Start here if you want to reduce default withholding without creating audit risk#

Use reduced withholding only when you can support a treaty claim, not just because a form was uploaded. This is for payer-side operators moving from default treatment to a defensible treaty-rate decision on Form W-8BEN that the U.S. withholding agent can explain later.

Set scope before form review#

Keep the scope narrow: income potentially inside your U.S. withholding process, and controls handled by the U.S. withholding agent. If the payment sits outside that lane, classify it first before you review the form. Start with basic routing:

- Is the payee an individual foreign beneficial owner, not an entity or U.S. person?

- Is the payment inside your withholding process and potentially treaty-eligible?

- Is the claim on Form W-8BEN, which is used for income not earned from personal services?

If the income is earned from personal services, route to Form 8233 instead of W-8BEN.

Require support, not just receipt#

A treaty benefit can mean an exemption or reduced withholding rate for certain income items, but it is never automatic. The payee is notifying the withholding agent of foreign status, and treaty-rate claims generally require a U.S. or foreign TIN, with limited exceptions such as certain marketable securities.

Operationally, the checkpoint is not "form received." It is "form received, matched to the payee, and documented enough to review the claim." At minimum, keep:

- W-8BEN on file

- Claimed country of residence

- TIN status

- Clear mapping from the form to the payment stream

Apply a conservative control rule#

If eligibility is not supportable, do not apply the treaty rate. That is the simplest way to reduce payer exposure and avoid rework later.

Document accuracy matters too. In a Taxpayer Advocate example, IRS matching compared 18 fields on Form 1042-S. Even small discrepancies could lead to rejection. Some claims were initially frozen for an average of 26 weeks. Treat document matching as a core control, not admin cleanup.

Set limits and escalation points up front#

This process gives you a defensible path, but it does not replace treaty-by-treaty verification. Exact rates, article conditions, income treatment, and full eligibility tests can vary by income tax treaty, and some treaties include limitation on benefits rules that can block claims.

Set one production rule at the start: if the treaty article or condition set is unclear, keep standard treatment and escalate before payout.

Why this matters for platforms paying global contractors and creators#

For platforms, the real risk is not slow form intake. It is a withholding decision the U.S. withholding agent cannot defend later. Speed matters in payout flows, but Form W-8BEN is not just an upload checkpoint. IRS instructions place it in Chapter 3 and Chapter 4 status establishment, so upload should never be treated as automatic approval.

Step 1 Keep payout speed separate from withholding approval#

Use a separate approval standard for withholding decisions. For a nonresident alien payee, the control point is simple: do you have a properly completed W-8BEN that is reviewable for a treaty claim?

Reduced withholding is conditional, not automatic. The claim must be supportable as treaty-country residence and beneficial ownership, and it generally requires a U.S. or foreign TIN, with limited exceptions. If those elements are missing or inconsistent, do not let payout speed drive the tax decision.

Step 2 Ignore generic payee advice when you operate at volume#

Single-filer instructions are not enough when you run a platform with many nonresident profiles. Your job is repeatable decision quality, not one-off form completion.

IRS guidance is clear on the failure mode: if ineligibility is known or suspected, the payor must not apply the treaty rate. In practice, your review should catch mismatches early, including treaty claims without usable residency support or a W-8BEN used when the income belongs on Form 8233 for personal services.

Step 3 Optimize against the two mistakes that matter#

Design your controls around the two outcomes that actually create risk:

- Unnecessary default withholding: applying default 30% withholding under section 1441 in cases where the payee could support tax treaty benefits

- Unsupported reduced withholding: granting treaty treatment without enough support

If the claim is supportable, apply the reduced treatment correctly. If the treaty position is unclear, keep default treatment and escalate before payout.

What to prepare before reviewing a single tax form#

Before you review treaty eligibility, build the file you would want to defend later. Starting without that packet increases the odds of outcomes you cannot support.

Step 1 Build the minimum evidence pack#

Start with the minimum file needed to rely on Form W-8BEN for an individual beneficial owner. That file should include the signed form, foreign tax identifying number (FTIN) status, support for claimed tax residency, and clear mapping to the exact payer account.

| File item | What to confirm | Note |

|---|---|---|

| Signed Form W-8BEN | Signed form is on file | For an individual beneficial owner |

| FTIN status | Confirm the FTIN position | Check whether line 6b states the individual is not legally required to obtain an FTIN |

| Claimed tax residency | Support for claimed tax residency is retained | Part of the minimum file |

| Exact payer account mapping | Clear mapping to the exact payer account | If account mapping is unclear, stop and fix that first |

| Line 10 representations | Review when treaty benefits are claimed | Do not treat treaty selection as automatic |

Check two fields explicitly. Confirm the FTIN position, including whether line 6b is used to state the individual is not legally required to obtain an FTIN in their residence jurisdiction. If treaty benefits are claimed, review required line 10 representations instead of treating treaty selection as automatic.

