Quick Answer

Choose USDC or USDT as your first production rail, assign the other as fallback, and keep EURC limited to euro-linked pilots until corridor results are proven. Make the go/no-go decision on recipient acceptance, off-ramp availability, and whether each payout can be traced from internal payout ID to on-chain reference and ledger entry. If Europe is in scope, include a MiCA availability check on regulated exchange access before launch.

USDC vs USDT vs EURC for platform payouts in plain terms#

For platform payouts, start with a simple rule: treat USDC or USDT as your likely primary rail, and treat EURC as a narrower option that needs proof before broad rollout. Your job is not to pick the token that looks best on a market chart. It is to choose a payout rail your team can operate and validate across the markets you serve.

A stablecoin is a programmable digital currency, typically pegged 1:1 to fiat. For payout teams, that matters because the goal is to reduce value drift between approval and receipt, not chase speculative upside. Stablecoins are no longer just a trading instrument. Recent market reporting suggests they account for more than two-thirds of crypto transaction value, with use cases that include international payments, liquidity management, and protection against currency fluctuations. That makes the category relevant, but your decision should still rest on operating evidence, not hype.

| Asset | What current evidence supports | What you must verify before scale | Practical stance now |

|---|---|---|---|

| USDC | Part of the two stablecoins that currently dominate liquidity with USDT | Recipient acceptance, off-ramp availability, and your internal reconciliation path by corridor | Strong candidate for a primary payout rail |

| USDT | Also part of the dominant liquidity pair with USDC | Same corridor and reconciliation checks, plus market-specific availability checks where regulation may affect access | Strong candidate where reach and counterparties support it |

| EURC | This section does not provide enough evidence on liquidity, reserve reporting cadence, or payout reliability | Explicit pilot validation by corridor before broad rollout | Test narrowly, do not assume parity with the two dollar rails |

The main checkpoint is corridor reality. Before you enable any asset, verify that recipients can actually receive it in the wallets you support, convert or spend it where needed, and that the payout lands correctly in your finance records. In practice, we tie each payout record to the internal payout ID, recipient identifier, asset, network, and on-chain transaction reference so Ops and Finance can review the same event.

A common early mistake is treating "stablecoin" as if it means "interchangeable." USDC and USDT have stronger operating evidence today because they sit inside the dominant liquidity pool. EURC may still be useful in some programs, but nothing here supports a broad rollout yet. It supports a controlled test.

One market-specific caution is worth surfacing now. One source says MiCA has reduced USDT availability on regulated European exchanges. Treat that as a validation task, not a blanket conclusion. If Europe matters to your program, make regulated exchange and off-ramp access part of your approval checklist before launch.

So the rest of the decision is straightforward: pick one primary rail, define one fallback rule, and launch only when Finance, Ops, and Engineering can audit the same payout trail end to end.

If you want a deeper dive, read Stablecoin Payouts for Platforms: How to Disburse USDC to Contractors Globally.

