Quick Answer

Yes. Treat buy now pay later b2b services platforms as a gated pilot, not a full rollout. Start with one buyer segment, then test whether conversion gains beat merchant fees, dispute costs, and A/R timing drag. Require written terms for default, fraud, and partial-service disputes before integration. Keep a fallback checkout path for declines, and scale only after finance can reconcile settlement files to orders, ledger postings, and payouts without manual patchwork.

Buy now pay later for B2B services can lift conversion or quietly hurt margin#

Treat BNPL as a unit-economics decision first, not a checkout feature. For B2B services platforms, faster closes may help, but fees, disputes, and risk-management work can wipe out the upside if you do not model them up front.

- The promise is clear, but you still need to validate it in your own mix.

BNPL lets buyers receive services now and repay over time through short-term installment financing. Provider messaging usually emphasizes less friction, faster decisioning, and quicker merchant payout. One example says merchants are paid within 1 to 3 business days. The point is not the claim itself. The point is whether that speed improves margin for your buyers and deal types. The strongest published conversion evidence still comes from retail and consumer settings, so B2B services teams should treat lift as possible, not proven, until pilot data says otherwise.

- The real risk is margin compression from fees and operations.

BNPL can improve conversion in some contexts while raising your effective fee and operations cost. The Richmond Fed (January 2025, No. 25-03) notes that BNPL merchant fees are often higher than standard credit-card fees, and the CFPB describes BNPL as a blend of payments and credit with merchant transaction fees. Disputes add operating cost too. On May 22, 2024, the CFPB said users have dispute and refund rights similar to credit cards under its interpretation, and reported more than 13% of BNPL transactions involved a return or dispute. That is consumer-market data, not a B2B services benchmark, but it is enough to justify planning for dispute handling as a cost center.

- This guide is about B2B services execution, not generic checkout advice.

In services platforms, underwriting and risk policy are part of implementation, not side issues. The OCC says banks offering BNPL should operate in a safe-and-sound way, including clear loan terms, underwriting criteria, repayment-capacity methods, fees, charge-offs, and credit-loss allowance considerations. Before launch, confirm in writing who owns non-payment risk, how disputes are resolved, what payout timing actually occurs, and what delivery evidence your team must provide when work is challenged. Some B2B setups market non-payment coverage, but risk transfer is contract-specific and needs to be verified before rollout.

Who this shortlist serves and who should skip it#

Use this shortlist if you already feel A/R and payout timing pressure in a multi-party flow and can measure whether BNPL improves economics by cohort. Skip it if compliance gates are weak or invoicing is highly custom.

- Best fit: platforms with two-sided cash-timing pressure.

If you collect from buyers while paying sellers, earlier settlement can solve an operating problem, not just a checkout problem. One provider says it pays merchants upfront within 1 to 3 business days, and TreviPay positions around simplifying accounts receivable, embedded net terms, and getting paid faster. The real test is whether earlier settlement reduces A/R drag and payout stress in your model.

- Best fit: teams that can instrument outcomes beyond topline volume.

You need visibility into transaction outcomes, capture and refund activity, and cohort-level economics before and after launch. Finance also needs to reconcile transaction events and settlement reports to bank deposits. One provider documents both reconciliation reporting and transaction lifecycle statuses such as Authorized. Without that visibility, it is hard to tell whether BNPL is improving economics or simply shifting costs.

- Skip for now: platforms that cannot enforce KYC, KYB, and AML controls.

Verification and monitoring are core requirements, not process polish. Adyen states users must be verified before payments, payouts, and financial products are enabled. U.S. AML guidance includes ongoing monitoring for suspicious transactions, and 31 CFR 1010.230 requires identifying and verifying beneficial owners of legal entity customers. If those gates are not operational, downstream risk stays high even when front-door approvals look healthy.

- Skip for now: sales motions built on custom invoicing terms.

Some BNPL programs run on standardized eligibility and purchase-amount constraints. Public terms for one option note that choices depend on purchase amount, may vary by merchant, and require eligibility checks, with published financing terms showing 0% to 36% APR based on credit. If your revenue model depends on negotiated invoicing structures, fit is usually weak.

Need the full breakdown? Read Account Hierarchy for B2B Platforms and Parent-Child Billing for Enterprise Clients.

