Quick Answer

Use the 76 million figure as a vendor benchmark, not a market census. Recurly ties it to data from 2,200 businesses, while Grand View, Market.us, and Juniper publish different forecast scopes and windows. Build a one-page comparison first, then require an evidence pack with source origin, methodology, segment definition, and geography coverage. Only fund roadmap or GTM expansion after those checks and your first launch slice passes compliance and lifecycle checkpoints.

What the 76 Million Signal Means for Platform Builders#

Subscription growth headlines are useful only until you have to fund product work, choose a launch market, or hire against a forecast. For platform builders, the real question is not whether subscription models are gaining traction. It is which claims are scoped tightly enough to support a decision, and which are only directional signals.

That is the lens for this piece on subscription economy growth trends platform builders 76 million: not to force one master number out of a mixed set of sources, but to separate market narrative from execution reality and turn that into a sequence you can use.

The source base here is intentionally narrow. Recurly presents the "76 million subscribers" figure as data from its own subscriptions report, and in a related analysis says it examined data from 2,200 subscription businesses and 76 million unique subscribers. That matters because it ties the figure to a specific dataset, not automatically to a market-wide total.

HTF Market Intelligence publishes a distinct forecast for the global subscription economy market, including a stated growth rate of 18.7%. Market.us Scoop publishes a different trajectory, projecting the market to grow from USD 487.0 billion in 2024 to USD 2,129.92 billion by 2034. Fulcrum Digital adds a looser but still useful signal, describing subscription-based models as a trend gaining traction in e-commerce.

Those are not interchangeable inputs. If one source is talking about a vendor dataset, another about a market forecast, and another about editorial trend framing, you should not average them into a single planning baseline. Before your roadmap, hiring plan, or GTM target references a headline number, confirm the source origin, the market definition, the time horizon, and the geography. If any of those are unclear, treat the number as context, not as a commitment trigger.

The biggest risk is false precision. Teams often see a large subscriber count, a strong CAGR, and a big dollar forecast and assume they all describe the same market from different angles. The material here does not support that. It supports a narrower and more useful conclusion: there are signals of momentum in subscription models, but the evidence comes from different scopes and methods, so your first job is to normalize definitions before you choose a vertical, a region, or a capability set.

The rest of this article follows that operator sequence. First, compare what each source is actually measuring. Then validate whether the evidence matches your target segment. Only after that should you sequence rollout and GTM spend with clear go or no-go checkpoints.

Define the market before you trust the growth number#

Use this as a gating rule: a platform-focused subscription view is not the same scope as the broader subscription economy market, so you should not plan from those numbers as if they are interchangeable.

Before any CAGR reaches your roadmap or hiring plan, put each claim into one comparison view with source, scope, geography, and market type. Grand View describes a broad market segmented by business model, subscription type, industry vertical, and region. Juniper highlights trends in subscription management platform solutions, which is a narrower product lens. Recurly's 76 million unique subscribers across 2,200 businesses is a vendor dataset signal, not a neutral whole-market baseline.

| Source | What it covers | Geography note | Market type |

|---|---|---|---|

| Grand View | Subscription economy market segmented by business model, subscription type, industry vertical, and region | Region is explicitly part of scope | Whole-economy |

| Market.us | Subscription economy market forecast | Not clear in excerpt | Whole-economy |

| Juniper | Subscription management platform solutions trend lens | Not clear in excerpt | Platform-focused |

| Recurly | Vendor dataset (2,200 businesses, 76 million unique subscribers) | Global dataset | Vendor signal, not baseline |

If market definitions differ, do not average the growth rates. Grand View's 13.3% (2025-2033) and Market.us's 15.9% (2025-2034) should be treated as separate scenarios with separate investment cases.

Use one case for broad market expansion and another for platform capability demand, for example retention, flexibility, and automation. If you cannot show source, scope, geography, and market type on one page, the growth number is still directional, not decision-grade.

Related: Subscription Fraud Trends for Platforms: How to Detect Free-Trial Abuse and Card Testing.

Compare vertical demand where monetization and ops actually align#

Pick the vertical where your lifecycle operations can reliably support the monetization model, not the one with the loudest growth headline. If your lifecycle controls are still weak, prioritize simpler retention mechanics before you move into more engagement-sensitive models.

Recurly's 2026 benchmarks are useful here because they compare outcomes by industry, including Software and Digital Media, across 76 million unique subscribers and 2,200 global businesses. Statista also supports keeping e-commerce in scope, noting that subscription models now reach "all corners of the e-commerce industry in both digital and physical form."

As one subscription product leader put it, "Competitive edge lies in knowledge, and benchmark data is the secret ingredient that can shape and accelerate your growth strategy."

| Vertical | Revenue predictability | Churn volatility | Implementation complexity |

|---|---|---|---|

| SaaS | Often steadier when ongoing value is clear | Varies by product and recovery performance | Usually centers on billing rules and access-state correctness |

| Media & OTT / content subscriptions | Can scale well, but is sensitive to engagement and renewal timing | More sensitive to lifecycle friction, especially return/reactivation flows | High operational sensitivity around pause, reactivation, trial-to-paid, and access timing |

| E-commerce subscriptions | Can repeat well, but depends on cadence and offer design | Varies with lifecycle flexibility and fulfillment reliability | Recurring billing must stay synchronized with physical operations |

Use benchmark signals as checks, not universal laws. In Recurly's data, 1 in 4 new sign-ups are returning subscribers, pause usage among top merchants rose 337%, and 2025 recovered revenue differed by vertical ($155M+ in Software vs nearly $100M in Digital Media). Those signals support one practical rule: validate lifecycle resilience before you scale demand assumptions.

For prioritization, run three evidence checks per vertical before you commit:

- Billing logic complexity: verify your core recurring flows run cleanly under normal and recovery states.

- Pricing flexibility needs: verify plan and state changes do not create avoidable lifecycle friction.

- Failure tolerance: verify a failed lifecycle event does not cascade into broken access or fulfillment.

Choose regions by constraint load not headline growth#

Choose region sequence by compliance and operating load first, then demand. North America may lead market-share summaries, but that is context, not a launch order by itself. One 2024 estimate places North America at more than 45% share and USD 219.15 billion in revenue, which is useful for sizing, not readiness.

Use North America and LATAM as a contrast set before you commit rollout. North America offers visible demand and clearer documentation paths, but it is not one ruleset. LATAM has distinct subscription demands and challenges, and even commonly cited evidence spans six countries and 6,400 subscribers rather than a single regime. If you treat either region as administratively uniform, launch sequencing usually breaks.

Build the matrix before the revenue model#

Before engineering or GTM commitment, map each target jurisdiction across these three checks:

| Check | What to confirm | Example |

|---|---|---|

| Auto-renewal rules | Consent, disclosure, reminder, and cancellation expectations in the exact market | California's Automatic Renewal Law amendment effective July 1, 2025 |

| Tax localization | Where recurring digital transactions require localized treatment | OECD VAT digital toolkits include Latin America and the Caribbean |

| Data privacy regulations | Collection, use, storage, and processing mapped to governing law | Canada: PIPEDA; Brazil: LGPD |

The predictable failure mode is shipping a functioning checkout, then discovering renewal language, tax treatment, or data handling is wrong for the first live market.

Make PCI-DSS a launch gate#

Treat payment security as a go/no-go gate, not post-launch cleanup. PCI DSS defines baseline technical and operational requirements for protecting payment account data, and PCI DSS v4.0.1 is the current publication marker for planning.

Your launch evidence should identify PCI scope ownership, card-data touchpoints, inherited provider responsibilities, and remaining operator controls. Using a processor does not remove the need to verify scope and ownership.

If unresolved questions across auto-renewal, tax localization, privacy, and PCI exceed your current legal and ops capacity, delay the region even when demand signals look strong.

Set non-negotiable platform capabilities before GTM spend#

Set your minimum platform capabilities before acquisition spend. If recurring billing works but lifecycle visibility and churn response do not, GTM spend usually scales waste instead of durable revenue.

