

- gruv.ai/blog/comparison-of-dubai-free-zones-for-e-co...external

- ifzabusinesssetup.com/2025/09/02/ifza-free-zone-company-setup-faqs...external

- ifzabusinesssetup.com/2025/09/11/setting-up-an-e-commerce-business...external

- rulebook.centralbank.ae/en/rulebook/32-customer-and-beneficial-owner...external

- tulpartax.com/ecommerce-business-in-a-dubai-free-zoneexternal

- u.ae/en/information-and-services/business/ecommerceexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

How to Manage Your Time Effectively as a Freelancer

*By Marcus Thorne, Productivity & Operations Expert | Updated February 2026*

Indian Gig Economy in 2026: Treat Platform Income as Variable Until Settlements Prove Stability

---