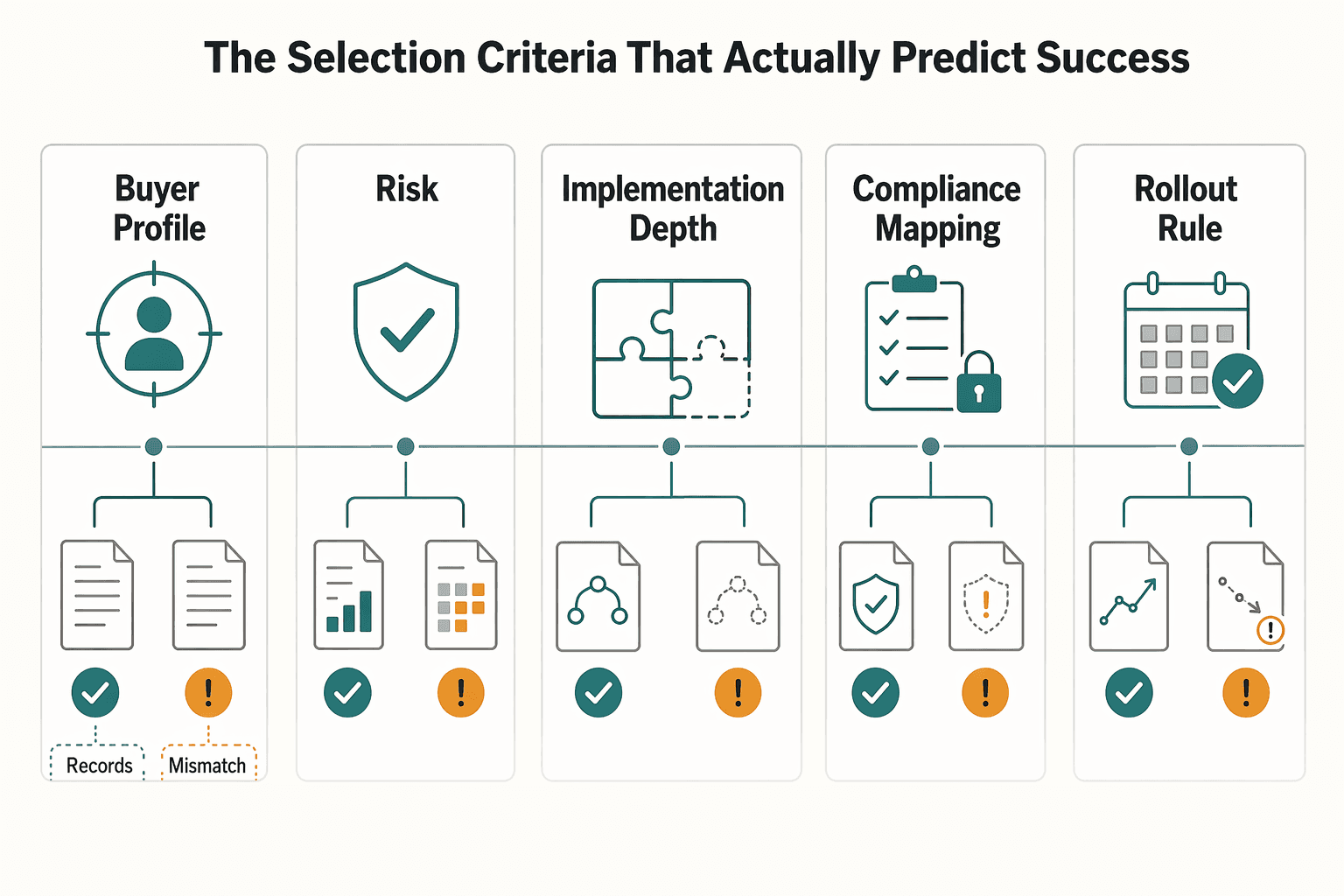

The selection criteria that actually predict success#

Start with buyer fit before pricing. Success usually comes from matching the provider's stated buyer profile and then proving that your risk, operations, and compliance flows hold up in production.

| Criterion | Grounded detail | What to check |

|---|---|---|

| Buyer profile fit | One B2B offer is positioned for eligible small businesses, including sole proprietors, with machine-learning underwriting and options across price points. Fit may be stronger if GMV is mostly checkout purchases from small operators and weaker if it depends on larger entities with negotiated invoicing. | Review recent buyers by legal form and order pattern before vendor calls. |

| Risk ownership | TreviPay describes reimbursing sellers while it assumes credit risk and manages collections. In the Amazon Business rollout, buyers proceed only if approved. | Get clear contract language on credit-loss allocation, reimbursement timing, and dispute handling. |

| Implementation depth | Stripe documents automatic webhook retries for up to three days, recommends duplicate-processing protection, and limits event retrieval for this workflow to the last 30 days. | Test delayed webhook, retry, and refund paths before broad launch. |

| Compliance mapping | 31 CFR 1020.220 requires a Customer Identification Program with risk-based identity verification, and 31 CFR 1010.230 requires written procedures to identify and verify beneficial owners of legal-entity customers. | Keep written verification procedures, beneficial-owner collection rules, onboarding decision logs, and exception handling. |

| Rollout rule | If approval uncertainty is high and gross margin is thin, start with one segment, keep a fallback payment path for declines, and expand only after measuring approvals, settlement timing, disputes, and margin impact by segment. | Do not launch to all buyers at once. |

- Buyer profile fit comes first.

Treat this as a go or no-go check. Your core buyers should resemble the segment the provider explicitly targets. One B2B offer is positioned for eligible small businesses, including sole proprietors, with machine-learning underwriting and options across price points. If your GMV is mostly checkout purchases from small operators, fit may be stronger. If it depends on larger entities with negotiated invoicing, fit may be weaker.

Before vendor calls, review recent buyers by legal form and order pattern. If you cannot separate demand from sole proprietors, small businesses, and larger legal entities, you cannot score fit reliably.

- Get risk ownership clear before you compare pricing.

The first question is who carries downside when approvals, disputes, or collections go sideways. TreviPay describes a model where sellers are reimbursed while it assumes credit risk and manages collections. Another provider highlights fraud and chargeback mitigation, but approvals can still be conditional in live B2B use. In the Amazon Business rollout, for example, buyers proceed only if approved.

Require clear contract language on credit-loss allocation, reimbursement timing, and dispute handling. If that language is vague, treat it as a commercial risk signal.

- Implementation depth is operational, not cosmetic.

A checkout embed is not enough. Your system needs durable event handling and finance-grade reconciliation. Stripe documents automatic webhook retries for undelivered events for up to three days and recommends duplicate-processing protection. Stripe also limits event retrieval for this workflow to the last 30 days.

Test failure paths before broad launch: delayed webhook, retry, and refund on the same transaction. If your ledger can double-post or finance cannot map transactions to payouts, pause rollout until that is fixed.

- Compliance has to map to your onboarding and payout flow.

KYC, KYB, and AML controls need to work in your actual process, not just exist in policy documents. For covered financial institutions, 31 CFR 1020.220 requires a Customer Identification Program with risk-based identity verification, and 31 CFR 1010.230 requires written procedures to identify and verify beneficial owners of legal-entity customers.

Use those requirements as a practical benchmark with providers and bank partners. Your operating evidence should include written verification procedures, beneficial-owner collection rules for legal entities, onboarding decision logs, and exception handling for suspicious-activity review.

- Set one hard rollout rule.

If approval uncertainty is high and gross margin is thin, do not launch to all buyers at once. Start with one segment, keep a fallback payment path for declines, and expand only after you can measure approvals, settlement timing, disputes, and margin impact by segment.

Quick comparison of current B2B BNPL options for services platforms#

Screen providers on buyer fit, payout timing, and risk ownership before pricing. Based on public materials, Affirm explicitly presents a point-of-sale offer for sole proprietors and eligible small businesses, TreviPay emphasizes B2B payments and A/R operations, and Shopify-native options require strict eligibility checks for service-led models.

Use this as a screening table, not a final ranking. The main launch blockers are still unclear eligibility, underwriting boundaries, and post-transaction risk ownership.

| Provider | Best for | Known strengths | Known unknowns | Key diligence questions | Go/no-go impact |

|---|---|---|---|---|---|

| Affirm BNPL for Business | Checkout flows serving sole proprietors and eligible small businesses | Explicit B2B point-of-sale offer for eligible small businesses and sole proprietors. States merchant payout in 1-3 business days. Publicly states buyer rates can range from 0%-36% APR based on credit, and says it helps reduce fraud and chargeback risk. | Public merchant pricing is not normalized. Exact underwriting criteria, approval boundaries by buyer type, and geography for your use case are not clear in the reviewed materials. Contract-level loss allocation is also not public here. | What percent of your buyers are sole proprietors or small businesses by legal entity? What decline and approval event outputs do you get? What happens operationally when a buyer is declined at checkout? | Go if your core buyer is small-business checkout and you keep a fallback payment path for declines. No-go if demand is mostly larger legal entities or negotiated invoice terms. |

| TreviPay | Platforms that need a B2B-focused payments and A/R orientation, especially with multi-country needs | Publicly positioned as a fully managed B2B payments platform and A/R automation provider. States BNPL network support in 32 countries for point-of-purchase invoicing and payments. | Public pricing, underwriting criteria, payout timing, and exact risk allocation are not provided in the reviewed pages. Coverage is stated at network level, but exact availability for your service model is still unknown. | In which of the 32 countries is your exact merchant and buyer flow supported? What seller reimbursement timing applies? What onboarding requirements apply by buyer entity type? | Go to diligence if cross-border B2B and receivables operations are your main pain point. No-go for launch until country coverage, settlement timing, and contract economics are confirmed in writing. |

| eCapital | Sellers that care most about getting paid upfront while giving buyers terms | Publicly markets B2B BNPL as letting buyers defer payment while the seller gets paid upfront and "risk-free." States buyer deferral examples of 30, 60, or 90 days and says it handles underwriting and repayment tracking. | Public fee structure, geography, exact eligibility, and the contract-level meaning of "risk-free" are not clear in the reviewed material. There is no normalized detail here on dispute handling or first-loss treatment. | What does "risk-free" mean in the merchant agreement? Who owns loss if a buyer defaults or disputes service delivery? Which buyer countries and entity types are supported? | Go to diligence if upfront cash timing is the main problem. No-go until legal and finance confirm what protections survive contract review. |

| Allianz Trade | Teams pressure-testing the risk model behind deferred B2B payment, especially non-payment exposure | Useful conceptual anchor. Allianz describes B2B BNPL as the digital equivalent of invoice for ecommerce and says non-payment risk means it should be backed by credit insurance. | Verify pricing, integration path, merchant onboarding, seller payout timing, and geography for this use case directly with the provider. | Are you evaluating an insurance layer, a financing product, or an embedded checkout option? What evidence is required for non-payment claims? Who handles underwriting and collections? | Go as a risk-model reference. No-go as a launch choice until you have product and contract detail, because the public material alone is not enough for implementation planning. |

| Shop Pay Installments | Shopify merchants with eligible stores in supported markets | Clear published availability for eligible stores in the United States, Canada, and the United Kingdom. Published order ranges: $35 to $30,000 USD, $35 to $30,000 CAD, and £50 to £30,000 GBP. | Major fit risk for services platforms: the platform says eligibility can be affected if your business is primarily a B2B service. Underwriting logic and broader B2B suitability are not detailed here. | Is your store already approved and active for Shop Pay Installments? How has the platform classified your business? Are your orders within supported country and amount ranges? | Go only if you are already on Shopify, clearly eligible, and your orders fit supported country and amount ranges. No-go if your store is primarily B2B services or eligibility is unconfirmed. |

| Klarna via Shopify Payments | Shopify merchants that want an additional local payment method inside Shopify Payments | Klarna can be added through Shopify Payments, and Klarna reviews business details before acceptance. That creates a real activation gate instead of assuming automatic availability. | Merchant pricing, exact geography by market, method mix, and underwriting rules are not normalized in the reviewed materials. Availability is constrained by approval and automated eligibility logic. | Has Klarna approved your business details? Which Klarna methods are enabled for your store and country? What happens to conversion when a method is not offered to a given buyer? | Go to pilot only if you are already centered on Shopify Payments and have written confirmation of activation. No-go if you need confirmed B2B availability before launch and do not yet have approval. |

Before vendor calls, map your last 90 days of orders by legal entity type, average ticket, country, and need for invoice-like terms. That cut will quickly narrow which providers are worth deeper diligence for your model.

A risk is treating "paid upfront" messaging as implementation-ready while finance still lacks contract and reconciliation detail. Do not move into build until you have the contract or addendum, a sample reconciliation export, and written confirmation of merchant eligibility for your buyer segment and geography.

Related: Accounts Receivable Management for Platforms: How to Collect from Buyers While Paying Sellers Fast.

Best fits by provider based on available evidence#

If you need a practical starting point, begin with the use case rather than the brand name. Based on public evidence, Affirm appears to fit eligible small-business point-of-sale flows, TreviPay is a strong B2B-focused diligence candidate, eCapital is relevant when upfront supplier cash timing is the priority, Allianz Trade is useful as a risk-model reference, and Shopify options can be practical for teams already operating there. Do not treat "paid upfront" or "protection" language as proof that your exact service flow is supported.

- Affirm

This is a clear public fit when buyers are eligible small businesses or sole proprietors at point of sale. Its B2B page states "instant decisioning" and merchant payout within 1-3 business days.

The gap is underwriting and eligibility boundaries for your exact segment. Confirm fit for your buyer mix and confirm what decision outcomes your product needs to handle.

- TreviPay

TreviPay is a strong diligence candidate if you want explicit B2B positioning. Publicly, it presents a fully managed B2B payments platform and A/R automation model, and the TreviPay Network claims BNPL-for-business support in 32 countries.

Keep it in diligence mode until implementation details are confirmed. A partnership page says it assumes credit risk, but that wording should not be treated as universal across every deployment.

- eCapital

eCapital is relevant when you need to offer terms while getting paid upfront. Its page describes B2B BNPL as buyer deferral with supplier payment upfront, including examples of 30, 60, or 90 days.

The key caution is the meaning of "risk-free" in contract terms. Validate fee mechanics, loss ownership, and reconciliation details before treating it as launch-ready.

- Allianz Trade

Allianz Trade is useful for framing deferred-payment risk coverage, not as a standalone launch spec. Its public positioning says Allianz Trade pay is for B2B e-commerce and includes trade credit insurance protection, with protection framed around insolvency, fraud attempts, and inability to pay.

Use it to sharpen diligence questions, then compare those requirements with checkout-oriented options and your own risk model. For related framing, see payment guarantees and buyer protection.

- Shopify options including Klarna and Shop Pay Installments

For teams already anchored there, Klarna and Shop Pay Installments are practical first checks. Klarna's page says buyers can pay later while merchants receive full payment upfront, and Shop Pay Installments lists $50 to $1000 (Standard) and $35 to $30,000 (Premium). The platform also states that Affirm collects customer payments so the merchant is not at risk if customers stop paying.

The open issue is fit for complex B2B service billing. Verify store eligibility and test a narrow service flow before treating native checkout BNPL as a full-platform solution.

How BNPL changes your margin math before and after launch#

Approve BNPL only when unit economics work, not when conversion looks better. For each financed order, test whether incremental gross profit covers BNPL fees, potential dispute or chargeback loss, and receivables timing effects within your payback window.

- Start with per-order contribution, not top-line lift.

Use one line of math per financed order: gross revenue - service delivery cost - BNPL merchant fees - estimated dispute/chargeback loss +/- cash-timing effect. Provider economics are merchant-fee driven, and those fees are often higher than card fees, so fee load is a core margin input. Faster payout can help cash timing, but it does not remove fee drag. Affirm's B2B page, for example, claims payout in 1-3 business days.

- Keep acquisition upside separate from financing cost.

Treat conversion lift as a testable hypothesis, not a default benefit. The January 2025 Richmond Fed brief cites higher conversion and ticket size, but it is explicitly consumer-focused, so B2B services impact is uncertain until your own cohort data confirms it. If you blend conversion gains into topline reporting, you can miss falling contribution margin per approved order.

- Cut cohorts by buyer type and ticket size.

Do not pool sole proprietors and larger business buyers into one average. Split by buyer type and ticket band so you can see differences in approval, disputes, support effort, and margin. Public ranges from Shop Pay Installments show why ticket size matters operationally: $50 to $999.99 for shorter interest-free installments and $35 to $30,000 for monthly installments.

- Use a hard rule before expansion.

If conversion lift does not offset BNPL cost, dispute exposure, and receivables effects inside your payback window, keep BNPL limited to narrow segments. Check BNPL versus non-BNPL cohorts regularly on approval rate, average ticket, contribution margin, payout timing, and first disputes or chargebacks. Also confirm dispute operations and loss handling responsibilities in contract terms. The CFPB's May 22, 2024 guidance on consumer dispute and refund protections makes that ownership question operationally important.

Before scaling, reconcile each financed order across provider settlement data, your order or invoice record, and proof of service delivery. If reconciliation is weak, both margin and DSO views can be unreliable. Keep early chargeback trendlines visible, because card-network programs use explicit thresholds, including Mastercard ECM at 100 to 299 and HECM at 300 or more.

For a step-by-step walkthrough, see Automating B2B Rebate Calculations and Disbursements for Platforms.

Before rollout, model BNPL fees against your current payment mix so conversion gains do not hide contribution-margin erosion; run a quick scenario in the payment fee comparison tool.

Who owns risk when things go wrong#

Risk ownership should be explicit before you launch BNPL for services. If the contract does not clearly assign default, fraud, and dispute losses, treat launch as incomplete.

| Risk area | Grounded detail | What to confirm |

|---|---|---|

| Repayment default | Affirm says it assumes repayment and fraud risk and pays merchants upfront and in full. The article notes recourse factoring exposure can return after a recourse window often described as 60 to 90 days in factoring examples. | Confirm written exclusions, reserve rights, clawback triggers, and whether upfront payment is non-recourse for your service model. |

| Fraud, fulfillment, and chargebacks | Shopify says it is not liable for chargebacks, and Shopify Protect reimbursement applies to specific protected fraud and unrecognized-charge disputes. Klarna frames risk coverage as conditional on merchant policy compliance for shipped goods or services. | Confirm what counts as valid fulfillment evidence for services. |

| Dispute handling and evidence deadlines | Affirm's dispute policy, last updated July 15, 2024, says merchants typically have 15 days to respond and targets outcomes within 15 calendar days of evidence collection. For Shop Pay Installments, Shopify says dispute notifications are sent through Affirm email to the store owner. | Test notification routing, response windows, and evidence assembly before launch. |

| Ambiguity in loss allocation | Allianz Trade describes indemnification for receivables due within 12 months, but that protection is conditional. The section says unclear assignment of principal loss, chargeback fees, refund responsibility, and evidence deadlines is a blocker. | Pressure-test approved buyer default, partial or unacceptable service claims, and late evidence submission in writing. |

- Repayment default

Start with the core failure case: the provider approved the buyer, you delivered, and the buyer does not repay. Your contract should state whether the provider keeps that loss or whether recourse can push it back to you later. Affirm says it assumes repayment and fraud risk and pays merchants upfront and in full, but you should still confirm any written exclusions, reserve rights, and clawback triggers for your service model. The practical question is whether "upfront" is truly non-recourse or works more like recourse factoring, where exposure can return after a recourse window (often described as 60 to 90 days in factoring examples).

- Fraud, fulfillment, and chargebacks

Keep these as separate risk buckets. Shopify states it is not liable for chargebacks on its platform, and Shopify Protect reimbursement applies to specific protected fraud and unrecognized-charge disputes. Klarna also frames risk coverage as conditional on merchant policy compliance for shipped goods or services. For services, confirm what counts as valid fulfillment evidence before signing, because fraud coverage may not protect you in delivery-quality or scope disputes.

- Dispute handling and evidence deadlines

"Buyer protection" language is not enough without a written workflow. Confirm who notifies you, your response window, acceptable evidence, and when funds can be reversed. Affirm's dispute policy, last updated July 15, 2024, says merchants typically have 15 days to respond and targets outcomes within 15 calendar days of evidence collection. If your team cannot assemble evidence in time, you may lose a dispute even when delivery was valid. For Shop Pay Installments, Shopify says dispute notifications are sent through Affirm email to the store owner, so that operational path should be tested before launch.

- Ambiguity is a commercial red flag

Treat unclear loss allocation as a pricing and launch risk, not a legal footnote. Pressure-test three scenarios in writing: approved buyer default after full delivery, partial or unacceptable service claims, and late evidence submission. If relevant, ask whether separate non-payment protection exists, such as trade credit insurance. Allianz Trade describes indemnification for receivables due within 12 months, but that protection is conditional. If principal loss, chargeback fees, refund responsibility, and evidence deadlines are not clearly assigned, pause and get marked-up terms before you ship.

Integration order that keeps finance and product aligned#

A practical integration order can improve control: capture the checkout decision, confirm payment status, post to the ledger, then release payouts.

- Checkout decision first

Treat the provider decision as an early checkpoint, not a buyer click. In Affirm's direct flow, approval returns a checkout_token, and the merchant uses that token to authorize and complete the order. In Klarna API-only flows through Adyen, webhooks are required to keep order systems updated on final payment status. That is a useful reminder that approval and final state are not always the same. Key differentiator: store approval artifacts and webhook outcomes as order records.

- Payment confirmation before ledger posting

Post ledger entries from confirmed payment events, not checkout UI state. BNPL flows can be asynchronous, and webhook-driven status handling is a core requirement. Key differentiator: book against a concrete money-movement artifact where available, such as a balance transaction, so finance can reconcile later.

- Connect payment events to MoR and Virtual Accounts logic

Event design should match your merchant-of-record responsibilities and your receivables model. Where virtual bank account numbers are used, incoming transfers can auto-reconcile to the right invoice. Key differentiator: use shared buyer and order identifiers across BNPL events, transfer events, and receivables records so traceability survives reconciliation.

- Release payouts last, with idempotency and settlement visibility

Keep payout release as a downstream control after accepted payment status and successful ledger posting. Charging and fund distribution can be separate steps, and payout timing can be managed by the platform in eligible connected-account setups. Key differentiator: enforce idempotency on payment and payout retries. Stripe idempotency keys can be up to 255 characters and may be pruned after at least 24 hours. Adyen settlement is batch-based after the sales day, defined as a 24-hour period (00:00 to 23:59). Route settlement batch and payout reconciliation status into finance ops views early so exceptions are visible before close.

Compliance and documentation you should require before go live#

Require a written, market-by-market control pack before launch, not a generic compliance deck. If no one can clearly show who owns beneficial-owner information collection, AML exception review, VAT country logic, and tax-form storage, pause rollout.

- Market control map

Start with jurisdiction, because AML/CFT controls are not one size fits all. FATF notes countries cannot all take identical measures, so your rollout sheet should list the market, legal entity, required customer due diligence and beneficial-owner steps, AML owner, and VAT treatment. In the U.S. MSB context, the AML program must be in writing and available to the Department of the Treasury on request. Key differentiator: where required, include beneficial-owner collection and verification for legal-entity customers, and capture the nature and purpose of the relationship so a risk profile can be developed.

- Tax and payout artifact rules

Define upfront which tax forms your model may need to collect and retain. Form W-9 provides a correct TIN to payers filing IRS information returns, and Form W-8 BEN is provided by a foreign beneficial owner to a withholding agent or payer when requested. If your flow can trigger information reporting, confirm whether reporting belongs on Form 1099-K instead of 1099-MISC or 1099-NEC for payment-card and certain third-party network transactions. Key differentiator: request sample outputs before go-live. Since January 1, 2024, the IRS e-file threshold is 10 aggregated information returns.

- Audit evidence pack

Your go-live file should include policy decisions, event logs, provider reference IDs, reconciliation exports, and a dated record of exception sign-offs. For EU flows, record the VAT place-of-taxation rule applied, since it determines which country's VAT rules apply. Key differentiator: test that evidence links across systems. Written policies alone are not enough if you cannot show they were followed.

Launch pilot design with hard go and no-go checkpoints#

Start narrow, then expand only if the pilot proves out under live conditions. Launch BNPL in one buyer segment and one service category first so you can isolate what is driving results.

| Pilot element | Grounded detail | What to watch |

|---|---|---|

| Pilot scope | Use a treatment-control structure with only a subset of buyers exposed first. Keep the pilot definition explicit in the launch brief: buyer segment, service category, and provider setup. | Whether the pilot is narrow enough to explain and unwind. |

| Weekly checkpoints | Monitor approval rate, take rate, payout timeliness, support load, and dispute or refund behavior every week. Stripe's evaluation set includes click-through, conversion, refunds, and disputes. | Fixed denominator definitions across weekly reporting. |

| Threshold examples | If you use Klarna, track dispute ratio on captured orders and watch the 1.5% threshold. For payout timing, compare actual funds receipt to the stated window; Shop Pay Installments states 1 to 3 business days after capture. | Dispute ratio and actual funds receipt. |

| Expand, hold, or roll back | Expand only when approval and take trends are stable and payouts and disputes stay within tolerance. Hold when conversion improves but support or reconciliation strain increases. Roll back when risk signals and metric drift appear together. | Pre-agreed thresholds and qualitative triggers before the first transaction. |

| Decline fallback | Stripe's published test kept at least one non-BNPL method eligible in-session. Use the same pattern so buyers can still complete payment when financing is unavailable. | Whether declined buyers still have a viable payment path. |

| Control cohort readout | Compare treatment versus control to separate incremental lift from payment-method shift. Stripe reported that more than two-thirds of BNPL volume was net-new in its test, but that evidence came from B2C companies, not B2B services. | BNPL and non-BNPL cohorts side by side before wider rollout. |

- Pilot one slice you can explain and unwind.

Use a treatment-control structure with only a subset of buyers exposed first, then increase exposure only if results hold. Stripe recommends this phased approach, but its published BNPL experiment was B2C, so use the method, not its outcome claims, as your benchmark. Keep the pilot definition explicit in your launch brief: buyer segment, service category, and provider setup.

- Track weekly checkpoints that tie demand to risk and operations.

Monitor approval rate, take rate, payout timeliness, support load, and dispute or refund behavior every week. Stripe's evaluation set includes click-through, conversion, refunds, and disputes, which helps prevent over-focusing on approvals alone. Keep denominator definitions fixed, and if you use Klarna, track dispute ratio on captured orders and watch the 1.5% threshold. For payout timing, compare actual funds receipt to the stated window; for example, Shop Pay Installments states 1 to 3 business days after capture.

- Set hard gates before go-live: expand, hold, or roll back.

Pre-agree thresholds and qualitative triggers before the first transaction so decisions are not rewritten mid-pilot. Expand only when approval and take trends are stable and payouts and disputes stay within tolerance. Hold when conversion improves but support or reconciliation strain increases. Roll back when risk signals and metric drift appear together.

- Design decline fallback paths up front.

A BNPL decline can still become a lost order if no alternative payment method is available. Stripe's published test kept at least one non-BNPL method eligible in-session. Use the same pattern so buyers can still complete payment when financing is unavailable. Dynamic payment-method logic can help keep financing conditional while preserving a viable alternative path.

- Read results against a non-BNPL control cohort.

Compare treatment versus control to separate incremental lift from payment-method shift. Stripe reported that more than two-thirds of BNPL volume in its test was net-new, but that evidence came from B2C companies, not B2B services. Your pilot readout should show BNPL and non-BNPL cohorts side by side before any wider rollout decision.

Red flags that usually mean do not expand yet#

Pause expansion when these appear. They usually point to eligibility visibility gaps, reconciliation control issues, or a timing problem that BNPL may not be the best tool to solve.

- Approval shifts without a clear explanation

Some approval variation is expected because eligibility checks apply and displayed plans can vary by purchase amount and customer profile. Treat it as a red flag when outcomes move across segments or order sizes and you do not have a documented eligibility, underwriting, or settings explanation. Before scaling, request the change log and compare it to your cohort cuts.

- Settlement data does not tie cleanly to accounts receivable

Do not expand if finance cannot reliably tie BNPL payouts to captured orders, A/R entries, and bank receipts. You are responsible for payout reconciliation, and settlement data is grouped into reporting categories, so this control has to work before volume grows. At month end, your team should be able to explain variances from exports and ledger evidence.

- Risk ownership needs proof in live dispute handling

Upfront merchant payout and shifted credit or fraud risk do not remove dispute and refund handling as an operational risk. CFPB communications and complaint signals indicate dispute and refund operations remain a real execution test. If early cases reveal confusion on dispute handling or refund timing, hold expansion.

- Real-time rails may fit the problem better than financing

If demand is healthy and the main pain is payment timing, compare BNPL with instant-rail options before expanding. FedNow is 24x7x365, and RTP is final and irrevocable, supports up to $10 million per transaction, and reported over 1,130 participants as of December 2025. That does not make rails automatically simpler, but it is enough reason to test whether faster bank payments solve the timing issue. For that comparison, see FedNow vs. RTP: What Real-Time Payment Rails Mean for Gig Platforms and Contractor Payouts.

The decision to make before implementation starts#

If you cannot show segment-level upside, do not implement BNPL yet. The pre-build decision is whether one defined use case can outperform financing cost, risk exposure, and control overhead.

- Back one segment, not the whole platform.

Start with a buyer group you can measure, then test whether conversion and order-value upside is likely to beat added payment cost and operational drag for that group. Shopify says Shop Pay Installments can improve conversion rates and average order value, but treat that as a hypothesis until your own cohort data confirms it. If your buyers are closer to eligible small businesses and sole proprietors, Affirm is directionally aligned with that point-of-sale focus.

Keep scope tight from day one. For a Shopify-based path, enforce documented limits first: eligible stores in the United States, Canada, and the United Kingdom, and in the U.S. an order range of $35 to $30,000 USD. Validate cash timing with real settlement files, not dashboard snapshots. Affirm says it pays merchants upfront within 1 to 3 business days. Do not average unlike buyer types together, or you can miss where economics work for one slice and fail for another.

- Choose a provider as an operating model decision.

Provider choice can change risk allocation, collections, disputes, reconciliation, and compliance ownership. TreviPay publicly describes assuming collection risk and guaranteeing upfront settlement, while Allianz Trade markets protection against insolvency, fraud attempts, and inability to pay. Those claims are not interchangeable and should not be treated as the same risk profile.

The decision turns on contract terms, reporting, and exception handling in your actual workflow. Federal Reserve guidance says third-party use does not remove your responsibility, and the OCC noted on June 6, 2023 that third-party relationships do not all carry the same risk or criticality. Before build, require redlined loss-allocation terms for default, fraud, and dispute scenarios, plus sample settlement exports and a tested dispute-evidence path. If "paid upfront" is clear in marketing but vague in contract language, treat that as a blocker.

- Approve only a gated pilot with named owners and auditable controls.

Move forward only when product, finance, and compliance each own a defined part of rollout. Product owns approval, decline, and fallback flows. Finance owns settlement-to-ledger reconciliation and exception review. Compliance owns onboarding controls required in each market, including U.S. beneficial-ownership controls where relevant. Under 31 CFR 1010.230, covered financial institutions must maintain written procedures to identify and verify beneficial owners of legal-entity customers at account opening.

Gate launch on evidence, not optimism. Your pre-launch pack should include signed risk-allocation terms, market and order-amount eligibility rules, onboarding screens, event logs, settlement exports, and one completed dispute test case for the buy now pay later flow. If any of that is manual, unclear, or not reproducible, hold rollout and keep the pilot limited until results justify expansion.

Related reading: Usage-Based Billing for B2B SaaS Platforms That Teams Can Operate.

If your pilot criteria point to a broader operating-model change, review how Gruv handles collection, compliance gates, and payout traceability in one flow via Merchant of Record.

Frequently Asked Questions

What is B2B BNPL for services platforms in practical terms?

B2B BNPL lets a business buyer receive the service now and pay over time while the supplier or platform can still be paid upfront. TreviPay also frames it as a type of trade credit, not a separate category. On services platforms, this can show up at checkout or point of sale rather than through invoice workflows.

Who takes credit risk in a B2B BNPL setup?

Risk depends on the provider terms and contract, so do not treat "paid upfront" as unconditional risk transfer. Klarna says it assumes credit and fraud risk, but its merchant protection policy adds fulfillment conditions. Shopify says merchants are not at risk if customers stop making Shop Pay Installments payments. Before launch, confirm written loss allocation for default, fraud, chargebacks, and partial-service disputes.

When is BNPL better than standard invoice terms for B2B services?

BNPL is usually a better fit when you need immediate decisioning at checkout and faster merchant cash availability. Affirm positions its B2B offer around instant decisions, and Stripe’s Affirm flow says the full order amount minus fees is made available upfront. Fit is weaker in flows that require recurring subscriptions, since Stripe’s Affirm path supports one-time line items only.

How should we evaluate BNPL impact on platform margin and cash timing?

Start at the transaction level: gross revenue, MDR, transaction fees, support costs, dispute and refund costs, and any A/R carry avoided. Affirm says settlements are reduced by MDR and transaction fees, and Shopify says Shop Pay Installments has higher fees than standard Shopify Payments processing, so faster cash does not automatically mean higher margin. For timing, use provider-stated settlement windows. Affirm says ACH funds are sent within 1-3 business days per transaction.

What should be true before we launch BNPL to all buyers?

Prove three things in pilot first: finance can reconcile settlements, product can handle approval and decline paths cleanly, and compliance can enforce market and product limits. Shopify states Shop Pay Installments is available only for eligible stores in the United States, Canada, and the United Kingdom. It also states U.S. order eligibility at $35 to $30,000 USD, so rollout logic has to enforce those boundaries.

How do we handle declines without hurting conversion?

Treat declines as a routing flow, not just a credit event. Affirm says merchants may not receive denial details for specific shoppers, and its decisions use multiple factors. Your checkout should immediately offer a fallback path rather than ending in a dead-end decline screen.

What is still unknown in most public provider materials and how should we verify it?

Public materials usually do not disclose exact underwriting thresholds, factor weighting, or account-specific pricing. Verify those gaps with operator evidence: a current pricing sheet or admin rates, redlined risk-allocation terms, sample settlement or reconciliation exports, available approval and decline reporting fields, and one tested partial-service dispute flow. That verification work determines whether the program is operationally usable, not just commercially attractive.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/manual/AssessingComplianceWithBSARegulatoryR...trusted

- bsaaml.ffiec.gov/manual/AssessingTheBSAAMLComplianceProgram/01trusted

- congress.gov/crs_external_products/IF/HTML/IF12734.web.htmltrusted

- consumerfinance.gov/about-us/newsroom/cfpb-takes-action-to-ensur...trusted

- consumerfinance.gov/compliance/compliance-resources/consumer-car...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- federalreserve.gov/frrs/guidance/interagency-guidance-on-third-...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: