Quick Answer

No. tax free digital nomad visas are not automatically tax free in practice, because visa permission and tax treatment are separate decisions. Use the 183-day rule as a planning alert, then confirm residency consequences, sourcing rules, and home-country obligations before paying fees. If you are a U.S. filer, plan for return filing and Form 2555 mechanics even when local tax appears low.

You're not buying a tax-free lifestyle, you're choosing a tax outcome#

A digital nomad visa can support a lower-tax plan, but it does not create a tax-free result on its own. Treat every promise as conditional until you map tax residency, filing duties, and income type in writing.

A digital nomad visa gives legal permission to live abroad and work remotely, often for 6 to 12 months and sometimes longer. That is different from a tourist visa, which typically restricts work activity. The upside is potential, not automatic. You may qualify for relief such as the Foreign Earned Income Exclusion, but only under specific conditions and only for earned income.

What you can expect from this guide#

If you use the 90-day relocation sequence, treat it as a planning tool, not a universal legal rule. The goal is to reduce avoidable delays before you commit to applications, flights, or housing. Use a reusable document checklist and a few decision points to test each country option early:

- Visa status check: confirm the permit allows remote work and fits your intended stay.

- Tax position check: identify whether foreign tax residency could apply and how your income is classified.

- Evidence check: keep travel logs and core income records from day one to support filing.

Where plans usually fail#

The most common mistake is treating tax-free as no filing. Compliance does not work that way. US citizens abroad are still expected to file US taxes annually and report worldwide income. For self-employment income, the filing threshold can be as low as $400 per year.

Another failure mode is waiting until tax season to organize records. Missing travel logs or income records can weaken your filing position. Missed filings can trigger penalties, interest, and enforcement risk.

Scope and limits#

Country programs can lead to different tax outcomes, and tax-free can mean very different results once tax residency applies. This guide separates marketing language from the mechanics that drive liability. If a rule is country-specific or unclear, treat it as unresolved until you verify it against program terms and your filing facts. Then define what tax-free means in your case before comparing countries.

What "tax-free digital nomad visa" means in real terms#

In practice, the phrase describes a possible tax outcome, not what the visa itself grants. A digital nomad visa can let you live and work abroad, but your actual tax position still depends on tax residency, home-country rules, and factors like citizenship, employment status, and company structure. Before you compare countries, pin down these terms:

- Digital Nomad Visa: permission for remote workers to live and work abroad.

- Tax residency: status that can change where you owe tax; a common rule of thumb is 183 days or more in one country.

- Citizenship-based taxation: for US citizens, tax filing obligations can continue even while living outside the United States.

Those definitions separate outcomes that often get blurred together. Ongoing filing obligations may still apply, and visa approval is separate from favorable tax treatment.

Public guidance is often inconsistent. One page may market zero tax while another says the answer is case by case, so treat broad claims as provisional until your facts are reviewed. Use this interpretation rule for every country option:

- If a claim says tax-free, check what changes at the tax residency trigger and what does not.

- If you are a US citizen, assume citizenship-based filing continues unless qualified advice confirms otherwise for your situation.

- If key terms are vague, pause and get professional review from an immigration and tax lawyer before paying fees.

If you want a deeper dive, read Croatia Digital Nomad Visa: Live and Work on the Adriatic Coast.

Choose your path before you compare countries#

Classify your tax exposure first, then compare countries. The visa is only one layer of the decision, so focus this step on residency status and income sourcing before you pay application fees. Use this pre-screen checklist as a filter, not a legal conclusion:

| Factor | What to track | Why it matters |

|---|---|---|

| Expected stay length | Day counts and approach to key thresholds | Use day counts as a trigger to review status before you cross key thresholds |

| Work location | Where services are physically performed | Sourcing can follow where work happens |

| Home-state ties | Domicile signals and filing posture | Keeps your timeline and records consistent |

Treat day-count rules as planning alerts, not final answers. California guidance uses a facts-and-circumstances approach, not a single bright-line test. New York guidance starts by classifying you as resident, nonresident, or part-year resident.

A common failure point is assuming state exposure ends as soon as you relocate. California can still treat income as California-source to the extent services are physically performed in California, and compensation may be apportioned using CA Workdays / Total Workdays.

Before you pay visa fees, build a classification file with your timeline, day logs, invoice dates, and where work was physically done. If California is in scope, prepare for Form 540NR; if New York is in scope, test filing triggers early, including the $4,000 and $3,100 thresholds in state guidance.

