Quick Answer

Yes, use the fair credit billing act process when the charge itself is wrong, then send a written dispute tied to the statement that first showed the error within 60 days. Start by reconciling the line item against your invoice, subscription, or cancellation record, and submit only documents that match the exact dispute reason. For business cards, confirm your issuer’s current written dispute terms the same day you file. Keep proof of submission and every status update in one case folder.

Your Secret Weapon Against Unfair Charges: A Business-of-One's Guide to the FCBA#

If you run a solo service business, start with the right filter: use the fair credit billing act track for credit card account billing errors, not for every payment dispute that feels unfair. Pull the statement line first, match it to the invoice or subscription record, and decide whether you have a billing-error problem or a service complaint.

Before you start: This section focuses on credit card account billing errors. If your payment method or card program is different, use your issuer terms as the rulebook for next steps.

Step 1. Use the right lane#

Use this as a sorting tool, not a catch-all remedy. The FTC consumer guidance points to the right starting place: "What to Do if There's a Billing Error on Your Credit Card Account," followed by a dedicated step called "How to Dispute Billing Errors."

That scope line matters. A billing-error dispute is not the same as "the work was poor" or "the software was disappointing." The FTC separates quality complaints from billing-error disputes. Mixing those up is a common failure mode. If the service was delivered and your issue is quality, you may still have a contract or refund argument, but it is a different track.

Step 2. Sort the issue before you file#

Start by labeling the problem clearly in your notes. That step shapes what you file, what evidence you gather, and what outcome is realistic. Use these as practical labels, not legal categories:

- Possible billing-error issue

The charge line on your credit card account does not reconcile to your records.

- Unrecognized charge line

You cannot tie the statement line to a vendor, order, or subscription you recognize.

- Quality complaint

The vendor delivered something, but it was defective, late, or below expectations.

| Scenario | Best first read |

|---|---|

| Your project-management tool bills the same monthly plan twice | Start with billing-error review |

| A foreign vendor's processor descriptor looks unfamiliar, but the amount matches your invoice | Verify first, then dispute if it still does not reconcile |

| A free trial converts to a paid tier you did not mean to keep | Review as a possible billing-error issue, then reconcile against your records |

| A consultant delivered unusable work, but the charge matches the signed proposal | Quality complaint, not a billing-error first step |

Step 3. Verify the record you will rely on#

Do not file from memory. Build a tight evidence pack first. For freelancers and consultants, that usually means the card statement screenshot, invoice, checkout receipt, cancellation email, contract or SOW, and any message confirming price, currency, or renewal terms. Also confirm whether the merchant name on the statement differs from the brand name you expected.

Use one checkpoint before you file: can a stranger look at your file and see exactly why the charge does not belong? If not, pause and reconcile first. That habit prevents weak disputes and helps you avoid turning a valid complaint into a credibility problem later.

If you also want the merchant-side view of dispute fallout, read How to Protect Yourself from Chargebacks as a Freelancer. For other Gruv tools and guides, see Germany Freelance Visa: A Step-by-Step Application Guide and Try the SOW generator.

Part 1: Fortify Your Operations to Prevent Disputes#

Start with prevention: control payment rails before charges happen, then keep records complete enough to support fast error reporting.

If your card program supports virtual cards, run this checklist:

- Assign one card per vendor so each charge maps to a single relationship.

- Set spend controls by vendor and update them as scope changes. Current limit example pending policy/source-record verification.

- Put trial subscriptions on tightly controlled cards and review renewal settings before conversion.

- Use a cancellation workflow: cancel in writing, save the confirmation the same day, and store it with the related invoice/statement line.

- Keep one communication owner for billing issues so reporting is immediate and consistent.

Pre-transaction controls are stronger than post-charge cleanup because weak process hygiene creates avoidable failure modes: incomplete records, delayed reporting, and missed updates.

| Checkpoint | What to verify before a problem starts |

|---|---|

| Vendor identity | Merchant descriptor matches the vendor you approved. |

| Documentation completeness | Your required records are complete and signed where applicable. |

| Update monitoring | You actively monitor vendor/account updates instead of relying only on optional notices. |

| Cross-border billing quality | Invoice shows clear billing currency, usable tax/VAT detail where relevant, and a support contact with response accountability. |

When an alert appears, follow a fixed sequence: flag the line item, reconcile it against your invoice or subscription records, package the evidence (statement, invoice, cancellation proof, key messages), and report suspected errors immediately through your designated contact path. Calendar your internal follow-up point, and verify the external filing window from official legal materials and issuer records before use.

If you want the downstream merchant-risk view after prevention controls, read How to Protect Yourself from Chargebacks as a Freelancer. Related: Taxes in Germany for Freelancers and Expats.

Part 2: Build Your "Digital-First" Paper Trail for an Unbeatable Dispute#

Build a submission-ready evidence package before you contact support so the issuer can verify the issue quickly. Keep each disputed charge tied to one clear explanation and one matched set of supporting documents. That makes your file easier to review and harder to reject as incomplete.

A digital-first workflow is practical because you can gather, label, and submit in one pass. The two common failure points are picking the wrong dispute reason and uploading files that do not clearly map to the exact charge.

Before you start#

Create one case folder, keep originals untouched, and upload copies. Save copies of everything you submit, plus confirmation artifacts. Use a consistent naming format such as YYYY-MM-DD_VendorName_amount_disputed-charge.png.

| Dispute type | Issue field | Optional sentence |

|---|---|---|

| Unauthorized | unauthorized | I did not authorize this transaction. |

| Duplicate | duplicate | I was charged more than once for the same transaction. |

| Canceled recurring charge | canceled but still billed | I canceled on the cancellation date, but billing continued. |

| Incorrect amount | incorrect amount | The posted amount does not match the agreed or authorized amount. |

Also keep a one-page chronology log with five columns: date, event, amount, artifact filename, and why it matters. This gives you a clean index if the issuer asks follow-up questions or limits uploads.

The same documentation discipline helps if this later turns into merchant pushback or chargeback handling. Related: How to Protect Yourself from Chargebacks as a Freelancer.

| Artifact | Why it matters | Example filename |

|---|---|---|

| Statement or transaction screenshot with the charge clearly marked | Identifies the specific disputed item | YYYY-MM-DD_BankStatement_charge-marked.pdf |

| Contract, invoice, order page, or cancellation record | Shows what was authorized or agreed | YYYY-MM-DD_Vendor_contract.pdf |

| Email thread or chat transcript | Preserves dates, facts, and responses | YYYY-MM-DD_Vendor_support-thread.pdf |

| Proof of non-delivery, duplicate billing, or wrong amount | Connects your claim to a concrete error | YYYY-MM-DD_duplicate-charge-comparison.png |

| Submission proof (confirmation screen or email) | Shows what you filed and when | YYYY-MM-DD_dispute-confirmation.png |

- Identify the exact disputed item.

Start with the exact entry: merchant name, transaction date, posted date (if shown), and amount. State the facts and why you dispute that item. If multiple charges are wrong, track each as its own line item.

- Check timing and submission path.

Log in, find the transaction, and use the issuer's dispute path if available. Record the statement date where the charge first appeared, then verify the current notice window from official legal materials and issuer records before use. Before you submit, confirm that the amount and merchant in the form match your evidence folder.

- Choose the closest accurate dispute reason and match evidence to it.

Pick the category that best fits the facts (for example: unauthorized, duplicate, incorrect amount, canceled but still billed, or service not provided). Attach only documents that prove that reason. If options are broad, choose the closest accurate one and clarify in the message box.

- Build one concise evidence pack.

Keep originals, upload copies. If multiple files are allowed, attach in chronology order. If only one file is allowed, merge into one PDF and add a short index page listing each artifact and what it proves. Keep full context in screenshots so dates, names, and amounts remain visible.

- Submit a factual message and save proof.

Keep your note short and specific. Ask the issuer to investigate and correct or remove the disputed item as appropriate. Save the confirmation screen, case number, acknowledgment email, and final uploaded file. If you also send paper documents outside the portal, certified mail with return receipt gives you proof of receipt.

Use this fill-in message in the portal:

I am disputing the following charge: the merchant name, the transaction date, the charge amount.

The issue is: [unauthorized / duplicate / incorrect amount / canceled but still billed / service not provided].

Facts: [1 to 3 short sentences with dates and what happened].

Supporting documents attached: [list 2 to 4 items].

Please investigate this item and [correct/remove/reverse] it if your review confirms the error.

Optional second sentence by dispute type:

- Unauthorized: I did not authorize this transaction.

- Duplicate: I was charged more than once for the same transaction.

- Canceled recurring charge: I canceled on the cancellation date, but billing continued.

- Incorrect amount: The posted amount does not match the agreed or authorized amount.

For a step-by-step walkthrough, see Credit Invoices Explained: How to Issue Reversals and Adjustments in a Subscription Billing Platform.

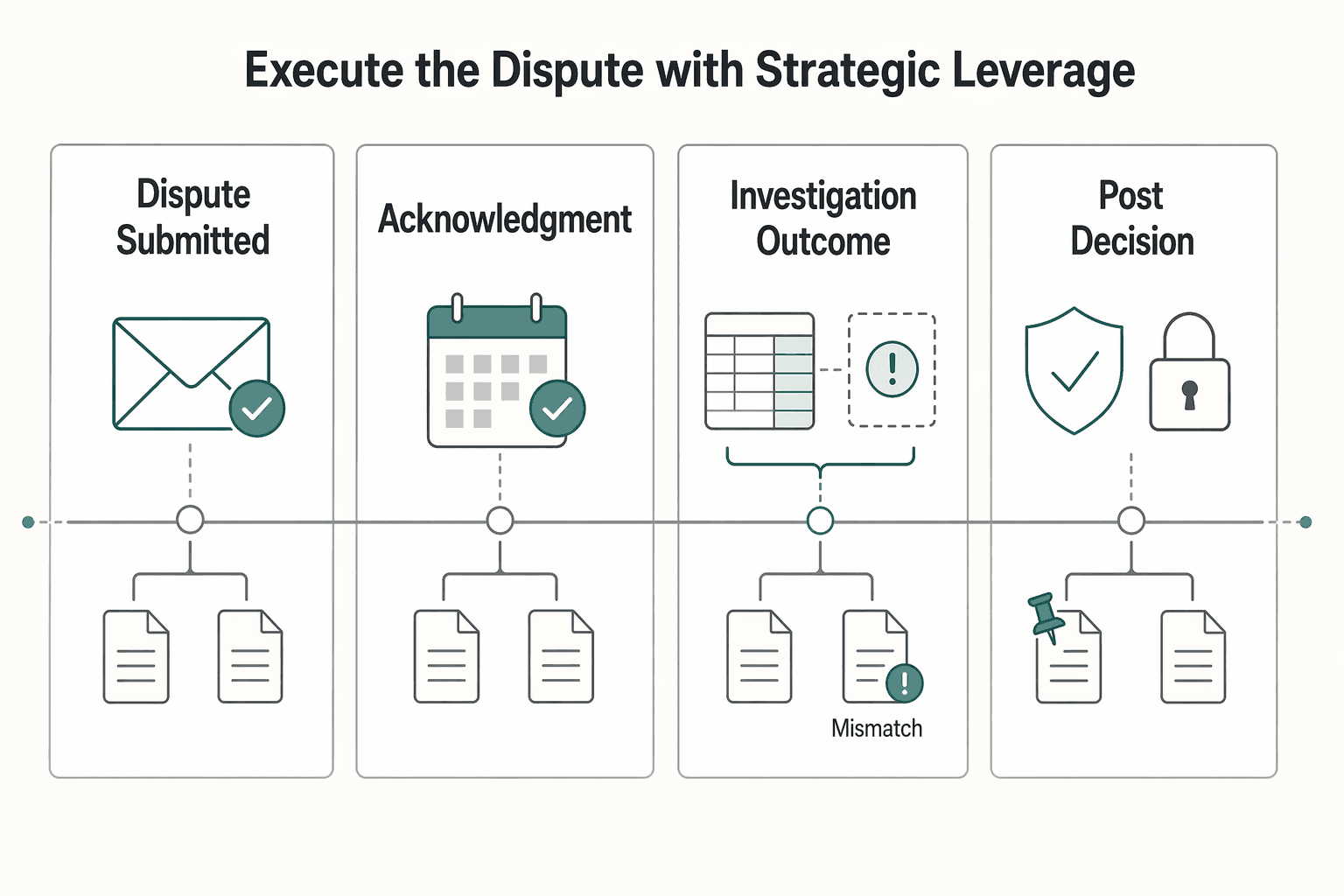

Part 3: Execute the Dispute with Strategic Leverage#

After you submit, shift into process control: confirm intake, track handling, protect service continuity, and escalate with records if the process breaks.

The sequence is: submit, monitor, contain, then escalate. Strong cases usually fail from weak follow-up, not weak evidence.

Step 1: Submit and freeze the record. Save the final narrative, all uploaded files, the confirmation screen, the case/reference number, and any visible timestamp. Then verify that the merchant, amount, and transaction date match your chronology log exactly.

If you used a business card, download the current cardmember agreement and dispute-policy page the same day. Do not assume consumer-card handling applies the same way, and confirm the exact process in the issuer's current written materials.

Step 2: Calendar checkpoints and verify current rules in writing. Use your issuer's written case notices, current agreement, and verified official legal materials. Do not rely on memory, old summaries, or chat-only guidance.

| Milestone | Deadline to verify | What you expect to see | Your next move |

|---|---|---|---|

| Dispute submitted | Day 0 (filing date) | Confirmation screen, case number, saved upload set | Calendar check-ins and note where status updates appear |

| Acknowledgment | Current acknowledgment deadline pending legal/source-record verification. | Written or portal confirmation that the case is open | If missing, send a secure message asking for written receipt and open date |

| Investigation outcome | Current resolution deadline pending legal/source-record verification. | Written decision, correction, or explanation | If missed, send a formal written follow-up and prepare escalation records |

| Post-decision review | Current response/review window pending legal/source-record verification. | Any rebill, reversal, fee treatment, or document request | Compare outcome to your original claim and reply in writing on any mismatch |

If you use FederalRegister.gov for reference, confirm you are relying on an official version. Its XML view is informational, and the page points you to a printable PDF route for record-quality verification.

Use this checklist to confirm how the disputed amount will be handled while review is open (especially for business cards, where issuer policy can differ):

- whether payment is still requested on the disputed amount

- whether interest/fees may continue posting and how corrections are handled if you prevail

- whether delinquency reporting or account restrictions may occur during review

- whether any denial includes a written explanation and response path

Step 3: Contain merchant-side risk early. Your issuer case does not guarantee uninterrupted service from the merchant. For critical tools (hosting, software, ads, infrastructure), request written continuity confirmation immediately. This pairs with broader continuity controls in How to Protect Yourself from Chargebacks as a Freelancer.

Use this short template:

We filed a card dispute for the disputed amount on the dispute filing date tied to the invoice or order reference because the reason for the dispute.

Please confirm in writing:

- whether service stays active during review, and

- the current billing/dispute status on your side.

Step 4: Escalate with evidence, not frustration. Escalate when you can document a process failure, not just an unfavorable result. Clear triggers include:

- missed issuer milestone after your own written verification (

Add verified timing reference) - case closure without written explanation

- repeated contradictions between support messages and formal notices

- account actions that conflict with the issuer's written dispute handling

For CFPB escalation, attach a tight evidence packet:

- statement page with disputed charge marked

- dispute submission confirmation and case number

- chronology log from Part 2

- dated secure messages, emails, and chat exports

- screenshots of portal status changes

- decision letters, rebills, fees, or related account entries

Final guardrail: do not mix billing-dispute law with credit-reporting law. The FTC's FCRA material (15 U.S.C. §§ 1681-1681x) addresses consumer reporting, not FCBA billing-error handling.

You might also find this useful: How AI Platforms Should Use Credit-Based Billing Models.

Conclusion: From Consumer Right to Executive Tool#

Used correctly, the FCBA is not just a legal backstop for consumers using open-end credit accounts. It is also a practical risk-control framework: document the issue in writing, trigger the creditor's acknowledgment and investigation process, and track the outcome.

The real value of this guide is the sequence: sort the charge correctly, build a clean evidence file, then manage the dispute like an operator. The risk does not disappear, but it is easier to contain when your records are tight and your next move is clear.

This is part of running your work like a business. Put guardrails around billing, know which rules apply to your account, and use the tools available to protect operations. For the systems side, we covered this in detail in How to Build a Subscription Billing Engine for Your B2B Platform. For legal conclusions, verify key details against official legal editions.

Frequently Asked Questions

What counts as a billing error under the fair credit billing act?

Focus first on classic billing errors on open-end accounts, such as unauthorized charges. Do not treat every bad purchase as a billing error. If the problem is product or service quality, try to resolve it with the merchant first, then notify the card company in writing if you are withholding payment until the matter is resolved.

What is the 60-day rule, and how should I track it?

Your written dispute must reach the creditor within 60 days of the billing statement date that first showed the error. Do not guess from memory or from when you happened to notice the charge. Save the statement, note the statement date in your chronology log, and send your notice early enough that you can show it was delivered on time.

What has to be in the written notice?

Include your name, address, account number, and the date and amount of the error. Attach copies, not originals, of receipts or other documents that support the claim, and keep a complete copy of what you sent. If you filed online, verify your issuer also treats that submission as satisfying its written-notice process.

What if the charge is on a business card?

Do not assume statutory protections map over automatically. Pull the current cardmember agreement and dispute-policy page, save the version available on the day you filed, and check exactly how that issuer handles billing errors, fraud, fees, and account restrictions.

Does a foreign merchant change the dispute process?

Treat the dispute with the same discipline: follow your issuer’s written process, track the 60-day deadline from the statement date, and include complete error details in your notice. Keep your records in one evidence set so your timeline is clear.

Can a software company suspend service during a dispute?

FCBA billing-error procedures focus on the card charge and do not by themselves resolve product or service quality complaints. For quality disputes, first try to resolve the issue with the merchant, then notify your card company in writing if you are withholding payment until the matter is resolved.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- consumer.ftc.gov/articles/sample-letter-disputing-errors-cred...trusted

- consumer.ftc.gov/articles/using-credit-cards-and-disputing-ch...trusted

- docs.cpuc.ca.gov/PublishedDocs/Efile/G000/M094/K269/94269837.PDFtrusted

- ecfr.gov/current/title-12/chapter-II/subchapter-A/par...trusted

- fairfaxcounty.gov/cableconsumer/csd/credit-cards-understanding...trusted

- federalregister.gov/documents/2004/11/30/04-26240/summaries-of-r...trusted

- federalregister.gov/documents/2025/12/15/2025-22772/fair-credit-...trusted

- files.consumerfinance.gov/f/documents/102012_cfpb_fair-credit-reportin...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Germany Freelance Visa Application Path for Freiberufler and Gewerbe

Choose your track before you collect documents. That first decision determines what your file needs to prove and which label should appear everywhere: `Freiberufler` for liberal-profession services, or `Selbständiger/Gewerbetreibender` for business and trade activity.

Taxes in Germany for Freelancers and Expats

Low-stress compliance in Germany comes from decision order, not tax tricks. Use this sequence: confirm core facts, apply conservative temporary assumptions, verify the few points that can break invoices or filings, and keep one evidence file that explains each decision.

How to Protect Yourself from Chargebacks as a Freelancer

**Chargeback prep can reduce avoidable losses, but it cannot guarantee a win.** The real goal is narrower and more useful: build a repeatable sequence you can follow before, during, and after a dispute so cash flow is less fragile and decisions are less reactive.