Quick Answer

Yes. Use USDC as a selectable payout rail, then hard-code fallback to ACH, SWIFT, or local rails when policy checks fail or recipient setup is incomplete. Ship only after you can prove three controls: idempotent payout initiation, pre-release eligibility checks (including W-8/W-9 paths where applicable), and a reconciliation pack linking invoice ID, provider reference, and ledger journal. If any of those are missing, keep USDC in pilot scope instead of broad rollout.

Decide whether USDC is a controlled payout rail#

If you're evaluating a get paid crypto freelancer USDC workflow at platform scale, the real question is not whether stablecoins are interesting. It is whether you can add USDC as a payout rail without creating compliance, reconciliation, or support problems. This guide takes that narrower, more practical view.

Before you start#

Start with three assumptions locked in:

- USDC is one payout option, not the whole payout strategy. Bank rails still matter when predictable fiat receipt and exception handling are the priority.

- Vendor speed claims are not an operating model. UniFi markets international wires as slow and expensive and says USDC sent from major exchanges can appear within seconds, but that is not proof of end-to-end reliability in your program or the corridors you support.

- Policy constraints are first order, not cleanup work. Stripe explicitly flags regulatory clarity and compliance risk as obstacles to broader stablecoin adoption, so launch decisions cannot sit only with product or engineering.

Define the scope in one sentence#

Define the scope in one sentence that finance, risk, and engineering would all sign. A good version is simple: enable contractor payout receipt in USDC where supported, with fallback to bank rails where policy checks or recipient setup do not line up.

That sentence does two jobs. It stops the team from treating USDC as a blanket replacement for existing rails. It also gives you a fallback rule when a crypto payout cannot be released. If your draft scope does not say what happens when USDC is unavailable or blocked, it is not ready.

Separate recipient experience from platform controls#

Keep the recipient experience separate from the platform control model. Freelancers may care about speed or the ability to receive digital dollars, and Request Finance describes getting paid in crypto as a common issue for web3 freelancers. Your team has a different job: decide who approves release, what evidence explains a payout, and how support traces a missing transfer.

An early practical checkpoint is wallet intake. Some providers, such as UniFi, give each account a dedicated USDC deposit address. You should verify how your provider handles address assignment and payout intake, because that choice changes how you reconcile receipts and investigate errors.

Set launch criteria before anyone writes payout code#

Set launch criteria before anyone writes payout code. At minimum, you need a documented answer for three failure points: a payout blocked by policy, a transfer that looks fast at the wallet level but is not usable by the recipient yet, and a payout that finance cannot tie back to an invoice or ledger entry.

That frame carries through the rest of this guide. We will treat stablecoin payouts as a controlled rail choice, compare them directly with bank options, and spell out what must be true before you let recipients choose USDC in production.

If you want a deeper dive, read How to Get Paid in Crypto as a Freelancer (and Manage the Risks).

Define the operating scope before you build#

Set the operating scope first: enable contractor payout receipt in USDC (USD Coin) where supported, with fallback to ACH or SWIFT. If the fallback rail is not explicit, later decisions on speed, fees, and support will not hold up in production.

Step 1: Write scope as a routing rule. Use a sentence finance, engineering, and support can execute, not a vision statement. The point is to define what happens when a crypto payout cannot be sent.

Step 2: State the non-claim. Do not frame this as "USDC is always faster or cheaper than bank or wallet rails." Pricing is corridor-specific: Wise says fees vary by currency, shows pricing starting from 0.57%, uses the live mid-market rate, and applies discounts only after 25,000 USD monthly volume; PayPal also updates rates and fees over time. Document USDC as a supported rail for defined programs, not a universal cost or speed win over Wise or PayPal.

A practical checkpoint is a one-page assumption sheet per launch market: payout rail, conversion point, who bears fees, and fallback rail. If that sheet is missing, rail comparisons are not decision-ready.

Step 3: Separate platform controls from recipient experience. Define platform-side controls first: approval rules, payout traceability, ledger references, and exception handling. Then define recipient-side experience: wallet requirement, expected timing, and what to do if they cannot receive USDC.

Keep the caveat up front: stablecoin support and off-ramp behavior vary by program, jurisdiction, and provider coverage.

For a step-by-step walkthrough, see The Best Way for a UK Freelancer to Get Paid by an Australian Client.

Compare payout rails and pick a default routing policy#

Use a routing rule, not a rail preference. Route to USDC when timing matters and the recipient is ready to receive and use it, and route to ACH, SWIFT, or a local bank rail when bank-account certainty matters more.

Stablecoin support should sit inside a multi-rail payout stack, not replace bank rails by default. Keep the policy grounded in operational readiness, wallet access, regulatory expectations, off-ramp workflow, and recipient preference for non-crypto methods.

Build a decision table that forces tradeoffs#

Run this by program and corridor so finance, product, and support evaluate the same criteria.

| Rail | Settlement predictability | Traceability | Exception handling | Conversion dependency | Known unknowns |

|---|---|---|---|---|---|

| USDC | Strong when recipient readiness and policy checks are clear | On-chain references can help, but send completion and usable cash outcome are not the same | Sensitive to wallet readiness, policy blocks, and off-ramp flow | Depends on whether funds stay in USDC or are converted | Spread visibility, off-ramp behavior at Coinbase/Kraken/Binance, corridor constraints |

| ACH | Often preferred when beneficiary bank certainty is the priority | Bank/provider references are familiar for support workflows | Bank-side exception paths are usually established | Depends on currency path into the beneficiary account | Bank and corridor handling differences |

| SWIFT | Useful for broader bank reach, with corridor-dependent predictability | Bank references exist but visibility can vary by provider flow | Exceptions can be slower and more manual | Often includes conversion dependency | Corridor constraints and fee visibility |

| Local rails (for example, PIX or IBAN paths) | Strong when local endpoint support is clear | Usually easier to match local payout records | Depends on provider support for local validation/returns | Lower when funding and payout stay in local currency | Coverage gaps and recipient data requirements |

Set the fallback in policy, not in ops memory#

Write the routing logic as if/then, and define fallback explicitly. If a USDC payout fails policy checks, auto-route to the pre-defined bank payout path for that recipient instead of defaulting to manual triage.

Keep one payout intent across the reroute so finance and support can trace the full path: selected rail, policy result, fallback decision, and final payout reference.

Treat vendor claims as hypotheses until your data confirms outcomes#

Treat claims from OpenDue, UniFi, or any provider page as inputs, not proof. Keep a visible "known unknowns" column until your own run data closes it, especially for spread visibility, off-ramp behavior, and corridor-specific constraints.

Related reading: How to Get a Mortgage in Portugal as a US Freelancer.

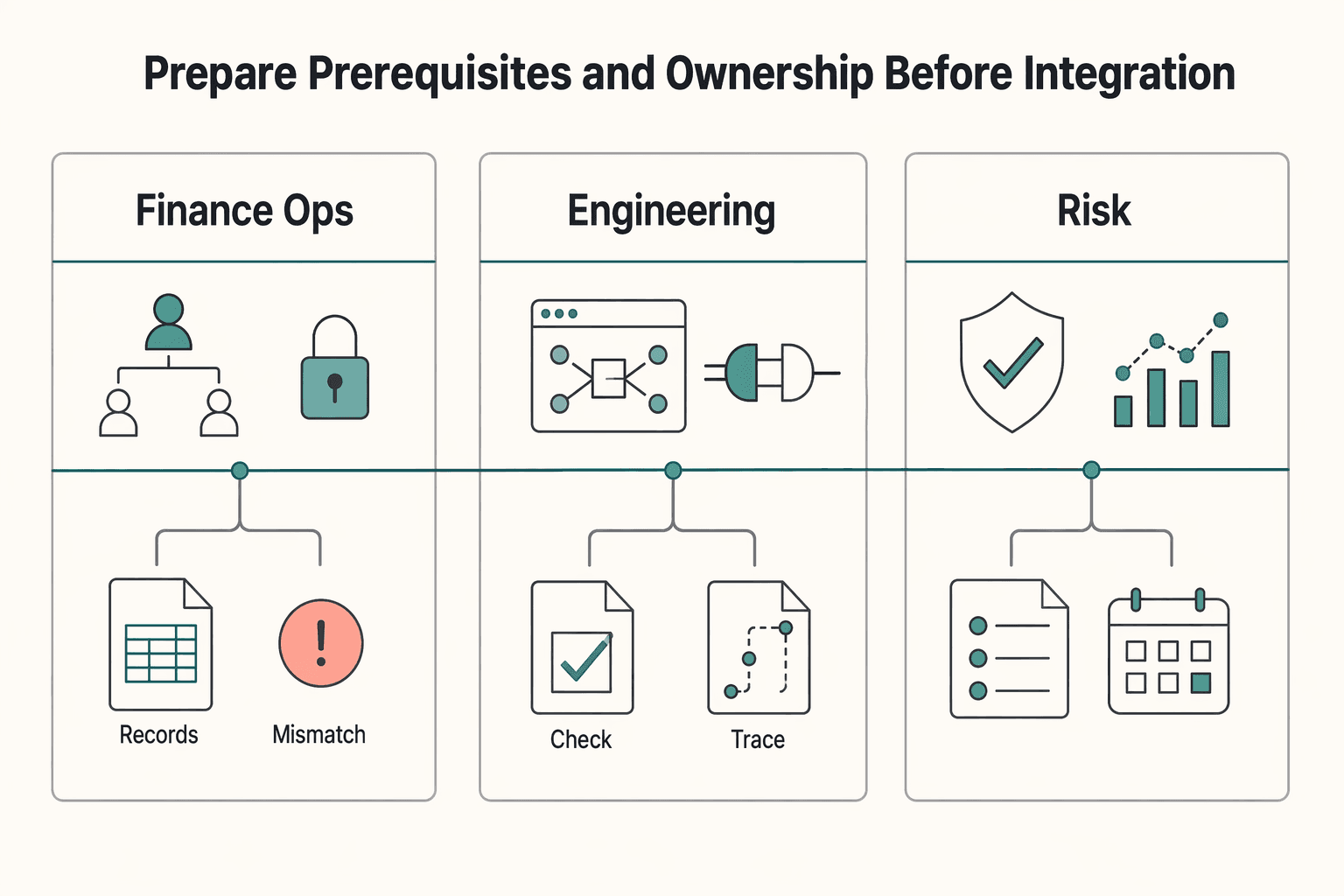

Prepare prerequisites and ownership before integration#

Before you integrate, lock ownership and data requirements so payouts do not stall or break at scale. Stablecoin payouts can improve speed and cost in some cross-border cases, but complexity rises with volume, especially around compliance checks, reconciliation, and reporting.

Step 1: Assign clear owners before any build work. Set one accountable owner for each decision that can release, hold, reroute, or dispute a payout. Keep ownership explicit across finance ops, engineering, and risk, with a defined handoff path.

| Function | Accountable for | Verification point |

|---|---|---|

| Finance ops | Rail selection rules, fallback approval, ledger posting integrity | Can trace one payout from invoice ID to final provider reference |

| Engineering | Data capture, payout initiation logic, status updates, reroute behavior | Can show the event history when a rail changes from USDC to ACH or SWIFT |

| Risk or compliance | Release gates, review holds, incident escalation | Can state what evidence clears a hold before funds are sent |

If support asks who can approve a rail switch and the answer is unclear, ownership is not ready.

Step 2: Confirm rail and endpoint support by market and program. Validate USDC, ACH, and SWIFT support per program and corridor before you code. For each case, confirm three items in writing: supported rail, supported recipient endpoint, and defined fallback rail. For USDC, that means wallet/address requirements. For bank rails, that means required bank details, such as IBAN or local account details.

Step 3: Freeze the invoice-to-payout data contract. Lock the minimum fields that must persist from invoice through payout and reconciliation:

- payer ID and payee ID

- invoice or payment request ID

- currency intent (invoice currency and payout currency)

- quote reference when conversion applies

- payout method metadata (selected rail and recipient endpoint at send time)

Snapshot payout metadata at initiation so ops can distinguish original endpoint issues from later profile edits or bank-side returns.

Step 4: Standardize recipient instructions before launch. Use one recipient standard that explains what to submit for USDC and what to submit if payout falls back to bank rails. It should clearly answer: what details are required, what must match your records, and what happens if the preferred rail is unavailable.

You might also find this useful: Invoice Financing for Freelancers: Get Paid Today Instead of Net-30.

Implement the end-to-end payout sequence with checkpoints#

Treat payout delivery as a controlled sequence of checkpoints, not a single send call. Keep the flow traceable from invoice creation to the status support sees in the UI.

Step 1: Lock one canonical event order. Use one strict sequence and do not skip gates: invoice/payment request created -> funds received -> ledger journal posted -> conversion decision recorded -> payout initiated -> status surfaced in webhook/UI. Only allow payout initiation after both the money-received event and ledger posting exist.

Step 2: Make retries idempotent before launch. Use one idempotency key per logical payout attempt, tied to the invoice/payment request plus rail and recipient endpoint snapshot. Retries with the same key should replay the original result, not create a second send to USDC or ACH.

Step 3: Add explicit conversion controls. If a payout moves from USDC to fiat for SWIFT or local bank delivery, treat conversion as its own checkpoint. Store quote reference and timestamp, reject stale quotes, and require explicit approval for post-intent conversion changes.

Step 4: Publish action-ready status states. Define one shared model for operations, support, and webhooks.

| Status | What it means | Owner action |

|---|---|---|

| pending | Created, not yet confirmed delivered | Validate event history, rail, and send reference |

| credited | Delivery confirmed on selected rail | Reconcile reference to ledger and close |

| held | Blocked by policy/review/data issue | Review, decide release/reject, record reason |

| returned | Funds came back after initiation | Post reversal/adjustment and decide reroute |

Step 5: Start narrower if async returns are not operational yet. If your team cannot reliably process late status changes and reversals, launch with fewer corridors and simpler rails first, then expand to mixed USDC/EURC only after return handling is stable.

Related: Getting Paid as a Freelancer with Cryptocurrency: Platforms and Tax Implications.

Build reconciliation and evidence packs finance can trust#

Finance should be able to audit every USDC payout end to end without engineering help. If you can show a send succeeded but cannot tie it to the invoice, ledger posting, and payout reference, the operation is not audit-ready.

Step 1: Standardize one reconciliation pack per payout. Use one daily pack shape per payout across rails. Include invoice or payment request ID, internal payout ID, provider reference, wallet or chain transaction reference, recipient endpoint snapshot, ledger journal entry, current status, and any adjustment or reversal record. Keep field names consistent so SWIFT and stablecoin records reconcile the same way.

Step 2: Split exception queues by failure type. Run separate queues for unmatched deposits, returned payouts, and delayed confirmations across SWIFT and stablecoin rails. Legacy rails are often reliable but slower, and newer options are often marketed as instant or same-day, but speed claims are not reconciliation evidence. A fast payout with a missing match or final confirmation is still an exception.

Step 3: Require daily exports finance can action directly. Export both current state and status deltas every day. Include prior status, new status, timestamp, trigger source, reference value, and linked journal or reversal entries so finance can answer what changed, what was adjusted, and what remains unresolved.

A useful control check: finance should be able to start from any anchor (invoice ID, ledger entry, or payout reference) and trace to the rest. This matters more as you add rails, because one route rarely covers all payout needs and reconciliation complexity grows quickly.

We covered this in detail in How a US Citizen Can Get Paid by a Brazilian Company Reliably.

Apply compliance and tax gates before payout release#

Gate payout release on compliance and tax checks first, for both USDC and bank rails. The payout record finance audits should also show why a payout was allowed, held, reviewed, or rejected.

| State | When used | Article note |

|---|---|---|

| Held | Missing or overdue KYC/tax data | Unblock with submitted W-8/W-9 data, corrected name/TIN/address details, and no outstanding requirements |

| In review | Data mismatch or policy exception | Example: tax profile and requested rail/corridor mismatch |

| Rejected | Unsupported policy combination | Resolution is reroute or denial, not unlimited document retries |

Step 1: Capture eligibility and tax artifacts at onboarding. Collect identity, tax status, and rail eligibility before first payout release, not after a failed send. If you use Stripe Connect, connected accounts must meet KYC requirements before they can accept payments and send payouts, and those requirements can change over time. For US tax residents, route through Form W-9 (correct TIN for information returns). For non-US tax residents, route through W-8 (name, address, and foreign TIN certification). Store evidence fields, not a checkbox: name, TIN or foreign TIN, address, and signed certification timestamp. If backup withholding applies, the rate is 24 percent.

Step 2: Define held, reviewed, and rejected states with explicit unblock evidence. Do not use a generic "compliance issue" state.

- Held: missing or overdue KYC/tax data. Unblock with submitted W-8/W-9 data, corrected name/TIN/address details, and no outstanding requirements. In a published provider flow, payouts paused for missing tax status should unpause within two business days after required submission if nothing else is outstanding.

- In review: data mismatch or policy exception (for example, tax profile and requested rail/corridor mismatch).

- Rejected: unsupported policy combination. Resolution is reroute or denial, not unlimited document retries.

Step 3: Encode market-aware policy before payout initiation. Run release checks by jurisdiction, payment currency, and rail before money moves. Availability can vary by location and payment currency, and rail support is not uniform. One live program example: Stripe stablecoin disbursement supports USDC only. So do not assume eligibility carries across USDC, ACH, and SWIFT. Test supported, bank-only, and blocked routes, and require deterministic status and reason codes before release.

Handle common failure modes and recovery paths#

Most payout exceptions here come from three issues: wrong destination details, overpromised speed, and unclear status visibility. Treat each as a controlled recovery workflow, not a one-off support ticket.

| Issue | What to do | Article note |

|---|---|---|

| Wrong destination details | Stop automatic retries, require the recipient to update wallet and network details, verify the corrected destination, and only then initiate a new payout | Once initiated or broadcast, a sent transfer generally cannot be canceled |

| Overpromised speed | Publish corridor-specific SLA ranges instead of "instant" language | One public pilot pairs near-instant messaging with a limited launch and broader rollout planned for the second half of 2026 |

| Unclear status visibility | Expose one canonical payout timeline to support: processing, posted, failed, returned, or canceled, plus provider reference or trace ID when supported | Do not treat posted as guaranteed recipient receipt |

Step 1: Verify destination details before any USDC re-send. Assume a sent transfer is irreversible: once initiated or broadcast, it generally cannot be canceled, and wrong-address or unsupported-network sends can be non-recoverable without recipient cooperation. Stop automatic retries, require the recipient to update wallet and network details, verify the corrected destination, and only then initiate a new payout.

Verification point: for every re-initiated payout, ops should be able to show the original destination, the corrected destination, and who approved the resend.

Step 2: Publish corridor-specific SLA ranges instead of "instant" language. Near-instant positioning can be accurate for some stablecoin flows, but availability and speed can still be staged by partner and corridor. In one public pilot, near-instant messaging is paired with a limited launch and broader rollout planned for the second half of 2026. Publish ranges by rail and corridor, and include exception windows for first payout scheduling and returns (for example, 7-14 days for initial scheduling in one provider program, and typically 2-3 business days for returns, with possible country-based variation).

Step 3: Expose one canonical payout timeline to support. Support should use the same state model as ops: processing, posted, failed, returned, or canceled, plus provider reference or trace ID when supported. Do not treat posted as guaranteed recipient receipt, because downstream institutions can still delay release.

Verification point: pick one posted payout and confirm support can explain the status, the provider reference, and the next expected action without escalating to finance ops.

This pairs well with our guide on How to Get Paid in Multiple Currencies Without Forced FX.

Final takeaway and copy/paste launch checklist#

Use USDC as one rail in a controlled payout system, not a blanket replacement for bank rails. Launch only when routing rules, retry behavior, and reconciliation evidence are production-ready end to end.

Define rail policy by corridor before you ship#

Write corridor-level policy for USDC, ACH, SWIFT, and local rails such as IBAN and PIX, with a default and fallback path for each recipient case.

The rails operate differently: ACH does not settle on weekends or federal holidays, Pix can move funds in a few seconds at any time, and SWIFT timing can range from less than five minutes on some routes to more than two days on slower ones. Your readiness check: for every live corridor, show a one-line routing rule for primary rail, fallback rail, and policy-fail behavior.

Make payout initiation retry-safe, quote-aware, and audit-ready#

Treat idempotent payout initiation as mandatory when retries can come from jobs, webhooks, or manual ops, so repeated requests return the original result instead of creating duplicate payouts. Use clear status states (for example, pending, credited, held, returned) so support and finance see one canonical timeline.

If conversion is involved, store the authenticated quote ID and reject or refresh expired quotes. Do not leave payouts stuck in "processing" when the quote is stale and conversion never executed.

Release funds only after evidence and eligibility checks are complete#

Release funds only after reconciliation evidence and eligibility checks are complete. At minimum, your reconciliation pack should tie invoice ID, provider reference, payout record, and ledger journal at payout-settlement-batch level, not just dashboard totals.

Where applicable, capture Form W-9 for IRS information reporting and collect beneficial-owner information for legal entities at account opening. Run wrong address, return, hold, and timeout scenarios in staging, then confirm who can release, reject, or re-initiate each case.

Use this checklist as your go/no-go gate:

- Rail policy defined for USDC, ACH, SWIFT, and local rails (IBAN/PIX) by corridor

- End-to-end sequence implemented with idempotent retries and clear status states

- Conversion and quote-expiry handling documented and tested

- Reconciliation pack ties invoice, provider reference, and ledger journal for every payout

- Compliance and tax gating rules documented with hold and release procedures

- Exception procedures validated for wrong address, return, hold, and timeout scenarios

Want a quick next step on USDC payout setup? Try the free invoice generator.

Frequently Asked Questions

What does “get paid in USDC” actually mean for a platform, not just a freelancer?

For a platform, it means adding a payout rail denominated in a digital dollar, not just offering “crypto” in the abstract. USDC is described by Circle as redeemable 1:1 for U.S. dollars, so the product decision is really about whether you can support a dollar-linked digital payout path with the same controls you expect on ACH or SWIFT. The platform work is routing, eligibility, reconciliation, and exception handling.

When should we route payouts to USDC instead of ACH, SWIFT, or local bank rails?

Consider USDC when non-business-day timing matters and your corridor, provider, and recipient are actually supported. ACH does not settle on weekends or federal holidays, and SWIFT timing can vary from less than 5 minutes on some routes to more than 2 days on slower ones. If you have a strong local rail such as PIX, which supports transfers in a few seconds at any time, do not assume stablecoin is the better answer by default.

Should recipients hold USDC or auto-convert to fiat at payout time?

If the recipient needs local spending certainty or cash in a bank account, auto-convert or offer a bank fallback. If they already manage dollars on-chain, holding USDC may be fine, but that can shift off-ramp and wallet responsibility to them. Red flag: forcing hold-by-default when the recipient has not confirmed how they will convert or spend the funds.

How should invoices be structured when settlement may happen in USDC?

A practical approach is to keep the invoice anchored to the commercial obligation first: payer, payee, service period, amount due, and intended currency. Then add payout metadata separately, including payout method, wallet address, network, and any quote reference or conversion timestamp if fiat is converted before payout. Failure mode: the invoice says “USD” but your records do not show whether settlement was by bank, by USDC, or at what quoted rate.

What is still unknown before we pick a provider for USDC payout support?

Eligibility is a real unknown, because some programs gate stablecoin payouts by the recipient’s residential address. You also need to verify supported corridors, recipient endpoint requirements, spread visibility, and how failed or returned payouts are surfaced to ops. Before signing, ask for one sample evidence pack that ties invoice ID, payout reference, status history, and destination details together.

Can we rely on claims like “instant” or “no hidden fees” without internal benchmarking?

No. Provider comparison data can be built from advertised exchange rates and fees, which is exactly why you should measure collected outcomes in your own corridors. Verification point: benchmark a small set of live payouts by route and compare promised timing and fees against actual posted time, receipt time, and total cost.

What minimum controls should be live before enabling USDC payouts in production?

Before launch, common minimum controls include payout eligibility gates, clear routing rules between USDC and bank rails, idempotent initiation, and one canonical status timeline for support and ops. You also need a reconciliation pack that ties invoice IDs, provider references, wallet movements, and ledger postings, plus a controlled resend path for wrong or corrected wallet details. If those are not live, do not ship just because the rail looks faster on a marketing page.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bis.org/cpmi/publ/swift_gpi.htmtrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- govinfo.gov/content/pkg/CHRG-118hhrg53287/html/CHRG-118h...trusted

- irs.gov/instructions/iw9trusted

- irs.gov/forms-pubs/about-form-w-9trusted

- stripe.com/resources/more/stablecoin-paymentstrusted

- wise.com/us/pricing/card-feestrusted

- wise.com/us/pricing/send-moneytrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Get Paid in Crypto as a Freelancer (and Manage the Risks)

Freelancers use crypto payments for a practical reason: slow payouts and high transfer costs can squeeze monthly cash flow. Traditional rails are still slow in many cases, and [crypto-freelance payment guides](https://www.request.finance/crypto-freelance/how-to-get-paid-in-crypto-a-freelancers-guide-2024) report regional fee pressure that can land around 5% to 10%. When a client wants to pay this way, the goal is not novelty. It is predictable settlement, clean records, and fewer avoidable disputes.

How Platform Teams Manage Crypto Freelancer Payouts

If you need to support workflows where freelancers get paid in crypto, start with the operating model. In practice, the choice is between marketplace-led discovery and a payout stack you control. For platform teams, the split is straightforward:

Invoice Financing for Freelancers Who Need Cash Before Net-30

Net 30 sounds simple until you are the one waiting on the cash. In plain terms, **Net 30** gives the buyer 30 days from the invoice issue date to pay in full. That can be manageable when reserves are strong, but it becomes an operating problem when core expenses come due before client payment does.