Use one hard checkpoint before moving on: can you prove this signed W-8BEN belongs to this exact payee account? If account mapping is unclear, stop and fix that first.

Step 2 Define the payment context before form review#

Classify the payment before reviewing the form. Document what is being paid and how your team is treating that payment for withholding analysis.

Do not ask the form reviewer to infer payment classification from vague labels. If payment facts are mixed or unclear, escalate for classification first and defer the treaty decision.

Step 3 Assign explicit owners before reliance#

Do not rely on any W-8 until ownership is clear. IRS requester guidance places responsibility on the withholding agent to obtain Forms W-8 before reliance, so your process should say who does what.

- Intake owner: collects the form, confirms account mapping, and flags missing or inconsistent fields

- Reviewer: assesses completeness, FTIN status, residency support, and treaty-claim details, including line 10 when relevant

- Approver: authorizes reduced withholding only when the claim is supportable

If roles are combined, document that choice so the control trail stays clear.

Step 4 Set retention and lifecycle expectations#

Retain the full decision record, not just the form. Keep the submitted W-8BEN, residency support used in review, account mapping evidence, payment-classification notes, and timestamped review and approval history.

Also align the process to lifecycle controls, including when to request a new Form W-8. The file should let another reviewer reconstruct why treaty treatment was accepted or declined without relying on memory.

Need the full breakdown? Read US-UK Tax Treaty Withholding Controls for Contractor Payment Platforms.

Step 1 classify the payee and route the correct form path#

Get the payee classification right before you do anything else. A complete form on the wrong payee type is not a real control and can create withholding and reporting errors downstream.

| Signal | Form or action | Note |

|---|---|---|

| Individual foreign beneficial owner | Form W-8BEN | Used for income not earned from personal services |

| Entity or organization | Form W-8BEN-E | Keep entity files off the individual path |

| Personal services income | Form 8233 | Use Form 8233 instead of W-8BEN |

| Account facts and submitted form type do not align | Stop and reroute | Hold the file for clarification |

For a U.S. withholding agent, IRS requester guidance is built around multiple W-8 variants and treats reliance as due diligence, not simple document collection. In practice, set a clear intake policy with distinct documentation paths based on payee classification, and do not rely on form collection alone.

Step 1A identify the payee before you inspect the form#

Start with payee identity, not the uploaded PDF. Use legal name, account type, contracting party, and payout setup to confirm whether you are paying a natural person or an organization.

This is a core checkpoint. IRS materials treat identifying the payee as part of intake, and beneficial-owner status remains a separate treaty-review criterion. If your team cannot explain who the beneficial owner is, pause before treaty review.

Step 1B stop and reroute on entity mismatch#

Build an intake gate for mismatches between account facts and submitted form type. If account profile, contracts, or invoicing point to entity status but the file is routed as an individual path, stop and reroute.

Do not keep the original route just to move payout faster. If onboarding records and tax documentation tell different stories about who is being paid, hold the file for clarification.

Step 1C link the routing decision to Form 1099 handling#

Tie payee routing to your reporting logic at intake. IRS examination guidance treats Form 1099 backup withholding and NRA withholding as separate topics, so this classification should determine which queue the payee enters.

That separation prevents cross-treatment errors later. For overlap context, see How to Handle a US-Sourced 1099 as a Non-Resident Alien.

Step 1D record who validated beneficial-owner status#

Document who made the classification call. At minimum, retain:

- reviewer name and date

- payee classification outcome

- evidence used to support that outcome

- final route outcome for the file

If this decision is undocumented, later reliance on the file is harder to defend.

Related: How to Fill Out Form W-8BEN for a Foreign Freelancer.

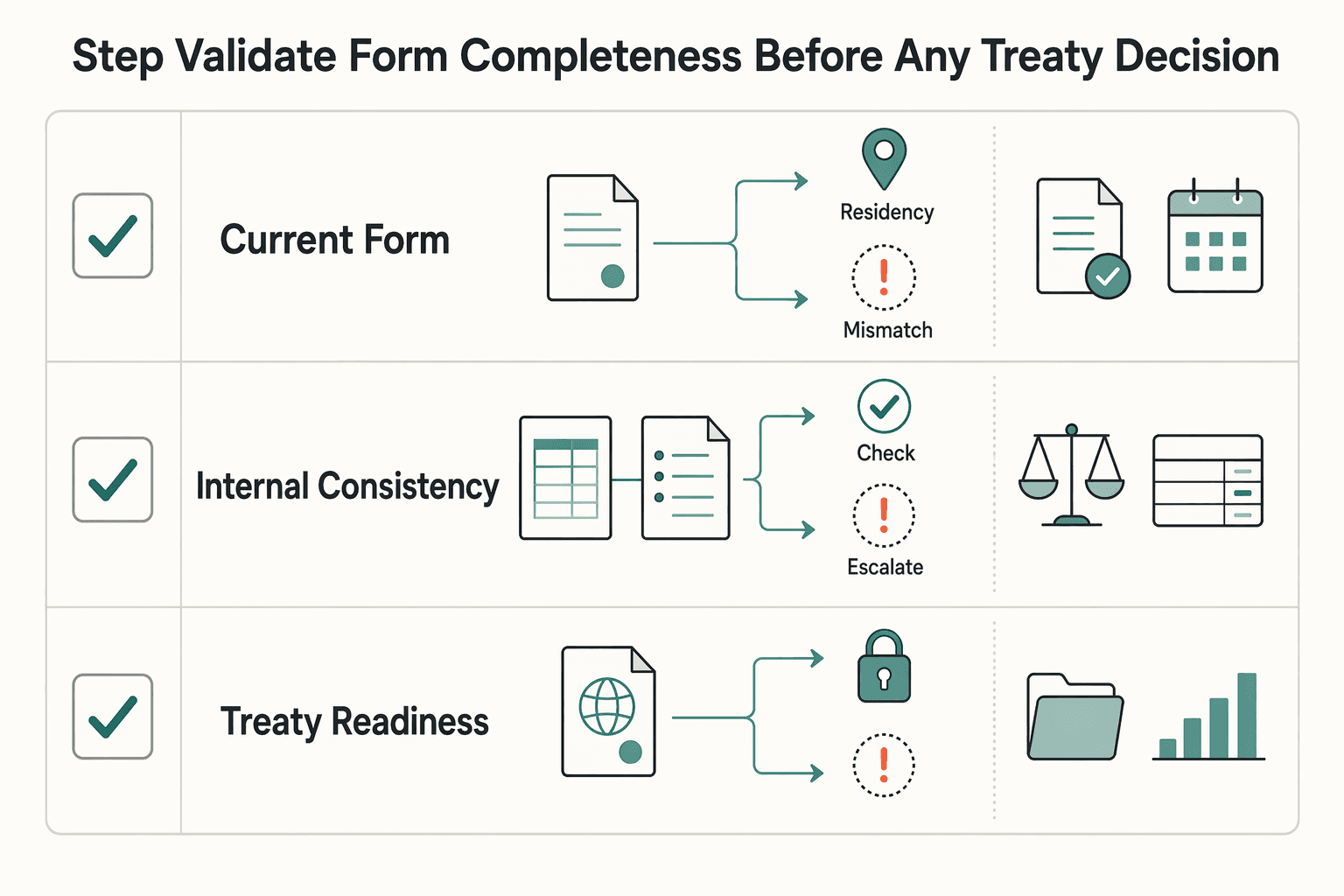

Step 2 validate form completeness before any treaty decision#

Before you analyze treaty eligibility, answer one simpler question first: is the certificate complete enough to review? Do not treat receipt, administrative completeness, and treaty eligibility as the same control.

Build a conservative completeness gate using the current Form W-8BEN package your team relies on and the requester instructions. Keep that gate current. The requester instructions excerpt here, Rev. June 2022, tells requesters to check developments at IRS.gov/UAC/AboutForm-W8 for latest updates.

Use a simple triage outcome for every file:

| Checkpoint | What to test | Common failure mode | Disposition |

|---|---|---|---|

| Current-form completeness | Confirm the certificate appears complete under the current form package and requester instructions (this excerpt does not enumerate specific W-8BEN fields) | Obvious missing or unusable entries | Hold for follow-up per policy |

| Internal consistency | Certificate data aligns with account and onboarding facts | Conflicting residency or account facts | Escalate |

| Treaty-readiness handoff | File is complete enough for treaty review | Team tries to decide treaty outcome at intake | Move to treaty review only after completeness pass |

Treat conflicts as escalation triggers, not cleanup tasks. If account facts and certificate details do not align, pause and route the file for follow-up or escalation instead of inferring what the payee meant.

Keep FATCA and account-context indicators as parallel risk signals, not treaty-decision shortcuts. The excerpts support FATCA as related context, but they do not provide a full W-8BEN approval rule or Model 1 IGA procedure for this step. Keep Form 8938 in its own process as well. It is attached to an annual return and filed by that return's due date, so it is not a substitute for withholding-certificate completeness review.

Also keep special withholding contexts visible in your checklist versioning. The requester instructions note updates, Rev. October 2021, tied to expanded section 1446(f) usage, including broker-related transfers of publicly traded partnership interests. Where that context applies, the cited rule is withholding of 10% of amount realized unless an exception applies.

Related reading: Withholding Tax Rate Lookup for Treaty Decisions Across 100+ Country Pairs.

Step 3 decide whether treaty benefits are supportable#

Once the form clears completeness, decide whether the claim is supportable before you set any reduced rate. If the treaty article, income type, or eligibility conditions are unclear, apply default withholding and escalate instead of guessing.

Check the claim in a fixed order#

Review each claim in the same order:

- Treaty country shown on Form W-8BEN

- Cited income tax treaty article or paragraph

- Actual income type being paid

- Stated conditions for the claim, including beneficial-owner status and TIN support

Do not jump straight to a rate table. A claim can look plausible and still fail basic routing. If country signals conflict across the form, permanent residence address, or onboarding facts, stop and escalate. If the payor knows or has reason to know a claim is invalid, the treaty rate must not be applied.

For treaty-rate claims, reduced withholding generally requires a U.S. or foreign TIN, with limited exceptions. If the file has a treaty claim but no usable TIN and no documented exception path, treat it as not supportable yet.

Separate supportability from rate confirmation#

At this stage, confirm that the claim path is coherent and documented. Do not treat that as final confirmation of the exact reduced percentage.

You can approve the path for further review when it points to a real treaty country, a specific article or paragraph, a matching income type, and relevant stated conditions. Exact country-by-income rates and full substantive eligibility still require treaty-specific verification.

Also check form routing. For income earned from personal services, the payee uses Form 8233 rather than Form W-8BEN. If the payout appears to be personal-services income, treat that as a form-path issue first.

Escalate cases that create payer risk#

Use a strict rule: if a reviewer cannot clearly explain why country, article, income type, and conditions fit together, do not move to reduced withholding.

| Scenario | Evidence required | Decision owner | Default action | Escalation path |

|---|---|---|---|---|

| Claim is coherent on its face | Form W-8BEN, treaty country, article or paragraph, income-type mapping, TIN, reviewer note | Tax reviewer | Hold reduced-rate setup until exact rate is verified | Approver confirms treaty-specific rate before release |

| Treaty article or paragraph missing or unclear | Form plus payee explanation only | Tax reviewer | Apply default withholding | Escalate to specialist review |

| Residency facts conflict | Form country conflicts with address, onboarding facts, or prior tax profile | Compliance or tax reviewer | Do not apply treaty rate | Return for correction or escalate |

| Special-topic flag appears | Facts suggest section 1446(f), section 6050Y reporting, or personal-services classification risk | Specialist owner | Default withhold or hold payout pending review | Specialist review before any reduced-rate decision |

Keep conflicting residency signals and section 1446(f) or section 6050Y edge cases as automatic escalation triggers.

Document why you said yes or no#

Write a short reviewer note that ties together country, article or paragraph, income-type mapping, TIN check, and final disposition. If denied or escalated, state the exact reason.

This protects downstream withholding and reporting quality. Historical refund-processing reviews found that even small discrepancies could trigger rejection, and one IRS matching program compared 18 fields on Form 1042-S. If you cannot show why the claim fits, do not support reduced withholding.

Step 4 apply the withholding decision in your payout operations#

Once review is complete, convert it into one payout action and keep that treatment fixed for execution unless a new tax review is completed. That prevents retries, manual edits, or overrides from changing withholding after the fact.

Map the review outcome to one payout action#

Your U.S. withholding agent decision should produce a single execution state per payout, or per payable line.

| Review outcome | Payout behavior | Verification checkpoint |

|---|---|---|

| Treaty claim approved | Apply the approved reduced withholding treatment tied to the reviewed Form W-8BEN | Confirm the payout record points to the exact form record and reviewer decision used for approval |

| Treaty claim not supportable | Apply default withholding treatment | Confirm the record shows why reduced treatment was not supported |

| Escalated or unresolved | Hold payout or hold reduced-rate release until review finishes | Confirm reduced treatment cannot be released without documented approval |

A common failure mode is system logic applying maximum automatic withholding after an invalid or mismatched W-8. A manual payout fix can then follow without a matching tax-decision update. If withholding changes without a clear decision trail, treat it as a control failure and re-review.

Keep retries idempotent#

Use the withholding decision as an immutable execution input. Retries should reuse the same decision reference and documentation unless tax facts change. If tax facts change, stop and request a new review. IRS requester guidance includes when to request a new Form W-8, so changed facts should not be handled as routine ops edits.

Store decision evidence with transaction references#

Attach decision artifacts directly to the payout or settlement record so finance can reconcile withholding outcomes to payee documentation. Keep at least:

- Payee ID and transaction reference

- Form type and stored form record, for example,

Form W-8BEN - Decision date and reviewer, plus approver if your control model requires it

- Applied treatment, either approved reduced treatment or default withholding

- Reason code for denial, hold, or escalation

- Link to the supporting reviewer note and stored form record

Cross-check reporting routing early#

Before volume builds, verify that form classification, withholding outcome, and reporting queue are aligned, including any section 6050Y-related routing your team uses. If a record documented under Form W-8BEN is routed into a conflicting reporting workflow, stop and fix routing before year-end cleanup.

Step 5 handle exceptions without breaking compliance or payout SLAs#

Exception handling should stay simple: one rule per bucket and one primary action per bucket. That keeps compliance decisions consistent and prevents payout overrides from quietly changing withholding treatment.

Bucket exceptions before payout#

| Exception bucket | What to verify first | Primary action | Practical note |

|---|---|---|---|

Missing Form W-8BEN | No current form record is linked to the payee or payout | Hold | Do not release reduced treatment without a stored form record tied to the payee ID |

Changed or no longer reliable tax residency facts | Profile country, address, or other residency evidence conflicts with the form on file | Request correction | Treat this as a change-in-circumstances trigger and run a fresh review |

Incomplete foreign tax identifying number (FTIN) | FTIN is missing and line 6b is not marked | Request correction | A blank FTIN is not the same as a valid line 6b "FTIN not legally required" statement |

| Conflicting beneficial-owner data | Beneficial-owner details conflict across submitted records | Escalate to specialist review | Do not let frontline ops resolve ownership conflicts with ad hoc edits |

Use default-withhold where the applicable rule defaults to withholding if no exception is validated. For specialist areas such as section 1446(f), route early, because some cases require withholding unless an exception applies.

Separate future treatment from prior payouts#

When late corrections arrive, complete review and link the updated form before applying updated treatment to upcoming payouts. For prior payouts, use tax/legal escalation and documented remediation procedures rather than ad hoc adjustments.

Operationally, keep two timing lanes separate:

When to providedocumentation to the withholding agent for upcoming payoutsChange in circumstancesevents that require a fresh review before continuing reduced treatment

Track repeat patterns to reduce exception volume#

Log each exception with at least the bucket, payee type, corridor, and collection surface. Review those patterns regularly so you can fix intake and routing where exceptions repeat, instead of reprocessing the same defects every cycle.

Common failure modes and how to recover quickly#

When something breaks, the fastest recovery is usually the same: stop unsupported reduced treatment, fix the failed decision point, and escalate any case you cannot re-support from the file before the next payout.

Step 1 re-review complete forms that were treated as automatically treaty-eligible#

A complete Form W-8BEN may be required, but it does not prove treaty eligibility by itself. Reopen any logic that treated "signed form on file" as enough.

Re-check the line 10 treaty-benefit claim, residency details, and FTIN handling, including whether line 6b is properly used when an FTIN is not legally required. If treaty support is unclear, or you have reason to know the facts do not align, stop reduced treatment for future payouts and escalate.

Step 2 separate individual and entity routing before you release anything#

Mixing Form W-8BEN and Form W-8BEN-E is a control failure. Individuals and entities need to stay on their correct form paths, and reduced treatment should remain frozen until routing is corrected and approved.