Use a baseline that is hard to waive: recurring billing, lifecycle analytics, churn prediction, pricing controls, and basic personalization. This is not a claim that every platform in the market uses one universal checklist. It is a practical threshold to avoid the common pattern where conversion grows but retention, recovery, and pricing execution lag.

| Capability | Why it is non-negotiable | What to verify before launch |

|---|---|---|

| Recurring billing | Subscription models are built on recurring revenue and ongoing customer relationships. | Confirm the billing layer reliably handles your first paid plan, renewal, and cancellation path. |

| Lifecycle analytics | Strong execution is treated as one loop across conversion, payment, and retention. | Check that your event model connects those stages for your first two target segments. |

| Churn prediction | Churn prediction is now treated as an operational capability, and one industry report says 40% of companies have begun using AI for revenue recovery and churn prediction. | Verify churn signals trigger an action, not just a dashboard view. |

| Pricing controls | Vendor positioning now includes direct pricing and retention workflow actions, not only reporting. | Test whether your team can change plan logic, offers, or packaging without a long engineering cycle. |

| Basic personalization | Lifecycle performance depends on treating subscriber states differently as they move through conversion, payment, and retention. | Confirm at least one segment-specific intervention or retention flow for each launch segment. |

Risk mapping matters more than feature labels. Weak lifecycle analytics plus weak churn response usually means paid acquisition waste, because you cannot isolate whether losses come from fit, failed payments, onboarding, or pricing friction. Weak pricing controls create a different issue: you can see problems but cannot respond fast enough.

Use vendor claims as category signals, not requirements#

Use Recurly Compass claims as a category signal, not a day-one requirements list. The October 16, 2025 launch frames lifecycle support as action-oriented, with claims about launching growth plays, adjusting pricing, and triggering retention flows, powered by 15+ years of data and released with over 30 new features.

Juniper reporting also treats AI and automation in subscription management platform solutions as a current trend area. So when a vendor says "AI-powered growth," ask for operational detail: what it predicts, what it changes, and where in the subscriber lifecycle it acts.

Scope to the first two segments#

For your first two target segments, keep a short evidence pack: billing journey, event coverage across conversion/payment/retention, churn signal inputs, pricing-change path, and one live personalized intervention. If that pack is missing, delay additional GTM spend. A common mistake is buying feature breadth before proving execution depth.

For a step-by-step walkthrough, see Indian Gig Economy in 2026: Treat Platform Income as Variable Until Settlements Prove Stability.

Build an evidence pack that validates the 76 million claim before commitment#

Treat the 76 million figure as unverified outside Recurly's own reporting. In the provided excerpts, HTF Market Intelligence and Market.us focus on market size and CAGR projections, and Fulcrum Digital uses Netflix's subscriber count as an example. None independently validates Recurly's statement that its 2026 report analyzes data from 76 million unique subscribers across 2,200 global merchants.

Use the number as a proprietary dataset signal, not a confirmed market baseline. The operational risk is turning a headline figure into a hiring, roadmap, or expansion commitment before you can trace how that figure was produced.

| Evidence pack item | What you need to see | Red flag |

|---|---|---|

| Source origin | Who sponsored the research and who conducted it | Summary claims with no clear sponsor or producer |

| Methodology transparency | Data collection strategy, inclusion rules, study window, and enough detail for independent review | Headline count with no explanation of how records were collected or filtered |

| Segment definition | Whether the count represents one vendor dataset, a platform-market estimate, or a broader subscription-market estimate | Mixed scopes presented as one market fact |

| Geography coverage | Which regions are represented and what "global" covers in practice | Global label with no country or regional breakdown |

AAPOR disclosure standards are a useful checkpoint because they require enough detail for independent review and verification, including source origin and collection strategy. Hold the line on this: do not tie roadmap or hiring commitments to a subscriber headline unless the methodology is traceable. If it does not pass that test, keep it in narrative context, not budget planning.

Sequence rollout in phases with explicit go no-go checkpoints#

Treat expansion as gated execution, not momentum: launch one vertical in one region first, and move only when compliance readiness and lifecycle measurement are reliable.

| Phase | Scope | Go/no-go checks |

|---|---|---|

| Phase 1 | Use a narrow launch slice so failures are diagnosable | Payments scope is clear; auto-renewal mapping is jurisdiction-specific; lifecycle instrumentation is decision-ready |

| Phase 2 | Expand only after the first slice is stable enough to trust | Pause GTM expansion if retention-readiness or compliance-readiness is missed; avoid changing region scope and pricing model scope at the same time unless attribution remains clear |

| Phase 3 | Add a second vertical or region only with a fixed checklist | Legal constraints; payment operations readiness; support load; analytics completeness |

Phase 1#

Use a narrow launch slice so failures are diagnosable. Gate launch on three checks:

- Payments scope is clear: PCI DSS is a baseline for entities involved in payment card processing, so map what card data touches your product, vendors, and support workflows before GTM spend.

- Auto-renewal mapping is jurisdiction-specific: in the U.S., auto-renewal obligations span states and the District of Columbia, so review flows against the jurisdictions you plan to serve rather than a generic "U.S. compliant" label.

- Lifecycle instrumentation is decision-ready: if product, payments ops, and compliance cannot inspect the same subscriber journey with aligned definitions, your retention read is not trustworthy yet.

Phase 2#

Expand only after the first slice is stable enough to trust. Recurly frames retention as a growth engine, but also reports that 52% of consumers canceled at least one subscription in the past year, so noisy lifecycle data is a no-go for scaling.

Avoid changing region scope and pricing model scope at the same time unless attribution remains clear. If Phase 1 misses your retention-readiness or compliance-readiness checkpoint, pause GTM expansion and close the gap first.

Phase 3#

Add a second vertical or region only with a fixed checklist so decisions stay comparable across launches:

- Legal constraints: confirm local auto-renewal, privacy, and tax handling; for EU expansion, include OSS registration/filing mechanics, platform record-keeping obligations, and the cited EU-wide threshold of EUR 10 000.

- Payment operations readiness: verify ownership for retries, refunds, reconciliation, and renewal-failure escalation.

- Support load: confirm support can classify billing and cancellation contacts by region and plan.

- Analytics completeness: ensure lifecycle reporting is segmented by vertical, region, plan type, and payment outcomes; if pause is part of retention strategy, measure it directly (Recurly reports 337% year-over-year pause growth where pause-before-cancel was offered).

Treat release artifacts as gate inputs, not admin overhead: keep a decision log, assumption register, risk register, and named sign-off owners across product, payments ops, and compliance. If an owner cannot sign due to unclear PCI-DSS scope, incomplete legal mapping, or incomplete analytics, treat that as a no-go.

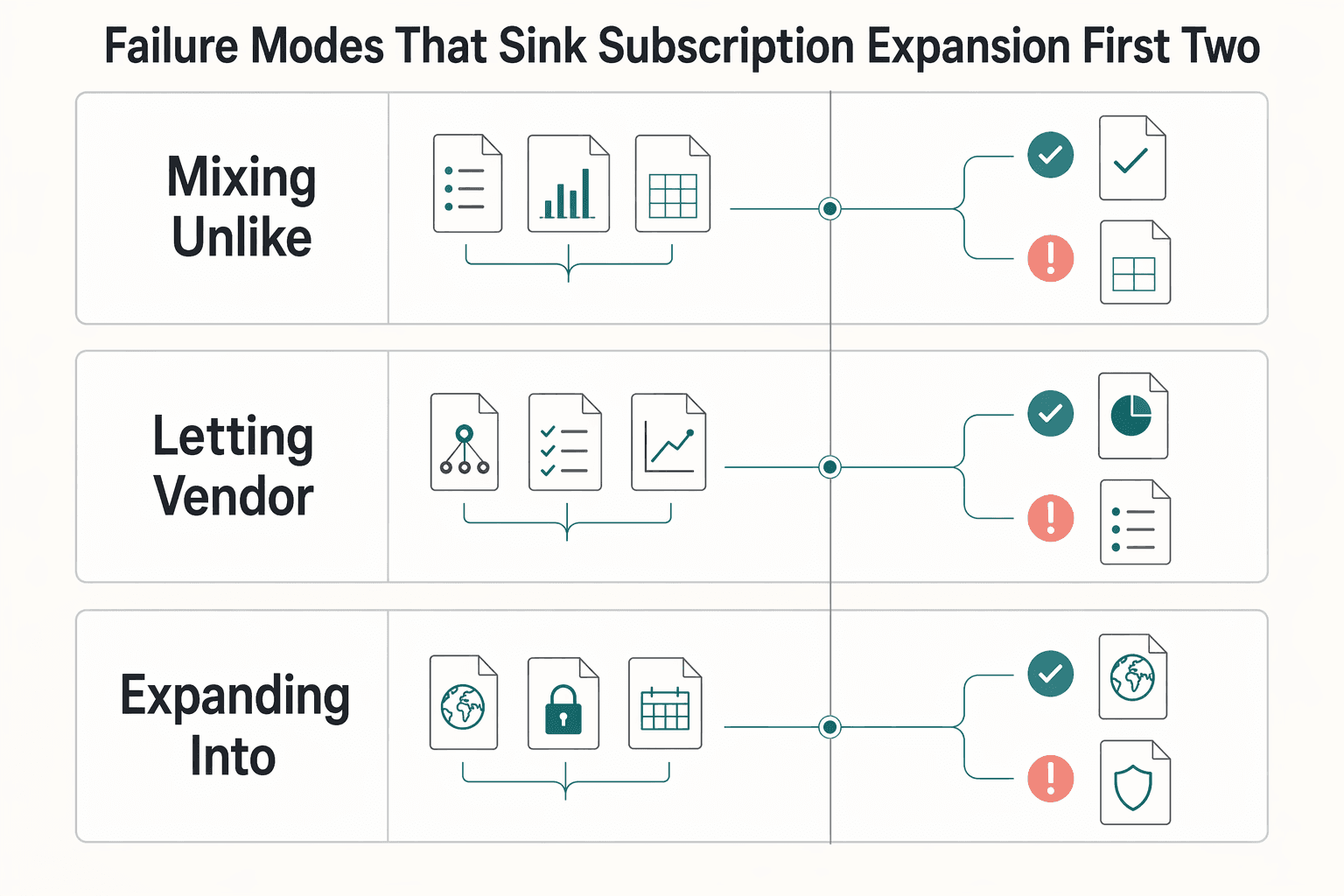

Failure modes that sink subscription expansion in the first two quarters#

The fastest way to derail early expansion is false certainty, not weak demand. Teams commit roadmap, hiring, and regional launch plans before they normalize market scope, vendor evidence, and compliance load.

| Failure mode | Grounded signal | Preventive step |

|---|---|---|

| Mixing unlike market definitions | 18.7% growth and USD 78.5B to USD 385.2B by 2033 vs 15.9% CAGR and USD 487.0B in 2024 to USD 2,129.92B by 2034 | Require a one-page comparison of segment definition, geography, and whether each figure describes the broad economy or the platform layer |

| Letting vendor benchmarks drive build order | Recurly: 76 million unique subscribers and 2,200 global merchants; Zuora: activity on Zuora Billing | Use vendor reports as a checklist, then test each capability against your launch slice |

| Expanding into regions before tax and privacy are mapped | EU VAT One Stop Shop includes record-keeping requirements for online marketplaces/platforms; personal-data protection rules apply inside and outside the EU | Require a region matrix covering tax handling, filing path where relevant, data collection points, and lifecycle processors before go-live |

Mixing unlike market definitions#

Do not treat similarly named market figures as interchangeable inputs. One cited summary projects 18.7% growth and a path from USD 78.5B to USD 385.2B by 2033, while another reports 15.9% CAGR and growth from USD 487.0B in 2024 to USD 2,129.92B by 2034. Those differences are large enough that averaging into one TAM creates planning error.

The scope boundary is the real issue. Market.us segments by service types such as content, product, service, and membership subscriptions, while Juniper discusses stakeholders from subscription management providers to regulators and subscription providers. If you treat these frames as equivalent, staffing and sequencing usually drift. Before you approve headcount, require a one-page comparison of segment definition, geography, and whether each figure describes the broad economy or the platform layer.

Letting vendor benchmarks drive build order#

Use vendor benchmarks as directional signals, not neutral baselines. Recurly says its report analyzes 76 million unique subscribers and 2,200 global merchants, and Zuora describes its index as activity on Zuora Billing. Both can inform priorities, but neither is the full market.

This failure mode usually shows up as capability overbuild in the wrong sequence. Instead of copying a mature platform's marketed stack, validate what your first vertical and region need to renew cleanly. Use vendor reports as a checklist, then test each capability against your launch slice.

Expanding into regions before tax and privacy are mapped#

Regional expansion stalls when tax and privacy obligations are not mapped into operations before launch. In the EU, VAT One Stop Shop includes record-keeping requirements for online marketplaces/platforms, and the European Commission states personal-data protection rules apply inside and outside the EU. If those requirements are discovered late, monetization often gets delayed by rework.

Make this a document gate, not a verbal check. Require a region matrix covering tax handling, filing path where relevant, data collection points, and lifecycle processors before go-live.

Ignoring lifecycle instrumentation compounds these risks. In Media & OTT and high-velocity e-commerce subscriptions, diagnosis becomes slower and less reliable when renewals, retries, cancels, refunds, and reactivations are not reconciled by plan and region. The common symptom is clear: churn rises, but the team cannot confidently separate pricing effects from issuer behavior, cancellation UX, or compliance-copy friction.

Conclusion#

Once you stop treating every growth headline as interchangeable, the decision gets clearer. The right move is not to anchor on the biggest number. It is to pick the market definition, vertical, and region mix your team can actually support with clean billing logic, credible evidence, and enough operational capacity to survive the first launch slice.

That matters because the source spread here is real, not cosmetic. You are looking at materially different frames: Recurly's report prompt around 76 million subscribers, Grand View's 13.3% CAGR from 2025 to 2033, Market.us at 15.9% from 2025 to 2034, and Juniper's $722bn in 2025 to $1.2tn in 2030. Those are not plug-compatible planning inputs. The 76 million figure is useful as a vendor-scale signal, but not as a neutral market census. Market.us also makes clear that scope can vary by service type and vertical, which is exactly why source normalization has to happen before TAM slides, hiring plans, or roadmap promises.

A practical closeout rule is simple: if you cannot explain what a number includes, where it came from, and which segment it actually describes, do not let it drive spend. The first verification checkpoint should be a one-page comparison table covering source, forecast window, segment definition, geography coverage, and whether the claim describes a platform category, a broader subscription market, or a vendor dataset. The second checkpoint is an evidence pack with methodology notes, assumptions, and named owners for sign-off across product and operations.

If you need a sharp recommendation, start there before you commit GTM or major build work. Then sequence execution around the operating realities highlighted in the source guidance: retention, flexibility, and automation. Recurly's own framing is strongest as a product-direction cue, not a market baseline, so use it to test whether your first launch measurably improves retention, flexibility, and automation outcomes.

The expensive failure modes are easy to spot:

- averaging conflicting CAGR figures into one planning number

- using a vendor report claim as board-level market truth without methodology review

- expanding vertical and region scope before your first launch slice is proven

So the next step is not another market narrative pass. Build the comparison table and evidence pack first. Commit roadmap and GTM only where your assumptions are auditable, your first-region constraints are understood, and your launch slice is small enough to measure before you scale.

Related reading: Build a Platform-Independent Freelance Business in 90 Days.

Frequently Asked Questions

What does subscription economy growth actually mean for platform builders making 12 month roadmap bets?

It means demand is real, but your best near-term bets are usually around retention, flexibility, and automation, not a broad feature land grab. Recurly explicitly frames the next wave that way, and it also points to reactivation as a growth input, with 1 in 4 new sign-ups described as returning subscribers. If your roadmap cannot improve renewals, retries, plan changes, and win-backs in a measurable way, a headline market number should not justify the spend.

Which capabilities are truly non negotiable at launch versus nice to have in later phases?

At launch, teams usually prioritize dependable recurring billing, pricing flexibility, and lifecycle visibility across renewals, cancels, refunds, and reactivations. A practical checkpoint is whether your team can reconcile those events by plan and region before paid acquisition scales. More advanced save tactics, like broader pause optimization or heavier automation, are valuable later, but only after the event data is trustworthy enough to show what is actually driving churn.

Which verticals are most attractive first for a team entering subscription commerce now?

There is no universal first pick, and you should be wary of anyone selling one. Market.us frames the space across service types like content subscriptions, product subscriptions, service subscriptions, and membership subscriptions, and across verticals including Media & Entertainment, Information Technology, and E commerce & Retail. The better entry point is the one where your billing logic, support burden, and retention mechanics are simple enough to observe end to end in the first launch slice.

Where is growth concentrated geographically, and how should that change launch sequencing?

The snippets here do not support a definitive country or region winner, so do not force a geography ranking from thin evidence. Sequencing should be based on your constraint load: regulatory requirements, data collection points, and processor coverage in the subscriber lifecycle. If that region matrix is incomplete, delay launch even if the market narrative sounds attractive.

Can I rely on the “76 million subscribers” figure in board planning today?

Not as a census of the whole market. The grounded claim is that Recurly’s 2026 State of Subscriptions report analyzes data from 76 million unique subscribers and 2,200 global merchants, which makes it a meaningful vendor dataset, not an independently audited view of the entire subscription economy. For board use, ask for the source origin, methodology, segment boundaries, and geography coverage first.

How should I handle conflicting CAGR numbers from different market reports?

Do not average them into one planning number. The grounded examples already conflict: 13.3% CAGR from 2025 to 2033 from Grand View, 15.9% CAGR from 2025 to 2034 from Market.us, and Juniper’s separate view of $722bn in 2025 to $1.2tn in 2030, or 68% growth. Treat each as a separate scenario, then attach roadmap pace, hiring, and launch scope to the scenario whose market definition actually matches your product.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- commission.europa.eu/law/law-topic/data-protection_entrusted

- oag.ca.gov/news/press-releases/attorney-general-bonta-i...trusted

- oecd.org/en/topics/sub-issues/vat-policy-and-administ...trusted

- vat-one-stop-shop.ec.europa.eu/index_entrusted

- aapor.org/wp-content/uploads/2022/11/TI-Attachment-C.pdfexternal

- aapor.org/standards-and-ethics/disclosure-standardsexternal

- bango.com/reports/subscription-wars-latin-americaexternal

- fulcrumdigital.com/blogs/the-ecommerce-subscription-economyexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Gig Economy 2026: Payment Volume Trends, Payout Rail Readiness, and Platform Consolidation

Treat **gig economy 2026 payment volume trends** as an execution question, not a headline-growth story. Some inputs are measurable now, including platform counts, payout-rail behavior, and jurisdiction-specific compliance requirements. What remains uncertain is any single, verified global gig payment volume number for 2026.

How Platforms Detect Free-Trial Abuse and Card Testing in Subscription Fraud

If your platform sells subscriptions while also handling contractor, seller, or creator payouts across markets, this is not just a signup filter issue. It is a control design issue that cuts across risk, finance, legal, compliance, and product. The damage often shows up later in the customer lifecycle, not only at account creation.

How Platform Builders Implement Subscription Pause for Retention

Treat subscription pause as a policy decision in your subscription lifecycle, not a nicer-looking button in the cancellation flow. If you only surface pause when someone tries to leave, you may see short-term retention wins while creating unclear billing behavior and status handling across systems.