Decision rule: if your plan may cross residency thresholds, pause country comparisons until residency classification and source-of-income treatment are clear in writing.

Compare visa tax models with one scoring table#

Use one scoring table to separate documented tax mechanics from marketing language. The point is to filter out assumptions and keep only options you can defend in writing.

Start with three model buckets: no local tax on foreign income, where explicitly stated; reduced local tax rate; and treaty-dependent treatment that requires written confirmation. Then score renewal friction, evidence burden, and unresolved items. With more than 50 countries offering remote-work visas as of 2025, this keeps your process consistent instead of guesswork.

| Program | Working model bucket | Concrete lever you can verify now | Renewal friction | Evidence burden | Unknowns that should stop payment |

|---|---|---|---|---|---|

| Barbados Welcome Stamp | Unknown from current pack | Program name is in scope for comparison only | Not established in current pack | Not established in current pack | Tax mechanics and residency conditions not documented here |

| Malta Nomad Residence Permit | Mixed signals: reduced-rate framing vs no-tax-on-foreign-income framing | One source describes a 1-year permit, renewable up to 4 years | Multi-year planning needed because renewals are capped in cited framing | Must reconcile conflicting tax descriptions before filing plan | Conflict on tax treatment: one framing cites 10% on locally sourced work plus a 12-month holiday, another cites 0% on foreign income |

| Greece digital nomad visa | Unknown from current pack | Program name is in scope for comparison only | Not established in current pack | Not established in current pack | Tax model and treaty interaction not documented here |

| Spain digital nomad visa | Reduced local rate with separate foreign-income treatment | One source summary cites 0% foreign income treatment and a 24% flat rate on local earnings for up to 6 years | Duration claim implies longer planning horizon | Need clear proof of what counts as local vs foreign earnings | Treaty treatment and residency interaction still require written confirmation |

| Italy digital nomad visa | Unknown tax model from current pack | One source summary cites a €32,400 annual income level | Not established in current pack | Income proof appears central based on cited threshold | Local tax mechanics and treaty interaction not documented here |

Treat uncertainty as a core risk signal, not a footnote. A moderate-tax option with transparent rules and predictable timelines is usually more usable than a low-tax claim with unclear residency conditions. Apply this decision rule before any fee payment:

- Keep only countries where visa status and tax mechanics are both documented in writing.

- Move countries with conflicting tax statements to a hold list.

- If treaty-dependent relief is the main value, get written confirmation that it applies to your facts.

- Reject options where renewal limits, tax model, or evidence requirements are still unclear.

Country examples that readers care about and where claims break#

Treat each country pitch as a starting assumption. Before you pay any fee, verify tax treatment, residency triggers, and renewal rules in writing.

| Country snapshot | What is commonly marketed | What you must verify before fee payment | Good fit if | Bad fit if |

|---|---|---|---|---|

| Croatia | Often marketed in nomad content as a remote-worker base with a lighter-tax narrative. | Tax residency trigger, source-of-income treatment, renewal terms, and current official requirements and fees. | You can track day counts and wait for written confirmation. | You need certainty from blog summaries alone. |

| Dubai (United Arab Emirates) | Often framed as tax-light for location-independent workers. | How your income is classified in practice, when residency status changes, renewal continuity, and home-country filing exposure. | Your records are clean and you can document where income is earned and received. | You assume visa approval automatically means favorable tax treatment. |

| Barbados | Often promoted as a lifestyle destination with remote-work access. | Income sourcing rules, renewal path, required document set, and whether guidance is still current on official channels. | You want a checklist and verify each item before travel. | You treat a marketing headline as a final tax answer. |

| Malta | Frequently presented as tax-efficient, but interpretation can vary by wording and personal facts. | Exact tax-treatment language, residency trigger, renewal limits, and any terms tied to foreign versus locally sourced income. | You are ready to get written clarification when wording is ambiguous. | You proceed while key tax terms remain undefined. |

| Island cluster (Anguilla, Antigua and Barbuda, Bermuda, Costa Rica, Dominica) | Often grouped as low-tax or tax-friendly choices in list articles. | For Costa Rica, confirm whether the route still extends a 90-day stay to one year with one renewal, plus current income and fee requirements. For the other islands, confirm current rules and costs on official sites because guides can go stale. | You compare documented requirements, not only destination appeal. | You choose based on older posts without validating current terms. |

For each option, keep a minimum verification pack:

- A dated capture of the official visa page with current requirements and fees.

- Required document proof, such as passport and insurance requirements, saved in your file.

- A day-count tracker that flags approach to the 183-day rule of thumb.

- Renewal continuity notes, including whether you may need to leave when status expires before re-entry.

A common failure point is confusing no income tax with no tax on foreign income. Those are different outcomes. If you are a US citizen, annual citizenship-based tax obligations can still apply while abroad, so destination choice alone does not remove filing duties.

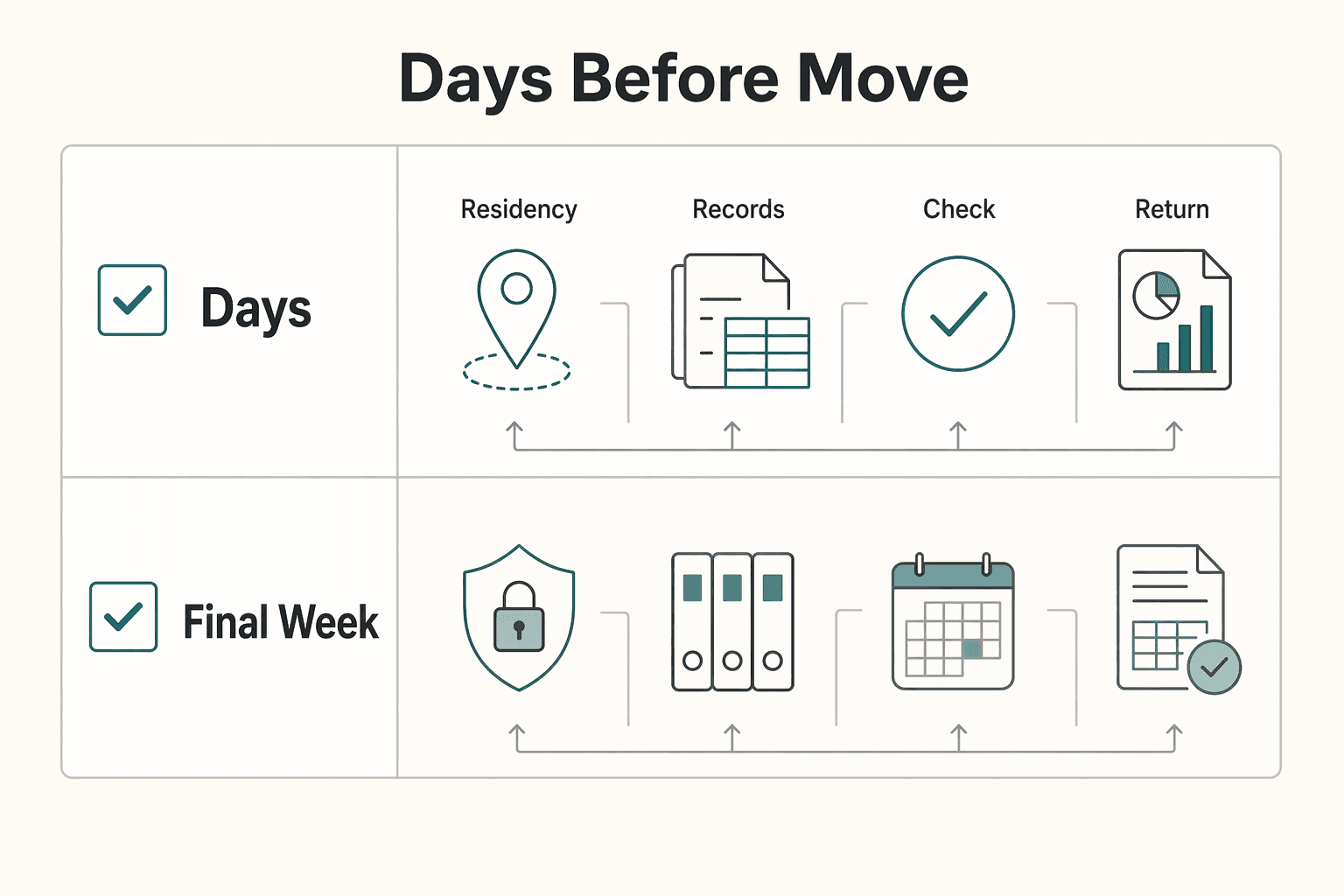

What to do in the 90 days before your move#

Before you pay final visa costs, lock in your filing plan and record process. Visa approval is only one input. Your goal in this 90-day window is a clear tax assumption set, a filing calendar, and records you can defend later.

| Window | Main focus | Key actions |

|---|---|---|

| Days 90 to 60 | Shortlist options and note tax exposure | Create one decision sheet per option with planned entry timing, expected day counts, income type, likely filing exposure, and open treaty questions for advisor review |

| Days 60 to 30 | Standardize the application package | Keep a dated copy of each official requirement page and match it to the exact documents you plan to submit |

| Days 30 to 7 | Finalize the filing plan | Draft your Form 2555 approach if you are a U.S. filer, track qualifying days, and calculate the foreign housing exclusion first if you are also claiming housing |

| Final week | Set up the record repository | Tag residency records, income records, filing records, and control records by date and jurisdiction |

Days 90 to 60#

Shortlist two or three visa paths and create one decision sheet per option. For each one, note planned entry timing, expected day counts, income type, likely filing exposure, and any open treaty questions for advisor review.

If your timeline or facts are unclear, pause fee payment until you have written clarity on classification and reporting impact. A short delay now is usually easier than correcting avoidable filing mistakes later.

Days 60 to 30#

Build your application pack early and standardize it across options. Keep a dated copy of each official requirement page and match it to the exact documents you plan to submit.

Focus on evidence quality, not just quantity. If wording is ambiguous or your records do not clearly support your case, resolve that now instead of during review.

Days 30 to 7#

Finalize your filing calendar, then draft your Form 2555 approach if you are a U.S. filer. U.S. citizens and resident aliens are taxed on worldwide income, and FEIE does not remove the requirement to file and report income.

For 2026, the FEIE maximum is $132,900 per qualifying person. FEIE applies only to wages or self-employment income for services performed in a foreign country. If you qualify for only part of the year, that limit is adjusted by qualifying days, so day tracking is critical. If you are also claiming housing, calculate the foreign housing exclusion first because it reduces income available for FEIE. The general 2026 housing limitation is $39,870, generally 30% of the FEIE maximum.

Also check whether any IRS-published waiver of time requirements applies to your country and dates. Flag any periods involving U.S. travel restrictions, because income earned during a period of violation does not qualify as foreign earned income. If you are leaving California but still have California-source work, prepare Form 540NR support and keep workday allocation records. Use IRS LB&I practice units as guidance, not binding authority.

Final week#

Set up one audit-ready repository before you travel, tagged by date and jurisdiction.

- Residency records: visa approval, entry records, address evidence, day logs

- Income records: contracts, invoices, payment confirmations, account statements

- Filing records: Form 2555 inputs, FEIE and housing calculations, calendar checkpoints

- Control records: requirement-page captures, issue dates, expiry dates, renewal reminders

This is where planning turns into execution. If rules change later, you can respond with dated evidence instead of memory. Turn the 90-day plan into a trackable timeline with the Tax Residency Tracker.

Build the document pack once and reuse it everywhere#

Treat documentation as part of the move, not cleanup work. Build one reusable pack so visa filing, U.S. tax filing, and account reporting all draw from the same records.

| Pack | Purpose | What to keep |

|---|---|---|

| Core visa pack | Reuse one master Digital Nomad Visa folder for each country application | Visa application records together, tagged with clear dates and jurisdictions |

| Tax pack for Foreign Earned Income Exclusion and Form 2555 | Build the pack around FEIE eligibility, not visa approval | Residency timeline, entry and exit records, day logs, source-of-income map, FEIE limit used ($130,000 for 2025, $132,900 for 2026), and a separate housing exclusion file if used |

| U.S. reporting pack where relevant | Track FBAR evidence throughout the year | Periodic statements supporting each account's maximum value and any non-Treasury exchange rate source used |

Core visa pack#

Create one master Digital Nomad Visa folder and reuse it across applications. Keep application records together and tag files with clear dates and jurisdictions.

Tax pack for Foreign Earned Income Exclusion and Form 2555#

Build this pack around FEIE eligibility, not visa approval. FEIE is claimed on Form 2555, and you still file a U.S. return reporting income. Keep a residency timeline, entry and exit records, day logs, and a source-of-income map showing where services were performed.

For planning files, keep the tax-year FEIE limit you are using ($130,000 for 2025, $132,900 for 2026) and any partial-year day-based adjustments. If you are using the housing exclusion, keep that calculation file separate. Keep records for exceptions, waivers, and restricted-country issues, since qualifying treatment still depends on actual days of presence and eligible income.

U.S. reporting pack where relevant#

Track FBAR evidence throughout the year. If a single-account maximum or aggregate maximum exceeds $10,000 during the calendar year, FBAR filing is required. Keep periodic statements that reasonably support each account's maximum value, and if you use a non-Treasury exchange rate, store that rate source with the file.

Use one tagging structure across all folders: date, jurisdiction, document_type, covered_dates, account_or_contract_id, and related form (Form 2555, FBAR).

Related: Dubai, UAE: The Ultimate Digital Nomad Guide (2025).

The US citizen reality check most listicles skip#

A digital nomad visa can change where you live, but it does not switch off U.S. tax compliance. Under citizenship-based taxation, U.S. citizens abroad are still taxed on worldwide income.

What does not change after you move#

Living abroad is not the same as leaving the U.S. tax net. Keep an annual filing calendar and treat U.S. filing as a recurring obligation, even if your host country has low or zero local tax.

One common year-one mistake is assuming exclusions mean no return. Foreign Earned Income Exclusion is a benefit for qualifying foreign earned income, not a filing waiver. You claim it on Form 2555, and you still file a U.S. return reporting income.

What FEIE and housing can reduce#

Foreign Earned Income Exclusion can reduce taxable income, but only if you qualify and only within annual limits. The maximum is $130,000 for 2025 and $132,900 for 2026 per qualifying person. If both spouses qualify in 2025, the combined exclusion can reach $260,000.

The foreign housing exclusion or deduction can reduce taxable income further, but it has separate limits. The general housing cap is 30% of the FEIE maximum, with stated limits of $39,000 for 2025 and $39,870 for 2026.

Waivers for war or civil unrest may apply in specific cases, but qualifying calculations still depend on actual days of residence or presence. Time in a country in violation of U.S. law does not produce qualifying foreign earned income for FEIE purposes.

Separate account reporting from tax return filing#

Income tax filing is one layer. FBAR is a separate layer through FinCEN when foreign account maximum values exceed $10,000, whether in a single account or in aggregate across accounts.

For FBAR support, keep periodic statements that reflect each account's maximum value, then record amounts in U.S. dollars rounded up to the next whole dollar. Keep ownership records, entity links, and balance evidence organized by holder and tax year.

What to verify in your first 30 days after arrival#

In your first 30 days, focus on two outcomes: a defensible record trail for U.S. reporting and a written list of unresolved local questions. Treat this as a verification window, not a waiting period.

Create a 30-day log for Digital Nomad Visa status, Tax residency questions, and Bilateral tax treaties assumptions. Keep these as country-specific unknowns until you receive official written confirmation.

Confirm status and evidence in parallel#

Set up one arrival-month folder and tag each file by date, jurisdiction, and document type. Keep official notices, account records, and transaction support together so you can explain what happened without relying on memory.

If your foreign account footprint changes, reopen your assumptions and document the change. When facts change, earlier notes may no longer hold.

Set monthly reminders for FBAR and Form 8938 hygiene#

Use recurring monthly checkpoints tied to your filing calendar.

- Save periodic account statements that fairly reflect each account's maximum value for the year.

- Track when a single account or aggregate foreign account maximum exceeds

$10,000, because FBAR is then required. - Treat FBAR and

Form 8938as separate checks. FilingForm 8938does not replace FBAR when FBAR is otherwise required. - For

Form 8938, track the applicable calendar year or tax year and remember it is attached to your annual return and filed by that return's due date, including extensions. - Keep records for specified foreign financial assets so threshold checks are straightforward at filing time.

- If you are not required to file an income tax return for the year,

Form 8938is not required.

Red flags that turn a "tax-free" plan into a tax problem#

The biggest red flag is treating a headline claim as your final tax position before your records support it. Use your first-month documentation habit to test assumptions early, not at filing time.

Day-count shortcuts without hard records#

A simple day-count shortcut is not enough on its own. If your position depends on days, keep one reconciled travel log with entry and exit dates, address periods, and work-location notes.

If records conflict, treat your count as unresolved until you reconcile it. This matters even more when plans change mid-year.

Program wording treated as universal#

A tax label used in one program is not a universal default in another. Problems start when people rely on marketing language instead of the exact program terms that apply to their facts.

The same caution applies to country-level claims. A headline does not automatically determine your personal filing outcome.

Home-country obligations discovered too late#

In the United States, FinCEN reporting can still apply even if your local setup looks clean. For FBAR, filing is required if one foreign account maximum or the aggregate maximum exceeds $10,000 at any point in the calendar year. If neither reaches that level, FBAR is not required.

Use periodic statements to support each account's maximum value, and if no Treasury exchange rate is available, use another verifiable rate and keep the source. For most people with an FBAR obligation, the due date remains April 15, 2026; the April 15, 2027 extension is limited to certain filers with signature authority but no financial interest.

State exposure is another common miss. If California is in your timeline, part-year residency and California-source income can still apply, and the workday ratio (CA Workdays / Total Workdays) can directly affect sourcing.

Pick clarity over hype and make your move defensible#

The goal is not just visa approval. It is a tax position you can explain and document if questioned later.

Treat every country claim as provisional until you can show where tax is owed, whether filings may be due, and which facts support that outcome. Country-hopping does not remove tax obligations, and some people can face obligations in more than one country in the same year.

Use this three-gate check before you pay any application fee:

- Classify the likely outcome first. Is this single-country taxation, possible multi-country exposure, or still unresolved?

- Test legal connection factors against your facts. Birthplace links, home access, and where you actually live can all affect where tax is owed.

- Verify your evidence pack. Keep one consistent record trail for travel dates, housing access, income declarations, and filing assumptions.

A day-count can help with planning, but it is not a complete defense on its own. If your records are inconsistent, or income is not fully declared and required taxes are not paid somewhere, a planning mistake can turn into potential evasion exposure.

Final caution: country-level commentary is useful for orientation, but jurisdiction details still need local confirmation before you rely on them. Treat unclear residency, filing, or proof requirements as high risk, even when marketing sounds simple.

Next step: shortlist two countries, run the same comparison table for both, and clear unknowns in writing before applying. Start with the Global Digital Nomad Visa Index. Then remove any option that cannot clearly answer residency, filing, and evidence questions. Before paying application fees, document your shortlist and assumptions in one place, then review Tools as needed.

Frequently Asked Questions

Are digital nomad visas actually tax free?

Usually not. A digital nomad visa handles immigration permission for a defined stay, but it does not automatically remove income-tax or social-security exposure. Treat tax free as unconfirmed until your residency and tax treatment are assessed under the rules that apply to your facts.

Does staying under the 183-day residency rule guarantee no tax?

No. The 183-day threshold appears in many systems, but countries apply their own residency tests and often use more than one trigger. Even a stay under six months can still leave tax exposure.

Can US citizens avoid taxes with a digital nomad visa?

A digital nomad visa does not, by itself, end US compliance. IRS international guidance still covers topics like foreign earned income exclusion and reporting of foreign financial accounts. Plan for ongoing filing and reporting review before you move.

What is the difference between tax relief and true tax-free treatment?

Tax relief means tax may be reduced under specific rules, while true tax-free treatment means no tax is due after applying the law to your exact situation. The key difference is evidence and eligibility, not marketing language.

Which documents prove my tax position if I’m audited?

There is no single universal document set that works in every jurisdiction. Keep a consistent record trail that supports your day count, residency position, income pattern, and any filings you rely on. What matters is whether your records support the position you are taking under the applicable rules.

How do bilateral tax treaties affect digital nomad visa holders?

Treaties can help when two countries both treat you as resident, but they do not apply automatically. Residency conflicts are typically resolved with tie-breaker criteria such as permanent home and center of vital interests. Treaty protection can be denied.

Is Malta’s remittance basis treatment the same as paying zero tax?

No. Remittance-basis treatment is not the same as guaranteed zero tax. Whether tax is due depends on your facts and how the relevant residency and tax rules apply during your stay.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The 2026 Global Digital Nomad Visa Index for 50+ Countries

Start with legal fit, not lifestyle filters. The practical order is simple: choose a route you can actually document, then decide where you want to live. That single change cuts a lot of wasted comparison work and stops you from falling in love with places that were never a real filing option.

Croatia Digital Nomad Visa: Temporary Stay Rules, Eligibility, and Application Planning

Treat this as a **temporary residence permit** route, not a tourist-stay workaround. People often say "digital nomad visa," but for move planning, the distinction that matters is simpler: short-stay entry and temporary residence solve different problems.

Dubai Digital Nomad Guide 2026 for a Practical Move Plan

If this move works for you, it will work because you sequence decisions well and keep risk reversible until your status is clear. Treat this route as a chain of checkpoints, not one giant yes or no decision made under time pressure.