Do not patch an entity case by editing an individual-form record in place. Confirm that the beneficial owner type and core account details match the form type before release.

Step 3 anchor disputed decisions on IRS instructions, not institution-specific shortcuts#

When guidance conflicts, use Internal Revenue Service (IRS) instructions and your documented internal policy as the controlling source. IRS requester guidance requires due diligence before relying on Forms W-8, including reason-to-know handling when facts are inconsistent.

For each disputed case, document which IRS instruction controlled the outcome and which internal rule applied. If the team cannot show that basis for reduced treatment, treat it as a process defect and correct policy routing before approving more cases.

Step 4 rebuild the evidence packet for any reduced rate you already applied#

A reduced rate without retained support is a high-risk failure. If you cannot show why the rate was applied, the decision is not defensible.

Rebuild a packet that includes the current form, payee and payout references, reviewer and approver record, residency and FTIN or line 6b support, and the treaty basis used in approval. Then have a second reviewer test it. If that reviewer cannot reach the same result from the packet, stop reduced treatment, escalate unresolved cases before further payouts, and revalidate form currency, including expiration checkpoints.

We covered this in detail in How Platforms Should Collect and Validate Form W-8BEN-E for Foreign Entities.

Keep the process audit-ready without overbuilding#

You do not need a large control stack to be audit-ready. Clear written procedures and traceable records usually matter more. Keep the control set small and explicit so a second reviewer can follow why the decision was made.

Step 1 document the minimum control set#

Use four artifacts as your internal baseline. Keep each one versioned, owned, and dated:

| Artifact | Tied to or shows | Record rule |

|---|---|---|

| Intake checklist | Payee classification, form type, receipt date, and account mapping | Keep it versioned, owned, and dated |

| Decision review checklist | Specific determination, key risk factors, and reviewer conclusion | Keep it versioned, owned, and dated |

| Exception matrix | What happens when facts are missing, conflicting, or changed | Keep it versioned, owned, and dated |

| Approval log | Each decision record | Keep it versioned, owned, and dated |

Use this validation test: pick one approved case and ask a different reviewer to trace it from intake to decision using only the file. If they cannot, the procedure is still too implicit.

Step 2 narrow PII but keep traceability#

Keep the approval log focused on traceability, not full document duplication. Record the payee identifier, form type, form received date, reviewer, approver, decision date, decision outcome, and the storage location for the signed source document.

Duplicating full identifier details or full form images across tools may increase exposure without improving decision quality. A practical baseline is one retained source document plus a log entry that points to it.

Step 3 test a sample of approved cases#

Run periodic control testing on a sample of approved cases. Do not test only rejects or exceptions.

For each sampled case, confirm that the assumptions were recorded, the approval matched the file at decision time, and the packet is still complete on re-review. If misses repeat, tighten the checklist or exception matrix before adding more manual approvers.

For a step-by-step walkthrough, see How to Build a Global Tax Withholding Engine: W-8 W-9 and Treaty Rate Automation.

Copy and paste checklist for finance and payments ops#

Use this as a release gate. If a checkpoint fails, do not apply a treaty rate. Hold the payout or apply default 30% withholding (for amounts subject to withholding) and escalate.

Step 1 classify the payee#

Confirm that the documentation path is correct before review starts: Form W-8BEN, Form W-8BEN-E, or Form W-9. If the payee profile and the submitted form do not align, stop and reroute before payout. Do not force personal-services income through this path. For personal-services income, the payee files Form 8233.

Step 2 validate minimum completeness#

Treat the file as unusable until core fields are complete. Confirm beneficial-owner certification, treaty-country residency fields, and the treaty-claim TIN requirement.

For treaty claims through Form W-8BEN or Form W-8BEN-E, confirm that a U.S. or foreign TIN is provided, with limited exceptions. If the withholding agent cannot associate the payment with valid documentation, return the file for correction.

Step 3 confirm the treaty decision packet#

A complete form alone is not enough to support reduced withholding. Confirm that the packet captures the claimed treaty basis and income type in your review record. If support is unclear, or you have reason to know the claim is not eligible, do not apply the treaty rate.

Step 4 confirm the execution record#

Confirm that the approved tax treatment was actually applied at payout. For internal controls, record the withholding action, link it to the payout reference, log exceptions, and assign follow-up ownership for open items.

As a final control, reopen one approved payout and verify that it still traces to the stored Form W-8 or Form W-9 documentation. If it does not, tighten the control flow before continuing.

If you want fewer incomplete submissions before review, start with the W-8 form generator and enforce your intake checklist before treaty analysis.

Final takeaway and next step#

Treat reduced withholding as a controlled approval decision, not a Form W-8BEN collection step. If the treaty position cannot be reviewed, tied to the payment facts, and documented, keep default treatment and escalate before payout release.

Step 1 Adopt the operating rule#

Set one rule this week: Form W-8BEN can be required, but it is not the decision by itself. The decision is whether the treaty claim is supportable for the specific payment, including review of treaty benefits as a separate item and Line 10 when claimed.

This is a withholding-agent control. Form W-8BEN is given to the withholding agent, and Chapter 3 withholding requirements include withholding-agent liability. Your process should show who reviewed the claim, what was reviewed, and why the applied rate was accepted.

A practical check: for any payout using reduced withholding, can you produce one packet with the form, treaty-claim details, payment type, and reviewer or approver? If not, you are still running a form-collection process, not a controlled withholding process.

Step 2 Implement the minimum controls this week#

Put these three controls in place now:

- Intake checklist - Confirm the Form W-8BEN is received, still valid, and attached to the correct payee record, with treaty-benefit claims visible for review.

- Treaty-review checkpoint - Require a checkpoint before release when reduced withholding is requested. Confirm treaty-country information, whether Line 10 is completed when claimed, and whether payment facts fit the claimed treaty position.

- Exception escalation path - Route unclear cases to a named owner before payout, including missing treaty details, expired documentation, or a change in circumstances.

The goal is a repeatable decision record: fewer unsupported treaty-rate decisions, fewer avoidable default-rate outcomes, and a clear rationale when finance or audit asks why a reduced rate was applied.

Step 3 Set the boundary and enforce it#

Use a firm boundary: if treaty interpretation is uncertain, pause, document, and escalate. Do not let payout timing pressure turn uncertainty into assumed approval.

Keep two checks active: one for Form W-8BEN expiration and change in circumstances, and the other for edge cases where treaty claims may not be accepted in the expected way, including some interest-payment contexts.

You do not need every treaty question answered in advance. You do need a controlled approval path, a documented exception path, and the discipline to stop release when the treaty basis is not clear enough to defend.

When you are ready to turn the control framework into day-to-day execution, use Gruv Payouts to run policy-gated payouts with clear status tracking and audit trails.

Frequently Asked Questions

Can Form W-8BEN reduce default withholding?

Yes, when the treaty claim is valid and the U.S. withholding agent accepts the documentation. The claim should be supported by residency and beneficial-owner certifications, and treaty-rate claims require a U.S. or foreign TIN.

What happens if no Form W-8BEN is on file at payout time?

Do not apply treaty treatment without usable documentation. Follow your normal withholding process and escalate instead of guessing.

Do payees send Form W-8BEN to the Internal Revenue Service (IRS)?

No. For reduced withholding, the form is provided to the payer, meaning the withholding agent. It is not filed directly with the IRS for that purpose.

How do we decide between Form W-8BEN and Form W-8BEN-E?

Use Form W-8BEN for an individual foreign beneficial owner and Form W-8BEN-E for an entity. If the payee profile indicates an organization, reroute to the entity form rather than forcing the individual path.

Is a complete form enough to grant reduced withholding?

No. A complete form is necessary, but it is not sufficient on its own. You still need to confirm treaty eligibility before applying a reduced rate.

What should we do when treaty-rate details are unclear?

Escalate and do not apply treaty treatment until support is confirmed. Forms W-8 are subject to due-diligence requirements, and if ineligibility is identified, the payor must not apply the treaty rate.

What should we verify before accepting a treaty claim on Form W-8BEN?

Confirm three minimum points: treaty-country residency certification, beneficial-owner certification, and a U.S. or foreign TIN for the treaty claim. If any of these are missing, the file is not ready for reduced withholding.

Are there cases where Form W-8BEN is the wrong document even for a foreign individual?

Yes. For income earned from personal services, the payee files Form 8233. Escalate treaty claims that require additional representations, including certain business-profits or gains contexts.

Which details are still unknown from high-level guidance?

High-level guidance does not provide exact treaty rates by country and income type. It also does not replace case-by-case treaty-eligibility review.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: