Quick Answer

Use a staged decision path: screen new trials with device and email signals, validate risk with payment instrument history and BIN patterns, then choose challenge, review, or block based on overlap. Keep trial access separate from payout eligibility so uncertain accounts cannot move funds early. For defensibility, store the rule version, trigger reason, analyst note, and any override memo for each case. This keeps fraud, finance, and legal reviews tied to evidence instead of one-off judgments.

Free trial abuse prevention for teams that own both fraud risk and regulatory exposure#

If you own fraud, compliance, legal, or finance, the goal is straightforward. Stop repeat trial abuse without hurting legitimate conversion, and do it in a way you can explain later. That matters most when the same account path can eventually touch payment processing, payouts, or entity onboarding across multiple markets.

- Start with the real promise

This article focuses on how to detect and block free trial abuse without breaking legitimate conversion. The pattern is not hypothetical. Stripe said its models detected 6.2x more abusive free trials from November 2025 to February 2026, and the abuse often looks like first-party abuse through repeated account creation and trial cycling. Key differentiator: the target is balanced control, not maximum friction. The real test is whether you reduce repeat abuse while keeping the experience workable for legitimate prospects.

- Keep the scope tight

This is for payment-enabled SaaS platforms, marketplaces, and AI startups that handle platform payments across jurisdictions. In those businesses, signup abuse does not stay confined to registration. It can spill into verification queues, payout eligibility, payment acceptance, beneficial ownership checks for legal entities at account opening, and AML review. Key differentiator: this is written for teams where trial access can become compliance exposure. Once your product touches payments or payouts, verification ties directly to enablement, and requirements can change by market, so one threshold or one review path will not fit every geography.

- Be clear about what this is not

This is not a pitch for any single tool. It is also not a pure growth piece about trial conversion design. Tools matter, but a control that creates blocks without evidence, ownership, or exception handling will not stand up when finance asks about losses or audit asks why a user was stopped. Key differentiator: the standard here is decision quality. A common failure mode is treating trial abuse like simple signup spam, then realizing later that no one kept rule versions, case notes, or override reasons.

- Aim for an evidence-backed control set

The deliverable is a concrete stack of controls, a monthly reporting checklist, and internal escalation triggers that can stand up to KYC, KYB, AML, and audit review. One early checkpoint matters more than most. If a legal entity reaches account opening, you should know whether beneficial ownership identification is required at that stage and whether the review result is retained with the case record. Key differentiator: auditability is part of the control, not a later add-on. Independent testing in AML programs is explicitly expected, so if you cannot show pre and post rule impact, sign-off, and the evidence behind a block or override, you have a governance gap, not just a fraud gap. If you want a deeper dive, read Subscription Fraud Trends for Platforms: How to Detect Free-Trial Abuse and Card Testing.

How to choose controls that cut abuse without creating compliance drag#

Choose controls that measurably reduce repeat trial abuse, keep false-positive impact manageable, and leave evidence your team can defend later. If a rule adds friction but does not show a measurable drop in account-creation abuse in a limited test, do not roll it out broadly.

- Detection lift

Prioritize controls that target behavior you are already seeing, not controls that only sound strict. For repeated signup patterns, velocity rules can block, detect, or add friction across related accounts. Key differentiator: backtest before rollout, then compare test results against a baseline so you can show the lift came from the rule.

- False-positive cost

Treat false positives as a core cost, not a side metric. Where tooling supports it, use rule-level estimated false positive rate instead of guessing. Key differentiator: when risk is high but the cost of a wrong block is also high, use challenge or review paths instead of defaulting to hard blocks.

- Implementation burden

Only ship controls your team can operate reliably. Some advanced rule capability depends on upgraded tooling such as Radar for Fraud Teams, and added challenge paths increase operational load. Key differentiator: do not ship a control unless it has a named owner, an exception path, and a rollback step for SaaS platforms or marketplaces.

- Auditability across KYC and AML

A deny event by itself is not enough. Keep evidence another team can validate later: rule version, trigger reason, case note, override reason, and linked KYC or AML review outcomes. Key differentiator: independent testing is expected to be risk-commensurate, and periodic review can run every 12-18 months, so trial-abuse decisions need a clear paper trail, not just blocks.

Related: How to Offer Free Trials That Convert: Design Rules for B2B Platform Operators.

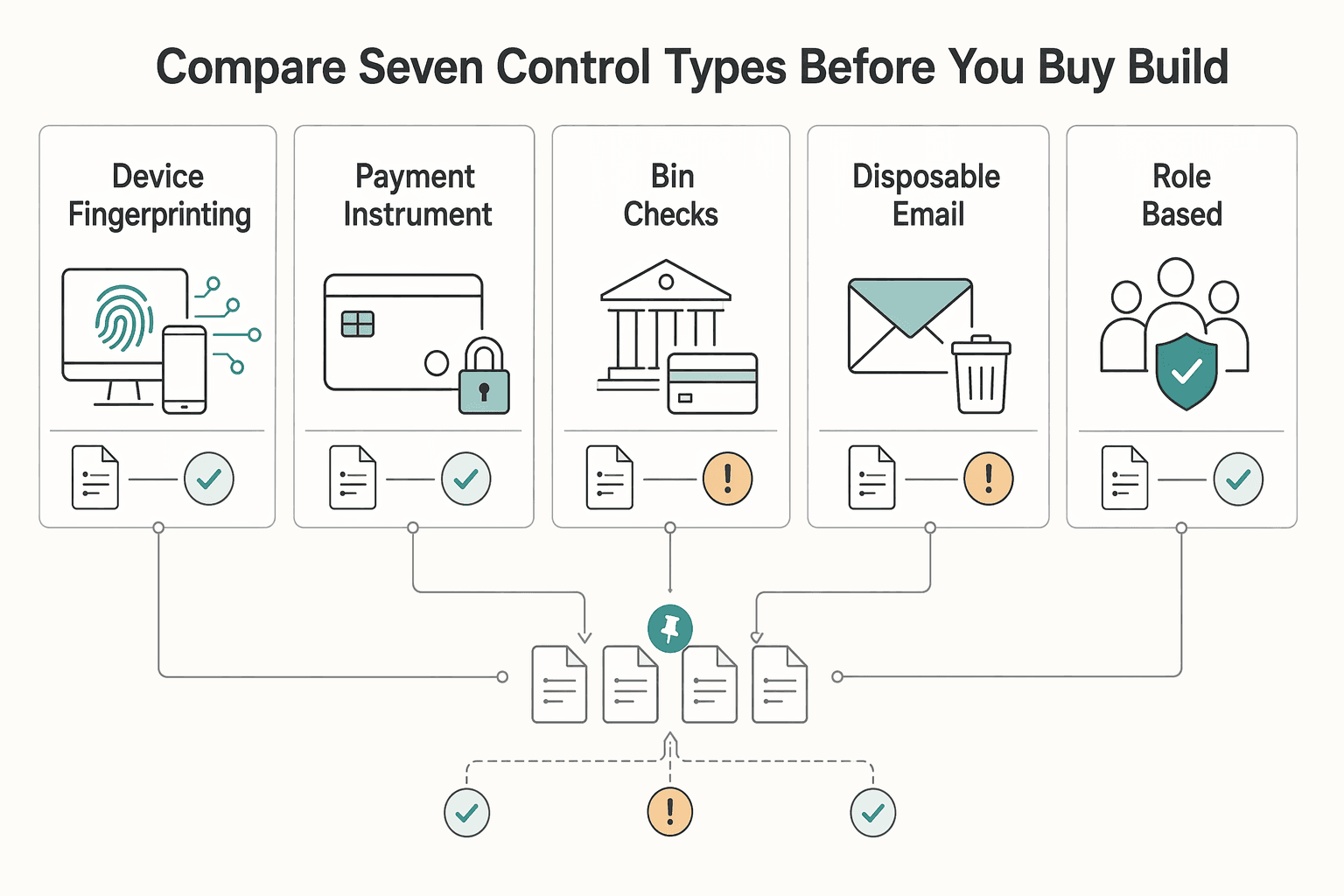

Compare the seven control types before you buy or build#

Use layered signals before auto-blocking: at least one identity signal, one payment signal, and one behavioral signal, with stepped verification when signals conflict.

| Control type | Best for | Key pros | Key cons | Concrete use-case | Owner team | Evidence artifact retained |

|---|---|---|---|---|---|---|

| Device fingerprinting | Early repeat-signup detection; especially relevant for AI startups with self-serve API access that see 10x more attempted abuse than enterprise AI motions | Catches repeat actors early; can return structured context like action, warning flags, and metadata | Legitimate shared environments can look risky; needs tuning | AI self-serve: challenge or block when one device appears across many new trial accounts | Risk or fraud with product engineering | Fingerprint verdict, action taken, warning flags, metadata, linked case note |

| Payment instrument reputation | Card-backed trials and trial-to-paid flows | Clear payment-layer scoring; tools like Stripe Radar assign risk scores and can auto-block high-risk attempts; Stripe says there is a 92% chance a card has been seen before on its network | Weaker when payment details are collected late; misses earlier non-paying abuse | AI self-serve or marketplace: flag reused high-risk cards and repeated failed authorizations tied to serial trials | Payments risk or fraud ops | Risk score, payment ID, decision outcome, failed auth history, override note |

| BIN checks | Fast routing when card data is collected up front | Cheap, interpretable routing signal from the first six or eight digits | Low precision alone; easy to overinterpret patterns and create false positives | Route higher-risk BIN patterns to review or challenge before provisioning credits or capabilities | Payments team with fraud support | BIN/IIN result, rule ID, route taken, reviewer note |

| Disposable email domain filtering | Low-cost front-door filtering for obvious burner-email abuse | Useful early screen when fraudsters use disposable or tumbling addresses for repeat signups | Easy to evade; can catch legitimate privacy-focused users | AI self-serve: block or challenge known disposable domains at signup | Growth ops or risk | Matched domain, domain-list version, action taken, appeal or override record |

| Role-based email filtering | B2B signup and marketplace onboarding that needs an accountable person | Flags generic prefixes that do not identify a specific person | Many legitimate teams use shared inboxes; weak as a standalone block signal | Marketplace/KYB context: route role-mailbox signups to added verification before full control | Product ops with compliance input | Prefix rule hit, verification result, override reason |

| Velocity and session anomaly rules | Signup floods, API key bursts, repeated trial attempts from clustered traffic | Direct response to suspicious traffic; intelligent rate limiting can use device risk | Ongoing tuning required; legitimate spikes can look suspicious | AI self-serve: throttle or challenge high-velocity clusters across related sessions/devices | Fraud engineering or SRE | Rule version, threshold/condition, trigger count, session log excerpt |

| Stepped verification | Medium-risk events where false-positive cost is high | Better conversion tradeoff than universal hard blocks; payment example: Adaptive 3D Secure on high-risk payments | Adds support load and drop-off; not every challenge stops repeat abuse | Marketplace/KYB context: escalate ambiguous cases to verification instead of immediate denial | Risk, compliance, and ops | Challenge type, outcome, reviewer note, linked KYC/KYB result |

The model split is practical: AI self-serve stacks usually need stronger identity plus behavioral controls early, while marketplaces usually need explainable challenge paths that align with onboarding obligations. Your platform is responsible for collecting required KYC/KYB information during onboarding, so decisions need a clear evidence trail.

If risk is elevated but the account may still be legitimate, delayed payout controls can be cleaner than a rushed hard block. Stripe Connect supports manual payouts, so you can delay payouts to certain accounts while review completes.

Treat BIN and email-domain logic as routing inputs, not high-confidence blockers by themselves. Reserve automatic blocks for overlap across identity, payment, and behavior, and confirm each control can export decision artifacts you can defend later.

Related: How to Create a Distraction-Free Home Office That Actually Holds Focus.

Identity and account integrity controls that catch repeat signups early#

Use layered identity signals early: combine Stytch Device Fingerprinting with email checks, and do not let email checks decide alone.

- Stytch Device Fingerprinting

This is the strongest early signal for account creation abuse because it can link repeat attempts before trial resources are consumed. It collects and interprets device attributes, and device identity can stay stable across sessions even when someone changes settings or uses a VPN. The main tradeoff is false positives in shared environments. Route suspicious device clusters to challenge or review first, then check which identifier fired (browser, hardware, or network) before deciding to block.

- Disposable email domains

Use this as a low-cost front-door filter. Blocking known burner domains at signup can stop obvious abuse before provisioning. Keep this in context: it is a fast routing control, not a complete defense. If you rely on domain checks alone, repeat actors can still pass with clean-looking domains while reusing stable devices.

- Role-based emails

Treat addresses like admin@, info@, or sales@ as routing signals, not standalone block signals. Many legitimate B2B users start from shared inboxes. A practical path is to allow corporate domains with added verification, request a named owner, or keep the account in a limited state until review is complete. Preserve an override path for legitimate teams that do not use person-named mailboxes.

The common failure mode is overvaluing email and undervaluing device linkage. When signals conflict, challenge and review instead of forcing a single-control auto-block, and retain the verdict, action, and override record.

Need the full breakdown? Read How to Overcome Writer's Block: Diagnose Strategy, Process, Resource, or Confidence Problems.

Payment and instrument controls that separate trial interest from nonpayment intent#

Payment and instrument signals work best as corroborating evidence, not a standalone decision. Use them to strengthen or challenge what you already see in identity and account-integrity checks.

| Signal | What to review | Handling note |

|---|---|---|

| Payment instrument history | Whether repeated trial attempts share a funding source; Stripe Radar gives each payment a risk score from 0-99 | Weigh the instrument history against identity signals before deciding on access, challenge, or restriction |

| BIN patterns | Issuer-context clusters based on the first six to eight digits of the card number | Treat BIN as a pattern signal, not proof, and keep the BIN observed, timing pattern, related accounts, and action taken |

| Card outcome and decline signals | Unique declines, excluding failed retries; issuer outcomes like insufficient funds or credit | Escalate when decline behavior repeats across linked accounts and aligns with other payment or identity risk indicators |

- Payment instrument history

Start with the payment instrument, not just the account profile. Stripe Radar evaluates each payment for fraud risk, and each payment includes a risk score from 0-99. The practical use is linkage: repeated trial attempts that look unrelated at the account level can still share a funding source. Review whether an instrument appears across prior failed or abandoned trial accounts, then weigh that against identity signals before deciding on access, challenge, or restriction.

- Bank identification number (BIN) patterns

A BIN is the first six to eight digits of the card number, and it helps you group activity by issuer context. This is useful for spotting clusters that span multiple cards but follow the same issuer pattern. Treat BIN as a pattern signal, not proof. Keep an evidence trail (BIN observed, timing pattern, related accounts, and action taken) so decisions are explainable and reviewable.

- Card outcome and decline signals

Decline data is useful when you read it correctly: analyze unique declines and exclude failed retries. Issuer outcomes like insufficient funds or credit are valid signals, but they do not prove abuse intent on their own. Escalate when decline behavior repeats across linked accounts and aligns with other payment or identity risk indicators. When signals conflict, route to added verification or limited access and document the decision logic.

You might also find this useful: How to Price a Clinical Trial Data Analysis Project.

Access and payout gating rules that prevent abuse from reaching money movement rails#

If a trial can reach payment rails, separate product access from money movement and gate it in stages. Apply stricter controls as users move toward accepting payments, withdrawing funds, or entering payout batches, because that is where trial abuse can become compliance exposure.

| Gate | Purpose | Key check or record |

|---|---|---|

| Signup gate | Stop obvious repeat-account abuse early with blocking or added friction | Record why the user was blocked, challenged, or allowed using the same identity and payment evidence from prior checks |

| Feature gate | Allow low-risk trial usage while keeping payment-enabled or balance-like features behind separate permissions | Keep sensitive actions locked, including bank-transfer setup details such as a virtual bank account number |

| Payout gate | Treat payout access as a separate approval tied to KYC, KYB, and AML readiness | Retain the hold reason, reviewer note, batch identifiers, and beneficial-owner identification and verification steps for legal entities |

For platforms acting as a Merchant of Record (MoR), the threshold is higher: the MoR is the legally responsible payment-processing entity and carries financial, legal, and compliance liability for transactions. Once funds can move, this is no longer only a growth decision.

- Signup gate

Use signup controls to stop obvious repeat-account abuse early, with either blocking or added friction. Keep this gate focused on low-cost signals, and record why the user was blocked, challenged, or allowed using the same identity and payment evidence from prior checks.

- Feature gate

Allow low-risk trial usage, but keep payment-enabled or balance-like features behind separate permissions. This staged middle step is useful when risk signals are mixed: the user can evaluate the product, while sensitive actions stay locked, including bank-transfer setup details such as a virtual bank account number.

- Payout gate

Treat payout access as a separate approval tied to KYC, KYB, and AML readiness. Before enabling charges and payouts, required connected-account information must be collected, and unmet verification requirements can lead to paused payouts or payments. For legal entities, include beneficial-owner identification and verification steps in your AML evidence file.

The tradeoff is operational, not theoretical: hard blocks reduce exposure earlier, while staged gating gives legitimate users time to complete onboarding. Do not let a clean signup or card check silently unlock payout batches. If KYC or KYB is incomplete, keep the account out of payout runs until review is complete, and retain the hold reason, reviewer note, and batch identifiers. Related reading: Tax Free Digital Nomad Visas and the Tax Outcome You Can Defend.

Monitoring and evidence packs your risk and finance teams should review monthly#

Your monthly pack should make one judgment easy to defend: controls are reducing repeat abuse, and exceptions are documented well enough for finance, legal, and compliance review. If it is only a dashboard, it is incomplete; include monitoring, testing, and outcomes analysis, not just alert totals.

| Item | What to log | Relevant detail |

|---|---|---|

| Form W-9 | Missing or corrected records | Keep tax-document exceptions visible without asking fraud analysts to make tax determinations |

| W-8BEN | Expiring forms | Keep tax-document exceptions visible |

| 1099-NEC | Exceptions that miss the January 31 filing deadline or later require correction | Track in the exception log |

| FEIE | Claimed eligibility | Physical presence test uses 330 full days in 12 consecutive months |

| FBAR | Foreign account reporting issues | Due April 15 with an automatic extension to October 15 |

- Metric table with attached artifacts

Use a scorecard where every number maps to evidence.

| Metric | What to review | Evidence to attach | |---|---|---| | Blocked trials | Volume, trend, top rules firing | Case notes, rule ID and version, sample decision logs | | Challenged trials | Pass rate, drop-off rate, rule mix | Challenge outcomes, analyst notes, device or payment evidence used | | Overrides | Who approved, why, downstream result | Override memo, approver name, linked account history | | False-positive cases | Confirmed legitimate users blocked or challenged | Reversal notes, customer evidence, remediation time | | Repeat-actor recurrence | Same actor returning after block or challenge | Linked identities, payment instrument history, device cluster notes |

- Case files mapped to policy versions and onboarding outcomes

For each material metric, attach the exact rule version in force and case notes explaining why a user was blocked, challenged, or overridden. When abuse intersects payout or account-opening flows, include related KYC, KYB, and AML outcomes. For legal entities, include beneficial-ownership checks where relevant, since 31 CFR 1010.230 requires identifying beneficial owners when a new account is opened. If available, add ledger-linked audit exports so finance can reconcile what was held, released, or never posted.

- Tax and documentation exception log for payout-touching cases

Keep tax-document exceptions visible without asking fraud analysts to make tax determinations. Track missing or corrected Form W-9 records, expiring W-8BEN forms, and 1099-NEC exceptions that miss the January 31 filing deadline or later require correction. Route claimed FEIE eligibility and foreign account reporting issues to tax or compliance: the FEIE physical presence test uses 330 full days in 12 consecutive months, and FBAR is due April 15 with an automatic extension to October 15.

- Rule-change checkpoint with pre/post impact

Treat high-impact rule changes as governed decisions. The packet should show the old rule, new rule, expected effect, same-window pre/post results, and false-positive movement, plus documented sign-off from risk and legal/compliance. That sign-off is governance discipline, not a universal legal requirement, and it prevents silent control shifts with no rollback path or shared tradeoff record.

For a step-by-step walkthrough, see How Freelancers Should Handle a Waiver of Jury Trial Clause.

Escalation triggers and ownership map across risk legal finance and ops#

Define escalation before the next abuse spike so decisions stay defensible and consistent under pressure. For each trigger, pre-name the owner and the evidence required for review.

- Trigger events that merit cross-team review

Use a short, predefined trigger list: a measurable jump in first-party fraud or free-trial abuse patterns, rising override rates, regulator-facing incidents, or major complaint/partner signals. A spike is not hypothetical: Stripe reported 6.2x more abusive free trials from November 2025 to February 2026. Each trigger should also define the proof set up front (for example: rule IDs firing, affected signup cohorts, complaint records, and sample decision logs).

- Owners by decision type, not org chart

Risk tunes controls and proposes threshold changes. Legal/compliance sets policy boundaries and reporting posture. Finance validates loss and reconciliation impact. Ops runs queue handling and customer communication. This aligns with three-lines-of-defence role separation, but your exact map should fit your operating model rather than assume one fixed legal template.

- Escalation rule when overrides rise but loss does not

Treat rising overrides with flat abuse loss as a warning signal that hard blocks may be too blunt. In that case, pause new hard-block expansions, keep challenge controls active, and re-tune thresholds before tightening further. Validate the decision against your monthly evidence pack: policy version, override rationale, false-positive outcomes, and complaint trends.

The takeaway for teams that need fewer surprises and cleaner decisions#

Cleaner outcomes come from better decisioning, not from adding more controls. The approach that holds up is tiered, explainable, and documented.

- Layered signals beat single checks

Use identity, payment, and behavior signals together, because repeat abuse rarely repeats just one trait. Stripe reported a 6.2x increase in abusive free trials from November 2025 to February 2026, and AWS notes these methods are often combined and automated. Prioritize correlation across signals: when device pattern, payment history, and signup behavior align, your basis to challenge or block is stronger than any single check.

- Explainability matters more than tool count

A control is not production-ready if risk can run it but legal, finance, or audit cannot understand why it fired. Stripe reports Radar can predict common trial-terms abuse with 90% accuracy when enabled, but that does not replace local validation or review. Keep decision evidence complete enough to reconstruct what happened later, including what rule fired, when it fired, and how exceptions were handled.

- Roll out in stages, then tune on outcomes

Apply staged gates instead of broad friction for everyone at signup. Start lighter, tighten where risk or cost is higher, and expand stricter blocks only after your own results show the change is helping. One-click controls can speed execution, but teams still need exception handling, monthly review, and clear ownership across risk, legal/compliance, and finance.

If you are unsure where to start, use the comparison table earlier in this article and begin with one signal from each category: identity, payment, and behavior. Then step up verification before hard blocks in mixed-confidence cases. We covered this in detail in How to Find Free Camping in the US.

Frequently Asked Questions

What is free trial abuse in payment-enabled SaaS platforms?

Free trial abuse is account-creation abuse where one actor opens multiple accounts to keep claiming trial credits. In a payment-enabled SaaS product, the impact is not just conversion; it can also consume operational resources before the pattern is obvious. The practical distinction is repeat behavior by the same actor, not a single messy signup.

Is blocking disposable email domains enough to prevent serial trial exploitation?

No. AWS notes that fraudulent users bypass simple email checks by creating multiple fake accounts or using disposable email services, and those methods are often combined and automated. Keep disposable-domain filtering because it can remove low-effort abuse, but do not treat it as a standalone control. A common miss is stopping at email checks while the same actor keeps returning through other signals.

When should we auto-block, step up verification, or allow with monitoring?

Use stepped decisioning, not one blanket action. Stripe Radar’s rule order matters here: step-up authentication can be evaluated before block, review, or allow rules, which gives you a middle path when suspicion is real but not conclusive. A practical policy is to reserve auto-blocks for repeated patterns, route mixed cases to review or verification, and allow lower-confidence cases with monitoring for later tuning.

How can we reduce false positives without opening a loophole for repeat abusers?

Keep your controls layered and your exception handling visible. Stytch frames the goal well: reduce wasted trial resources without impacting real users, which means rule changes should be checked for false-positive impact. A common failure mode is a hard block with no review path, which can catch legitimate users.

What should risk, legal, and finance review every month to prove control effectiveness?

Review blocked, reviewed, and allowed-with-monitoring volumes together, not in isolation. Include dispute-rate tracking and watch for shifts after major policy changes. Risk, legal, and finance should align on whether controls are reducing abuse while keeping dispute exposure manageable.

Which records should we retain to defend block decisions during audits or disputes?

Retain records that let you reconstruct the decision and the supporting evidence. For a dispute or chargeback, Stripe specifically allows text, images, and your counterargument, so keep those artifacts with any proof that the payment was valid. If you cannot reconstruct why the account was blocked and what evidence existed at the time, the decision is harder to defend later.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Platforms Detect Free-Trial Abuse and Card Testing in Subscription Fraud

If your platform sells subscriptions while also handling contractor, seller, or creator payouts across markets, this is not just a signup filter issue. It is a control design issue that cuts across risk, finance, legal, compliance, and product. The damage often shows up later in the customer lifecycle, not only at account creation.

How B2B Platform Operators Design Free Trials That Convert Profitably

The main mistake is simple: teams often optimize for more starts when they should optimize for more profitable paid customers. In B2B SaaS, **trial-to-paid conversion rate** is the share of trial users that become active paying customers in a defined period. That number only matters if the customers who convert are the right ones for your business.

How to Price a Clinical Trial Data Analysis Project

If you choose on fee alone, you are optimizing the smallest visible number, not the full cost of the decision. A better test is simple: **risk adjusted cost = expected project fee + probable rework cost + operational delay impact + the cost of switching vendors midstream**.