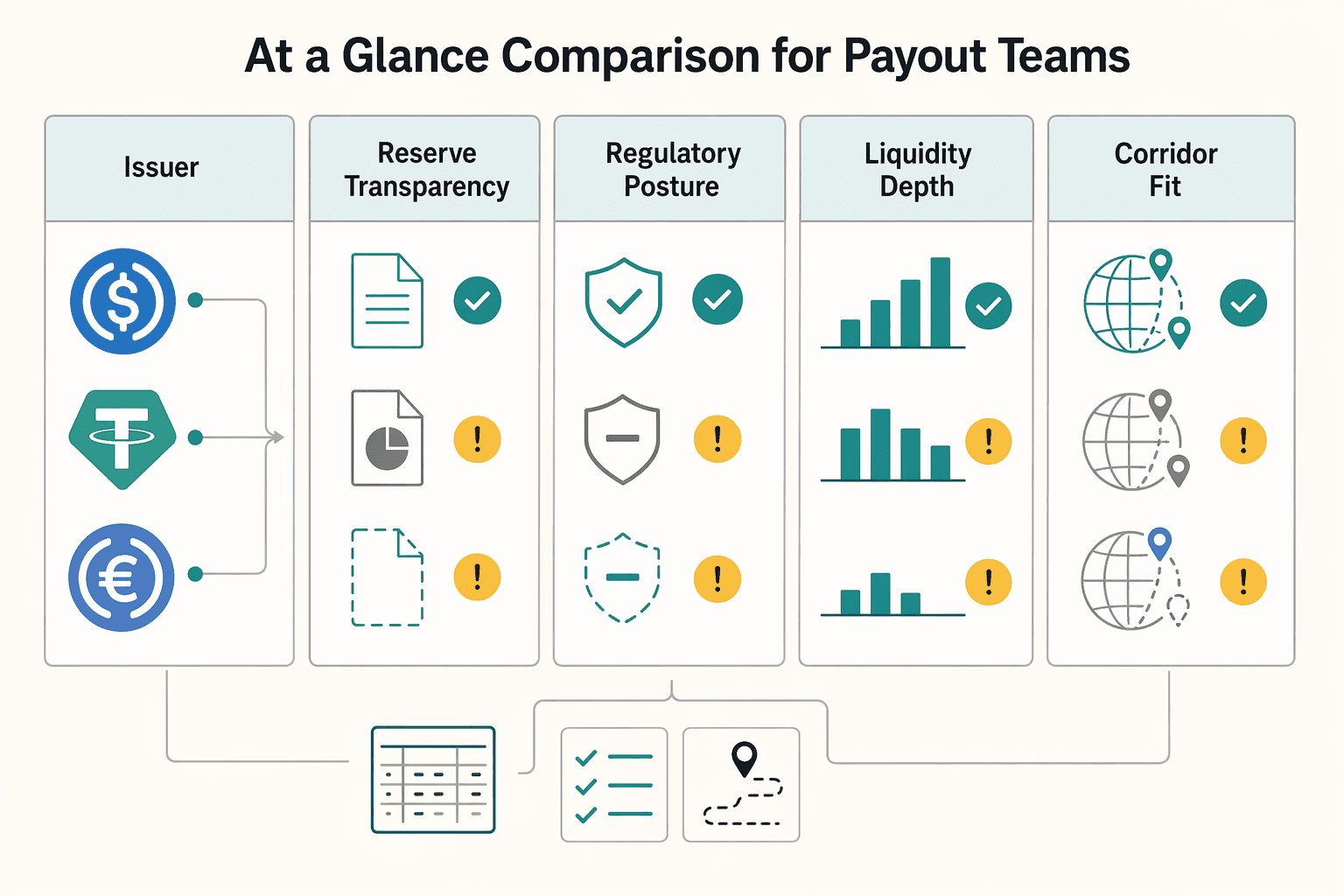

At a glance comparison for payout teams#

Use this as an execution table, not a brand-ranking exercise. Evaluate USDC and USDT for near-term rollout, and keep EURC behind pilot validation until corridor evidence is clear. Selection should follow your architecture, compliance requirements, and target corridors, not coin support alone.

| Checkpoint | USDC | USDT | EURC | Decision owner | Confidence now |

|---|---|---|---|---|---|

| Issuer | Circle | Tether Limited | Circle | Finance | Medium |

| Reserve transparency cadence | Verify current issuer attestation and reserve disclosures before approval; cadence is not established in this section | Verify current issuer disclosures directly; cadence is not established in this section | Follow the same issuer-document review path as USDC, but do not treat that alone as scale-ready evidence | Finance | Low |

| Regulatory posture | Approve by market and program, based on your compliance setup | Same, with market-by-market checks on venue and partner access | Same, with tighter launch gating due to thinner operating evidence | Finance | Medium |

| Liquidity depth | Primary-rail candidate only after venue and off-ramp checks by corridor | Same | Do not assume parity with dollar rails; require pilot validation | Payments Ops | USDC medium, USDT medium, EURC low |

| Corridor fit | Confirm recipient wallet support, convertibility, and routing in each target market | Same | Use where euro-denominated need is real and corridor results are clean | Payments Ops | USDC medium, USDT medium, EURC low |

| Treasury exposure | Review reserve-asset model, redemption assumptions, and issuer-risk notes in your approval file | Review the same issues through Tether Limited documentation | Review the same issues through Circle documentation | Finance | Low to medium |

| Operational risk | Prove idempotent payout creation, webhook reliability, and ledger mapping | Same | Same, plus tighter exception monitoring during pilots | Engineering | High control need; low EURC operating confidence |

Your coin choice and your delivery stack are related, but not identical. The source comparison lists Circle with USDC and EURC, multi-chain, bring-your-own compliance, and no fiat delivery; it also lists Coinbase with USDC/custom stablecoins on Base and Ethereum, partial compliance, and no fiat delivery. Token support can look fine on paper while compliance and fiat exit still sit with your team.

Keep ownership explicit: Finance owns issuer documentation and approval artifacts, Payments Ops owns corridor performance and fallback routing, and Engineering owns replay safety and webhook idempotency. The ECB's warning on rapid stablecoin growth as a financial-stability concern is a useful reminder to document venue, off-ramp, and compliance path by market instead of assuming broad access.

Use the table to assign owners, then close the evidence gaps before launch. Keep USDC and USDT in full evaluation. Keep EURC pilot-only until your own corridor data supports broader rollout.

For a step-by-step walkthrough, see How Platform Teams Enable USDC Freelancer Payouts Without Losing Control.

How to choose your primary rail on day one#

Pick one primary dollar rail, either USDC or USDT, set the other as fallback, and keep EURC in a narrow euro-linked pilot until corridor performance is proven in your own data.

Most stablecoin payment volume is still USD-denominated, mainly in USDC and USDT, so most day-one production rollouts start with those two. Make the decision by architecture, compliance requirements, and target corridors, not by coin support alone. Because cross-border performance varies by corridor, your primary rail can differ by audience segment and market.

| Operating condition | Primary rail | Fallback rail | Verify before launch |

|---|---|---|---|

| Compliance and approval workflow is the gating step | USDC or USDT (the one your program can approve cleanly first) | The other dollar rail | Approval artifacts, corridor list, recipient wallet support, treasury/redemption notes |

| Recipient-side liquidity and cash-out success is the gating step | USDC or USDT (the one with better corridor outcomes) | The other dollar rail | Venue/off-ramp acceptance by corridor, failed-withdrawal handling, route-change ledger mapping |

| Liabilities are meaningfully euro-linked | EURC (pilot only) | USDC or USDT | Corridor-specific on/off-ramp reliability, return handling, reconciliation quality, explicit approval scope |

When we roll out a multi-rail setup, we keep the routing policy explicit: one primary rail, one fallback rail, and written triggers approved by Finance and Risk. Only use the fallback when the primary is not accepted, corridor outcomes are materially better on fallback, or Finance has restricted the primary for that program. Avoid ad hoc rail selection during operations. It creates reconciliation noise and inconsistent payout outcomes.

Tie the final choice to who you actually pay. Contractor, creator, and marketplace seller payouts can have different corridor priorities, so run controlled tests by segment and keep the evidence pack: approval date, issuer artifacts, recipient acceptance, exceptions, and reconciliation samples.

You might also find this useful: USDC Payouts for Platforms: How to Offer Stablecoin Settlement to Contractors.

For a quick next step, try the free invoice generator.

Where EURC helps and where you still need proof#

Use EURC when euro-linked liabilities are operationally meaningful and you want payout currency to better match treasury exposure. Do not treat it as a default replacement for USDC or USDT without corridor-level proof.

| Situation | Where EURC helps | What you still need to prove |

|---|---|---|

| Euro-heavy contractor or seller obligations | Closer currency alignment between liabilities and payouts | Recipient wallet or venue acceptance in each named corridor |

| Treasury wants less USD mismatch on euro programs | A cleaner operating model for euro-denominated obligations | Return handling, reversals, and ledger mapping back to the original payout |

| Broad multi-market payout rollout | Limited support in this pack for EURC as a default rail | Consistent completion and reconciliation quality before expansion |

The gap in evidence is real. This material gives broader comparison coverage for USDC and USDT, including MoonPay framing them as leading stablecoins, while EURC appears in a narrower USDC/EURC settlement reference in an RWA context. That is not corridor-level payout proof, so treat EURC assumptions as unvalidated until your own pilot confirms them.

Before you widen scope, run a corridor-specific pilot. Cross-border outcomes vary by corridor. Require proof of consistent payout completion across repeated test batches, clean return handling when recipients cannot receive EURC, and reconciliation quality from payout request through ledger close. Include failed and returned cases in the test, not just successful sends. If those checks pass in a euro-heavy lane, keep EURC there. If not, route back to your approved USD rail and keep EURC in the treasury-alignment bucket.

This pairs well with our guide on Choosing SWIFT or Local Bank Transfers for Cross-Border Platform Payouts.

Compliance and treasury checks before you enable any rail#

Do not enable any stablecoin rail until your compliance gates, tax handling, and treasury approvals are documented and auditable.

Set gates before outbound money moves#

Define KYC, KYB, and AML controls by market and by payout program, then tie them to a binary release state: approved for outbound stablecoin payouts or not. Passing onboarding for platform access is not enough. If you have not explicitly cleared an account for crypto disbursement, block payout creation and queue remediation before funds move.

Decide tax paperwork before scale#

Design tax operations with the rail, not after launch. Decide upfront which payee types require W-8, W-9, and 1099 workflows, where records are stored, and what blocks payout when records are missing or expired.

| Tax item | Define before launch | Blocking rule |

|---|---|---|

| W-8 | Decide which payee types require it | Store records and block payout when records are missing or expired |

| W-9 | Decide which payee types require it | Store records and block payout when records are missing or expired |

| 1099 | Decide which payee types require the workflow | Store records and block payout when records are missing or expired |

Include Form 8938 in your finance approval memo and annual review:

| Item | Grounded rule to apply |

|---|---|

| Certain U.S. taxpayers | If specified foreign financial assets exceed $50,000, report on Form 8938 with the annual income tax return (with higher thresholds for joint filers and certain U.S. taxpayers abroad). |

| No income tax return required | Form 8938 is not required. |

| Certain specified domestic entities (tax years after Dec 31, 2015) | File Form 8938 if value is over $50,000 on the last day of the tax year or over $75,000 at any time during the tax year. |

| FATCA context | Treat Form 8938 controls as part of your FATCA-related tax reporting discipline. |

Log issuer review by asset#

Keep a separate treasury approval log for each asset you allow: USDC, USDT, and EURC. For each asset, record who approved it, the review date, reserve-transparency and redemption assumptions used, and the fallback rail if conditions change.

If you cannot produce the approval artifact, date, and approver for a given asset, treat that rail as not approved for production payouts. Related: Crypto Payouts for Contractors: USDC vs. USDT (What Platforms Must Know).

Integration sequence across product, engineering, and finance#

Set the implementation order before you launch: define routing policy, implement integration and async event states, test retries, then run limited live batches. Out of order, you only prove that USDC, USDT, or EURC can move, not that your team can explain each movement afterward.

This sequence matters because stablecoins operate 24/7 and can have near-instant finality, while internal records may update later. Product, Engineering, and Finance need to work from one shared source of truth before go-live, especially as stablecoins now account for more than two-thirds of recent crypto transaction value and are widely used for international payments.

| Stage | What must be decided | Owner check | Evidence to retain |

|---|---|---|---|

| Routing policy | Which asset is primary, which is fallback, and when a payout can switch rails | Finance and Risk approve lane rules before code freeze | Signed routing note by market and payout program |

| Integration states | How your product records in-flight and final outcomes from provider responses and later events | Engineering confirms the internal status model is documented | State definitions used in API handling, webhook handling, and exports |

| Retry testing | How duplicate requests, delayed events, and replays are handled without duplicate payouts or duplicate postings | Engineering and Ops review test cases together | Test results showing one business outcome per payout attempt |

| Limited live batches | Which markets, payee types, and daily volume caps are allowed first | Finance and Ops approve the first production scope | Batch log, exception review, and release approval |

Make every payout traceable end to end#

Every payout should be traceable from request to provider reference to ledger posting. That chain is the minimum you need when a payee reports missing funds, Finance finds an export mismatch, or Support needs to confirm whether funds actually left your control.

Use a simple pilot checkpoint: trace one successful payout and one failed payout without stitching together spreadsheets. If you cannot tie one provider reference cleanly to one ledger entry, you are not ready to scale.

Design for delayed truth, not perfect timing#

Assume request time, settlement time, provider confirmation time, and export time will not line up. Stablecoins move continuously, so delayed asynchronous updates are normal.

Test duplicated outbound requests and delayed status events before go-live. Aim for one payout, one financial outcome, with later events updating status cleanly without manual patching.

Do not launch without an evidence pack#

Require a go-live pack signed by Finance, Ops, and Engineering:

| Artifact | What it must cover | If missing |

|---|---|---|

| Failed payout taxonomy | Reasons Support and Finance will actually use | Keep launch scope narrow |

| Retry behavior notes | Duplicate requests and replayed async events | Keep launch scope narrow |

| Reconciliation sample | Request, provider reference, and ledger posting alignment from a real pilot batch | Keep launch scope narrow |

| Market-specific compliance approval | The exact launch scope | Keep launch scope narrow |

If any artifact is missing, keep launch scope narrow. Rail comparison only matters in production when exception handling is as clear as payout execution. For the full breakdown, read How CFOs Evaluate a Global Payout Platform.

Failure modes that cause expensive surprises#

Once your pilot is traceable end to end, the highest-cost failures usually come from control gaps, not transfer speed. The four usual offenders are hidden operating cost, weak governance records, ambiguous routing, and compliance ownership gaps.

| Failure mode | What teams underestimate | What the cost looks like in practice | What to verify before scale |

|---|---|---|---|

| Hidden cost trap | Low network fees are treated as total cost | Failed withdrawals, weak corridor completion, and manual exception handling erase fee savings | Track completion and exception rates by corridor, then add support and finance handling time |

| Governance trap | USDC/USDT selection is approved without written issuer/reserve assumptions | Audit and finance review slows when assumptions cannot be shown | Keep a signed asset memo with issuer/reserve assumptions and approval date |

| Product trap | Multiple rails are enabled without deterministic routing rules | One payout request can produce ambiguous attempts and support escalations | Prove one payout request maps to one authoritative business outcome, including retries and delayed events |

| Compliance trap | Technical integration is treated as launch-ready control coverage | Payouts get paused while reporting logic is rebuilt after go-live | Assign owners and evidence requirements for FinCEN and market-specific reporting before broad rollout |

Deterministic routing is not optional#

If the same payout can switch rails without fixed triggers, you create ambiguity fast. Support cannot clearly answer whether funds were attempted once, retried, or rerouted, and Finance loses a single authoritative trail. Lock fallback triggers in policy, and make them visible in logs before scale.

Compliance work that blocks scale#

For FinCEN reporting workflows, assign ownership before launch. FBAR is FinCEN Form 114, and maximum account value handling has specific mechanics: record values in U.S. dollars, round up to the next whole dollar, value each account separately, convert foreign currency using the Treasury Financial Management Service rate, and enter 0 if the calculated maximum value is negative.

| FBAR item | Grounded instruction |

|---|---|

| Form | FBAR is FinCEN Form 114 |

| Currency | Record values in U.S. dollars |

| Rounding | Round up to the next whole dollar |

| Account treatment | Value each account separately |

| FX conversion | Convert foreign currency using the Treasury Financial Management Service rate |

| Negative value | Enter 0 if the calculated maximum value is negative |

If your launch plan says compliance review will happen later, keep scope narrow. The reliable path is straightforward: document asset assumptions, lock routing logic, and assign reporting ownership before expanding volume.

Related reading: How to Build a Global Accounts Payable Strategy for a Multi-Country Platform.

Your 30-day decision checklist and pilot scorecard#

Use this as a 30-day gate: if you cannot name a primary rail, fallback rail, and control owner by the end of week 1, keep the pilot narrow.

| Week | Decision | Evidence to verify | Hold or reroute trigger |

|---|---|---|---|

| 1 | Pick USDC or USDT as primary, define fallback, and document where EURC is allowed by corridor | Signed asset memo, fixed routing rules, and corridor-level EURC scope | Verbal-only approval, or EURC enabled without corridor-specific rules |

| 2 | Run controlled payout batches | Completion outcomes, exception volume, and reconciliation lag by corridor from payout logs, provider references, and ledger entries | Low fees look good, but exceptions or reconciliation delays create manual cleanup |

| 3 | Review policy adherence | KYC/KYB/AML checks applied as designed, plus ownership for W-8/W-9 and 1099 handling where applicable | Compliance still "in progress," or tax-document ownership is unclear |

| 4 | Decide to scale, hold, or reroute | Finance, Ops, and Engineering review the full pilot evidence and confirm expansion decision | Mixed results, unresolved routing ambiguity, or low confidence in EURC corridors |

Week 1 usually decides the real operating model: which rail you trust first and exactly when fallback is allowed. If EURC is in scope, keep it limited to explicitly approved corridors until completion and reconciliation quality are consistently acceptable.

By week 4, make the call from evidence, not momentum. Policy conditions are still shifting: TRM reports 2025 developments across 30 jurisdictions, with over 70% progressing stablecoin regulation. Wharton's March 2023 calibrated model found higher run risk for USDT than USDC, while still indicating significant run risk for USDC. Treat that as a risk signal, not a universal verdict, and keep your approval memo, monitoring cadence, and rollback path current.

Pick the rail that matches your operating risk, not hype#

Choose one primary rail plus one fallback, and do not scale until Finance, Ops, and Engineering can show clean checkpoint evidence. For most teams, that means USDC for governance and approval comfort or USDT for reach and liquidity. Treat EURC as a narrow, corridor-tested option rather than a broad default.

| Rail | What it is strongest for | What should make you cautious | What to verify before expansion | Practical role |

|---|---|---|---|---|

| USDC | Transparency and compliance-oriented positioning | Treasury and issuer-risk assumptions still need active review | Check the latest issuer attestation and reserve materials, confirm supported corridors and provider references, and match payout logs to ledger entries from pilot batches | Strong primary rail when internal approvals and auditability matter most |

| USDT | Deep liquidity across global exchanges, supported by early market presence | Governance and issuer-risk questions need explicit sign-off | Require a written issuer-assumption memo, corridor-specific withdrawal proof, and reconciliation samples from controlled payouts | Strong primary or fallback rail when liquidity in tougher corridors is the blocker |

| EURC | Targeted treasury/currency alignment use cases | This section does not provide enough evidence to assume broad corridor reliability or liquidity | Keep scope narrow, then validate payout completion, return handling, and reconciliation quality by corridor before wider enablement | Targeted tool, not a broad default |

The core judgment is to prioritize USDC and USDT first, because the evidence here is denser on those two and one cited abstract says they account for approximately 90 percent of stablecoin market capitalization. That alone does not decide your rail, but it does make pilot interpretation clearer.

Operationally, the main failure mode is ambiguous routing, not abstract coin debates. If a contractor, creator, or seller gets USDT in one case and USDC in another, your team should be able to point to a fixed rule, a corridor setting, and an approval record.

To build implementation confidence, run a narrow pilot first: one corridor, one user segment, and one fallback rule. Expand only after you have:

- payout completion results from controlled batches

- a failed-payout taxonomy with retry outcomes

- reconciliation samples tying request, provider reference, and ledger posting

- sign-off that KYC, KYB, AML, and tax-document handling are assigned

USDC's institutional traction is useful context. The cited excerpt reports Visa launched USDC settlement in the United States in December 2025, with US bank settlement described as available seven days a week, including weekends and holidays. Treat that as context, not a substitute for your own corridor proof.

Recommendation: start with USDC when approval quality is the first constraint, start with USDT when liquidity is the real blocker, and use EURC only in tightly scoped corridors with clean pilot evidence.

We covered related payout tradeoffs in ACH vs Wire Transfer for Contractor Payouts When Platform Teams Should Use Each.

Frequently Asked Questions

Which stablecoin should a platform default to for contractor payouts?

Default to USDC if your first constraint is reserve transparency and a compliance-oriented posture. The grounded case here is USDC’s positioning around transparency and regulatory compliance, including monthly attestations. If you choose it, still define the primary rail, fallback rail, and the exact corridors where each is allowed.

When is USDT the better choice than USDC for payout operations?

Use USDT when your main blocker is market reach or exchange liquidity in tougher corridors, not when you just want optionality. The grounded case here is deep global liquidity and broad adoption, while the cited sources also flag transparency and regulatory scrutiny concerns. If you pick USDT first, pair that decision with explicit risk and compliance review rather than treating liquidity alone as approval.

When does EURC make sense for treasury and payout design?

EURC should not be treated as a replacement for USDC or USDT without corridor proof. The practical rule is narrow first: approve EURC only in named corridors, then expand only after pilot results hold up.

Can one platform run USDC, USDT, and EURC at the same time safely?

Potentially, but only if routing is deterministic and ownership is clear. One platform may support multiple stablecoins, including USDC and USDT, yet that alone is not proof that your setup is operationally safe. Verify each enabled coin and corridor against your architecture and compliance requirements before running them together.

What checks are required before enabling a new stablecoin payout corridor?

At minimum, verify fit against your architecture, compliance requirements, and target corridors, because rail choice is not just a coin-support question. Then confirm the required KYC/AML and tax-control ownership for that corridor, since no coin alone satisfies those obligations.

What is the minimum evidence pack Finance and Ops should approve before scaling?

Keep it small but auditable: documented routing rules, approved corridor scope, assigned control ownership, and reconciliation evidence from controlled pilot batches. If the evidence pack still relies on verbal assurances, or a corridor is enabled without corridor-specific results, do not scale yet.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Stablecoin Payouts for Platforms Disbursing USDC to Global Contractors

**Step 1. Set the operating model before you talk about speed.** This guide is for platform operators shipping stablecoin contractor payouts in production, not for freelancers choosing a wallet. The core stance is simple: approve compensation in USD, use a stablecoin as the settlement rail, and treat controls as product requirements from day one. Stablecoins are built to behave like money, and businesses already use them for supplier payments, cross-border invoicing, and treasury movement. That makes stablecoin payouts worth a look, but only if your payout process is as disciplined as your fiat process.

Crypto Payouts for Contractors: USDC vs. USDT - What Platforms Must Know

Treat this as an operating decision first. If you are a platform team building contractor payroll, the early mistake is to frame USDC versus USDT as a recipient wallet preference. The real choice sits with Finance, Ops, Product, and Engineering.

USDC Payouts for Platforms and Stablecoin Settlement for Contractors

For teams evaluating USDC payout options, the real decision is operational, not ideological. You are deciding whether to add USDC as a contractor or creator payout rail without disrupting finance controls, month-end reconciliation, support handling, or compliance review.