Quick Answer

Separate free-trial abuse from card testing first, then run one escalation path across sign-up, trial use, billing, and refunds. Use Stripe’s lifecycle framing to classify account abuse, trial cycling, and refund abuse, and treat abnormal authorization clustering as a billing-rail signal. Keep hard actions tied to linked-entity evidence such as payment identifiers, not single-event alerts. Review changes weekly with legal and finance because Stripe reported a 6.2x rise in abusive free trials from November 2025 to February 2026.

Subscription fraud on platforms is a control design problem, not just a signup problem#

If your platform sells subscriptions while also handling contractor, seller, or creator payouts across markets, this is not just a signup filter issue. It is a control design issue that cuts across risk, finance, legal, compliance, and product. The damage often shows up later in the customer lifecycle, not only at account creation.

Step 1 Define the operating scope#

Be clear about who this article is for and what is in scope. The relevant operator is a platform team managing recurring plans in a multi-market environment, where abuse can affect billing quality, disputes, customer treatment, and internal reporting.

That cross-market framing matters. Merchant Risk Council's 2026 global context draws from over 1,200 eCommerce merchants across over 35 countries. That is a useful reminder that you are usually balancing local obligations with one operating model, not applying one universal rule everywhere.

Before you touch controls, confirm who owns three decisions today: who can change trial access, who reviews payment abuse trends, and who signs off when customer-facing friction changes. If those answers are fuzzy, the first failure mode is not missed detection. It is delayed escalation and weak documentation when finance or legal asks why a control was tightened.

Step 2 Pair free-trial abuse and card testing under one fraud lens#

Treat free-trial abuse and card testing as related fraud problems because both affect payment operations and often pull in overlapping teams. They are not the same threat, but they collide operationally.

Stripe's first-party fraud material is especially useful on trial abuse, account abuse, and refund abuse across lifecycle stages. It explicitly describes users abusing policies by creating multiple accounts, cycling free trials, or exploiting refunds, and reports 6.2x more abusive free trials from November 2025 to February 2026.

Stripe defines card testing as attempts to determine whether stolen card information is valid, and notes that this pressure is an unavoidable part of online commerce. That is enough to justify handling both threats in the same control program, but detailed card-testing tactics warrant a narrower claim than free-trial abuse coverage.

Step 3 Aim for a lean control and escalation sequence#

Keep the program practical, not maximal. You want a sequence for controls, reporting, and escalation that reduces operational surprises without layering on friction or approvals your team cannot maintain.

Visa's public guidance is a helpful reference point for why this needs more than product attention. Free trials or introductory offers that convert into recurring charges can create problems for cardholders and clients. That is why legal, finance, and risk should be involved early.

Design for the full lifecycle first, then add controls in order of evidence and owner readiness. If you cannot explain why a rule exists, who approved it, and what customer impact you expect, do not launch it yet. That discipline is what keeps your response credible under review, instead of turning it into a pile of ad hoc blocks that suppress good users and still miss the real pattern.

Related: What Is a Subscription Lifecycle? How Platforms Manage Trial Active Paused and Churned States.

Free-trial abuse and card testing are different threats that collide operationally#

Treat these as two lanes from the start, even when they appear in the same signup spike. Free-trial abuse is first-party behavior abuse across the customer lifecycle, including trial cycling, account abuse, and multi-account abuse. Card testing is payment-instrument validation abuse on checkout or billing rails, and it can appear inside free-trial signup flows.

Step 1 Define free-trial abuse as lifecycle behavior abuse#

Start with behavior links across accounts. A common pattern is repeated account creation to keep accessing a benefit intended for one account, including trial cycling without intent to convert.

Use shared customer identifiers, for example card, email, or shipping address, as triage signals for multi-account risk. Treat those links as review evidence, not standalone proof.

Step 2 Define card testing as credential-validation pressure#

Card testing is a different mechanism: attempts to validate payment credentials, often through low-value checks such as $1 before larger misuse. Enumeration/account testing is commonly automated, which is why auth activity can spike even when trial intent is not the core issue.

If authorization attempts cluster abnormally on cards, treat that first as card-testing pressure rather than ordinary trial-abuse behavior.

Step 3 Triage by signal, and keep the evidence boundary explicit#

Use a simple if/then rule:

- If repeated new accounts share payment identifiers, start with multi-account trial-abuse triage.

- If abnormal authorization clustering is the primary signal, start with card-testing triage.

Keep scope disciplined: free-trial abuse and refund-fraud controls are well-supported, but card-testing detection internals and a definitive attempt threshold require verification with your payment processor's documentation.

If you want a deeper dive, read Free Trial Abuse Prevention: How Platforms Detect and Block Serial Trial Exploiters.

Prepare the minimum evidence and owners before changing controls#

Do not tighten controls until ownership, baseline evidence, and review definitions are clear. Weak governance can create as much risk as weak detection.

Step 1 Assign named owners for detection, approval, and escalation#

Start with single accountability for each decision, even when multiple teams contribute. You should be able to name, without debate, who owns detection, who approves friction changes, and who handles escalation.

What matters before rollout is delegated authority and clear reporting lines. If a rule blocks signups or adds identity checks, define in advance who can launch it, reverse it, and respond when complaints or dispute spikes appear.

Step 2 Build a baseline pack before you add friction#

Build your baseline from normal operating data, not only the week that triggered concern. At minimum, include:

| Baseline item | Use in review | Grounded note |

|---|---|---|

| Current signup funnel by SaaS segment | Baseline from normal operating data | Keep segment definitions stable so before/after comparisons are valid |

| Dispute trends | Include even when the trigger is signup abuse | First-party fraud pressure can surface later in disputes |

| Trial-to-paid conversion quality by cohort | Baseline from normal operating data | Keep cohort definitions stable so before/after comparisons are valid |

Keep segment and cohort definitions stable so before/after comparisons are valid. Include dispute trends even when the trigger is signup abuse, since first-party fraud pressure can surface later in disputes (Stripe reports 62% of merchants saw increased disputes from first-party fraud over the past year).

Step 3 Normalize link data and define false positives up front#

Make linked-account review auditable by capturing consistent account-creation inputs every time: account metadata, identity signals, and payment identifiers such as card or bank fingerprints. Payment fingerprints are what make repeated signups reviewable instead of anecdotal.

Also define your false-positive standard before adding friction. Use a clear team rule for whether you count only hard declines or also legitimate users who drop off after extra checks, especially in cross-market onboarding where normal patterns vary.

Map abuse points across the customer lifecycle and decide where to intervene first#

Intervene at the earliest lifecycle stage where abuse creates real cost or where evidence becomes hard to defend later. In practice, that usually means mapping sign-up, trial use, billing, and post-service refunds first, then placing the first control where it is both effective and reviewable, not defaulting all friction to sign-up.

Step 1 Map the lifecycle before you rank controls#

Put four stages on one page: sign-up, trial use, billing, and post-service refunds. Stripe's lifecycle framing separates account abuse at sign-up, free-trial abuse during product evaluation, and refund fraud after a customer has already received goods or services, which helps you avoid treating all abuse as one problem.

For each stage, define the main failure mode in plain language. At sign-up, map account abuse and linked-account creation. During trial use, map trial cycling or repeated access expansion across related accounts. At billing, keep payment-rail issues like card testing in a separate lane, since Stripe recommends monitoring card testing and notes dispute impact can worsen over time. After service delivery, map refund or policy abuse, including false non-receipt or manipulated claims.

Your check is simple: can a reviewer trace each stage to retained evidence, not just a risk score? If your map only says "high risk user," it will not hold up in appeals, finance review, or audit discussions.

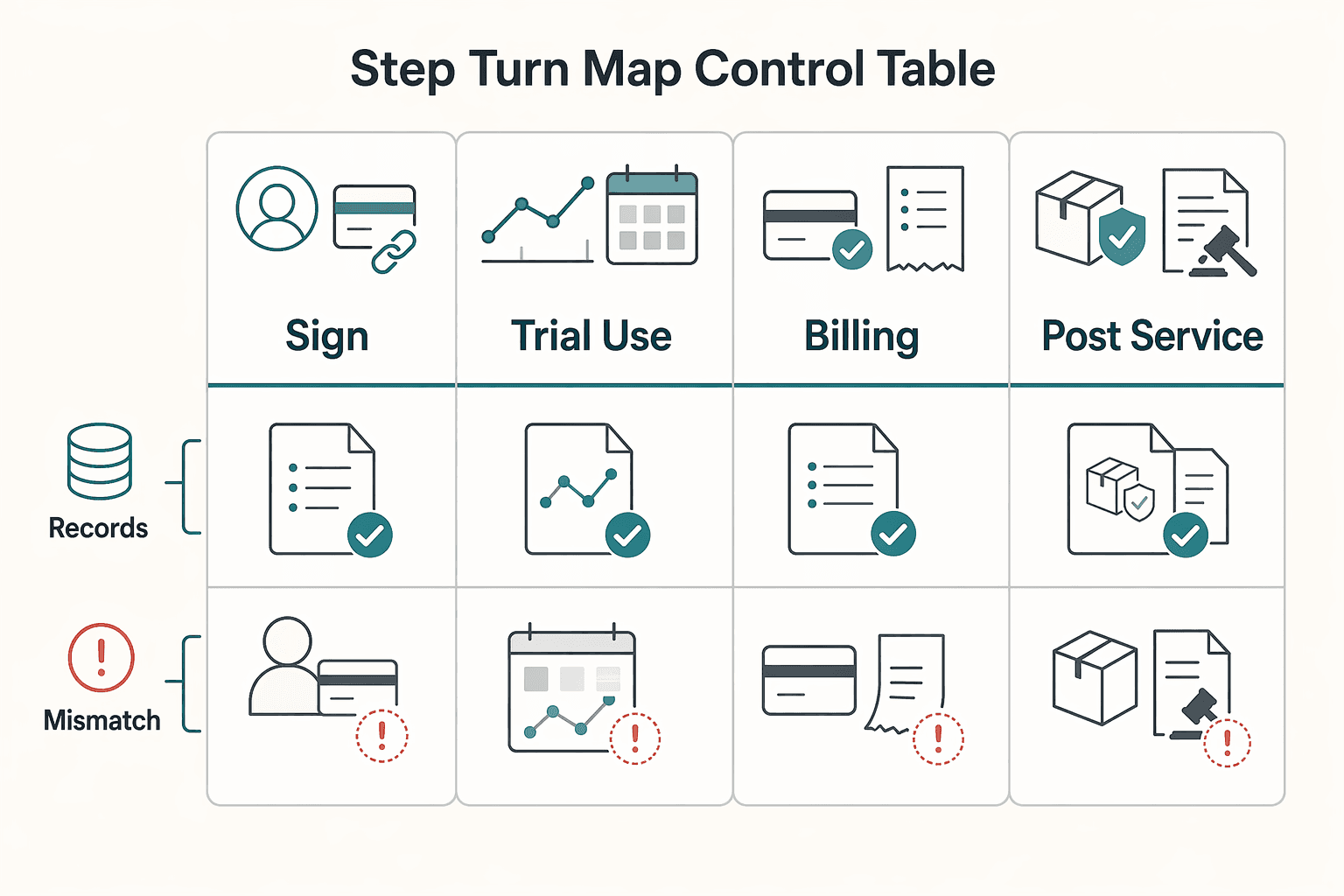

Step 2 Turn the map into a control table#

Convert the lifecycle map into one compact control table with named owners, and prioritize controls that leave an audit-ready record chain.

| Lifecycle stage | Signal | Risk hypothesis | Control action | Control owner | Escalation trigger |

|---|---|---|---|---|---|

| Sign-up | Reused identity details, linked account attributes, repeated payment identifiers | Account abuse or multi-account setup | Limit initial entitlement, queue review, retain link evidence and timestamp | Risk, with product approval for friction changes | Linked clusters grow or activation quality drops materially |

| Trial use | Rapid consumption across new accounts, repeated trial starts, expansion requests from related entities | Trial cycling or costly account abuse | Cap usage, require stronger verification before more access, preserve usage logs | Risk and product | Same entity reappears or variable-cost exposure starts mounting |

| Billing | Abnormal scripted or clustered authorization attempts | Card testing pressure on billing rails | Route to separate monitoring queue, tighten payment checks, retain payment event history | Payments or risk | Disputes begin rising or auth anomalies persist |

| Post-service refunds | Repeat non-receipt or refund claims after value was delivered | Refund fraud or policy abuse | Require claim evidence, document delivery or service use, route exceptions to finance or legal | Finance, with legal input when needed | Repeated claims by linked entity or dispute trend changes |

The operational detail that matters most is the evidence attached to each row: linked-account proof at sign-up, usage history during trial, payment event history at billing, and service-delivery plus claim records for refunds.

Step 3 Choose the earliest sensible intervention point#

Choose intervention timing based on your cost curve. Stripe notes account abuse is especially costly for AI companies when compute costs are tied directly to usage, so earlier controls can make sense there. For lower-marginal-cost trials, lighter sign-up gates with stronger checks later, for entitlement expansion, upgrade, or refunds, are often more proportionate.

Keep severity language anchored to known references. Stripe is useful for lifecycle placement and for the warning that card testing can create negative outcomes that worsen over time through disputes. Merchant Risk Council is useful for post-purchase exposure: on Mar 12, 2025, it stated Refund/Policy Abuse remained the most prevalent fraud type faced by merchants in the prior 12 months.

The 2026 Global eCommerce Payments & Fraud Report adds benchmarking context from 1,278 merchant professionals in 37 countries, fielded in November and December of 2025. Use this evidence to describe risk as prominent, prevalent, costly, or compounding, without inventing card-testing velocity thresholds or treating survey rankings as automatic legal triggers.

If your map shows immediate variable cost, intervene earlier. If losses cluster in disputes or refunds, invest more in later-stage evidence and escalation.

Step 1 instrument detection so alerts are actionable, not noisy#

Build detection around linked entities, not single events, so reviewers can act quickly and defend decisions later. Isolated alerts on one email, one IP, or one failed authorization usually create noise and miss multi-account patterns.

1 Track linked entities at account creation#

Start at account creation, where evidence is freshest. For free-trial abuse, collect a device or browser fingerprint, then correlate it with email, IP, and external signup metadata so related accounts are visible in business context.

Include payment identifiers in the same linking layer, especially card-level identifiers where available. In Stripe, a card fingerprint can serve as a card-level identifier because the fingerprint is unique for a given Account. This helps when account details change but the payment instrument is reused.

Alert on clusters, not isolated attributes. A single shared signal can be benign; a pattern of shared device fingerprint, reused payment identifier, and repeated trial starts across new accounts is a stronger multi-account abuse case.

Stripe's reporting shows the trend is material: from November 2025 to February 2026, its models detected 6.2x more abusive free trials.

Your verification check is simple: an alert should show linked accounts, matched attributes, and match timestamps. If it only says "high risk signup," it is not practical.

2 Split monitoring lanes for trial abuse and card testing#

Keep trial-abuse alerts and payment-rail alerts separate, even during the same traffic spike. Trial abuse is typically first-party behavior to extend trial value. Card testing is payment-fraud activity that probes card validity through repeated authorization attempts.

| Monitoring lane | What should trigger it | First response |

|---|---|---|

| Trial abuse | Linked accounts across email, IP, device, and payment identifiers; repeated trial starts; trial cycling | Limit initial entitlement, queue review, and prepare step-up identity verification before more access |

| Card testing | Multiple failed attempts on different cards with slight variations; frequent small authorization attempts, including from a few cents to less than $5 | Isolate billing pressure, tighten payment checks, and retain payment event history |

| Mixed or unclear | Reused payment identifier plus unusual authorization behavior across new accounts | Route for manual classification and preserve both account-link evidence and billing events |

This separation keeps triage decisions accurate. Conflating lanes can push the wrong response: account friction for a billing-rail problem, or payment treatment for a trial-abuse problem.

3 Review alert precision weekly and define escalation before volume rises#

Review top alert types weekly for precision, not just volume. Sample high-volume alerts, document false-positive reasons in plain language, and require named owner sign-off before rule changes. That is an internal consistency control, not a regulator-mandated format here.

Document each review as an investigation record: procedures performed, evidence obtained, and conclusions reached. For linked-account cases, retain matched attributes, account IDs, timestamps, reviewer decision, and downstream outcome. For card-testing cases, retain payment event history, failure pattern, and the classification rationale.

Set escalation logic in advance. If linked-account clusters grow while conversion quality drops, tighten trial entitlements and step up identity verification before additional credits or higher-cost access. If conversion quality is stable but repeated failed attempts across cards increase, prioritize payment-rail controls instead of broad trial friction.

Related reading: Fair Credit Billing Act for a Business-of-One: How to Dispute Credit Card Billing Errors.

Step 2 apply graduated controls that protect conversion quality#

After alerts are reliable, apply friction in steps so you reduce abuse without overblocking legitimate trial activity. Start with broad, low-friction controls, then escalate only when linked signals show stronger confidence of abuse or trial cycling.

Treat this as a control ladder, not a single on/off decision. Stripe frames this as balancing risk and revenue, and its risk settings show estimated accepted-payment impact using projections from the last four months of payment data. Use that impact view before tightening rules.

| Abuse signal confidence | First control | When to step up | What to verify |

|---|---|---|---|

| Low | Monitor and keep initial access narrow | Signals repeat across linked accounts | Conversion quality in the affected cohort remains stable |

| Medium | Add stepped friction, such as stronger identity verification or review before more access | Signals persist after the first control | Reviewers can explain why the case moved from monitoring to friction |

| High | Stop access expansion; block for clearly automated abuse when your vendor returns a block verdict | Pattern is consistent and validated by rule testing | The block logic matches the historical cases you intended to catch |

Keep the decision rule simple: low confidence means monitor first, high confidence means stronger controls, and clear automation with a block verdict means block.

Test the control before you expose the funnel#

Test rule changes against historical live-mode traffic before launch. Stripe supports this and summarizes expected forward impact, so you can estimate what the rule would have caught and what legitimate activity it would have touched.

For risk and legal review, attach a short evidence pack to each control change: trigger signals, expected customer impact, affected segment, and why you chose review or added friction instead of immediate hard blocking.

Define rollback before launch#

Define rollback criteria before rollout so control changes stay reversible. You do not need one universal threshold, but you do need named metrics and a clear owner.

If activation drops in a segment without a matching reduction in linked-account abuse, roll back and document why. Record the rollback trigger, approver, and post-launch evidence check to avoid policy drift across product, risk, and support.

Step 3 set escalation thresholds and reporting cadence for legal and finance#

Make escalation predictable: route issues to legal and finance when patterns are repeatable, materiality is at risk, or a control change could alter customer treatment, refunds, or enforcement options.

Define triggers in the terms those teams already use. For finance, that means dispute volume and trajectory over time, not one alarming event. Internally, mirror threshold-based logic: track recurring subscription fraud patterns, then trigger formal review when a pattern is sustained, growing, or linked to rising dispute exposure.

Use a simple triage rule:

- Keep isolated events in risk operations.

- Escalate when patterns repeat across linked accounts, payment identifiers, or dispute reason codes.

- Score incidents with a repeatable method so decisions are consistent.

- Set thresholds to your risk profile instead of copying a generic number.

Run a weekly governance pack#

Use a weekly pack to keep decisions current and auditable. Stripe reported that from November 2025 to February 2026, its models detected 6.2x more abusive free trials, which shows how quickly conditions can shift. Your weekly pack should answer:

| Pack item | What it should answer |

|---|---|

| Top abuse modes this week | trial abuse, account abuse, refund abuse, dispute pressure |

| Open investigations | who owns them, and what evidence is missing |

| Control changes | what went live, and which customer segments were affected |

| Exceptions | including accounts allowed through despite risk signals |

| Cross-functional decisions | what was made, and what still needs legal or finance sign-off |

If finance cannot see dispute reason-code movement, or legal cannot see which decision changed customer treatment, the pack is not ready.

Preserve the record chain and tag specialist review early#

For each major decision, keep one audit-ready record with rationale, approver, date, evidence reviewed, expected customer impact, and review date. Keep investigation notes, dispute reason-code trends, linked-entity findings, and impact checks with that record so the decision trail is complete.

Add a clear specialist advice required flag when jurisdiction or contract terms could change enforcement options. This is especially important in cross-market programs where obligations can differ. If a response could affect renewal handling, cancellation treatment, refunds, or enforcement under your terms, pause for specialist input before rollout.

Common implementation mistakes and how to recover quickly#

The quickest recovery is to separate threat types, require corroboration before hard blocks, measure both abuse and legitimate conversion quality, and document every control change.

| Mistake | Recover by | Detail |

|---|---|---|

| Treating all anomalies as one fraud type | Split queues for free-trial abuse and card testing, with distinct response owners | Report separate volumes, actions, and outcomes for each lane |

| Hard blocking on one signal | Require multi-signal corroboration before suspend, deny, or step-up actions | Pair at least one payment identifier with timing, signup pattern, and actual trial use |

| Optimizing only for blocked abuse | Pair abuse KPIs with conversion-quality KPIs | Track legitimate trial activation, trial-to-paid quality, and dispute movement by cohort |

| Undocumented control changes | Log every rule change with date, approver, signals reviewed, expected customer impact, and rollback criteria | Documented change decisions are easier to defend with legal, finance, and audit |

Mistake 1: treating all anomalies as one fraud type. Recover by splitting queues for free-trial abuse and card testing, with distinct response owners. Trial cycling across linked accounts is a different pattern from clustered authorization attempts with little real product use, so your weekly pack should report separate volumes, actions, and outcomes for each lane.

Mistake 2: hard blocking on one signal. Recover by requiring multi-signal corroboration before suspend, deny, or step-up actions: at least one payment identifier plus behavioral context. On Stripe, card.fingerprint is a concrete cross-account identifier; pair it with timing, signup pattern, and actual trial use to reduce false links.

Mistake 3: optimizing only for blocked abuse. Recover by pairing abuse KPIs with conversion-quality KPIs. Track abuse reduction alongside legitimate trial activation, trial-to-paid quality, and dispute movement by cohort. This matters when conditions move quickly: Stripe reported 6.2x more abusive free trials from November 2025 to February 2026.

Mistake 4: undocumented control changes. Recover by logging every rule change with date, approver, signals reviewed, expected customer impact, and rollback criteria. Documented change decisions are easier to defend with legal, finance, and audit than screenshots and memory.

You might also find this useful: How to Offer Free Trials That Convert: Design Rules for B2B Platform Operators.

Build controls your teams can run every week#

Run a weekly control set that is small, explicit, and auditable. If your team cannot name the owner, the evidence for the rule, and the rollback trigger, it is not ready for live traffic.

Step 1: Split operating lanes before tuning controls. Treat free-trial abuse and card testing as separate lanes, even when both appear near signup. Free-trial abuse is one actor creating multiple accounts to claim more trial value. Card testing is often automated, high-velocity payment probing. The response should follow the lane: free-trial controls on account/trial access, and card-testing controls at checkout (CAPTCHA, rate limits, and access controls).

Step 2: Map lifecycle points to owners and escalation triggers. Document who owns detection, who approves control changes, and when escalation moves to legal, finance, or compliance. Keep this map tied to your subscription lifecycle states so decisions are operational, not ad hoc.

Step 3: Run the weekly review on evidence, not anecdotes. Use one recurring report for abuse patterns, control changes, open exceptions, and customer impact. If you use Stripe, Radar analytics can anchor payment-side monitoring because it tracks fraud and dispute rates against card monitoring program thresholds. For threshold-sensitive decisions, label market/program scope clearly and check primary network documentation, since Stripe's page is a general guide. Visa's VAMP threshold updates, for example, were communicated with an effective date of 1 June 2025.

Your evidence pack should let another team reconstruct the decision path: rule changed, signals reviewed, approver, date, expected impact, and unresolved exceptions.

Step 4: Pair each control with conversion guardrails and rollback criteria. If confidence is low, start with lighter limits and monitoring. If signals are strong and repeated, escalate controls. Define rollback criteria before launch so conversion risk and abuse reduction are reviewed together.

Use this weekly checklist:

- Confirm separate lanes for free-trial abuse and card testing.

- Confirm the lifecycle map lists owners, triggers, and escalation paths.

- Confirm the weekly report includes evidence reviewed, decisions made, and unresolved exceptions.

- Confirm each new control has conversion guardrails and rollback criteria.

- Confirm market-specific or program-specific decisions are labeled as such, and involve specialist counsel where obligations may vary.

Frequently Asked Questions

What is the practical difference between free-trial abuse and card testing for platform risk teams?

Free-trial abuse is usually first-party policy abuse. One actor creates multiple accounts, cycles trials, or exploits refunds to extract value. Card testing is different because attackers use card setup or small payments to learn whether stolen or enumerated card data is valid. If your cluster is centered on repeated account creation and entitlement use, treat it as account abuse. If it is centered on abnormal authorization attempts and later Early Fraud Warnings, treat it as payment-rail probing.

What are the earliest reliable signals of multi-account abuse at signup?

Look for linked accounts that share a payment identifier plus repeated timing or behavior patterns, not just one weak match. A single overlap signal can be noisy, so use it as a review trigger rather than an automatic block.

What minimum controls can a platform deploy in the first 30 days?

There is no universal 30-day standard in the sourced material, so treat this as a conservative starting set, not a rule. Separate free-trial abuse from card-testing alerts, document control changes, and use multiple signals plus behavioral context before hard blocks. If card testing is active, expect engineering work because Stripe notes mitigation typically requires code-level changes.

When should free-trial abuse be escalated to legal or compliance instead of handled in product ops?

The sourced material does not define fixed legal or compliance thresholds, so use a conservative boundary. Escalate when the response is no longer just a product decision, including cases where contract terms, market-specific obligations, or external reporting questions may shape what you can do next. If the case can be handled by entitlement limits and standard review, product ops can usually stay in front.

How do you reduce abuse without overblocking legitimate trial users?

Use stepped friction. Start by capping entitlement or monitoring closely when confidence is low, then require stronger checks only when linked-account evidence is stronger. That matches the grounded goal for free-trial defense: reduce wasted trial resources without hurting real users, so review abuse metrics beside activation and trial-to-paid quality.

What evidence should be retained to support an external audit or regulatory question?

The sourced material here does not prescribe specific retention durations. For defensibility, keep a clear decision chain: the signals reviewed, linked-account evidence, the action taken, approver, date, expected customer impact, and rollback criteria. A useful verification point is whether someone outside the original team could reconstruct why a rule changed and which customers it affected.

How should risk controls differ for AI companies versus lower-cost SaaS trials?

Apply the same principle in both: balance abuse reduction with user impact, start with lighter controls, and increase friction as linked-account or card-testing signals strengthen.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- cisa.gov/news-events/news/cisa-national-cyber-inciden...trusted

- docs.stripe.com/disputes/prevention/card-testingtrusted

- docs.stripe.com/disputes/prevention/abusetrusted

- guides.gaoinnovations.gov/greenbook/2025/principle-3-establish-structu...trusted

- justice.gov/criminal/criminal-fraud/page/file/937501/dltrusted

- stripe.com/blog/analyzing-first-party-fraud-trends-acco...trusted

- support.stripe.com/questions/how-can-i-detect-duplicate-cards-o...trusted

- checkout.com/blog/card-testing-fraudexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Free Trial Abuse Prevention for Platforms Blocking Serial Trial Exploiters

If you own fraud, compliance, legal, or finance, the goal is straightforward. Stop repeat trial abuse without hurting legitimate conversion, and do it in a way you can explain later. That matters most when the same account path can eventually touch payment processing, payouts, or entity onboarding across multiple markets.

What Is a Subscription Lifecycle? How Platforms Manage Trial Active Paused and Churned States

Subscription lifecycle states matter only when they tell your team what happens next. In **subscription lifecycle states platform management**, a label like `Active` or `Suspended` should tell finance, billing ops, and product what changes in charges, access, edits, and reconciliation.

How B2B Platform Operators Design Free Trials That Convert Profitably

The main mistake is simple: teams often optimize for more starts when they should optimize for more profitable paid customers. In B2B SaaS, **trial-to-paid conversion rate** is the share of trial users that become active paying customers in a defined period. That number only matters if the customers who convert are the right ones for your business.